Time-driven Activity based Costing Method for Calculating Unused

Capacity of Endoscopy Services: A Case Study of XYZ Hospital

Roberta Fifin Amandaningrum and Thomas H. Secokusumo

Faculty of Economic and Business, Universitas Indonesia, Jl. Salemba Raya No. 4 Jakarta 10430, Indonesia

Keywords: Hospital, Time-Driven Activity based Costing, Cost Analysis, Unused Capacity, Indirect Cost, Endoscopy.

Abstract: Competition in the healthcare industry and the growth of Endoscopy services prompted XYZ Hospital to

evaluate the cost of its services. Management of quality and cost control are key to success in applying value-

based healthcare strategy. The purpose of this case study is to demonstrate how Time-Driven Activity Based

Costing (TDABC) method is applied in Endoscopy unit of XYZ Hospital by understanding the service

processes and the indirect cost allocation using time as the main cost driver so that unused capacity can be

identified, and capacity-based income statement can be prepared for better cost control. This is a descriptive

case study with qualitative and quantitative approaches through cost analysis in the Endoscopy unit. Data

collection based on XYZ Hospital database from January to December 2017 and the results of interviews and

a direct observation conducted in October and November 2018. The result of this case study concludes that

TDABC enables detail and accurate cost and profitability analysis of endoscopy services where indirect costs

are allocated according to the actual usage of resources. Therefore, the efficiency indicator for cost control

can be clearly defined and more measurable by showing the unused capacity of each resource group in the

capacity-based income statement.

1 INTRODUCTION

The hospital industry is trying hard to run its business

process efficiently by always stressing on quality

control, cost control, and patient safety. With the

purpose of cost control implementation, hospital

needs to do cost analysis with appropriate cost

method for all its services. Result of cost analysis will

be used for the decision maker in making policies

about efficiency program, pricing, and business

development strategy. (Porter, Michael E.; Lee, 2013)

The number of hospitals in Indonesia has

increased by around 1,000 hospitals since 2011 until

2017. The growth of hospitals per year reached 13.3%

in 2011 to 2014 and then weakened to around 4.4%

per year in 2014 until 2017. In 2017, 63% of the total

2,724 hospitals in Indonesia were private hospitals.

(Britton, Koseki, & Dutta, 2018)

Since January 1

st

, 2014, Indonesia healthcare

industry has been transforming by the

implementation of Jaminan Kesehatan Nasional

(JKN) conducted by Badan Penyelenggara Jaminan

Kesehatan (BPJS). Until 2017, member of BPJS is

estimated around 175 million people. However, most

of the tariff assigned by BPJS (INA CBGs) are far

below the economic price of private hospital

operations. This gap between the regular tariff of the

hospital and the tariff assigned by BPJS put the

healthcare industry in a big challenge. (Thabrany,

2017).

The hospital business is basically a capital and

labor intensive and carrying out business as well as

social functions. This condition requires operational

management to balance its profitability, service

quality and socio-economic conditions of the

community.

A systematic review of literature conducted by

Keel et al. in 2017 shows that nowadays the

healthcare industry is eagerly applying value-based

healthcare strategy. The hospital’s ability to

understand the cost of care and calculate it

appropriately will enable the hospital in evaluating its

health outcomes and cost for better value delivery.

The study also shows that Time-Driven Activity

Based Costing (TDABC) is a cost accounting system

that applicable in the hospital industry and can help

the hospital in managing cost efficiently. (Keel,

Savage, Rafiq, & Mazzocato, 2017)

XYZ Hospital is type B hospital which is

accommodated by outpatient and inpatient facilities

380

Amandaningrum, R. and Secokusumo, T.

Time-Driven Activity based Costing Method for Calculating Unused Capacity of Endoscopy Services: A Case Study of Xyz Hospital.

DOI: 10.5220/0008431503800387

In Proceedings of the 2nd Inter national Conference on Inclusive Business in the Changing World (ICIB 2019), pages 380-387

ISBN: 978-989-758-408-4

Copyright

c

2020 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

with 355 beds and operated total by 1.400 employees.

The number of endoscopy procedures has been

growing about 15% in 2017 (873 procedures) from

2016.

XYZ Hospital has been struggling in estimating

cost per service care and valuating hospital

profitability. Cost calculation in XYZ Hospital is

carried out by traditional cost accounting method

which allocates hospital overhead cost by its service

volume. This cost allocation method creates flat cost

allocation for each service or procedure, therefore,

some services are overcosted or undercosted.

The implementation of Time-Driven Activity-

Based Costing (TDABC) in healthcare has been

growing and has shown its strengths. TABCD simply

use time as the main cost driver, replacing many cost

drivers in Activity-Based Costing method. TDABC

delivers a powerful method for cost analysis because

it provides more accurate cost method than the

traditional method and simpler than Activity-based

costing (Demeere et al.; 2009)

2 METHODOLOGY

This study is a single-case (holistic) design type. This

is a descriptive case study with a qualitative and

quantitative approach through cost and profitability

analysis in the Endoscopy unit. This study illustrates

the application of cost calculation of Endoscopy

procedures in the Endoscopy unit of XYZ Hospital

using Time-Driven Activity Based Costing method.

(Yin, 2013).

Data collection were from primary and secondary

data. Primary data were collected from the interview

result. Interviews were conducted in October and

November 2018 for a Head of Endoscopic Unit, one

internal medicine physicians and two nurses in

Endoscopic unit. Secondary data were collected from

accounting and transaction reports (billing report) of

January – December 2017 and also standard operating

procedures of the endoscopic unit.

2.1 Framework of TDABC Steps

In this study, the steps of applying the TDABC

method was adopted from a pilot study on the

implementation of TDABC at the Metro Health's

Outpatient Clinic (Clark & Sopariwala, 2017), and

are complemented by the studies conducted by

(Campanale, Cinquini, & Tenucci, 2014) and (Keel et

al., 2017).

The steps of applying the TDABC method at the

XYZ Hospital are as follows:

1. Mapping The Process of Endoscopy Procedures

2. Identifying Cost of Resource Group (Cost of

Capacity Supplied)

3. Determining Practical Capacity of Resource

Group (Minutes)

4. Calculating Cost of Resource Group per Minute

(Capacity Cost Rate)

5. Determining The Numbers of Procedures

6. Obtaining Time Estimation of Each Procedure

7. Calculating Total Time Usage and Cost for Each

Resource Group

8. Determining Unused Capacity Costs and Creating

Capacity-Based Income Statement.

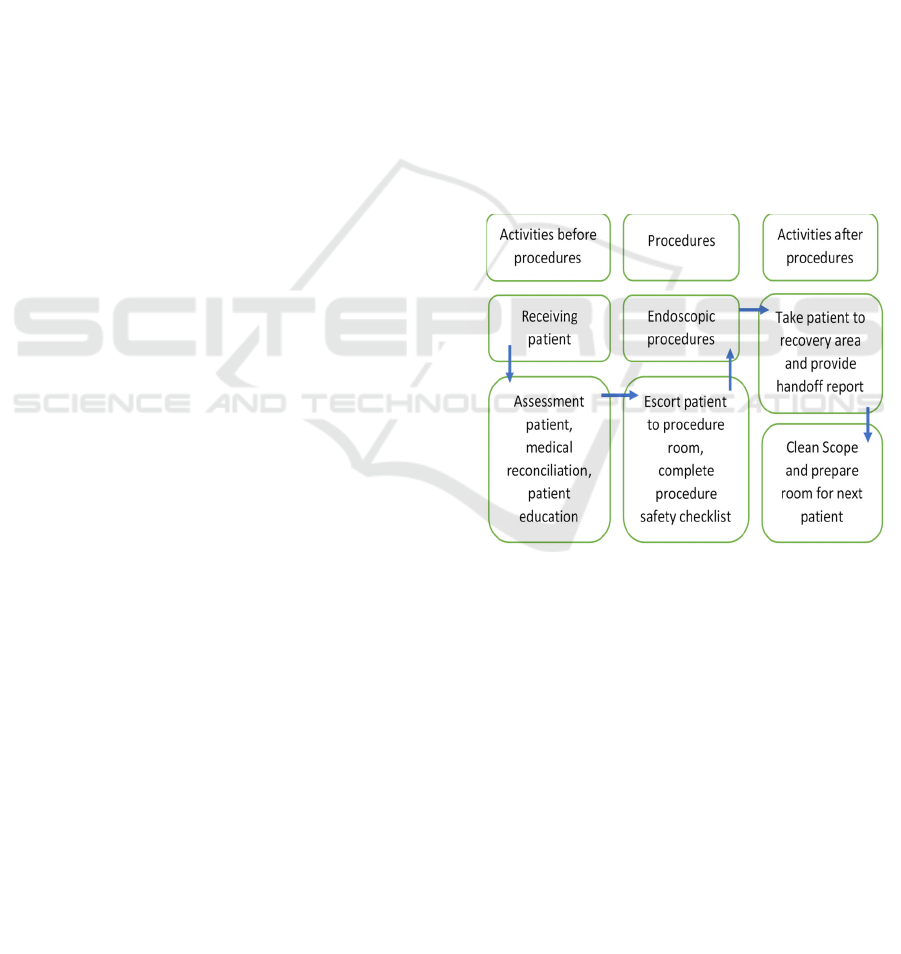

The process mapping shows what resources (who) are

used to carry out activities during certain times and its

frequencies (how). At this stage, the resource group

is identified.

The process stages of endoscopy procedures were

generated from the hospital's standard operating

procedures of the endoscopy unit and the interview

results.

Figure 1: The main activities for endoscopic procedures.

In identifying cost of capacity supplied, the direct

and indirect costs are determined into each group of

resources used. Direct and indirect cost data are

obtained from accounting reports.

Practical capacity is obtained by identifying the

capacity of the resource group used such as employee

work hours, hours of machine/tool usage. The

practical capacity does not include breaks or

downtime. The number of hours of effective work

(practical capacity) is set in minutes.

The amount of capacity cost rate is determined by

dividing the cost of capacity supplied with practical

capacity, the formula can be seen in equation (1). At

this stage, capacity cost rates are calculated for each

resource group.(Kaplan & Anderson, 2007).

Time-Driven Activity based Costing Method for Calculating Unused Capacity of Endoscopy Services: A Case Study of Xyz Hospital

381

Cost of capacity supplied

Capacity cost rate =

Practical capacity of

resources supplied

(1)

The number of frequency of activities (endoscopy

procedures) is attained from transaction data in the

hospital information system.

Time estimation of each endoscopic procedure

can be identified from interviews with key parties

(physicians, nurses, etc.) The time estimates gained

from the interviews can be validated through direct

observation of Endoscopic procedures

The actual total time (minutes) used by each

activity (endoscopic procedure) is the result of the

time estimation of procedure multiplied by the

volume of procedure. While the total cost used for all

endoscopic procedures is obtained by multiplying the

total estimated time of each procedures with the cost

per minute (the capacity cost rate).

The total cost is the sum of the costs of each

procedure. If the total cost of all procedures is smaller

than the cost of capacity supplied, then the difference

is the cost for unused capacity. By knowing the

unused capacity costs of each resource group per

procedure, a Capacity-Based Income Statement can

be prepared.

3 RESULTS AND DISCUSSION

3.1 The Implementation of TDABC

3.1.1 The Process of Endoscopic Procedures

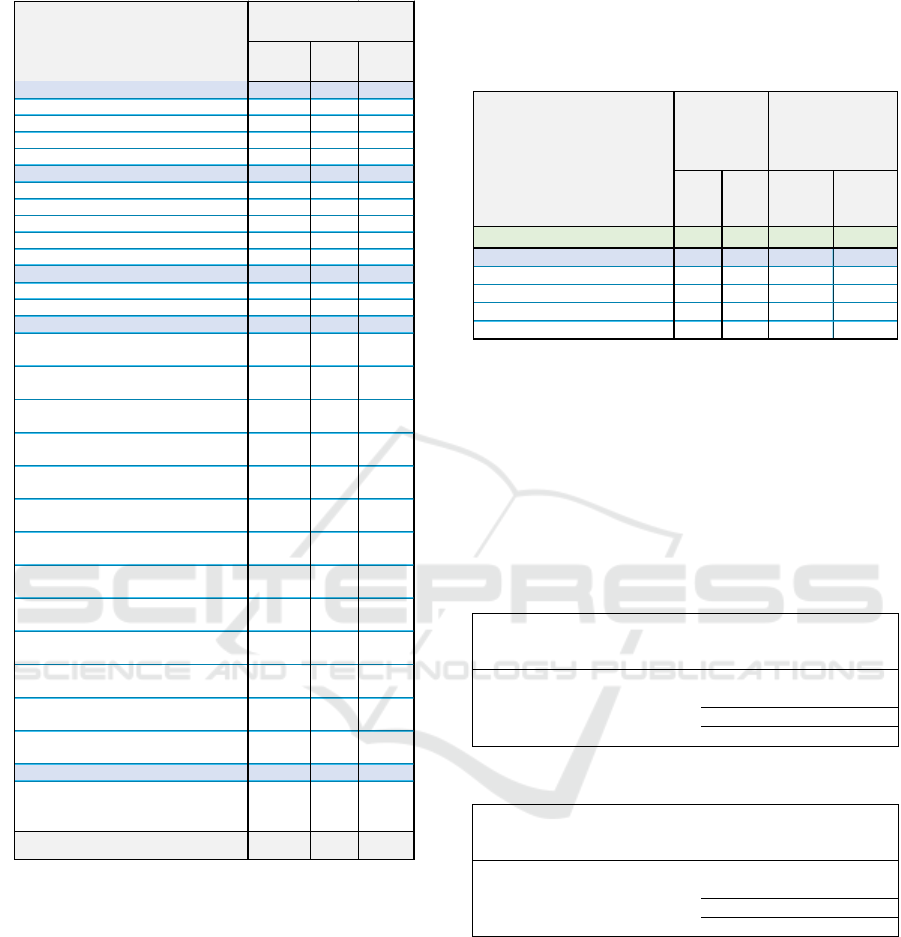

The service process in Endoscopy unit of XYZ

Hospital is carried out in 3 stages, namely pre-

procedure, intra procedure and post procedure. From

service process mapping (figure 2), it can be

identified resource used in each service activities

which are personnel (physicians, nurses), room,

equipment, supplies (drugs).

Figure 2: The main activities for endoscopic procedures.

3.1.2 Cost of Capacity Supplied

After resource groups (personnel, room, equipment,

supplies) are identified, the next step is to identify

each cost of capacity supplied of resource groups for

each endoscopy procedure. This step group costs into

direct costs, indirect costs and not allocated costs.

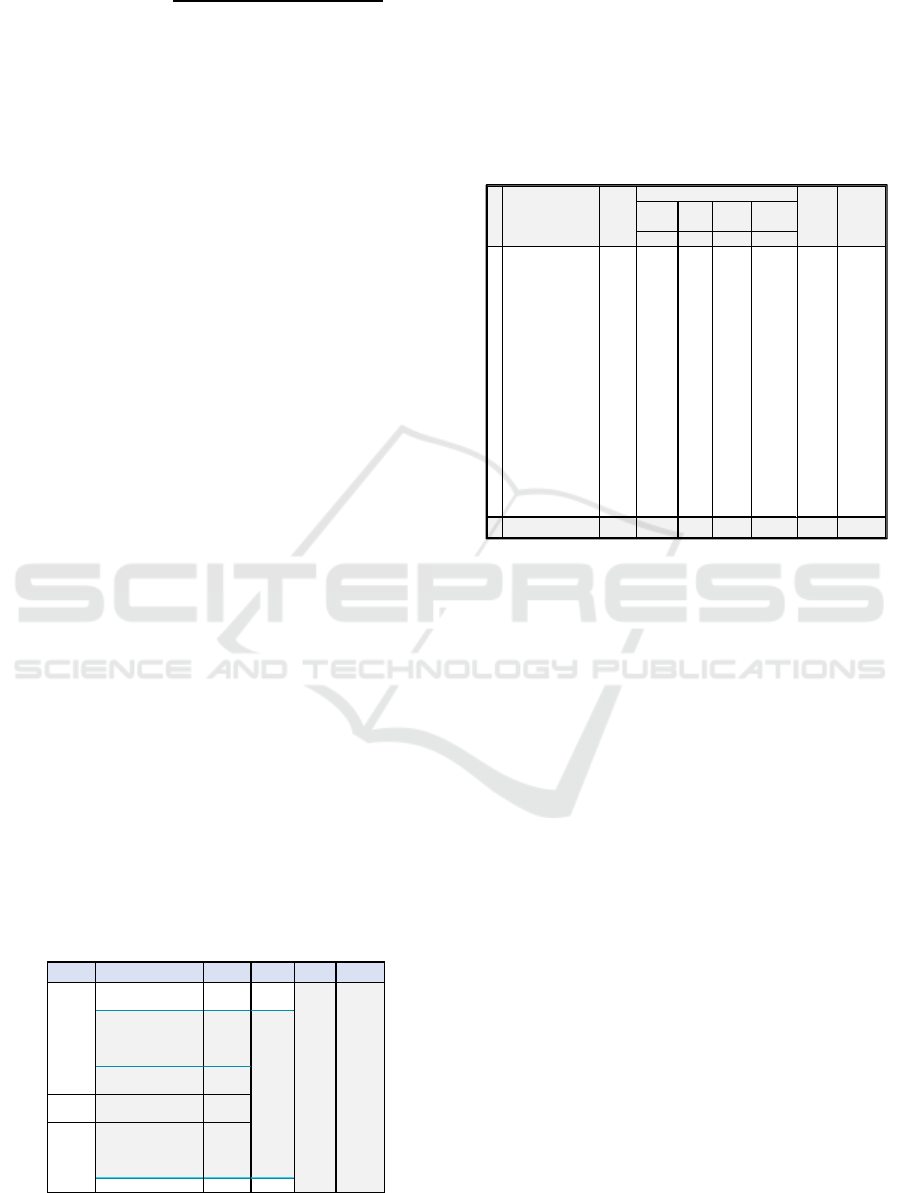

Table 1: Cost of Capacity Supplied of Resource Group.

In Table 1, as income statement report of 2017,

the total direct cost consisting of physician and nurse

fee, drugs and other medical supplies expenses is

Rp.1.759 million. Total indirect cost amount to

Rp.1.060 million consisting of personnel expenses

(salary etc.) Rp. 342 million, room expenses

(electricity, maintenance, etc.) Rp. 82 million,

medical equipment expenses (depreciation,

maintenance, etc.) Rp. 636 million. Not allocated cost

which consists of office department and other

supplies expenses amount to Rp. 171 million.

Office department expenses are not directly

related to procedure activities, while other supplies

expenses are difficult to trace as direct costs for each

endoscopy procedure. Hence, these costs are included

in the not allocated cost group which will be

presented separately in capacity-based income

statement. So that costs can be analyzed in more

detail and accurately. (Sopariwala, 2017)

3.1.3 Practical Capacity

Determining the practical capacity of a resource

group is based on the effective working hours of the

personnel because room and medical equipment can

only function when there are nurses operating.

The number of working hours in 2017 is 291 days

(1.790 hours). The total effective working hours per

year for 1 nurse is 1.790 working hours – (12 day off

Stages Activity Personnel Equipment Room Direct Cost

Assessmen patient, medical

reconciliation, patient education

Physicians,

Nurses

Procedures safety checklist,

patient observation, equipment

preparation, patient's data,

physicians colaboration

Physicians,

Nurses

Premedication & sedation Physicians,

Nurses

Intra

Procedure

Endoscopy Procedures Physicians,

Nurses

Physicians : prepare patient's data

image and handoff report . Nurse

1: oberserve patient reponse.

Nurse 2: Clean scope.

Physicians,

Nurses

Prepare room for next patient Nurse

Pre

Procedure

Endoscopy

Room

Drugs, other

supplies,

physicians &

nurse's fee

Medical

Equipment

Post

Procedure

Description

(In Million Rupiah) Person-

nel

Room Equip. Total

Allocated

a b c d=a+b+c

1 Physicians &

Nurses's fee

1.295 1.295

2 Personnel's Salar

y

342 342 342

3Su

pp

lies

(

dru

g

s

)

465 465

4 Maintenance

(electricity, water,

building, laundry,

sterilization

)

72 72 72

5 Office Departemen

Ex

p

enses

155 155

6 Other supplies

(

office stationar

y)

15 15

7 Medical Equipment

(maintenance,

depreciation,

re

p

lacement cost

)

636 636 636

8 Building

De

p

reciatio

n

9 9 9

Total Expenses 2.990 342 82 636 1.060 1.759 171

Not

Allocated

No Total

Expen-

ses

Indirect cost

(

In Million Ru

p

iah

)

Direct

Cost

ICIB 2019 - The 2nd International Conference on Inclusive Business in the Changing World

382

x 7 hours/day) – (45 training hours) – (10 minutes

briefing x 291 days) – (1 meeting hour x 52 week) –

(1-hour meeting x 12 months) = 1.536 hours per

person /year. The total practical capacity of personnel

for 3 nurses is 276.420 minutes per year. (Table 2).

The practical capacity of the endoscopy room

with 2 bed for procedures and 1 bed for emergency is

184.280 minutes per year (Table 3)

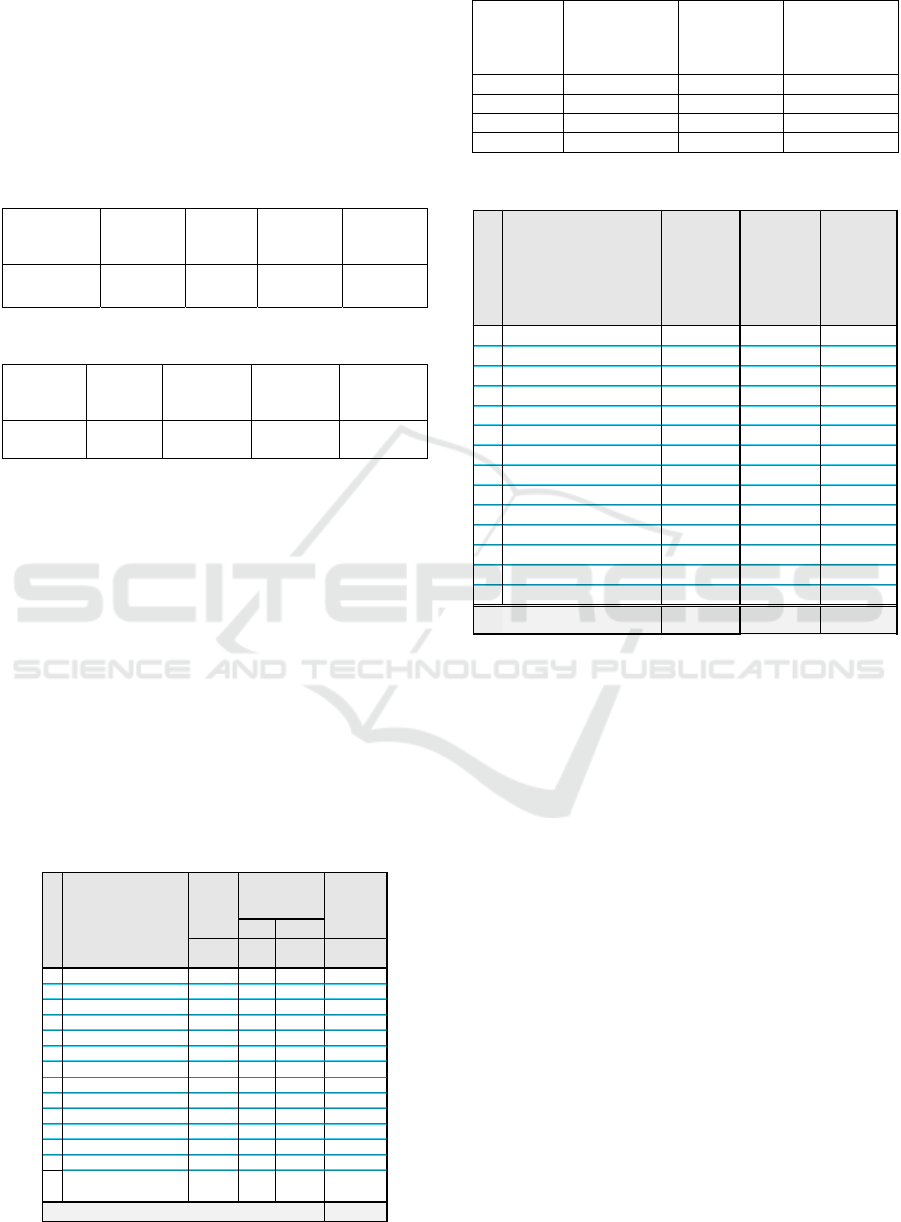

Table 2: Practical Capacity of Personnel.

Resource

Groups

Hours/

Year

Minutes/

Year

Hours/

Person/

Day

Minutes/

Person/

Day

Personnel

(3 nurses)

4.607 276.420 5,3 317

Table 3: Practical Capacity of Room.

Resource

Groups

Hours/

Year

Minutes/

Year

Hours/

Bed/

Day

Minutes/

Person/

Day

Room

(2 bed)

3.071 184.280 5,3 317

While, the practical capacity per year of medical

equipment is 2.027.080 minutes obtained from the

sum of practical capacity of each medical equipment

(Table. 4). Practical capacity of each type of

equipment is calculated by the quantity of equipment

multiply by minutes per day of practical capacity for

291 days.

3.1.4 Capacity Cost Rate

Calculation of the capacity cost rate per minute of

each resource group (Table 5) is done by dividing the

cost of capacity supplied by practical capacity per

year for each resource group (personnel, room,

equipment).

Table 4: Practical Capacity of Equipment.

Table 5: Capacity Cost Rate of Resource Groups.

Resource

Group

Cost of Capacity

Supplied

(million Rp)

Practical

Capacity per

Year

(minutes)

Capacity Cost

Rate

per Minute

(million Rp)

(a) (b) (c=a/b)

Personnel 342 276.420 0,001239

Room 82 184.280 0,000443

Equipmen

t

636 2.027.080 0,000314

Table 6: Capacity Cost Rate of Equipment.

Moreover, the breakdown of the cost of each type

of equipment is described in Table 6. Cost of capacity

supplied of each type of equipment is generated from

medical equipment expenses (depreciation,

maintenance, etc.).

3.1.5 Frequency of Procedures

After knowing the capacity cost rate for each resource

group, the next step is to determine the frequency of

each endoscopy procedure.

It can be seen in Table 7, there are 3 types of

Endoscopy procedures namely Gastroscopy,

Colonoscopy and Bronchoscopy. There are also types

of procedures based on a combined variation of 2

types of procedures and 3 types of procedures taken

in one episode.

3.1.6 Time Estimation of Each Procedures

Time estimation for Endoscopy procedures are shown

in table 7. The purpose of determining the time

estimation (minutes) of resource used in each

endoscopy procedure is to become a basis for indirect

cost allocation using the TDABC method. Time

Equipment

Hours M inute s (M inute s)

a b c d = a x c x

291 days

1Patient Bed 2 5,3 317 184.280

2Patient Monitor 2 5,3 317 184.280

3 Patient Troley 2 5,3 317 184.280

4 SterilizationTroley 2 5,3 317 184.280

5 Video scope Set 2 5,3 317 184.280

6 Medical Image Station 2 5,3 317 184.280

7 Suction Pump 1 5,3 317 92.140

8 Gastrovideoscope 2 5,3 317 184.280

9 Colonvideoscope 2 5,3 317 184.280

10 Bronchovideoscope 1 5,3 317 92.140

11 Electromic Surgical Unit 1 5,3 317 92.140

12 Duodenovideoscope 1 5,3 317 92.140

13 Anesthesia Machine 1 5,3 317 92.140

14 Flushing Aid (used all

together per procedure)

45,3 317 92.140

Total (Minutes) 2.027.080

Quantity Practical

Ca

p

acit

y

(per day)

Practical

Capacity

(per year)

Resource Grou

p

Me dical Equipments

(million Rp) (minutes) (million Rp )

1 Patient Bed 5 184.280 0,000029

2 Patient Monitor 13 184.280 0,000070

3 Patient Troley 6 184.280 0,000032

4 SterilizationTroley 3 184.280 0,000018

5 Video scope Set 116 184.280 0,000628

6 Medical Image Station 9 184.280 0,000050

7Suction Pump 3 92.140 0,000036

8 Gastrovideoscope 121 184.280 0,000657

9 Colonvideoscope 109 184.280 0,000592

10 Bronchovideoscope 23 92.140 0,000249

11 Electromic Surgical Unit 133 92.140 0,001442

12 Duodenovideoscope 39 92.140 0,000420

13 Anesthesia Machine 39 92.140 0,000427

14 Flushing Aid 16 92.140 0,000176

Total 636 2.027.080 0,000314

Cos t of

Capacity

Supplie d

Practical

Capacity

per Ye ar

Capacity

Cos t Rate

per Minute

Time-Driven Activity based Costing Method for Calculating Unused Capacity of Endoscopy Services: A Case Study of Xyz Hospital

383

(minutes) is the main cost driver in determining the

indirect cost allocation to each procedure.

Table 7: Time Estimation.

The use of personnel and room resource has begun

since the patient admission process when there is

interaction with nurses and physicians as well as the

use of room and bed. The use of medical equipment

begins when the medical equipment is prepared for

procedures.

The use of personnel resource is influenced by the

number of personnel need in carrying out a procedure.

Some procedures can be carried out simultaneously

with 3 nurses so that some procedures use 1,5 nurses

per procedure. Total personnel time is the total time

spent by all nurses.

Table 8: Time Usage of Resource Groups (minutes).

3.1.7 Total Time Usage and Cost for Each

Resource Group

The total time spent for personnel, rooms and medical

equipment is gained from time estimation multiply by

frequency of procedures. The total time of resource

used is 121.678 minutes. The use of a room is 68.436

minutes, and the overall use of medical equipment is

447.838 minutes. (Table 8.)

After the time usage of personnel, room and

equipment is defined, then the next step is calculating

the total cost of each resource group.

Room

Equip-

me nt

I

Gastroscopy

1 Gastroscopy without Biopsy 43 90 60 360

2 Gastroscopy with Biopsy 501 93 62 376

3 Ligation of Esophageal Varices 22 105 70 440

4 Gastric Polypectomy 3 300 100 760

II Kolonoskopi

1 Colonoscopy without Biopsy 60 125 83 544

2 Colonoscopy with Biopsy 92 128 85 560

3 Colon Polypectomy 7 330 110 850

4 Rectosigmoidoscopy without Biopsy 1 98 65 400

5 Rectosigmoidoscopy with Biopsy 11 101 67 416

III Bronkos kopi

1 Bronchoscopy without Biopsy 22 390 130 1.030

2 Bronchoscopy with Biopsy 19 420 140 1.120

IV Combination 2 Procedures

1 Gastroscopy without Biopsy & Gastric

Polypectomy

1

405 135 1.015

2 Gastroscopy without Biopsy & Ligation of

Esophageal Varices

8

210 105 670

3 Gastroscopy with Biopsy & Ligation of

Esophageal Varices

1

214 107 686

4 Gastroscopy without Biopsy &

Colonoscopy without Biopsy

2

276 138 962

5 Gastroscopy with Biopsy & Colonoscopy

with Biopsy

28

284 142 998

6 Gastroscopy with Biopsy & Colonoscopy

without Biopsy

33

280 140 980

7 Gastroscopy without Biopsy &

Rectosigmoidoscopy with Biopsy

1

244 122 818

8 Gastroscopy with Biopsy &

Rectosigmoidoscopy with Biopsy

1

248 124 836

9 Gastroscopy with Biopsy &

Rectosigmoidoscopy without Biopsy

2

244 122 818

10 Colonoscopy without Biopsy & Colon

Polypectomy

7

504 168 1.312

11 Colonoscopy with Biopsy & Colon

Polypectomy

4

510 170 1.330

12 Colonoscopy without Biopsy &

Hemorrhoid Ligation with Scope

1

290 145 920

13 Bronchoscopy without Biopsy &

Gastroscopy with Biopsy

1

561 187 1.403

V Combination 3 Procedures

1 Gastroscopy with BiopsyC & olonoscopy

without Biopsy & Colon Polypectomy

2

645 215 1.805

Grand Total 873 7.093 2.992 21.409

Endoscopy Proce dures

Number

of Fre-

que ncy

Time Es timation per

Procedures (Minutes)

Person-

ne l

Person-

nel

Room

Equip-

ment

I

Gastroscopy

1 Gastroscopy without Biopsy 3.870 2.580 15.480

2 Gastroscopy with Biopsy 46.593 31.062 188.376

3 Ligation of Esophageal Varices 2.310 1.540 9.680

4 Gastric Polypectomy 900 300 2.280

II Kolonoskopi

-

1 Colonoscopy without Biopsy 7.470 4.980 32.640

2 Colonoscopy with Biopsy 11.730 7.820 51.520

3 Colon Polypectomy 2.310 770 5.950

4 Rectosigmoidoscopy without Biopsy 98 65 400

5 Rectosigmoidoscopy with Biopsy 1.106 737 4.576

III Bronkoskopi

-

1 Bronchoscopy without Biopsy 8.580 2.860 22.660

2 Bronchoscopy with Biopsy 7.980 2.660 21.280

IV Combination 2 Procedures

-

1 Gastroscopy without Biopsy & Gastric

Polypectomy

405 135 1.015

2 Gastroscopy without Biopsy &

Ligation of Esophageal Varices

1.680 840 5.360

3 Gastroscopy with Biopsy & Ligation of

Esophageal Varices

214 107 686

4 Gastroscopy without Biopsy &

Colonoscopy without Biopsy

552 276 1.924

5 Gastroscopy with Biopsy &

Colonoscopy with Biopsy

7.952 3.976 27.944

6 Gastroscopy with Biopsy &

Colonoscopy without Biopsy

9.240 4.620 32.340

7 Gastroscopy without Biopsy &

Rectosigmoidoscopy with Biopsy

244 122 818

8 Gastroscopy with Biopsy &

Rectosigmoidoscopy with Biopsy

248 124 836

9 Gastroscopy with Biopsy &

Rectosigmoidoscopy without Biopsy

488 244 1.636

10 Colonoscopy without Biopsy & Colon

Polypectomy

3.528 1.176 9.184

11 Colonoscopy with Biopsy & Colon

Polypectomy

2.040 680 5.320

12 Colonoscopy without Biopsy &

Hemorrhoid Ligation with Scope

290 145 920

13 Bronchoscopy without Biopsy &

Gastroscopy with Biopsy

561 187 1.403

V Combination 3 Procedures

-

1 Gastroscopy with BiopsyC &

olonoscopy without Biopsy & Colon

Polypectomy

1.290 430 3.610

Grand Total 121.678 68.436 447.838

Endoscopy Procedures

Total Time Usage (Minutes)

ICIB 2019 - The 2nd International Conference on Inclusive Business in the Changing World

384

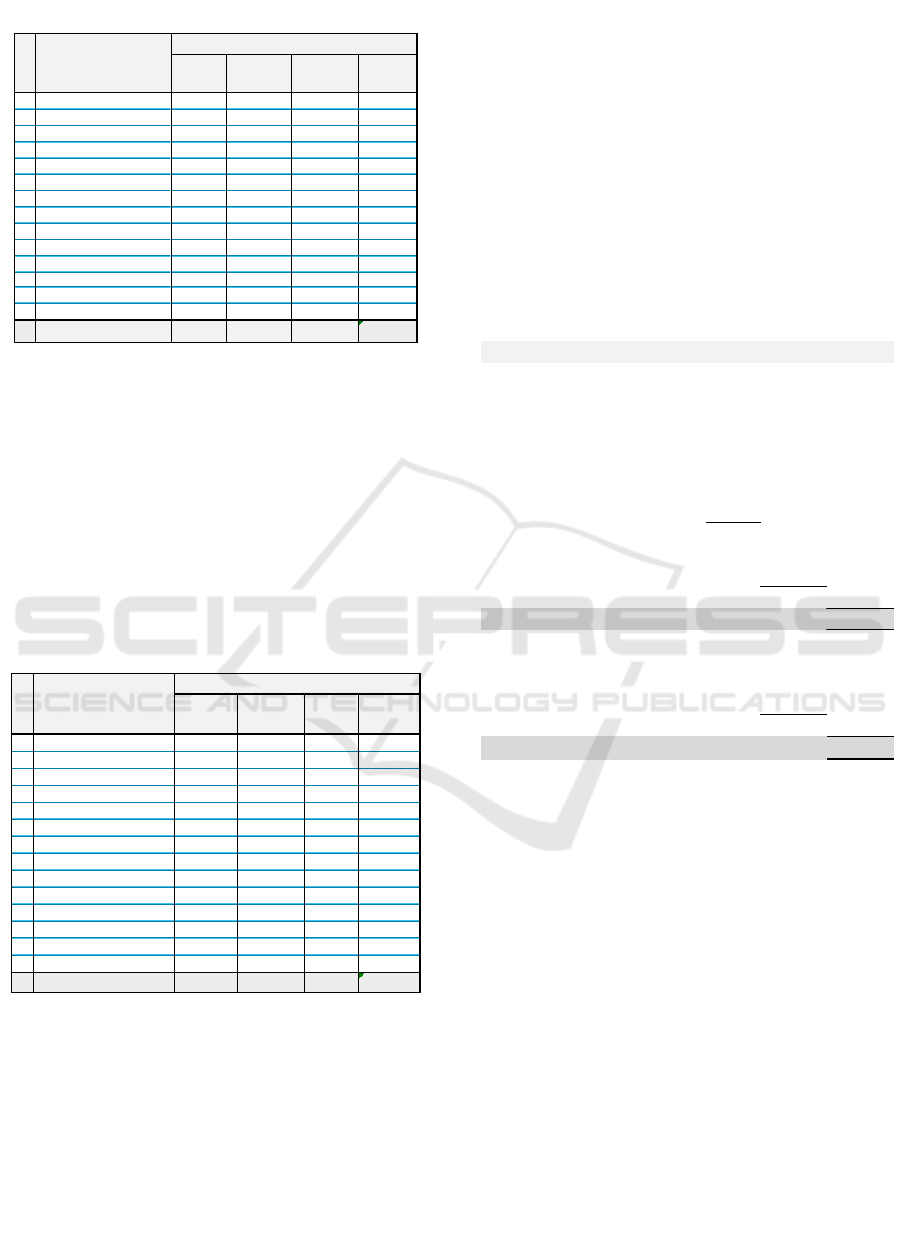

Table 9: Cost of Resource Groups (Million Rp).

The actual cost of the use of a resource group

(personnel, room dan equipment) for all procedures

in 2017 is shown in Table 9. In total, the cost of

personnel usage is Rp.150,73, - million, room usage

is Rp.30,34, - million, and overall usage of medical

equipment is Rp.86,49, - million.

Table 10 shows the sample of calculating cost of

each type of equipment for each procedure

(gastroscopy).

3.1.8 Unused Capacity Costs and Capacity-

based Income

One of the main advantages of the TDABC method is

that TDABC is able to describe the idle capacity or

unused capacity of available resources for each

service product/cost object. (Kaplan & Anderson,

2007).

Table 10: Cost of Each Type of Equipment.

As in table 11, the value of unused capacity of

personnel is 56%, there are 154.742 minutes a year or

2.95 hours per day per person. The cost of unused

personnel capacity is Rp. 191,68 million.

While the value of unused capacity for room is

63%. In table 12, with the capacity of 2 beds, there

are 115,854 minutes per year or 3,3 hours per day that

the beds are not used. The amount of unused capacity

is Rp.51,35,- million.

Table 11: Unused Capacity of Personnel.

Resource Group

Personnel

Resource Rate

per Minute

(million Rp)

Capacity

Usage

(Minutes)

Cost

(million Rp)

Used Capacity 1.239 121.678 150,73

Unused Capacity 154.742 191,68

Total 276.420 342,41

56% 56%

Table 12: Unused Capacity of Room.

Resource Group

Room

Resource Rate

per Minute

(million Rp)

Capacity

Usage

(Minutes)

Cost

(million Rp)

Used Capacity 443 68.436 30,34

Unused Capacity 115.844 51,35

Total 184.280 81,69

63% 63%

The unused capacity of medical equipment shows

varying values according to their utility. As in table

13 and table 14, Unused capacity of medical

equipment reaches Rp. 549,49 million, - with an

average of 79% of unused capacity. This high unused

capacity is also affected because there are medical

devices that are only used for a certain procedure,

such as Gastrosvideoscope for Gastroscopy,

Colonosvidescope for Colonoscopy, Electronic

Surgical Units for Polypectomy, Bronchovidescope

and Anesthetic for Bronchoscopy.

Person-

nel

Room

Equip-

ment

I

Gastroscopy

1 Gastroscopy without Biopsy 4,79 1,14 2,79

2 Gastroscopy with Biopsy 57,72 13,77 34,06

3 Ligation of Esophageal Varices 2,86 0,68 1,76

4 Gastric Polypectomy 1,11 0,13 0,72

II Kolonoskopi

1 Colonoscopy without Biopsy 9,25 2,21 5,75

2 Colonoscopy with Biopsy 14,53 3,47 9,08

3 Colon Polypectomy 2,86 0,34 1,85

4 Rectosigmoidoscopy without Biopsy 0,12 0,03 0,07

5 Rectosigmoidoscopy with Biopsy 1,37 0,33 0,80

III Bronkoskopi

1 Bronchoscopy without Biopsy 10,63 1,27 3,80

2 Bronchoscopy with Biopsy 9,89 1,18 3,58

IV Combination 2 Procedures

1 Gastroscopy without Biopsy & Gastric

Polypectomy

0,50 0,06 0,32

2 Gastroscopy without Biopsy &

Ligation of Esophageal Varices

2,08 0,37 0,98

3 Gastroscopy with Biopsy & Ligation of

Esophageal Varices

0,27 0,05 0,13

4 Gastroscopy without Biopsy &

Colonoscopy without Biopsy

0,68 0,12 0,43

5 Gastroscopy with Biopsy &

Colonoscopy with Biopsy

9,85 1,76 6,26

6 Gastroscopy with Biopsy &

Colonoscopy without Biopsy

11,45 2,05 7,24

7 Gastroscopy without Biopsy &

Rectosigmoidoscopy with Biopsy

0,30 0,05 0,18

8 Gastroscopy with Biopsy &

Rectosigmoidoscopy with Biopsy

0,31 0,05 0,19

9 Gastroscopy with Biopsy &

Rectosigmoidoscopy without Biopsy

0,60 0,11 0,36

10 Colonoscopy without Biopsy & Colon

Polypectomy

4,37 0,52 2,85

11 Colonoscopy with Biopsy & Colon

Polypectomy

2,53 0,30 1,65

12 Colonoscopy without Biopsy &

Hemorrhoid Ligation with Scope

0,36 0,06 0,16

13 Bronchoscopy without Biopsy &

Gastroscopy with Biopsy

0,69 0,08 0,23

V Combination 3 Procedures

1 Gastroscopy with BiopsyC &

olonoscopy without Biopsy & Colon

Polypectomy

1,60 0,19 1,23

Grand Total 150,73 30,34 86,49

Endoscopy Procedures

Total Cost of Resource

Usage (million Rp)

Patient

Bed

Gastro

video-

scope

Patient Bed Gastro

video-

scope

Equipment Cost Rate / Minute 0,000029 0,000657

I

Gastroscopy

1 Gastroscopy without Biopsy 60 40 0,001756 0,026298

2 Gastroscopy with Biopsy 62 42 0,001814 0,027613

3 Ligation of Esophageal Varices 70 50 0,002048 0,032873

4 Gastric Polypectomy 100 80 0,002926 0,052596

Equipment

Usage per

Procedure

(Minutes)

Equipment Usage per

Proc edure (millio n Rp)

Endoscopy Procedures

Time-Driven Activity based Costing Method for Calculating Unused Capacity of Endoscopy Services: A Case Study of Xyz Hospital

385

Table 13: Unused Capacity of Equipment (Minutes).

Also, there is a medical device

(Gastrovideoscope) that requires backup with

consideration of the high volume of use of the tool

and the length of time needed to repair the device if

damage occurs. A backup tool is provided to reduce

the risk of service that is hampered due to damaged

medical devices. The more medical devices that are

owned means the higher the cost of available capacity

(capacity cost supplied) so that at the same utilization

level will increase the unused capacity cost of the

tool.

Table 14: Unused Capacity of Equipment (million Rp).

Endoscopic procedures consist of pre, intra and

post stages. The post stage takes quite a long time

because it is necessary to observe the patient's

condition by the nurse to ensure the patient has fully

recovered when exit the Endoscopy room. At that

stage, even though the procedure process (use of

medical devices) is complete, the room facilities are

still used until the patient recovers.

The capacity-based income statement shows in

figure 3 that the operating income is Rp.1.464,88, -

million or 40% of total income. However, the idle

capacity reaches an amount of Rp.792,53, - million

(22% of total revenue). If the idle capacity is

calculated, then the net income becomes Rp. 672,35

million, or 18.4% of total revenue. Unused capacity

takes a portion of 26.5% of the total cost (Rp.2.990,12

million, -) which consists of direct costs, indirect cost

(used capacity), not allocated cost and idle capacity

cost.

By creating a capacity-based income statement,

the target improvement plan can be clearer and more

measurable. This idle capacity information can be

used as a performance indicator for management to

improve performance.

Figure 3: Capacity Based Income Statement.

4 CONCLUSIONS

By using TDABC, the cost of endoscopic procedures

can be calculated in more detail per type of

procedures. It also enables the calculation of various

services. Calculation of costs can be done for the total

cost, per group of resources (personnel, facilities and

room, medical equipment) and per type of

procedures.

TDABC allocates indirect costs to each resource

group in accordance with the actual usage of

resources, so that unused capacity (idle capacity) can

be presented separately. Information on the amount

of unused capacity in the form of time (minutes) and

costs (rupiahs) then can be used as a clearer and more

measurable management indicator in order to

improve performance through efficiency measures.

1 Patient Bed 68.436 115.844 184.280 63%

2 Patient Monitor 49.126 135.154 184.280 73%

3 Patient Troley 49.126 135.154 184.280 73%

4 SterilizationTroley 49.126 135.154 184.280 73%

5 Video scope Set 49.126 135.154 184.280 73%

6 Medical Image Station 49.126 135.154 184.280 73%

7 Suction Pump 49.126 43.014 92.140 47%

8 Gastrovideoscope 31.906 152.374 184.280 83%

9 Colonvideoscope 19.605 164.675 184.280 89%

10 Bronchovideoscope 4.637 87.503 92.140 95%

11 Electromic Surgical Unit 2.841 89.299 92.140 97%

12

Duodenovideoscope -

92.140 92.140 100%

13 Anesthesia Machine 4.637 87.503 92.140 95%

14 Cleaning Equipment 21.020 71.120 92.140 77%

Total 447.838 1.579.242 2.027.080 79%

Re s ource Group

Equipment

Equipment (Minute s)

Used

Capacity

Unus e d

Capacity

Total Idle

Capacity

1 Bed Pasien 2,00 3,39 5,39 63%

2 Patient Monitor 3,43 9,43 12,85 73%

3 Patient Troley 1,57 4,31 5,88 73%

4 Troley Bahan Steril 0,88 2,42 3,30 73%

5 Set Video scope 30,87 84,93 115,80 73%

6 Medical Image Station 2,45 6,74 9,19 73%

7 Suction Pump 1,78 1,56 3,35 47%

8 Gastrovideoscope 20,98 100,18 121,16 83%

9 Colonvideoscope 11,60 97,45 109,05 89%

10 Bronchovideoscope 1,15 21,76 22,91 95%

11 Electromic Surgical Unit 4,10 128,73 132,82 97%

12 Duodenovideoscope - 38,72 38,72 100%

13 Mesin Anastesi 1,98 37,34 39,32 95%

14 Pembersih alat 3,71 12,54 16,25 77%

Total 86,49 549,49 635,99 79%

Total Unus e d

Capacity

Resource Group

Equipme nt

Equipme nt (million Rp.)

Use d

Capacity

Unuse d

Capacity

Revenue 3.662,47

Less : Expenses

Direct Cost 1.759,29

Indirect Cost (Used Capacity)

Personnel 150,73

Room 30,34

Equipment 86,49

267,56

Not Allocated Cost

Office Departement & Other Supplies 170,74

2.197,59

Operating Income

1.464,88

Less :

Idle Capacity Cost

Personnel 191,68

Room 51,35

Equipment 549,49

792,53

Net Income

672,35

C

A

PACITYBASEDINCOMESTATEMENT

Total Cost

ICIB 2019 - The 2nd International Conference on Inclusive Business in the Changing World

386

REFERENCES

Britton, K., Koseki, S., & Dutta, A. (2018). Expanding

Markets while Improving Health in Indonesia: Private

Health Sector Market in the JKN Era. Washington, DC:

Palladium; Health Policy Plus; Jakarta, Indonesia:

TNP2K.

Campanale, C., Cinquini, L., & Tenucci, A. (2014). Time-

driven activity-based costing to improve transparency

and decision making in healthcare. Qualitative

Research in Accounting & Management, 11(2), 165–

186. https://doi.org/10.1108/QRAM-04-2014-0036

Clark, J., & Sopariwala, P. R. (2017). Applying Time-

Driven Activity-Based Costing to Metro Health’s

Outpatient Clinic. Cost Management, 31(2), 16–29.

Retrieved from https://search.proquest.com/docview/

1901188028?accountid=39260

Kaplan, R. S., & Anderson, S. R. (2007). Time-driven

activity-based costing: a simpler and more powerful

path to higher profits. Harvard Business School Press

Books, 82, 266. https://doi.org/10.1080/

09638180701814171

Keel, G., Savage, C., Rafiq, M., & Mazzocato, P. (2017).

Time-driven activity-based costing in health care: A

systematic review of the literature. Health Policy,

121(7), 755–763. https://doi.org/10.1016/j.healthpol.

2017.04.013

Porter, Michael E.; Lee, T. L. (2013). The Strategy That

Will Fix Health Care. Harvard Business Review,

(October), 1–39. Retrieved from http://hbr.org/2013/

10/the-strategy-that-will-fix-health-care/ar/1

Sopariwala, P. R. (2017). FACILITY-LEVEL ACTIVITY

COSTS. Cost Management, (july/August), 41–48.

Retrieved from remote-lib.ui.ac.id:6066/docview/

1929405512/578C46F04E324CC2PQ/1?accountid=17

242

Thabrany, H. (2017). JKN Mematikan Swasta. Retrieved

from https://kompasi.id/baca/opini/2017/04/08/jkn-

mematikan-swasta/

Yin, R. K. (2013). Validity and generalization in future case

study evaluations. Evaluation, 19(3), 321–332.

https://doi.org/10.1177/1356389013497081.

Time-Driven Activity based Costing Method for Calculating Unused Capacity of Endoscopy Services: A Case Study of Xyz Hospital

387