Effect of Demographic Factors and Financial Training towards the

Level of Financial Literation of Crafts and Furniture SMEs in

Sleman District

R. Hendri Gusaptono, C. Ambar Pudjiharjanto, Yuninur Fadzilah

Universitas Pembangunan Nasional Veteran Yogyakarta,

Keywords: Financial Literacy, Demographics, SMEs

Abstract: The low level of financial literacy SMEs are one of the causes of the lack of access to financial institutions in

this sector. The SMEs tend to lack understanding of financial products offered by other financial institutions

so that they are only able to depend on conventional banking financing. This is the background of the research.

To analyze the data using descriptive statistics and multiple regression. Based on the results of data analysis,

it was concluded that the average level of financial literacy of crafts and furniture business owners in the

Sleman sub-district has a fairly high level of financial literacy. The level of literacy is significantly influenced

by demographic factors and financial training, both together (simultaneously) and each variable. The lowest

value of financial literacy is in financial planning.

1 BACKGROUND PROBLEM

Indonesia is a country that has the 4th largest

population in the world, with a total population of

more than 265 million people, ranked one below the

superpower, namely the United States, which has a

population of more than 362 million inhabitants.

Although the population of Indonesia always

increases every year, according to data from the

Central Statistics Agency in March 2018, the poverty

rate has decreased to 9.82%. This figure is certainly

an extraordinary achievement, considering that since

1999, the percentage of Indonesian poverty has

always consisted of 2 digit numbers. The success of

reducing the percentage of poverty is inseparable

from the role of Small and Medium Enterprises

(SMEs), according to Katadata.co.id in 2016 the

SMEs sector has been able to dominate 99.9% of

business units in Indonesia and able to absorb almost

97% of the Indonesian workforce. From this figure,

the types of micro-businesses absorb the most

workforce by 87%, medium businesses by 4%, small

businesses by 5.7%, while large businesses can only

absorb 3.3%.

According to a survey conducted by the Ministry

of Cooperatives proving that the competitiveness of

SMEs in Indonesia is quite good, a survey conducted

by the Financial Services Authority (OJK) in 2016

showed that the financial literacy rate in Indonesia

was 29.6%, and financial literacy for SMEs actors by

27.7%. This figure is an increase compared to the

results of the 2013 FSA survey, which was still

21.8%. However, this figure is relatively small when

compared to the level of financial literacy in other

Southeast Asian countries.

The OJK survey in 2016 divides the level of

national financial literacy into conventional, sharia,

and mixed (composite) categories. The conventional

financial literacy rate is 29.5%, sharia 8.1%, and

composite 29.7%. The people with the highest

average financial literacy level were DKI Jakarta at

40%, and the lowest in West Papua at 19.27%, while

DI Yogyakarta was ranked 3rd with a large

percentage of 38.55%.

The Governor of Bank Indonesia (BI) Agus DW

Martowardjojo revealed, the problems in running

Micro, Small and Medium Enterprises (SMEs) are

not limited to financial management and limited

resources management, but also access to capital

owned by business actors. The low level of financial

literacy of SMEs is one of the causes of the lack of

access to financial institutions in the sector. The

SMEs tend to lack understanding of financial

products offered by other financial institutions so that

they are only able to depend on manual and

conventional banking financing, until 2016 the

Gusaptono, R., Pudjiharjanto, C. and Fadzilah, Y.

Effect of Demographic Factors and Financial Training towards the Level of Financial Literation of Crafts and Furniture SMEs in Sleman District.

DOI: 10.5220/0009960006310638

In Proceedings of the International Conference of Business, Economy, Entrepreneurship and Management (ICBEEM 2019), pages 631-638

ISBN: 978-989-758-471-8

Copyright

c

2020 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

631

number of adults who have bank accounts only

reaches 36%.

According to Abdulloh Mubarok and M.

Faqihudin (2011), in general, SMEs ' problems can be

classified into external problems and internal

problems. Internal problems include the quality of

human resources, capital, financial administration, or

accounting, while external problems include the

business climate, market access and facilities, and

infrastructure.

In general, the activities of SMEs only emphasize

the production and marketing fields, while the

financial reporting activities are ignored. The

activities of preparing financial statements, are still

considered luxurious and not yet comparable to their

uses. As a result, the SMEs do not know exactly how

much income should be received, how much

operating costs should be incurred, and how much

should be left, which they know is only the current

financial condition.

Yogyakarta Special Region is one of the

provinces with the highest level of financial literacy

number 3 in Indonesia, according to the results of a

survey conducted by the OJK in 2016. However,

according to the Head of the UMKM Office and the

Yogyakarta Special Region Cooperative, Tri

Saktiyana said that based on field observations,

almost 98% of SMEs do not understand how to

organize financial statements properly. Therefore, the

SMEs cannot calculate profits accurately, so that the

development of the business scale is hampered. Also,

according to Tri Saktiyana, the absence of a neat

checking account makes them unable to access the

People's Business Credit (KUR). The SMEs who

have been able to access KUR is only around 10%,

while the rest are still in the form of startup funded by

cooperatives and own capital.

According to the Head of the UMKM Division of

the Yogyakarta UMKM and Cooperative Office,

Agus Mulyono, there are still around 238,000 SMEs

in Yogyakarta. Of this amount, 60% of them are

micro-businesses, and around 30% are small

businesses, the remaining 10% are medium

businesses. Agus Mulyono said that the difficulty of

SMEs entrepreneurs to access the capital was because

the SMEs did not make business plans when starting

a business, because the majority of them only

followed trends the existing.

In general, according to the Yogyakarta Central

Statistics Agency (BPS), the business climate in

Yogyakarta is somewhat conducive, as evidenced by

an increase in production growth of large and medium

manufacturing industries (IBS) in the fourth quarter

of 2016 increased by 12.8% compared to the same

period in 2015. The increase in Yogyakarta's IBS

growth index in 2016 was boosted by positive growth

in almost all types of industries. Among them the

food industry, apparel, rubber, rubber and plastic

goods, machinery industry, and equipment and crafts

and furniture.

Many variables affect someone's financial

literacy, including demographic factors and financial

knowledge. Previous research conducted by Chen and

Volpe (1998) states that men have higher financial

literacy than women. It is supported by research

conducted by Jeyaram and Mustapha (2015) that men

have better levels of financial literacy than women.

Apart from gender, education, age of manager,

and length of business are also aspects that affect a

person's level of financial literacy. Also supported by

the results of a study conducted by Bonita and

Setiawina Nyoman Djinar (2017) that simultaneously

variables of education level, length of business, and

gender significantly influence the level of financial

literacy. But according to the results of a study by

Cynthia Nur Fitriana Ichwan (2016) found that

education affects financial literacy while

demographics and length of business do not affect

financial literacy. This was also supported by the

results of a study conducted by Mukhtar et al. (2017)

that found that the level of education, age, and length

of business did not affect financial literacy, but

training influenced financial literacy. Yogyakarta

Special Region Province is included in the top 3

provinces with a high level of financial literacy of its

citizens in Indonesia, especially SMEs in Yogyakarta

itself from year to year, always experiencing an

increase. One of the regencies that has the highest

number of SMEs in Sleman Regency, with the most

distribution being in Sleman District. To be a known

level of financial literacy of SME crafts and furniture

that is in the district of Sleman, the researchers were

motivated to research.

2 LITERATURE REVIEW

2.1 Understanding Financial Literacy

Education Development Center (ECD) states that

literacy is the ability of individuals to use all the

potential and skills possessed in their lives, not just

the ability to read or write alone. According to the

National Institute for Literacy, defining literacy is the

ability of individuals to read, write, speak, count, and

solve problems at the level of expertise needed in

work, family, and society.

ICBEEM 2019 - International Conference on Business, Economy, Entrepreneurship and Management

632

Ridwan and Inge (2003) state that finance is the

science and art of managing money that affects the

lives of everyone and every organization. Finance

deals with the processes, institutions, markets, and

instruments involved in the transfer of money

between individuals as well as between business and

government.

To clarify the notion of Financial Liters, the

OECD (2012) states that financial literacy is a

combination of the awareness, knowledge, skills,

attitudes, and behaviors needed to make sound

financial decisions and ultimately achieve individual

financial well-being. According to the Australian

Government (ASIC, 2014), Financial literacy is about

understanding money and finance and being able to

apply that knowledge to make effective decisions

confidently. Financial Literacy is one's understanding

of financial concepts and choices in the context of

their economic situation, combined with their

behavior and judgment to apply knowledge to achieve

the desired level of financial welfare, which is another

understanding of financial literacy according to

Australian Unity.

Mendari and Kewal (2014), financial literacy is a

basic need for everyone to avoid financial problems.

According to the Financial Services Authority, the

financial literacy is defined as a series of processes or

activities to improve knowledge(knowledge),

confidence(competence), skills(skills)of consumers

and the public at large so that they can manage their

finances better (Financial Services Authority, 2014).

So that the conclusion of financial literacy is the

knowledge and understanding of financial science,

ways to plan, manage, and invest the money owned

both for individuals, communities, or businesses that

they manage to reduce the risks in finance.

2.2 Financial Literacy Aspects

Chen and Volpe (1998; Dancing and Kewal, 2014)

states that financial literacy is divided into 4 (four)

aspects, namely:

a. General Personal Finance Knowledge,

including understanding several matters

relating to basic knowledge about personal

finance.

b. Saving and borrowing, this section covers

knowledge relating to savings and loans, such

as the use of credit cards.

c. Insurance, this section covers basic knowledge

of insurance and insurance products such as life

insurance and motor vehicle insurance.

d. Investment, this section covers knowledge of

market interest rates, mutual funds, and

investment risks.

Based on the Functional Financial Literacy Model

(Heenkenda, 2014), there are five domains of

financial literacy, that is

a. Saving behavior, which contains Banking

practice, parents' influence, and saving habits

b. Investment and payment mechanism, which

contain People's attitudes towards better

financial practices, Money investment

behavior, Principal financial decision-maker of

the household, and Households’ payment

mechanisms,

c. Awareness on financial which contain

Knowledge about financial products and

services and usage, Factors affecting for

selecting a financial institute, and Methods of

obtaining information about financial services

d. Risk Management which contains Borrowings

in an emergency, and Retirement plan and

insurance

e. Financial Knowledge Which contains

Knowledge of financial planning, Preferred

financial objective, Recordkeeping behavior,

and Knowledge interest rates and concept of

inflation

2.3 Factors Affecting Financial

Literacy

According to the Financial Services Authority (2014),

factors that affect the level of financial literacy,

namely:

a. Gender

b. Level of education

c. Level income.

According to Cynthia (2016), demographic

factors that can affect a person's level of literacy are

Gender, Educational History, Age Old Age

Enterprises.

According to Neha and Shveta (2018), factors that

can influence the level of financial literacy from

demographics and socio-economics are Age, Gender,

Family background.

2.4 Demographic Factors

This study uses demographic factors as one of the

research variables. The demographic factors used are

Gender, Education History, Age, and Length of

business operation.

Effect of Demographic Factors and Financial Training towards the Level of Financial Literation of Crafts and Furniture SMEs in Sleman

District

633

2.4.1 Gender

Sex (sex) is the difference between women and men

biologically since someone was born (Hungu, 2007).

Women and men have special conditions that are

different, both in terms of physical-biological and

psychological terms. The difference is the source of

the different functions and roles carried by women

and men. If you pay attention to the different roles and

functions carried by women and men, it will be seen

that the movements or trips made by women have

different patterns from the movements or trips made

by men (Amaliyah and Witiastuti, 2015).

Margaretha and Pambudhi (2015) state that

gender influences financial literacy. Nababan and

Sadalia (2012) state that men tend to have higher

personal financial literacy than women. Men do not

consider many variables related to investment

decisions, because the character of men, is inversely

proportional to women that is very independent, not

too emotional, very logical, easy to make decisions,

very confident, and do not need a sense of security.

Women tend to be more careful in making financial

decisions.

2.4.2 Age

According to the RI Department of Health, age or age

is a unit of time that measures the time of the

existence of an object or creature, both living and

dead. In the US, for example, people in the prime age

group (25-65 years) tend to do about five percent

better to understand the question than those who are

under 25 years or over 65 years. Lusardi and Mitchell

(2011) hypothesize that individuals tend to

accumulate knowledge over time, which then decays

as they age.

2.4.3 Level of Education

The level of education is the highest level of formal

education ever undertaken by respondents (not

including courses). The level of education possessed

by a person is thought to affect the income received

at work, and education provides knowledge not only

in the implementation of work but also the foundation

to develop themselves in utilizing the facilities and

infrastructure that are available for the sake of smooth

work (Artianto 2010).

According to Fernando (2016), that education

level is the most important thing in one's life, with the

education of someone who is of productive age can

compete in the job market. The higher the education,

the more knowledge, understanding, and broad

insights that increase income.

According to Law No. 20 of 2003 concerning the

National Education System, the measurement of the

level of formal education is classified into 4 (four),

namely:

1) Level of higher education, which is a minimum

of never having taken a tertiary level.

2) Higher education level, namely high school

education or equivalent

3) . Medium education level, namely junior high

school education or equivalent

4) Level low education, namely elementary

school education or equivalent

2.4.3 Long Operating Operations.

According to Patty and Rita (2010), stated that the

length of the business is the period the entrepreneur is

in carrying out his business or the period of work of

someone in pursuing a field of work. According to

Priyandika (2015), the length of a business is the

length of a business or business actor doing his

business. Besides, Priyandika (2015) also said that the

length of a business could lead to an experience of

doing business, where experience can affect one's

observations in behavior. The length of time the

business will affect its productivity (professional

ability or expertise) so that it will increase efficiency

and be able to reduce production costs smaller than

the sales.

2.5 Financial Training

According to Mukhtar, Ira, and Darman (2014) state

that financial training is very useful for the level of

financial literacy of women entrepreneurs in the

creative gloves industry donggala. According to

Pangabean (2004), training can be defined as a means

used to provide or improve the skills needed to carry

out current work. Whereas education places more

emphasis on increasing one's ability to understand

and interpret knowledge.

An important attribute of successful micro-

entrepreneurs is their ability to save and reinvest their

results to expand their business. One of the financial

constraints experienced by SMEs is the lack of

available trained personnel (Catal, 2007) and

information gaps (Saulles, 2006). Financial training

affects the level of financial literacy among SMEs,

which makes them more vulnerable to financial crises

compared to large companies in the economy.

According to the 2009 European Commission

Report and the OECD Report 2002, ongoing training

and continuous learning are considered important

elements of competitiveness and strategic

ICBEEM 2019 - International Conference on Business, Economy, Entrepreneurship and Management

634

management. On the other hand, Nunoo and Andoh

(2012) show that better financial literacy can provide

benefits for SMEs such as 1) Increased demand for

financial services, 2) More efficient, 3) Better risk

management, 4) Reduction in volatility economics, 5)

Increased intermediation and 6) Accelerating

financial development. This situation will cause

increased competition in the financial markets and a

more balanced distribution of capital for the people.

3 RESEARCH HYPOTHESIS

The hypothesis formulated in this study is based on

the formulation of the problem; the hypothesis is:

:

Demographic factors and financial training

simultaneously affect the level of literacy.

: The length of time the business operates affects

the level of financial literacy

: The size of SMEs managers affects the level of

financial literacy

:

Age of managers of SMEs affects the level of

financial literacy

: The education level of SMEs managers

influences the level of financial literacy

: Financial training affects the level of financial

literacy

4 RESEARCH METHODS

4.1 Research Design

This research is a type of quantitative research, which

will describe the

results of statistical tests on the

factors that affect the level of financial literacy of

handicraft and furniture business SMEs in Sleman,

Yogyakarta. The research method used in this study

is a survey method. This research was carried out in

the Sleman sub-district, Sleman regency, Yogyakarta.

The location of this research was chosen purposively

with the consideration that Sleman is one of the

districts that have a relatively fast-growing level of

SMEs development. According to the Australian

Unity Financial Wellbeing Questionnaire - design

and validation (25th July 2014), financial literacy can

be measured using 5 (five) indicators, namely.

Gender is one of the qualitative variables, therefore to

be a quantitative variable, gender is formed into a

dummy variable with (0) if it is male, and (1) if it is

female. Age was classified into five classes as

follows: (1) 20-29 years (2) 30-39 years, (3) 40-49

years, (4) 50-59 years, and (5)> 60 years. The

business duration Divided into five classes, namely

(1) <3 years, (2) 3-5 years, (3) 6-8 years, (4) 9-11

years, and (5)> 12 years. Manager's Education Level

1) No School, 2) Elementary School, 3) Middle

School, 4) High School, and 5) Higher Education.

Financial training is formed into a dummy variable

with (1) if you have received financial training, and

(0) if you have never received financial training.

To evaluate effect demographic Factors and

training business financially on financial literacy, a

series of OLS regressions were run, and our

specification is:

Υ = α + β_1 X_1 + β_2 X_2 + β_3 X_3 + β_4 X_4

+ β_5 X_5 + e (1)

Where Υ is financial Literacy, X_1: length of effort,

X_2: gender, X_3: manager's age, X_4: education

level X_5: financial training,

5 RESULT

5.1 Financial Literacy

The results of measurement of the average level value

financial literacy of the management of SMEs Crafts

and Furniture in Sleman District who were

respondents in this study amounted to 90.89 with a

standard deviation of 11,374, which means the

deviation from the average value is quite small (little

data variation). An average value of 90.27 indicates

that the financial literacy level of SME managers is

already high.

5.2 Regression Analysis

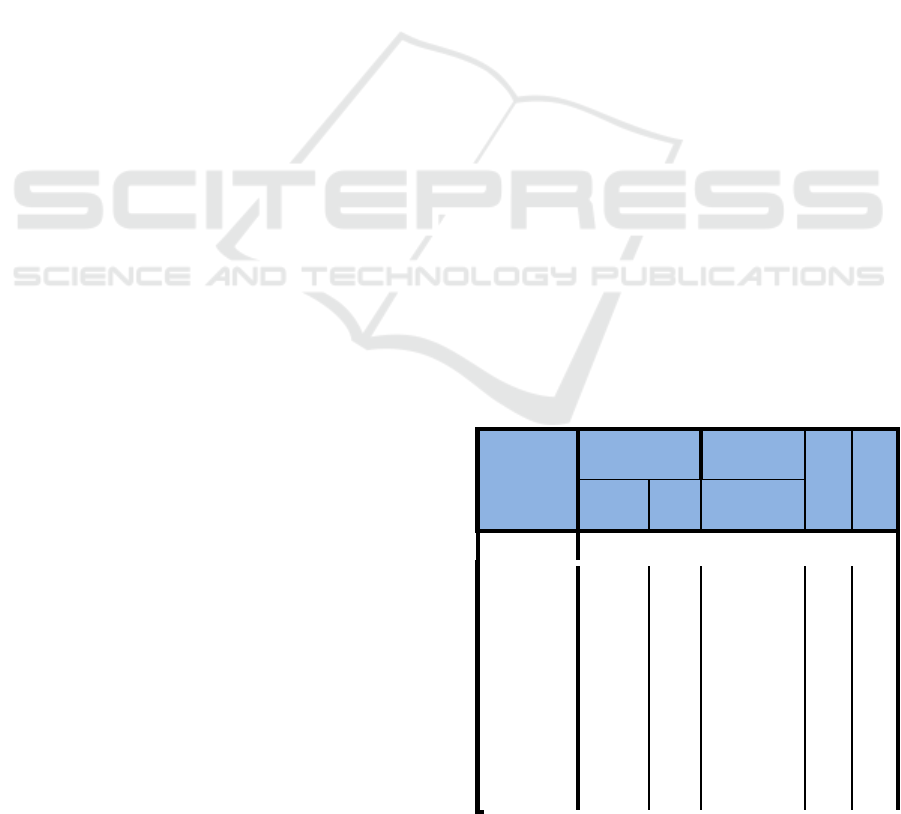

Table 1. Regression analysis

Model

Unstandardized

Coefficients

Standardized

Coefficients

t Sig.B

Std.

Error Beta

(Constant) 49.500 5.543 8.930 .000

Long

Operating

Operations

.209.032 1,086

2,014 2,187

The sex of

SMEs

managers

.194.043 3,003

2,207 6,626

Age of

managers

of SMEs

.222.049 1,274

2,079 2,649

Effect of Demographic Factors and Financial Training towards the Level of Financial Literation of Crafts and Furniture SMEs in Sleman

District

635

The

education

level of

SMEs

managers

.491.000 1,007

5,344 5,753

Financial

training

5,178 2,309 .218 2,242 029

Table 1 shows the results of testing the hypotheses

of the factors that influence the level of financial

literacy among craft and furniture SMEs in the

Sleman district.

The second hypothesis, which states that the

length of time the business operates affects financial

literacy, is accepted. The third hypothesis, which

states that gender variables influence financial

literacy, is accepted. The fourth hypothesis, which

states that the age of the manager, influences financial

literacy, is accepted. The fifth hypothesis, which

states that the manager's education level affects

financial literacy, is accepted. The sixth hypothesis,

which states that financial training affects financial

literacy, is accepted.

6 DISCUSSION

The test results show that gender, age of manager,

length of business of operation, level of education of

managers (demographic factors) and financial

training affect the level of financial literacy among

SMEs managers, the probability value of the

simultaneous influence obtained from the regression

with the help of SPSS is over 0,000 less than 0.05, so

the first hypothesis is accepted. This study is in line

with the results of research conducted by Bonita and

Setiawina (2016), which states that demographic

factors (sex, length of business, and level of

education) simultaneously influence the level of

financial literacy of traders in traditional markets in

the city of Denpasar.

The test results show that the length of time the

business operates affects the level of financial literacy

among SME owners or managers, so the second

hypothesis is accepted. Vijayanti and Yasa (2016)

revealed that business duration has a direct influence

on the efficiency of a business.

Based on the results of descriptive statistical tests

that have been carried out on SMEs based on the

length of their business in operation, the results show

that the longer the business is established and

managed, the higher the financial literacy level of the

SME owner. The time owned by a business actor in

running his business affects the maturity in making

decisions, the longer the business operates, the more

experience and lessons have by the business actor. So

that the longer the business is established and

operating, the higher the level of financial literacy

that is owned by SME entrepreneurs.

The test results show that gender affects the level

of financial literacy among SME owners or managers,

so the third hypothesis is accepted. In this study, it

was found that women have higher financial literacy

than men. The results of this study are consistent with

the results of research by Margaretha and Pambudhi

(2015), which shows that gender influences student

financial literacy. Krishna's discovery, et al. (2010)

stated that female students have higher financial

literacy compared to male students. Based on the

results of descriptive statistical testing of

demographic factors on the level of financial literacy

shows that women have a higher level of financial

literacy. Men do not consider many variables related

to investment decisions, while women tend to be

more careful in making financial decisions (Christanti

and Mahastanti, 2011). These different characteristics

cause differences in the level of financial literacy in

women and men.

The more cautious nature of women in making

decisions about investing causes women to learn

many things about financial concepts to make the

right decisions. This condition causes the level of

knowledge of women is higher than men, with a high

level of knowledge; the level of their understanding

will be deeper. Therefore female respondents will try

to learn many financial concepts so that their financial

literacy levels tend to be high.

The test results show that the age of the manager

affects the level of financial literacy among SME

owners or managers, so the fourth hypothesis is

accepted. According to Lisa and Bilal (2012), based

on World Bank, survey results found that financial

literacy tends to peak among adults in the middle of

the life cycle, and is usually lowest among young

people and parents.

The test results show that the level of education

affects the level of financial literacy among SMEs

owners or managers, so the fifth hypothesis is

accepted, this study supports the results of research

conducted by Bonita and Setiawina (2016) which also

found that the level of education will positively

influence the level of financial literacy traditional

market traders in the city of Denpasar. According to

Fernando (2016), that education level is the most

important thing in one's life, with the education of

someone who is of productive age can compete in the

ICBEEM 2019 - International Conference on Business, Economy, Entrepreneurship and Management

636

job market. The higher the education, the more

knowledge, understanding, and broad insights that

increase income.

This statement is supported by the results of

descriptive statistical tests that have been carried out

on SME actors based on the level of education of

SME actors who have differences at each level of

education. SMEs who have been educated through

junior high, high school and university are able to

understand the statements meant by researchers when

conducting interview sessions to fill out the

questionnaire, so that it can make a picture that the

higher the educational level of SMEs, the higher the

knowledge and ability to understand every statement

or question raised to them.

The test results show that financial training affects

the level of financial literacy among SMEs owners or

managers so that the sixth hypothesis is accepted, this

study supports the results of research conducted by

Bayrakdaroğlu and Fırat Botan San (2014) which

found that the level of financial literacy from

managers increased with training finance.

According to the study of Drexler et al. (2010),

financial training based on standards and

fundamentals, using simpler training and practical

rules, can produce economically meaningful

improvements in SMEs. In other words, training

SMEs, according to their basic financial needs, is the

most appropriate and efficient way for the economic

development and growth of these companies.

This statement is supported by the results of

descriptive statistical tests that have been carried out

on SMEs based on financial training experience.

SMEs who have attended financial training can

respond smoothly and quickly to the statements

referred to by researchers when conducting interview

sessions to fill out questionnaires, while SMEs

practitioners who have never attended financial

training tend to experience a lot of confusion still

when answering. Financial training that is also

supported by education from SMEs actors can make

the SME's understanding of finance or business

management financially increased.

7 CONCLUSION

Based on the results of data analysis conducted in this

study, it was concluded that the average level of

financial literacy of handicraft and furniture business

owners in the Sleman sub-district has a fairly high

level of financial literacy. The level of literacy is

significantly influenced by demographic factors and

financial training, both together (simultaneously) and

each variable. The financial literacy variable in this

study uses five indicators, of the five indicators,

financial planning, which has the lowest average

value is 3.72. The low value held by financial

planning indicators is because there are still many

SMEs that have not yet made financial statement

records, also exacerbated by the absence of separation

between private money and venture capital so that

many SMEs have complained about running out of

venture capital and the difficulty of developing their

businesses. The allocation of most of the profits

received into inventory without any planning and

calculation of inventory turnover, making many

inventory items unemployed, causing maintenance

costs, and stagnating business operating capital.

8 SUGGESTION

Based on the results of research and data analysis that

has been done, the suggestions that can be given are

as follows:

1. For Further Researchers

Based on the value of the adjusted R square is 0.622

or 62.2%. This means that 62.2% of financial literacy

variables can be explained by five independents

(independent) variables. The difference of 37.8% is

explained by other variables outside this research

model. Therefore, further researchers are expected to

research with more variable variables. Ensuring the

number of SMEs that are still operating is a must

before researching so that researchers can search for

data more effectively and efficiently.

2. For the Local Government

Based on the results of a survey that has been done, it

shows that there are still many business actors who

have not participated in financial training conducted

by the Sleman district government.

One indicator of financial literacy that still has little

value is financial planning. Therefore the government

must add material related to financial planning in the

training that is held such as investment planning, risk

or insurance, personal tax planning, old age planning,

and inheritance planning.

3. For SMEs

The number of SMEs actors who make records of

financial statements and financial planning is still

very small, so the initial step that must be taken is to

inventory the types of income and routine expenses.

Effect of Demographic Factors and Financial Training towards the Level of Financial Literation of Crafts and Furniture SMEs in Sleman

District

637

In this way, businesses can learn patterns of income

and expenses as well as savings.

So by making a record of business finances and

separating between personal money and business

operating capital, it will accelerate the development

of the business being run.

REFERENCES

Anggraeni, Birawani Dwi. (2015). Effect of Financial

Literacy Level of Business Owners on Financial

Management. Case Study: Umkm Depok. Journals

Indonesian Vocational Volume 3. Number 1. January –

June 2015

ANZ, 2011. Adult financial literacy in Australia: Full report

of the results from the 2011 ANZ survey, SL: ANZ.

Australian Government, 2014. National Financial Literacy

Strategy.

Chen, Haiyang & Volpe, Ronald P. (1998). An Analysis of

Personal Financial Literacy Among College Students.

Financial Services Review, 7 (2): 107-128

Sleman Regency SME Data 2017

https://dinkopukm.slemankab.go.id/data-statistik/data-

ukm/(accessed October 14, 2018)

Fatoki, Olawale. 2014. The Financial Literacy of Micro-

Entrepreneurs in South Africa. Journal of Business and

Management, 40 (2), pp: 151-158.

Hungu 2007. Indonesian Health Demographics. Jakarta:

Grasindo Publisher.

Ichwan, Cynthia Nur Fitriana. (2016). Financial Literacy

Study of Small and Medium Enterprises Managers in

the Gerbangkertasusila Region. Bachelor Thesis,

Accessed January 23, 2017, from PERBANAS

Institutional Repository

Jeyaram, Sangita A / P and Mazlina Binti Mustapha. 2015.

Financial Literacy and Demographic Factors. Journal of

Technology Management and Business.

Lusardi, Annamaria. 2013. Financial Literacy Around the

World (FLAT World). Insights: Financial Capability-

April 2013.

Lusardi, A and Mitchell, OS 2008. Planning and Financial

Literacy: How Do Women Fare. Journal of the

American Economic Association, 98 (2), pp: 413-417.

Heenkenda, S. (2014). Inequalities in the Financial

Inclusion in Sri Lanka: An assessment of the Functional

Financial Literacy. Discussion Paper No.194, Graduate

School of International Development, Nagoya Japan,

01-37.

Mandell, L., & Klein, LS. 2009. The Impact of Financial

Literacy Education on Subsequent Financial Behavior.

Journal of Financial Counseling and Planning, Volume

20, No. 1.

Maulani, septi. 2016. Analysis of Factors Affecting

Financial Literacy (Study of Management Department

Students in the Faculty of Economics, Semarang State

University Active Even Semester Year (2015/2016).

Semarang: Faculty of Economics, State University of

Semarang.

Mubarok Abdulloh and Faqihudin, 2011, "Financial

Managers for Small and Medium Enterprises ".

Tangerang: Suluh Media

Mukhtar Tallesang, Ira Nuriyasanti1, and Darman 2018,

Analysis of Finacial Literation of Entrepreneurs in the

Sarung Industry Weaving in Central Sulawesi,

Proceedings of the Seminar on Research Results

(SNP2M) 2018 (pp.353-35), 978-602-60766-4-9

Nababan, Darman and Isfenti Sedalia. 2012. Personal

Financial Literacy Analysis and Financial Behavior for

Undergraduate Students of the Faculty of Economics,

North Sumatra University. Medan: Faculty of

Economics and Business, University of North Sumatra.

Salim A. Abbas, 2000. "Insurance and Risk Management."

Jakarta: PT Raja Grafindo Persada

Sawir Agnes, 2001. "Financial Performance Analysis and

Corporate Financial Planning". Jakarta: PT Gramedia

Pustaka Utama

Sugiyono. 2013. "Business Research Methods (Qualitative

Quantitative Approach and R&D ) ". Bandung:

Alfabeta

ICBEEM 2019 - International Conference on Business, Economy, Entrepreneurship and Management

638