Management Accounting in the Hospitality Industry:

Taiwan Hotel Case Studies

Kanitsorn Terddpaopong

Rangsit University, Pathumthani, 12000 Thailand

Keywords: Management Accountingtools, Hospitality, Hotel Industry, Competitive Market, RevPAR

Abstract: The enormous changes during the last ten years in service operations and information technology have

dramatically affected the environment of management accounting practices in the hospitality industry. The

objective of this study is to investigate the management accounting practices of medium and large-sized

hotel businesses in Taiwan. Five in-depth interviews of the Chief Financial Officers (CFOs) and senior

accounting managers in carefully selected hotels were conducted. The interviews were taken towards the

end of 2018. They focused on how management accounting tools/systems are implemented, including

obtaining information concerning cost structure analysis and measures of financial and non-financial

performance of the selected hotels.The five hotels are unique and representative of 3 – 5 star hotels in

Taiwan. The hotels chosen for the interviews represented three hypothetical operational situations: normal

operation, a temporary closure, and a permanent shut down. The information obtained from the interviews

proved to be helpful in better understanding whatmanagement accounting information essential for decision

are. This is especially for the sustainability of specialty hotels in a highly competitive environment.

1 INTRODUCTION

Hospitality is a general term that refers to a segment

of the service industry that includes hotels,

restaurants, entertainment, sporting events, cruises

and other tourism-related services. The hospitality

industry is essential not only to societies as a whole,

but also to a country’s economy as well as customers

and employees.

The hospitality industry generates revenue for

local economies directly when tourists spend money

on hotels, restaurants and entertainment venues. It

also helps economies of countries indirectly due to

tourist spending on retail goods, foods, souvenirs

and crafts. Besides, tourism can stimulate the

demand for services such as tour guides, translators,

and operators, restaurants and entertainment

services, and infrastructures such as airports, roads

and public transportation.

Also important are the jobs created by the

industry. World Travel and Tourism Council

recently published an article detailing the economic

impact of the tourism industry. In 2017 the

hospitality industry accounted for 313 million jobs

worldwide. This translates to 9.9% of total

employment and 20% of all global net jobs created

in the past decade(World Travel & Tourism Council,

2018). Hospitality also supports jobs in the arts and

culture industries, helping theaters and arts festivals

to thrive.

The hotel sector is another major beneficiary. In

the United States, for example, there has been a

significant rise in occupancy rates. Using statistics

from Smith Travel Research (STR), Sheel (2017)

reports that the year-to-date occupancy increased

0.6% to 67.4%, relative to 66.9% for the same

period in 2016. The year-to-date average daily rate,

or ADR (September), grew 2.0% to $127.14.

In IHG Annual Report and Form 20-F 2018

mentioned that in 2018, the global hotel industry is a

USD525bn industry. The 54% of rooms are

affiliated with a global or regional chain, up from

50% in 2012, and 46% are unaffiliated or

independent hotels. The top five hotel groups

namely IHG, Marriott, Hilton, Wyndham and Accor,

account for 25% of market share, rising from 19% in

2012, and 58% of the global development pipeline

of hotels in planning or under construction.

In a fragmented market, competitor pressures

among the leading brands are intensifying as all of

the major players pursue growth strategies through

business acquisitions, organic growth and

Terddpaopong, K.

Management Accounting in the Hospitality Industry: Taiwan Hotel Case Studies.

DOI: 10.5220/0009203003090323

In Proceedings of the 2nd Economics and Business International Conference (EBIC 2019) - Economics and Business in Industrial Revolution 4.0, pages 309-323

ISBN: 978-989-758-498-5

Copyright

c

2021 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

309

diversification. In the digital era, consumer decisions

about where to stay and how to book hotels has

become a significant development. Hotel companies

must compete and try to survive in this increasingly

competitive environment by using online travel

intermediaries including peer-to-peer home rental

companies and serviced apartments.

There are several metrics for measuring hotel

industry performance. RevPARis an important

indicator of the value guests ascribe to a given hotel,

brand or market and increases when guests stay

more often or pay higher rates. Rooms supply is also

significant because it is reflective of the

attractiveness of investing in the hotel industryand

is influenced by the assumed profitability of a brand

or market. Driven by strong economic fundamentals,

the global hotel industry has seen growth in both

RevPARand rooms supply over the past decade. It

also plays a vital role economically, accounting for

every 1 in 10 jobs around the world (IHG, 2018,

p.

8

).

The hospitality industry is growing worldwide.

However, there are variations among countries.

Several researchers who studied hospitality industry

focused on the country context. For example,

Jeffrey, Barden, Buckley, and Hubbard (2002)

studied the hotel industry in England; Min & Min,

1997; Tsai, Song, and Wong (2009) studied in U.K.

hotel market; Briciu, Scorte and Mester (2013)

investigated the hospitality industry in Bihor

County, Romania; El-Shishini (2017) examined the

relationship between contextual variables and the

use of management accounting techniques in hotels

industry in Bahrain; Pavlatos (2011) conducted

research on 85 leading hotels in Greece;

Makrigiannakis and Soteriades (2015) investigated

48 four and five-star hotels in Greek; Yu and

Huimin (2007) analyzes and compares Chinese hotel

financial performances; Shieh (2012) using 68

international tourist hotels in Taiwan from 1997 to

2006 as samples of the study, are among many

others.

This present paper reports on a research project

that focused on the Taiwan hotel industry. Taiwan

has a dynamic capitalist-type economy with a semi-

presidential government. The country enjoys strong

growth sustained by the dynamism of the entire

region, a population with high purchasing power,

and an economy focused on technology. From the

statistics, Taiwan has one of the lowest fertility rates

in the world, which portends a looming labor

shortage soon. In an attempt to counter this, new

Taiwan regulations provide preferential tax

incentives to foreign professionals employed in

Taiwan. The goal is aimed at improving the overall

environment for recruiting and attracting

professionals from other countries.

There are major drawbacks, however, for

conducting business in Taiwan, the main one being

the lack of direct communication with China, and

another is a very limited domestic market.

Nonetheless, Taiwan is ranked very high because of

the ease of doing business and its strategic

geographical location which serves as an entryway

to China and the ASEAN markets. Despite these

drawbacks, with modern infrastructure and

innovation capabilities, Taiwan is an attractive

destination for investors (Market Entry, 2018).

Despite the conflict between the China and

Taiwan, the Peoples’ Republic of China (PRC) is

still the largest market for Taiwan businesses.

However, in 2018 the number of Chinese visitors

has dropped dramatically by 37.9%: from 974,000 to

605,000. Based on Market Entry (2018), the number

represents the lowest number since 2012. Decreasing

numbers of PRC visitors and tour groups have

caused the industry to focus on regional source

marketsto partially offset this trend. In the long-

term, Taiwan needs more innovation in its tourism

sector in order to capture higher-rated foreign

independent travelers (Voellm, 2017). Fulcoon was

somewhat pessimistic when he concluded that the

hospitality industry in Taiwan may not be expected

to return to normal or riseagain soon (2018).

2 LITERATURE REVIEW

The hospitality industry has been undergoing

tremendous changes and disruptions over the last

two decades. New challenges as well as new

opportunities makes the hospitality industry

attractive. New trends that have reshaped the

hospitality industry especially in hotel business are

such as virtual communities by which social

networks have had a profound impact on customers;

sharing economy like Airbnb represents a major

disruption in the hotel industry; and online travel

agents. These are a few new trends among several

others that have an impact on hotel industry and they

are making the competitive landscape even tougher

than ever (Masset and Weisskopf, 2019).This

contributes to the result that not all hotels have been

successful in this new trends. Some hotels are

successful even though in the highly competitive

environment, while others are bankrupt and close

down and make the end of their hospitality

businesses. The questions rise to both practitioners

EBIC 2019 - Economics and Business International Conference 2019

310

and scholars what makes for a successful hotel? The

research article by Jeffrey, Barden, Buckley, and

Hubbard (2002) give insights into hotel

management. They had followed 15 years of hotel

occupancy analysis in England. Using time-series

analyses of daily and monthly occupancy rates in

different samples of hotels in England for over 15

years, the result reveals consistent temporal

components of occupancy performance. These

differentiate hotels in terms of overall occupancy

levels, seasonality, length of a season, trend and

within-week variations. They concluded that the

components are related to the characteristics of

hotels and their management (Jeffrey, Barden,

Buckley and Hubbard, 2002).

The hospitality industry experienced a dynamic

growth. Challenges facing not only the global crisis

but also market changes, consumer behavior and

technological trends. With an increasing role of the

hospitality industry to the economy of the country,

research on hospitality has been conducted

worldwide. The aim of the studies in this field may

differ depending on each research initiative;

however, the ultimate goals of such research

contribute to improve and sustain the hospitality

industry. This will indirectly and relatively impact

the economy of the countries or region. Accounting,

the language of business, is therefore required to

keep up with changes made to each particular area or

industry, hospitality is no exception. The more

sophisticated the businesses environment is, the

increasing role of accounting, especially on

management accounting, to meet the demand of

management becomes.

In a situation where the competitiveness between

hotels is increasing, hotel managers increase the

focus on improving their performance as it can

become their advantage. With competitive

benchmarking these improvements must be

identified and made by the hotel management (Min

& Min, 1997; Tsai, Song, and Wong, 2009). The key

managerial competencies required and the

importance of hospitality experience of hotel

financial controllers are studied. Data from a

longitudinal study of the hotel financial controllers

have been analyzed. The same authors gathered

information using a content analysis of job

advertisements, a survey of U.K. hotel financial

controllers and interviews with key financial

managers in Burgess (2017) research. The findings

show that although there are many similarities with

the generic accounting profession, the hotel finance

role is unique. Their experience, combining with

hospitality management competencies can support

operational managers. Their understanding of the

complexity of the operation, in a dynamic and

perishable environment, enables hotel financial

controllers to act,on behalf of stakeholders,as

business advisors to other managers, thereby

enhancing profitability (Burgess, 2017).

Briciu, Scorte and Mester (2013) investigated the

hospitality industry in Bihor County, Romania

regarding the impact of accounting information on

the managerial decision. They conclude that 65.93%

of their surveyed managers believe that the

accounting information is very useful in decision

making, compared to 62.63% believe in financial

accounting. The most important factor influencing

the quality of management decision is the lack of

cost calculation system (88%) and the subjectivity of

the accountants (78%).

El-Shishini (2017) examined the relationship

between contextual variables and the use of

management accounting techniques in hotels

industry in Bahrain. He believes that the size of the

hotel, the intensity of competition and the quality

level of the hotel have a positive effect on the use of

management accounting techniques. He explored

these assumptions through the distribution of the

questionnaires to the 37 hotels in Bahrain and found

that benchmarking, absorption costing, budgeting for

organizational activities, in ranking order, are the

most use by the hotel managers, while activity-based

costing (ABC), activity-based management (ABM),

and long-range forecasting are the least used by the

hotel managers. He concluded that traditional

management accounting techniques were widely

used at hotels more than the recent management

accounting techniques. Also, his result indicated that

the intensity of competition has a significant positive

relationship with the use of management accounting

techniques, while the size and quality level of the

hotel does not have any relation with the use of

management accounting techniques. Part of this

finding, is contradict to the conclusion made by

Fathi, Dozdahiri (2015), which the authors stated

that advanced technologies are implemented in

hotels to lower their expenses. The same authors

used ABC implementation as a focus of their study

and concluded that organizational, technological,

individual and environmental factors influence on

ABC implementation in the hotel industry. Pavlatos

(2011) conducted research on 85 leading hotels in

Greece regarding the impact of strategic

management accounting and cost structure on ABC

system. The same author found that the adoption of

ABC system is positively associated with the extent

of use of strategic management accounting

Management Accounting in the Hospitality Industry: Taiwan Hotel Case Studies

311

techniques and with the cost structure while size of

the hotel has no relation to the adoption of ABC

system. In other words, no matter what size the hotel

is, the ABC system can be adopted. This finding,

again, contradicts with a result of Poldrugovac,

Tekavcic and Jankovic (2016) as they found that

there is a significant relationship between sizes and

hotel efficiency.

Management accounting is also studied in Greek

hotels. The majority of Greek hotels operate on a

seasonal basis for about six to seven months per

year. As a result, prices are heavily discounted and

contribution margins are low (Makrigiannakis and

Soteriades, 2015). The authors investigated 48 four

and five-star hotels in Greek and found that size and

sales mix structure have a positive impact on the

number of operational departments' analyses of

contribution margins. In other words, hotels with a

high sales volume are more sensitive to calculation

accuracy of profit sensitivity analyses and thus make

extensive use of cost information for pricing.

Not only the studies conducted in developed

countries, a developing country such as China is also

in the pace of changes. Current development of the

hotel industry in China, particularly the rapid growth

of Chinese hotel brands and international hotel

companies, is also concerned. The challenges facing

hotel financial management in China and the rapid

globalization of hotel development and operation

and financial performance are the concern of

researchers. The article by Yu and Huimin (2007)

analyzes and compares hotel financial performances

managed by international hotel companies, Chinese

hotel management companies, and Chinese

independently-managed hotels. They provided

recommendations for improving hotel financial

reporting and management for China's hotel

industry(Yu & Huimin, 2007). The link between

cost efficiency and financial performance as it

pertains to the hotel industry is studied by Shieh

(2012). This study employs the data envelopment

analysis approach to estimate cost efficiency and

uses three traditional financial indicators—the ratio

of net operating profit before taxes, the ratio of

earnings before taxes, and return on assets before

taxes—to measure financial performance. Using 68

international tourist hotels in Taiwan from 1997 to

2006 as samples of the study, the significant finding

indicates that cost efficiency is insignificantly

associated with the financial performance regardless

of the financial performance variable used (Shieh,

2012).

The optimal occupancy rate, operational, and

profitability efficiency of Taiwan's international

tourist hotels are studied by Chiu and Huang (2011).

They stated in their research that high performance

in operational effectiveness does not necessarily

ensure high profitability. The same study shows that

increasing sales is not the best way to improve

performance, actually better to decrease the

occupancy rate to enhance operational and

profitability efficiencies. Evidence from the same

authors concluded that the inconsistent occupancy

rate targets can be remedied through an empirical

model (Chiu & Huang, 2011).

Of course, both financial and non-financial

performance is of the management concerns. Recent

research on non-financial performance measurement

in Cape Town, South Africa hotel industry is studied

by Mjongwana and Kamala (2018). They found that

their 100 responding hotels use non-financial

performance measurement to improve the hotel

operation. Customer-oriented measures were the

most frequently used by the small and medium-sized

hotels in Cape Town – sales growth percentage, and

occupancy levels, guest satisfaction (with the results

of means of 4.77, 4.73, and 4.67 out of 5,

respectively). These non-financial performance

measurements provide businesses with feed-forward

information and are used for improving profitability,

productivity and effectiveness as well as improving

decision making (Mjongwana and Kamala, 2018).

The past literature gave heed on how the hotel

management use management accounting tools to

support their management decision. Due to a

different environment, different economic context,

competitive environment, technological

advancement, country development and culture, a

country context is commonly used as a subject of the

study. In this study, in-depth investigation of the use

of management accounting tools in Taiwan hotel

industry is studied. Like other hospitality industries

in other countries, Taiwan is facing great

competitive challenges. Taiwan tourism is an

essential component of Taiwan's economy, as well

as a significant source of foreign exchange revenues,

contributing 9.3% of the country's GDP (Mordor

Intelligence, 2018). The political issue between

Taiwan and mainland China that plays a vital role in

Taiwan hotel industry development. This article

does not touch on this topic instead on the

management accounting tools being used by the

management of Taiwan hotels.

This paper discusses Taiwan hotel industry, the

research method used for data collection, the

definition of critical terms regarding complexity and

findings of this research and conclusion and

suggestion in this order. The questions that will be

EBIC 2019 - Economics and Business International Conference 2019

312

addressed in this present paper are i) how is

management accounting implemented in the Taiwan

hotel industry?; ii) how advanced of technological-

based implemented in Taiwan hotel industry,

especially on complex hotels; iii) what are the

revenue and cost structures of the Taiwan hotels; iv)

what management accounting tools are being used

by the hotel executives in Taiwan?

The argument makes in this paper is the level of

management accounting tools used by the hotel

management depends on the “complexity” of the

hotels. The more complex either on the type of the

hotels as chain hotels, the multiple locations of the

hotels, the luxuries of the hotels which normally

classified by the number of stars, the more

sophisticated of management accounting tools would

have been used by the hotel management. The hotels

with such complexity will use more often and

sophisticated or advanced level of management

accounting tools to help in decision making. The

level of complexity of the hotels that the more

complex they are, the full range of management

accounting tools will be sought for by management

of the hotels.The proposition makes in this paper

does not directly relate to the size of the hotels.

However, there is a tendency that the larger hotels

will possibly use more often and more advanced in

management accounting tools due to the rising level

of issues to solve, and in the same time, larger hotels

would have a financial capacity to invest in

management systems to assist in their businesses.

3 METHOD

Much of the previous research surveyed in the

previous section did not use in-depth interviews,

while most of the researchers used questionnaires.

Thus, the findings of those earlier studies may be, to

some extent, less reliable due to such obstacles such

as questionnaire bias, including the way individual

questions were designed, and in the way the

questionnaires were administered. Additionally,

there may have been unanticipated communication

barriers between the investigator and the

respondents. Another perceived flaw in the previous

research related to the use of a predetermined list of

responses, rather than the use of open-ended

approaches (Choi and Pak, 2005). To overcome

theseissues, this present study used an in-depth

interview method to investigate and to understand

more deeply management accounting practices in

the hotel industry.

As the study aimed to gain knowledge from

those directly involved in the selection and

management of accounting tools, this present study

focused on five leading hotels in Taipei, the capital

city of Taiwan.The five wereselected because of

their unique qualities and were representative of 3 –

5 star hotels. Permission to carry out this study was

negotiated beforehand by an exchange of written and

verbal communication. In each case the Chief

Financial Officers (CFOs)agreed to collaborate.

Intensive individual in-depth interviews of the

CFOs of the fivehotels in Taipei were conducted

during November – December 2018. The interviews

were carried out mostly in English while certain

questions and responses needed an interpreter. The

interpreter worked in parallel with the researcher to

ensure understanding and accuracy of the exchanges.

Each of the in-depth interviews took place at the

respective hotel venues and were between 1.5 – 2.0

hours in length.

An interview protocol was used to ensure

consistency among the interviews, and thus increase

the reliability of the findings. Most of the questions

were open-ended. After each interview, the recorded

data were then transcribed and reviewed. Patterns or

themes among the participants were identifiedand

grouped. The data from the interview was labelled

‘Case 1’,‘Case 2’, and so on. The finding will be

presented according size – the number of hotel

rooms – beginning with the smallest and ending with

the largest.

4 FINDINGS

4.1 The Characteristics of the Selected

Hotels in Taiwan

The degree of complexity is the extent of variability

in the business environment. Awang, Ishak, Radzi

and Taha (2008) define the degree of environmental

complexity of the hotel industry according to 6

dimensions: 1) geographic concentration of

competitors; 2) geographic concentration of industry

sales; 3) geographic concentration of labor

availability; 4) level of products/services

differentiation; 5) geographic concentration of

customers; and 6) technological diversity used in the

industry.

The level of complexity of the hotel industry

also affects hotel classification. For example, one

classification system is based on size, star,

location/clientele, ownership, level of services. The

Institute of Hotel Management Bhubaneswar,

Management Accounting in the Hospitality Industry: Taiwan Hotel Case Studies

313

Ministry of Tourism, Government of India (2017),

for example,uses a classification system based on

size (small, medium, large, very large); on Star (1

star up to 5 stars); on location (downtown hotel, sub-

urban hotel, resort hotel, airport hotel, motel, floatels

and hotels); on clientele (business or commercial

hotels, transient hotels, boutique hotels, residential

hotels, suite hotels, bed & breakfast hotels, casino

hotels, conference centres, and green hotel); on

ownership (independent hotels, chains, management

contracts, franchise, referral groups, time-share

hotels, condominium); on level of services (upper-

market which are luxury, world-class services

hotels; mid-market; budget/economy hotels).

In this study, the level of complexity has three

levels: highly complex, complex, and less complex.

The level of complexity is determined by the

combination of at least three of the following: 1)

number of stars, 2) size according to the number of

rooms, 3) the number of employees, and 4)

ownership. Table 1 shows the classification of

complexity used in this present study.

Table 1: Complexity classification

Levels of complexity Star Room Employee Ownership Level of

services

Highly complex 4 – 5 Over 400 Over 500 Chains,

management

contracts,

franchises

Upper –

market

Complex 3 – 4 Over 100 Over 300 Chains,

management

contracts,

franchises

Upper –

mid-market

Less complex 2 – 1 Less than 100 Less than 300 Independent

hotels

Mid-market

– Budget

economy

Source: Compiled by the author

In this study, two of the five case studies are

classified as ‘complex’ hotels and the other three are

‘highly complex’. The specific features of each of

hotel classifications are shown in Table 2.

Case 1

The“Case 1” hotel was established in 1998 and has

been operational for 20 years. Being a small luxury

four-star hotel, it can provide high quality service. It

features a famous restaurant - the steakhouse, which

was recommended by Michelin. Even though the

hotel is quite small it boast a high standard of

service quality, and it is that which attracts its

customer-base.

Case 2

The "Case 2" hotel has been operating for 39 years

(since 1979) as a family business. The ownership

has now been transferred to the second generation.

The current Chief Executive Officer (CEO, a family

member, has an overseas education from the United

States of America and has lived there for more than

20 years.

Case 3

The Case 3hotel was established in 1999. It is a large

five-star hotel, under the Tourism Group of Taiwan,

and is located in a business area of Taipei. The

Group also operates other hotels as well as a theme

park and property residences. This hotel has been

financially supported by its group. In April 2018,

the hotel announced that it would close on 31

December 2018. Its occupancy rate was 70% in

2017, with an average daily room rate of NT$6,387

(US$209).

Case 4

The Case 4 hotel is a franchised luxury hotel under

the IHG (InterContinental Hotels Group PLC)

group. The IHG business modelpredominantly

franchises its brands and manages hotels on behalf

of third-party hotel owners. The hotel in Taipei is a

five-star hotel and has been in operation for more

than 20 years. It is a large hotel with over 500 rooms

and more than 1,000 employees. It is a highly

complex hotel.

Case 5

The ‘Case5” hotel was incorporated in 1962. Itwas

Taiwan’s first international standard luxury hotel in

Taipei’s city center, and in 1982 it was listed on the

Taiwan Stock Exchange. It is generally regarded as

one of Taiwan’s most respected and successful

companies. The company operates in two other

locations in Taiwan: Kaohsiung (1981) and Hsinchu

(2001). The company is owned by a group of

families. The owner of the Case 5 hotel is also the

CEO of the hotel. In addition to being an

international-standard luxury hotel in Taiwan, it has

become a ‘hallmark of residential luxury and

gracious Taiwanese hospitality, while continuing to

create new hospitality brands and services’. The

Case 5 hotel in Taipei is especially well-known for

its Michelin chef and restaurant, a steak house, and a

five-star bakery.

EBIC 2019 - Economics and Business International Conference 2019

314

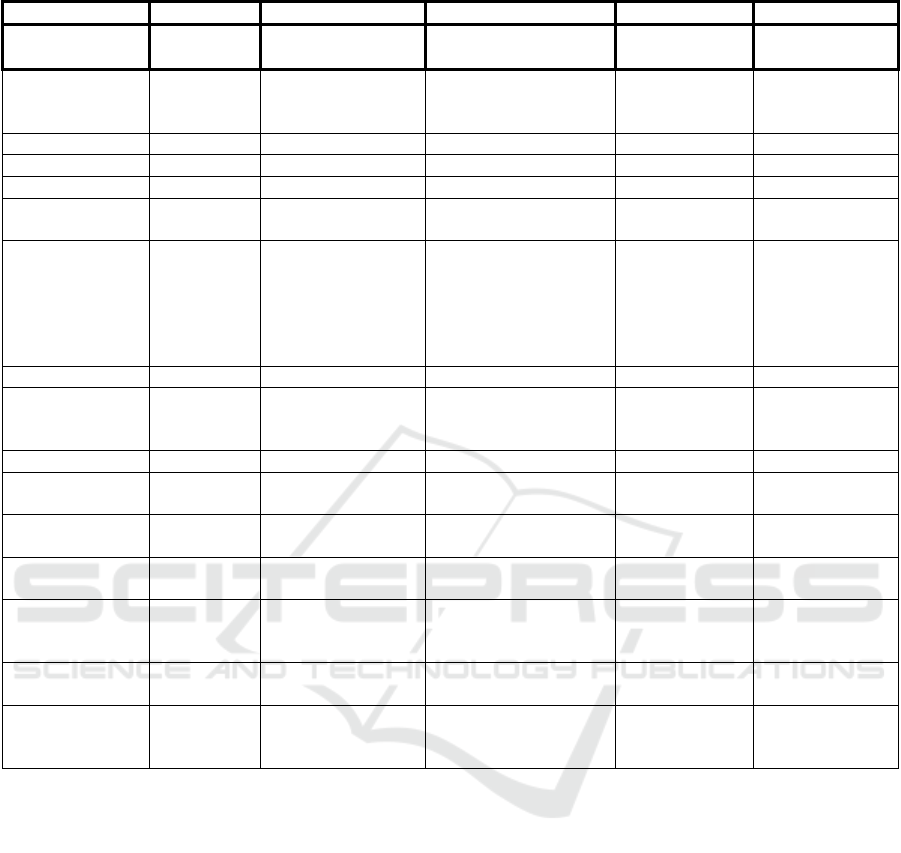

Table 2: Characteristics of the five hotels

Case 1 Case 2 Case 3 Case 4 Case 5

Complexity

classification

Complex Complex Highly complex Highly complex Highly complex

Years of

establishment

until 2019

21 40 20 More than 20 55

Size Small Medium Lar

g

eLar

g

eLar

g

e

Stars **** *** ***** ***** ****

Number of Rooms 96 287 288 540 1,020

Number of

Em

p

lo

y

ees

300 200 500 1,000 1,200

Number of

Products/Services

1 Hotel in 1

location

Taipei

1 Hotel in 1 location

Taipei

1 Hotel under a business

group

Taipei

1 Hotel under

IHG Brand

Taipei

3 Hotel Locations

under the same

brand

Taipei

Kaohsiung

Hsinchu

Room rental

Restaurants &

Bakery &

Cafeteria

Sho

p

s

Total Revenue

(

TWD Million

)

700 330 1,300 Approximate

2,000

1,700

Total Assets

(TWD Million)

4000 700 n.a. n.a. 11,255.171

% Profit to total

revenue

17.5 5% Loss n.a. 25.81%

Ownership

structure

Family

Business

Family Business Listed Company +

Family Business

Listed Company

+

Family Business

Listed Company

+

Family Business

Interview date 20 December

2018

7 November 2018 18 December 2018 21 December

2018

6 December 2018

Remarks Temporarily close

and will be

reopening soon

Permanently close down

the business on 31

December 2018

Source: Compiled by the author

4.2 Trust of the President, the Chief

Executive Officer (CEO) towards

the Chief Financial Officer (CFO)

Who Controls Management

Accounting Implementation

For an independent and small to medium-sized

hotel, the implementation of management

accounting processes is likely to be different from a

dependent/branded and large hotel. For a small

hotel like Case 1 and also being a family business,

trust between the management and the owner of the

hotel is very important either in terms of

management or implementing new accounting and

managerial systems. For a medium-sized hotel like

Case 2, the trust between the two parties is the key

to implementing management accounting. In this

particular Case 2 hotel, the CFO is not new but has

had considerable experience in hotel management.

The CFO had been working with the prior president

of the hotel for more than 15 years. With the CFO’s

background of working as an auditor in a big

accounting firm in the past, the CFO has great

experience in both hotel management and

accounting, auditing and management. The CFO had

earned trust from both previous and current

presidents and has made a significant contributions

toward management changes and newly

implemented management accounting practices.

The CFO has received positive support from both

prior and current presidents on the implementation

of new management accounting reports, for

example. From the interview, the issue of the trust

Management Accounting in the Hospitality Industry: Taiwan Hotel Case Studies

315

was asked. The response from the Case 2 CFO is as

follows.

Regarding the support received from the

president and the CEO of the hotel, I

received a great support from them. The

previous president is a bit conservative,

however, the current president who is

also the CEO gave me a great support

regarding issues such as new

implementation of accounting report as

previously there was little reports

produced from accounting department.

(Excerpt from the interview on7

November 2018with the respondent

Case 2 Hotel)

The CFO was asked to rate the level of support

on a scale of 1 (lowest) to 10 (highest). The level of

9 point scale was the feedback as referring to the

support received. However, staff cooperation is also

a key to the success of the implementation. When

new management accounting tools were firstly

introduced, the CFO required further and detailed

information from the accounting department, as well

as from others.

The initial resistance from the related

stakeholders was rather high. I assumed

it was really high if you asked me,

probably at the 9-point scale out of 10.

However with the high support and

encouragement from the president and

the CEO, plus with thorough

explanations from me and my staff about

the benefits or advantages from having

such required information. The resistance

from the staff gradually reduced and at

the current stage, the resistance is

considerably low probably 3-point scale

(from the CFO's own assessment).

(Excerpt from the interview on 7

November 2018 with the

respondent Case 2 Hotel)

This data comes from CFO of a small/medium-

sized hotel with one owner. While in larger hotels,

the trust among executive management is managed

through the controlling system. Case 4, being a

chain hotel,and Case 5, being a listed company in

the stock exchange, the management and controlling

system for large hotelsis very clear and

decentralization of responsibility among several

departments of the Hotel. The CEO supports the

transparent synergy, whereas the CFO is the main

person in charge of the management accounting

practices of the Hotel.

The hotel uses the controlling system

such as the contracts with suppliers, the

management controlling system through

each department. Staff at the accounting

department work hard to keep up the

reports required by executives. Meetings

between executives of the hotels and

accounting department are conducted

regularly. Due to the fact that a hotel is in

a fast speeding industry, meetings are

done in a weekly basis.

Excerpt from the interview on21

December 2018 with the

respondent Case 4 Hotel)

The accounting department of the hotel is

a large department and consist of many

accounting senior, middle, and junior

staff. With the high requirement on

financial information – both on financial

accounting and managerial accounting,

accounting information for routine

reports is conducted in a professional

manners, while quite often that

managerial accounting information is

requested by the executives, but most of

the time they are on request.

(Excerpt from the interview on6

December 2018with the respondent

Case 5 Hotel)

For small hotels, the support from top

management is one of the crucial factors to the

success of new management accounting

implementation and new controlling initiatives. To

implement a new management system,

implementing a follow-up system, planning and

controlling system, the support from the president or

the CEO and the collective hard works of the CFO

and accountants are believed to be the main factors

leading to success. In a larger hotel, the management

accounting system is set and there are control

mechanisms.

4.3 Implementation of a Technological

BusinessModel

Sustainability in a highly competitive hotel business

environment requires effective business strategies

and tools. Technology, such as an online booking

system, including checking-in and check-out are

EBIC 2019 - Economics and Business International Conference 2019

316

typical in the modern-day hotel industry. However,

small hotels may still be reluctant to adopt such

time-saving and cost-saving tools. Larger hotels are

more likely to have such supporting tools in place

while small hotels may not. Data from the interview

with the CFO of the Case 2hotel revealed adopting

such technology would hurt an important customer

base, namely Japan. Such a tool would be unfamiliar

to that segment. Hence the old system which relied

on long-term relationships with travel agencies

continued. However, the new CEO dramatically

changed the business model as revealed in the

following excerpt from the interview.

Under the modern management of the

new CEO, instead of relying more on a

long-term relationship with travel

agencies, the new CEO has started a

business via an online travel agency

(OTA) such as Agoda, booking.com,

TripAdvisor, Priceline, Liberty Holidays,

Expedia and Hotel.com. With the new

media platform the hotel attracted a

broader range of customers from all over

the world. Even though the primary

customers are still from Japan (50%),

customer diversification has varied since

the new media platform was adopted.

The second group is Mainland China

customers, and the third is local

Taiwanese customers.

(Excerpt from the interview on7

November 2018with the respondent

Case 2 Hotel)

After the implementation of OTA, sales revenue

increased by about 15%. While this practice

appeared to be rather new for small hotels, it was

quite usual in larger hotels where major management

decisions in terms of technology adoption and

implementation are normally a headoffice decision.

4.4 Revenue and Cost Structures

In the hotel industry, RevPAR and KPI are standard

performance metrics. They provide important

financial information within a specific

period.Management can assess such data as room

occupancy and the price of the average room.

However, RevPAR alone, may not the only metric

which needs to be used. For example, it could be the

case that a hotel may have a low RevPAR but at the

same time having many rooms which would yield

higher revenues. Therefore, a hotel manager often

considers it together with average daily rate and

occupancy rate as performance measures. All the

hotels, of course, seek to increase the average daily

rate by focusing on pricing strategies, including

upselling, cross-sale promotions, and complimentary

offers such as free spa and dining service in the

hotel, while an overall economy is an additional

significant factor in price setting.

Cost classifications for hotels could be fixed

costs and variable costs. They could be labelled as

direct costs and indirect costs. The cost structure of

hotels varies. For example, in the Case 2 hotel,the

direct cost was the cost of goods/services sold with

an average of 56% of the hotel revenue, while the

indirect cost was about 20%. However, the most

profitable department was in the rental department,

which earned the highest contribution margin, while

the restaurant department did not do so well as the

rental department. In Case 5, the hotel’s restaurant

earneda major international award. Some 60% of the

total hotel revenue came from that restaurant

compared to 40% from the room rental division.

The RevPAR of Case 5was set at NTD 4,500 per

day (room rate of NTD 5,000 multiplied by 90% of

occupancy rate). The restaurant revenue last year

(2017) was NTD 1,200 million where the fixed

costswere 30 %, and the variable costs were 40 %

ofrevenue. As a result, the margin for the restaurant

was about 30 % of its income. What follows are

statements from the respondent:

For the room revenue, the hotel reported

its revenue last year of NTD 500 million,

with the fixed cost of 30 % and variable

cost of 10%, leaving the hotel margin

from this revenue at about 60% of its

revenue. The profit margin of room

revenue was 60%, while that of the

restaurant was 30%. The profit margin

of room revenue was double of the

restaurant revenue. This is due to the

cost structures of the Hotel, where room

revenue the cost is more on fixed, while

the restaurants are more on both variables

(40%) and fixed (30%).

(Excerpt from the interview on6

December 2018with the respondent

Case 5 Hotel)

4.5 Implementing Management

Accounting Practices

The accounting department regularly prepares

financial statements – basically the monthly income

Management Accounting in the Hospitality Industry: Taiwan Hotel Case Studies

317

statement. While other reports from each profit

department are prepared on a fortnight basis. The

contribution margin income statements are prepared

by each profit department and are monitored by the

CFO and CEO in the meeting normally held twice a

month for planning and decision making purposes.

The contribution margin income statement shows all

variable expenses deducted from sales and arrives at

a contribution margin. Fixed expenses are then

subtracted to arrive at the net profit or loss for the

period. The amounts remaining can be used to cover

fixed costs and contribute to operating profit.

Variance reports, budgeting reports, break-even-

point reports, together with RevPAR, are normally

reported on a regular basis.

Despite the highly competitive environment for

the hospitality industry, complex accounting tools

are not commonly used as in case of Case 2 hotel

management. Basic and less complicated

management accounting reports are more commonly

used. Complex accounting reports such as balanced

scorecard, activity-based costing, total quality

management report, lean or just in time report are

not practiced in that hotel.

There are other types of reports which are less

complicated and which seem to be more practical for

small specialized hotel such as the Case 2 hotel. For

example, total quality management (TQM) which is

commonly used in many industries, including, but

not limited to, manufacturing, banking and finance,

and medicine. It focuses on developing a work

culture that emphasizes customer satisfaction. All

members of the organization participate in

improving processes, products, and services. The

goal is to achieve continual improvement of business

operations.

The Case 2 hotel strives to ensure allemployees

work toward common goals of improving service

quality, as well as improving the procedures that are

already in place. Particular emphasis is put on fact-

based decision making, and using performance

metrics to monitor progress. High levels of

organizational communication are encouraged to

maintaining employee involvement and morale. The

CFO did not recognize the term ‘Total Quality

Management (TQM)', however from the interview,

all the process that the hotel practiced are those

embodied in the TQM concept, but in a simplified

version. And, the CFO’s office requires less time

consuming and less complicated reports.More

information comes from the interview.

For instance, the hotel has adopted the

system known as Hotel Housekeeping

Standard Procedures and Standard

Operating Procedure (SOP). The

housekeepers need to execute cleaning

and maintenance tasks at various places

in the hotel based on the set standards.

The housekeeping staff can contribute to

retaining guest satisfaction as well as to

generate new guests willing to repeat

their visits to the hotel. This will bringsin

more revenue to the hotel. What the hotel

performs towards guest satisfaction and

works productivity together, is an

integral part of total quality control. The

second example is on supply chain

management. Due to the restaurant and

cafeteria departments, ingredients

supplying to the Hotel are from

contracted suppliers. The hotel goals

when it comes to food and beverage

services is to provide the top quality food

and beverages. All cuisines and bakery

are in-house produced. The hotel keeps a

10-day delivery contract with its food

suppliers. With the software assisting in

the control stock and inventory, the

urgent purchase can be made. The hotel

has at least three potential suppliers at a

time. If one does not qualify either due

to price, quality, quantity, or delivery

schedule, the next potential supplier can

replace such purchasing orders.

(Excerpt from the interview on 7

November 2018 with the

respondent Case 2 Hotel)

The concept of ‘just in time (JIT) and lean’ has

often been employed in the manufacturing industry;

however, to the hotel industry, perhaps some

justification may be needed. The Hotel has

implemented the JIT and lean system by having a lot

size of ingredients such as food, to be delivered, and

a lead time (10 days in this case) that is adjusted to

consumption. These practices are similar to those

used in the manufacturing industry, but less

complicated.

As a standard practice, the accounting

department prepares the financial statements –

basically the income statement on a monthly basis.

In the Case 5 hotel, accounting software is used. The

operational accounting software – Oracle, Infrasys

(Infrasys Gourmate software for all Food and

Beverage Sectors in the hotel), and the Taiwan

Accounting System (ALL NEW GL) are being

used.As an example, Infrasys software can integrate

with external systems such as hotel property

EBIC 2019 - Economics and Business International Conference 2019

318

management systems, membership systems, catering

software, as well as accounting and inventory

management systems. The software can switch

ordering modes (fine dining / fast food) in real-time.

With the aid of accounting software, it usually takes

three business days to prepare and complete the

financial statements. The segment reports prepared

using the contribution income statement format.

Variance reports, budgeting reports, break-even-

point reports, together with RevPAR, are reported

regularly.

The CEO of the Case5hotel initiated the activity-

based costing (ABC) system some three years ago.

Each year, in the executive meeting, the topic of the

cost drives is the topic of discussion. Information on

the cost drivers is collected and presented for

discussion. Every department is represented at this

meeting and a decision is reached as to which are the

best cost drivers for their cost allocation. There were

28 cost drivers in 2018. Examples of the main cost

drivers are:

1. CEO expense → Budget revenue (TWD)

2. Human Resource expense →Employee number

3. MIS expense → Equipment quantity

4. Purchase expense → %Working hours

5. Banquet expense → Banquet revenue (TWD)

The cost allocation using ABC was about NTD$

300.00 million, which was 70% of total expenses.

The problem that the Case 2 Hotel experienced in

implementing ABC was an argument about the cost

drivers being used and allocated to the expenses of

related departments. Several departments tried to

negotiate about which costs would be allocated to

them.

Oracle Hospitality (OPERA Cloud Services) is

an enterprise platform for hotel operations and

distribution. It offers comprehensive, next-

generation capabilities hotels can use to enhance

guest experiences and improve operating

efficiency.It creates a platform for a hotel property-

management system and point-of-sale system. It

manages the hotel, food and beverage operations.

Integrated Oracle Hospitality hotel solutions

increase operating efficiency and enable better guest

experiences for independent hotels and hotel chains.

The top accounting programs used in the hotel

industry todayare i) FreshBooks, ii) Sage Intact, iii)

Inn-Flow, iv) Hotelogix, and v) M3AS software. To

supply quality materials to the hotel, the hotel

involves over 1,000 suppliers throughout the world.

The contracts with suppliers are renegotiated every

three months, based on quality and quantity

considerations.

4.6 Role of Accounting Tools in Senior

Management Hotel Decision

Making

Management accounting plays a significant role in

decision making. In the Case 2 hotel, which is

classified as a small hotel, management accounting

alone may not play a very large role without senior

management support. The CEO has taken the

initiative to make the hotel a five-star hotel and to

change it into a Green Building Hotel in the near

future. At the time of the interview (end of 2018),

the hotel was in a transitioning mode and would be

in less than a year temporarily closed. The

interviewee commented:

In this transitioning period, management

accounting tools are used due to the high

demand for decision making. The need

for management accounting tools such as

the report on costs during the period of

pausing the business, the budget for new

investment, the brake-even point, the

budget on reopening the business, the

budget on wages to keep permanent staff,

the comparative sources of finance report

and many more. These reports in a

normal situation may not be highly

required.

(Excerpt from the interview on 7

November 2018 with the

respondent Case 2 Hotel)

The situation on the importance of management

accounting reports is also found in the interview

with the Case 3 hotel interviewee. Due to a deficit,

the management made the decision to close down

the hotel. The interview took place just ten days

before its closing. Prior to that several reports had

been required from both the CFO and CEO for

making what was considered to be a very serious

decision. Interestingly the decision to close down the

business became a revenue-producing decision.

Together with the marketing department, the hotel

management launched an attractiveroom sales

promotion for customers who booked rooms prior to

December 31 (the last check out time was the

afternoon of 31 December).

This date coincided with the last date of

operation after which all the furniture and hotel

decorations would be removed. .In such a case,

Management Accounting in the Hospitality Industry: Taiwan Hotel Case Studies

319

accounting information was essential. The rooms

were sold out right awayand the hotel was able to

derive substantial revenue at the last minute. The

interviewee stated:

The selling price of the rooms on 31

December 2018 was set considering the

salvage value of the items in the guest

rooms. The Accounting department and

the Sales department were consulted in

regard to the price of the rooms to be

sold on this occasion. This revenue will

be considered a plus income to the hotel.

These selling last day rooms are actually

a selling gimmick of the hotel.

(Excerpt from the interview on18

December 2018with the respondent

Case 3 Hotel)

The interviewee was asked about the managerial

accounting information that was provided to the

hotel executives. Since the rent on the property is so

high, the revenue generated from the hotel business

was insufficient. What were the facts that led to the

decision to close the property? The interviewee

explained:

The hotel executives were informed all

along regarding the deficits of the hotel.

However, the executives believed that

they could overcome this situation by

either generating more income or

negotiating with the landlord. However,

generating new income could not

outweigh the high expense on rent. The

executives had tried to keep the hotel in

business for so many years. Every year

was just topping up on the existing loss.

(Excerpt from the interview on 18

December 2018 with the

respondent Case 3 Hotel)

4.7 Financial and Non-financial

Performance of the Hotels

Hotel management personnel routinely concern

themselves with financial performance

measurements. Most use financial ratios such as

return on assets (ROA), the return on equity (ROE),

percentage of the cost of goods sold to total revenue,

profit margin ratio, and net operating profit ratio.

Unlike financial performance measures, non-

financial performance measurements (NFPMs)

provide the hotel with feed-forward information, a

future-oriented measure. These are more relevant for

planning purposes and day-to-day operations.

Hotels have used non-financial measurements to

provide a closer link to long-term organizational

strategies, while financial performance measures

generally focus on annual or short-term performance

against accounting standards. NFPMs are also

progressive with regard to meeting and exceeding

customers' expectations as well as gaining and

maintaining a competitive advantage over

competitors. As mentioned by Micheli and Manzoni

(2010) non-financial performance measurements are

more critical to decisions that affect profitability and

other long-term strategic goals. Hotels also have

used several measures based on customer

perspectives such as.

- Guest complaints on employee helpfulness,

on facilities, on services standards and

other types of complaints

- Guest satisfaction surveys via online travel

agencies

- Percentage of sales growth on a monthly

period, quarterly period, and annually

- Room occupancy percentages

- Number of repeat customers

- Market share percentage

For the internal business operation, hotels also

use non-financial performance measurements such

as

- Ability to adjust, rectify, and respond to

guest’s complaints/requests

- Response time to guest requests

- Hotel supplies meeting the hotel purchasing

standards (time, quality, quantity, price)

- Training hours of the staff (for example,

training staff on work attitudes, how to deal

with customer complaints, restaurant

management, hospitality administration and

catering)

The CFO of the Case 2 hotel discussed the issue

of customer satisfaction:

Customer satisfaction is one of the main

non-financial indicators hotel

management uses to monitor

performance. For example, the hotel has

set the customer satisfaction score at least

8.5 from 10 point-scale which the survey

done via the online travel agencies.

Furthermore, the hotel will take

consideration of the customer complaints

EBIC 2019 - Economics and Business International Conference 2019

320

thoughtfully. The hotel has strategically

tiedthe employee's benefit or bonuses to

customer satisfaction. The hotel has

differentiated its strategy by building

customer experience as the culture of the

hotel. The bonuses to employees who

receive complaints and who do not show

improvement will be deducted according

to the hotel's criteria.

(Excerpt from the interview on 7

November 2018 with the

respondent Case 2 Hotel)

Case 2 interviewee stressed that the effort to

personalize the services to its customer will build,

retain and increase a strong relationship. Other hotel

financial managers also emphasized customer

relationships. This is especially true in the case of

the leading luxury hotel with its long history in the

hospitality industry. Valuing long-term customers is

important.

5 CONCLUSIONS AND

SUGGESTIONS

The hotel industry is facing the challenge of

reducing its costs significantly and to structure an

efficient internal processof it is to compete

successfully in a competitive market. Hotels in

Taiwan are no exception. Management accounting

reportsaretherefore of great importance to hotel

managers on a day-to-day and long-term basis.There

are a variety of factors which influence the usage of

management accounting practices in the hotel

industry. From the interviews, the main factors can

be categorized under three (3) labels.

Firstly, size. The size of the companyis

positively associated with management accounting

sophistication used by the hotels. Small hotels tend

to rely on trust between the owner/shareholder and

CFO, while larger hotels would set up a controlling

system by which management accounting reports are

put in place for management.

Secondly, sophistication. Modern-day tools are

sophisticated and require highly skilled personnel.

They may consider to be able to implementing

activity-based costing, and balanced scorecards, for

example. These implementations due to the

complication when implementing require to have

strong support from the high levels of management.

And, thirdly, complexity. The hospitality

industry, specifically hotels, to able to survive in

today’s highly competitive market, must adopt and

make use of management tools for making routine

decisions, and for the continuous management of

many critical operations. This research learned that

somehotels are still not generally using very

sophisticated management accounting practices.

Most of the hotels used tools relate to cost

determination and for controlling purposes.

The interview data revealed that many

sophisticated practices were not being used. Among

there are the following: the lean method in

warehouse management, reduction of movement of

housekeeping, supply chain management software,

just-in-time, and real-time information reports.

These tools were rarely mentioned by interviewees.

When compared to the manufacturing industry, for

example, where such sophisticated tools are

common, hotels continue using rather simple

management accounting practices. Even though the

hotel business is highly competitive, and becoming

more so, there seems to be a reluctance to consider

implementing practices which would improve the

precision of key decisions and increase

sustainability. Particularly owners of smaller hotels

are urged to consider adding more complex

management accounting tools to their operations.

Consumers are changing, too. Millennials are

increasingly looking for unique and authentic

experiences. They are today’s ‘baby boomers’. They

have money and time to travel, and they increasingly

expect technology to aid, inform and enrich their

travels. Several new ‘smart’ applications now

available include intuitive booking apps, chatbots,

and mobile check-in/check-out. Today’s and future

hotel customers expect technology to be integrated

into many areas of the travel experience. To meet

this trend, the ability of hotel companies to work in

partnership with technology providers has become

increasingly important. Hotel owners and investors

should take note.

In addition, another feature of today’s world has

to do with data generation, storage and use. Cloud

storage has further changed the game, giving

accommodation providers, such as hotels, easy

access to diverse real-time data. Such data enables a

more personalized and efficient service.

Operationally it allows providers to use data to tailor

guest experiences faster and create a more

personalized relationship with them. With this trend

comes a growing responsibility to handle data

responsibly, respecting consumer preferences

and rights.

Due to an increasing demand for branded

experiences, owners and investors are advised to

Management Accounting in the Hospitality Industry: Taiwan Hotel Case Studies

321

consider the merits of affiliating with a branded

hotel chain. The recent addition of multiple new

brands by big-branded players illustrates the level of

capacity in the hotel market. There is little doubt

that hotels need to have personnel who can assist

decision making in all levels of the hotel business.

It is hoped that this study fills a gap in the

literature by using an in-depth research methodology

that focused on how management accounting tools

and practices are being accepted and being

implemented. Of course, other aspects should be

further explored, too. The interaction of Information

Technology (IT) and contemporary management

accounting systems is an emerging research area.

Financial issues regarding hotel performance could

be further explored. Another important topic for

research could be identifying factors that affect the

improvement of hotel financial performance, for

example exploring the relationship between

Accounting Information Systems (AIS) user

satisfaction and activity-based costing(ABC) use

with respect to hotel financial performance, lean

management in the hotel industry, and sustainability

reporting of the hotel industry.

ACKNOWLEDGMENT

The author would like to thank the Ministry of

Foreign Affairs of the Republic of China (Taiwan)

for the support through the 2018 Taiwan Fellowship

Program (MOFATF201800090). In that connect,

thanks to Professor Hsuan-Lien Chu from

Department of Accountancy, College of Business,

National Taipei University. It was he who hosted

this Taiwan Fellowship Program. Also, to Assistant

Professor SheChih Chiu who accompanied the

author and assisted in the interviews as interpreter.

Finally, special thanks to the CFOs and senior

financial managers of the five hotels for their

cooperation and for providing such a wide range of

rich and insightful information.

REFERENCES

Awang, K.W., Ishak, N.K., Radzi, S.M., & Taha, A.Z.

(2008). Environmental variables and performance:

Evidence from the Hotel Industry in Malaysia.

International Journal of Economics and Management,

2(1), 59-79.

Briciu, S., Scorte, C., & Mester, I. (2013). The impact of

accounting information on managerial decision –

Empirical study conducted in the hospitality industry

entities in Romania. Theoretical and Applied

Economics, 9(586), 27-38.

Burgess, C. (2017). Managerial Competencies for U.K.

Hotel Financial Controllers: Are They Hospitality

Managers or Accountants? The Journal of Hospitality

Financial Management, 25(1), 27–43. Available at

https://doi.org/10.1080/10913211.2017.1313612

Chiu, Y.-H., & Huang, C.-W. (2011). Evaluating the

optimal occupancy rate, operational efficiency, and

profitability efficiency of Taiwan’s international

tourist hotels. The Service Industries Journal, 31(13),

2145–2162.

https://doi.org/10.1080/02642069.2010.503889

Choi, B. C., & Pak, A. W. (2005). A catalog of biases in

questionnaires. Preventing chronic disease, 2(1), A13.

CIMA. (2008). Activity Based Costing Topic Gateway

Series No. 1. Available at

http://www.cimaglobal.com/Documents/ImportedDoc

uments/cid_tg_activity_based_costing_nov08.pdf.pdf

(Retrieved on 24 August 2019).

El-Shishini, H. (2017). The Use of Management

Accounting Techniques at Hotels in Bahrain. Review

of Integrative Business and Economics Research, 6,

64-77.

Fathi, Z., & Dozdahiri, E.S.M. (2015). A survey of

activity-based costing in hotel industry. Management

Science Letters, 5, 855-860.

Fulcoon, M. (2018). Taiwan’s Hotels Grapple with

Oversupply. Taiwan Business Topic. Available at

https://topics.amcham.com.tw/2018/12/taiwans-hotels-

grapple-with-oversupply/ (Retrieved on 3 August

2019)

IHG. (2018). IHG Annual Report. Available at

https://www.ihg.com/hotels/gb/en/ (Retrieved on 12

March 2019).

Institute of Hotel management Bhubaneswar, Ministry of

Tourism, Government of India. (2017). Available at

http://www.ihmbbs.org/upload/2)Classifi%20of%20H

otels.pdf (Retrieved on 5 August 2019).

Jeffrey, D., Barden, R. R. D., Buckley, P. J., & Hubbard,

N. J. (2002). What Makes for a Successful Hotel?

Insights on Hotel Management Following 15 Years of

Hotel Occupancy Analysis in England. The Service

Industries Journal, 22(2), 73–88. Available at

https://doi.org/10.1080/714005078

Market Entry. (2018). Tourism and Hotel Industry in

Taiwan: Analysis of Growth, Trends and Progress

(2015-2020). Available at

https://www.mordorintelligence.com/industry-

reports/market-entry-tourism-and-hotel-industry-in-

taiwan (Retrieved on 3 August 2019).

Makrigiannakis, G., & Soteriades, M. (2015).

Management Accounting in the Hotel Business.

International Journal of Hospitality & Tourism

Administration, 8(4), 47-76.

Masset, P., & Weisskopf, J.P. (2019). Top 10 Trends

Reshaping Hospitality in 2019. Available at

https://hospitalityinsights.ehl.edu/2019-top-

hospitality-trends (Retrieved 25 August 2019).

EBIC 2019 - Economics and Business International Conference 2019

322

Micheli, P., and Manzoni, J. F. (2010). Strategic

Performance Measurement: Benefits, Limitations and

Paradoxes. Long Range Planning. 43. 465-476.

10.1016/j.lrp.2009.12.004.

Min, H., & Min, H. (1997). Benchmarking the quality of

hotel services: managerial perspectives. International

Journal of Quality & Reliability Management, 14,

582–597.

Mjongwana, A., & Kamala, P. N. (2018). Non-financial

performance measurement by small and medium sized

enterprises operating in the hotel industry in the city of

Cape Town. African Journal of Hospitality, Tourism

and Leisure, 7(1), 1-26.

Mordor Intelligence. (2018). Industry Report. Available at

https://www.mordorintelligence.com/industry-reports

(Retrieved on 8 March 2019).

Pavlatos, O. (2011). The impact of strategic management

accounting and cost structure on ABC systems in

hotels. The Journal of Hospitality Financial

Management, 19(2), 37-55.

Poldrugovac, K., Tekavcic, M., & Jankovic, S. (2016).

Efficiency in the hotel industry: an empirical

examination of the most influential factors. Economic

Research-Ekonomska Istraživanja, 29(1), 583–597.

https://doi.org/10.1080/1331677X.2016.1177464

Sheel, A. (2017). Hotel Industry Performance in 2016–

2017 and the JHFM Index. The Journal of Hospitality

Financial Management, 25(2), 75–76. Available at

https://doi.org/10.1080/10913211.2017.1406743

Shieh, H.-S. (2012). Does Cost Efficiency Lead to Better

Financial Performance? A Study on Taiwan

International Tourist Hotels. The Journal of

Hospitality Financial Management, 20(1), 17–30.

Available at

https://doi.org/10.1080/10913211.2012.10721889

Tsai, H., Song, H., & Wong, K. K. F. (2009). Tourism and

Hotel Competitiveness Research.Journal of Travel &

Tourism Marketing, 26(5–6), 522–546. Available at

https://doi.org/10.1080/10548400903163079

Voellm, D. J. (2017). Taiwan Hotel Market Update. HVS

Asia-Pacific. Available at

https://www.hvs.com/article/8094-taiwan-hotel-

market-update (Retrieved on 3 August 2019).

World Travel & Tourism Council. (2018). Travel and

Tourism Economic Impact 2018: World.Available at

https://www.wttc.org/ (Retrieved on 15 March 2019).

Yu, L., & Huimin, G. (2007). An Analysis of Hotel

Financial Management in China. The Journal of

Hospitality Financial Management, 15(2), 39–48.

Available at

https://doi.org/10.1080/10913211.2007.10653841

Management Accounting in the Hospitality Industry: Taiwan Hotel Case Studies

323