Analysis of Assessment Cycle of Migration Data from OROS to SAP

Hana using Activity based Costing Method in Telecommunication

Industry

Vindha Novriani Tanjung

1

, Muhardi Saputra

1

and Warih Puspitasari

1

1

Information System, Telkom University, Bandung, Indonesia

Keywords:

ERP, SAP S/4 Hana, SAP Controlling, Activity-Based Costing, Assessment Cycle, SAP Activate.

Abstract:

Indonesia had one of the biggest company in the telecommunication sector, it was PT ABC. The company

certainly requires accurate and fast data for all divisions, especially the financial division. PT ABC wants

everything to be integrated and automated. Therefore, the SAP application was used to integrate data in the

company and also the OROS application to calculate profitability analysis. PT ABC only uses the OROS

application to calculate profitability analysis, while the data to calculate it was in SAP. The OROS application

had also begun to be abandoned because one of its weaknesses was that OROS was not real-time application

and was not integrated directly into SAP, so it was considered ineffective and inefficient for the company.

Overcoming the problem above, the researchers will analyze the assessment cycle data in OROS to be migrated

to SAP HANA using the method of costing Activity-Based Costing to match the data cycle in OROS and SAP

HANA, so that it can be used to generate reports to the Profitability Analysis (CO- PA).

1 INTRODUCTION

Enterprise Resources Planning (ERP) is a software

used by an organization or company to manage

daily activities in business, for example, accounting,

project management, procurement, risk management

and compliance, and some supply chain operations.

ERP systems can be integrated with many business

processes and allow data flow between them (Oracle,

2019). SAP is a corporate application software can

be used to manage ERP to help organizations inte-

grate business data and corporate partners. SAP offers

a business platform basic data (Savchuk and Kirsta,

2019). SAP HANA is cloudbased software that be

the first provider application offered by SAP (King,

2014). PT. ABC is one of the largest telecommunica-

tions companies in Indonesia, which is currently go-

ing live SAP HANA and still using OROS application

to calculate data for profitability analysis only.

OROS Modeler itself has started to not be used

for companies, besides OROS Modeler is an applica-

tion that is not real-time, OROS Modeler applications

are also less user-friendly. OROS has also changed

its name to SAS CPM (Greiner, 2019). The era that

has been completely advanced, encourages PT ABC

to immediately go live SAP HANA and leave OROS

Modeler. SAP HANA can create several business data

platforms that will later be run on a cloud base directly

and in a modern way to scale costs more effectively.

(SAP, 2019). The benefits of using SAP HANA, it

will help us manage data in one platform in memory,

so we can take the action. It’s also speed up the pace

of innovation and run directly in this new digital econ-

omy(SAP, 2019).

Migrating data from OROS to SAP HANA re-

quires a lot of preparation. We must first understand

the concepts of OROS and SAP HANA. We need to

map components and data from OROS that are needed

later in migrating data to SAP HANA. Using Activity-

Based Costing in SAP HANA can help the entire pro-

cess of migrating OROS data to SAP HANA because

the OROS application also applies an activity-based

costing method. Even so, it still needs to be adjusted

in SAP HANA, whether all data in the OROS appli-

cation are suitable and can be used or not.

An assessment cycle is needed in this analysis as

the allocation of company allocation. This assessment

cycle is a challenge for researchers to match whether

the allocation data from OROS with those in SAP

HANA are correct or not. The researcher will also

create an architecture for the assessment cycle as pos-

sibilities for data flow that will appear when mapping

OROS data flow.

Tanjung, V., Saputra, M. and Puspitasari, W.

Analysis of Assessment Cycle of Migration Data from OROS to SAP Hana using Activity based Costing Method in Telecommunication Industry.

DOI: 10.5220/0009908702530260

In Proceedings of the International Conferences on Information System and Technology (CONRIST 2019), pages 253-260

ISBN: 978-989-758-453-4

Copyright

c

2020 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

253

2 LITERATURE REVIEW

2.1 OROS

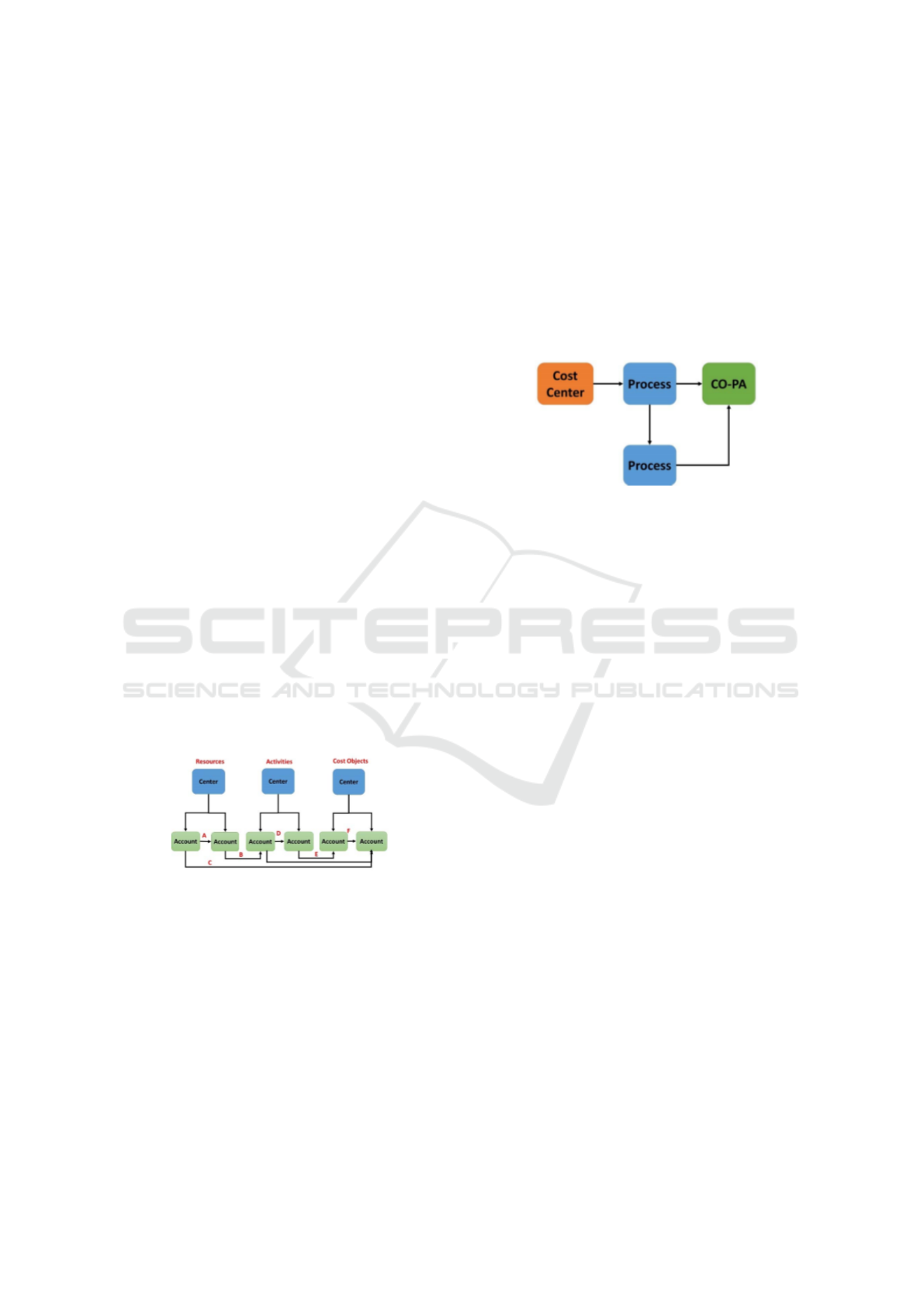

The basis of the Oros model is its three modules,

there are Resources, Activities and Cost Objects. The

Resource Module contains company resources. Re-

sources are released as a result of the activities carried

out. The activities carried out are contained in the Ac-

tivity Module. Products, services, customers, and so

on, are built into the Cost Object Module to determine

the dimensions used for profitability analysis. (SAP,

2001)

Each module consists of a hierarchy that is de-

termined by the logistics center, accounts, and cost

grouping elements. The center contains the center and

other accounts. Account contains cost elements. The

center not only helps to determine the hierarchical re-

lationship between objects in the module, but also al-

lows the cost to roll-up. Scrolling creates a collection

of costs. Accounts are usually grouped into centers

based on resources, activities, or cost objects. (SAP,

2001)

2.2 ERP (Enterprise Resource

Planning)

Enterprise Resource Planning system (ERP) is a bun-

dled software solution that integrates all systems, for

all core business processes and data into one reposi-

tory. ERP is required in the integration and integra-

tion of all core businesses into one central database

that is required to be able to take business inputs (re-

sources) in the form of materials, people and equip-

ment, and transform these inputs into goods and ser-

vices for customers (Lee et al., 2017).

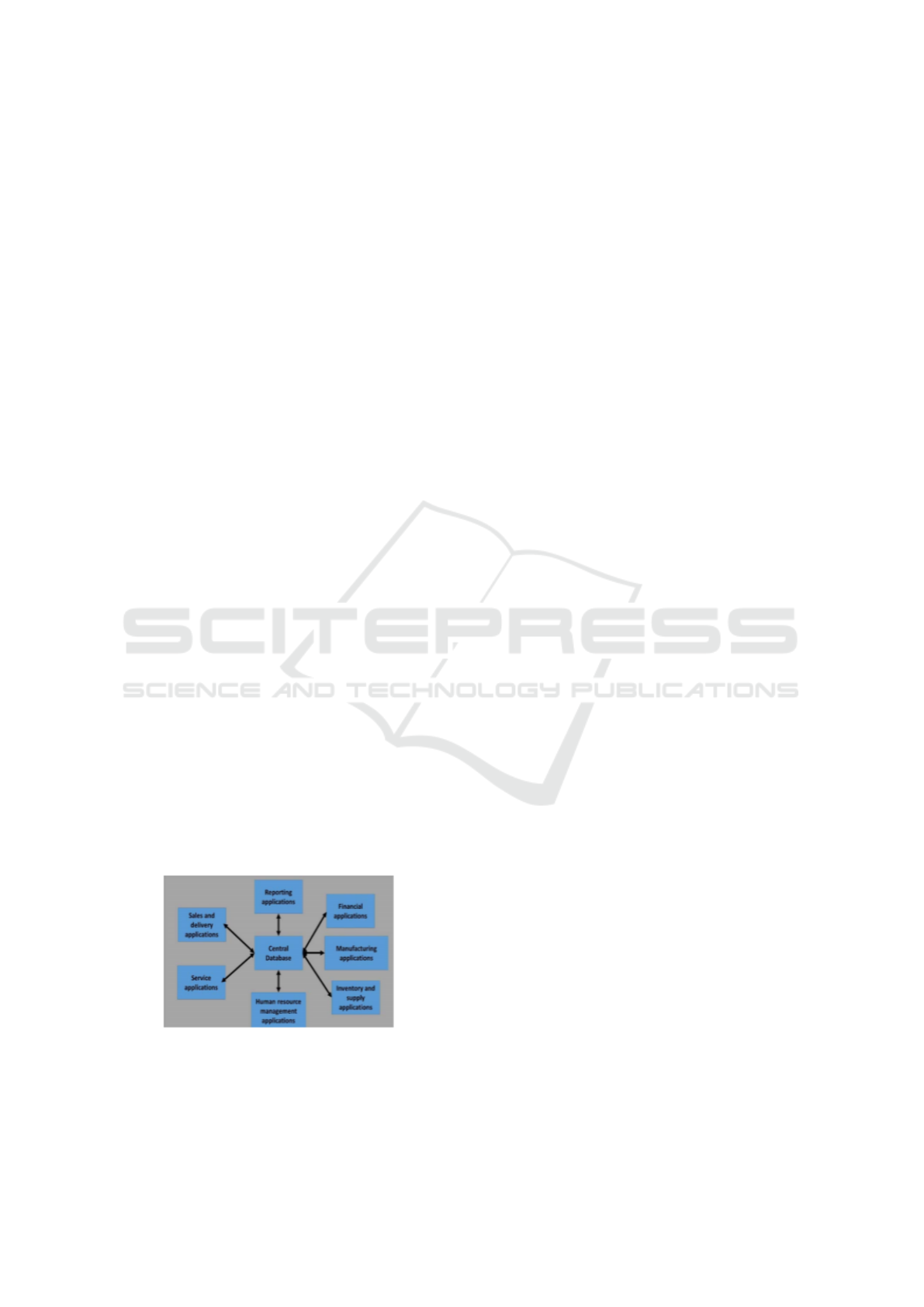

Figure 1: General ERP Model.

Figure 1 explain the general ERP Model that com-

bine and integrate all core business function(s) into

one central database.

2.3 SAP HANA

SAP HANA was introduced in 2015 as a cloudbased

ERP that can support a platform in memory to in-

crease speed and comparative data analysis with an

older version, which requires a longer implementa-

tion time (Lee et al., 2017).

SAP HANA has basic data which is a core compo-

nent of the SAP HANA road map to support all SAP

and non-SAP business processes from an application

perspective and data management perspective to be

more efficient. Positioned to act as a platform (Lee

et al., 2013).

SAP HANA has benefits, one of the benefits of

using SAP HANA is reducing complexity, can be

accessed anywhere because SAP HANA is cloud-

based, and real results (SAP, 2019). Business data

platform that processes transactions and analysis in

SAP HANA will work at the same time on all data

types, with integrated advance analytics and multi-

model data processing engines that can be used to

develop next-generation applications for smart com-

panies (SAP, 2019).

2.3.1 SAP Controlling

SAP CO (Control) is a module that contains informa-

tion that will be taken into consideration for manage-

ment decision-making and usually in toplevel posi-

tions in companies such as supervisors. This module

can facilitate coordination, facilitate and optimize all

processes in an organization. This involves record-

ing the consumption of the factors of production and

services provided by an organization. The point is

Controlling is used for internal company (Sapbrain-

sonline, 2019).

Sub modules of the SAP CO module are :

1. Cost Element Accounting

2. Cost Center Accounting

3. Internal Orders

4. Activity-Based Costing (ABC)

5. Product Cost Controlling

6. Profitability Analysis

7. Overhead Cost Controlling

8. Profit Accounting Center.

2.3.2 Activity-Based Costing (ABC)

ABC is a method that assumes that activities will pro-

duce cost objects (products, services, customers) and

some product cost incurred will create demand for ac-

tivities (SAP, 2001).

CONRIST 2019 - International Conferences on Information System and Technology

254

This ABC system recognizes that a business must

understand the factors that drive an activity (activity),

the costs incurred by the activity, and how those ac-

tivities are linked to the cost object. First, ABC will

place costs on activities that have actually resulted in

these costs. After that, the costs of activities are only

charged to products that do require the activity (SAP,

2001).

Figure 2: Activity Based Costing in the SAP system.

From the picture above, calculating ActivityBased

Costing (ABC) can increase the cost of costing prod-

ucts. Resource center costs can be allocated to busi-

ness processes based on the provision of actual activ-

ities (SAP, 2001).

By including ABC in profitability analysis, it

makes a more realistic view of your income position.

The main goal is not only to improve individual pro-

cesses, but also to improve the entire process chain.

Other objectives of ABC include shortening waiting

time and improving quality (SAP, 2001).

At Figure 2, we can see some processes, products,

product families, customer, and distribution channel.

They all connect to cycle and Activity-Based Costing

is inside CO-OM-ABC, CO-PC, and CO-PA.

2.4 Company Code and Chart of

Account

A chart of account is a list of accounts used by compa-

nies (Projects, 2019). There are three types of account

charts: Account operations charts, country specific

account charts, group account charts. The Chart of

Account that deals with and posts all regular business

transaction processes is an Operational Chart. The re-

maining account charts are used for different business

scenarios. At the request of the client, we can specify

another account chart (Projects, 2019).

The definition of a company code is the smallest

independent organizational unit that has its own ac-

counting book and is obliged to prepare legitimate in-

dividual financial statements, such as balance sheets

and income statements. The definition of the com-

pany code is mandatory (Portal, 2017).

2.5 Cost Center

Cost center is a location where the cost adds up in or-

ganisation indirectly adds to profit. Typical examples

include marketing, customer service, research and de-

velopment .

Cost centers are responsibility for all areas costs

within organization and used to capture actual costs

of an organization (“What is a Cost Center in SAP —

How to Create Cost Centers in SAP,” 2018).

2.6 Cost Element

The cost element is a carrier of costs associated with

collecting costs and summarizing costs in controlling

and posting to the reconciliation ledgers of financial

accounting to control from one controller object to an-

other (Projects, 2019). Cost accounting elements are

useful for posting across companies, in all areas of

business posting to financial accounting when com-

panies follow the concept of crosscompany cost ac-

counting codes. There are two types of Cost Element,

Primary and Secondary Cost Element.

In the financial module, another way to call the

ledger account is the primary cost element. To trans-

form a ledger account into a primary cost element, we

must specify the category of the primary cost element

that determines the nature of the element in control.

The secondary cost element is exclusively made to

control. By category, secondary elements can be used

for other purposes that are more specific to be made.

There are several types of secondary cost elements,

including:

1. Internal order settlement

2. Overhead rate

3. Assessment

4. Internal activity allocation.

2.6.1 Assessment

The assessment cycle consists of segmentation, each

of which has a unique relationship between receivers,

senders, and assessment rules. This can be defined on

the CO-PA (Westney, 1997).

Method of Assessment is a cost budget without

prioritizing the primary cost element. In this method,

the allocation will be done through the secondary

cost element. The difference between the distribu-

tion and the assessment method is the assessment

method which is more directed to the periodic report-

ing method and the renewal method (Projects, 2019).

In the assessment, we will do cost allocation. The fo-

cus is on moving data from one cost center to another

cost center or even to a business process.

Analysis of Assessment Cycle of Migration Data from OROS to SAP Hana using Activity based Costing Method in Telecommunication

Industry

255

Definition of data migration itself, researchers

take refer to the relevant literature from the field data

migration. Data migration is a technical process from

aggregation and / or separation of information enti-

ties from embedding system to match information ex-

change requirements include adjusting data formats

as needed. If the company does not have an approach

model for their data migration activities, they cannot

guarantee that data migration will be successful and

that is the risk (L

¨

ussem and Harrach, 2013).

2.7 Profitability Analysis (CO-PA)

CO-PA is used to analyze the profitability of a com-

pany according to existing market segments, catego-

rized by products, customers, orders or a combina-

tion of all of these, or strategic business units, such as

sales organizations or business areas, which relate to

the profit or margin contribution of a company.

2 types of profitability analysis are: cost-based

and account base. Cost-Based Profitability Analysis

is a form of profitability that focus on analysis groups

costs and revenues based on value fields and cost-

based valuation approaches, both of which you can

set yourself. This guarantees you access at any time

to a complete short-term profitability report. Account

Based Profitability Analysis is a form of profitabil-

ity analysis that is regulated in an account and uses an

account based valuation approach. The distinguishing

characteristic of this form is the use of cost and rev-

enue elements. It gives you a profitability report that

is permanently reconciled with financial accounting.

3 METHODOLOGY

3.1 SAP Activate Methodology

The SAP activate methodology is a simple, modular

and agile framework for implementation or conver-

sion to SAP S / 4HANA. We can use it ourselves,

with SAP Partners or with SAP Direct. It was built on

its predecessor ASAP Methodology and SAP Launch

Methodology (Kralji

´

c and Kralji

´

c, 2018). There are

6 stages in Activity Methodology, which are discover,

prepare, explore, realize, deploy and run.

Figure 3: SAP Activate Methodology.

Figure 3 explain all 6 phases in SAP Activate

Methodology :

1. Discover

This phase need to identify all requirements, de-

velop strategies and road-map use on the imple-

mentation journey. Books, journals, and literature

study used to discover related knowledge along

the implementation process such as methodology

and basic knowledge.

2. Prepare

The second phase project is initiated and planned,

including quality and risk plans. Software and

system environment is set up, including best prac-

tices with ready to run processes.

3. Explore

In Explore phase, use fit/gap analysis to iden-

tify the solution and extensions that best meet the

company’s requirements.

4. Realize

In this phase, the SAP application will be config-

ured and extend the system based on prioritized

requirements captured in explore phase. Struc-

tured testing and data migration activities help en-

sure quality.

5. Deploy

In this phase is final preparations to set the pro-

duction before cut over to new system and ensure

that the system data and users are ready for tran-

sitioning to production environment.

6. Run

Purpose of Run phase is to continue adoption of

implemented solution across the organization and

meet evolving business needs with SAP.

3.2 Research Method

In this paper will focus on implementing 3 phases

from SAP Activate Methodology, start from Discover,

Prepare, and Explore to see fit/gap analysis in the new

design/method.

Figure 4: SAP Activate Methodology for Research method.

Figure 4 explain 4 phases in SAP Activate

Methodology that will use for research method. The

researcher has analyzed the assessment cycle data

in OROS to be migrated to SAP HANA using the

CONRIST 2019 - International Conferences on Information System and Technology

256

method of costing Activity-Based Costing to match

the data cycle in OROS and SAP HANA, so that it can

be used to generate reports to the Profitability Analy-

sis (CO-PA) and for SAP Activate Methodology, re-

searchers only focus untilalize stage because they are

still analyzing data from OROS to SAP HANA. The

researchers also focuses on finding relation from the

processes that exist in OROS and SAP HANA. To be

able to continue the process up to phase run, the re-

searchers must fully understand how to migrate data

from OROS to SAP HANA and determine what is

needed by SAP HANA in inputting data.

4 ANALYSIS AND DISCUSSION

4.1 Analysis

4.1.1 Discover

In this Discover, researcher define the environment

system in OROS. Researchers analyze activity based

costing business processes and identify mass data that

must be input one by one. Books, journals, and liter-

ature study used to discover related knowledge along

the implementation process such as methodology and

basic knowledge.

OROS Modeler is a fairly simple application con-

cept that only have 3 core components which are Re-

source, Activity and Cost Object but to implementing

application of OROS Modeler itself can be difficult.

The path of the data must be correct.

Figure 5: Oros Path.

As shown in the above figure, the possible assign-

ment paths in OROS Modeler, are:

A - From a Resource account to another Resource

account

B - From a Resource account to an Activity account

C - From a Resource account to a Cost Object

account

D - From an Activity account to another Activity

account

E - From an Activity account to a Cost Object

account

F - From a Cost Object account to another Cost

Object account.

Data flow from OROS Modeler can be very com-

plex and difficult to track provenance. We need to

map objects from OROS from resources to cost ob-

jects. In addition, in OROS there are also Cost drivers

that are used to charge activity costs to output that are

structurally different from those used in conventional

cost systems or causal factors that explain overhead

consumption. Cost drivers are the basis used to charge

fees collected on a collection of costs for the product.

Figure 6: SAP Activate-Based Costing

From the picture above explains that in SAP

HANA, there are a few similarities like OROS Mod-

eler. SAP HANA has 3 main components, namely

Cost center (resource), Process (Activities) and CO-

PA (as a product). For Cost Object in OROS is a

product, but another thing in SAP HANA. In SAP

HANA, Cost object is a container for company costs

and there are various types of cost objects in SAP,

which are internal orders, cost centers, Work Break-

down Structure (WBS), production orders, maintain

processes and business processes. Business process

itself is a cost object for activity based costing.

In Figure 7, the data migration process starts from

the OROS application. At OROS, the main compo-

nents that can be matched with Activity-Based Cost-

ing in SAP are predetermined. After that, Record the

data that we need in SAP such as Cost Centers, Cost

Elements and others. At SAP HANA, we will view

whether Cost Center data, Cost Elements, and other

data are the same as data that has been entered by

companies in SAP. If yes, we continue to check the

suitability of the data in SAP. If not, we need to create

new data in SAP. After that, just create an Account

Chart to classify the parent account. After this stage,

we will begin to make an assessment cycle using the

KSU1 transaction code. When finished, do a Test Run

on the KSU5 transaction code to see there is an error.

If there is a warning, check the error and fix it. If not,

run it and the process is complete. This research will

stop until we can run the assessment cycle because

here is the final purpose of this paper.

Analysis of Assessment Cycle of Migration Data from OROS to SAP Hana using Activity based Costing Method in Telecommunication

Industry

257

space

Figure 7: Data migration process flowchart.

4.1.2 Prepare

The second phases focus on initiated and planned. Af-

ter knowing the components in OROS and SA, we

need to create an architect for the assessment cycle

to facilitate the migration of data to SAP HANA.

Figure 8: Architecture for Assessment Cycle.

The picture in figure 8 is the architect’s assessment

cycle in SAP HANA which may appear when migrat-

ing data from OROS to SAP HANA. When migrat-

ing data from a Cost center to a Cost center or a Cost

Center to a Business Process, you can use the KSU1

in transaction code (TCODE). Before making a cycle

at KSU1, we need to prepare several things such as

Chart of Accounts, determine senders and receivers,

make assessment CELe, group cost centers or cost el-

ements if needed, and determine the cycle names.

This stage is also needed in migrating data from

the Cost Center to the Business Process. The differ-

ence is when the Cost Center goes to the Business

Process, the receiver is the Business Process. Busi-

ness Process can also be in groups if needed.

In the cycle of making this, we use secondary cost

elements. The secondary cost element is a tool for

conducting assessments. Secondary cost elements are

posts that occur between controller objects in CO.

The secondary cost element is basically an account

that only exists in the CO module (internal company),

not in FI (external company). When costs are moved

(e.g., from one cost center to another using valuations,

or from cost centers to production orders), no posts

are made on P&L FI. Instead, a secondary cost ele-

ment is used to track the post in the CO document.

4.1.3 Explore

In Explore phase, researchers will use fit/gap analysis

to identify the solution and extensions that best meet

the company’s requirements and needs. The solution

for company is mapping data flow in OROS and mi-

grating all data to SAP HANA with assessment in ac-

tivity based costing.

CONRIST 2019 - International Conferences on Information System and Technology

258

space

Figure 9: Fit and Gap analysis.

4.1.4 Realize

In this phase, the SAP application will be configured

and extend the system based on prioritized require-

ments captured in explore phase. Structured testing

and data migration activities help ensure quality. Re-

searchers conducted an experiment in migrating data

finance in SAP HANA using activitybased costing

method and assessment cycle. Researchers do a cost

allocation from the base salary account which will be

allocated to RCV Gaji as cost center group and will

stop at T663H01 Cost Center.

space

Figure 10: Base Salary and allocation.

In the Figure 10 above, it can be seen that the base

salary account before being allocated has a cost of

Rp. 72,116,445,146 and that cost will be allocated

using the 99010002 assessment account to cost center

group. 99010002 is the assessment that we make to

allocate the cost from base salary. In assessment, we

must know how much cost percentage that we want to

allocate. To solve that issue, we used Statistical Key

Figures to put how much cost that we need to allocate.

From base salary, it will allocate cost to

RCV Gaji. RCV Gaji is Cost center group. We can

group cost centers and also cost elements if needed.

The function of grouping is that we map costs to be

allocated according to several cost centers or cost el-

ements needed.

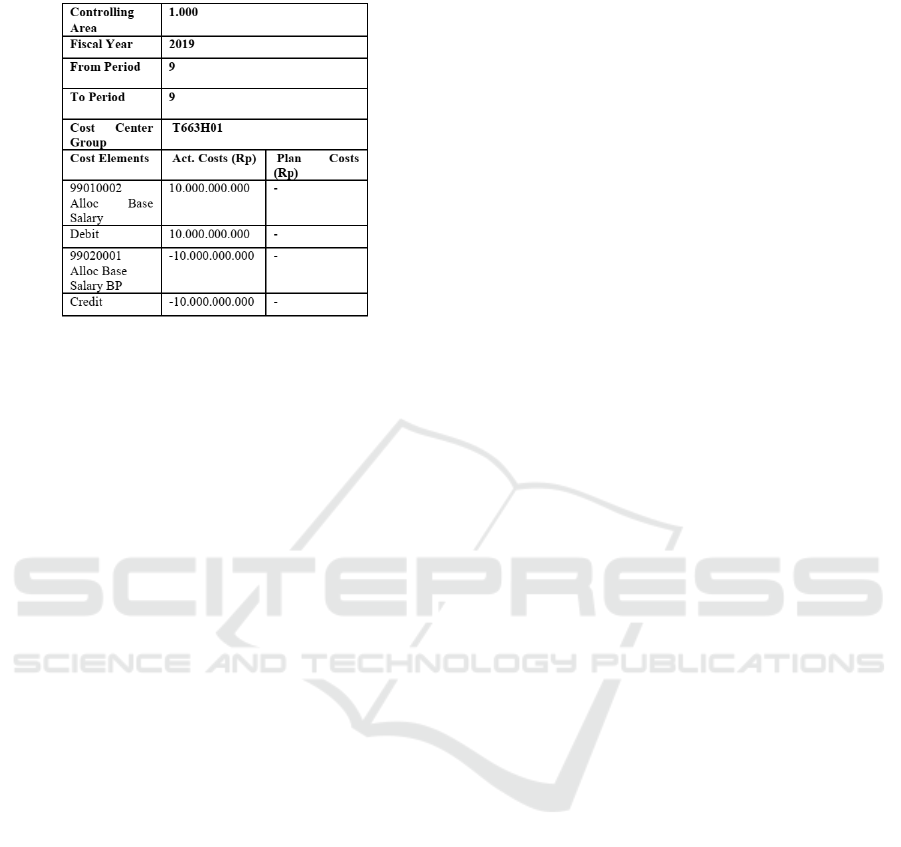

Figure 11: RCV Gaji allocation.

In the Figure 11 above, it can be seen that

RCV Gaji receives cost allocation from the 99010002

assessment account. From RCV Gaji will allocate

cost to the T663H01 cost center, using the 99020001

assessment account. A minus sign indicates that the

costs are allocated.

Analysis of Assessment Cycle of Migration Data from OROS to SAP Hana using Activity based Costing Method in Telecommunication

Industry

259

space

Figure 12: T663H01 Cost allocation.

5 CONCLUSIONS

PT ABC is transitioning to SAP HANA from SAP

R/3. Choosing SAP HANA is the right choice be-

cause SAP HANA has many advantages than SAP

R/3. SAP HANA has capabilities include database

services, advanced analytics processing, app develop-

ment, data access, administration, and openness. The

benefits to use SAP HANA, it helps us manage data

in a single in-memory platform, so we can take ac-

tion at the moment. Accelerate the pace of innova-

tion and run live in this new digital economy. Activ-

ity Based Costing also the right choice to make cost

allocation because all business processes at PT ABC

based on Activity. Consultants or workers who are

familiar with the OROS and SAP HANA applications

are needed, so that it can facilitate the process of mi-

grating data from OROS to SAP HANA. In this study,

researchers successfully migrated data and were able

to allocate finance base salary data using the assess-

ment cycle. The weakness of this assessment cycle is

that there is a lot of data and must be mapped one by

one, it takes a long time, and we must understand very

well the cycle that we made. The strength of this as-

sessment cycle is that we can see the cost allocations

and where the cost allocation came from.

For future research, using LSMW might help to

automate the data in SAP HANA and also use the

ABAP program for data adjustments.

space

ACKNOWLEDGEMENTS

We thank you to the previous researchers for provid-

ing useful knowledge and assistance in the writing of

this paper and special thank you to everyone involved.

REFERENCES

Greiner, L. (2019). Sas canada celebrates partners at sas

global forum.

King, R. (2014). Sap’s new cloud strategy includes app

marketplace, new pricing scheme.

Lee, J., Kwon, Y. S., F

¨

arber, F., Muehle, M., Lee, C.,

Bensberg, C., Lee, J. Y., Lee, A. H., and Lehner, W.

(2013). Sap hana distributed in-memory database sys-

tem: Transaction, session, and metadata management.

In 2013 IEEE 29th International Conference on Data

Engineering (ICDE), pages 1165–1173. IEEE.

Lee, M. J., Wong, W. Y., and Hoo, M. H. (2017). Next era of

enterprise resource planning system review on tradi-

tional on-premise erp versus cloud-based erp: Factors

influence decision on migration to cloud-based erp for

malaysian smes/smis. In 2017 IEEE Conference on

Systems, Process and Control (ICSPC), pages 48–53.

IEEE.

L

¨

ussem, J. and Harrach, H. (2013). How to make data mi-

gration processes more efficient by using togaf: Best

practice data migration approach applied to sap finan-

cial services-policy management. In 2013 ACS Inter-

national Conference on Computer Systems and Appli-

cations (AICCSA), pages 1–6. IEEE.

Oracle (2019). What is erp?

Portal, S. H. (2017). Company code - sap help portal.

Projects, E. (2019). Sap book for beginners and learners.

SAP (2001). Activity-based costing (co-om-abc).

SAP (2019). What is sap hana?

Sapbrainsonline (2019). Sap co tutorial – controlling func-

tional module.

Savchuk, R. R. and Kirsta, N. A. (2019). Managing of the

business processes in enterprise by moving to sap erp

system. In 2019 IEEE Conference of Russian Young

Researchers in Electrical and Electronic Engineering

(EIConRus), pages 1467–1470. IEEE.

Westney, R., L. N. R. P. (1997). The engineer’s cost hand-

book: Tools for managing project costs.

CONRIST 2019 - International Conferences on Information System and Technology

260