The Effect of Return Volatility Mature Market on Emerging Market:

Economometry Model Approach-Granger Causality,

Vector Autoregression, Autocorrelation Condition Heteroscedasticity/

General Autocorrelation Condition Heteroscedasticity

Yunita Astikawati, Avelius Dominggus Sore

Economic Education, STKIP Persada Khatulistiwa, Jl. Pertamina-Sengkuang, Sintang, Indonesian.

Keywords: Return Volatility, Emerging Market, Mature Market

Abstract: The mature market dominates and affects the economic conditions in the emerging market. One of the

influences occurs in stock trading in the capital market. Therefore, it is necessary to do analysis to prove that

there is an influence of volatility return on the mature stock index on the emerging stock index. The mature

market index used are NYA, NASDAQ, FTSE100, HANGSENG, SSEC, and STI. The indices of emerging

markets are the IDX, SENSEX, SET, JSE, and TSEC. This analysis conducted by using the data from 2014-

2018. Data analysis used an econometry approach that is granger causality, VAR, and ARCH/GARCH. The

analysis which has done showed some results. First, the results of the analysis showed a reciprocal relationship

between the indices in the mature market and emerging market. Secondly, regional factors have an impact on

each of these indices that can be seen from the reciprocal relationship between mature and emerging index

residing within the same area. Thirdly, the return volatility index mature market simultaneously does not

affect on the return volatility index emerging market. Therefore, it is needed further analysis to predict the

emerging market influence on the mature market in a shorter time.

1 INTRODUCTION

Investments can be made by anyone and everywhere.

Investments can be said to be one of the factors

related to economic development. This economic

development can also be classified into three

categories: they are strong, developing, and weak

economies. In general, countries that have strong

economies often dominate the developing and weak

countries in various fields. One of that is the

economy. The developed country, which has

progressed in the field of economics, can create safe

investments and profitable. This leads to many

prospective investors who are more interested in

investing in developed countries. On the other hand,

developing and weak countries also have their own

appeal to potential investors. Developing and weak

countries generally provide a high return rate for

investors. High returns are also associated with a high

level of risk. Returns can be obtained in various ways,

one of them through a stock trading transaction.

Stock trading transactions can be made intraday. This

transaction can be a transaction to buy and sell shares

of the company.

Companies that perform well are more in demand

by investors because they produce attractive returns.

Return generated from stock trading also generally be

influenced by various factors; one of them is the

economic condition. When the economic condition of

a country is good, then the resulting return also

increases. Conversely, if the economic condition of

the country is not good or in other words, experienced

a crisis, then the resulting return will decrease. The

crisis in a certain country can also affect the condition

of other countries. One of them is the Venezuelan

economic crisis that impacted other countries through

the trade route.

American and Chinese trade war also provide

stimulation for other countries, especially developing

countries such as Indonesia. These two incidents have

an impact on Indonesia. It is seen from the weakening

of the rupiah exchange rate. The rupiah exchange rate

is an indirect effect of retaliatory concern made by

Americans against China. Overheating also has a role

in elevated inflation. The Increase in inflation makes

Astikawati, Y. and Sore, A.

The Effect of Return Volatility Mature Market on Emerging Market: Economometry Model Approach-Granger Causality, Vector Autoregression, Autocorrelation Condition

Heteroscedasticity/General Autocorrelation Condition Heteroscedasticity.

DOI: 10.5220/0009961402110220

In Proceedings of the International Conference of Business, Economy, Entrepreneurship and Management (ICBEEM 2019), pages 211-220

ISBN: 978-989-758-471-8

Copyright

c

2020 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

211

investing more at risk. This risk is called systematic

risk. The systematic risk of increasing inflation is

followed by decreasing the exchange rate and interest

rate (Adisetiawan And Ahmadi, 2107). This

condition causes investors to transfer their

investments to other places that are considered safe.

This is due to the number of hot money in Indonesia.

In addition to the crisis, the economic policy also

impacts the investment return. Especially if the

economic policy is made by developed countries,

then it will impact on investment returns not only in

developed countries but also in developing and weak

countries. This impact can be both positive and

negative. This impact can be perceived directly and

indirectly to investors. This is due to the strong

influence of the developed countries to global

economic development. It is also proposed by

Triyono and Rubiyanto (2017), which states there are

mature country capital market relations represented

by the Americans that have an emerging influence of

Indonesia. Therefore, it is needed to analysis to prove

the strong economic influence on developing

economies through trading in stock indices. The

indices of shares are used, representing developed

countries or mature markets and emerging markets.

This analysis proves that the adverse effects of the

economy not only originate in developing countries

but also come from developed countries. This

analysis is different because in this study, using more

stock index in developed and developing countries

with a fairly long period of time. In addition, the

selected index already represents developed and

developing economic forms and represents the

general conditions of the region or continent.

Therefore, this research can prove the contagion

effect theory.

2 LITERATURE REVIEW

Capital market is a place where prospective investors

can meet to execute transactions. Capital market

based on the forms is divided into three, namely weak

form, semi-strong, and Stong. This market form has

an integral relationship with one another. There are a

few terms that can explain the chain effect of the

phenomenon transmission in the economic field.

Those terms are:

2.1 Domino Effect

Domino effect is a chain reaction that due to changes

in the economic field that causes changes in areas that

have similar characteristics. These changes are

propagating and continuously.

2.2 Ripple Effect

The ripple effect is like a wave that propagated into a

wider area. This can be modeled after a phenomenon

that occurs in a country that is transmitted to

neighboring countries.

2.3 Contagion Effect Theory

The contagion effect is a result of a financial crisis

that occurs in a country and affects other countries

(Trihadmini, 2011). This infectious effect has

occurred several times in this decade. Generally,

countries will be influenced when there is an

extraordinary phenomenon such as the economic

crisis, changing state status such as the exit of certain

countries in areas such as Brexit, which occurred in

2016. Contagion effects are defined in three types

(Hsien, 2012), i.e., basic, limited, and very limited.

The contagion effect of this basic type generally

occurs when there is good and bad information. This

impact will affect the economy between countries as

there will be shocks. However, this shock is not

necessarily caused by a crisis but can be caused by

other information such as an increase in interest rate.

The contagion effect that is limited meant that

changes or shocks that occur in a country would be

related to other countries. The other countries will get

positive and negative impacts. These impacts

generally occur beyond some fundamental channels.

Contagion effects that are very limited meant that the

impact which is gotten by the other countries is

limited only when the shocks occur and does not

affect the normal economic conditions.

2.4 Factors That Cause Contagion

Affect

The contagion effect is not only limited to the

consequences of financial turmoil that occur but can

also be caused by attitudes and fundamentals.

Investor behavior triggers volatility that has an impact

on diversification and hedging decisions (Alikhanov,

2013). The contagion effect caused by fundamental

factors divided into three types: they are common

causes, trade channels, and devaluative competition,

as well as financial channels.

The contagion effect caused by common causes

recently occurred when the Fed announced the

increase in the interest rate of the treasury bond

becomes 3.13%. It triggers capital flow from different

ICBEEM 2019 - International Conference on Business, Economy, Entrepreneurship and Management

212

countries to the State of America. This is, of course,

causing the movement or shifting of the flow of funds

from one country to another, thereby triggering

economic turmoil for other countries. Economic

turmoil is also felt by the country in the region of

Asia, especially Indonesia. The exchange rate of

Indonesian currency has decreased against the dollar

(depreciation). This change also affects the

movement of stocks in the country due to the number

of hot money coming out of the country.

Second types of Contagion Effect, i.e., Trading

channels and competition devaluative This Contagion

Effect is a little unique because this impact is caused

by local turmoil in a country but has a large impact on

the other countries. This generally occurs as a result

of trade relations between countries with turbulent

countries. The volatility is a depressive currency. A

depreciation currency provides greater value for trade

transactions. But on the other hand, it gives the

opportunity for the Exportir to get the benefit because

foreign countries will assume that the export value is

cheaper.

The last types of Contagion Effect, i.e., Financial

link, which occurs through the trading path made

between countries. The trading path carries a variety

of information flows and assets. When a country is

experiencing a crisis, it has a lot of impact on other

countries that have a direct trade relationship with the

country (Cheung et al., 2012) This financial problem

is not a major problem in the economy but what

triggers financial problems is the attitude of investors.

Therefore, this effect of transmission cannot be

separated from the problem of investor behavior.

2.5 Contagion Effect Caused by

Investor Behaviour

Cognitive, emotions and investor attitudes are the

main factors of a contagion effect (Beisswingert et al.,

2016). When an investor makes a decision to invest

or revoke his or her investment in a particular

country, it will have an impact on countries that have

a close relationship with the country. This impact can

be decreased investment interest that can be seen

from declining currency value, the stock trading value

decreases, occurrence of crisis, and others. Investor

behavior that triggers the effect of transmission is

caused by three aspects, they are 1)

liquidity problems, incentives, information

asymmetry, and coordination issues, 2) multiple

equilibria, 3) Regulatory changes about the

international financial system.

2.6 Types of Contagion

The contagion effect based on its type is divided into

two, namely spillovers and financial crises.

2.6.1 Spillovers

Spillover is an impact of which countries can not

stand alone in conducting economic activities or

better known as interdependence. When the state is

experiencing dependencies on the other countries,

then it is likely to be influenced in the economic

phenomenon is greater. The impact of the

phenomenon can be channeled through a financial

pathway that correlates with a trading route and a real

link.

2.6.2 Financial Crisis

The financial crisis is a situation where a country is

decreasing financial asset decline. The impact of the

contagion effect on the crisis period is generally more

perceived by the emerging market (Celik, 2012).In

addition, the problem of low-quality audits can also

trigger a contagion effect. This contagion effect is

actually due to changes in behavioral investors rather

than fundamental economic problems (Jere And Paul,

2013). It is caused that sometimes investors

overreaction to a piece of information so that the

decision is made into irrational.

Investors can invest directly in a company through

the purchase of shares. Investors get benefits during

the purchase of a stock sale transaction. The profit is

called return stock. Based on the type of return, it is

divided into two, namely expected return and realized

a return. Return shares do not loose relation with

stock volatility. The higher the volatility, the greater

the likelihood that investors will gain and loss. Return

can be calculated by using the following formula

(Jogiyanto, 2009).

(1)

Description:

Rm: return market

Pt: stock price now

Pt-1: the share price of the previous period

3 METHODOLOGY

This research aims to provide empirical evidence on

the interconnectedness of mature and emerging

The Effect of Return Volatility Mature Market on Emerging Market: Economometry Model Approach-Granger Causality, Vector

Autoregression, Autocorrelation Condition Heteroscedasticity/General Autocorrelation Condition Heteroscedasticity

213

markets. The subjects of research in this study are all

the stocks that are included in the stock index, such as

NYSE, NASDAQ, FTSE 100, SSEC, HANG SENG,

Kopsi, STI, SENSEX, IDX, JSE, Stock Exchange

Thailand, and TSEC Taiwan. This research will be

conducted by using daily data from 2014-2018. This

research used a quantitative approach. Research data

obtained from secondary data, which is data from

other subjects (Sekaran And Bougie, 2013).

Secondary data is obtained from the website:

investing, yahoo finance, Bloomberg, and capital

market websites in each country. Data analysis used

an econometric approach, and they are granger

causality, VAR, and ARCH/GARCH. The GARCH

was originally developed by Engle in 1982 as ARCH.

Autoregressive Conditional Heteroscedasticity

(ARCH) was redeveloped by Bollersev in 1986, and

now we know it as Generalized ARCH. GARCH is

relatively accurate for analyzing time-series data.

Based on the type, GARCH is divided into several

types, namely EGARCH, AGARCH, FIGARCH, and

SWARCH. GARCH is formulated as follows

(Winarno, 2011):

⍵

(2)

Description:

Σ _ T ^ 2: Conditional variant

⍵ : On average

ε _ (T-1) ^ 2: Volatility of the previous year

Σ _ (T-1) ^ 2: variant of the previous period

GARCH is used to calculate return volatility in the

mature index and emerging market. As it is known

that the ARCH model has many types, therefore,

before making a conclusion, it is worth determining

the best model with attention to the R2 value and sees

the coefficient of AIC and SIC.

4 RESULTS AND DISCUSSION

This analysis was done in several phases. The first

stage of data would be tested using causality granger

tests. In the second model selection analysis, the

selection of this model depends on the results of the

analysis of the causality granger. If the results of the

causality granger indicate a simultaneous

relationship, then the data would be tested using a

vector autoregression model. If there is no

simultaneous relationship, then the data will be tested

using the regression model. After analysis of the data,

regression will be analyzed using ARCH/GARCH.

4.1 Granger Causality

The entire variable is not the normal distribution of

JB's probability value of 0.00000 smaller than the

standard deviation of 5%. The results of the

Correlation Test showed that the data did not contain

multicollinearity problems. The data experiences a

multicollinearity problem if the correlation value is

more than 0,8 (Gujarati And Porter, 2009). Further

analysis was the causality granger test. This test was

done to see the reciprocal relationship between the

market index. Analysis results of causality granger

can be concluded as follows:

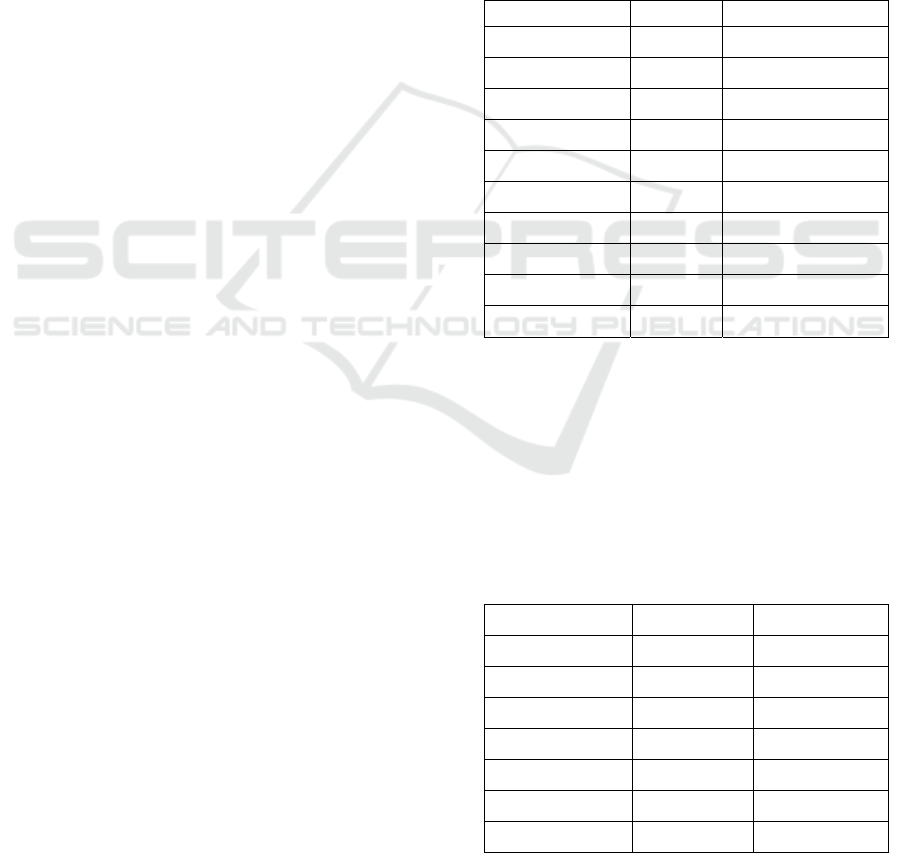

Table 1: Variables mutually affect simultaneously

according to the causality Granger test

X Y FORM

FTSE NYA SIMULTANEOUS

HANGSENG SSEC SIMULTANEOUS

KOSPI NYA SIMULTANEOUS

KOSPI STI SIMULTANEOUS

KOSPI TSEC SIMULTANEOUS

NASDAQ SSEC SIMULTANEOUS

NYA STI SIMULTANEOUS

NYA SET SIMULTANEOUS

SET TSEC SIMULTANEOUS

NASDAQ FTSE SIMULTANEOUS

Source: data processed eviews 7, 2019.

The results of the analysis above showed that the

relationship between a mature market and an

emerging market is not always direct. Moreover, not

all of the mature market indexes can affect the

emerging market.

VAR analysis for all variables affecting the above can

be resumed as follows:

Table 2: Summary of VAR test results with vector error

correction estimates

X Y R-Squares

FTSE NYA 0,442229

HANGSENG SSEC 0,457461

KOSPI NYA 0,451845

KOSPI STI 0,416653

KOSPI TSEC 0,423754

NASDAQ SSEC 0,484539

NYA STI 0,417251

ICBEEM 2019 - International Conference on Business, Economy, Entrepreneurship and Management

214

NYA SET 0,417135

SET TSEC 0,396980

NASDAQ FTSE 0,528429

4.2 Data Stationary Analysis

A stationary data test has done to see if each data was

stationary at a specific lag. The stationary test can be

done using a test of unit root test. The test root unit

results are presented as follows:

Roots of Characteristic Polynomial

Endogenous variables: FTSE HANGSENG IHSG JSE

KOSPI NASDAQ NYA SENSEX SET SSEC STI TSEC

Exogenous variables: C

Lag specification: 1 2

Date: 08/01/19 Time: 20:37

Root Modulus

-0.231244 - 0.403114i 0.464731

-0.231244 + 0.403114i 0.464731

-0.335029 + 0.293437i 0.445365

-0.335029 - 0.293437i 0.445365

0.013674 - 0.430347i 0.430565

0.013674 + 0.430347i 0.430565

0.172637 + 0.392257i 0.428566

0.172637 - 0.392257i 0.428566

0.297139 + 0.186774i 0.350964

0.297139 - 0.186774i 0.350964

-0.265798 + 0.185789i 0.324294

-0.265798 - 0.185789i 0.324294

-0.303985 0.303985

-0.007448 + 0.287453i 0.287549

-0.007448 - 0.287453i 0.287549

0.067636 - 0.251268i 0.260212

0.067636 + 0.251268i 0.260212

-0.134741 + 0.208202i 0.247998

-0.134741 - 0.208202i 0.247998

0.189189 - 0.074995i 0.203510

0.189189 + 0.074995i 0.203510

-0.182813 0.182813

-0.044866 + 0.098981i 0.108674

-0.044866 - 0.098981i 0.108674

No root lies outside the unit circle.

VAR satisfies the stability condition.

The above analysis used Lag 1

st

and obtained the

results of modulus value that there was no one greater

than 1. Return index stocks of mature markets and

emerging markets affect one another just in 1 period.

It can also be concluded that all data is stable or

stationary.

4.3 Modelling Analysis

The modeling analysis would be conducted to

determine whether a mature market and emerging

market index would be analyzed using regression or

other models. The first phase of data would be

analyzed using the least-squares regression model.

The analysis results are as follows:

4.3.1 NYA, NASDAQ, FTSE, HANGSENG,

SSEC, STI, KOSPI on the IDX

The result of regression Penggujian can be seen as

follows:

Dependent Variable: IHSG

Method: Least Squares

Date: 08/02/19 Time: 09:12

Sample: 1 870

Included observations: 869

Variable Coefficient Std. Error t-Statistic Prob.

C -0.000804 0.001203 -0.667956 0.5043

NYA -0.010759 0.167589 -0.064201 0.9488

NASDAQ 0.124303 0.116095 1.070703 0.2846

FTSE 0.118572 0.161193 0.735590 0.4622

HANGSE

NG 0.008941 0.154570 0.057846 0.9539

SSEC 0.028738 0.083012 0.346190 0.7293

STI 0.076751 0.160001 0.479691 0.6316

KOSPI 0.233211 0.173711 1.342523 0.1798

R-squared 0.014246 Mean dependent var -0.000691

Adjusted

R-squared 0.006232 S.D. dependent var 0.035528

S.E. of

regression 0.035418 Akaike info criterion -3.834056

Sum

squared

resid 1.080040 Schwarz criterion -3.790168

Log-

likelihood 1673.897

Hannan-Quinn

criter. -3.817263

F-statistic 1.777619 Durbin-Watson stat 1.081409

Prob(F-

statistic) 0.088439

Regression results indicate that all of the variables are

not significant. The value of Durbin Watson (DW)

1.081409 was smaller than the dl value that was

1.867606, so it can be concluded that data contains an

autocorrelation problem. The autocorrelation

problem generally occurs when data was time series.

The tests of heteroscedasticity test: Breusch Pagan

Godfrey is presented as follows:

The Effect of Return Volatility Mature Market on Emerging Market: Economometry Model Approach-Granger Causality, Vector

Autoregression, Autocorrelation Condition Heteroscedasticity/General Autocorrelation Condition Heteroscedasticity

215

Heteroskedasticity Test: Breusch-Pagan-Godfrey

F-statistic 0.222001 Prob. F(7,861) 0.9803

Obs*R-

squared 1.565619 Prob. Chi-Square(7) 0.9800

Scaled

explained SS 575.4494 Prob. Chi-Square(7) 0.0000

The results showed the value of OBS*R-squares

probability 0.9800 was much larger than the standard

error of 5%, so that can be concluded that data was

free of the problem of heteroscedasticity. Based on

the results of the above analysis, it can be concluded

that the best model for the mature return market to the

emerging market, which is represented by the IDX is

the regression model.

4.3.2 NYA, NASDAQ, FTSE, HANGSENG,

SSEC, STI, KOSPI against JSE

The first phase of the regression test would be carried

out and subsequently make an analysis model

decision whether to keep using regression or other

models such as ARCH/GARCH. Regression results

are presented as follows:

Dependent Variable: JSE

Method: Least Squares

Date: 08/02/19 Time: 09:16

Sample: 1 870

Included observations: 870

Variable Coefficient Std. Error t-Statistic Prob.

C 0.012090 0.010616 1.138848 0.2551

NYA 0.855876 1.479076 0.578656 0.5630

NASDAQ -0.255257 1.024463 -0.249161 0.8033

FTSE 0.501080 1.422389 0.352281 0.7247

HANGSE

NG 0.744040 1.364085 0.545450 0.5856

SSEC -0.460075 0.732635 -0.627973 0.5302

STI -0.965260 1.412069 -0.683579 0.4944

KOSPI -1.718689 1.532958 -1.121158 0.2625

R-squared 0.003253 Mean dependent var 0.011894

Adjusted

R-squared -0.004841 S.D. dependent var 0.311829

S.E. of

regression 0.312583 Akaike info criterion 0.521260

Sum

squared

resid 84.22443 Schwarz criterion 0.565108

Log-

likelihood -218.7480 Hannan-Quinn criter. 0.538037

F-statistic 0.401884 Durbin-Watson stat 2.201840

Prob(F-

statistic) 0.901422

The results of the analysis showed simultaneous all of

the variables are not significant. The value of DW

2.201840 was greater than 4dl value, which was

2.132394, so it was decided that occur autocorrelation

problem. The results of heteroskedasticity analysis

using the HETEROSKEDASTICIT test: Breusch

Pagan Godfrey acquired Obs*R-Squares value

probability 0.9885 and greater than the standard error

of 5%. It was concluded that data does not contain a

heteroscedasticity problem. Therefore data analysis

could use regression.

Heteroskedasticity Test: Breusch-Pagan-Godfrey

F-statistic 0.330644 Prob. F(7,862) 0.9402

Obs*R-

squared 2.329732

Prob. Chi-

Square(7) 0.9394

Scaled

explained SS 913.9632

Prob. Chi-

Square(7) 0.0000

4.3.3 NYA, NASDAQ, FTSE, HANGSENG,

SSEC, STI, KOSPI against SET

The result of the causality granger analysis above

shows that NYA and SET have simultaneous and

unidirectional relationships. Therefore NYA and SET

are tested using VAR. NASDAQ, FTSE,

HANGSENG, SSEC, STI, KOSPI have no

simultaneous connection to SET would be tested

using the regression model. The results of the

regression analysis are as follows:

Dependent Variable: SET

Method: Least Squares

Date: 08/02/19 Time: 09:23

Sample: 1 870

Included observations: 870

Variable

Coefficie

nt Std. Error t-Statistic Prob.

C 0.000291 0.000261 1.115233 0.2651

NASDAQ 0.011768 0.025196 0.467037 0.6406

FTSE 0.143512 0.029918 4.796775 0.0000

HANGSEN

G 0.142436 0.033553 4.245141 0.0000

SSEC

-

0.017029 0.018013 -0.945388 0.3447

STI 0.158738 0.034668 4.578809 0.0000

KOSPI 0.121329 0.037515 3.234156 0.0013

ICBEEM 2019 - International Conference on Business, Economy, Entrepreneurship and Management

216

R-squared 0.254501 Mean dependent var 0.000338

Adjusted R-

squared 0.249318 S.D. dependent var 0.008875

S.E. of

regression 0.007690 Akaike info criterion

-

6.889908

Sum squared

resid 0.051028 Schwarz criterion

-

6.851541

Log-

likelihood 3004.110

Hannan-Quinn

criter.

-

6.875228

F-statistic 49.10228 Durbin-Watson stat 2.146134

Prob(F-

statistic) 0.000000

The results of the above regression can be concluded

that both return index mature market does not affect

the return index of the emerging market. However,

partially FTSE, HANGSENG, STI, and KOSPI

positively affect to the SET. Further, the data would

be tested using the test of heteroskedasticit test:

breach pagan godfre. The test results can be seen as

follows:

Heteroskedasticity Test: Breusch-Pagan-Godfrey

F-statistic 0.636463 Prob. F(6,863) 0.7011

Obs*R-

squared 3.832794 Prob. Chi-Square(6) 0.6993

Scaled

explained SS 11.46290 Prob. Chi-Square(6) 0.0751

The probability value was 0.6993 or greater than 0.05,

so it can be concluded that data did not contain

problems heteroskedasticity. It was concluded that

the exact model was a regression.

4.3.4 NYA, NASDAQ, FTSE, HANGSENG,

SSEC, STI, KOSPI against TSEC

Analysis results of the causality granger showed that

KOSPI and TSEC have a simultaneous relationship,

then the data would be tested using VAR. NYA,

NASDAQ, TFSE, SSEC, STI, HANGSENG would

be tested using the regression model. Regression test

results can be seen as follows:

Dependent Variable: TSEC

Method: Least Squares

Date: 08/02/19 Time: 09:28

Sample: 1 870

Included observations: 870

Variable Coefficient Std. Error t-Statistic Prob.

C 1.27E-05 0.000234 0.054197 0.9568

NYA 0.029506 0.032395 0.910806 0.3627

NASDAQ 0.168801 0.022331 7.559020 0.0000

FTSE 0.169464 0.031292 5.415526 0.0000

HANGSEN

G 0.335148 0.027147 12.34585 0.0000

SSEC -0.028502 0.015999 -1.781542 0.0752

STI 0.081432 0.031070 2.620929 0.0089

R-squared 0.497959 Mean dependent var 0.000181

Adjusted R-

squared 0.494468 S.D. dependent var 0.009679

S.E. of

regression 0.006882 Akaike info criterion

-

7.111776

Sum squared

resid 0.040874 Schwarz criterion

-

7.073408

Log-

likelihood 3100.622

Hannan-Quinn

criter.

-

7.097095

F-statistic 142.6637 Durbin-Watson stat 2.164091

Prob(F-

statistic) 0.000000

Regression results indicate that jointly return mature

markets do not affect the return emerging market. But

partially NASDAQ, FTSE, HANGSENG, STI

significantly positive effect on TSEC. The results of

the analysis also showed that the data had been

autocorrelation because the value of DW 2.164091

was greater than 4dl, which was 2.132394.

Heteroskedasticity Test: White

F-statistic 18.86131 Prob. F(27,842) 0.0000

Obs*R-

squared 327.8819 Prob. Chi-Square(27) 0.0000

Scaled

explained

SS 686.2510 Prob. Chi-Square(27) 0.0000

The test results of the heteroscedasticity test: breusch

pagan godfre. It appeared that data had a

heteroscedasticity problem. It was intended that the

value of obs*R-squares Probability was smaller than

0.05. Therefore the data would be tested using

ARCH/GARCH.

ARCH/GARCH analysis would be done with the

principle of trial and error. This is because data

should be tested using many ARCH/GARCH models

to determine the best model. Based on the results of

trial and error was known that there was no

simultaneous influence between the return index

mature market to the return index emerging market.

But partially NASDAQ, FTSE, and HANGSENG

were significantly positive against TSEC. It can be

seen as follows:

The Effect of Return Volatility Mature Market on Emerging Market: Economometry Model Approach-Granger Causality, Vector

Autoregression, Autocorrelation Condition Heteroscedasticity/General Autocorrelation Condition Heteroscedasticity

217

Dependent Variable: TSEC

Method: ML - ARCH (Marquardt) - Normal distribution

Date: 08/02/19 Time: 09:40

Sample: 1 870

Included observations: 870

Convergence achieved after 25 iterations

Bollerslev-Wooldridge robust standard errors &

covariance

Presample variance: backcast (parameter = 0.7)

GARCH = C(9) + C(10)*RESID(-1)^2 +

C(11)*GARCH(-1)

Variable Coefficient Std. Error z-Statistic Prob.

@SQRT(GA

RCH) 0.101095 0.156149 0.647428 0.5174

C -0.000565 0.000975 -0.579237 0.5624

NYA 0.013580 0.052494 0.258700 0.7959

NASDAQ 0.166521 0.026651 6.248133 0.0000

FTSE 0.154400 0.037784 4.086350 0.0000

HANGSEN

G 0.338273 0.031439 10.75978 0.0000

SSEC -0.009648 0.020967 -0.460155 0.6454

STI 0.070778 0.044035 1.607335 0.1080

Variance

Equation

C

3.79E-

06

1.33E-

06 2.848742 0.0044

RESID(-1)^2

0.1331

14

0.0461

14 2.886623 0.0039

GARCH(-1)

0.7921

94

0.0564

78 14.02665 0.0000

R-squared

0.4968

11

Mean

dependent var 0.000181

Adjusted R-

squared

0.4927

25

S.D.

dependent var 0.009679

S.E. of

regression

0.0068

94

Akaike info

criterion -7.190470

Sum

squared

resid

0.0409

68

Schwarz

criterion -7.130179

Log-

likelihood

3138.8

55

Hannan-

Quinn criter. -7.167401

Durbin-

Watson stat

2.1542

10

4.3.5 NYA, NASDAQ, FTSE, HANGSENG,

SSEC, STI, KOSPI against SENSEX

The results of the causality granger test showed that

there is no reciprocal link between the return market

variables on the SENSEX. Therefore the first stage

would be carried out regression tests. The regression

test results are as follows:

Dependent Variable: SENSEX

Method: Least Squares

Date: 08/02/19 Time: 09:51

Sample: 1 870

Included observations: 870

Variable Coefficient Std. Error t-Statistic Prob.

C 0.000586 0.000278 2.103643 0.0357

NYA 0.095234 0.038791 2.455039 0.0143

NASDAQ 0.078287 0.026868 2.913767 0.0037

FTSE 0.157247 0.037304 4.215235 0.0000

HANGSE

NG 0.195162 0.035775 5.455225 0.0000

SSEC -0.053183 0.019214 -2.767852 0.0058

STI 0.032565 0.037034 0.879345 0.3795

KOSPI 0.167667 0.040204 4.170393 0.0000

R-squared 0.310601 Mean dependent var 0.000688

Adjusted

R-squared 0.305003 S.D. dependent var 0.009834

S.E. of

regression 0.008198 Akaike info criterion

-

6.760706

Sum

squared

resid 0.057932 Schwarz criterion

-

6.716858

Log-

likelihood 2948.907

Hannan-Quinn

criter.

-

6.743929

F-statistic 55.48071 Durbin-Watson stat 2.014021

Prob(F-

statistic) 0.000000

Test results of heteroscedasticity test: breusch pagan

godfre could be seen that the data have

heteroscedasticity problem because obs*R-squares

probability 0.0155 was smaller than 0.05. Further,

data would be tested using ARCH/GARCH.

Heteroskedasticity Test: Breusch-Pagan-Godfrey

F-statistic 2.499172 Prob. F(7,862) 0.0152

Obs*R-

squared 17.30535

Prob. Chi-

Square(7) 0.0155

Scaled

explained SS 39.52839

Prob. Chi-

Square(7) 0.0000

ICBEEM 2019 - International Conference on Business, Economy, Entrepreneurship and Management

218

ARCH/GARCH analysis results can be seen as

follows:

Dependent Variable: SENSEX

Method: ML - ARCH (Marquardt) - Normal distribution

Date: 08/02/19 Time: 09:58

Sample: 1 870

Included observations: 870

Convergence achieved after 29 iterations

Bollerslev-Wooldridge robust standard errors &

covariance

Presample variance: backcast (parameter = 0.7)

GARCH = C(10) + C(11)*RESID(-1)^2 +

C(12)*GARCH(-1)

Variable Coefficient Std. Error z-Statistic Prob.

@SQRT(GA

RCH) 0.116339 0.292554 0.397666 0.6909

C -0.000249 0.002309 -0.107796 0.9142

NYA 0.107584 0.047788 2.251302 0.0244

NASDAQ 0.086600 0.042781 2.024259 0.0429

FTSE 0.154962 0.045433 3.410787 0.0006

HANGSEN

G 0.203045 0.037782 5.374085 0.0000

SSEC -0.067711 0.027824 -2.433544 0.0150

STI 0.007846 0.065144 0.120437 0.9041

KOSPI 0.176170 0.045295 3.889381 0.0001

Variance Equation

C 3.57E-06 2.63E-06 1.353285 0.1760

RESID(-

1)^2 0.037982 0.020765 1.829186 0.0674

GARCH(-1) 0.909533 0.050917 17.86313 0.0000

R-squared 0.309544 Mean dependent var 0.000688

Adjusted R-

squared 0.303129 S.D. dependent var 0.009834

S.E. of

regression 0.008209 Akaike info criterion

-

6.777017

Sum squared

resid 0.058021 Schwarz criterion

-

6.711245

Log-

likelihood 2960.002

Hannan-Quinn

criter.

-

6.751851

Durbin-

Watson stat 2.014881

The results of the analysis showed that

simultaneously return the mature index market does

not affect the return index emerging market

represented by SENSEX. The data do not have

autocorrelation problems because the value of DW

2.014881 was between DU 1.915896 and 4-DU

2.084104.

4.4 Discussion

The effect of return index market mature overall

proved do not affect the return index market of the

emerging markets simultaneously. But after some

analysis, it can be known that the countries in the

same area have a reciprocal relationship. Although

the country has different market characteristics and

forms. The examples are HANGSENG, SSEC,

KOSPI, STI, TSEC, SET, which are located within

the Asian region, have a reciprocal relationship. In

addition, reciprocal relations also occur among the

return index of mature markets such as FTSE, NYA

NASDAQ, SSEC, HANGSENG, and KOSPI.

Reciprocal relations also occur between the return

index emerging market like SET, and TSEC. The

results of this analysis differ from the results, which

are stated by Adisetiawan and Ahmadi in 2018, who

stated that the Thai capital market has a reciprocal

relationship with the Indonesian capital market. It is

an overview that an incident that occurs in the mature

market capital market does not directly affect

emerging capital markets. This is because emerging

economies can take this opportunity to convince

investors to invest their funds in developing

countries. Of course, it is accompanied by

macroeconomic policies that are able to provide a

sense of security for investors. Developing countries

can cooperate with domestic companies to increase

economic growth by increasing exports. Increased

exports will certainly increase the profitability level

of the company and state. Profitability, which

increases, will certainly appeal to investor attention

and also increase investor confidence

.

5 CONCLUSION

This analysis has been concluded that there is no

effect on the mature market return index on the

emerging market return index. But there is a

reciprocal relationship between the return index in the

mature market. Likewise, in emerging markets, there

is a reciprocal relationship. In addition, the area factor

also has a big influence on the reciprocal relationship

between the index in both the mature market and the

emerging market.

6 SUGGESTION

Further research can perform the same analysis with

shorter time periods. Subsequent studies can also

The Effect of Return Volatility Mature Market on Emerging Market: Economometry Model Approach-Granger Causality, Vector

Autoregression, Autocorrelation Condition Heteroscedasticity/General Autocorrelation Condition Heteroscedasticity

219

analyze the emerging market's influence on mature

markets. This is because, generally, crisis and

economic problems begin in the country that is in the

emerging market.

ACKNOWLEDGMENTS

The researchers give thanks to the Ministry of

Research, Technology, and Higher Education of the

Republic of Indonesia and STKIP Persada

Khatulistiwa, who have supported and funded this

research.

REFERENCES

Adisetiawan, R, And Ahmadi. 2018. Contagion effect antar

negara ASEAN-5. Jurnal manajemen dan sains. 3(2):

203-216.

Alikhanov A. 2013. To What Extent Are Stock Returns

Driven By Mean And Volatility Spillover Effects? –

Evidence From Eight European Stock Markets. Review

Of Economic Perspectives. 13(1):3–29. doi:

10.2478/V10135-012-0013-7

Beisswingert BM , Zhang K, Goetz T, Fischbacher U .

2016. Spillover Effects of Loss of Control on Risky

Decision-Making. PloS ONE. 11(3):1-19.

doi:10.1371/journal.pone.0150470

Celik S. 2012. The More Contagion Effect On Emerging

Markets: The Evidence Of DCC-GARCH Model.

Economic Modelling. 29(5): 1946-1959.

Https://doi.org/10.1016/j.econmod.2012.06.011.

Cheung W, Fung S, Tsai S. 2012. Global Capital Market

Interdependence And Spillover Effect Of Credit Risk:

Evidence From The 2007-2009 Global Financial Crisis.

The Review of Financial Studies. 25(4):1111–1154.

https://doi.org/10.1093/rfs/hhr100

Gujarati, D.N. dan Porter, D.C., 2009, Basic Econometrics,

Mcgraw-Hill, New York, Fifth Edition.

Hsien, Lee Y.2012. The emerging market type putting

market size and growth in BRIC countries into

perspective. critical perspectives on international

business. 8(3): 241-258. doi

10.1108/17422041211254969

Jere R F, Paul NM. 2013. The Contagion Effect of Low-

Quality Audits. The Accounting Review. 88(2): 521-

552.. ttps://doi.org/10.2308/accr-50322

Jogiyanto. H., 2009. Teori Portofolio dan Analisis

Investasi, Yogyakarta, edisi keenam.

Sekaran U, Bougie R., 2013. Research Methods For

Business, Wiley. New York, Sixth Edition.

Trihadmini N,. 2011. Contagion Dan Spillover Effect Pasar

Keuangan Global Sebagai Early Warning System.

Finance And Banking Journal.13(1):47-61.

Triyono, D., & Robiyanto,. 2017. The Effect of Foreign

Stock Indexes and Indonesia’s Macroeconomics

Variables Toward Jakarta Composite Stock Price Index

(JCI) Advanced Science Letters, 23 (8):7211-7214.

Winarno WW,. 2011. Analisis Ekonometrika Dan Statistika

Eviews, UPP STTM YKPN. Yogyakarta, Edisi ketiga.

www.investing.com

www.yahoofinance.com

www.bloomberg.com

ICBEEM 2019 - International Conference on Business, Economy, Entrepreneurship and Management

220