Environmental Management Accounting Implementation in Higher

Education: Case Study in Universitas Negeri Semarang

Kusmuriyanto, Anna Kania Widiatami and Nurdian Susilowati

Department of Economic Education, Universitas Negeri Semarang, Kampus Sekaran, Gunungpati, Semarang, Indonesia

Keywords: Environmental Management Accounting, Environmental Cost, Environmental Impact, Higher Education.

Abstract: Environmental problem issues that increasingly worrisome has become a central focus of all entire

community, including educational institution. As a form of the University Social Responsibility (USR),

Universitas Negeri Semarang (UNNES) is committed to becoming a conservation university. This research

methodology uses a qualitative method utilizing an in-depth interview. The research subjects were the

Technical Implementation Unit (UPT) of the University Conservation Development and the Group

Conservation Unit. UNNES not fully implementing yet Environmental Management Accounting; only

information about the use of electricity and paper has physical and monetary. Although there are several

obstacles to implementing EMA, UNNES has applied to the movements and activities related to the

environment. These environmental care movements have proven to produce cost efficiencies.

1 INTRODUCTION

The issue of environmental problems is still a

significant concern around us. ALMI (Indonesian

Young Scientists Academy) and Thamrin School of

Climate Change and Sustainability researches warn

this global warming problem to be solved

immediately. If it is not to be solved immediately,

then the risks will occur. Such as the threat of

ecosystem and biodiversity diversity, food security,

health, and even economic stability (din/evn, 2019).

The impact of global warming is increasingly evident

that forces us to begin to fix our behavior so that the

rate of increase in the earth's temperature slows. The

role of the community is needed to realize the slowing

increase in the earth's temperature. The role of

management in every organization, both the private

sector and government, need the implementation of

environmental accounting.

Environmental accounting is one means of

reporting costs incurred related to the environment in

operational activities. In the environmental

accounting sub-section, there is an environmental

management accounting (EMA) as a reference in

making decisions related to information on

environmental costs. The definition of EMA is an

identification, collection of analysis, and use of two

types of information used for internal decision

making. The information used includes physical

information (in the use of energy, water, and

materials) and also financial information on costs

associated with the environment (IFAC, 2005).

EMA has begun to be applied to government,

especially Higher education institutions. Higher

education activities have direct and indirect impacts

on environmental issues, although not as significant

as the manufacturing industry (Chang, 2013). The

consumption of paper, electricity (for air conditioners

and lamps), and water excessively are examples of

causes of rising earth temperatures, which are a direct

impact of activities in educational institutions.

Embedding the character towards the environment

through both the education system and the research

conducted are the indirect impacts in an educational

activity. Managing and reducing total energy, water

use, and materials used by organizations helps to

reduce the impact of organizational activities on the

environment indirectly (IFAC, 2005).

Increasingly, more and more universities have

begun implementing University Social

Responsibility (USR) as a form of university

responsibility towards the environment. One of the

Higher Education institutions implementing USR is

Universitas Negeri Semarang (UNNES). UNNES is

the first Conservation University in Indonesia. Based

on the website of the UNNES Conservation Unit, on

March 12, 2010, UNNES declared itself a

Kusmuriyanto, ., Widiatami, A. and Susilowati, N.

Environmental Management Accounting Implementation in Higher Education: Case Study in Universitas Negeri Semarang.

DOI: 10.5220/0009966704950502

In Proceedings of the International Conference of Business, Economy, Entrepreneurship and Management (ICBEEM 2019), pages 495-502

ISBN: 978-989-758-471-8

Copyright

c

2020 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

495

conservation university. Since then, UNNES was

determined to apply conservation principles. UNNES

implemented through its vision and mission both

within the University and in each faculty (Bangvasi

UNNES, 2017).

As the first conservation university, UNNES has

the mission to be a conservation-oriented and

internationally reputable university. Unfortunately,

UNNES never becomes the first on the Indonesia Top

10 greenest campuses. Based on the UI Green Metric

Ranking 2017, UNNES was at the fourth position on

Indonesia's top 10 greenest campuses. Even in 2018,

UNNES’s position dropped to the fifth position. It

caught the researcher's attention to see how

management implementing the environmental

activity, especially in the management accounting

field at University.

Previous research in the public sector found that

several states and local governments have compiled

environmental reports that show trends in ecological

and ecosystem functions. At different levels, the

United Kingdom is encouraging governments in

every government department to report on

environmental costs, including the use of water,

garbage, and energy use (Ball & Bebbington, 2008).

Another research that focuses on green accounting in

public hospitals in Denmark found that

environmental reports record with financial and non-

financial measurements (Füssel & Georg, 2000). The

University exert resources and funds in carrying out

programs related to conservation, so environmental

accounting is needed to measure whether the eco-

efficiency method used has had an impact on the

environment (Sutherland, Lord, & Ball, 2008). Now

accounting faces a big challenge for environmental

preservation efforts not only through the role of

recording and reporting but also has a role in

managing environmental performance.

There was previous research on the application of

EMA at Universitas Negeri Semarang. The results

showed that budgeting for funding the

implementation of EMA at UNNES had proceeded

after the SOP using the SIANGGAR budget system

and recorded in the accounting system, SIKEU.

Whereas for the assessment of the performance of

UNNES uses benchmarks in the UI Green Metric and

ranked 6 in 2016. However, from the limitations of

previous research, innovations in the application of

EMA in universities are still needed (Latifah,

Kardiyem, & Susilowati, 2019). Therefore,

researchers want to dig deeper related to the

application of EMA in Universitas Negeri Semarang.

2 RESEARCH PURPOSES

This research aims to know how extent Universitas

Negeri Semarang (UNNES) to implementing

Environmental Management Accounting (EMA).

Further, the explanation of the research question in

detail as follows:

1. What policies have been implemented to

support the implementation of EMA in

universities?

2. To what extent can EMA be implemented in

teaching and learning activities and

administrative activities within the University?

3. What are the obstacles to implementing EMA in

universities?

4. Is EMA useful in creating cost efficiency?

Through this research, it is expected to provide a

clear picture of the implementation of EMA

information. From the EMA Information, we will see

the obstacle and the benefits of UNNES as a

conservation university.

3 THEORETICAL BASIS

Contingency theory is the application of various

management accounting studies in the era of the 70s.

Contingency variables classify into three groups,

namely environment, organizational structure, and

technology (Emmanuel, Otley, & Merchant, 1990).

These three variables occur in almost all research in

management accounting. The role of business

strategy in designing accounting systems is another

flow in contingency research. An uncertain

environment is one of the variables that can be linked

to environmental accounting management (Osborn,

2005). Because the focus of this research is on the

natural environment, the attention and focus are on

the uncertainty associated with the natural

environment.

Environmental accountability requires an

organization to be involved in environmental

management and provide financial and non-financial

resources for environmental impacts and the

implementation of environmental-related

management activities (Burritt & Welch, 1997). The

development of environmental accountability in

management accounting is environmental costs,

investment appraisals, environmental performance

indicators, capital budgets, and environmental-related

management strategies (Parker, 2000).

Environmental accountability is the result of

managers' responsibility towards environmental

performance if the concept of information

transparency is applied. Managers are responsible for

ICBEEM 2019 - International Conference on Business, Economy, Entrepreneurship and Management

496

environmental improvement in a sustainable manner

(Gray, Owen, & Adams, 1996). The major territory

environmental accounting can be described as below:

Figure 1: The fundamental territory of environmental

accounting

The pressure through regulations on

organizational responsibility for the environment has

arisen lately. Organizations are required to minimize

their activities that have an impact on the

environment.

For this reason, the information on environmental

costs needed to become one of the benchmarks of an

organization's responsibility to the environment. The

information on environmental costs, namely, a cost

that appears from prevention and environmental

management, materials and energy used, waste from

activities of the organization activities. By applying

environmental management cost, it can help identify

cost savings (Wang, Wang, & Wang, 2018).

The main focus of the EMA concept is to foster

manager awareness about potential interests, both

positive and negative, of the environmental impact on

company performance. So the information presented

by EMA must include hidden costs in overhead or the

future period and impacts that occur outside the

organization that cannot be provided by conventional

accounting (Burritt, Hahn, & Schaltegger, 2002;

Qian, Burritt, & Monroe, 2011). The implementation

of EMA has attracted the attention of managers to

help regulate environmental performance. EMA

implementation provides benefits as a decisive

decision-maker because they highlight environmental

costs and allocate these costs appropriately. So,

Environmental Management Accounting (EMA) is a

tool used by management in improving financial

performance through increased environmental

accountability (Jalaludin, Sulaiman, & Ahmad, 2011;

Chang, 2013; Latifah, Kardiyem, & Susilowati,

2019). The application of EMA requires the

classification of different information, including

(IFAC, 2005; Qian, Burritt, & S.Monroe, 2018):

1. Information on monetary units and physical

units related to environmental activities and the

use of relevant materials and energy.

2. Indirect internal costs to the organization but are

hidden in overhead or ignored in future periods.

3. Recognition of external environmental costs,

impacts, and opportunities not seen in a

conventional accounting

Environmental Management Accounting (EMA)

classified into two categories, as follow (Ambe,

Ambe, & Fortune, 2015):

1. Monetary Environmental Management

Accounting (MEMA)

2. Physically Environmental Management

Accounting (PEMA)

3.1 Monetary Environmental

Management Accounting (MEMA)

The application of environmental management

accounting requires information as a management

tool in making decisions related to environmental

costs. Monetary Environmental Management

Accounting or MEMA is a sub-system of EMA that

only looks at the financial impact of environmental

performance (Ambe, Ambe, & Fortune, 2015).

MEMA is used by internal managers to help evaluate

better in monetary terms when making decisions.

Examples of monetary unit information, namely,

costs to prevent environmental pollution, costs for

material purchases to costs incurred to overcome

environmental problems that occur due to

organizational activities.

3.2 Physically Environmental

Management Accounting (PEMA)

Managements need monetary and physical unit

information to make decisions regarding

environmental costs. PEMA is the generalization and

recording of physical data from energy inputs, use of

materials, waste products, and emissions used by

internal managers to make decisions (Ambe, Ambe,

& Fortune, 2015; Gunarathne & Lee, 2015).

Examples of physical Information needed in higher

education activities include the use of water and

gasoline measured in litters, electricity measured in

kWh, use of paper in reams, and others. PEMA, as an

internal environmental accounting approach provides

(Burritt, Hahn, & Schaltegger, 2002):

1. Analyze tools designed to detect ecological

strengths and deficiencies

2. Techniques that support decisions that focus on

the quality of the relative environment

3. Measurement tools that are an integral part of

other environmental measurements such as

environmental efficiency

Environmental Management Accounting Implementation in Higher Education: Case Study in Universitas Negeri Semarang

497

4. Tool for controlling both, directly and

indirectly, the environmental consequences

5. A neutral and transparent accountability tool for

internal, indirect and communication with the

external

6. A close and complementary tool with a set of

tools developed to help sustainably develop

ecology.

4 RESEARCH METHODS

This research uses a qualitative approach, namely,

case studies. The reason for using case studies is that

they are considered more flexible. It helps researchers

find essential factors that arise from real-life contexts.

This research will produce a model of environmental

management accounting records so that what is

budgeted (planned), implemented (program), and

produced (evaluation and monitoring) can be

measured economically. Besides, the records of

management accounting will obtain information

related to environmental performance, so that the

program can be measured both financially and non-

financially. In subsequent studies, the environmental

accounting records is an embryo of environmental

management accounting. So that University can

achieve environmental accounting reporting and can

report environmental responsibility to the public.

The subjects of this study were all members and

staff of the University Conservation Unit and

conservation groups in each faculty unit.

Conservation UPT members are people chosen by the

University to be responsible for the University's

conservation program. They are very aware of the

activities carried out related to the environment at the

university level. Meanwhile, the conservation group

is responsible for all types of activities related to the

environment at the faculty level. The type of research

data is quantitative and qualitative data. Quantitative

data in this research is the document that related to

budget information for conservation or

environmental purposes. The research also needs the

data that report relates to achieving conservation or

environment program. Qualitative data in this

research is information on what activities are carried

out in the field of conservation or the environment.

In-depth interviews with the head of the University's

conservation UPT and conservation groups in each

faculty unit have done to obtain the data.

Data analysis techniques used in this study were

carried out with quantitative and qualitative

approaches. When the researcher analyses the budget

document data during the context analysis activity

was using the quantitative technique. Also, when the

researcher was analyzing the results of the activity-

based environmental management accounting model

validation. Through Focus Group Discussion (FGD),

the qualitative techniques were done to obtain the

data. Focus Group Discussion (FGD) was held to

discuss the environmental cost budgeting mechanism

in each unit and the implementation of the budget

planning of it. The participants of FGD were 8

participants that are the head of conservation groups

in every faculty at UNNES.

In-depth interviews use the checklist sheet as

follows to obtain the data:

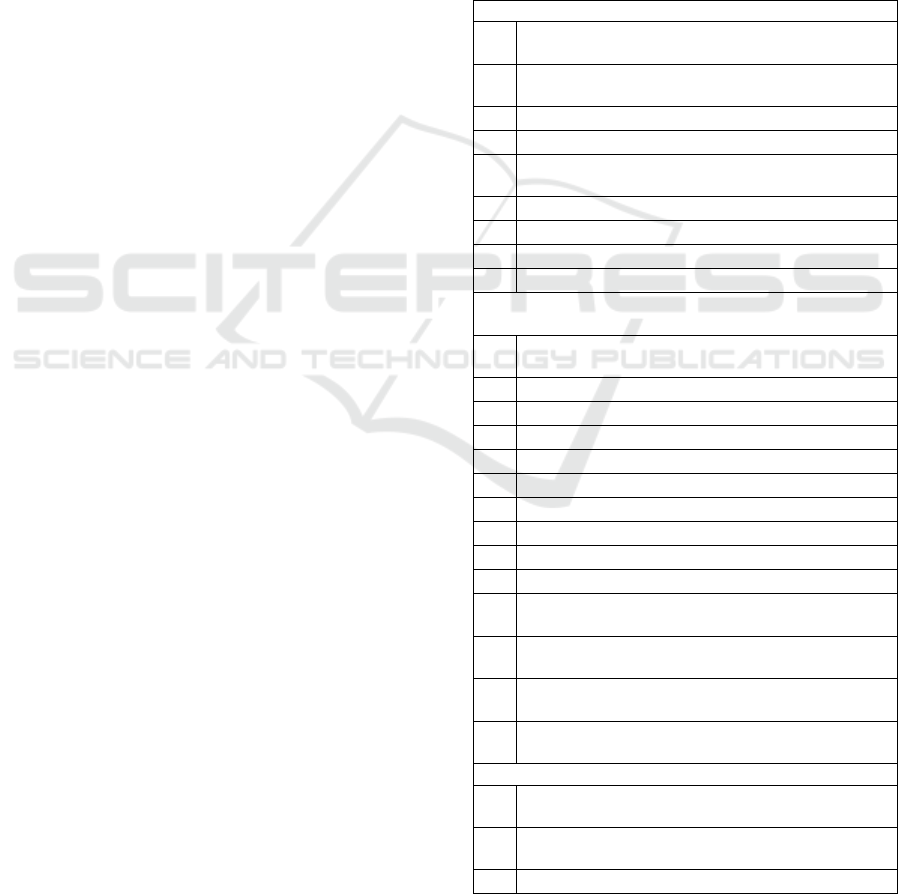

Table 1: Checklist sheet on Data Analysis

Budgeting

1

The budget on garden management and

maintenance

2

The budget on using eco-friendly materials

building

3

The budget on the internal transportation system

4

The budget on waste management cost

5

The budget on training for UPT management and

conservation groups

6

The budget on conservation activity.

7

The budget for art and culture activity

8

The budget on conservation research

9

The budget for renewable energy

Environmental Management Accounting (EMA)

Implementation

1

Environmental cost identified and calculated

separately

2

Each of environmental cost recorded physically

3

Each of environmental cost recorded monetary

4

Information on waste produced

5

Policy on saving electricity usage

6

Policy on saving water usage

7

Policy on paperless

8

Policy on reducing waste yields

9

Conservation activity annually

10

Art and culture activity annually

11

Training for UPT management and conservation

groups annually

12

UPT management and conservation groups have a

green building concept program

13

Policy on Internal transportation system to reduce

pollution.

14

Plant care was doing routinely

Realization and Supervision of Budget Cost Usage

1

Supervision on the realization of environmental

cost budget.

2

Supervision on garden management and

maintenance realization

3

Supervision on conservation activity realization

ICBEEM 2019 - International Conference on Business, Economy, Entrepreneurship and Management

498

4

Supervision on art and culture activity realization

5

Supervision on conservation research realization

6

Supervision on training for UPT management and

conservation groups realization

7

Electricity cost reduce since the policy of saving

electricity implemented

8

Water cost reduce since the policy of saving water

implemented

9

Paper purchase cost decrease due to the policy of

paperless implemented

10

Waste management cost decrease due to the policy

of waste produce restriction

11

All the budget that has prepared used following

with budget planning

In-depth interviews conducted during context

analysis activities and checklist sheets when

conducting alternative solutions (brainstorming) and

product reviews. Therefore, in this study, the position

of the two analytical techniques is expected to be

complementary.

5 DISCUSSION

5.1 The Policies That Have Been

Implemented to Support the

Application of EMA in Universities

Universitas Negeri Semarang, which is one of the

state universities in Semarang, Central Java province,

Indonesia, as a place for a case study of this research.

UNNES declared itself a Conservation University on

March 12, 2010. Principles to be implemented soon

include protecting, ordering, and utilizing natural

resources more wisely, reserving arts and culture, and

applying the University's Tri Dharma (Three

Principles) with a friendly insight environment. In its

efforts to implement it, a conservation team was

formed and then tasked with designing and making a

blueprint to prepare UNNES as a Conservation

University. The specifical task of the conservation

team is to develop policies and activities related to

biodiversity, green architecture, and internal campus

transportation management, waste management,

clean energy, paperless policies, arts, and cultural

conservation, and management of conservation

cadres. The issuance of the Minister of National

Education Regulation of the Republic of Indonesia

Number 8 of 2011 concerning the Statute of the

Universitas Negeri Semarang was confirming the

position of UNNES as a conservation university. At

that statute, stated that the vision of UNNES was to

become a world-class, healthy, superior, and

prosperous conservation university in 2020. In 2011,

under UNNES, Rector Decree No. 35 / P / 2011 was

transforming the conservation team into the

Conservation University Development Board. In

2016, the Conservation Development Agency was

changed to become the Conservation Development

Technical Implementation Unit (UPT).

The supporting policies of EMA are Rector of

Universitas Negeri Semarang Regulation No. 21 of

2019 concerning the prohibition of the use of

disposable plastics, Rector of Universitas Negeri

Semarang Regulation No. 51 of 2018 concerning

accounting guidelines and management of Public

Service Agency accounts receivable, and Rector of

Universitas Negeri Semarang Regulation No. 41 of

2018 concerning electronic budget monitoring and

evaluation. Head of UPT Development Conservation

in University states there are not much-written

policies yet related to the conservation program.

“No written policies yet related to the

conservation that implemented in UNNES except the

prohibition of the use of disposable plastics. All the

conservation program only is written appeals, such

as stickers to wisely use water and electricity when

not in use and culture for cycling or walking in

UNNES.”

Going forward, UNNES is currently negotiating

the concept of issuing other regulations relating to

other environments as a form of commitment by the

Conservation University.

5.2 Implementation of Environmental

Management Accounting (EMA)

Accounting records at UNNES have used an

integrated system, namely SIKEU. This financial

information system allows accountants to make

accounting records following the budget that has

planned. The reports uploaded into the system with

the transaction receipt attached to control the

payment. Decisions concerning the environment

made based on budget and financial accounting,

according to SIANGGAR (budget system) and

SIKEU (financial accounting system).

Universitas Negeri Semarang pays full attention

to the environment and its preservation. The

Conservation Development Technical

Implementation Unit (UPT) is proof of it. The team

has a task to manage conservation and environment

issues in UNNES. Their responsibility is to manage

funds for various activities such as biodiversity, green

architecture, waste management, clean energy,

paperless policies, arts and cultural conservation, and

management of conservation cadres for students.

Conservation UPT embeds and maintains the

character in students as agents of change to care about

environmental issues.

Environmental Management Accounting Implementation in Higher Education: Case Study in Universitas Negeri Semarang

499

Funding for the activities related to the

environment at UNNES comes from previously

budgeted funds. As for the amount, it depends on the

budget proposed by the Conservation Development

Technical Implementation Unit (UPT) by submitting

a program proposal along with its costs. Furthermore,

after the submission of this proposal, the amount will

be distributed, depending on the decision made by the

Governance Organization. The preparation of the

budget itself involved many parties, such as members

of the Conservation Technical Implementation Unit

(UPT), the leader, in this case, the Vice-Rector IV,

and the University's budget department. The

budgeting process has used a particular system,

namely, SIANGGAR (budget system).

UNNES has not been entirely applying physical

recording as management information or Physically

Environmental Management Accounting (PEMA).

Most of the environmental costs in monetary terms or

Monetary Environmental Management Accounting

(MEMA).

“Physical records are only applied to the use of

electricity and paper. We record the physically of

electricity used based on the bill that we paid

monthly. For paper, we record it physically to ask to

the procurement department. Based on the usage of

paper, we spent 40 reams in a year for administrative

purposes.”

There is a budget for the environmental activities

are held regularly to support the conservation

program.

“There is an annual conservation event that new

students have to join. All new students have to plant

trees in the university environment, and they have the

responsibility to take care of the tree that they plant.”

UNNES also held environmental activities for all

employees. Every Friday morning, all employees

require to join in sports activities. Besides, UNNES

held wayang performances regularly that rarely found

now. That is a conservation movement to preserve art

and culture. So, the budget will always be prepared

for all of those environmental activities that are held

regularly.

On the academic side, there is also a particular

budget for lecturers who will conduct research or

service related to conservation or the environment. It

is an effort to have an indirect impact on

conservation. The more research and service on the

environment has done, the more environment

knowledge will be spread.

The recently adopted regulation is a prohibition

on the use of disposable plastics in the university

environment. This regulation is applying as an effort

to reduce plastic waste. All activities at UNNES, such

as meetings, workshops, seminars, or other activities,

have required participants to bring their drinking

bottles. A refill water station will be available in

every room to support this program. Also, to reducing

paper waste from these activities, the packaged

consumption provided using bamboo baskets and

buffet dishes. So, the regulation is expecting to create

that "zero waste" even from the meeting activities. As

an effort to limit the use of paper or other paperless

activities, UNNES utilizes technology such as

WhatsApp and telegram to share the information.

Also, all other administrative matters. Such as

semester learning plans, attendance for students and

employees, published annual financial reports have

also utilized technology to upload and download the

data. UNNES collaborates with third parties to

manage waste generated from daily activities.

Another implementation of environmental

management is to replace the lights in the rectorate

building. Rectorate building is the main building that

consuming the most electricity. The movement to

reduce electricity is by changing the CFL lamp using

an LED lamp. Also, install the sensors that can turn

off the lights automatically if no one is in a particular

room. The new buildings also have the guidelines as

"green buildings" or buildings with an

environmentally friendly concept. The form of

renewable energy from natural processes was to build

solar panels and bio pores. The effort to reduce

pollution, UNNES, provides electric cars as a means

of transportation in the UNNES environment.

5.3 The Obstacle to EMA

Implementation

As a conservation university, there are several

obstacles to implementing environmental

management accounting. According to the head of the

UPT University Conservation, the main obstacle in

implementing EMA is the lack of human resources

that individually handle conservation activities within

the University. The board of UPT University

Conservation and conservation groups in the faculty

is lecturers and students who are volunteers.

"The Head of Division and the conservation

group at UNNES are lecturers who have their

activities. Lecturers have responsibility for tri

dharma, namely, teaching, research, and serving. So,

it is tough to hold UPT officials and groups to always

be on standby in conservation activities."

While students as agents of change only have

volunteer status, so there are no special funds that can

be used to maximize the operational UPT of

conservation development. The limitation of human

resources is the cause of the absence of detail the

environmental reporting as information. No one has a

task to do individual supervision and to classify the

ICBEEM 2019 - International Conference on Business, Economy, Entrepreneurship and Management

500

more detailed costs associated with environmental

costs.

The next obstacle for the implementation of

EMA, according to the chairperson of the UPT

University Development Conservation, is the limited

budget funds for developing conservation activities

within the University.

UPT University Development Conservation also

lacks "power" as the organization is under the Rector

so they cannot drive the conservation activities.

"Besides human resources, another obstacle is

limited funds, so the UPT cannot execute the activities

directly, especially related to research in the UNNES

environment. So, we are only able to provide concepts

and give to the Rector for the implementation. For

example, the construction of new buildings, we

always give the concept of green building, but to be

implemented or not, the decision is on the Rector and

not our authority."

The readiness of budget implementers who do not

fully understand the accountability of activities is the

obstacle in implementing EMA. The budget-related

environmental issues that have planned cannot be

implemented by 100%. They only aim to spend the

budget that has been provided by not giving a real and

apparent contribution. Another obstacle is that

several University policies do not legally yet. So that

implementation in each unit cannot be entirely

executed.

5.4 The Benefits of EMA in Creating

Cost-Efficiency

Although Universitas Negeri Semarang has not been

entirely implementing the application of EMA, the

information on the use of electricity and paper has

been recorded physically and monetarily. This

information encourages environmental management

in the UNNES Rectorate Building to use LED lights

and sensors that can turn off lights automatically

when there is no one in a room. Also, several

buildings have been built using solar panels.

“The decision to changes on LED Lamp and

install the sensor at the rectorate building. The sensor

can turn off lights automatically when there is no one

in a room. It impacts on reducing a lot the cost. It has

an impact on saving electricity costs paid every

month compared to before applying the concept.

However, it is the only implementation in the

Rectorate Building and not the whole building yet at

UNNES.”

The physical recording of paper usage helps

universities to control excessive use of paper. One of

the paperless efforts undertaken by UNNES is to

utilize technology as an administrative tool.

Implementing the paperless movement creates cost

efficiency and work time effectiveness in managing

matters related to the administration.

The presence of bipori in several university

buildings also has an impact on cost savings.

According to Wulandari, Banowati, and Putro (2015),

plant roots and soil organisms activate biopori

infiltration holes and will maintain groundwater

infiltration without human intervention. It certainly

saves energy and costs for the maintenance of biopori

itself. Biopori is also useful for optimally absorbing

rainwater into the soil, so there is no rainwater in the

University environment. Puddles of rain that do not

flow can be a source of disease and the risk of

flooding in the rainy season. With this biopori, it can

reduce the allocation of costs for flood mitigation and

can be maximized for other cost allocations.

6 CONCLUSION

Environmental Management Accounting (EMA) is a

management tool for improving financial

performance through increased environmental

accountability. The main focus of the EMA concept

is to foster manager awareness about potential

interests, both positive and negative, of the

environmental impact on company performance. So,

the information presented by EMA must include

hidden costs, both physically and monetary

information. As a conservation university, UNNES

has not applied environmental management

accounting entirely. Lack of detailed information

regarding environmental costs is proof that it does not

implement entirely. Physical and monetary

recordings or units just can be seen from the use of

electricity and paper. The use of water only records

as monetary units. Besides, there is no specific

supervision in environmental activities. The lack of

human resources and some regulations that do not

legally yet are considered to be the main obstacles in

implementing environmental management

accounting in UNNES. There is no particular person

in charge to supervise the environmental activists in

the field and records the environmental cost, both

physically and monetary. The absorption of funds is

the benchmark of environmental activities evaluation

from the year's budget that has prepared.

Fully implementation of EMA can be seen only

from the use of paper and electricity. Restrictions on

the use of paper and utilization technology on

administrative matters prove efficiency cost. Also,

the decision to changes on LED Lamp and install the

sensor that can turn off lights automatically in the

Rectorate Building prove it too. However, it just

applied at rectorate building and not the entire

buildings in University. For the future, UNNES is

Environmental Management Accounting Implementation in Higher Education: Case Study in Universitas Negeri Semarang

501

expected to implement environmental management

accounting in full, to realize the efficiency of costs

related to the environment. Also, the decision taken

by management is expected to provide benefits to

support environmental preservation efforts.

As a place of education, UNNES also embed the

characteristics of students to care for environmental

issues and preserve nature. It can be realized by

planting trees and regenerating students as agents of

change that will help campaign for environmental

issues. As a conservation university, UNNES has

committed to continue to implement activities that

support the environment following the University's

vision and mission. The electricity and paper saving

movement, the building of green buildings with solar

panels and biopores, and the provision of electric cars

as operational cars within the University are

examples of UNNES 'commitment to becoming a

conservation university.

REFERENCES

Ambe, C. M., Ambe, Q. N., & Fortune, G. (2015).

Assessment of Environmental ManagementAccounting

at South African Universities: Case of Tshwane

University of Technology. Journal of Governance and

Regulation Vol. 4, Issue 1, 274-288.

Ball, A., & Bebbington, J. (2008). Editorial: Accounting

and Reporting for Sustainable Development in Public

Service Organizations. Public Money and

Management, 323-326.

doi:http://dx.doi.org/10.1111/j.1467-

9302.2008.00662.x

Bangvasi UNNES. (2017). Retrieved from

http://konservasi.unnes.ac.id/badan-konservasi-unnes/.

Burritt, R. L., & Welch, S. (1997). Accountability for

environmental performance of the Australian

Commonwealth public sector. Accounting, Auditing &

Accountability Journal, Vol. 10 No. 4, 532-561.

doi:https://doi.org/10.1108/09513579710367494

Burritt, R. L., Hahn, T., & Schaltegger, S. (2002). Towards

a Comprehensive Framework for Environmental

Management Accounting - Links BetweenBusiness

Actors and Environmental Management Accounting

Tools. Australian Accounting Review, Vol. 12, No. 2,

39-50.

Chang, H.-C. (2013). International Journal of Sustainability

in Higher EducationEnvironmental management

accounting in the Taiwanese higher education sector:

Issues and opportunities. International Journal of

Sustainability in Higher Education: Vol. 14 No. 2,

2013, 133-145.

doi:https://doi.org/10.1108/14676371311312851

din/evn. (2019). Pemanasan Global Ancam Ketahanan

Pangan Hingga Ekosistem. Retrieved from

cnnindonesia.com.

Emmanuel, C., Otley, D., & Merchant, K. (1990).

Accounting for Management Control. Boston, MA:

Springer. doi:https://doi.org/10.1007/978-1-4899-

6952-1_13

Füssel, L., & Georg, S. (2000). The Institutionalization of

Environmental Concerns: Making the Environment

Perform. International Studies of Management and

Organisation, Vol. 30 No. 3, 41-58.

Gray, R., Owen, D., & Adams, C. (1996). Accounting &

Accountability: Changes and Challenges in Corporate

Social and Environmental Reporting. London: Prentice

Hall.

Gunarathne, N., & Lee, K.-H. (2015). Environmental

Management Accounting(EMA) for Environmental

Management and Organizational Change: An Eco-

control Approach. Journal of Accounting &

Organizational Change, Vol. 11 Iss 3, 1-25.

doi:http://dx.doi.org/10.1108/JAOC-10-2013-0078

IFAC. (2005). International Guidance Document:

Environmental Management Accounting, International

Federation of Accountants. New York.

Jalaludin, D., Sulaiman, M., & Ahmad, N. N. (2011).

Understanding Environmental Management

Accounting(EMA) Adoption: a New Institutional

Sociology Perspective. Social Responsibility Journal,

Vol. 7 Issue: 4, 540-557.

doi:https://doi.org/10.1108/17471111111175128

Latifah, L., Kardiyem, & Susilowati, N. (2019).

Investigating the Existing of Environmental

Management Accounting for Better Environment

Management: A Case Study in a University. European

Journal of Business and Management, Vol 11, No. 8,

46-51. doi:10.7176/EJBM/11-8-06

Osborn, D. (2005). Process and Content: Visualizing the

Policy Challenges of Environmental. Implementing

Environmental Management Accounting: Status and,

81-104.

Parker, L. D. (2000). Green Strategy Costing: Early Days.

Australian Accounting Review 10 (1), 46-55.

Qian, W., Burritt, R. L., & S.Monroe, G. (2018).

Environmental Management Accounting in Local

Government: Functional and Institutional Imperatives.

Financial Accounting& Management, 1-18. doi:DOI:

10.1111/faam.12151

Qian, W., Burritt, R., & Monroe, G. (2011). Environmental

Management Accounting in Local Government: A Case

of Waste Management. Accounting, Auditing &

Accountability Journal, Vol. 24 Issue: 1, 93-128.

doi:https://doi.org/10.1108/09513571111098072

Sutherland, M., Lord, B., & Ball, A. (2008). Environmental

Management Accounting. Social and Environmental

Accounting Research. Adelaide.

Wang, S., Wang, H., & Wang, J. (2018). Exploring the

effects of institutional pressures on the implementation

of environmental management accounting: Do top

management support and perceived benefit work? Bus

Strat Env, 1-11. doi:DOI: 10.1002/bse.2252

ICBEEM 2019 - International Conference on Business, Economy, Entrepreneurship and Management

502