Strategic Development of Management Accounting at Large

Industrial Corporations

Nina Ilysheva

1a

, Vasily Karaulov

2b

and Kristina Bulgakova

1

1

Ural Federal University, Yekaterinburg, Russia

2

Vyatka State University, Kirov, Russia

Keywords: Management accounting, strategic approach, strategic management accounting, integrated performance

management system, strategic objectives, key performance indicators, key efficiency indicators.

Abstract: The given publication's objective is to research into the formation process of a strategic approach in the

management accounting of large industrial corporations in a competitive environment in oder to maintain the

leading position in their business segment. Meeting the formulated objective, the following tasks were set: to

consider the management accounting formation process and the prerequisites for the strategic management

accounting formation; to develop a theory of an integrated performance management system as the basis for

the strategic management accounting. Works of scientists and economists in accounting, management

accounting, economic, financial and strategic analysis have served as the theoretical and methodological basis

for this publication. Based on the results of this study, we have come to the following conclusions. Today, the

tools of traditional production accounting in management accounting are inapplicable. One should use any

useful methods such as: value chain analysis, balanced scorecard, mathematical methods and many others.

The strategic approach to planning, accounting, cost analysis is a new, higher level of the accounting and

analytical system of the enterprise. At which point one selects the key indicator, that affects the costs, the

choice of the relevant mathematical model, describing the costs forecast. This indicator forms high-quality

information background for a company's management in making effective management decisions. An

integrated performance management system is to solve the afore-said problems. The practical significance of

the research is in the application of the outcomes and recommendations to the management accounting at an

enterprise, thus improving the quality of management decisions.

1 INTRODUCTION

As the world economic situation is getting more

unstable, the international and in-country competition

increasing, management accounting is becoming

more important.

The task of forming a modern management

accounting system is one of the most urgent. The

range of opinions on the definition of the

management accounting is quite extensive. Some

researchers interpret it as an accounting subsystem

whose main task is to collect, register and summarize

information. However, others consider it to be an

enterprise management system that performs all

management functions such as: accounting, planning,

analysis, control and decision making.

a

https://orcid.org/0000-0002-7876-9376

b

https://orcid.org/0000-0002-9599-3740

In the current economic conditions, which are

characterized by intensifying competition,

acceleration of scientific and technological progress,

it becomes impossible to maintain traditional

management accounting at an enterprise, based on

cost calculation and affecting the internal activities of

the company. Such accounting has been characteristic

of the industrial and, to some extent, post-industrial

era, now it is necessary to expand the management

accounting system by including information about the

company's external environment: buyers, suppliers,

competitors, government acts. One should also use

new methods for getting the information to make

effective decisions by the company's management,

which is the strategic management accounting

system's objective.

Ilysheva, N., Karaulov, V. and Bulgakova, K.

Strategic Development of Management Accounting at Large Industrial Corporations.

DOI: 10.5220/0010694000003169

In Proceedings of the International Scientific-Practical Conference "Ensuring the Stability and Security of Socio-Economic Systems: Overcoming the Threats of the Crisis Space" (SES 2021),

pages 111-116

ISBN: 978-989-758-546-3

Copyright

c

2022 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

111

The acuteness of the strategic management

accounting, both theoretically and practically,

predetermined the research choice, its objectives,

subject and research methods.

The given publication's objective is to research

into the formation process of a strategic approach in

the management accounting of large industrial

corporations in a competitive environment in oder to

maintain the leading position in their business

segment.

To achieve the aforementioned objective, the

following tasks have been set:

to consider the management accounting

formation process and the prerequisites for the

strategic management accounting formation;

to develop a theory of an integrated performance

management system as the basis for the strategic

management accounting.

The research is focused on the patterns of strategic

management of large industrial corporations in a

competitive environment.

The subject is the strategic management

accounting.

2 MATERIALS AND METHODS

Works of scientists and economists in accounting,

management accounting, economic, financial and

strategic analysis, accounting normative and

legislative acts, Internet sources have served as the

theoretical and methodological basis for this

publication.

The emergence of the management accounting

system is published in the works by Sokolov, Drury,

Horngrem, Foster, Shank, et al.

The management accounting has been researched

by: Vakhrushina M.A., Volkova, O.N., Gerchikova

I.N., Ivashkevich V.B., Kerimov V.E., Kondrakov

N.P., Nikolaeva S.A., Sokolov Ya.V., Sheremet A.D.

et al.

The following researchers have delved into the

strategic development of enterprises, their

competitiveness: Ansoff, Gaponenko, Ilyshev,

Ilysheva, Karanina, Pankrukhin, Thompson

Strickland Porter, Fatkhutdinov, Fleischer, Yurieva et

al.

However, at the current stage of science

development there is a small number of works on the

problems of forming strategic management

accounting in large industrial corporations.

The study used general scientific research

methods - comparison, grouping, graphic method.

3 RESULTS AND DISCUSSION

3.1 The Management Accounting

Formation Process and the

Prerequisites for the Strategic

Management Accounting

Formation

For a company's management to make effective

management decisions, management accounting is

intended. This is one of the main tasks of

management accounting. The main purpose of this

type of accounting is to create and support the

information system within the company. This is a

fundamental prerequisite for the effective functioning

of the management accounting system.

The origin and formation of the management

accounting are the systems of costing and production

accounting.

When the first exchange operations appear, the

manufacturer needs to calculate the cost of goods sold

and services rendered, which is a prerequisite for the

formation of cost accounting. At first, however, it was

simple enough, all the calculations were made in the

mind and account records were not required.

The industrial revolution that took place at the end

of the 18th century, the transition from individual to

factory production, the emergence of numerous

industrial enterprises and free business activity

contributed to competition, capital market, goods

market and labor market, as well as free pricing. In

these conditions, the importance of calculating

accounting increased primarily as a tool to assess the

profitability of goods, and the market prices

(Horngren, Foster, 2000).

At the end of the 20th, the beginning of the 21st

century, the cost record got a boost in its

development. As a result of the scientific and

technological advances that took place at that time,

there was a concentration of production, which made

it difficult to sell products (goods and services) and

the need to borrow due to a lack of working assets.

Interested parties, such as investors, creditors, tax

authorities, needed detailed information about the

financial and economic activities of a company. For

these reasons, the problems of costing accounting,

providing information that is not immediately

possible to influence, became apparent.

The main goal of a business was to obtain

maximum profit, which directly depended on the

operational, successful actions of management

personnel aimed at efficient organization of

production, through the appropriate and profitable

SES 2021 - INTERNATIONAL SCIENTIFIC-PRACTICAL CONFERENCE "ENSURING THE STABILITY AND SECURITY OF

SOCIO - ECONOMIC SYSTEMS: OVERCOMING THE THREATS OF THE CRISIS SPACE"

112

allocation of the company's resources. All these

changes were prerequisites for changing the entire

accounting system of a company.

In the late 1940s and early 1950s, there were

global changes in the accounting system in

industrialized countries. Accounting ceased to be

simply a means of collecting, processing and

grouping economic information, instead the

information started being used for forecasting,

analysis, control and management decisions.

Significant attention was paid to the production costs,

the volume of manufactured products, as well as the

comparison of the actual and projected output of a

company.

As a result of the expansion, increase in the

production output, the formation of large companies

and the resulting need to preserve trade secrets,

accounting split into financial and management (cost)

ones.

The main task of management (cost) accounting

was to provide the company's management with

operational and analytical information on the costs

and revenues of the company's structural units, so that

the management could make effective decisions.

The next stage in the development of the costing

system is the emergence of a standard-cost system,

the essence of which was to create material and

manpower standards for their more economical use.

The prerequisites for the creation of this system were

the need for operational cost control and the ability to

regulate the cost of the products produced. Constant

comparison of standards with the actual cost made it

possible to quickly eliminate any bias, thus there

appeared a new way of cost managing - deviation

(bias) management.

With the use of the standard-cost system in the

management (calculus) accounting, accounting

ceased to be simply a record of facts of business

activities of the enterprise.

In 1936, Harrison, an American scientist, first

coined the term "direct-costing." The idea of this

accounting system was to separate the fixed and

variable costs. This was the next stage in the

development of costing accounting and gave way to

the formation of the company's pricing and strategic

policy.

An important step in the formation of

management (costing) accounting was the emergence

of cost accounting based on "the centers of

responsibility" as the further development of the

standard-cost system. The use of the responsibility-

centers accounting made it possible to track

deviations of actual costs from standard costs, which

demonstrated the effectiveness of managers.

Thus, the emergence of new production cost

accounting methods such as: standard-cost, direct-

cost and responsibility centers accounting made a

huge impact on the development of the costing

accounting system, transforming it into a production

accounting system and then turning it into a

management accounting system.

The official division of accounting into financial

and management ones took place in 1972.

In the early 21st century, the next stage in

management accounting development was the

development of an approach, driven by the need for

strategic accounting, planning and analysis of a

company's business activities. There was a division of

management accounting into a tactical (information

about the current activities of a company) and

strategic (long term information) ones.

Features of strategic management accounting

include:

external environmental factors;

aim at taking into account uncertainty, risk

management strategy, all components of the subject's

risk system (Karanina E., 2017;

is the basis for making rational, effective

management decisions (P.A. Vinogradov, 2018).

The main task of strategic management

accounting is to create a relevant information base for

the management of a company.

The object of strategic management accounting is

the capital expenditures of an enterprise, which are of

a long-term nature; would-be results of the business

activities of a company as a whole and its individual

structural units; pricing that takes into account market

prices and the expected inflation rate; strategic

planning (Kim L.I., 2019).

Based on the aforesaid, we will formulate the

author's vision of strategic management accounting.

Strategic management accounting at a large

industrial enterprise is an accounting system in which

financial and non-financial information is generated

in terms of management objectives, on three main

components: planning, monitoring and analysis of the

company's activities. This applies not only to the

costs of the enterprise, as it was in traditional

management accounting, but also to its external

business environment (suppliers, buyers,

competitors, government actions), and the internal

business environment (production process, labor and

material resources, as well as social processes).

Strategic management accounting uses any useful

method, such as balanced scorecards, benchmarking,

target costing, ABC (Activity-Based Costing), value

chain analysis, risk analysis, mathematical methods

and many others.

Strategic Development of Management Accounting at Large Industrial Corporations

113

The main distinguishing feature of strategic

management accounting is the possibility and

necessity of its use to assess the financial and

economic activities of an enterprise both in terms of

financial (expressed in monetary terms) and non-

financial (expressed in shares, percentages, natural

units) indicators, which makes it possible to obtain a

more detailed view of the company's efficiency.

Today, large industrial corporations are in intense

competition, dynamic development of the production

base, therefore, in the accounting and analytical

system of an enterprise it is impossible to limit

ourselves to the tools of classical management

accounting of production costs. New methods of

accumulating management information, adequate for

modern conditions, are needed, and the strategic

management accounting system possesses such

methods.

So, the strategic approach to management

accounting at the present stage of development of

society plays a dominant role in relation to

operational (current) accounting.

The stage of development of management

accounting in the 21st century is fundamentally new.

Since this accounting and analytical system

increasingly begins using the methods of various

sciences - mathematics, computer science, sociology,

statistics, a comprehensive approach to management

accounting in the 21st century is inevitable in order to

achieve such goals as: manyfold increase in labor

productivity, a significant strengthening of

competitive positions of our country in world markets

and many others.

3.2 Formation of an Integrated

Performance Management System

as the Basis of Modern Strategic

Management

Based on aforesaid, we conclude that in large

industrial corporations there is a need for the 21st

century management accounting that meets all the

requirements and current business conditions, in other

words, a strategic approach to enterprise accounting.

The strategic approach is to form an integrated

performance management system as the basis for

strategic management.

The main tasks to be solved by the performance

management system are the following:

measuring the efficiency of the enterprise in

order to show how satisfied customers are with the

goods and services provided to them;

clarity and accuracy of the strategic objectives of

the enterprise;

attention to the key business processes and key

indicators at the enterprise, as well as notification of

management about improvements or deterioration in

performance;

point out critical business success factors that

require the most attention;

creation of basis for identifying achievements

and setting up appropriate reward system.

So, the performance management system is a set

of interrelated elements such as: strategic objectives,

key company strategies, critical success factors and

key performance indicators.

In order to develop new indicators of enterprise

performance, it is necessary to define the strategic

objectives and important factors of the company's

success, which form the basis of an integrated

performance model. The elements of this system

include:

a statement of the company's vision and mission;

strategic objectives;

customer needs;

systems of incentives and rewards (Averchev,

2011).

Company Vision Statement describes the main

objectives, characteristics and philosophy that guide

the strategic activities of the company.

Mission statement includes a clear statement of

the specific needs of the customer that the company

seeks to satisfy; not the products or services offered.

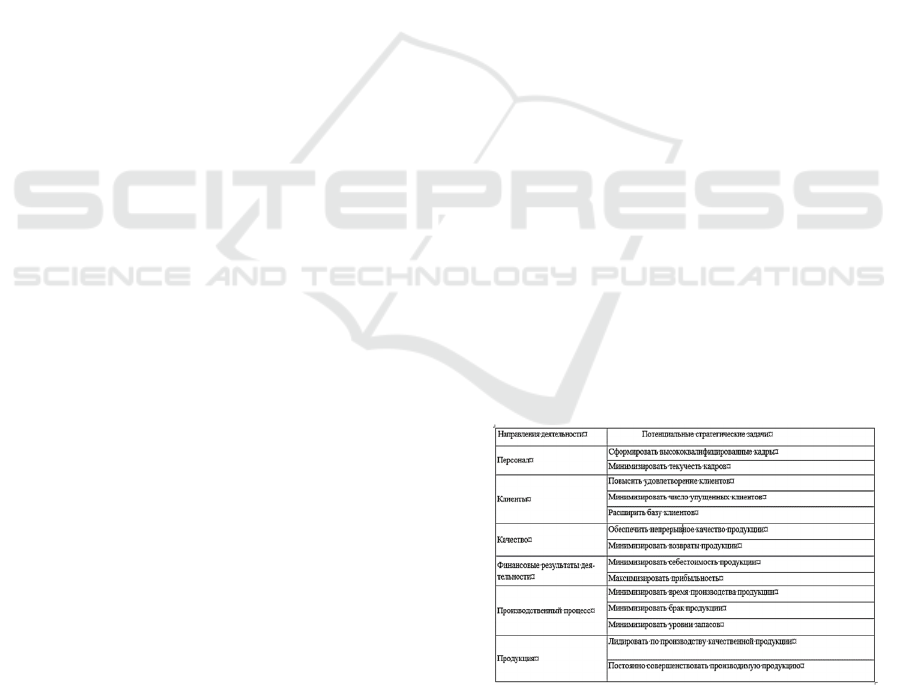

A well-defined and clear set of a company's

strategic objectives is at the heart of the performance

management process that shapes the strategic line of

the company. Examples of strategic objectives are

given in Table 1.

Table 1: Strategic objectives.

Afterwards, one needs to identify the main

success factors. They focus on the key performance

indicators that differentiate a firm from its

competitors in order to achieve its goals and meet

customer requirements.

SES 2021 - INTERNATIONAL SCIENTIFIC-PRACTICAL CONFERENCE "ENSURING THE STABILITY AND SECURITY OF

SOCIO - ECONOMIC SYSTEMS: OVERCOMING THE THREATS OF THE CRISIS SPACE"

114

A company's basic success factors are the

following:

production of goods that consumers will

rate as products of the highest quality;

rapid development of new types of

products;

keeping the cost of products and services

low;

fast and a comprehensive response to

customer needs.

For critical success factors to be effective and

understandable, they need to be quantified through

key performance indicators. When choosing such

indicators, one can address the concept of a balanced

scorecard (BSC), it considers any enterprise from

four angles:

financial indicators;

customers;

business processes;

staff (Yur'eva, 2013).

To achieve the strategic goals of the company, an

integrated system

of financial and non-financial indicators is

created, thanks to which the company gets assessment

tools of its financial and economic activities. An

example is the strategic risk system of an enterprise,

which determines strategic risk indicators in

conjunction with performance indicators (Karanina

E., 2017).

Based on the information received about the

strategic intentions of the company, the main business

processes, critical success factors and key indicators,

an integrated model of the company's performance is

drawn up (See Figure 1).

Figure 1: Integrated performance model.

Upon the selection of key indicators, the protocol

of the company's performance becomes an important

tool, which provides an easy, visual interpretation of

the indicators and is a concise report on the daily

performance.

For the performance management system to work,

it is necessary to turn to digital technologies as an

essential condition for the successful functioning of

large industrial corporations in the digital economy.

The most suitable in our case is the Customer

Relationship Management (CRM) system, the

purpose of which is to computerize business

processes in marketing, sales, service quality;

collecting customer information for subsequent

analysis and making effective management decisions.

The integrated performance management system

is a constantly changing system, i.e. a dynamic one.

Key performance indicators of the company also

cannot remain unchangeable. Therefore, one should

constantly monitor the data of the system,

maintaining its relevance, providing the company's

management with timely information to analyze

decisions and courses of action at a constantly

changing set of customers and needs.

As companies are now entering a new era of

globalized markets in a highly competitive

environment and are increasing their flexibility and

responsiveness of their product delivery policies and

delivery mechanisms, a well-designed system of

indicators is becoming increasingly important. An

effective performance management system is a

snapshot of the health of the enterprise and should

provide management with information to manage

current operations and to plan future opportunities

and development strategies.

4 CONCLUSIONS

Based on the results of this study, we have come to

the following conclusions.

In modern conditions, it is impossible to use

only traditional production accounting tools in

management accounting, it is necessary to use any

useful methods such as: benchmarking, balanced

scorecard, direct costing, target costing, value chain

analysis, ABC (Activity-Based Costing), risk-

analysis, mathematical methods and many others.

A strategic approach to the accounting and

analytical system of an enterprise is to form high-

quality information support for the company's

management staff for making effective management

decisions by introducing an integrated performance

management system.

The results of this study are applicable in setting

up modern management accounting at large industrial

corporations, which will significantly improve the

Strategic Development of Management Accounting at Large Industrial Corporations

115

adequacy of the decisions made by the management

of the enterprise.

In modern conditions, which are characterized by

intense competition, the need to increase the

efficiency of the use of production resources,

increased requirements for exceptional, unique

characteristics of the goods sold, dynamic changes in

consumer demand, as well as the improvement of

production means, it is necessary to form a strategic

approach to management accounting of large

industrial corporations.

ACKNOWLEDGEMENTS

The article was prepared with the support of the grant

of the President of the Russian Federation NSh-

5187.2022.2 for state support of the leading scientific

schools of the Russian Federation within the

framework of the research topic «Development and

justification of the concept, an integrated model of

resilience diagnostics of risks and threats to the

security of regional ecosystems and the technology of

its application based on a digital twin».

REFERENCES

Averchev, I. V., 2011. Management accounting and

reporting. Statement and implementation, Rid grupp. p.

416.

Babina, S. I., 2019. Digital and information technologies in

enterprise management: reality and a look into the

future. Creative economy. 13 (4).

Gribanovskiy, V. M., 2010. The concept of management

accounting at the present stage of development of the

Russian economy). In Management Accounting. 1. pp.

7-11.

Horngren, Ch. T., Foster, Dzh., 2000. Accounting: the

management aspect. Finance and statistics. p. 416.

Karanina, E., 2017. Conceptual and analytical aspects of

regional economy's risk system. In The 11th

International Days of Statistics and Economics

September 14–16.

Karanina, E., 2017. Indicators of economic security of the

region: a risk-based approach to assessing and rating. In

IOP Conference Series: Earth and Environmental

Science: 19th International Scientific Conference on

Energy Management of Municipal Transportation

Facilities and Transport (EMMFT 2017). 90(1).

Kim, L. I., 2019. Strategic management accounting,

INFRA-M. p. 202.

Vakhrushina, M. A., Sidorova, M. I., Borisova, L. I., 2018.

Strategic management accounting: textbook,

KNORUS. Moscow. p.184.

Vinogradov, P. A., 2018. The problem of introducing

strategic management accounting at an enterprise). In

Young scientist. 50 (236). pp. 118-122.

Yur'yeva, L. V., 2013. Strategic management accounting

for business, NITS INFRA-M. p. 336.

SES 2021 - INTERNATIONAL SCIENTIFIC-PRACTICAL CONFERENCE "ENSURING THE STABILITY AND SECURITY OF

SOCIO - ECONOMIC SYSTEMS: OVERCOMING THE THREATS OF THE CRISIS SPACE"

116