On Bayes Factors for Success Rate A/B Testing

Maciej Skorski

DELL, Austria

Keywords: Hypothesis Testing, Bayesian Statistics, AB Testing, Information Geometry.

Abstract:

This paper discusses Bayes factors, an alternative to classical frequentionist hypothesis testing, within the

standard A/B proportion testing setup - observing outcomes of independent trails (which finds applications

in industrial conversion testing). It is shown that the Bayes factor is controlled by the Jensen-Shannon di-

vergence of success ratios in two tested groups, and the latter one is bounded (under mild conditions) by

Welch’s t-statistic. The result implies an optimal bound on the necessary sample size for Bayesian testing, and

demonstrates the relation to its frequentionist counterpart (effectively bridging Bayes factors and p-values).

1 INTRODUCTION

1.1 Background and Motivation

A/B Proportions Testing. A/B testing is the

methodology of collecting data from two parallel ex-

periments, and deciding which group performs better

by means of statistical inference (to account for ef-

fects that may be due to change). The most frequent

use case concerns two success-counting experiments,

for example how many customers convert (purchase,

subscribe etc) on two versions of a web page (for ex-

ample the old page vs the optimized one).

In order to make the decision statistic-driven the

business question is formulated as the question about

unknown conversion rates p

1

, p

2

in the compared

groups, that are to be estimated from collected (ob-

served) data D . Usually one states the problem as

choosing one of the two possibilities

(a) The null hypothesis states that conversion rates

are equal (zero-effect), written as H

0

= {p

1

= p

2

}

(b) The alternative hypothesis claims a difference,

for example H

a

= {p

1

6= p

2

} or H

a

= {p

1

=

p

2

+ δ}

A/B Model Assumptions. We assume that in each

of the two groups we observe r independent Bernoulli

variables (each one is success or failure). Success

rates p

i

for group i are to be estimated from ths data

(we allow unknown rates p

i

to depend on hypothe-

ses via prior distributions). The data set D contains

two binary sequences describing outcomes (success

or failure for each trial) for each of the two groups.

Statistical Testing and Bayes Factors. The fre-

quentionist approach falsifies the null hypothesis

based on the two-sample t-test (Welch, 1938), so that

it is rejected when the test value is sufficiently un-

likely for given data (probability of which, falsely re-

jecting the null, is p-value).

The Bayesian approach is more coherent and flex-

ible as it directly compares the likelihoods of two hy-

potheses (for given data). By Bayes’ theorem

Pr[H

0

|D]

Pr[H

a

|D]

| {z }

posterior odds

=

Pr[D|H

0

]

Pr[D|H

a

]

| {z }

data likelihood ratio

·

Pr[H

0

]

Pr[H

a

]

| {z }

prior odds

(1)

where the likelihood ratio

K =

Pr[D|H

0

]

Pr[D|H

a

]

(2)

is also called the Bayes factor. Prior odds usually

equal 1, when one gives no prior preference to H

0

or

H

a

. Then the posterior odds equal K and the decision

depends on its magnitude: the bigger K from 1, the

more it supports H

0

. This may be also seen as decid-

ing upon the expected (posterior) cost of a certain risk

function (Lavine and Schervish, 1999).

Confidence scales depending on the magnitude

have been developed (Kass and Raftery, 1995; Jef-

freys, 1998; Lee and Wagenmakers, 2014).

Hypotheses are arbitrary “prior” probabilities on

rates p

1

, p

2

which can be formally written as H =

{(p

1

, p

2

) → P

H

(p

1

, p

2

)}. This includes point state-

ments of the form H = {p

1

= p

2

= 0.01} as well

us uncertainty distributions such as beta priors H =

{p

1

= p

2

= p, p ∼ Beta(0.5,0.5)}. Priors usually are

weakly informative, that is they give less preference

to “unrealistic” values like those near 0 or 1.

332

Skorski, M.

On Bayes Factors for Success Rate A/B Testing.

DOI: 10.5220/0007954503320339

In Proceedings of the 8th International Conference on Data Science, Technology and Applications (DATA 2019), pages 332-339

ISBN: 978-989-758-377-3

Copyright

c

2019 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

Under prior distributions specified the data likeli-

hood equals

Pr[D|H] =

Z

Pr[D|p

1

, p

2

] ·dP

H

(p

1

, p

2

)

=

Z

2

∏

i=1

p

¯p

i

r

i

(1 −p

i

)

(1− ¯p)

i

r

·dP

H

(p

1

, p

2

)

(3)

where r is the number of events and ¯p

i

is the success

rate observed for each group i in the collected data

D. Computation of the corresponding factor K can

be done in statistical software such as in R package

BayesFactor (Morey and Rouder, 2018).

1.2 Problem: Bayesian A/B testing

Estimates, neither frequentionist nor bayesian, will

not be conclusive without sufficiently many samples.

Frequentionists widely use rules of thumbs that are

derived based on t-tests. Under the bayesian method-

ology this is little more complicated because hypothe-

ses can be arbitrary priors over parameters (hence

composed out of infinitely many choices). Under the

described A/B model, we answer the following ques-

tions

• When, given data, a bayesian hypothesis on zero

effect may be rejected (we want to guarantee that

for any H

0

it holds K 1 for some H

a

)?

• What is the relation to the classical t-test?

• What are most plausible null and alternative hy-

pothesis, for a given dataset?

This will allow us to understand data limitations when

doing bayesian inference, and relate them to widely-

spread frequentionists rules of thumb. It is impor-

tant to note that Bayesian modelling has recently be-

come very popular in industrial conversion optimiza-

tion (Keser, 2017), so that these questions are also of

considarable practical interest.

1.3 Related Works and Contribution

Our problem, as stated, is a question about maximiz-

ing minimal Bayes factor; this is because we compare

any null against its most favorable alternative. For

certain simple problems, particularly for testing nor-

mality, minimal Bayes factors are known to be related

to frequentionists p-values (Edwards et al., 1963;

Kass and Raftery, 1995; Goodman, 1999), which

bridges the Bayesian and frequentionists worlds. This

should be contrasted with a wide-spread belief that

both methods are very incompatible (Kruschke and

Liddell, 2018).

The novel contributions of this paper are (a) de-

termining the Bayes factor - for testing success ratios

(b) demonstrating the relation to the frequentionist ap-

proach and (c) discussion of Bayesian sample bounds.

To the best author’s knowledge, this is the first result

of this sort in the context of testing success rates in

independent trials.

1.3.1 Main Result: Bayes Factor and Welch’s

Statistic

The following theorem shows that no “zero-effect”

hypothesis can be falsified, unless the number of sam-

ples is big in relation to a certain data statistic. This

statistic turns out to be the Jensen-Shannon diver-

gence, well-known in information theory; we further

show how to relate it to the Welch’s t-statistic. Doing

so we connect the classical frequentionist analysis and

the Bayes factors analysis.

Theorem 1 (Bayes Factors for Success Rate Testing).

Consider two experiments, each with r independent

trials with unknown success probabilities p

1

and p

2

respectively. If observed data D has r · ¯p

i

successes

for group i = 1,2, then

max

H

0

:{p

1

=p

2

}

min

H

a

Pr[D|H

0

]

Pr[D|H

a

]

= e

−2r·JS( ¯p

1

, ¯p

2

)

(4)

where the maximum is over null hypotheses H

0

such

that p

1

= p

2

, the minimum is over all valid alternative

hypotheses (priors) H

a

over p

1

, p

2

, and JS denotes

the Jensen-Shannon divergence.

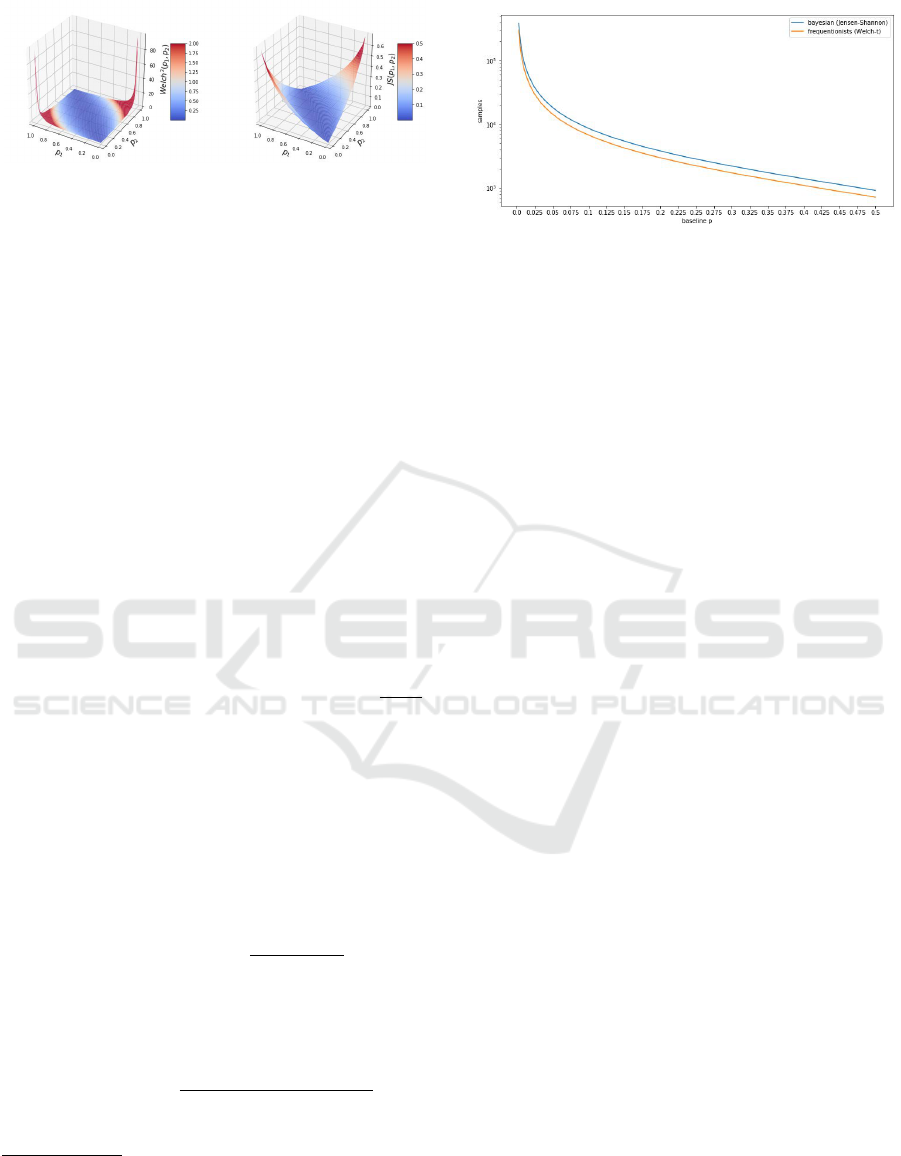

When comparing the Jensen-Shannon divergence

with the Welch’s t-statistic one should note that the

second one is unbounded, as illustrated in Figure 1.

Specifically, the Welch’s t is unbounded where one

rate is close to zero but the second one is closed to

one. It is however possible to have a bound of the

form JS = Ω(t

2

Welch

), under mild additional assump-

tions for example when both rates are smaller than 0.5

(which in practice don’t limit the usability). The re-

sult is formally stated in the theorem below, the proof

appears in Section 4. We note that the current proof

fails to achieve the optimal constant (see Section 5).

Theorem 2 (Comparison with T-Test). Under the

condition 0 6 ¯p

1

, ¯p

2

6

1

2

it holds that the Jensen-

Shannnon divergence is bounded from below by the

Welch’s t-statistic

JS( ¯p

1

, ¯p

2

) >

t

Welch

(r, ¯p

1

, ¯p

2

)

2

32r

(5)

so that the Bayes factor in Equation (4) can be

bounded by

max

H

0

:{p

1

=p

2

}

min

H

a

Pr[H

0

|D]

Pr[H

a

|D]

6 e

−t

Welch

(r, ¯p

1

, ¯p)

2

/16

. (6)

On Bayes Factors for Success Rate A/B Testing

333

Figure 1: Surface plots of the squared t-statistic t

2

Welch

(left) and Jensen-Shannon divergence JS which controls the

Bayes factor (right), as functions of success rates p

1

, p

2

.

Note that t

Welch

is unbounded (around the corners).

Remark 1 (Min-max Game Intepretation). The min-

max formula in Equation (6) comes from the fact that

we evaluate every null against its most plausible al-

ternative (so that the bound holds regardless of the

null prior). This can be seen as a two-player zeros-

sum game where one player chooses the null hypothe-

sis, the second player chooses the alternative and the

payoff is the Bayes factor. Theorem 1 describes the

saddle point in this game.

The following corollary shows what are most

“plausible” null and alternatives for a given data set

(they realize equality in Equation (4))

Corollary 1 (Characterization of Most Favorable Hy-

potheses). Note that

• Maximally favorable alternative (H

a

which maxi-

mizes Pr[D|H

a

]) is p

1

= ¯p

1

and p

2

= ¯p

2

• Maximally favorable null H

0

on zero-effect, that is

of the form p

1

= p

2

, is given by p

1

= p

2

=

¯p

1

+ ¯p

2

2

If null is of the form p

1

= p

2

= p for some constant p,

then the bound becomes e

−r·KL( ¯p

1

,p)−r·KL( ¯p

2

,p)

.

1.3.2 Application: Sample Bounds

The main result implies the following sample size rule

Corollary 2 (Bayesian Sample Bound). To confirm

the non-zero effect (p

1

6= p

2

) the number of samples r

for the bayesian method should be

r

bayes

> log K

critical

·

1

2JS( ¯p

1

, ¯p

2

)

(7)

where usually K

critical

≈10

1

. Under the frequenionist

method the rule of thumb is t

Welch

t

critical

, which

gives (see Section 2)

r

f req

> t

critical

·

¯p

1

(1 − ¯p

1

) + ¯p

2

(1 − ¯p

2

)

( ¯p

1

− ¯p

2

)

2

(8)

where usually t

critical

≈ 1.9

2

1

This corresponds to the Bayes factor of 10

−1

against

null, interpreted as strong evidence in common scales (Lee

and Wagenmakers, 2014).

2

This roughly holds for the significance level of 0.95,

the exact value depends also on degrees of freedom.

Figure 2: Comparison of the bayesian (7) and the frequen-

tionist (8) sample lower bounds, where observed data are

¯p

1

= p and ¯p

2

= p ·(1 + δ) for δ = 0.1 (relative uplift by

10%), and the zero-effect hypothesis p

1

= p

2

is to be re-

jected. Bounds are away by a constant factor, here are very

close for constants calibrated under typical rejection rules:

t-statistic of 1.9 and Bayes factor of 0.1.

Note that both formulas needs assumptions on lo-

cations of expected rates; testing smaller effects or

smaller conversion rates require more samples.

Exact constants, hidden under K

critcal

and t

critcal

,

depend on the significance one wants to achieve: p-

value for the extreme t-statistic, respectively the mag-

nitude of the Bayes factor. Apart from constants

(or when constants are callibrated for “typical” tests

strength) bounds in Equation (7) and Equation (8) are

close to each other. The difference is illustrated on

Figure 2, for the case when one wants to prove the

difference (reject the zero-effect hypothesis) in pres-

ence of an observed lift of 10%. The code is attached

in Section 5.

It is important to stress that our lower bounds hold

with respect to zero-effect hypotheses and regardless

of priors, testing effect of a fixed size or using more

diffuse priors may require more samples.

1.3.3 Application: Bayes Factors vs P-Values

Since high values of t

Welch

mean small p-values, we

conclude that the frequentionist p-values bound the

Bayes factor and indeed are evidence against a null-

hypothesis in the well-defined bayesian sense.

However, because of the scaling t

Welch

→

e

−Ω(t

2

Welch

)

in the minimal Bayes factor in Equa-

tion (6), Bayesian rejection corresponds to p-values

much lower than the standard frequentionist thresh-

old of 0.05. In a way, the bayesian approach is more

conservative and reluctant to reject than frequention-

ist tests; this conclusion is shared with (Goodman,

1999).

DATA 2019 - 8th International Conference on Data Science, Technology and Applications

334

2 PRELIMINARIES

Entropy, Divergence. The binary cross-entropy of

p and q is defined by

H(p,q) = −plog q −(1 −p) log(1 −q) (9)

which becomes the standard (Shannon) binary en-

tropy when p = q, denoted as H(p) = H(p, p). The

Kullback-Leibler divergence is defined as

KL(p,q) = H(p,q) −H(p) (10)

and is non-negative. The Jensen-Shannon diver-

gence (Lin, 1991) is defined as

JS(p,q) =

1

2

KL

p,

p + q

2

+

1

2

KL

q,

p + q

2

(11)

being symmetric and non-negative (because KL di-

vergence is non-negative). Alternatively, using Equa-

tion (10) and Equation (9) we can write

JS(p,q) = H

p + q

2

−

1

2

H(p) −

1

2

H(q) (12)

which shows that the Jensen-Shannon divergence is

bounded.

The following lemma shows that the cross-entropy

function is convex in the second argument. This

should be contrasted with the fact that the entropy

function (of one argument) is concave.

Lemma 1 (Convexity of Cross-entropy). For any p

the mapping x →H(p, x) is convex in x.

Proof. Since −plog(·) for fixed p ∈ [0,1] is convex

we obtain

−γ

1

plog x

1

−γ

2

plog x

2

> −p log(γ

1

x

1

+ γ

2

x

2

)

for any x

1

,x

2

and any γ

1

,γ

2

> 0, γ

1

+ γ

2

= 1. Replac-

ing x

i

by 1 −x

i

and p by 1 −p in the above inequality

gives us also

−γ

1

(1 −p) log(1 −x

1

) −γ

2

(1 −p) log(1 −x

2

)

> −(1 − p)log(γ

1

(1 −x

1

) + γ

2

(1 −x

2

))

= −(1 − p)log(1 −γ

1

x

1

) −γ

2

x

2

)

Adding side by side yields

γ

1

H(p,x

1

) + γ

2

H(p,x

2

) > γ

1

H(p,x

1

) + γ

2

H(p,x

2

)

which finishes the proof. This argument works for

multivariate case, when p,x are probability vectors.

Convexity Properties of Jensen-Shannon Diver-

gence.

Lemma 2. Let δ = p −q, then for every fixed q we

have

∂

2

∂δ

2

JS(p,q) =

1

2

p

2

−2pq −q

2

+ 2q

p(p −1)(p + q)(p + q −2)

(13)

which is strictly positive for 0 < p, q < 1.

Proof. The derivative is calculated in Section 5, with

the Python package SymPy (Meurer et al., 2017). The

numerator (skiping the constant

1

2

) can be written as

2q(1 −q) + (p −q)

2

which is non-negative. The de-

numerator is non-negative because p,q are between 0

and 1.

Bernoulii Variables. For a Bernoulli variable with

success probability p we denote by Var(p) = p(1 −

p) the variance. We have the following identity

Var(p) + Var(q) = 2Var

p + q

2

−

(p −q)

2

2

(14)

which in particular demonstrates that the variance is

concave.

2-Sample Test. To decide whether means in two

groups are equal, under the assumption of unequal

variances, one performs the Welch’s t-test with the

statistic given by (Derrick et al., 2016)

t

Welch

=

µ

1

−µ

2

r

s

2

1

r

1

+

s

2

2

r

2

(15)

where s

i

are sample variances and µ

i

are sample

means for group i = 1,2. The null hypothesis is re-

jected unless the statistic is sufficiently high (in abso-

lute terms). In our case the formula simplifies to

Claim 1. If rθ

1

and rθ

2

success out of r trials have

been observed, respectively in the first and the second

group, then

t

Welch

(r,θ

1

,θ

2

) = r

1

2

·

θ

1

−θ

2

p

θ

1

(1 −θ

1

) + θ

2

(1 −θ

2

)

(16)

3 PROOF OF THEOREM 1

Notation. We change the notation slightly, un-

known success rates will be p and q, and the number

of observed successes r ·θ

1

,r ·θ

2

.

On Bayes Factors for Success Rate A/B Testing

335

Best Alternative. Maximizing over alll possible

priors P

a

over pairs (p,q) and using Equation (3) we

get

max

P

a

Pr[D|H

a

] =

max

P

a

Z

e

−rH(θ

1

,p)−rH(θ

1

,q)

P

a

(p,q)d(p,q) (17)

Since H(θ

1

, p) = H(θ

1

, p) + KL(θ

1

, p), H(θ

1

,q) =

H(θ

1

,q)+KL(θ

1

,q) and KL is non-negative we con-

clude that the maximum over the integrals equals

max

P

a

Pr[D|H

a

] = e

−rH(θ

1

)−rH(θ

2

)

(18)

achieved for P

a

being a unit mass at (p,q) = (θ

1

,θ

2

),

that is at observed rates.

Best Null. Let H

0

states that the effect is 0. This is

equivalent to a prior P

0

(p) on the baseline conversion

p with the condition q = p. We obain

Pr[D|H

0

] =

Z

e

−rH(θ

1

,p)−rH(θ

2

,p)

dP

0

(p) (19)

The integrand, due to Lemma 1, has a global maxi-

mum at some p. Thus the integral is maximized for

dP

0

(p) being a point mass.

Bayes Factor. Using the above observations on

most plausible hypotheses we can write the max-min

Bayes factor (in favor of H

0

) as

max

H

0

min

H

a

Pr[D|H

0

]

Pr[D|H

a

]

=

max

H

0

Pr[D|H

0

]

max

H

a

Pr[D|H

a

]

= e

−r·(H(θ

1

,p)+H(θ

1

,p)−H(θ

1

)−H(θ

2

))

(20)

Using the relation between the KL divergence and

cross-entropy we obtain

max

H

0

min

H

a

Pr[D|H

0

]

Pr[D|H

a

]

= e

−rKL(θ

1

,p)−rKL(θ

2

,p)

(21)

We will use the following observation

Claim 2. The expression KL(θ

1

, p) + KL(θ

2

, p) is

minimized under p = θ

∗

=

θ

1

+θ

2

2

, and achieves value

2JS(θ

1

,θ

2

).

Proof. We have

KL(θ

1

, p) + KL(θ

2

, p)

= H(θ

1

, p) + H(θ

2

, p) −H(θ

1

) −H(θ

2

)

Now the existence of the minimum at p = θ

∗

follows by convexity of p → H(θ

1

, p) + H(θ

2

, p),

proved in Lemma 1. We note that H(θ

1

, p) +

H(θ

2

, p) = 2H

θ

1

+θ

2

2

, p

for any p (by definition),

and thus for p =

θ

1

+θ

2

2

= θ

∗

we obtain H(θ

1

, p) +

H(θ

2

, p) = 2H(θ

∗

) and KL(θ

1

, p) + KL(θ

2

, p) =

2H(θ

∗

) −H(θ

1

) −H(θ

2

). This combined with the

definition of the Jensen-Shannon divergence finishes

the proof.

We can now bound Equation (21) as

min

H

a

Pr[D|H

0

]

Pr[D|H

a

]

6 e

−2r·JS(θ

1

,θ

2

)

(22)

This ends the proof of Theorem 1, from the proof we

also conclude Corollary 1.

4 PROOF OF THEOREM 2

In order to compare JS and t

Welch

we use the

parametrization q = p + δ. For convenience we

slightly abuse the notation writing t

Welch

(p,q) =

t

Welch

(r, p,q)/

√

r = t

Welch

(1, p, q). The result reduces

to the following lemma

Lemma 3 (Convexity of the Gap between

Jensen-Shannon Divergence and Welch’s t). In

the region

0 6 q 6 p 6

1

2

(23)

we have that JS(p,q) −

1

32

·t

Welch

(p,q)

2

is convex in

δ = p −q for any fixed q. In particular for every q it

achieves the minimal value at δ = 0, which is equal to

0.

Proof. It suffices to consider q 6 p as both JS and

t

Welch

are symmetric. Because of continuity we con-

sider the strict inequalities 0 < q < p <

1

2

. The proof

involves symbolic differentiation and factoring which

we do in the Python package SymPy (Meurer et al.,

2017).

We start with the ratio of the second derivatives

Claim 3 (Second Derivatives Ratio). We have that

∂

2

∂δ

2

JS(p,q)

∂

2

∂δ

2

t

Welch

(p,q)

=

1

4

·ψ ·φ (24)

where

ψ(p,q) =

p − p

2

+ q −q

2

3

p(1 − p)(p + q)(2 − p −q)

φ(p,q) =

p

2

−2pq −q

2

+ 2q

−2p

3

q + p

3

+ 3p

2

q + 6pq

3

−9pq

2

−3q

3

+ 4q

2

Proof of Claim. The code deriving formulas is in-

cluded in Section 5.

DATA 2019 - 8th International Conference on Data Science, Technology and Applications

336

Claim 4 (Denumerator of φ is non-negative). Let V =

−2p

3

q + p

3

+3p

2

q +6pq

3

−9pq

2

−3q

3

+4q

2

be the

denumerator of φ. Then V > 4p

2

(1 −p

2

).

Proof of Claim. It holds that

∂

2

V

∂p

2

= 6·(p+q−2pq) =

6(p(1 −q) + q(1 − p)) which shows that V is con-

vex in p for all (p,q) ∈ [0, 1]

2

. Next, we have

∂V

∂p

=

−3(p −q)

2pq − p + 2q

2

−3q

. Looking for global

minimas we note that the second factor 2pq − p +

2q

2

−3q = −q(1 − p) − p(1 −q) −2q(1 −q) is al-

ways non-positive and zero if and only if p = q = 0

or p = q = 1. The first factor gives us q = p. Sum-

ming up, the global minimum for each p is given by

q = p. Substituting this we obtain V (p,q) > V (q,q) =

4p

2

(1 −p)

2

which finishes the proof.

Claim 5 (Bound on φ). Let U,V be as before. Un-

der the condition 0 < q < p <

1

2

we have U · p(1 −

p) −

1

2

V > 0, and the claim before implies φ =

U

V

>

1

2p(1−p)

.

Proof of Claim. We have

U p(1 −p) −

V

2

=

p −q

2

1

2

−p

1

2

p

2

−pq −

3

2

q

2

+ 2q

=

p −q

2

1

2

−p

(p −q)

2

2

+ 2q(1 −q)

which is non-negative when

1

2

> p > q > 0. By the

previous claim U is non-negative so that we can di-

vide both sides. For completeness we include the

code used for deriving the formulas in Section 5.

Summing up, from the claims we obtain

Claim 6 (Bounding the Second Derivative Ratio).

Under the condition 0 < q < p <

1

2

we have

∂

2

∂δ

2

JS(p,q)

t

Welch

(p,q)

>

(Var(p) + Var(q))

3

32Var

2

(p)Var

p+q

2

(25)

which is bigger than

1

32

.

Proof of Claim. The previous claim implies

∂

2

∂δ

2

JS(p,q)

t

Welch

(p,q)

=

1

4

·ψ ·φ

>

1

4

·ψ ·

1

2p(1 − p)

(26)

which is equivalent to Equation (25) if we consider

the explicit form of ψ and use variance expressions.

The lower bound of

1

32

follows as under the assump-

tion 0 < q < p <

1

2

we have

Var(q) < Var

p + q

2

< Var(p) (27)

The convexity part in the lemma follows directly

from the last claim. The minimum for each q exists

because of convexity and is achieved for δ = 0, as at

this point the first derivative vanishes (see calculations

in Section 5).

5 CONCLUSION

We have studied Bayes factors in the context of A/B

testing of event rates, which is relevant to the impor-

tant problem of conversion optimization.

The result can be easily extended to cover the case

of unequal group sizes. Also it is possible to derive

bounds for testing a fixed-size effect δ instead of zero-

effect as the null hypothesis.

Finally, regarding the problem of comparing the

Welch’s t and Jensen-Shannon divergence we conjec-

ture that the inequality in Theorem 2 can be improved,

namely

Proposition 1 (Open problem). Let 0 6 q 6 p 6

1

2

.

Find the biggest constant C such that

JS(p,q) > C ·

t

Welch

(r, p,q)

2

r

(28)

The current proof is based on global convexity

which works under a subptimal constant C =

1

32

.

ACKNOWLEDGMENTS

The author thanks to Evan Miller for inspiring discus-

sions.

REFERENCES

Derrick, B., Toher, D., and White, P. (2016). Why welch’s

test is type i error robust. The Quantitative Methods

in Psychology, 12(1):30–38.

Edwards, W., Lindman, H., and Savage, L. J. (1963).

Bayesian statistical inference for psychological re-

search. Psychological Review, 70(3):193–242.

Goodman, S. N. (1999). Toward evidence-based medical

statistics. 2: The bayes factor. Annals of internal

medicine, 130 12:1005–13.

Jeffreys, H. (1998). The Theory of Probability. Oxford

Classic Texts in the Physical Sciences. OUP Oxford.

Kass, R. E. and Raftery, A. E. (1995). Bayes fac-

tors. Journal of the American Statistical Association,

90(430):773–795.

Keser, A. (2017). Goodbye, t-test: new stats models

for a/b testing boost accuracy, effectiveness. https:

//www.widerfunnel.com/goodbye-t-test-new-stats-

models-for-ab-testing-boost-accuracy-effectiveness/.

On Bayes Factors for Success Rate A/B Testing

337

Kruschke, J. K. and Liddell, T. M. (2018). The bayesian

new statistics: Hypothesis testing, estimation, meta-

analysis, and power analysis from a bayesian perspec-

tive. Psychonomic Bulletin & Review, 25(1):178–206.

Lavine, M. and Schervish, M. J. (1999). Bayes factors:

What they are and what they are not. The American

Statistician, 53(2):119–122.

Lee, M. D. and Wagenmakers, E.-J. (2014). Bayesian cog-

nitive modeling: A practical course. Cambridge uni-

versity press.

Lin, J. (1991). Divergence measures based on the shannon

entropy. IEEE Transactions on Information Theory,

37(1):145–151.

Meurer, A., Smith, C. P., Paprocki, M.,

ˇ

Cert

´

ık, O., Kir-

pichev, S. B., Rocklin, M., Kumar, A., Ivanov, S.,

Moore, J. K., Singh, S., Rathnayake, T., Vig, S.,

Granger, B. E., Muller, R. P., Bonazzi, F., Gupta, H.,

Vats, S., Johansson, F., Pedregosa, F., Curry, M. J.,

Terrel, A. R., Rou

ˇ

cka, v., Saboo, A., Fernando, I., Ku-

lal, S., Cimrman, R., and Scopatz, A. (2017). Sympy:

symbolic computing in python. PeerJ Computer Sci-

ence, 3:e103.

Morey, R. D. and Rouder, J. N. (2018). BAYESFACTOR:

computation of bayes factors for common designs. r

package version 0.9.12-4.2. http://CRAN.R-project.

org/package=BayesFactor.

Welch, B. L. (1938). The significance of the difference be-

tween two means when the population variances are

unequal. Biometrika, 29(3/4):350–362.

APPENDIX

Code

The following Python code implements the compari-

son sketched on Figure 2.

import numpy a s np

from m a t p l o t l i b import p y p l o t a s p l t

H=lambda p , q:−p ∗np . l o g ( q)−(1−p ) ∗ np . l o g (1−q )

KL=lambda p , q :H( p , q)−H( p , p )

JS=lambda p , q : ( KL( p , ( p+q ) / 2 ) + KL( q , ( p+q ) / 2 ) ) / 2

Welch=lambda p , q : ( p−q ) / np . s q r t ( p∗(1 −p )+ q∗(1 −q ) )

r b a y e s = lambda p , q : np . l o g ( 1 0 ) / ( 2 ∗ JS ( p , q ) )

r f r e q = lambda p , q : 1 . 9 ∗∗2 ∗Welch ( p , q )∗∗( −2)

p= np . l i n s p a c e ( 0 , 0 . 5 , 2 0 1 )

d e l t a = 0 . 1

q= p ∗(1+ d e l t a )

p l t . f i g u r e ( f i g s i z e = ( 1 2 , 6 ) )

p l t . p l o t ( r b a y e s ( p , q ) , \

l a b e l = ’ b a y e s i a n ( JS ) ’ )

p l t . p l o t ( r f r e q ( p , q ) , \

l a b e l = ’ f r e q u e n t i o n i s t s ( Welch−t ) ’ )

p l t . y s c a l e ( ’ l o g ’ )

p l t . x t i c k s ( np . a r a n g e ( 0 , 2 0 1 , 1 0 ) , \

np . l i n s p a c e ( 0 , 0 . 5 , 2 1 ) . round ( 3 ) )

p l t . l e g e n d ( )

p l t . y l a b e l ( ’ sa m p l e s ’ )

p l t . x l a b e l ( ’ b a s e l i n e p ’ )

p l t . show ( )

Proof of Lemma 3

Below we compute the formula in Claim 3

import sympy

p , q , d = sympy . s y m bo l s ( r ’ p q d ’ )

# d e f i n e JS and Welch ’ s t

wel c h = ( p−q ) ∗∗2 / ( p∗(1−p ) + q∗(1−q ) )

H = −p ∗sympy . l o g ( p)−(1−p ) ∗sympy . l o g (1−p )

JS = H . s u b s ( p , ( p+q ) / 2 ) − 1 / 2 ∗H − 1 / 2 ∗H . s u b s ( p , q )

# s e c o n d d e r i v a t i v e s

o u t 1 = JS . s u b s ( p , q+d ) . d i f f ( d , 2 ) . su b s ( d , p−q )

o u t 2 = wel c h . s u b s ( p , q+d ) . d i f f ( d , 2 ) . s u b s ( d , p−q )

# r a t i o o f s e c o n d d e r i v a t i v e s

( o u t 1 / o u t 2 ) . f a c t o r ( )

o u t

Below we include the code used to derive formu-

las in the proof of Claim 5

import sympy

p , q = sympy . s ym bo l s ( r ’ p q ’ )

U = ( p ∗∗2 − 2∗p∗q − q ∗∗2 + 2∗q )

V = (−2∗p ∗∗3∗q + p ∗∗3 + 3∗p ∗∗2∗q \

+6∗p∗q ∗∗3 − 9∗p ∗q ∗∗2 − 3∗q ∗∗3 + 4∗q ∗∗2 )

(U∗p ∗(1−p ) −1/2 ∗V ) . f a c t o r ( )

The following piece of code is used to validate the

claim about the global minimum at δ = 0, the end of

the proof of Lemma 3

import sympy

wel c h = ( p−q ) ∗∗2 / ( p∗(1−p ) + q∗(1−q ) )

H = −p ∗sympy . l o g ( p)−(1−p ) ∗sympy . l o g (1−p )

JS = H . s u b s ( p , ( p+q ) / 2 ) − 1 / 2 ∗H − 1 / 2 ∗H . s u b s ( p , q )

# ou t 1 = JS . s u b s ( p , q+d ) . d i f f ( d , 2 ) . s u b s ( d , p−q )

# ou t 2 = w e l c h . s u b s ( p , q+d ) . d i f f ( d , 2 ) . s u b s ( d , p−q )

# ( o u t 1 / o u t 2 ) . f a c t o r ( )

d e r i v a t i v e = ( JS −1/32∗we lc h ) . s u b s ( p , q+d ) . d i f f ( d , 1 )

d e r i v a t i v e . s u b s ( d , 0 )

The next piece of code evaluates the second

derivative in Lemma 2

H = −p ∗sympy . l o g ( p)−(1−p ) ∗sympy . l o g (1−p )

JS = H . s u b s ( p , ( p+q ) / 2 ) − 1 / 2 ∗H − 1 / 2 ∗H . s u b s ( p , q )

JS . s u b s ( p , q+d ) . d i f f ( d , 2 ) . s u b s ( d , p−q ) . f a c t o r ( )

DATA 2019 - 8th International Conference on Data Science, Technology and Applications

338

Plots

import nump y as np

from m a tp l ot l ib import pyp l o t as plt

from scip y import sp e cia l as sc

H = lambda p : -sc . x l ogy ( p , p )- sc . x logy (1 - p ,1 - p )

JS = lambda p , q : H (( p + q ) /2) -0.5* H ( p ) -0.5* H (q )

Welch = lambda p , q : np . d ivid e ((p - q ) , np . sqrt ( p *(1 - p )+ q *(1 -q )) ,

out = np . ze r os _ li k e ( p ) , wh e re = p *(1 - p )+ q *(1 - q ) >0)

p = np . lins p ace (0 ,1 ,1 0 0 + 1 )

q = np . lins p ace (0 ,1 ,1 0 0 + 1 )

xx , yy = np . me sh g rid (p , q )

zz_js =JS ( xx ,yy )

zz_ w el c h = Welc h (xx , yy )

zz = z z_w e lch

labe l s = { ’ We l c h ’: ’ $ W elch ˆ2( p_1 , p_2 ) $ ’ , ’ JS ’: ’ $JS ( p_1 , p_2 ) $ ’}

vmax = { ’ Wel c h ’ :2 , ’ JS ’ :0 . 5 }

fig = plt . figure ( fi g siz e =(1 6 ,6))

for i ,( zz , label ) in enumerate(zip([ z z _we l ch **2 , zz_j s ],

labe l s . key s () ) ) :

ax = fig . add_ sub pl o t (1 ,2 ,1+ i , proj e ct i on =’ 3 d ’)

surf = ax . plot _s u rf a ce (xx , yy , zz ,

cmap = p lt . cm . c o o l w a r m , rstr i de =1 , cst r ide =1 ,

li n ewi d th =0 , vmax = vm ax [ l abel ])

ax . se t _x l ab e l ( r " $p _ 1 $ " )

ax . se t _y l ab e l ( r " $p _ 2 $ " )

ax . se t _z l ab e l ( label s [ labe l ])

ax . zaxis . lab e lpa d =10

ax . in v er t_ x ax i s ()

fig . c olo r ba r ( surf , s hrin k =0.5 , a s pect =5)

plt . rc ( ’ a x es ’ , l abe lsi z e =15)

plt . show ()

On Bayes Factors for Success Rate A/B Testing

339