Model of Leadership Style on Job Satisfaction in Internal Audit Team

at Regional Inspectorates with Locus of Control and Cognitive Style

as Moderated Variable

Nurzaimah, Firman Syarif

Faculty of Economics, Universitas Sumatera Utara, Indonesia

Keywords: Leadership Style, Locus of Control, Cognitive Style, Job Satisfaction.

Abstract: Purpose: The purpose of this study is the identification and development of good practices in governance of

the Regional Inspectorate, to obtain empirical evidence of how much leadership style in the Regional

Inspectorate audit team, how big is the model of leadership style interaction with the Locus of control in the

Regional Inspectorate audit team, how large model of leadership style interaction with cognitive style in the

Regional Inspectorate audit team affect job satisfaction.

Findings: With its leadership, the team leader is also expected to be able to create cooperative interactions

between team members in achieving the stated assignment goals and can also encourage the awareness and

responsibility of members of the Regional Inspectorate (Internal Audit) team in conducting audits.

Practical Implications: The success of an audit assignment depends very much on the personnel

incorporated in an audit team. To optimize the work of the audit team, the role of the team leader is needed.

Originality/Value: The virtue of this research is the input and consideration in carrying out the preparation

of the Regional Inspectorate audit team, and as the role of researchers in developing theories in the field of

accounting and auditing especially relating to the behavior of the Regional Inspectorate.

1 INTRODUCTION

The success of an audit assignment is highly

dependent on the personnel who are members of an

audit team. To optimize the work of the audit team,

the role of the team leader is needed. With his

leadership, the team leader is expected to create

cooperative interactions between team members in

achieving the stated assignment goals and can also

encourage the awareness and responsibility of the

members of the Regional Inspectorate (Internal

Auditor) team in conducting audits.

Effective leadership must be able to provide

direction to the efforts of team members in achieving

the objectives of the assignment. As is known, the

audit team consists of personnel who each have

different individual goals. Without leadership, the

relationship between individual goals and assignment

goals may become out of harmony. As a result, team

members work to achieve their personal goals.

Meanwhile, the purpose of the assignment was

neglected.

Leadership is a process with various ways of

influencing people or groups of people to achieve

common goals. Leadership is closely related to the

work to be completed (task function) and the

cohesiveness of the people they lead (Suwandi,

1999). Thus in an audit assignment, the influence of

team leaders can be seen from the attitude of team

members to the work they do. One such attitude is

the job satisfaction of team members.

Regional autonomy (Law No.22 of 1999) means

that it has transferred most of the authority that was

in the central government to be handed over to the

autonomous region, so that the autonomous regional

government can more quickly respond to the

demands of local communities by following their

capabilities. Because the authority to make policies

(Perda) is fully the authority of autonomous regions,

with regional autonomy the implementation of

general tasks of government and development will be

able to run faster and be of higher quality. The

success of the implementation of regional autonomy

is highly dependent on the ability of regional finance

(PAD), human resources owned by the region, and

the ability of the region to develop all the potential

that exists in the autonomous region. Problems Faced

The implementation of the decentralization and

Nurzaimah, . and Syarif, F.

Model of Leadership Style on Job Satisfaction in Internal Audit Team at Regional Inspectorates with Locus of Control and Cognitive Style as Moderated Variable.

DOI: 10.5220/0009205303690385

In Proceedings of the 2nd Economics and Business International Conference (EBIC 2019) - Economics and Business in Industrial Revolution 4.0, pages 369-385

ISBN: 978-989-758-498-5

Copyright

c

2021 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

369

regional autonomy policies which have been running

for nine years, have experienced much progress.

However, it was realized that the journey to achieve

the objectives of the implementation of

decentralization and regional autonomy was still

experiencing many problems. Some of the main

problems felt by the government are, among others,

the aspects of structuring the laws and regulations,

structuring regional government institutions,

enhancing the quality and capacity of local

government officials, processing regional finances,

implementing inter-regional cooperation, structuring

new autonomous (DOB).

Cognitive style is an interesting topic because

common sense can be understood that cognitive style

or personality type is an important factor in

responding to one's leadership style, but research on

that topic is still limited. Some research has been

done, but not directly related to his leadership, such

as Blaylock and Rees (Kinicki, 2001) and Cheng et.

Al (2003).

2 LITERATURE REVIEW

2.1 Regional Autonomy and

Decentralization

The development of public sector accounting,

especially in Indonesia, has been accelerating with a

new era in the implementation of regional autonomy

and fiscal decentralization. One of the MPR Decrees

is MPR Decree Number XV / MPR / 1998

concerning "Implementation of Regional Autonomy;

Regulation, Distribution, and Utilization of

Equitable National Resources and Central and

Regional Financial Balances within the framework

of the Unitary State of the Republic of Indonesia,

constituting the legal basis for the issuance of Law

No. 22 of 1999 concerning Fiscal Balance between

Central and Regional Governments as a basis for the

implementation of regional autonomy.

The second main mission of the law is

decentralization. Decentralization means not only

the transfer of authority from the central government

to the lower government but also the transfer of

some government authority to the private sector in

the form of privatization.

Theoretically, decentralization is expected to

produce two tangible benefits, namely:

1. Encourage increased participation, initiative, and

creativity of the community in development, and

encourage the distribution of development

outcomes (justice) in all regions by utilizing the

resources and potential available in each region.

2. Second, improving the allocation of productive

resources by shifting the role of public decision

making to the lowest level of government that

has the most complete information (Mardiasmo,

2005).

The results of Hutler and Shah's research (1998)

in Mardiasmo (2005) in 80 countries show that

decentralization has a positive correlation with the

quality of government. Since the enactment of

regional autonomy on January 1, 2001, the State of

Indonesia has experienced many significant changes.

The enactment of regional autonomy in 2001 caused

the bureaucracy to spearhead the implementation of

government and the key to the success of regional

development (Erika Revida, 2007). This is stated in

Law No.22/1999 concerning Regional Government

and Law No.25/1999 concerning Financial Balance

between Central and Regional Governments.

However, the implementation of regional autonomy

has entered a new development in 2004. This is

evidenced by the issuance of a new law on regional

autonomy, namely Law No.32/2004 concerning

Regional Government and Law No.33/2004

concerning Financial Balance between the Central

Government and Local Government. With the

passage of these two laws, the two previous laws

namely Law No.22/1999 and Law No.25/1999 have

been deleted.

With the enactment of regional autonomy in

2001, hopes of the government and all levels of

society are greater, that is, they want better

government performance. Because, with the

enactment of regional autonomy, the implementation

of government activities no longer has to be based on

the central government, but rather by each region.

According to Law No.32/2004 (2004: 4), "Regional

autonomy is the right, authority and obligation of

autonomous regions to regulate and manage their

government affairs and the interests of local

communities by statutory regulations". This means

that the regional government has the right to make

decisions and policies according to what is happening

in the region. Thus, the regional government will get

closer to the community because in this case, the

local government will deal directly with the

community as an extension of the government (Erika

Revida, 2007).

Besides, the implementation of regional

autonomy gives rise to decentralization. According to

Law No.32/004 (2004: 5), "Decentralization is the

transfer of governmental authority by the

Government to autonomous regions to regulate and

EBIC 2019 - Economics and Business International Conference 2019

370

administer government affairs within the Unitary

State of the Republic of Indonesia" system. This

transfer of authority results in responsibilities that are

centered on regional government.

But in its implementation still found many

deficiencies. Theories and laws concerning regional

autonomy are not by their implementation. This is

indicated by the existence of cases of corruption,

collusion and nepotism, also known as KKN and

other cases. Even after the implementation of

regional autonomy, the number of cases found has

even increased. This shows the low quality of public

services that causes a decrease in public trust in

government performance.

Research conducted by Dwiyanto, et al (2002)

concluded that the performance of public

bureaucratic services in the region is still low, the

practice of KKN in government and public services

is still ongoing, even with an ever-expanding scale

and actors, people's desire to enjoy efficient,

responsive, accountable public services is far from

reality. Regional autonomy is synonymous with

demands for accountability, good governance, and so

on. A good government is a government that can be

honestly responsible for the trust of its people

(Roesyanto, 2007 1). So that a good Audit Team

Leadership Style Model is needed to improve the

Government's performance.

2.2 Leadership Style

Leadership is one of the most popular topics and can

be seen from any angle it will be watched. From

time to time leadership is a concern for humans.

Some argue that leadership is as old as human

history. Human leadership is needed, because of

certain limitations and advantages in humans. On the

one hand, humans have limited ability to lead, on the

other hand, some people have an excess of ability to

lead. This is where the need for leaders and

leadership arises.

According to Robin (1951) in Toha (2007)

leadership can be interpreted as the exercise of

authority and decision making. Meanwhile,

according to acting, Kemphill (1954) interpreted an

initiative to produce a consistent pattern to find a

solution from a common problem. Furthermore,

George R. Terry formulated that leadership is an

activity to influence people to be directed towards

achieving organizational goals.

The concepts of leadership and power translation

from power have generated an interesting interest to

be discussed throughout the evolutionary growth of

management thinking. The concept of power is very

close to the concept of leadership. Power is a means

for management to influence the behavior of

followers (Stogdill, 1982).

Some leadership styles that influence the

behavior of many of his followers. At any time if

someone is trying to influence the behavior of

others, it has been explained in advance that such an

activity has involved someone in leadership

activities If the leadership occurs in a particular

organization, and the person needs to develop staff

and build a motivational climate that results in a

level of productivity high, then the person is

displaced need to think about his leadership style.

According to Toha (2007) leadership style is the

norm of behavior used by someone when the person

is trying to influence the behavior of others as he

sees it. In this case, the attempt to harmonize

perceptions among people that will influence

behavior with those whose behavior will be

influenced becomes very important.

From the above definition, leadership can be

concluded as the ability possessed by someone to

influence others to work to achieve goals. According

to Maridjo (2001), there are five implications of the

definition of leadership. First, leadership involves

other people, namely subordinates or followers.

With the willingness of subordinates or followers to

receive direction from superiors, group members

have helped strengthen the position of leader and

allow the leadership process to run well, without

people being led, the overall quality of the leader

becomes irrelevant. Second, leadership involves the

distribution of power between leaders and

subordinates or followers. The leader becomes more

powerful than subordinates or followers. Third,

leaders can easily influence subordinates or

followers but subordinates or followers find it

difficult to influence their leaders. Fourth, leaders

can instill values to subordinates, but subordinates

do not easily do the same to their leaders. Fifth,

leadership is the art or process of influencing others.

Because leadership is an art, its effectiveness cannot

be formulated but depends on the situation. In the

audit context, leadership can be practiced at different

levels, reflecting the hierarchical structure in the

audit organization or institution.

2.3 Job Satisfaction

Job satisfaction shows how much subordinates like

their work. Locke (176) in Greenberg and Baron,

2003) defines job satisfaction as an individual's

positive or negative attitude toward work. By

definition, job satisfaction reflects a person's feelings

Model of Leadership Style on Job Satisfaction in Internal Audit Team at Regional Inspectorates with Locus of Control and Cognitive Style

as Moderated Variable

371

towards his job. This can be seen in the subordinate's

positive attitude towards work and everything

encountered in the work environment.

Organizational factors and job satisfaction. One

of the most important aspects of job satisfaction in

organizations is the reward system. Job satisfaction

will increase if subordinates perceive a fair and

appropriate reward system. Further aspects of

organizational policies will increase innate

satisfaction if subordinates participate in

determining policies regarding responsibility and

authority. With this involvement, subordinates will

truly carry out their duties because the policy is a

joint decision. Finally, the quality of supervision.

Subordinates who expect supervision to act fairly

and competently because this will increase their job

satisfaction.

Job factors, spatial planning, and job satisfaction.

Job satisfaction will increase if subordinates are

given mentally challenging jobs, varied jobs, and

pleasant social interactions. Another specific aspect

of the job is the job characteristic model which

includes diverse expertise, job identity, level of

importance of a job, autonomy, and feedback.

Related to workspace layout, aspects that affect job

satisfaction include the number of subordinates in

one room, room lighting, distance between tables,

temperature, noise, and water quality. Finally, the

social environment includes coworkers. Job

satisfaction will increase if co-workers are mutually

helpful and friendly.

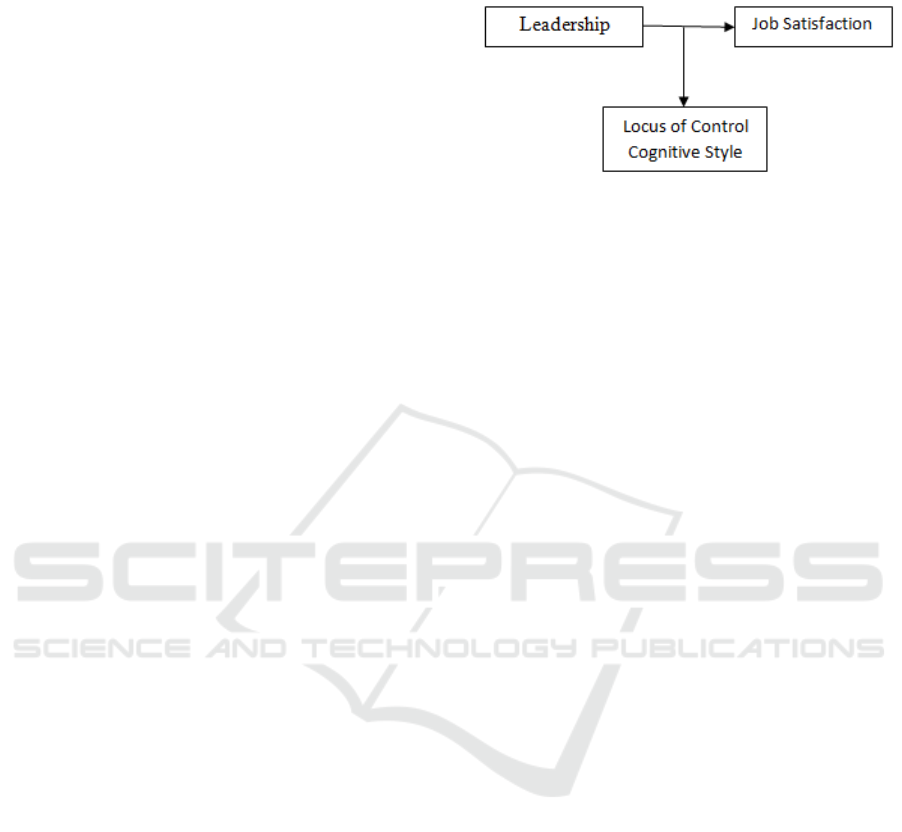

2.4 Framework for Thinking

The proposed research framework is to use the

framework proposed by Evans (1970) and House

(1971). The framework shows that the leadership

style interacts with some optional variables such as

the ability and personality of subordinates, the

structure of tasks and the authorization system in the

organization. Situational variables that the

researchers propose are locus of control and

cognitive style variables. The research framework in

this study is presented in figure 1.

3 RESEARCH MODEL

Figure 1.

3.1 Hypothesis Development

This study aims to examine how leadership styles

and individual characteristics affect job satisfaction

in audit teams. For this reason, the researcher

proposes the following hypotheses:

3.1.1 Effect of Leadership Style on Job

Satisfaction

An effective leader can influence group

performance, satisfaction, and motivation

(Anonymous, 2005). In the Path-Goal model, leaders

are categorized into 4 leadership styles, namely

directives. supportive participative, and oriented

orientation. Several previous studies have shown

that leadership style influences job satisfaction, such

as Filley, et. Al (1976); Schriesheim and DeNisi

(1981, in Luthans 1995); Weed, et al (1976, in Pratt

and Jiambalvo 1982), Pratt and Jiambalvo (1982),

and Keller (1989) Filley et al. (1979) put forward

several studies as follows: first, a study of 7

organizations and found that directive leadership

style interacts positively with job satisfaction and

expectations of subordinates who work on

ambiguous tasks and interacts negatively with job

satisfaction and expectations of subordinates who

work in the clear task; second, a study of 10

different employee samples and found that

supportive leadership styles interact positively with

job satisfaction in subordinates who are in a state of

work pressure, frustration, or unsatisfactory work;

third, research in the manufacturing industry shows

that in jobs that are unstructured and involve

selfishness, employees achieves high satisfaction

with participative leadership style; fourth, a study of

3 different organizations found that subordinates

who carry out unstructured and ambiguous tasks,

will achieve high satisfaction with achievement

leadership style.

Schriesheim and DeNisi (1981) found that the

higher the structure of work carried out by

EBIC 2019 - Economics and Business International Conference 2019

372

subordinates, the higher the relationship between

supportive leadership style and job satisfaction.

Furthermore, the higher the job structure, the lower

the relationship between directive leadership style

and job satisfaction. Weed, et. al (1976) uses task

structure, task ambiguity, and subordinate

authoritarianism as moderating variables. This

research proves that subordinates will achieve higher

job satisfaction with leadership behavior oriented to

social relations.

Jiambalvo and Pratt (1982) examined the

relationship between partner manager behavior with

job satisfaction and the motivation of assistant staff

with the Path-Goal model of consideration and

initiating leadership styles. This research was

conducted on 61 assistant staff from 37 audit teams

on two Big Eight KAPs and hypothesis testing was

performed with ANOVA. The results showed that is

a significant interaction effect between consideration

behavior and task complexity. The consideration

leadership style satisfies the assistant in low task

complexity. While the interaction between initiating

structure behavior and task complexity is not

significant, because initiating structure behavior can

be used in high task complexity.

Research conducted by Keller (1989) uses the

Path-Goal model and the need for clarity of

information as a moderating variable for 477

professional employees from four organizations

which are engaged in research and development.

This study shows that the need for clarity of

information accounts has a moderate effect on the

relationship of initiating structure with job

satisfaction so that the higher the need for clarity

between subordinates, the stronger the relationship

between initiating structure and job satisfaction

Based on literature review and the results of several

previous studies.

This research will try to analyze the influence of

leadership style on job satisfaction in a more specific

scope, namely in the audit team. Therefore, the

satisfaction proposed is as follows:

H1: The leadership model of the audit team

leader significantly influences the job satisfaction

of team members.

3.1.2 The Effect of Leadership Model on Job

Satisfaction with Locus of Control as

Moderating Variables

Locus of control tends to be an internal or external

direction, when internal tend to feel things are more

controlled by the environment outside of themselves.

Several studies have tried to see how the locus of

control interacts with leadership styles in influencing

job satisfaction, such as Janto (1994) and Nugroho

(1996) in Koemiati (1998); Mitchell et al (1975) in

Hughes et al, 199: Hening (1998) and Basri (2000).

Janto (1994) conducted a study to look at locus

of control with a contingency approach to job

satisfaction. This research was conducted at the

banking industry in Yogyakarta using a sample of

middle and line managers. The results of this study

indicate that a participative leadership style will

increase subordinate work extinction when

compared with directive and locus of control

leadership styles do not moderate the influence of

leader behavior with job satisfaction. While

Nugroho (1996) examined the influence of

leadership roles on subordinate satisfaction at PT.

Semen Cibinong by taking a sample of employees at

the level of the Division Head and employees up to

three levels below the Division Head The results of

the study indicate that the role of the leader who

tends to be more participatory will increase

subordinate job satisfaction compared to the

directive level. Besides, this research did not

succeed in proving the influence between the

interaction of leadership roles and locus of control

with subordinate job satisfaction.

Mitchell et. al (1975) found that subordinates

with internal locus of control would feel more job

satisfaction with participative leadership style while

external locus of control with directive leadership

style. Basri (2000) examines the relationship

between leaders and subordinates in service and

manufacturing companies with the Otley and Pierce

(1995) model, namely consideration and initiating

structure as well as locus of control and need

achievement as moderating variables. The results of

his study indicate that there are differences in the

influence of the inclusion of dimensions,

considerations as moderating variables. Influence

between leadership styles. Besides, the structure of

the initiative for job satisfaction has not changed.

Likewise, the locus of control does not affect the

relationship between leadership style and job

satisfaction. However, need achievement influences

the relationship between leadership style and job

satisfaction. At the time of high consideration, there

was no effect on job satisfaction, while at the time of

low consideration job satisfaction differed between

the need for high and low achievement.

Simultaneous locus of control and need achievement

do not influence the influence of leadership style on

job satisfaction.

Several other studies on locus of control

conducted by Hyatt and Prawit (2001) examine the

Model of Leadership Style on Job Satisfaction in Internal Audit Team at Regional Inspectorates with Locus of Control and Cognitive Style

as Moderated Variable

373

suitability between the use of structured audit

technology and locus of control on performance in

Big-six public accounting firms. The results show

that auditors with internal locus of control achieve

high performance in unstructured KAP’s.

Tsui examines the effect of economic pressure

and locus of control on ethical auditors in auditing

conflict situations. This research was conducted on

80 auditors in KAP Big Six and Non-Big Six. The

results showed that the auditor with locus of control

(convinced that the impact was a consequence of

fate) would respond more ethically and

independently if the audit fees received were very

significant related to the microeconomic

consequences of losing clients and lawsuits. While

Brownell (1982) examines the relationship between

budgetary participation and job satisfaction and

performance that is moderated by the locus of

control. This research was conducted on 48 managers

in manufacturing companies. The results show that

the interaction between participation in budgeting

and job satisfaction at the research stage and locus of

control significantly influences performance and job

satisfaction in research and surveys.

Based on the theoretical basis and the various

results of previous studies, the proposed hypothesis

is as follows:

H2: The interaction of leadership style with locus

of control has a significant effect on job

satisfaction of team members.

3.1.3 The Effect of Leadership Style on Job

Satisfaction with Cognitive Style as

Moderating Variables

Cognitive Style is a personality in gathering

information and then making decisions. Jung (192)

in Kreitner and Kinicki, 2001) divides cognitive

style into four categories, namely sensation/thinking

(ST), intuition/thinking (IT), sensation/feeling (SF),

and intuition/feeling (IF). Some research on

cognitive style has been done by Blaylock and Rees,

1984; Gul, 1984 in Kiniciki (2001), Mills (1996);

Cheng et. Al (2003); and Hough and Ogilvie (2005).

Blaylock and Rees (1984) asked cognitive style

for 50 MBA students and the results showed that

different cognitive styles influence the use of

information in strategic planning issues. Besides,

people who have different cognitive styles prefer

certain types of work, such as those who emphasize

intuition prefer a career in psychology, advertising,

teaching, and the arts. Research conducted by Gul

(1984) shows that individuals who make decisions

using the thinking approach have greater motivation

and quality of work than the feeding approach.

Besides, people with sensations will have a higher

level of job satisfaction compared to intuition.

Cheng et. Al. (2003) conducted an experiment

using the MBTI instrument. This study examines

differences in cognitive style on the quality of

performance of dyads decisions for complex

decision making. The results show that decision

quality significantly increases cognitive dyads that

differ beyond sensor dyads homogeneous. Different

quality differences are not observed between

homogeneous intuitive dyads. Mills (1996)

examined the effect of cognitive style on decision

making on the function of internal auditors. This

research was conducted on 51 auditors from two Big

Six Public Accountant Firms using FI-Fixed,

Fimobile, FD-fixed, FD-mobile. The results showed

that FD / FI had no significant effect.

Flowchart to achieve that goal. The leadership

team will have one of the most prominent styles of

the four styles of Path-goal model leadership that is

directive, participative, supportive, and

achievement-oriented. To measure leadership style,

the instrument used is a questionnaire developed by

Timpe (1987).

This questionnaire aims to assess trends in

leadership style on the audit team so it can be seen

whether the team leader is inclined directive,

participative, supportive, or achievement-oriented.

This model has also been used by previous research

Hening (1998), which in his research at the batik

maker company added factor locus of control as a

moderating variable.The Questionnaire used in this

study consisted of 24 questions by using a four-point

Likert scale, those who strongly disagree are given 1

point to strongly agree with 4 points.

Based on the theoretical basis and the various

results of previous studies, the proposed hypothesis

is as follows:

H3: The interaction of leadership style with

cognitive style has a significant effect on job

satisfaction of team members.

3.2 Locus of Control

Locus of control is the tendency of each team

member towards internal or external. If it’s an

internal tendency, a team member relies more on

personal abilities. Therefore, success obtained is the

result of his ability while failure is a result of his

inability. If someone tends to be external, he will

more consider the environment around him is too

difficult to change and everything is more controlled

by the environment outside himself. To measure the

EBIC 2019 - Economics and Business International Conference 2019

374

locus of control, the instrument used in this study is

the Work Locus of Control Scale (WLCS) scale

developed by Spector (1988), taking into account the

WLCS has advantages in terms of measurements

that are more specific to the lotus of control. This

WLCS has also been used by Basri (2000) in his

research which examines the relationship between

superiors and subordinates in service and

manufacturing companies using locus of control as

one of the moderating variables. WLCS consists of

16 questions using a four-point Likert scale.

3.3 Cognitive Style

Cognitive style is the personality of team members

in gathering information and then making decisions.

Team members will have one of the most prominent

personalities of the four personality types, namely

sensation/thinking (ST), intuition/thinking (IT),

sensation/feeling (SF) and intuition/feeling (IF).

To measure cognitive style, the instrument used

was the Myer-Briggs Type Indicator (MBTI) model

developed by Bringgs (1980). Currently, MBTI has

been widely used for various personality studies in

the education and business environment (Kreitner

and Kinicki, 2001). The MBT questionnaire

consisted of 16 questions using the answer choices.

3.4 Job Satisfaction

Job satisfaction is a condition where team members

get a level of satisfaction in the implementation of

the assignment, such as the existence of awards,

relationships among team members, and supervision.

To measure work satisfaction, the instrument

used was the Minnesota Satisfaction Questionnaire

(MSQ) model developed by Weiss et. al (1967). The

Questionnaire material covers 7 aspects, namely

aspects of the cost of assignment, self-development

for a career, leadership style, leader policy,

relationships with colleagues, work environment and

loyalty. The questionnaire consisted of 21 questions

using a four-point Likert scale.

4 DATA ANALYSIS AND

DISCUSSION

4.1 General Description of the

Respondent

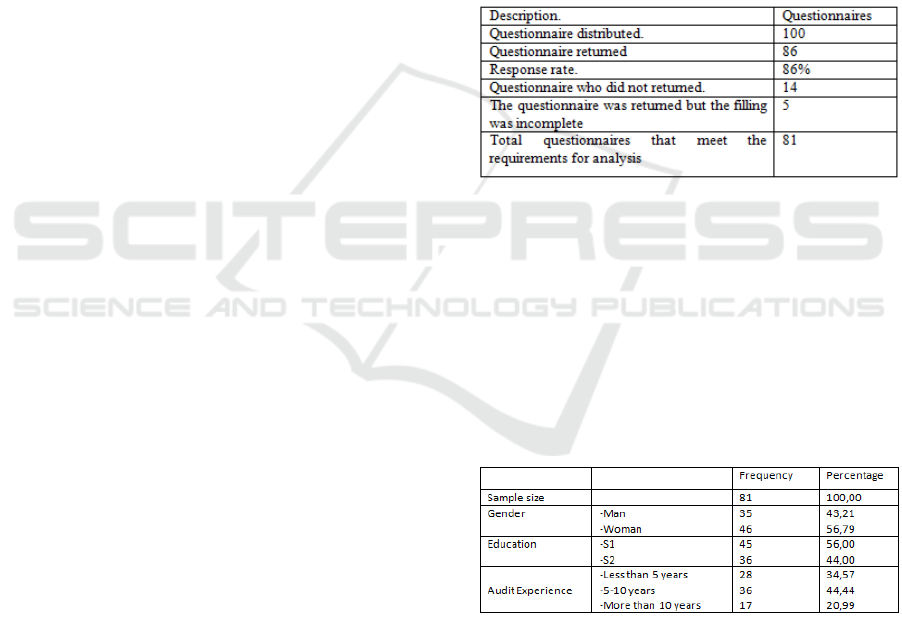

The data collection process was carried out from the

end of July to the beginning of August 2010. Data

collection can be done by distributing questionnaires

to respondents directly or collected through certain

people.

The questionnaire was distributed to Regional

Inspectorates (Internal Auditors) to be filled out and

returned directly. Questionnaires were distributed to

the Inspectorate District. Langkat, Deli Serdang, and

Serdang Bedagai were 100 questionnaires.

Questionnaires were distributed to Kab. A total of 30

questionnaires, Deli Serdang 35, and Serdang

Bedagai as many as 35 questionnaires. Of the 100

questionnaires distributed, 86 were returned (86%),

and only 81 questionnaires could be processed.

The following are the results of the assessment

of questionnaire distribution.

Table 4.1. Questionnaire distribution results

Source: primary data processed

Table 4.2. Review the general description of

respondents who are the subjects in this study.

Profile of respondents consisted of gender,

education, position, auditor functional, and audit

experience. In general, respondents were dominated

by women (56.79%) with S1 (56%) and S2

education (44%), and audit experience ranged from

5-10 years to 44.44%.

Table 4.2. Review the General Description of Respondents

4.2 Validity Test and Reliability

This research use 4 questionnaire which has been

standardized. the composition questionnaire is :

1. Questionnaire of leadership style (Timple) *24

question

2. Locus of control questionnaire (Spector) *16

question

Model of Leadership Style on Job Satisfaction in Internal Audit Team at Regional Inspectorates with Locus of Control and Cognitive Style

as Moderated Variable

375

3. Questionnaier of cognitive style (Myers briggs

type indicator) *16 question

4. Questionnaire of job satisfaction (Minnesota

satisfaction questionnaire) *20 question

Testing the validity of the question items is done

using the Pearson Product Moment correlation

method. Processing is done by correlating the scores

obtained for each question item with the item scores.

The total item score is the value obtained from the

sum of the question items. Based on SPSS output

version 15 the value of the correlation coefficient (r)

can be seen from each item against the total score.

To test whether the correlation is significant or not,

the results of the r count test can be compared r table

with a significance level of at least 95% From the r

table data, N = 81 with a level of 95%, then the r

table is 0.2159. Or it can be seen from the SPSS

output which automatically gives a two-star (**) if

the correlation coefficient is significant at the 1%

level and one star (*) if the correlation coefficient is

significant at the 5% level.

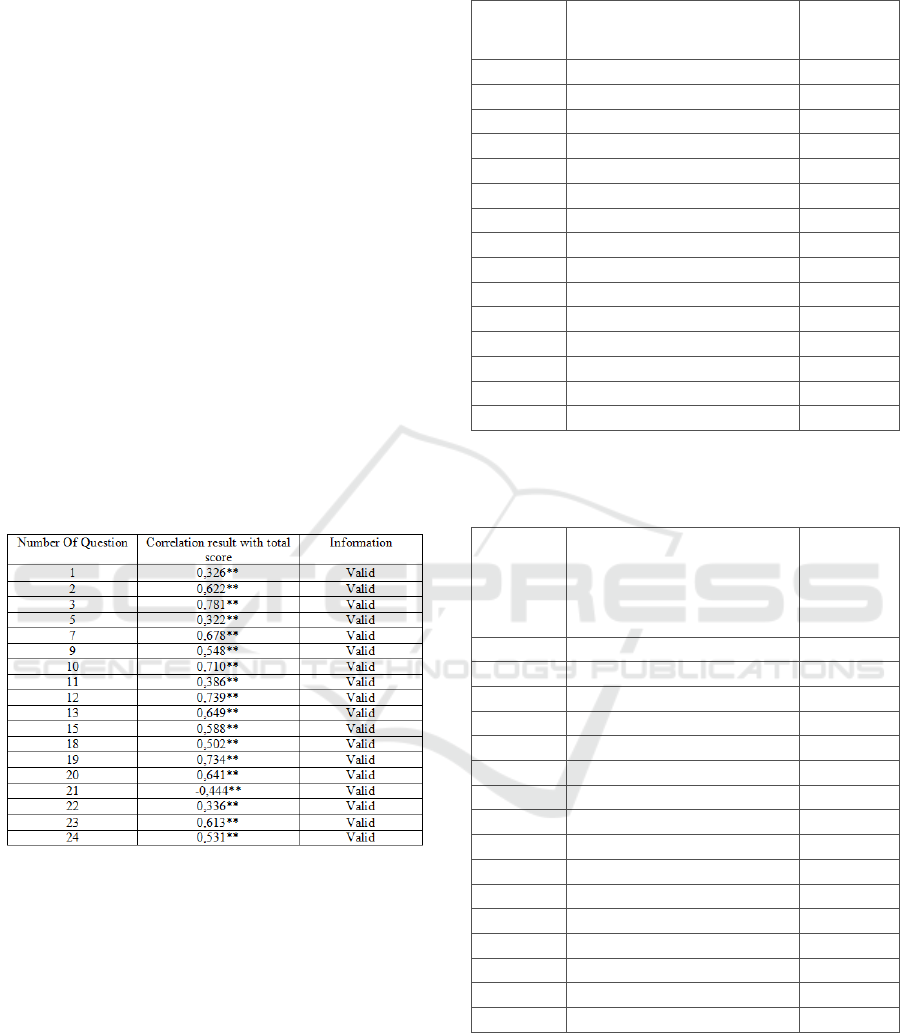

Table 4.3. Validity Leadership Style Test Result

The results of testing of leadership style items

indicate that there are 19 significant items

(considered valid), while 5 items (item number 6, 8,

14, 16, and17) are not significant (invalid) The five

invalid items are excluded from the original data and

then the correlation test is recalculated. The results

show that the question items are valid, but there is

still 1 item Invalid questions, initemnumber 4. After

being recalculated by issuingitemnumber 4, the

remaining question items all become valid. The test

results for the leadership style items are presented in

Table 4.3.

Table 4.4. Validity test results – Locus of Control

No.

Question

Correlation results with total

scores

Information

1 0,332** Vali

d

2 0,252** Vali

d

3 0,221** Vali

d

4 0,240** Vali

d

5 0,286** Vali

d

6 0,427** Vali

d

7 0,518** Vali

d

8 0,574** Vali

d

9 0,355** Vali

d

10 0,586** Vali

d

11 0,439** Vali

d

12 0,501** Vali

d

13 0,269** Vali

d

14 0,489** Vali

d

16 0,481** Vali

d

Source of data processed in 2010

**Significant correlation at the level of 1% (2- tailed)

Table 4.5. Validity test results - Work Decisions

No.

Question

Correlation results with total

scores

Information

1 0,392** Vali

d

2 0,309** Vali

d

3 0,403** Vali

d

4 0,592** Vali

d

6 0,666** Vali

d

7 0,574** Vali

d

8 0,573** Vali

d

9 0,641** Vali

d

12 0,375** Vali

d

13 0,719** Vali

d

14 0,644** Vali

d

15 0,627** Vali

d

16 0,605** Vali

d

17 0,321** Vali

d

18 0,659** Vali

d

20 0,496** Vali

d

The results of tests on work satisfaction items

indicate that there are 16 significant items (which

are considered valid) and the remaining 4 items

(items number 5, 10, 11, and 19) not significant

(invalid). The invalid items are excluded from the

original data and then the correlation test is

recalculated. The result is the rest of the items all

EBIC 2019 - Economics and Business International Conference 2019

376

become valid. The test results for the job satisfaction

items are presented in Table 4.5.

Table 4.6. Summary of Reliability Test Results

Variable name Cronbach Alpha Criteria

Leadership Style 0,8221 Good

Locus of Control 0,6182 Acceptable

Job satisfaction 0,8294 Good

Data source: Data processed (2010)

After the questionnaire as a measuring

instrument proved to be valid, testing was then

carried out on the reliability of the question items

using the Cronbach alpha technique. The results of

the calculation of the reliability performed on item

questions in each variable are job satisfaction (Y),

leadership style (x9 and locus of control (X2)), with

the help of the SPSS version 15 program obtained

the following results: Cronbach alpha for leadership

style questionnaire for 0, 8221, locus of control was

0.6182 and job satisfaction was 0.8294. Referring to

Sckaran (2003), leadership style reliability was

categorized as good, locus of control reliability was

categorized as acceptable and job satisfaction

reliability was categorized well Based on the results

of the reliability test, it could be explained that the

questionnaire used to measure all the variables used

in this study is reliable even though it has different

reliability criteria Summary of reliability testing is

presented in table 4.6.

The results of the questionnaire about cognitive

style were not tested for data quality. The

questionnaire was adopted directly from Kreitner

and Kinicki (2001) without developing questions.

The questionnaire was designed not on a Likert

scale, but each number consisted of 2 question items

A or B, with a score of 1 and 0, so that it was not

possible to conduct a data quality test as was done in

the leadership style. locus of control, and job

satisfaction. Full test results can be seen in Appendix

2 for the validity test and Attachment 3 for the

reliability test.

4.3 Multicollinearity

Interpretation of the multiple regression equation

implicitly depends on the assumption that the

independent variables in the equation are not

correlated with each other. Regression coefficients

are usually interpreted as a measure of changes in

the dependent variable if one of the independent

variables rises by one unit and all other independent

variables are considered fixed. However, this

interpretation is incorrect if there is

multicollinearity, i.e.

Linear relationship between independent

variables (Chatterjee and Price, 1977). To detect

multicollinearity, this study uses correlation matrix

analysis. Regression models are declared free of

multicollinearity if there is no correlation value

above 0.90.

Table 4.7. Coefficient Correlations (a)

ACH DIR SUPP PART

Correlations ACH

DIR

SUPP

PART

1,000

-,262

-,388

-,299

-,262

1,000

-,316

-,288

-,388

-,316

1,000

-,538

-,299

-,288

-,538

1,000

a. Dependent Variable: SATISFIED

The test results show that only supporting

variables that have a high enough correlation with

participatory with a correlation level of -0,538 or

around 53.80%. Because this correlation is still

below 95%, this means there is no multicollinearity

between variables in the Regression Model I.

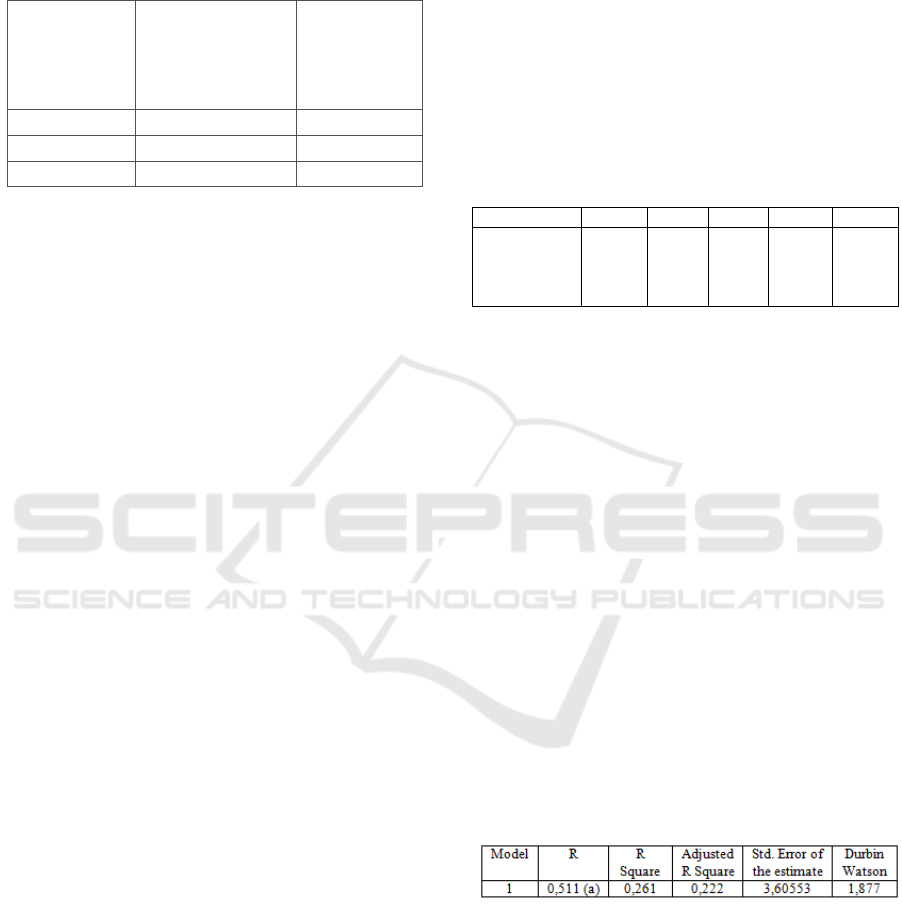

4.4 Autocorrelation

An autocorrelation test is performed to find out

whether the regression model was found a

correlation between residuals (confounding errors) at

different observations of time or individuals.

Generally, many cases of autocorrelation occur in

time series. To detect the presence of

autocorrelation, this study used the Durbin-Watson

(DW) test. The regression model is declared free

from autocorrelation if the DW number is between

(du) and (4-du) in the Durbin-Watson table.

Table 4.8. Model Summary (b)

a. Predictors: (Constant), ACH, DIR, SUPP, PART

b. Dependent Variable: SATISFIED

With the number of samples = 81 and the

number of variables = 4, the values of du and dl in

each table are du = 1,743 and dl = 1,534, so 4-dl =

2,466 and 4-du = 2m257. The test results show the

Durbin-Watson (DW) rate of 1.877. The number is

between 1,743 (du) and 2,257 (4-du). This means

that there is no autocorrelation in the Regression

Model I.

Model of Leadership Style on Job Satisfaction in Internal Audit Team at Regional Inspectorates with Locus of Control and Cognitive Style

as Moderated Variable

377

4.5 Heteroscedasticity

Heteroscedasticity test is performed to find out

whether absolute residual variation is the same or

not the same for all observations. To detect

heteroscedasticity, this study tests the Glejster test.

The regression model is declared free of

heteroscedasticity if the independent variable is not

statistically significant affecting the dependent

variable.

Table 4.9. Coefficients

a

The test results show that there are no

statistically significant independent variables that

affect the dependent variable absolute value. This

can be seen from the significance level above 0.50.

This means that the regression model does not

contain heteroscedasticity.

4.6 Normality Test

Normality test is done to test whether the residuals

in the regression model have a normal distribution.

To test normality, this study uses the Kolmogorov-

Smirnov (K-S) non-parametric statistical test. If the

significant value in the one-sample K-S test table is

above 0.05, this shows that the residual data has a

normal distribution.

The test results show the value of Kolmogorov-

Smirnov is equal to 0.828 at the significant 0.499.

This is good enough to estimate variations in team

member satisfaction caused by the leadership style

of the team leader in an audit team.

5 HYPOTHESIS TESTING

This research will test the four hypotheses that have

been proposed in Chapter II previously by using the

regression model that was compiled in Chapter III.

Testing this hypothesis using SPSS version 15.

5.1 Hypothesis Testing 1

The first hypothesis aims to test whether the

leadership style of the regional inspectorate team

leader significantly influences the job satisfaction of

team members. The data used in testing the first

hypothesis are Leadership Style and Job Satisfaction

data, as presented in Appendix 4. Leadership styles

in Path-Goal theory, namely directive, supportive,

participative, and achievement-oriented. It aims to

examine the effect of each type of leadership style

on job satisfaction. Thus, the regression model I

compiled in Chapter II. The following has

accommodated the objectives of testing.

Table 5.1. SPSS Output-Regression Model 1

Variable Coefficient Value T Sig.

(1) (2) (3) (4)

A Constant 23,951 4,525 0,000

GP direct 0,560 -0,348 0,729

GP support -0,181 -0,085 0,932

GP particip 3,031 1,499 0,138

GP achieve 3,596 2,014 0,048

Based on the SPSS output in the table above,

Regression Model I is as follows:

PUAS = 23,915 + 0.560GP Direct + 0.181GP

Supported + 3.031GP Particip + 3,596GP

Achievement + E

5.1.1 Goodness of Fit Test

1) Determination coefficient

The value of r2 = 0.261 indicates that all four style

type variables leadership can explain 26.1% of the

variations in job satisfaction, while the rest is equal

73.90% is explained by other factors outside the

model.

2) Overall Parameter Significance Test

The F test shows that the F value of 6.719 is

significant at p = 0,000,means the influence of the

four leadership styles together on job satisfaction

was statistically significant at a = 5% (0,000 <0.05).

3) Significant Parameters Individually Test

The t-test showed that only the GPachieve variable

had a statistically significant effect at a = 5% (0.024

<0.05), while the other leadership style variables,

namely GPdirect, GPparticip, and GPachieve, had

no statistically significant effect at a = 5%. Positive

signs (+) in GPdirect, GP support and GP participle

indicate that the three types of leadership styles are

has a positive effect on job satisfaction, even though

only GPachieve has a significant effect, while

GPdirect and GPparticip have no significant effect.

The negative sign (-) in GP support shows that this

type of leadership style has a negative influence on

job satisfaction.

EBIC 2019 - Economics and Business International Conference 2019

378

Based on the description above, it can be

concluded that overall, the style leadership

influences job satisfaction, but individually, only the

type of achievement-oriented leadership style

(GPachieve) is an influential significant effect on job

satisfaction of team members. Accordingly, this test

empirically reject the null hypothesis and accept the

alternative hypothesis (H1).

5.2 Hypothesis Testing 2

The second hypothesis aims to test whether the

interaction between leadership styles with Locus

control has a significant effect on job satisfaction.

The data used in testing the second hypothesis are

Leadership Style data, locus of control, Interaction

between Leadership Style with locus of control, and

job satisfaction, and in Appendix 5. Leadership

styles are classified into directive, supportive,

participative, and achievement-oriented leadership

styles, while the locus of control classified into 3

categories, namely external locus of control,

balanced external and internal locus of control, and

internal locus of control. It aims to examine the

effect of the interaction of the four types of

leadership styles with each locus of control category

on job satisfaction. Accordingly, the Regression

Model II which has been prepared in the following

Chapter IIl has accommodated the objectives of

testing.

PUAS = a+ B1.1Gpdirect + B1.2GPsupport +

B1.3Gpparticip + B14Gpachieve + B2LOC + B3.1

GPdirectLOC + B3.2GPsupportLOC +

B3.4GPparticipLOC + B3.4GPachieveLOC

A summary of the output is presented in table 4.1,

below:

Table 5.2. Summary of SPSS Output-Regression Model II

Variabel Coefisient Value T Si

g

(

1

)

(

2

)

(

3

)

(

4

)

A Constant 69,315 2,450 0,013

GP

direct

-19,519 -2,405 0,019

GP

support

-7,160 -0,666 0,507

GP

particip

4,017 0,384 0,702

GP

achieve

11,258 1,239 0,220

LOC -17,840 -1,628 0,108

GP

direct

LOC 8,476 2,494 0,015

GP

suppor

tLOC 2,438 0,556 0,580

GP

particip

LOC -0,207 -0,050 0,960

4GP

archieve

LOC -3,350 -0,923 0,359

R

2

= 0,338 F = 4,027

Adj. R

2

= 0,258 p = 0,000

PUAS = 69,315-19,519GPdireect –

7,160GPsupport+ 4,017GPparticip +

11,258GParchieve – 17,840LOC +

8,476GP(direct_LOC) + 2,438GP(support_LOC)

– 0,207GP(particip_LOC) – 3,350GP(achv_LOC)

+ £

5.2.1 Goodness of Fit Test

1) Coefficient of Determination

The difference with the regression model I, in this

regression model II added locus of control variables

and leadership style interaction variables with locus

of control. it can be seen that the R2 value of the

regression model II shows a figure of 0.338, which

means that the leadership style, locus of control, and

interaction between leadership style and locus of

control can explain 33.80% of the variations in job

satisfaction, while the rest is 66, 20% is explained by

other factors outside the model. When compared

with R2 of the regression model I of 0.261, it

appears that the value of R2 of regression model II is

greater. This shows that the addition of locus of

control and leadership style interaction with locus of

control can increase R2, which means that these

variables are also factors that influence job

satisfaction.

To see whether the addition of these variables

has a significant effect or not, R2 must be compared

with adjusted R2. If the addition of the independent

variable is a good predictor, it will cause a good

variant and in turn adjusted R2 increases (Kuncoro,

2001). It can be seen that the adjusted R2 of the

regression model II shows the number 0.254. This

figure increased compared to the Regression I model

which only showed an adjusted R2 of 0.222. This

increase in adjusted R2 shows that of the

independent variables added some variables have a

significant effect on job satisfaction. Which

variables that have a significant effect will be shown

through the t-test.

2) Test the overall significance of the parameters

The F test shows that the F value of 4.027 is

significant at 0,000, meaning that the influence of

the four leadership styles, locus of control, and

interaction between the four types of leadership style

with locus of control together on job satisfaction was

stated to be statistically significant at α = 5% (0,000

<0.05).

3) Test the parameter significance individually

The t-test showed that all coefficients of the

independent variable had a statistically significant

Model of Leadership Style on Job Satisfaction in Internal Audit Team at Regional Inspectorates with Locus of Control and Cognitive Style

as Moderated Variable

379

effect on α = 5% (0.024 <0.05), namely the GP

direct variable (Gpdirect leadership style directive

leadership style) GpdirectLOC (interaction of

directive leadership style with locus of control).

Other leadership style variables namely, Gpsuport,

GPparticip, GPachieve with locus of control, and

interactions between Gpsuport, GPparticip, and

GPachieve with locus of control have no statistically

significant effect at α = 5%, although the Gpdirect

and GpdirectLOC variables have a significant effect,

but both These variables have different directions,

GPdirect variable which has a sign (-) means that

directive leadership style has a negative effect on job

satisfaction, while GPdirectLOC variable which has

a sign (+) means the interaction between directive

leadership style and locus of control has a positive

effect on job satisfaction.

If an interaction variables have coefficients that

have a significant effect, then these variables are

moderating variables (Ghozali, 2005) GPdirectLOC

variables are interactions between leadership style

directory with locus of control and t-test shows that

the variable has a statistically significant effect. This

means that the locus of control variable is a

moderating variable. Thus the locus of control can

moderate the directive leadership style in

influencing job satisfaction. Based on testing the

goodness of fit as described above, it can be

concluded that overall leadership style, locus of

control, and interaction between leadership style and

locus of control have an influence on job

satisfaction, but individually, only the type of

directive leadership style with locus of control which

has a significant effect on job satisfaction of team

members. The GPaeaLOC variable coefficient is

statistically significant, this means that locus of

control can moderate the directive leadership style in

influencing job satisfaction. Thus, this test

empirically rejects the null hypothesis and accepts

an alternative hypothesis (H2).

5.3 Testing Hypothesis 3

The third hypothesis aims to examine whether the

interaction between leadership style and cognitive

style significantly influences job satisfaction. The

data used in testing the third hypothesis is leadership

style data. Cognitive Style, the interaction between

leadership style and cognitive style, and job

satisfaction, as presented in Appendix 6. Leadership

style data are classified into directive, supportive,

participative, and achievement-oriented leadership

style, while cognitive style data are classified into 4

categoriesthat is sensation thinking, ignition

thinking, sensation feeling and intuition feeling. This

aims to examine the effect of the interaction of the

four types of leadership styles with each category of

cognitive style on job satisfaction.

Table 5.3. Summary of SPSS Output-Regression Model

III

Variable Value Coefficient T Sig.

(

1

)

(

2

)

(

3

)

(

4

)

20,879 1,644 0,105

-3,488 -0,987 0,327

1,484 0,311 0,757

4,908 1,119 0,267

4,167 1,097 0,276

0,270 0,045 0,965

2,839 1,416 0,161

-0,720 -0,350 0,728

-0,850 -0,374 0,710

-0,759 -0,339 0,736

R² = 0,319 F= 3,689

Adj. R² = 0,232 p = 0,001

Based on the output in the table above, the

Regression Model III becomes as follows:

SATISFIED= A review of the regression model

based on table 5.3 shows the following things.

5.3.1 Goodness of Fit Test

1) Difference Determination

Coefficient with Regression Model I, in this

Regression Model II I added a variable cognitive

style and leadership style interaction variables with

cognitive style. It appears that the R2 value of the III

Regression Model shows a figure of 0.319, which

means the variable type of leadership style,

cognitive style, and interaction between types of

leadership style with cognitive style can explain as

much as 31.90% of the variations in satisfaction

work, while the remaining 68.10% is explained by

factors that are other outside the model. When

compared with R Regression Model I of 0.261, it

appears that the value of R2 Model Regression II is

greater. This shows that the addition of cognitive

style variables and leadership style interaction

variables with cognitive style can increase the

number R, which means these variables are also

factors that influence job satisfaction.

It can also be seen that the adjusted R 2

Regression Model III shows the number 0,232. This

figure is increasing compared to Regression Model I

which only shows the adjusted R number of 0.222.

Increased adjusted number This R shows that the

added variables are present variables that have a

EBIC 2019 - Economics and Business International Conference 2019

380

significant effect on job satisfaction. Any variable

which has a significant effect will be shown through

t-test.

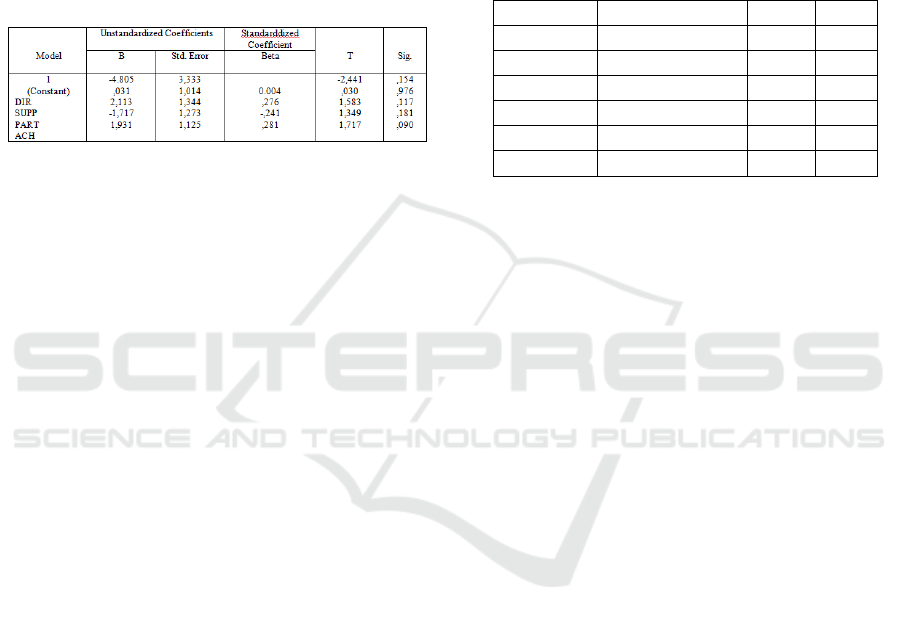

2) Overall Parameter Significance

The F test shows that the F value of 3.689 is

significant at p-0.001, meaning the influence of the

four leadership styles, cognitive styles, and

interactions between the four types of leadership

style with cognitive style together on job satisfaction

was statistically significant at a-5% (0,000 <0.05).

3) Test the Significance of Parameters

Individually

Test shows that all coefficients of independent

variables do not statistically significant effect at a-

5% (0.024 <0.05). And GP (LOC _support) shows

that the three independent variables have a positive

effect on job satisfaction, but the effect is not

statistically significant. As for the negative sign (-)

in GPdirect, GP (supp_COG), GP (Part_ Cog) and

GP (Achv_coG) have a negative effect on

satisfaction employment, although the effect is not

statistically significant.

Based on testing the goodness of fit as described

above, it can be concluded that overall leadership

style, cognitive style, and interaction between

leadership style with cognitive style has an influence

significant on job satisfaction, but individually there

are no variables significant. Thus, this test was

empirically unsuccessful reject the null hypothesis.

This means the interaction between leadership styles

with cognitive style possessed by team members has

no significant effect on job satisfaction of team

members.

6 DISCUSSION OF HYPOTHESIS

TESTING RESULTS

6.1 The Effect of Leadership Style on

Job Satisfaction

The results of the regression test showed that

leadership style had an effect on job satisfaction

with an R2 of 0.261. This means style leadership can

explain 26.10% of variations in job satisfaction. This

test results support the first hypothesis which states

that the force leadership effect on job satisfaction.

The results of the regression test also showed

that of the four leadership styles in the Path-Goal

model, only the achievement-oriented leadership

style significantly influence job satisfaction. The

results of this test can be interpreted that team

members will feel job satisfaction if team leaders

apply an achievement-oriented leadership style in

the team an audit.

Compared to the other three types of leadership

styles, achievement-oriented leadership styles are

more flexible to various situational factors.

According to Wofford and Srinivasan (1983),

achievement-oriented leadership style is suitable

applied to the conditions: (1) the characteristics of

the task structured and unstructured ; (2)

subordinates who practice or are not trained; (3P

broad or limited formal authority; and (4) work

teams with networks Strong social and achievement-

oriented organizational culture. In something, an

audit team characterizes these conditions, for

example in a division of tasks. The division of tasks

is adjusted to the audit objectives.

Each team member is expected to complete the

work for which they are responsible. the role of the

team leader here is to provide challenges in

achieving goals to team members and show

confidence that they can achieve that. Team leaders

can trust that they can achieve these goals. team

leaders can delegate tasks and allow team members

to work and make their own decisions. in completing

work, the team leader encourages independence and

expects team members to like the work for which

they are responsible. team leaders can help solve

work problems by providing examples of solutions.

Auditing requires flexibility, adapted to

conditions, so that what is needed by team members

is clear goals, clear goals, discussions and inputs that

can help solve an achievable oriented problem that

positively influences team member job satisfaction.

thus, the results of this study consistently support the

results of previous studies which stated that

leadership style has an influence on work, led by

Filley, et. al. (1976); Schriesheim and Denisi (1981);

weed, et.al. (1976); Pratt and Jiambalvo (1982); and

Keller (1989).

6.2 The Influence of the Interaction of

Leadership Style with Locus of

Control on Job Satisfaction

Regression test results showed that the interaction

between leadership style and locus of control had a

significant positive effect on job satisfaction with a

coefficient of R2 of 0.254. this means that the

interaction of leadership style with locus of control

can explain 25.40% of job satisfaction variations. the

results of this test support the second hypothesis

which states that the interaction between leadership

Model of Leadership Style on Job Satisfaction in Internal Audit Team at Regional Inspectorates with Locus of Control and Cognitive Style

as Moderated Variable

381

style and locus of control affects job satisfaction

Regression test results also showed that the

interaction variables between directive leadership

style and locus of control had a significant effect on

job satisfaction. this means that the locus of control

attribute is a moderating variable so that by entering

the locus of control attribute will strengthen the

influence of the directive leadership style on job

satisfaction.

The directive leadership style in the Path-Goal

model is best applied to situations: (1) (2) unclear

task objectives; (3) limited formal authority; (4)

work teams with strong social networks; and (5) the

characteristics of subordinates who do not have

adequate expertise (Wofford and Srinivasan, 1983).

The characteristics of the audit team and the

personnel in the audit team characterize some of

these studies, so it is reasonable that the interaction

of directive leadership styles with locus of control

has a significant effect on job satisfaction of team

members. During an audit assignment, team

members are faced with unstructured and complex

work, audits programs that are not all applicable in

the field, and the different expertise and experience

of team members. While team members provide

space to do creativity within a framework of

deepening and overcoming problems that occur, but

because of such problems, it is very possible if the

team members do not discuss how to do effective

work. Supporting, they only have low expectations

for the success of the audit. At times like this, team

members ask for directions and clear directions. The

direction of the leader with the leadership style by

the existing situation. The team leader can help

improve the work requested by providing

instructions and explanations for the job.

In this case, the team leader makes clear the path

to achieving the assignment goals carried out by

team members will achieve the achievements

expected by team members (goal path). Thus, team

members will increase their expectations and

subsequently increase their efforts at work. With the

locus of control's characteristics, the behavior of

team members who have an internal locus of control

will be different from the external in addressing

situational factors with a directive leadership style.

Team Members with internal locus of control will

tend to behave proactively because they have

confidence that audit assignments are a

responsibility answer. They will immediately follow

the path given by the team leader. Whereas team

members with external locus of control will tend to

be passive because they believe that the assignment

is luck or chance. Therefore, the team leader with

style directive leadership will encourage team

members who have a locus of external control by

giving them more specific instructions can easily run

a job.

6.3 Effects of Leadership Style

Interaction with Cognitive Style on

Job Satisfaction

Regression test results indicate that the interaction

between leadership styles and cognitive style does

not affect job satisfaction. Significance test The

individual also shows that the interaction variable is

not significant statistically. This means cognitive

style is not a variable moderating, so cognitive style

cannot strengthen the influence of style leadership

on job satisfaction. Thus, this study does not

managed to support the third hypothesis which states

that the interaction between leadership style and

cognitive style affect job satisfaction.

Other studies as a comparison of these results are

difficult to obtain, because indeed research on

cognitive style in responding to leadership style

someone is still very limited. Some research on

cognitive style has been done, but not directly

related to leadership, as research conducted by

Hough and Ogilvie (2005). These studies link more

between cognitive style with the process of

gathering information for decision making.

6.4 Things That Need Attention

In addition to the results of the partial regression test

as stated in point 5.1. to 5.3, a thorough analysis of

the four results of the regression test shows some

things that need attention, namely; (1) value R ^ 2 of

the regression equation relatively low; (2) leadership

style is only able to explain 20% of variations in

satisfaction, and (3) cognitive style is not a variable

individual moderating, but must be together with the

locus of control.

First, the four regression models show relatively

low R values. Tatas how the 20% competition ends.

Statistically, 'R' wears a relatively low mask. The

bigchange in the data in-some studies show that this

study collects, that is, circular data. Dangerous level

investigation commands for variables analyzed in

the shortcoming the data obtaine is data minimum.

It's relatively low, but it's either large or rather low

depending on the variety of server data attention.

The decline in this study is relatively low

because of the change in sizeone's appearance. Field

survey of variables being investigated. There are

most differences.There's an auditor on the conveyor.

EBIC 2019 - Economics and Business International Conference 2019

382

Different educational and audit experiences are also

different. And there's a look order as a predictor

dynamic. We replaced the audit team instead of the

leader team. I think the situation is hulk because of

the Change in Leadership20s. There is a significant

difference in the level of satisfaction of the team

members.

Second, with R? only with a 20% price change

in Leadership Potential and Interaction Adjustment

in their 20s.Cognitive style can only explain about

20% of the variation in job satisfaction of team

members, while the remaining 80% is explained by

other factors outside the model. This is because

leadership style is not the only factor affecting job

satisfaction of team members in the inspectorate

team. Many other factors influence job satisfaction

of team members in the inspectorate team, but have

not been included in the model, such as a fair reward

system in accordance with team members, the

quality of implementation of supervision carried out

by the person in charge, and supporting facilities in

assignments (such as space work and computer).

These factors are not included in the model because

this study does not aim to identify the factors that

influence job satisfaction of inspectorate team

members. The focus of this research is to analyze the

extent of leadership style and its interaction with

individual characteristics (locus of control and

cognitive style) that affect the satisfaction of team

members.

Third, the results of regression tests in

Regression Model II show that locus of control is a

moderating variable, while the results of regression

tests in Model l show that cognitive style is not a

moderating variable, but the results of regression

tests in Regression Model IV show that the locus of

control and cognitive style together are moderating

variables. It can be seen that the locus of control can

be a moderating variable both individually and

together with cognitive style, whereas cognitive

style cannot be a stand-alone moderating variable,

but must be together with the locus of control.

This, cognitive style is a personality attribute

that cannot stand alone in strengthening the

influence of leadership style on job satisfaction, but

must be together with other personality attributes,

which in this study are locus of control To ensure

that cognitive style attributes cannot be variables

moderating individually, the researcher will

reexamine cognitive style variables with residual

analysis. Residual analysis aims to examine the

effect of deviations (deviations) from an equation

model. The objective of analysis is the lack of fit

resulting from the deviation of the linear relationship

between the independent variables. Lack of fit is

indicated by the residual value in the regression

equation.

COG a b1PUAS + e

If the coefficient value of b1 job satisfaction is

negative and significant, this indicates that the

cognitive style variable is a moderating variable.

Table 6.1. Coefficients

Model Unstandardized

Coefficients

Standardized

Coefficient

BStd.erro

r

Beta t Si

g

(Constant)

PUAS

,629

,006

,521

,011

0,060

1,206

,536

,231

,593

This test ensures that the cognitive style attribute

is not a moderating factor, so it cannot strengthen or

weaken the influence of the leadership style on team

members' job satisfaction. This happens because of

the lack of fit between leadership style and cognitive

style so that cognitive style variables cannot be used

as moderating variables. Thus, the results of this test

support the results of testing in hypothesis 3 which

states that the interaction between leadership style

and cognitive style is significant. Job satisfaction

does not affect.

7 CONCLUSIONS AND

SUGGESTIONS

7.1 Conclusion

Hypothesis testing results show the following:

1. The achievement leadership style shows a

statistically significant effect. This means that

the achievement leadership style influences job

satisfaction. Thus, when not considering the

personality attributes of team members, the

application of style, achievement leadership in

the inspectorate team will increase job

satisfaction felt by team members. These results

support the first hypothesis which states that

leadership style influences job satisfaction.

2. The interaction of directive leadership styles with

locus of control shows a statistically significant

effect. This means that locus of control is a

moderating factor, so that it can strengthen the

influence of force directive leadership to team

members' job satisfaction. The results of this test

support the second hypothesis which states that

the interaction between leadership style and

locus of control affects job satisfaction.

Model of Leadership Style on Job Satisfaction in Internal Audit Team at Regional Inspectorates with Locus of Control and Cognitive Style

as Moderated Variable

383

3. The interaction of leadership style with cognitive

style does not show a statistically significant

effect. This means cognitive style isn't is a

moderating factor, so it cannot strengthen or

weaken the influence of leadership style on team

members' job satisfaction. In other words, the

influence of leadership style on team member job

satisfaction does not depend on the cognitive

style of team members. This result does not

support the third hypothesis which states that the

interaction between leadership style and

cognitive style influences job satisfaction.

7.2 Suggestion

When not considering aspects of locus of control

and cognitive style from team members, this

research successfully found that leadership style

achievement has a positive effect on job satisfaction

of team members in the inspectorate team. By

providing clear goals accompanied by a delegation

of tasks and the greater the responsibility to the team

members, the job satisfaction felt by the team

members is also higher. Whereas when considering

aspects of the locus of control and cognitive style of

the members of this research team managed to find

that the directive leadership style had a positive

effect on job satisfaction of team members in the

inspectorate team.

So that team member job satisfaction is achieved

so that work motivation also increases, the effective

leadership style is a combination of directive and

achievement leadership styles. The directive

leadership style provides clear instructions and

direction, while the achievement leadership style

encourages team members to be independent in each

assignment. One example of applying this

combination of leadership styles is to make the audit

program as concrete as possible, but gives the team

members the freedom to be creative in deepening

and expanding in the field.

The results of this study are expected to be input

for the Regional Inspectorate to make efforts to

make policies in forming teams to increase job

satisfaction received by team members through

situational factors consisting of many aspects such

as authoritarianism, abilities, task structure, formal

authority systems and norms and group dynamics.

REFERENCES

As’ad, Moh. 2003 PsikologiIndustri, Liberty, Yogyakarta

Bologna, G. Jack and Robert J. Lindquist, 1995. Fraud

Auditing and Forensic Accounting, Second Edition.

John Willey & Sons, Inc.

Brownell, Peter. 1982, A Field Study Examination of

Budgetary Participation and Locus of Control.

Accounting Review, Vol LVII, No. 4. Pp. 766-777.

Cheerington, Davidd J. 1994, Organizational Behavior:

The Management of Individual and Organizational

Performance. Second Edition. Ally and Bacon.

Cherg, Mandy M; Luckett, Peter F; Schulz, 2003. The

Effect of Cognitive Style Diversity on Decision

Making Dyads: An Empirical Analysis in the context

of a Complex Task. Behavior Research in Accounting,

Vol. 15, pp. 39.

Ghozali, Imam, 2005. AplikasiAnalisis Multivariate

dengan Program SPSS. Edisi 3. Badan

PenerbitUniversitasDiponegoro.

Gordon, Judith R. 1991, A Diagnostic Approach to