Is Age and Power of Top Management Team Important in Leverage

Decision?

Nilmawati, Wisnu Untoro, Bambang Hadinugroho, and Atmaji

Sebelas Maret University, Solo, Indonesia

Keywords: Leverage, age, power, Upper Echelon Theory

Abstract: This study aims to examine the influence of the age of the top management team on corporate leverage, by including

power as a moderating variable. The study was conducted using panel data with 283 samples of non-financial

companies listed on the Indonesia Stock Exchange in the period 2010-2017. Testing is done using moderated

regression analysis (MRA). Leverage is measured using the book and market leverage, while the age of the

top management team is measured by the average age of the team, and power is measured using average share

ownership by a team divided by the number of shares outstanding. This research found that when the top

management team has power in the company, the older top management team will be more likely to choose

lower leverage decisions. This result is consistent with the Upper Echelon Theory which states that the

observable characteristics of the top management team can influence the company's strategic decisions.

1

INTRODUCTION

A number of studies have investigated the role of

manager characteristics in strategic organizational

decisions, such as in investment decisions, it was

found that the characteristics of the chief executive

officer (CEO) and the top management team

significantly influence the company's R&D

expenditures (Barker and Mueller, 2002, Chen, Hsu,

and Huang 2010). The managerial characteristics also

influence IPO decisions, and it was found that the

demographic characteristics of the CEO are the main

determinants in corporate risk-taking, namely the IPO

(Farag, and Mallin, 2016). As well as research by Yim

(2013), Jenter and Lewellen (2015) found that

managerial preferences, as measured by the

demographic characteristics of managers, influence

the tendency for acquisition decisions by companies.

The decision about leverage is one of the

company's strategic decisions that must be taken by

management. However, the decision about the use of

debt (leverage) is risky. The use of debt as one source

of external funding, on the one hand, is able to

improve company performance, as in the research of

Berger and Patti (2006), Cheng and Tzeng (2011),

Gharaiber (2015) found that debt financing

decisions by companies have a positive effect on

company performance. But on the other hand, debt

increases the risk of companies that can lead

companies to financial distress. Due to default

(Detthamrong, Chancharata, and Vithessonthic,

2017). The financial crisis that occurred in Asia and

America has raised questions about the aggressive

behavior of top executives (Tarraf, 2011). This makes

the manager's characteristics important to discuss

related to the use of debt by the company.

In Upper Echelon Theory, the executives act

based on their interpretations of the strategic

situations they face. These actions are influenced by

the cognitive base and their values, which will show

the valuable skills, knowledge basis, and information

processing abilities in the decision- making the

process (Hambrick, 2007). The cognitive and other

values from these top executives can be measured

through the demographic characteristics of the

manager, one of which is age. Young managers are

associated with new ideas and acceptance of risk

compared to older managers. Older managers tend to

have lower mental stamina and physical condition

than younger managers, more risk-averse, and

maintain the status-quo (Hambrick and Mason,

1984).Young managers are more likely to pursue

risks such as increasing financial leverage or an

unrelated diversification strategy.

The study about the effect of the chief executive

officer on debt decisions has not done much, and the

results are still provided mixed conclusions. The

424

Nilmawati, ., Untoro, W., Hadinugroho, B. and Atmaji, .

Is Age and Power of Top Management Team Important in Leverage Decision?.

DOI: 10.5220/0009960304240431

In Proceedings of the International Conference of Business, Economy, Entrepreneurship and Management (ICBEEM 2019), pages 424-431

ISBN: 978-989-758-471-8

Copyright

c

2020 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

study from Serfling (2014) showed that young

managers lead to higher debt levels, while older

managers show lower debt levels. Bertrand and

Schoar (2003) found that CEOs from the older

generation chose a lower level of financial leverage.

However, Malmendier et al. (2011) reported that

older CEOs have more debt. Whereas, Frank and

Goyal (2007) did not find any relationship between

age of CEO and leverage.

The inconsistency of research results which

linking age and leverage are likely due to variables

that moderate this relationship. According to

Carpenter (2004), in examining the relationship

between a manager's characteristics and company

strategy, there are several variables that can moderate

or mediate the relationship, including power. Power

has a very important role in decision making, when

CEOs power increases, their ability to influence

decisions will also increase (Daily and Johnson,

1997), and more easily imprint their personal

preferences on the firm (Korkeamäki, Liljeblom, and

Pasternack (2017). Bigley and Wiersema (2002)

mentioned that the interaction between power and

cognitive orientation of managers would affect

company strategic decisions. The prediction about the

use of power by the CEO requires an understanding

of the CEO's cognitive orientation towards the

company's strategy because power is the ability to

realize the desired preferences.

Thus, from this explanation, we can say that older

managers who tend to be more risk-averse are more

likely to choose lower leverage when they have power

in the company. In other words, power will strengthen

the negative influence of age on leverage.

The object of research in this study is the top

management team. Using the management team will

increase the potential strength of the theory to be

predicted since the chief executive shares the task and

gives strength to other team members to some extent

(Hambrick and Mason, 1984).

The first stage of this study investigates the effect

of age on company leverage decisions. Age is

measured using the average age of the top

management team. Whereas, leverage uses two

measurements, namely the book leverage and market

leverage. The results of this study are consistent with

the previous studies, which stated that age has a

negative effect on the leverage decision. This result

supports the Upper Echelon Theory.

The second stage of this study examines the effect

of power related to the effect of age toward leverage

decisions. In this study, power is measured using the

share ownership owned by managers compared to the

number of shares of the companies outstanding. The

results show that power strengthens the negative

effect of age toward leverage decisions. This result is

consistent with the study conducted by Bigley and

Wiersema (2002), who stated that power and

cognitive orientation should interact if it is related to

company strategic decision. The results are also

consistent with agency theory. The higher proportion

of ownership, managers tend to choose lower

leverage decisions. Through share ownership by

managers, the agency problem is reduced.

The main contribution of this study adds the

empirical evidence of the effect of the manager's

characteristics, namely age, toward company

leverage in the context of the company in Indonesia,

considering the small amount of the research on this

topic. Furthermore, this study also provides the

relationship model between age and company

leverage decision by including power as a moderating

variable.

2

LITERATURE REVIEW AND

HYPOTHESIS DEVELOPMENT

2.1

Age and Leverage

Young managers are often associated with new ideas

and risk acceptance than older managers who tend to

have less physical and mental stamina, more risk-

averse, and are attached to status-quo (Hambrick and

Mason, 1984). This makes young manages more

likely to pursue risky strategies such as increasing

financial leverage or carrying out unrelated

diversification.

Research by Wiersema and Bantel (1992) show

that demographic characteristics can reflect the

manager's cognitive perspectives. Using a sample of

large manufacturing companies in America, they

found that top management teams with higher

average age avoided changing strategies.

The study from Serfling (2014), showed the

results that risk-taking behavior decreases as CEOs

get older, since older CEOs invest less in research and

development, diversify acquisition, manage

companies with more diversified operations, and

Maintain lower operations leverage. Overall, the

results imply that the age of the CEO can have a

significant impact on risk-taking behavior and

company performance.

Bertrand and Schoar (2003) found that a

significant level of heterogeneity in investment,

finance, and company practices can be explained by

the permanent effects of managers. Executives from

Is Age and Power of Top Management Team Important in Leverage Decision?

425

earlier (older) birth groups on average appear to be

more conservative (prefer fewer debts). From this

explanation, the proposed hypothesis is:

H1: Age of top management team has a negative

effect on leverage.

2.2

The Effect of Power toward the

Relationship between Age on

Leverage

Power is defined as the capacity of individual actors

to use their will. The use of power in strategic making

decisions of the company has become the main

discussion (Finkelstein, 1992). However, according

to Bigley and Wiersema (2002), predictions about the

use of power by the CEO require an understanding of

the CEO's cognitive orientation towards the company

strategy, because power is the ability to realize the

desired preferences. Meanwhile, the relationships

between the cognitive orientation of the CEO and

company strategy presupposes that the CEO has

enough power to realize the desired preferences.

Therefore, the power and cognitive orientation of the

manager will interact with the company's strategic

decision.

The results of the research from Bigley and

Wiersema (2002) showed that managers would use

their power in determining choices of strategy that

depend on the cognitive orientation of the manager

(the variable used by the CEO's successor

experience). When substitute CEO experience

increases (more oriented to maintain the status quo),

managers will use less power to choose corporate

strategic refocusing. Thus, it is logical to explain that

the age of managers will interact with the power they

have in leverage decisions. Managers who have

power in the company will be more likely to realize

the desired preferences based on their cognitive

orientation. Older managers will be more likely to

choose a low average when they have power in the

company. Therefore, the proposed hypothesis of this

study is:

H2: Power strengthens the negative effect of age

of the top management toward leverage.

3

SAMPLE SELECTION,

VARIABLE CONSTRUCTION,

AND DATA DESCRIPTION

3.1

Sample Selection

Companies that become the sample of this study are

all non-financial companies listed on the Indonesia

Stock Exchange from 2010 to 2017. After removing

companies that are not always listed throughout 2010-

2017, and companies that have no complete data from

their management team, the sample has amounted to

283 companies. Thus, the number of observations for

eight years have reached 2.264 observations. The data

is obtained from the company’s annual report. Table

1 presents descriptive statistics of research variables.

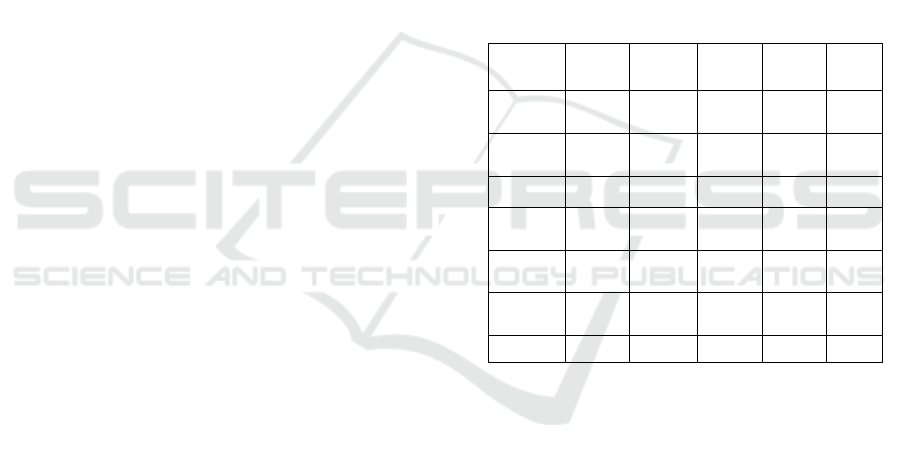

Table 1: The Summary of Descriptive Statistics of Research

Variables

Value

Type

Mean Med Max Min. Std.

Dev

Book

Lev.

0.57 0.480 16.834 0.0002 0.814

Market

Lev

0.44 0.434 0.992 0.0001 0.269

. Age 50. 51 73 31 5.5

Stock

Own

1,87 0 51 0 5,846

Profitabili

ty

0.06 0.060 2.557 -1.733 0.273

Tangibilit

y

0.31 0.273 0.962 0.0012 0.231

Size 6.34 6.340 8.470 3.705 0.775

3.2

Age of Management Team, Power,

and Leverage Measurement

Age is the age of the manager in the year. For the

calculation of age in the top management team, the

procedure used follows the method from Chen et al.

(2010), which is done by calculating the average age

of the top management team.

The calculation for leverage is done using the

method from Huang and Kisgen (2013) with the

following formula:

Book leverage = Total debt/(total debt + book value

of common equity) (1)

Market leverage = Total debt/(total debt + market

value of common equity) (2)

Power (stock own) is measured by share

ownership of the manager. The number of shares

owned by the CEO is divided by the total number of

ICBEEM 2019 - International Conference on Business, Economy, Entrepreneurship and Management

426

shares outstanding of the company (Bigley and

Wiersema, 2002).

3.3

Control Variables

The first control variable of this study is profitability.

It is calculated using the formula from Danis et al.

(2014):

Profitability = Operating Income/Total assets (3)

The second control variable of this study is

tangibility. It is calculated using the formula from

Yildirim et al. (2018):

Tangibility = Fixed Assets/Total assets (4)

The third control variable of this study is the size. It

is calculated using logarithms of the total assets

owned by the company. (5)

The formulas used to test the first hypothesis are

as follows:

Book Leverage = α0 + α1Age + α2StockOwn +

α3Profitability + α4Tangibility + α5Size + ε (6)

Market Leverage = β0 + β1Age + β2StockOwn

+ β3Profitability + β4Tangibility + β5Size + ε

(7)

It is expected that the regression coefficients of

α1, α2, and β1, β2, are significant at the specified

level of significance (1%, 5%, or 10%).

The formulas used to test the second hypothesis

are as follows:

Book Leverage = γ0 + γ1Age + γ2 StockOwn+

γ3Age*StockOwn + γ4Profitability + γ5Tangibility

+ γ6Size + ε (8)

MarketLeverage = δ0 + δ1Age + δ2StockOwn +

δ3Age*StockOwn + δ4Profitability + δ5Tangibility

+ δ6Size+ ε (9)

It is expected that the regression coefficients of

γ3, andδ3, are significant at the specified level of

significance (1%, 5%, or 10%).

4

RESEARCH RESULTS

4.1 Age of Top Management Team and

Leverage

The effect of the age of the top management team

toward leverage is tested, which is also to answer the

first hypothesis. The test is carried out using the least

square regression panel, with a fixed effect as the

chosen model. The fixed effect model is chosen after

the Chow test (to choose between the common effect

and fixed effect models), and the Hausman test (to

choose between the fixed effect and random effect

models) are conducted. The Chow test and Hausman

test results lead to the choice of the fixed-effect

model. The summary of the test results of the age of

the top management team toward leverage is shown

in Table 2.

Table 2: Summary of the Test Results of the Effect of age

on Leverage (Main Effect)

Variable

Book

leverage

Market

leverage

(1) (2)

C 4.436683*** -0.424970***

(0.0000) (0.0000)

Age -0.057126* -0.020622**

(0.0877) (0.0158)

StockOwn -0.425264*** 0.000298

(0.0000) (0.9922)

Profitability -0.398154*** -0.054049***

(0.0000) (0.0000)

Tangibility 0.292367** 0.132593***

(0.0142) (0.0000)

Size -0.541346*** 0.146647***

(0.0000) (0.0000)

R-squared 0.600263 0.762677

Adjusted R-

squared

0.542205 0.728208

Cross-sections

included

283 283

Total panel

(balanced) obs.

2.264 2.264

The effect of age toward book leverage shows the

direction of a negative relationship with a regression

coefficient of -0.001785 (model 1). Likewise, the

effect on market leverage shows the negative effect

with a coefficient of -0.002155. (model 2). These

results indicate that companies with top management

teams that mostly consist of older people are more

likely to choose lower debt compared to companies

with top management teams that consist of younger

Is Age and Power of Top Management Team Important in Leverage Decision?

427

people (Bertrand and Schoar, 2003, Serfling, 2014).

This supports previous studies.

(Yim, 2013, Jenter and Lewellen, 2015, Croci.,

Giudice, and Jankensgard, 2017) that age will have an

effect on the company policy and risk-taking in which

young managers are easier to accept risk compared to

older managers.

4.2 Is Power Strengthen the Effect of

Age on Leverage?

This study examines whether greater power (stock

own) of the top management team will increase the

negative effect of age of top management team on

leverage. This test is done to answer hypothesis 2.

The testing is done using the moderated regression

analysis. The summary of the test result is shown in

Table 3.

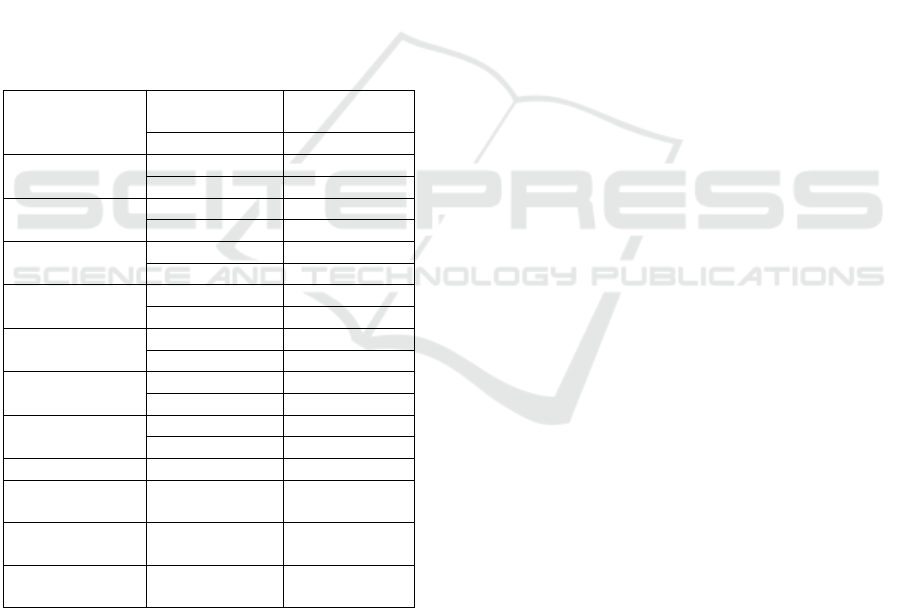

Table 3: Summary of Test Results of the Effect of Age

toward Leverage with Power (Stockown) as Moderating

Variable (Moderation Effect)

Variable

Book

leverage

Market

leverage

(1) (2)

C 4.038317*** -0.471381***

(0.0000) (0.0039)

Age 0.018535*** -0.000977

(0.0001) (0.7314)

StockOwn -0.819521** -0.269376

(0.0043) (0.2319)

Age*StockOwn -0.019725*** 0.005200

(0.0000) (0.2277)

Profitability -0.394247*** -0.054180***

(0.0000) (0.0000)

Tangibility 0.274065** 0.132381***

(0.0214) (0.0000)

Size -0.536309*** 0.147109***

(0.0000) (0.0000)

R-squared 0.601728 0.762744

Adjusted

R-squared

0.543650 0.728147

Cross-sections

included

283 283

Total panel

(balanced) obs.

2.264 2.264

The regression coefficient of the age and stock

own interaction variable (age*stockown) in Model 1

shows a number of -0.019725and significant, but it is

insignificant in Model 2 with a coefficient of

0.005200. These results indicate that the greater the

share ownership owned by the top management team,

the stronger the negative effect of age toward

leverage. The top management team, which consists

of older managers will tend to choose low leverage,

and this decision will be more likely to

be taken if the share ownership by the top

management team is getting bigger. This study is in

line with Bigley and Wiersema (2002), using CEO's

succession events for companies listed on Forbes 500

in the period 1990-1994, they found that power and

cognitive orientation of managers interacted

regarding the strategic corporate strategic refocusing

This study is in line too with research by Korkeamäki,

Liljeblom, and Pasternack (2017). Using the CEO's

data in Finland from 2002 to 2005, they were found

that CEO's personal debt preferences affect corporate

debt decisions, and power is proven to moderate the

relationship. The effect of the CEO's personal debt

toward the company’s debt is weakened by share

ownership by CEO and share ownership by the block

holder.

4.3 Subgroup Analysis

Subgroup analysis is made to explore the interaction

of power (stock own) and age (age) of the top

management team toward leverage decisions among

groups.

Because of power (stock own) moderates in

models that use book leverage, subgroup analysis is

performed just to book leverage as the dependent

variable.

Data is divided into two groups, first groups with

high leverage (high leverage) and second groups with

low leverage (low leverage). Companies are

classified as high leverage if it's average leverage

from 2010-2007 is above the median, and companies

are classified as low leverage if it's average leverage

is in the median position or below the median. The

summary of the test results is in table 4.

In the group of high leverage (model 1), age has a

significant effect (negative ) toward book leverage

with a regression coefficient of -0.003792. The

interaction coefficient of age and stock own

(age*stockown) in the high leverage group (model

2) is negative and significant (-0.010176). These

results indicate that in the high leverage group, power

(stock own) moderates the effect of age toward

leverage.

While in the group of low leverage (model 3), age

has no effect toward book leverage with a regression

coefficient of -0.000387. The interaction coefficient

of age and stock own (age*stockown) in the low

leverage group (model 4) is positive and significant

(0.022903). This result shows that the interaction of

age and stock own does not moderate the effect of age

toward leverage, because the age coefficient in model

ICBEEM 2019 - International Conference on Business, Economy, Entrepreneurship and Management

428

3 (main equation) is not significant, although the

interaction of age and stock own in model 4 is

significant (moderation equation).

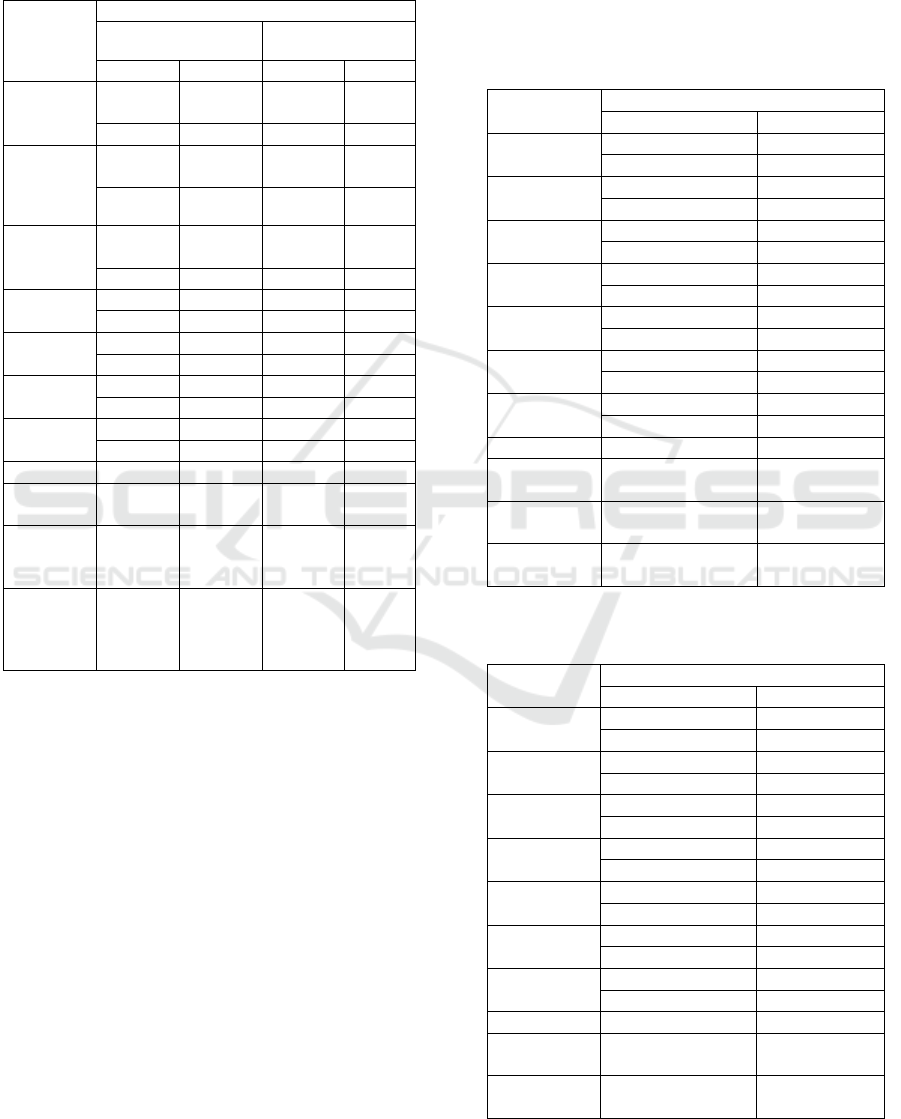

Table 4: Summary of Test Results of Subgroup Analysis

Variable

Book Leverage

High leverage firm Low leverage

fir

m

(1) (2) (3) (4)

C 3.198*** 2.632*** 4.102*** 0.891***

*

(0.000) (0.000) (0.00) (0.000)

Age -0.004** 0.002 -0.001 -

0.015***

(0.014) (0.498) (0.749) (0.000

1

)

Stock Own -0.15*** 0.742*** -0.010** -

1.271***

(0.001) (0.004) (0.004) (0.000)

Age*

StockOwn

- -0.010** - 0.023***

(0.042)

(0.000)

Profita-

bility

0.042*** 0.034*** 0.008 -0.064

(0.001) (0.008) (0.184) (0.210)

Tangi- bility -0.16*** -0.15*** -0.02*** 0.136***

(0.000) (0.000) (0.000) (0.000)

Size 0.177*** 0.185*** -0.004* 0.033***

(0.000) (0.000) (0.056) (0.066)

R-squared 0.488 0.499 0.500 0.509

Adjusted

R-squared

0.412 0.424 0.426 0.436

Cross-

sections

included

141

141

142

142

Total panel

(balanced)

obs.

1.128

1.128

1.136

1.136

From the analysis of subgroups, it can be

Concluded that the interaction of age and stock own

will moderate the effect of age toward leverage will

be more visible in the high leverage group.

Companies in the high leverage group have a higher

risk than the lower, so the role of power in

strengthening older managers choose lower leverage

to be more visible.

4.4 Robustness Tests

A robustness test is done to test the consistency of the

results of the study that have been obtained. The

testing is done by changing the leverage proxy. In the

previous stage, leverage uses a total debt proxy,

replaced by long term debt, so that the new leverage

is calculated by dividing long-term debt with long-

term debt plus equity. The summary of the results of

the robustness test is set out in table 5 and table 6.

Model 1 in Table 4 shows that age has a

significant negative effect on book leverage. The

same result is seen in model 1 in table 5; that age has

a significant negative effect on market leverage.

These findings are consistent with the research results

in the previous stage.

Table 5: Summary of the consistency of the effect of age

toward book leverage (long term debt) test

Variable Book Leverage (LongDebt)

(1) (2)

C 3.28041*** 1.591722***

(0.0000) (0.0000)

Age -0.001006* -0.006966

(0.0696) (0.2059)

StockOwn -0.059110*** -1.233927***

(0.0005) (0.0065)

Age*StockOw

n

- -0.018193**

- (0.0359)

Profitability 0.000942 -0.088928

(0.8925) (0.0025)

Tangibility -0.040962** 0.217989***

(0.0146) 0.0020

Size 0.037450*** -0.144993***

(0.0000) (0.0000)

R-squared 0.351865 0.476438

Adjusted

R-squared

0.257728 0.400091

Cross-sections

included

141 141

Total panel

(balanced) obs.

1.128 1.128

Table 6: Summary of the consistency of the effect of age on

market leverage (long-term debt) test

Variable Market Leverage (LongDebt)

(1) (2)

C -0.80069*** -0.840934***

(0.0000) (0.0000)

Age -0.026211** -0.002003

(0.0018) (0.4734)

StockOwn -0.014607 -0.379500*

(0.5623) (0.0863)

Age*StockOw

n

- 0.008129

- (0.0549)

Profitability -0.038438 -0.038250

(0.0021) (0.0021)

Tangibility 0.166571*** 0.166861***

(0.0000) (0.0000)

Size 0.178969*** 0.177271***

(0.0000) (0.0000)

R-squared 0.723033 0.723737

Adjusted

R-squared

0.682805 0.683451

Cross-sections

included

141 141

Is Age and Power of Top Management Team Important in Leverage Decision?

429

Total panel

(balanced) obs.

1.128 1.128

Model 2 in table 4 shows that the interaction

coefficient of age and stock own is significant

negative. This means that the interaction of age and

stock own strengthens the negative effect of age

toward book leverage. On model 2 in table 5, it is

known that the interaction coefficient of age and

Stockown is insignificant. This indicates that the

interaction of age and stock own does not moderate

(does not strengthen) the effect of age toward market

leverage. This result is also consistent with the

original findings. Therefore, it can be concluded that

the results of this study are robust.

5

CONCLUSIONS

This study provides evidence that the age of top

management team affects the company's leverage

decisions. The results of the study are consistent with

the Upper Echelon Theory, in which young managers

are associated with new ideas and higher risk

acceptance than older managers. Thus, young

managers are more likely to pursue a risky strategy,

such as an increase in leverage.

In addition, this study also shows that interaction

of the power of top management team with a

cognitive orientation, which is measured from the age

of manager, will affect leverage decisions. When the

age of the top management team gets older, it will

tend to choose lower leverage decisions. This will be

more likely to happen if the manager has power (stock

own) in the company.

REFERENCES

Barker, III, L, V, and Mueller, C, G, 2002. CEO

Characteristics and Firm R&D Spending, Management

Science, 48 (6), 782-801.

Berger, N, P. and Patti, B, E, 2006. Capital structure and

firm performance: A new approach to testing agency

theory and an application to the banking industry,

Journal of Banking & Finance, 30 (4), 1065-1102

Bertrand, M. and Schoar, A. 2003. Managing With Style:

The Effect Of Managers On Firm Policies, Quarterly

Journal of Economics, 118, 1169–1208.

Bigley, A, G. and, Wiersema F, M. 2002. New CEOs and

Corporate Strategic Refocusing: How Experience as

Heir Apparent Influencesthe Use of Power,

Administrative Science Quarterly, 47 (4), 707-727

Carpenter, A.M.,Geletkanycz, A.M., and Sanders, G. 2004.

Upper Echelons Research Revisited: Antecedents,

Elements, and Consequences of Top Management

Team Composition, Journal of Management, 30(6),

749–778

Chen, L.H., Hsu,T.W. and Huang, S.Y. 2010. Top

Management Team Characteristics, R&D Investment

and Capital Structure in The IT industry, Small

Business Economic, 35,319–333

Cheng, M.C. and Z.C. Tzeng, 2011. The effect of leverage

on firm value and how the firmfinancial quality

influence on this effect, World Journal of Management,

3(2), 30-53

Daily, M, C. and Johnson, L, J. 1997, Sources of CEO

Power and Firm Financial Performance: A

Longitudinal Assessment, Journal of Management, 23,

(2), 97- 117

Danis, A. Rettl, A.D. and Whited, M.T. 2014. Refinancing,

Profitability, And Capital Structure, Journal of

Financial Economics, 114 (3), 424-443

Detthamronga, U., Chancharata, N. and Vithessonthic, C.

2017. Corporate Governance, Capital Structure And

Firm Performance: Evidence from Thailand, Research

in International Business and Finance, 42, 689–709.

Farag, H. and Mallin, C. 2016. The influence of CEO

Demographic Characteristics on Corporate Risk-

Taking: Evidence from Chinese IPOs, The European

Journal of Finance, 24(16), 1528-1551

Finkelstein,S. 1992. Power In Top Management Teams:

Dimensions, Measurement, and Validation, Academy

0f Management Journal, 35 (3), 505-538.

Frank, M.Z. and Goyal, V.K. 2009. Corporate Leverage :

How Much Do Managers Really Matter?, Unpublished

Working Paper, University of Minnesota and Hong

Kong University of Science and Technology

Gharaiber 2015). Gharaibeh, A.M.,(2015). The Effect of

Capital Structure on the Financial Performance of

Listed Companies in Bahrain Bourse., Journal of

Finance and Accounting, (3),50- 60

Hambrick, C.D. 2007. Upper Echelons Theory: An Update,

Academy of Management Review, 32 (2), 334–34

Hambrick, C, D. dan Mason, A, P. 1984. Upper Echelons:

The Organization as a Reflection of Its Top Managers,

Academy of Management Review,. 9(2), 193-206.

Huang, J. and Kisgen, J.D. 2013. Gender and Corporate

Finance: Are Male Executives Overconfident Relative

to Female Executives? Journal of Financial Economics,

108 (3), 822-839

Jenter, D. and Lewellen, K. 2015. CEO Preferences and

Acquisitions, The Journal of Finance,70 (6), 2813-

2852.

Korkeamäki, T, Liljeblom, E, and Pasternack, D. 2017,

CEO power and matching leverage preferences, Journal

of Corporate Finance, 45, 19-30

Rivas , J, L. 2012. Diversity & internationalization: The

case of boards and TMT’s, International Business

Review, 21, 1–12

Serfling, M.A. 2014. Ceo Age and The Riskiness of

Corporate Policies. Journal of Corporate Finance , 25,

251-273

Tarraf, H. 2011. The Role of Corporate Governance in the

Events Leading Up to The Global Financial Crisis:

ICBEEM 2019 - International Conference on Business, Economy, Entrepreneurship and Management

430

Analysis of Aggressive Risk-Taking, Global Journal of

Business Research, 5, 93-105

Yildirim, R., Masih,M. and Bacha, I.O. 2018. Determinants

of Capital Structure: Evidence from Shari'ah Compliant

and Non-Compliant Firms, Pacific-Basin Finance

Journal, 51, 198-219

Yim, S. 2013. The Acquisitiveness of Youth: CEO Age and

Acquisition Behavior, Journal of Financial Economics,

108 (1), 250–273

Wiersema, F, M, and Bantel, A, K. 1992, Top Management

Team Demography And Corporate Strategic Change ,

Academy Of Management Journal, 35, (1), 91-121.

Is Age and Power of Top Management Team Important in Leverage Decision?

431