The Role of After-sales Service for Online Shopping Loyalty

Budi Setyanta

1

, Dian Citaningtyas Ari Kadi

2

, Danang Wahyudi

2

, Kartinah

2

, Titop Dwiwinarno

2

and

Aswin Siddik Sarumaha

3

1

Fakultas Ekonomi Universitas Janabadra Yogyakarta, Tentara Rakyat Mataram street, Yogyakarta, Indonesia

2

Fakultas Ekonomi Dan Bisnis, Universitas PGRI Madiun, Madiun, Indonesia

3

Fakultas Ekonomi Universitas Janabadra Yogyakarta, Yogyakarta, Indonesia

Keywords:

Loyalty, Perceived Risk, Perceived Benefit, Trust, After-Sales Service

Abstract:

This study aims to identify the effect of after-sales service on online shopping loyalty. Sample 200 in this

study is people who have done online shopping to meet the sample adequacy requirements in the structural

equation model test. The results of the study indicate that after-sales service moderates the customer loyalty

model. This study only uses 200 samples and does not divide the sample according to specific criteria. Future

research is expected to increase the number of samples and divide the sample based on specific criteria so that

the results of the study can be more precise in explaining the increasing phenomenon of online shopping.

1 INTRODUCTION

Online shopping is a rapidly growing phenomenon

and is one of the most astonishing trends (Lim et al.,

2016). The definition of online shopping in this study

is shopping through the Internet. The Internet affects

consumer behaviour in conducting searches, shop-

ping and product payments (Yannopoulos, 2011). At

present, the Internet is developing not only as a means

of communication and information search engine but

has become one of the essential tools to improve com-

petitiveness. The Internet plays a role in encourag-

ing sales transactions and increasing cost efficiency

(Yannopoulos, 2011). The Internet because it af-

fects the daily lives of consumers (Nam, 2003). The

growth of internet users in Indonesia is very rapid and

is estimated to reach 143 million in 2017 (Bohang,

2018) so that Indonesia is a potential market for on-

line stores. Although the number of online transac-

tions has increased, more than half of internet users

have expressed confusion and frustration at online

shopping activities (Horrigan, 2008). Perceived in-

convenience indicates that in addition to providing the

benefits of online shopping it also faces risks due to

uncertainty (Egeln and Joseph, 2012). To reduce cus-

tomer perceived risk, the seller provides after-sales

service (Asugman et al., 1997). After-sales service

is an ongoing relationship with customers after pur-

chase (Sigala et al., 2008), by providing guarantees or

repair services to increase customer satisfaction and

loyalty (Ladokun et al., 2013). After-sales service can

increase competitive advantage because it can attract

the attention of customers (Chien*, 2005). Compa-

nies invest significant funds to make differentiation

by providing additional services (Loomba, 1998).

Many studies on the role of after-sales service on

purchasing behaviour indicate that after-sales service

has a positive effect on customer behaviour. After-

sales service is a necessary construct that influences

customer behaviour. Customers receive positive ben-

efits from the after-sales service provided, but cus-

tomer perceptions of after-sales service vary. Previ-

ous research put the role of aftersales service as a pre-

dictor of buying behaviour has not yet explained the

role of after-sales service in moderating buying be-

haviour.

This research aims to identify the role of aftersales

service as a moderating model of customer loyalty.

Transactions that are potentially at risk, customers

need a loss-free guarantee. Even though the product is

of good quality and profitable for the customer, if the

customer faces a risk, then aftersales service becomes

an essential consideration in the decision-making the

process. Customers who give full trust to the seller

may be insignificant after-sales service in the buying

process.

This study divides customers into two groups.

Groups that have the perception that after-sales ser-

vices are critical, namely high groups and groups that

have the perception after-sales services are less criti-

64

Setyanta, B., Kadi, D., Wahyudi, D., Kartinah, ., Dwiwinarno, T. and Sarumaha, A.

The Role of After-sales Service for Online Shopping Loyalty.

DOI: 10.5220/0009878100640069

In Proceedings of the 2nd International Conference on Applied Science, Engineering and Social Sciences (ICASESS 2019), pages 64-69

ISBN: 978-989-758-452-7

Copyright

c

2020 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

cal, namely low groups.

2 HYPOTHESIS

Risk plays a vital role in consumer behaviour because

it influences the process of making consumer purchas-

ing decisions and reduces consumer intention to make

online purchases (Barnes et al., 2007). Risk includes

all the negative consequences of consumer purchases

that cannot be anticipated. There are two theoreti-

cal perspectives on risk: one that focuses on the un-

certainty of the outcome of the decision to make a

purchase and the other focuses on the costs or con-

sequences of the results of online purchases (Barnes

et al., 2007). There is no agreement on the defini-

tion of risk, but often more shows the results of ad-

verse decisions (Gefen, 2002a). Consumers have dif-

ferences in assessing risk, and there are differences in

consumer attitudes towards risk.

Previous research shows that perspectives of risk

are negatively and significantly related to online pur-

chases; if customer perceptions of risk are high, then

the attitude of customers to online shopping is low.

Based on this, the second hypothesis in this study is.

H1: Risk perception has a negative effect on on-

line shopping loyalty

The perceived benefits of online shopping com-

pared to buying in traditional stores is one of the main

driving factors for online purchases. The choice of

one’s behaviour to make an online purchase is a con-

sequence of the satisfaction felt by the customer.

Consequences that consumers feel significantly

influence the behaviour of online shopping. In other

words, an individual will make an online purchase if

they feel the benefits (positive consequences) or will

not make an online purchase if the consumer feels

critical negative consequences. This finding is con-

sistent with research from (Kurnia and Chien, 2003)

which indicate that perceived benefits and ease of use

are felt to have a positive effect on online shopping

behaviour.

Consumers’ perceived consequences significantly

influence online shopping behaviour. In other words,

an individual will make an online purchase if they feel

the benefits (positive consequences) or will not make

an online purchase if the consumer feels critical neg-

ative consequences.

(Forsythe and Shi, 2003) found evidence that there

was a positive and significant relationship between

perceived internet shopping profits and the frequency

of spending and the amount spent online. Based on

previous research, the first hypothesis in this study is.

H2: Perception of benefits has a positive effect on

online shopping loyalty

Trust is an essential variable in online purchas-

ing because one party does not take advantage of the

weaknesses of the other party in trade, willingness to

accept the actions of others because of the expecta-

tion that the other party takes actions that are impor-

tant to him (Mayer et al., 1995). Trust in the context

of online purchases is related to risk factors (Van der

Heijden et al., 2003). Trust is one of the main fac-

tors that influence the context of online purchases and

as a determinant of individual attitudes or online pur-

chase intentions (Gefen et al., 2003). Trust indicates

that higher consumer confidence in online shopping,

higher shopping behaviour. Based on previous re-

search, the third hypothesis in this study is.

H3: Trust has a positive effect on online shopping

loyalty

After-sales service is a continuous relationship

with customers after the purchase (Sigala et al., 2008),

by providing after-sales services and ensuring reliable

product functions (Ahn and Sohn, 2009), for exam-

ple warranty or repair services, so as to increase sat-

isfaction and customer loyalty (Ladokun et al., 2013).

After-sales service can increase competitive advan-

tage because it can attract the attention of customers

(Chien*, 2005).

After-sales service is an activity carried out by

the company after the purchase of products that can

increase competitive advantage by ensuring that the

product is problem-free for the duration of the prod-

uct, failed product replacement and guaranteed re-

pairs during the warranty period, timely repairs and

affordable repair costs.

The higher the after-sales service provided to cus-

tomers, the greater customer loyalty because of get-

ting a guarantee of the costs spent. After-sales service

is a variable that can moderate customer loyalty by di-

vide into high and low after-sales services. Based on

this understanding, the hypothesis in this study is.

H4: After-sales service moderates the effect of

risk perception on customer loyalty on online shop-

ping

H5: After-sales services moderate the influence

of perceived benefits on customer loyalty on online

shopping

H6: After-sales service moderates the effect of

trust in customer loyalty on online shopping

The Role of After-sales Service for Online Shopping Loyalty

65

3 RESEARCH METHODS

3.1 Population and Samples

The object in this study is online shopping loyalty.

The population in this study are people who have the

intention to repurchase online shopping intending.

In this study, the sample size to be taken is 200

according to the requirements of the study sample ad-

equacy using SEM analysis tools.

Data collection uses a questionnaire given to peo-

ple who have the intention of shopping online through

convenience sampling techniques.

4 RESULTS AND DISCUSSION

The Structural Equation Modeling (SEM) test uses

sample adequacy assumptions, data normality and

outliers. The number of respondents in this study was

200 to fulfil the sample adequacy requirements.

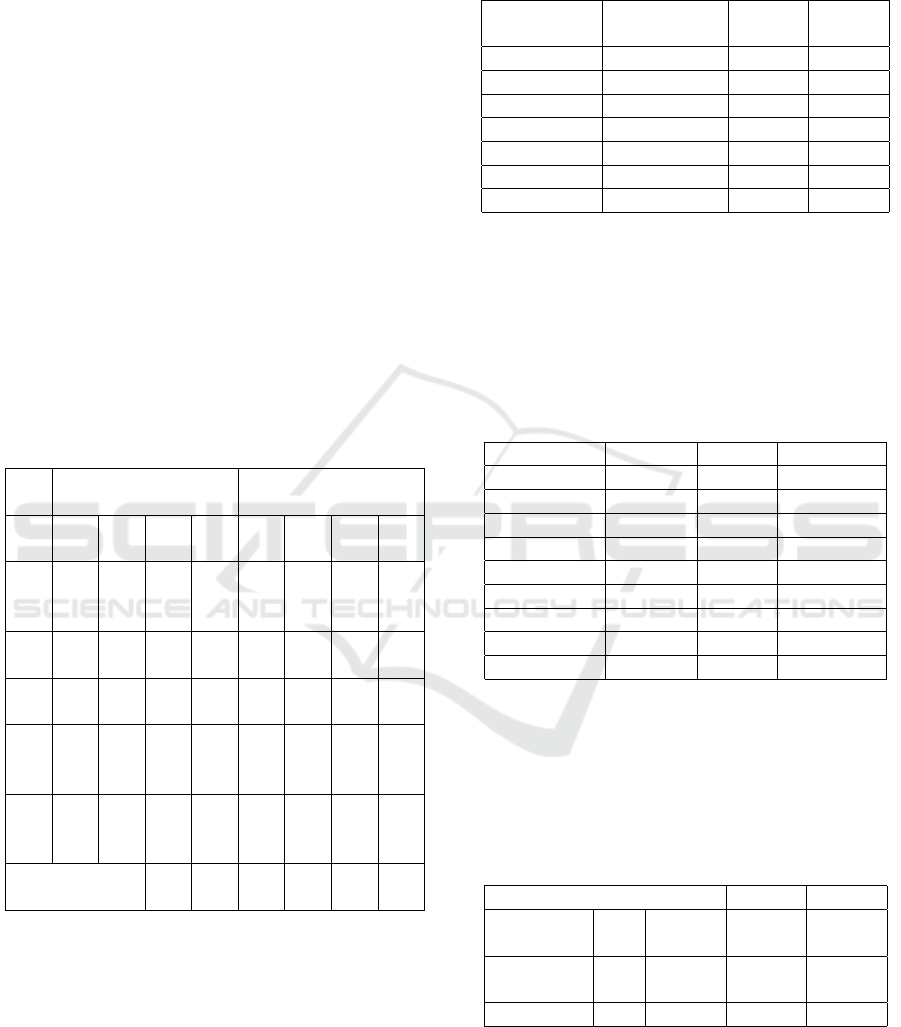

Table 1: Normality Test Result

item

Before

Transformation

After

Transformation

sk

ew

c.r. kurt

osis

c.r. sk

ew

c.r. kurt

osis

c.r.

R2 -

0.61

-

3.0

05

-

0.4

08

-

4.7

15

0.0

32

2.3

37

0.1

08

2.2

1

R3 0.9

92

1.6

2

1.0

2

3.7

7

0.7

61

1.2

08

1.3

35

2.0

9

M1 1.3

82

1.5

4

1.4

6

4.0

5

1.0

46

1.3

34

1.0

6

1.8

9

P1 -

0.5

92

-

3.2

21

-

0.4

51

-

3.3

32

0.0

26

0.4

97

-

0.2

88

-

1.0

58

P2 0.3

39

4.6

84

-

0.8

57

-

3.1

02

0.3

28

1.3

82

-

0.9

85

-

0.9

97

Multivariate 89.

081

15.

557

66.

037

9.0

48

The normality test consists of two parts. Univari-

ate abnormalities identified from the value of the criti-

cal ratio (c.r) skewness and multivariate normality are

identified from the value of the critical kurtosis ra-

tio (c.r). Univariate and multivariate normality is ac-

cepted if the critical ratio (c.r) is between the critical

values of -2.58 and 2.58. The results of the normality

test after data transformation indicate that the data is

normally distributed univariately. Although the distri-

bution of multivariate normality data is not fulfilled,

because the amount of research data is quite large (n>

100), the assumption of normality can be ignored .

Table 2: Outliers Test Resut

Observation

number

Mahalanobis

d-squared

p1 p2

104 102.96 0 0.09

95 99.04 0 0.08

88 83.75 0 0.06

87 66.53 0 0.05

52 63.05 0 0.04

33 58.44 0 0.04

9 49.32 0 0.04

The number of indicators in this study is 25, and

the case said that if the outliers are married, the Maha-

lanobis d-Square value is greater than χ2 (25; 0.001)

= 44,314. The test results in this study indicate that

there are six outlier cases, but because there are no

specific reasons for issuing outlier data, the data can

still be used in subsequent statistical tests.

Table 3: Goodness-of fit test results

Indeks Cut-off Result Conclusion

Chi Square Kecil 382.091

P ≥ 0.05 0.822 Fit

CMIN/DF ≤ 2.00 0.981 Fit

GFI ≥ 0.90 0.934 Fit

AGFI ≥ 0.90 0.871 Marginal

CFI ≥ 0.95 1 Fit

TLI ≥ 0.95 0,995 Fit

RMSEA ≤ 0.06 0.01 Fit

IFI ≥ 0.95 0,990 Fit

Goodness-of-fit test to identify whether the model

developed can explain data according to the underly-

ing theory. The goodness-of-fit test results identify

only AGFI that has marginal values so that the re-

search model is indicated to be fit and able to explain

the phenomenon of research.

Table 4: Regression Test Before Moderation

β C. R

Perception

Risk

→ Loyalty -0,104 205

Perception

Benefit

→ Loyalty 0,162 3,11

Thrust → Loyalty 0,117 2,17

To identify the causality relationship between re-

search variables and hypothesis testing, the Structural

Equation Modeling (SEM) test is used, by analyzing

the significance level of the effect of independent vari-

ables on the dependent variable based on the CR value

ICASESS 2019 - International Conference on Applied Science, Engineering and Social Science

66

(z-count) greater than or equal to the z-table value (z-

count ≥ z-table). The test results before being mod-

erated by the trust as follows.

The regression test results between the risk per-

ception variables and loyalty indicate that perceived

risk has a positive and significant effect on loyalty (β

= -0.104, and CR = 2.05), so H1 is supported. The

regression test results indicate that the perceived risk

hurts online shopping loyalty, so to increase online

shopping loyalty, a program is needed to reduce per-

ceived risk.

The implies of the result that perceived risk influ-

ence online shopping behaviour. The results of this

study support previous research. (Barnes et al., 2007)

which states that risk plays a vital role in consumer

behaviour because it affects the process of making

consumer purchasing decisions and reduces the inten-

tion of consumers to make online purchases. (Gefen,

2002b)(Liu, 2012)(Sweeny et al., 1999) which state

that the chance of loss experienced by consumers both

financial and nonfinancial losses will have a negative

and significant effect on the attitude of online shop-

ping. Although tested in a different context from pre-

vious research, this study identifies that the effect of

perceived risk on loyalty tends to lead to negative and

consistent influential phenomena.

The regression test results between perceived ben-

efit variables and online shopping loyalty indicate that

perceived benefits have a positive and significant ef-

fect on online shopping loyalty (β = 0.162, and CR

= 3.11), so H2 is supported. The result indicates that

if the benefits perceived by consumers as a result of

online shopping are getting bigger, the positive atti-

tude of consumers towards online shopping is getting

bigger.

The results of this research are supports the opin-

ion of (Forsythe and Shi, 2003) which states that the

perceived benefits of online shopping compared to

purchases in traditional stores is one of the main driv-

ing factors of purchase, because one’s choice of be-

haviour to make online purchases is a consequence of

satisfaction perceived by customers. In other words,

an individual will make an online purchase if they feel

the benefits (positive consequences) or will not make

an online purchase if the consumer feels essential neg-

ative consequences. This finding is consistent with

research from (Kurnia and Chien, 2003), who found

the fact that perceived benefits and ease of use were

positively affected by online shopping attitudes.

Although tested in a different context with previ-

ous research, this study identifies that the influence of

perceived benefits on online shopping loyalty tends to

lead to a phenomenon that has a positive and consis-

tent effect.

This study also found the fact that trust had a pos-

itive and significant effect on online shopping loyalty

(β = 0.117, and CR = 2.17), so the third hypothesis

(H3) in this study was supported. The result indicates

that if consumers increasingly believe in online shop-

ping, the positive attitude of consumers will be higher

in doing online shopping. Online business actors must

increase consumer trust because trust is a vital vari-

able in online purchases due to uncertainty. Online

stores require effort to improve integrity, kindness,

and competence and provide what has been promised

to strengthen customer loyalty.

The results of this study support previous studies

conducted by (Liu, 2012)(Teo, 2002) which state that

trust is one of the main factors that have a positive ef-

fect in the context of online purchases, (Gefen et al.,

2003). That the higher the customer’s trust in online

shopping, the higher the customer’s attitude towards

online purchases. Although tested in a different con-

text with previous research, this study identified that

the influence of trust on customer loyalty tends to lead

to a phenomenon that has a positive and consistent ef-

fect.

Table 5: Regression Test Before Moderation

High Low

B C.R β C.R

Perce

ived

Risk

→ Loya

lty

-

0,091

1,35 -

0,233

2,04

Perce

ived

Ben-

efit

→ Loya

lty

0,221 2,94 0,181 2,19

Thrust → Loya

lty

0,193 1,56 0,126 2,52

difference chi square test (∆χ2) = 572,366 - 544,027

= 28,34

difference df (∆df) = 338 - 301 = 37

chi square table (37;0,05) = 52,192

chi square table (χ2) > difference chi square

calculate (∆χ2)

The Constrained model is significantly different from

the Unconstrained Model

The results of the multi-group regression test after

moderating after-sales service indicate that after-sales

service moderate the research model (chi-square table

(χ2)> chi-square difference count (∆χ2)) so that the

constrained model is significantly different from the

unconstrained model.

Table 5 shows that in the after-sales service group,

high perceptions of risk and trust do not affect on-

line shopping loyalty, while perceived benefits have

a positive and significant effect on online shopping

The Role of After-sales Service for Online Shopping Loyalty

67

loyalty. In the low after-sales service group, that per-

ceived benefits, perceived risk and trust affected on-

line shopping loyalty.

In the high after-sales service group, the results of

the regression test between risk perception variables

towards online shopping loyalty indicate that risk per-

ception does not affect online shopping loyalty (β =

-0.091, C.R. = 1.35). The results of this study in-

dicate that after-sales service as providing a solution

that reduces risk perception — various opportunities

for losses that occur on online shopping minimized by

the guarantee.

In the low after-sales service group, this study in-

dicates that risk perceptions have a negative and sig-

nificant effect on online shopping loyalty (β = -0.233,

C.R. = 2.04). This result indicates that aftersales ser-

vices provided by online stores do not reduce percep-

tions opportunities for losses that can be borne by the

customer. In the low after-sales service group, cus-

tomers consider that the aftersales service provided

by online stores is not a variable that significantly re-

duces potential losses. The results of this study sup-

port the fourth hypothesis (H4). ’

Based on the multi-group test, it identifies that the

influence of after-sales service moderated the effect of

risk perception variables on online shopping loyalty

in the high and low groups because the chi-square ta-

ble (χ2)> chi-square count difference (∆χ2) — after-

sales service as having a different influence on the ef-

fect of risk perception on online shopping loyalty.

The regression test results between the perceived

benefit variables and online shopping loyalty at high

after-sales service (β = 0.221, C.R. = 2.94) indicate

that perceived benefits have a positive and significant

effect on online shopping loyalty. This result shows

that the after-sales service guarantee facility improves

customer perceptions of the benefits received on on-

line shopping.

The regression test results between the perceived

benefit variables and online shopping loyalty at low

after-sales services (β = 0.181, C.R. = 2.19) indicate

that the perception of benefits has a positive and sig-

nificant effect on online shopping loyalty. The mod-

eration test results show that in high and low after-

sales services, the benefit perception variable influ-

ences online shopping loyalty. Based on the multi-

group test, it identifies that the influence of after-

sales service moderated the effect of benefit percep-

tion variables on online shopping loyalty in the high

and low groups because the chi-square table (χ2)>

the difference in chi-square count (∆χ2). The results

of this study support the fifth hypothesis (H5). After-

sales service is perceived to have a different influence

on high and low after-sales service groups, identify

from different standard coefficient quantities in the

high and low after-sales service group.

The results of the multi-group regression test in

the high after-sales service group indicate that the

trust variable does not affect online shopping loyalty

(β = 0.193, C.R. = 1.56. The results of this study

indicate that customers who have a positive percep-

tion of after-sales service, trust, reliability, the ability

to maintain customer privacy, complete information,

and the belief that the product does not affect cus-

tomer loyalty. In the group of customers who have a

positive perception of after-sales service have the per-

ception that after-sales service can guarantee trust in

online shopping.

The results of the multi-group regression test in

the low after-sales service group showed that the trust

variable affected online shopping loyalty (β =0.126,

C.R. = 2.52). The results of this research indicate

that trust affects customer loyalty. In the low after-

sales service group, trust is an essential variable in

customer loyalty.

Based on the multi-group test, that the effect of

after-sales service moderated the influence of the trust

variable on online shopping loyalty in the high and

low groups because the chi-square table (χ2)¿ the dif-

ference in chi-square count (∆χ2). The results of this

study support the sixth hypothesis (H6). After-sales

service as having a different influence on consumer

perceptions about the effect of trust in after-sales ser-

vices.

5 CONCLUSIONS

This study focuses on high and low after-sales ser-

vices, which in the previous study have not explained

yet. Before moderates test the level of after-sales

service online shopping loyalty, risk perception, per-

ceived benefits and trust affect online shopping loy-

alty.

After moderation test, in the high-after-sales ser-

vice groups, perceived benefits affect online shopping

loyalty, but perceived risk and trust not influence. In

the low after-sales service group, perceived benefits,

perceived risk and trust affect online shopping loyalty.

This research indicates that after-sales service

moderates online shopping loyalty.

The results of this study as a basis for online

stores in developing marketing strategies to increase

online shopping loyalty by designing stimuli that can

increase customer loyalty. The stimulusstimulus in

question is related to increasing online shopping loy-

alty, namely by considering the different levels of

after-sales service.

ICASESS 2019 - International Conference on Applied Science, Engineering and Social Science

68

Future research can develop this research model in

the context of loyalty to online shopping outside and

research outside the context of online shopping loy-

alty — subsequent research to improve generalization

of broader concepts.

This research model uses online shopping loyalty

as an object of research, so it has an impact on the lim-

itations of generalizing the concept of research, and

its application only in Yogyakarta. In connection with

these limitations, it is recommended to illustrate this

research model d at different locations and objects to

improve the generalization of the concept.

ACKNOWLEDGEMENTS

A Janabadra university grants partly funded this re-

search.

REFERENCES

Ahn, J. S. and Sohn, S. Y. (2009). Customer pattern search

for after-sales service in manufacturing. Expert Sys-

tems with Applications, 36(3):5371–5375.

Asugman, G., Johnson, J. L., and McCullough, J. (1997).

The role of after-sales service in international market-

ing. Journal of International Marketing, 5(4):11–28.

Barnes, S., Brown, K. W., Krusemark, E., Campbell, W. K.,

and Rogge, R. D. (2007). The role of mindfulness

in romantic relationship satisfaction and responses to

relationship stress. Journal of marital and family ther-

apy, 33(4):482–500.

Bohang, F. K. (2018). Berapa jumlah pengguna internet

indonesia. Kompas. Available online: https://tekno.

kompas. com/read/2018/02/22/16453177/berapa-

jumlah-pengguna-internet-indonesia (accessed on 22

September 2018).

Chien*, Y.-H. (2005). Determining optimal warranty pe-

riods from the seller’s perspective and optimal out-

of-warranty replacement age from the buyer’s per-

spective. International Journal of Systems Science,

36(10):631–637.

Egeln, L. S. and Joseph, J. A. (2012). Shopping cart aban-

donment in online shopping. Atlantic Marketing Jour-

nal, 1(1):1.

Forsythe, S. M. and Shi, B. (2003). Consumer patronage

and risk perceptions in internet shopping. Journal of

Business research, 56(11):867–875.

Gefen, D. (2002a). Customer loyalty in e-commerce. Jour-

nal of the association for information systems, 3(1):2.

Gefen, D. (2002b). Nurturing clients’ trust to encourage

engagement success during the customization of erp

systems. Omega, 30(4):287–299.

Gefen, D., Karahanna, E., and Straub, D. W. (2003). Trust

and tam in online shopping: An integrated model. MIS

quarterly, 27(1):51–90.

Horrigan, J. (2008). Online shopping: Convenient but

risky. Washington, DC: Pew Internet & American Life

Project. Retrieved November, 11:2011.

Kurnia, S. and Chien, J. (2003). The acceptance of the on-

line grocery shopping. In The 16th Bled Electronic

Commerce Conference, Bled, Slovenia. Citeseer.

Ladokun, I., Adeyemo, S., and Ogunleye, P. (2013). Impact

of after-sales service on consumer satisfaction and re-

tention: a study of lg electronics in ibadan, nigeria.

Journal of Business and Management, 11(4):54–58.

Lim, Y. J., Osman, A., Salahuddin, S. N., Romle, A. R.,

and Abdullah, S. (2016). Factors influencing online

shopping behavior: the mediating role of purchase in-

tention. Procedia economics and finance, 35(5):401–

410.

Liu, T.-H. (2012). Effect of e-service quality on customer

online repurchase intentions. Lynn University.

Loomba, A. P. (1998). Product distribution and service sup-

port strategy linkages. International Journal of Phys-

ical Distribution & Logistics Management.

Mayer, R. C., Davis, J. H., and Schoorman, F. D. (1995). An

integrative model of organizational trust. Academy of

management review, 20(3):709–734.

Nam, M.-W. (2003). Predicting intention to use the internet

information search and shopping apparel among ko-

rean female computer users. International Journal of

Human Ecology, 4(2):39–53.

Sigala, M., Rigopoulou, I. D., Chaniotakis, I. E., Lymper-

opoulos, C., and Siomkos, G. I. (2008). After-sales

service quality as an antecedent of customer satisfac-

tion. Managing Service Quality: An International

Journal.

Sweeny, J., Soutar, G., and Johnson, L. W. (1999). The

role of perceived risk in the quality-value relationship.

Journal of Consumer Research, 20(September):271–

80.

Teo, T. S. (2002). Attitudes toward online shopping and

the internet. Behaviour & Information Technology,

21(4):259–271.

Van der Heijden, H., Verhagen, T., and Creemers, M.

(2003). Understanding online purchase intentions:

contributions from technology and trust perspectives.

European journal of information systems, 12(1):41–

48.

Yannopoulos, P. (2011). Impact of the internet on marketing

strategy formulation. International Journal of Busi-

ness and Social Science, 2(18).

The Role of After-sales Service for Online Shopping Loyalty

69