The Instrument Development for Evaluating the School Budgeting

Planning Management at Yogyakarta Elementary School

Siti Maisaroh

1

, Dedek Andrian

2

1

Elementary School Teacher Education, Yogyakarta PGRI University, Yogyakarta, Indonesia

2

Department of Mathematics Education, Universitas Islam Riau, Pekanbaru, Indonesia

Keywords:

Instrument, Development Research, Evaluating, School Budgeting Planning Management, Elementary School

Abstract:

The purpose of this research is to develop the instrument to evaluate the Budgeting Planning Management at

Yogyakarta Elementary Schools. Type of This research is a development research consisting of four phases: 1)

phase of the initial investigation, 2) phase of design and 3) phase of expert validation, and 4) phase of the trial.

From the phase of initial investigation obtained 6 components of the evaluation that is; 1) school program;

2) Financing; 3) fund source;4) Planning;5) organizing; 6) Implementation; 7) supervision; 8) evaluation.

The phase of design is done by studying from various the theory and making the instrument in the form

the questionnaire as many as 31 items. The phase of expert validation is done by 2 evaluation experts, the

school management expert and, and 6 management practitioners. The assessment results from expert and

practitioners were analyzed using the Aiken’s formula. The phase of the trial was analyzed using confirmatory

factor analysis (CFA) and construct reliability with the assistance Lisrel software 8.80. From the analysis

results of validity and reliability acquired 31 items of the questionnaire were valid and feasible to be used to

evaluate the Budgeting Planning Management at Yogyakarta Elementary Schools.

1 INTRODUCTION

Government Regulation No. 17 of 2010 concerning

Education Management and Implementation,

especially in articles 50 and 51 states that the unit of

education must plan and develop education policies

following schools regulation. One of the education

policies that are the obligation of the school is to

develop an annual work plan and prepare an annual

income and expenditure budget. The government

hopes that with the planned school activities, the

government will ease in monitoring and evaluating

school development. This school activity plan can

be a reference and working guide in submitting what

educational resources needed in developing schools’

program.

School expenditure budget management will

make it easier for schools to find out what activities

will be carried out by the school so that the expected

goals can be achieved and school obligations can

be fulfilled. In terms of participation, school

budget management can provide an overview of

what is needed and what support is needed by

school stakeholders both internally and externally.

This is in line with the regional autonomy policies

developed within the scope of formal education,

namely School-Based Management (SBM). SBM

makes the school’s education development better in

terms of school management, school funding, and

supervision. Schools become more independent and

have a responsibility for managing and developing

their schools. Schools will ease and flexible

in developing school programs have designed or

planned following the needs and the school resources

capabilities.

Budget planning is an activity of planning

activities for the future and how much funding

is needed to support the intended activities and

to explore sources of funds, collect, also describe

into activities that have been programmed for

the achievement of an educational goal. School

financing planning requires accurate and complete

data so that all future planning needs can be

anticipated in the draft budget. The position of the

Principal as a leader must be able to develop some

dimensions of administrative actions. The ability to

apply educational programs into cost equivalents is

important in preparing the budget. Activities to make

budgets are not routine or mechanical work, involve

consideration of the basic purposes of education and

Maisaroh, S. and Andrian, D.

The Instrument Development for Evaluating the School Budgeting Planning Management at Yogyakarta Elementary School.

DOI: 10.5220/0009038800130017

In Proceedings of the Second International Conference on Social, Economy, Education and Humanity (ICoSEEH 2019) - Sustainable Development in Developing Country for Facing Industrial

Revolution 4.0, pages 13-17

ISBN: 978-989-758-464-0

Copyright

c

2020 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

13

programs Based on these perspectives the planning

of school education costs must be able to open the

way for the development and explanation of concepts

about desired educational goals.

Harjanti’s (2010) research on budget planning

concluded that there were still important school

needs that had not been identified, budget planning

implemented in schools was still not accordance

to school needs, schools’ program targets, program

alternatives selection, and selection of effective

costs. If budget planning is not done well,

then budget implementation often appears important

but unplanned programs beforehand. activities to

evaluate the budget will be difficult because some

components of the budget are not recorded in

planning but implemented.

The school budgeting will be a success if

involve of all parties, namely the community, parent,

principal, teachers, schools committee and students.

The results of research conducted by Yuliastuti &

Prabowo (2014) state that the principals, teachers,

and school committees have involved in the budget

planning process of the school. the principals and

teachers in planning the school budget in the good

category but the school committee is still lacking in

planning and controlling the process of the school

budget planning. The school committee also signed

the ratification of the APBS but in the budget planning

process, the school committee didn’t get involved.

In the preparation of the school budget, a budgeting

team has been formed, but the school does not

yet understand how to estimate the ideal budget,

so many school programs are not carried out by

school, and there was a lack of commitment to the

budget prepared. Reports made by schools were less

accountable because the administration wasn’t neatly

arranged. Budgeting management transparency is

still lacking because the APBS is not disseminated to

school residents.

The elementary school in Yogyakarta also faces

a big dilemma between the strong desire to provide

quality-assured education on the one hand and the

fact that there is a lack of funds from the government

on the other side. Of the 93 Elementary Schools

in the city of Yogyakarta, the sources of funds in

the School Expenditure and Revenue Budget Plan

(SERBP) that come from School Operational Costs

(SOC) funds are on average 55 percent, from the

State School Operational Costs (SSOC) an average

of 24 percent, and those that come from school

committee contributions are on average 23 percent.

The use of financial resources for the construction and

procurement of school facilities and infrastructure

averages 22 percent, for school needs as much as 20

percent, for teaching and learning activities as much

as 19 percent, for honorariums as much as 16 percent,

for student activities as many as 16 percent, and for

other purposes as much as 3 percent (Setyaningrum,

2010).

Thus, the quality of education can be guaranteed

by program synchronization with the budget planning

at each year. Planning is the first and foremost

thing to do. If in carrying out activities there is no

planning, then the goal will not be achieved so that

waste occurs and activities are not as expected. based

on the problems that have found, the development of

instruments to evaluate budget planning needs to be

carried out so that weaknesses or shortcomings can be

identified that need to be improved in improving the

quality of learning through the management of good

school budgets.

The purpose of budget planning is to facilitate

future work, so decisions can be made with careful

planning. According to Robbins & Coulter (2012:

204), ”planning involves determining the objectives

of the organization, strategies for achieving goals,

and developing networks to achieve goals. Poston,

(2011: 5), states that school budget planning is part

of prediction, communication, and decision making,

(Lipham, 1985: 237) ”School budgets are systematic

planning for income and expenditure related to

educational programs and supported by data that

reflects the needs, goals, and results that the school

wants to achieve.

Anthony & Govindarajan (2005: 373) states that

budgeting planning is one of important activity for

effectively developing, controlling, and planning an

institution like schools. Budget planning is one

strategy to help the program made by schools in

achieving institutional goals have planned . Budget

planning is affected by the length of management

carried out by schools stakeholders (Sato, 2012).

Based on the expert statement above, it can conclude

that budgeting planning management of schools is an

important thing have to consider in implementing an

education program.

(Sisk, 1969) states that school management is a

unity of all resources through a process of planning,

organizing, directing and controlling. Education

management is activities that related to education

management at school (Sun, 2014). Management

made by stakeholders aims to check standards or

criteria with their implementation, which can increase

the attitude of the value of the individual in the

workgroup (Berggren and S

¨

oderlund, 2008). School

management is various roles in education were

made by schools to give education and training to

schools community who are carried out teaching and

ICoSEEH 2019 - The Second International Conference on Social, Economy, Education, and Humanity

14

learning process (Pant and Baroudi, 2008). School

management is a system needed to handle student

diversity so that the school can get the goal of the

school program was the transferring knowledge to

the student (Passailaigue and Estrada, 2018; Oplatka

and Arar, 2017) stated that school management is

an important part to implement good atmosphere for

school staff in getting a good quality of teaching and

learning in the classroom.

2 RESEARCH METHOD

Research on instrument development to evaluate The

Instrument Development for evaluating the School

Budgeting Planning Management at Yogyakarta

Elementary Schools using research and development.

The purpose of this research is to develop a valid and

reliable instrument of a questionnaire for evaluating

the budgeting planning management at Yogyakarta

elementary schools.(Borg, 1983) model was an

appropriate model for carrying out this research. This

model consisting of 10 steps which are simplified into

four steps:

• phase of initial investigation

• phase of design

• phase of expert validation

• phase of trials

Initial investigations were done by studying

the theory from a variety of sources and FGD

with 10 Participants consisting of 6 expert and 4

practitioners. The purpose of the FGD is to get

what is component can be used to evaluate budgeting

planning management of Elementary Schools of

Yogyakarta Province. The instrument design

phase was conducted by developing a questionnaire.

Validation Phase conducted by 2 evaluation experts

or 1 measurement expert and 4 practitioners. The

validation phase aims to see the validity of the

contents of the developed questionnaire. Content

validity affects the accuracy of data to be obtained

in the field. The trial used to see the validity and

reliability of component or indicators have got from

studying the theory.

2.1 Population and Sample

The population in this study were all elementary

schools from 5 districts in Yogyakarta Province,

namely; 289 schools from Kolun Progo Regency,

280 from Bantul Regency, 431 from Gunung Kidul

Regency, 379 from Sleman Regency, and 99 from

Yogyakarta City. The sampling technique in this

study is the Proportional Random Sampling Cluster

technique, which is school sampling in each region.

Sampling is based on the school from a defined

area using the Krejcie & Morgan table developed

from Isaac and Michael, if the population is 1,464

Elementary Schools with an error rate of 5%, the total

sample is 284 Primary Schools.

2.2 Population and Sample

The instruments in this study were expert validation

sheets and instrument effectiveness sheets.

Instrument validation sheet is used to assess the

content of the instrument being analyzed. the

instrument effectiveness sheet is used to test whether

the instrument is effective in gathering information.

The instrument to be developed in this study is

a questionnaire consisting of 8 components or

indicators, namely; school programs, financing,

Fund Source, Planning, Organizing, Implementation,

Supervision, and Evaluation.

2.3 Analysis Data Technique

Analysis data in this development research used

Content Validity uses Aiken’s Validity, Construct

Validity uses CFA, Cronbach’s Alpha, and Construct

Reliability. Aiken’s Validity used to see the content

quality of the instrument. CFA used to check the

construct validity of the instrument has developed.

Cronbach’ Alpha used to analysis the reliability of

items of instrument. The construct reliability used to

analysis the construct reliability of each indicator or

components.

3 RESULT & DISCUSSION

3.1 Content Validity

Content Validity analyzed with the help excel

program based on Aiken’s Formula. The assessment

of experts and practitioners analyzed from the score

have given through the assessment sheet. the result

shows that 31 items of the instrument has a high

category and middle category. 19 items with the

high category and 12 items with the middle category.

these results show that all items have developed by

researcher have a good category and can use to get

good data from the field.

The Instrument Development for Evaluating the School Budgeting Planning Management at Yogyakarta Elementary School

15

3.2 Reliability of Instrument

Reliability of instrument based on all items or items

total was analyzed with Cronbach’s Alpha. For

getting the reliability coefficient, the researcher gives

the instrument to the respondent as many as 30

respondents and analyzed using Cronbach’s Alpha

Formula with the help SPSS software. From the

analysis, the result was got the coefficient Cronbach’s

Alpha about 0.87. Based on this result can make a

conclusion that the instrument was developed by the

researcher was reliable.

3.3 Validity and Reliability of Construct

3.3.1 Confirmatory Factors Analysis (CFA)

CFA used to check so far model measurement has

developed by studying theory from various sources

is fit with data to have acquired from the field.

Measurement model can be said fit with the data

from the field if this model already fulfills criteria

or standard from statistics expert or consensus of

statistics expert based on statistics theory that is

Goodness of Fit Index. The result of analysis CFA

in this model can be seen in Table 1.

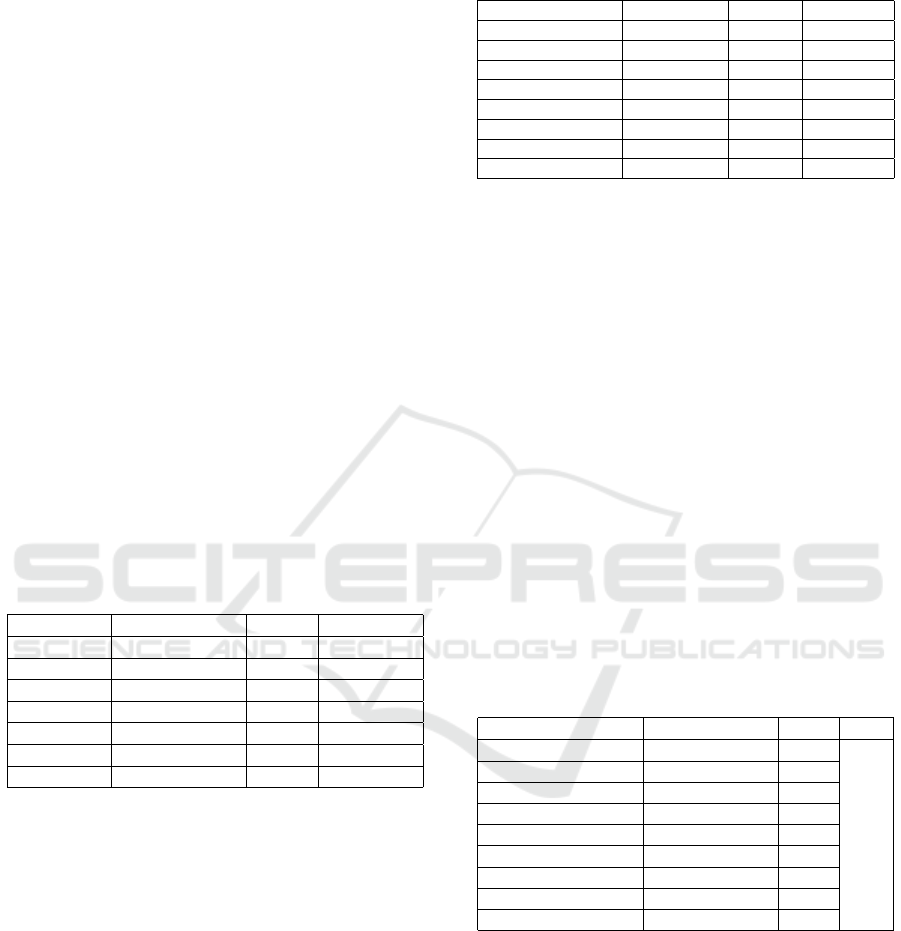

Table 1: Standard and Result of Goodness of Fit Model

Budgeting Planning Management.

GOF Standard Result Conclusion

Chi-Square P >0,05 0,4421 Fit

RMSEA RMSEA <0.08 0,000 Fit

GFI GFI ≥ 0.90 0.96 Fit

NFI NFI ≥ 0.90 0.95 Fit

CFI CFI ≥ 0.90 0.96 Fit

IFI IFI >0.80 0.96 Fit

RFI RFI 0-1 0.91 Fit

From table 1 acquired that seven criteria of GOF

show the data was fit with the measurement model

was built by the researcher. From this result can be

concluded that the measurement model has built from

studying theory from various sources was fit with data

were acquired at the field

CFA is the measurement model that shows one

latent variable can be measured by one or more

observed variables. CFA will see so far the observed

variables or indicators were got from studying the

theory are the variable builder. CFA will be helped by

Lisrel Software. At this analysis, observed variables

or indicators must meet established standard with

loading factor at standardized>0.3 or T-value>1.96.

The analysis result can be seen clearly in table 2

From Table above can be concluded that planning,

organizing, implementation, supervision, evaluation,

Table 2: Summary of Measurement Model of Manifest

Variables

Manifest Variables Standardized T–value Decision

Planning 0,48 12,28 Significant

Organizing 0,26 8,41 Significant

Implementation 0,65 15,1 Significant

Supervision 0,51 12,86 Significant

Evaluation 0,55 13,45 Significant

School program 0,63 13,98 Significant

Financing 0,73 15,08 Significant

Fund Sources 0,43 11,41 Significant

school program, financing, and fund sources are

significant so that eight indicators have found from

studying the theory were indicators as variables

builder of budgeting planning management variable.

indicators of budgeting management variable have

T-value score more 1.96 so that indicators have found

from studying the theory has fulfilled the good of

measurement standard.

3.3.2 Construct Reliability

Construct reliability used to the analysis level of

construct reliability from various indicators from

studying the theory both the references book

or journals have published at various publishers.

Good indicators are indicators have high construct

reliability coefficient is more 0.70. this reliability

was calculated with error and loading factor have

found from analysis uses CFA. the summary of CFA

analysis can be seen in Table 3 below.

Table 3: Construct Reliability

Observed Variables Loading Factor Error CR

Planning 0,70 0,51

0,82

Organizing 0,55 0,70

Implementation 0,84 0,20

Supervision 0,68 0,54

Evaluation 0,69 0,33

School program 0,80 0,37

Financing 0,85 0,27

Fund Sources 0,66 0,56

Total 2,31 1,20

Based on Table 3, it was got construct reliability

coefficient about 0.82. This value or coefficient more

good standard of measurement theory that is more

0.70. from this table can make a conclusion that all

of the indicators have found from studying the theory

were valid and reliable based on construct so that

this instrument can be used to get information or data

about the school budgeting planning management.

Evaluating an education program needs an

instrument valid and reliable based on content and

construct. the content validity shows how far

ICoSEEH 2019 - The Second International Conference on Social, Economy, Education, and Humanity

16

items have developed from indicators are fulfilled or

appropriate indicators definition or items represent

indicators have found from studying the theory of

various references sources, while construct explains

how far indicators are valid and reliable which marked

have good loading factor is more 0.30 (Andrian

et al., 2018) Feasibility of an instrument to evaluate

an education program is very important in the

measurement theory. This thing shows for getting

good data from field needed a good instrument. The

instrument becomes the main key in getting good

information or data in the field.

The instrument for evaluating the school

budgeting planning management already valid and

reliable in content and constructively (Wynd et al.,

2003). This instrument is expected to provide

convenience in evaluating the school budgeting

planning management at elementary school fo

Yogyakarta Province. The instrument has a good

validity of content and construct can give valid

information and the right conclusion (Setiawan and

Mardapi, ). The valid and reliable instrument will

describe what happened in the education program

evaluated. The valid and reliable instrument will give

accurate information about weakness and strengthen

of educational programs have created or designed

the government or private (Wright and Craig, 2011).

If an instrument was good in content and construct,

it will give a good conclusion in making a policy

(HADI et al., 2019).

4 CONCLUSIONS

Based on the analysis result can be made the

conclusion that the instrument was developed by the

researcher as many as 31 items were valid and reliable

in content and construct. Analysis of Aiken’s formula

shows all items have assessed by experts have score

or coefficient with middle and high category, while

the reliability of instrument based on total items

show coefficient from Cronbach’s Alpha is more 0.70.

Construct reliability was analyzed with CFA shows

all indicators have loading factor is more 0.3 or has

fulfilled the good standard of measurement theory,

while construct reliability has coefficient more 0.70.

The Instrument for evaluating the school budgeting

planning management is feasible to get good or valid

data in the field.

REFERENCES

Andrian, D., Kartowagiran, B., and Hadi, S. (2018). The

instrument development to evaluate local curriculum

in indonesia. International Journal of Instruction,

11(4):921–934.

Berggren, C. and S

¨

oderlund, J. (2008). Rethinking project

management education: Social twists and knowledge

co-production. International Journal of Project

Management, 26(3):286–296.

Borg, W. (1983). Gall. m. d. Educational research (4th ed.).

New York: Longman.

HADI, S., ANDRIAN, D., and KARTOWAGIRAN, B.

(2019). Evaluation model for evaluating vocational

skills programs on local content curriculum in

indonesia: Impact of educational system in indonesia.

Eurasian Journal of Educational Research (EJER),

(82).

Oplatka, I. and Arar, K. (2017). The research on educational

leadership and management in the arab world since

the 1990s: A systematic review. Review of Education,

5(3):267–307.

Pant, I. and Baroudi, B. (2008). Project management

education: The human skills imperative. International

journal of project management, 26(2):124–128.

Passailaigue, R. M. and Estrada, V. (2018). Educational

management with technology support. International

Journal of Applied Engineering Research,

13(12):10647–10650.

Sato, Y. (2012). Optimal budget planning for investment in

safety measures of a chemical company. International

Journal of Production Economics, 140(2):579–585.

Setiawan, A. and Mardapi, D. Supriyoko, & andrian,

d.(2019). the development of instrument for

assessing students’ affective domain using self-and

peer-assessment models. International Journal of

Instruction, 12(3):425–438.

Setyaningrum, T. (2010). The education budget

commitment in the education city of Yogyakarta still

hasn’t reached 20 percent. Jurnal Populasi.

Sisk, H. L. (1969). Principles of management: A systems

approach to the management process. South-western

Publishing Company.

Sun, M. (2014). 30 years of chinese educational

management: achievements, characteristics and

problems. International Journal of Educational

Management, 28(3):340–348.

Wright, P. M. and Craig, M. W. (2011). Tool for assessing

responsibility-based education (tare): Instrument

development, content validity, and inter-rater

reliability. Measurement in Physical Education and

Exercise Science, 15(3):204–219.

Wynd, C. A., Schmidt, B., and Schaefer, M. A. (2003).

Two quantitative approaches for estimating content

validity. Western Journal of Nursing Research,

25(5):508–518.

The Instrument Development for Evaluating the School Budgeting Planning Management at Yogyakarta Elementary School

17