Indicators of Threats to the Accounting System When Assessing

Information Security of an Enterprise

Natalia Nikolaevna Karzaeva

a

FKK “Partners”, Moscow, Russia

Keywords: Accounting activity, information, security, threats, indicator, materiality.

Abstract: The article substantiates the possibility of determining the level of security of the accounting system by means

of indicators reflecting its threats. Based on the results of the analysis of the structure of threats to the

accounting system proposed by Russian scientists, the author specified four groups according to the criterion

of the structure of threats (informational, methodological, personnel-organizational and technical) and two

groups according to the criterion of influence on reliability of financial information (directly and indirectly

influential). The author concluded that it is necessary to build indicators for threats that have a direct impact

on qualitative properties of information and formulated principles of their construction: validity, measurability,

simplicity. The article presents a system of indicators offered by the author for each threat to the accounting

activity. The developed indicators correspond to the stated principles. A model for assessing the level of

security of the accounting activity was offered, this model includes the level of general materiality, determined

both for the purpose of monitoring the reliability of financial information and for organizing accounting.

1 INTRODUCTION

At the turn of the 20th and 21st centuries financial and

economic crises began to be permanent. The

implementation of entrepreneurship in crisis

conditions led to rapid development of activities to

ensure the economic security of systems of different

levels from enterprises to states. This circumstance

predetermined formation of a system of legal

regulation of activities in this area, including risk

management and reporting: COSO ERM 2017, ISO

31000: 2018, "Principles for effective risk data

aggregation and risk reporting" (Basel Committee on

Banking Supervision, 2013), Integrated Reporting

(International Integrated Reporting Council), IFRS 7

Financial Instruments: Disclosures, IFRS 9 Financial

Instruments, etc. These acts regulate the procedure for

the provision of information by enterprises about the

risks in which they conduct their production, financial,

commercial and investment activities. However,

scientists and experts note the presence of risks when

implementing activities related to formation of

information, for example, accounting (Borimskaya

E.P., Granitsa Y.V., Demina I.D., Ishchenko O.V.,

Merkutsenkov S.N., Panchenko I.A., Stafievskaya

a

https://orcid.org/0000-0003-0255-0946

M.V., Khodarinova N.V., etc.). There is also a

professional opinion that the information contained in

financial reports makes it possible to identify business

risks (Avdiyskiy V.I., Granitsa Y.V., Demina I.D,

Merkutsenkov S.N., Trushanina A.D., etc.). Scientists

offer various indicators of threats to business,

calculated on the basis of information contained in

financial reports (Avdiyskiy V.I., Granitsa Y.V.,

Demina I.D., Merkutsenkov S.N., Trushanina A.D.,

etc.). However, there are currently no works in which

indicators characterizing the level of threats to the

actual accounting activities are presented.

Due to the lack of studies on assessing the impact

of threats to the accounting activity on reliability of

information in financial reports, it seems appropriate

to confirm or reject the following hypothesis:

assessment of effectiveness of the accounting activity

through indicators of its threats will allow assessing

the level of reliability of financial information

provided to users.

The purpose of our study is to develop indicators

of threats to the accounting activity on formation of

financial information about the activities of the

enterprise. In accordance with this goal, the following

research objectives were identified:

270

Karzaeva, N.

Indicators of Threats to the Accounting System When Assessing Information Security of an Enterprise.

DOI: 10.5220/0010698500003169

In Proceedings of the International Scientific-Practical Conference "Ensuring the Stability and Security of Socio-Economic Systems: Overcoming the Threats of the Crisis Space" (SES 2021),

pages 270-274

ISBN: 978-989-758-546-3

Copyright

c

2022 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

- to form and systematize threats to the accounting

activity;

- to build up indicators of threats to the accounting

activity;

- to develop an indicator of the security level of

the accounting system.

2 MATERIALS AND METHODS

The methodological basis of the study is the

fundamental provisions of the theory of accounting

and control, economic security. When building

indicators of threats to the accounting activity,

methods of economic modeling were used. When

building a model for assessing the level of safety of

the accounting activity, methods of mathematical

modeling were used.

The study is based on a logical analysis of

scientific works on the risks of the accounting activity

of business entities.

Table 1: Classification of threats to the accounting activity

Types of

threats to the

accounting

activit

y

Threat structure

Information - lack of support for transparency and openness on the part of people who generate information

(Avdiyskiy and Trushanina, 2019);

- information distortion (Borimskaya and Panchenko, 2013; Naam and Rozhkova, 2020; Sungatullina

and Gogoleva, 2014);

- leakage of confidential information (Borimskaya and Panchenko, 2013);

- untimeliness, unreliabilit

y

of external information

(

Naam and Rozhkova, 2020

)

Personnel - insufficient knowledge of heads of the accounting department, their insufficient competence

(Borimskaya and Panchenko, 2013);

- low professional level of accounting employees (Borimskaya and Panchenko, 2013);

- leakage of confidential information due to the fault of the accounting department workers

(Borimskaya and Panchenko, 2013);

- manipulations with accounting documents and reports (Borimskaya and Panchenko, 2013);

- deliberate violation of tax legislation, including an unjustified reduction in the tax burden

(Borimskaya and Panchenko, 2013; Sungatullina and Gogoleva, 2014);

- recording in documents unacted facts of the economic life (Borimskaya and Panchenko, 2013);

- technical errors in accounting (Naam and Rozhkova, 2020);

- corruption schemes using official powers (kickbacks, bribes, commercial bribery) (Borimskaya and

Panchenko, 2013)

Methodological - accounting methodology (Borimskaya and Panchenko, 2013);

- violation of principles and rules of accounting (Borimskaya and Panchenko, 2013);

- incorrect accounting policies (Sungatullina and Gogoleva, 2014);

- financial miscalculations when choosing accounting methods regulated by accounting and financial

reporting standards (Borimskaya and Panchenko, 2013);

- incorrect content, procedure for formation and presentation of the company financial reports to

external users

(

Sun

g

atullina and Go

g

oleva, 2014

)

Organizational-

technical

- violation of confidentiality (Avdiyskiy and Trushanina, 2019);

- violation of the storage regime for accounting information that constitutes the commercial secret

(Borimskaya and Panchenko, 2013);

- absence or non-compliance with internal control rules, including control over the accountant's

activities (Borimskaya and Panchenko, 2013; Bezdenezhnykh, Bezdenezhnykh & Karanina, 2020;

Grytsay and Havran, 2020; Plikus, 2017);

- outdated information technologies that do not correspond to processing, storage and presentation of

accounting information to individual groups of users (Borimskaya and Panchenko, 2013);

- violation of the document flow regime (Borimskaya and Panchenko, 2013);

- incorrect Regulation on the accounting service of the enterprise (Sungatullina and Gogoleva, 2014);

- non-recording of facts of the economic life in documents (Sungatullina and Gogoleva, 2014)

Indicators of Threats to the Accounting System When Assessing Information Security of an Enterprise

271

3 RESULTS AND DISCUSSION

The International Standard "Integrated Reporting"

regulates the obligation of the enterprise management

to inform users of these reports about risks in which

management will perform activities to create a product

in short-term, medium-term and long-term periods.

Also, this reporting discloses tools for leveling these

risks. The procedure for generating information about

risks involves, firstly, identification of information

about risks, secondly, its selection from incoming

information, thirdly, appropriate processing

(classification, systematization, transformation),

fourthly, presentation of outgoing information in

various formats (financial reports, explanation reports,

integrated reports).

A part of information on risks presented in the

financial and explanation reports is processed in the

accounting system, which is a part of the general

information system of the company. In addition, the

accounting activity, like other types of activities

(production, financial, commercial, etc.), is subject to

various threats, implementation of which may lead to

formation of inaccurate financial reports. Therefore,

many scholars identify accounting risks (Avdiyskiy

& Trushanina, 2019; Borimskaya & Panchenko,

2013; Grytsay & Havran, 2020; Naam & Rozhkova,

2020; Stafievskaya, Nikolayeva ets, 2015;

Sungatullina and Gogoleva, 2014).

To build a system of indicators of threats to the

accounting activity, it is necessary to define the

concepts that underlie it. We understand a risk in

economic security as a result of implementation of a

threat, namely material or financial damage that may

be caused to the company. At the same time, a threat

is a disadvantageous event, an action that is likely in

nature and which employees of the company can

influence and prevent. In information security or

information system security, a risk can be viewed as

a loss of information properties, such as reliability.

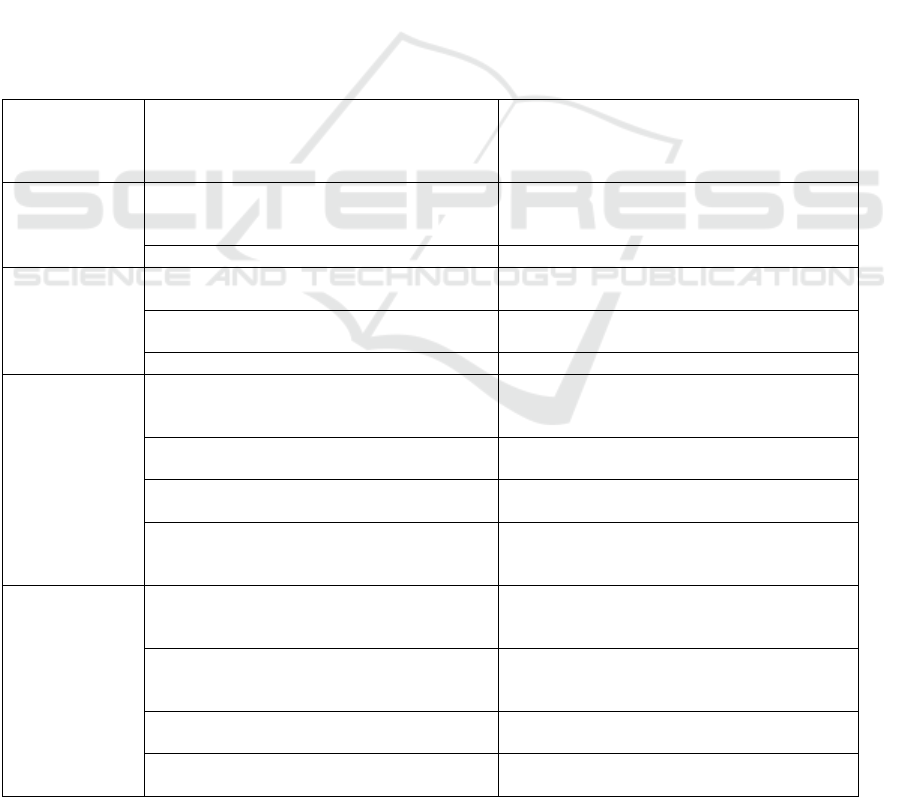

Table 2: Indicators of threats to the accounting activity

Types of threats

to the

accounting

activit

y

Threat structure Indicators

Information

untimeliness of external information

valuation of objects that are recorded in

external information and should have been

included in the financial re

p

orts

(

I

1

)

unreliabilit

y

of external information de

g

ree of distortion of valuation of ob

j

ects

(

I

2

)

Personnel

violation of tax legislation

amount of claims filed by tax authorities based

on the results of tax audits (I

3

)

recording in documents unacted facts of the

economic life

valuation of unacted facts of the economic life

recorded in documents (I

4

)

technical errors in accounting valuation of technical errors in accounting (I

5

)

Methodological

violation of principles and rules of

accounting, regulated by the accounting

p

olic

y

valuation of violations of accounting

principles and rules (I

6

)

incorrect accounting policies

amount of deviations from the regulated

methods and accounting methods (I

7

)

financial miscalculations when choosing

accountin

g

methods re

g

ulated b

y

local acts

value of deviations of the chosen from the

rational accountin

g

method

(

I

8

)

incorrect content, procedure for formation

and presentation of the company financial

reports to external users

valuation of errors made in the procedure for

creation and presentation of financial reports

(I

9

)

Organizational-

technical

absence or non-compliance with internal

control rules, including control over the

accountant's activities

valuation of errors in accounting and financial

reporting missed by the internal control

system (I

10

)

violation of the document flow regime

valuation of objects recorded in documents,

executed and transferred with violations of the

workflow schedule

(

I

11

)

non-recording of the facts of the economic

life in documents

valuation of facts of the economic life not

recorded in documents (I

12

)

loss of primary accounting documents

valuation of objects recorded in lost primary

documents

(

I

13

)

SES 2021 - INTERNATIONAL SCIENTIFIC-PRACTICAL CONFERENCE "ENSURING THE STABILITY AND SECURITY OF

SOCIO - ECONOMIC SYSTEMS: OVERCOMING THE THREATS OF THE CRISIS SPACE"

272

Of course, risks in the form of financial losses (for

example, for compensation for moral damage, etc.)

and material losses (for example, loss of structural

elements of IT systems) remain relevant for

information security. In this article, we will focus

only on the loss of information properties - its

reliability, which is closely related to the concept of

materiality.

We systematized lists of accounting threats

presented by the authors based on the dualistic nature

of accounting (as a type of activity and information

system) into four groups: information,

organizational-technical, methodological and

personnel (Table 1).

Problems of indicative assessment of the level of

safety are considered by many scientists (Karanina,

Ryazanova & ets. 2018). When constructing a system

of indicators characterizing the safety of the

accounting activity, we use four basic principles that

we proposed earlier (Karzaeva & Davydova, 2020):

- relevance of indicators to the content of a

specific threat;

- measurability, preferably in natural or monetary

units;

- validity of indicators;

- simplicity of their calculation.

The analysis of the structure of these threats in

order to build indicators allowed to divide them into

two groups: 1) directly influencing a decrease in the

level of reliability of financial information and 2)

indirectly influential. Rationality of organization of

the process of assessing the level of security of the

accounting activity supposes development of

indicators only for the first group of threats (Table 2).

In addition, indicators are built to assess reliability

of information contained in financial reports;

therefore, the structure of threats includes only threats

that influence its indicators. We also excluded threats

that generalize other threats, for example, distortion

of information, accounting document and report

manipulation, a particular case of which is the failure

to reflect facts in accounting documents.

Indicators are built on the basis of data for the

previous reporting period, usually it is a calendar

year. The possibility to use the indicators expressed

in terms of valuation allows to compare them with the

level of materiality, which is of great importance for

perception of users of information contained in

financial reports. We proposed methods for

constructing the level of materiality earlier in our

works (Karzaeva, 2019). Here we only note that the

comparison of the sum of particular indicators of

threats to the accounting activity (I) with the given

general level of materiality (M) will allow to assess

the level of security of the accounting system (K).

𝐼𝑀К

If the difference between the sum of particular

indicators of threats to the accounting activity and the

specified level of materiality is higher than zero, the

level of security of the accounting system can be

considered satisfactory. If this difference does not

reach zero, the security level of the accounting system

is unsatisfactory.

4 CONCLUSIONS

As a result of the study, the following main

conclusions were formulated:

- threats to the accounting activity for the

purpose of monitoring and organizing activities to

prevent them should be systematized according to a

meaningful criterion in four groups: information,

personnel, methodological and organizational-

technical;

- threats to the accounting activity in order to

construct their indicators should be divided according

to the criterion of the degree of influence on financial

reports indicators into two groups: directly

influencing a decrease in the level of reliability of

financial information and indirectly influential;

- with the purpose of rational organization of the

process of assessing the level of security of the

accounting activity, develop indicators only for

threats that directly influence a decrease in the level

of reliability of financial information;

- indicators of threats to the accounting activity

can be measured in value;

- comparison of the sum of particular indicators

of threats to the accounting activity with the general

level of materiality allows us to assess the level of

security of the accounting system.

The conclusions confirm the hypothesis of the

possibility of assessing the security of the accounting

activity by means of indicators of its threats and,

accordingly, assessing a possible decrease in the level

of reliability of financial information provided to

users tested in this study.

Indicators of Threats to the Accounting System When Assessing Information Security of an Enterprise

273

REFERENCES

Avdiyskiy, V. I., Trushanina, A. D., 2019. Minimizing

accounting risks using digital technologies. In Modern

Economy Success. 6. p. 188-193.

Bezdenezhnykh, V., Bezdenezhnykh, A., Karanina, E.

2020. Synergy of Interaction of Control and

Supervisory Structures in Ensuring the Stability of the

socio-economic System: Principles and Organization.

In E3S Web of Conferences. "International Scientific

and Practical Conference "Environmental Risks and

Safety in Mechanical Engineering", ERSME 2020". p.

07030.

Borimskaya, E. P., Panchenko, I. A., 2013. Directions of

the organization of accounting in the context of risk-

based management. In International accounting.

38(284). pp. 55-63.

Grytsay, O., Havran, M., 2020.Accounting and Analytical

Support for Formation of Enterprise Security Costs and

their controlling. In Process Economics,

Entrepreneurship, Menegment. 7-1(13). pp. 75-83.

Karanina, E. V., Ryazanova, O. A., Timin, A. N.,

Domracheva, L. P., 2018. Diagnostigs and Monitoring

of Economic entities Security. In E3S Web of

Conferences. 2018 Topical Problems of Architecture,

Civil Engineering and Environmental Economics,

TPACEE 2018. p. 08002.

Karzaeva, N. N., 2019. Indikator Metod of Asseeeing

Nateriality. In International Journal on Emerging

Technologies. 10(2). pp. 182-187.

Karzaeva, N. N., Davydova, L. V., 2020. Methodological

methods for creating a system of safety indicators for

the company's utopia and Praxis Latinoamericana.

25(6). pp. 219-228.

Naam, M. N., Rozhkova, D. A., 2020. Ways to minimize

risks in the accounting system. In Topical issues of the

modern economy. 3. pp. 645-655.

Plikus, I., 2017. Investigation of Methods of Counteracting

Corporate Fraudulence. In Accounting-Legal

Approaches to the Identification of Abusonment

Technology audit and production reserves. 4-4(36). pp.

22-28.

Stafievskaya, M. V., Nikolayeva, L. V., Kreneva, S. G.,

Shakirova, R. K., Semenova, O. A., Larionova, T. P.,

Filyushin, N. V., 2015. Accounting Risks in the

Subjects of business Systems. In Review of European

Studies. 7(8). pp. 127-137.

Sungatullina, R. N., Gogoleva, O. L., 2014. Identification

of risks of material misrepresentation of information

about facts of the economic life when assessing the

internal control system. In Auditor. 12. pp. 38–49.

SES 2021 - INTERNATIONAL SCIENTIFIC-PRACTICAL CONFERENCE "ENSURING THE STABILITY AND SECURITY OF

SOCIO - ECONOMIC SYSTEMS: OVERCOMING THE THREATS OF THE CRISIS SPACE"

274