The Impact of Triple Bottom Line-oriented Environmental

Management System on Firms’ Performance in China: Evidence

from Yangtze River Delta

Yijie Chen and Youlin Huang

111 Ren’ai Road Suzhou Dushu Lake Science and Education Innovation District Suzhou Industrial Park Suzhou 215123,

Xi’an Jiaotong Liverpool University, China

Keywords: Triple Bottom Line, Corporate Social Responsibility, Top Management Leadership, Corporate Social

Responsibility Policy, Corporate Financial Performance, Guanxi, Government and Business Relation.

Abstract: This research investigates the impact of Triple Bottom Line oriented Environmental Management System on

the firms’ performance in China. This research is going to attempts to compose a conceptual framework to

demonstrate how Triple Bottom Line Influence Corporate Social Responsibility activities which it may

potential impact firm’s financial performance. This paper will introduce the background of Corporate Social

Responsibility at the beginning. It will address the nature of this study in philosophy part in order to point

the direction of the research and it will be leading the decision to methodology for this research. This study

collected valid 225 sample questionnaire surveys out of 330 respondents. We approved CSR policy is essential

for CSR in China by employee AMOS v.21. to test the validity of the Structural Equation Modeling. Our

finding implies that the Guanxi effect is not significance as well as the past decades in the implementation of

CSR activities and government needs to engage within relevant industry to promote CSR by issue CSR

policies. This is the first empirical research to test if Triple Bottom Line oriented Environmental Management

System will effect firms’ performance.

1 INTRODUCTION

1.1 Research Background

Companies have to pay attention to Corporate Social

Responsibility (CSR). Corporate social responsibility

is a concept for enterprises to understand that how

their business activities will influence the society and

the environment where it operates the business

activities (Globerman, 2011). CSR emphasizes that a

company should not just care about profit, but also

needs to take care about the society and the

environment as a whole. The role of Elkington (1994)

establish a concept named Triple Bottom Line (TBL)

which is essential to understanding CSR. It suggests

a company to attain sustainable development in

environmental, societal and economic terms.

Nowadays, accomplishing sustainable TBL oriented

environment management system has been well

documented, which focuses on the achievement of

sustainability through three dimensions namely,

economic, social and environmental factors in firms’

internal business operations (Slaper and Hall, 2011).

Triple Bottom Line is a concept that established by

Elkington in 1994, and it offers ideas about the firm

should keep a balance between social, economic and

environment when they run their business. To date

there has been little attempt to research how TBL

oriented environmental management systems

influence the performance of firms in contemporary

China. This proposed research will investigate the

impact of TBL oriented environment management

system on the firms’ performance in China. Today

businesses operating in China strive not only to

achieve economic performance outcome but also to

address sustainability and environment issues in their

operation and management that are currently

generating considerable attention of managers, policy

makers, and academics (Chen and Torstensson, 2015).

Companies that fail to meet their responsibilities may

increase regulatory control, suffer fines, face lost

business opportunities and decreased reputation in the

long run. The main potential benefits that arise from

this approach is, positive customer ratings and

increased customer loyalty (Quazi, 2003). It is critical

60

Chen, Y. and Huang, Y.

The Impact of Triple Bottom Line-oriented Environmental Management System on Firms’ Performance in China: Evidence from Yangtze River Delta.

DOI: 10.5220/0007738600600069

In International Conference on Finance, Economics, Management and IT Business (FEMIB 2019), pages 60-69

ISBN: 978-989-758-370-4

Copyright

c

2019 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

to understand why and how a TBL oriented

environmental management system would help the

firm to achieve better performance. This research is

going to broaden and deepen the understanding of

Triple Bottom Line in order to examine whether TBL

oriented environmental management system has

positive effect to firm’s financial performance. This

research will adopt quantitative method as the way to

analyze. It will identify if Guanxi with Government

(‘Government influence’ here and after) has an effect

on CSR concept during firm’s daily operation and if

it also effects firm’s performance. The empirical

study will exam the validity of each factors

established in the conceptual model by approve those

hypotheses which are proposed in the following. First

of all, the questionnaire will be formulated based on

the previous study and several steps will be engaged

in order formulate an accurate survey. Then, we will

drop a pilot test around 20 samples. We will modify

some questions based on the feedback of the pilot test.

Finally, we will drop the formal questionnaire to

collecting data for this study. The findings from

analysis will be concluded at the end and we will

evaluate the findings as a discussion part of this

research.

1.2 Research Gap

TBL oriented environment management system has

now been documented as some standards in form of

certificates such like ISO series (Barla, 2007). ISO

certificate has become one of the most popular

certificates to establish corporation in worldwide,

especially those firms who involved in GVC. On the

other hand, firms always achieve special advantage

among their competitors, because they have good

GUANXI with local government (Zhai et al, 2013).

The local government will have certain policy to

protect local firms and they will also play a role to

connect those firms to other firm which in advanced

level in GVC, thus, GUANXI has played a significant

role in CSR in China. This is a challenge to

implementing TBL concept in the business aspect.

The research gap is to identify what are the latent

factors in which it may implementing the TBL-EMS

to firms in order to better promote CSR within the

greater China Region.

1.3 The Selection of Research Scope

The selection of this research has narrowed down to

specific area. The Yangtze River Delta, composed of

Zhejiang, Jiangsu Province, and Shanghai, has

become the center of China economy in terms of

foreign trade and FDI by 2010 (iFeng, 2016). Jiangsu

and Zhejiang Region is differentiated from other

regions of China. Firstly, Jiangsu Region features a

high socio-economic profile (gross domestic product

= 4.17 trillion CNY in 2015 with an 8.2% annual

growth; Xinhua, 2016a; Tencent, 2016), and is seen

as one of the most dynamic parts of China (XJTLU,

2013). Secondly, the Zhejiang Region has been

perceived as a significant industrial states and major

economic region of Yangtze River Delta (China

Jiaxing, 2016)

2 LITERATURE REVIEW

2.1 Triple Bottom Line Oriented

Environmental Management

System

Organizations spread results not only in economic

terms but in the way their business activities affect the

social surroundings and environment (Mitchell et al.,

2008). Most businesses have identified that their

long-term sustainable global success depends

on economic, societal and environmental

performance (Elkington, 1998). Firms will have to

oppose consumers and society as a whole if they only

pursue profit because profit maximization motives

may stand in the way of their success. CSR is not

simply confined to donation and charity, and it is

more than just complying with the law. It requires

firms to take care more about their employees and

also have to offer high-quality products and services

to society in terms of producing environmentally

friendly products towards meeting the expectations of

the consumers. TBL is the nucleus of CSR Scholars

(Marquis and Qian, 2014) emphases on importance of

TBL due to increasing environmental vulnerability,

corporate profits, social responsibility and

environmental responsibility care the cores of TBL

which lays the foundation of an enterprise and its

continuous development. Furthermore, Chinese firms

are experiencing challenges which makes the

business environment increasingly volatile. As a

result, incorporating corporate social responsibility

(CSR) into internal management system has gained

momentum (Kiron et al, 2015). The popularity of the

concept CSR has gained a rapid growth since 1990s

and it has been accepted by academia and business

practitioner as one of the vital concepts in procedure

of business strategy to achieve competitive

advantages in worldwide (Moura-Leite, 2011).

The Impact of Triple Bottom Line-oriented Environmental Management System on Firms’ Performance in China: Evidence from Yangtze

River Delta

61

Therefore, our first two hypotheses are proposed as

follows:

H1: An environment management system has a

positive effect on CSR policy.

H2: An environment management system has a

positive effect on Top management leadership.

2.2 Top Management Leadership

2.2.1 Corporate Governance Link to Firm’s

Performance by Top Management

The existing literature has shown that the agency

theory and stakeholder theory are in the guidance to

demonstrate the relationship between corporate

governance and firm’s performance (Jensen and

meckling, 1976; Freeman, 1984). Under the

stakeholder theory, Michelon and Parbonetti (2012)

believe that good CG can enhance the relationship

between enterprises and stakeholders by promoting

the sustainability of enterprises. They see good

corporate governance and sustainability as

complementary mechanisms for better stakeholder

management. They further point out that stakeholder

theory provides a link between governance

mechanisms and sustainability initiatives for

adjusting long-term management-stakeholder goals.

Thus, the top management leadership are the most

relevant role in between all these stakeholders. The

leadership role of top management has always been

perceived as influential in the implementation of

internal practices such as TBL oriented environment

management system possess necessary expertise and

access to key resources to implement TBL oriented

environment management system. Quinn and Baltes’

research concluded a summary that 73 percent of the

respondents believed that top management leadership

is instrumental in the development of the

management system that helps firms to achieve their

continuous success (Quinn and Baltes, 2007).

Likewise, their research also shows that 92 percent of

respondents agreed that firm’s success would be

measured not merely in economic terms but also by

customer satisfactions, operational efficiency, social

caring, and minimizing adverse environmental effect

where leadership role of top management is perceived

an important predictor (Coles et al, 2008). To sum up,

top management leadership is a vital factor impacting

firms’ performance from the point of view of the

bottom line perspective (Barla, 2007). Therefore, our

third hypothesis are proposed as follows:

H3: Top management leadership has a positive effect

on firms' performance.

2.3 Corporate Social Responsibility

Policy

Research reveals that internal CSR policy of firms is

not enough to protect them from the local

environment. Recently, the Chinese government has

enacted a new environmental regulation to replace the

25-year-old environmental legislation by providing

for severe penalties for firms involved in pollution

(Duggan, 2014). The previous regulation dealt with

light punishment for violating firms which were never

made public. Therefore, this suggests that Chine firms’

policy on CSR is an important consideration for the

long-term growth and performance of firms in China.

The complexity of doing CSR activities in China is

that the Government is a vital factor in successfully

implementing CSR program. Firms in China will be

influenced by the government deeply since China is a

socialist state and government have a significant

influence when producing policy or legislation.

H4: CSR policy has a positive effect on firms’

financial performance.

2.4 Guanxi with Government

Guanxi has been documented as an embedded role for

business practice in China. At the same time, Guanxi

has also emerged as important issue in academic

discussions especially in a methodological context

(Kriz, Gummesson and Quazi, 2013). It can be used

as an effective lubricant to boost the business

progress and this could also cause problem because

the firms may potentially violate other firms in form

of justice and fairness by using bribing and corruption

which will allow firm gain individual/organizational

advantage among rivals, yet damage the society’s

economic (Yin and Quazi,2016).

The business relationship in social embeddedness

in China is unique compare to other regions in the

world. The context factor Guanxi has now identified

by previous study as one of the most effective

lubricant to tie business relationship with other

stakeholders in the society at both individual and

organizational levels (Kriz et al. 2014). On the other

hand, Yin and Quazi (2016) believes that unethical

issues are inevitable results such like stock market

manipulations happened earlier in 2015, and this is

due to the nature of Chinese governmental

environment which caused by the ineffective and

inefficient governance structure (Yin and Quazi,

2016). Apparently, businesses think that CSR

activities are dictated by economic imperatives but in

actual practice, it is managed by the government in

FEMIB 2019 - International Conference on Finance, Economics, Management and IT Business

62

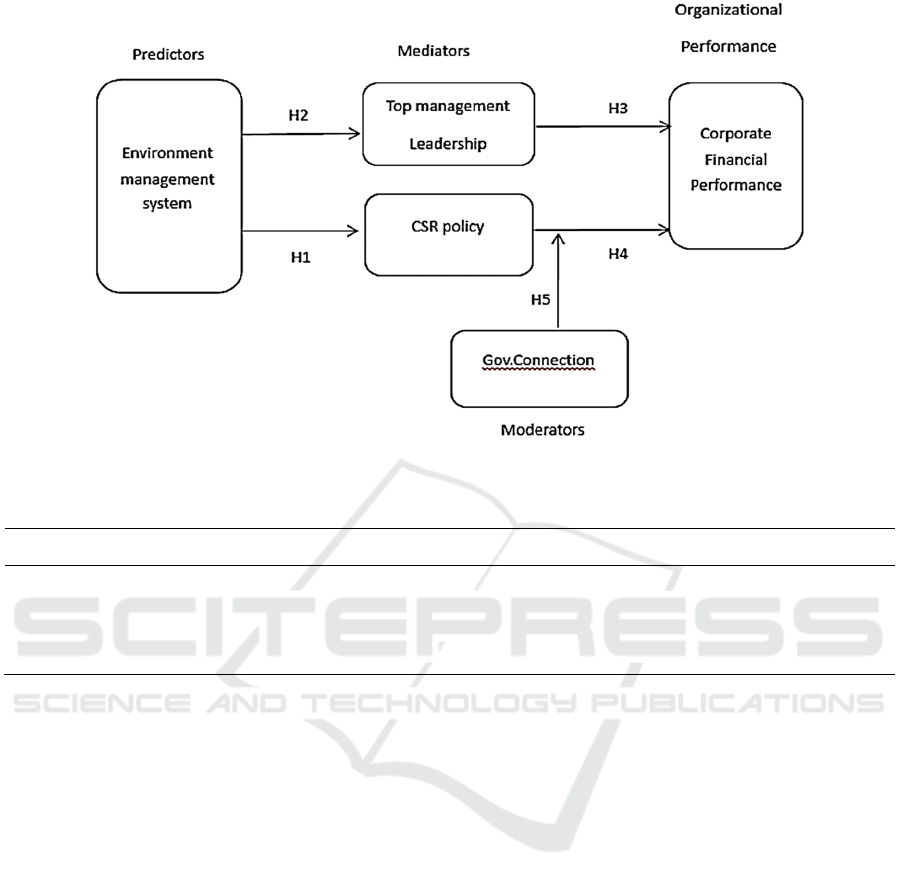

Figure 1: Conceptual Framework.

Table 1: Sample Description.

Zhejiang Jiangsu Anhui Shandong others

Male 73 12 22 15 19

Female 68 5 6 1 4

Total 141 17 28 16 23

China. Liao and other researchers (2014) point out

lots of CSR programs are get initiated by the

government in form of organize CSR activities and

establish some specific policy to restrict firm’s

operation activities. Research shows Chinese

government would like to quickly get involved in

businesses that are becoming stronger in growth.

Ithas been observed that 40 out of 46 Chinese

companies listed in the Fortune 500 are state-owned

enterprises where government plays a dominant role

in the operation and management of those firms

(China Briefing, 2011). Thus, it is expected that the

firms’ performance and implementation of TBL

oriented environment management system would be

greatly influenced by the government in China.

Therefore, our last but not least hypothesis are

proposed as follows:

H5: Guanxi network with government (government

connection) moderates the relationship between CSR

policy and firms' performance.

2.5 Theoretical Background and

Research Design

To sum up, we propose our conceptual framework for

this research, as illustrated in Figure.1.

3 METHOD

3.1 Questionnaire Design

To control the quality of the collected questionnaire

and data, we did add interrupts questions in the

questionnaire. We set few interrupt questions which

are conducted by contract-rephrasing to increase the

creditability of the survey. See Measurement Table at

Appendix.

3.2 Data Collection

Firstly, Data will be collected through survey

questionnaire, and questionnaire will be developed on

The Impact of Triple Bottom Line-oriented Environmental Management System on Firms’ Performance in China: Evidence from Yangtze

River Delta

63

the basis of established scales available in the extant

literature in the specific context of Chinese economy.

Measurement is attached in the Appendix 1. The

questionnaire will be designed as 7-point Likert scale

ranging from “1” strongly agree to “7” strongly

disagree. The questionnaires will be sent to the target

population comprising the top managers of

manufacturing companies listed by the State

Administration for Industry and Commerce of the

PRC where over 2000 companies are listed.

3.3 Sample

For this study, there are 330 participants in total who

participated in this research and there are 300 valid

survey questionnaires collected at Jiangsu and

Zhejiang respectively. We kept 225 valid survey

questionnaires in order to control the quality of the

data. We produce a table to present the sample

descriptive information as below.

The samples (see Table 1) collected from survey

questionnaire is satisfied with our expectation within

the limited time. Most of the Top Management

participants from manufacturing industry have

completed the questionnaire in assistant to our

research. We found many Internet Protocol (IP) of

the participant are from different region rather than

Jiangsu and Zhejiang region. This is maybe caused by

the physically transportation movement of

participants, and or their enterprise has moved to

other states.

4 ANALYSIS

4.1 Convergence Validity,

Average Variances Extracted

(Aves), Composite Reliability and

Cronbach’s Alpha

We firstly did test the convergence validity where the

item loadings based on the standardize shall be at

reach 0.7 for minimum (Feng et al., 2014) or greater

than 0.7 (Gefen et al., 2000). In this study, we pick up

the items from each construct that produces a

standardized factor loading greater than 0.65 from the

measurement model. After doing this, four items were

reserved from construct TBL, three were selected

from TML, five from CSR policy, and three from

Corporate Financial Performance. Thus, we dropped

other items that do not meet this benchmark in the

subsequent analysis. See Appendix for kept item.

Then, all average variances extracted (AVEs) value is

greater than0.5 in our as well as all of the composite

reliability (CR) value are beyond the standardized

value at 0.70. At the end, Cronbach’s alpha

coecients in this study satisfied the criterion of all

measurement constructs at level of 0.7.

With the regard of the value of Cronbach’s alpha,

we conducted each latent of the conceptual model in

the Table. 2. We can see from the results that the

Cronbach’s alpha is greater than 0.7 and this has

proved that the construct in the model has a good

reliability.

Table 2: Correlations between Latent Constructs and Descriptive Statistics.

EMS CSR Performance TML

EMS .531

a

CSR .431 *** .642

Performance .430 *** .588 *** .727

TML .328 *** .567 *** .361 *** .609

Mean 4.874 5.389 4.921 6.081

Standard deviation 2.023 1.785 1.866 1.681

Composite

reliability

0.818 0.898 0.889 0.821

Cronbach’s alpha 0.864 0.897 0.888 0.813

Note: * p < 0.05. ** p < 0.01. *** p < 0.001.

a: The diagonal entries represent the squared root of AVE of each construct.

FEMIB 2019 - International Conference on Finance, Economics, Management and IT Business

64

4.2 Discriminant Validity of the

Measurement Model

Regard to the discriminant validity, previous study

conducted the guidance for our analysis where the

AVE value of each construct was compared with its

squared correlation with any other construct (Hair et

al., 2014, p. 620). As shown in the bivariate

correlations, all AVE values (i.e., on the diagonal)

were 0.54 or higher, while all squared correlation

values were smaller than 0.346 (given the strongest

correlation of 0.588). The Table. 2 has shown the

bivariate correlations, all AVE values are greater than

0.54 or equal to 0.54 at least, meanwhile, the squared

correlation values were all smaller than 0.346 where

the strongest correlation is 0.588. thus, discriminant

validity has proved for the measurement model.

4.3 Model Fit

By the previous study guidance, our model fit of CFA

is satisficed as well as the model fitness indexes (CFI

= 0.956, NFI = 0.919) beyond than the desired value

of 0.9 and based on typically suggestion that badness

of fit measures (RMSEA = 0.069) shall smaller than

the threshold value of 0.08.

4.4 The Construction of Structured

Equation Model

Following CFA, we developed a structural equation

model in AMOS v.21. to test the research hypotheses.

By using maximum likelihood estimation, the model

demonstrates an overall satisfactory fit. The ratio of χ2

to the degrees of freedom was 2.159 (χ2 = 170.584, df

= 79), which is smaller than the desired threshold of 3.0

(Hair et al., 2014, p. 579). The model fit indexes (CFI

= 0.955, NFI = 0.921) were greater than 0.90 and

badness of fit measures (RMSEA = 0.072) were

smaller than 0.08, which suggests acceptable model fit.

Table 3 summarizes the results of hypotheses testing.

Regarding H1, TBL-EMS had a significantly

positive impact on the Top Management Leadership

(β = 0.423, p < 0.001). This finding has justified that

our assumption that TBL-EMS will influence the

awareness of Top management Leadership within

their firm. Regard to H2, TBL-EMS will positively

affect the CSR policy (β = 0.499) at a 0.001

significance level, and therefore, H2 has well

established where it maybe implies that firm’s CSR

policy that related to environment is in the importance

of environment sustainability in order to achieve

firm’s success of sustainable levels of developing of

the business, in this case, TBL-EMS has positive

effect on TML within the firm. Thus, H2 was

supported.

In accordance with H3, Top Management

Leadership of the firm is rejected based on the

analyzed data evidence (β = 0.075, p > 0.05), this

indicating that the Top Management Leadership is not

affecting firm’s Corporate Financial Performance

even it is one of the vital roles of implementing the

Triple Bottom Line oriented Environmental

Management System to their strategy. Hypothesis H4

were also found to be proved based on the analysis,

in that CSR Policy has positive effect with the

Corporate Financial Performance (β = 0.712) (at

0.001 significance level). The data have given us

implication where CSR policy is essential to firms in

order to achieve success on Corporate Financial

Performance or we can spot that CSR policy will

affect the Corporate Financial Performance.

4.5 Model Extension

4.5.1 Mediation Test

To achieve a comprehensive analysis working among

EMS, TML, and Corporate Financial Performance -

(CFP), the study tested the mediating role of Top

Table. 3: Structural Equation Model Result of the Hypotheses Testing.

Standardized

Estimation

Standard

Error

p-value Conclusion

H1: EMS→TML 0.423 *** 0.070 <0.001 Supported

H2: EMS→CSR 0.499 *** 0.067 <0.001 Supported

H3: TML→CFP 0.075 0.784 .433 Rejected

H4: CSR→CFP 0.712 *** 0.087 <0.001 Supported

Note: * p < 0.05. ** p < 0.01. *** p < 0.001.

Model fit statistics: χ2/df = 170.58/79 = 2.159, CFI = 0.955, NFI = 0.921, RMSEA = 0.072.

The Impact of Triple Bottom Line-oriented Environmental Management System on Firms’ Performance in China: Evidence from Yangtze

River Delta

65

Table. 4: Mediation and Moderation Test Results.

Dependent Variables:

Performance

Conclusion

Direct Effect Indirect

Effect

Mediation

EMS→TML→CFP

0.349 *** 0.081 ** Complementary mediation

supported

EMS→CSR→CFP

0.216 ** 0.213 *** Complementary mediation

supported

Moderation

H5: CSR→moderated by Guanxi→

Performance

n.s. Moderation not supported

Note: * p < 0.05. ** p < 0.01. *** p < 0.001.

n.s. insignificant. All tests are one-tailed.

Management Leadership and CSR policy in the EMS

CFP relationship under engage with bias-corrected

bootstrapping analysis remained with the function of

AMOS v.21. Table 4 demonstrated the results of

mediation test. First of all, TBL- EMS has both

significantly indirect and direct mediation eect

(p<0.05) on the Corporate Financial Performance,

this implies that Top Management Leadership fully

mediates (complementary mediation) the relationship

between EMS and Corporate Financial Performance.

Similarly, the CSR policy had a significant and

positive complementary mediation impact on the

Corporate Financial Performance.

The two supported complementary mediation

results have given us a hint that the Triple Bottom

Line oriented Environment Management System has

indirect and direct effect to Corporate Financial

Performance, and we identified that CSR will be

significant to influence Corporate Financial

Performance. The insignificance of H3 in this

complementary relationship here implies that the Top

Management Leadership either do not agree to imply

the EMS to their firm or they are not the most

effective stakeholder who effect the Corporate

Financial Performance mostly, even the participated

SMEs are mostly private own firms.

4.5.2 Moderation Test

We also tested the moderator that we proposed in our

conceptual framework which is Guanxi with the

government that moderates the relationship between

CSR and CFP. We ask the participant few questions

to test the relationship between the CSR policy and

local government to identify if the guanxi network is

going to affect the Corporate Financial Performance.

We attached our question in the Appendix. To

performance the moderation test, we first perform

factor analysis to examine the factor loading of each

item. The factor analysis shows that the factor loading

for item 1 to 4 is larger than 0.65 and consequently

we save those four items to construct a new variable

used in the moderation test.

However, the Guanxi with local government did

been proved that it is not a significant moderator in

the relationship between CSR and Corporate

Financial Performance (p>0.05). The effect by the

Guanxi with local government of the firm is not

significant, and this has led a consequence that CSR

policy is not significantly affected by the government.

We will further discuss this phenomenon in the

discussion section.

5 DISCUSSION

In the last part, we introduce the analysis results of

this study. In this section, we will evaluate these key

findings based on existing research, items, and other

relevant aspect.

This study focused on whether Triple Bottom

Line-oriented Environmental Management System

(TBL-EMS) has impact on Corporate Financial

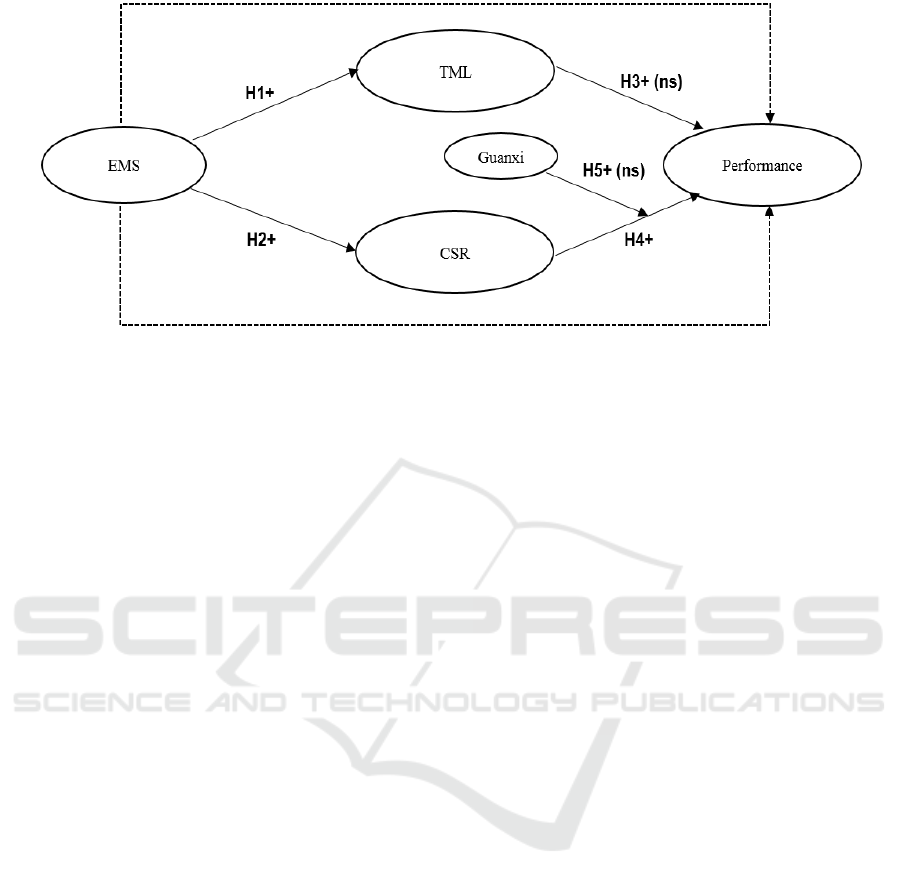

Performance (CFP). Our results, as illustrated in

Figure 2, point to a complex process, with several

FEMIB 2019 - International Conference on Finance, Economics, Management and IT Business

66

Figure 2: Conceptual Model.

factors influencing Corporate Financial Performance,

which in turn affects the likelihood that a firm may

need government’s external CSR policy to

constraint this industry. Our research is in Chinese

cultural context, previous study has justified that the

government is in dominance to influence the firm’s

performance in China due to the cultural context

(Yin and Quazi, 2016). In the past decades, the

concept CSR has become one of the most popular

recognized concepts from window dressing and

irrelevant role under the witness of the business

expert and professional academics (Aguinis and

Glavas, 2012).

This research has proved that CSR policy is an

essential role to effect SMEs in today’s China and

this is in consistent with the extant studies. On the

other hand, the firm’s Top Management Leadership

shall have significantly positive effect to Corporate

Financial Performance since most of the SMEs are

privately owned enterprise, our research did not

align with this point of view and this is inconsistent

with previous study. Moreover, Government

effecting power is not significant in our study and

this has been given a hint based on previous study

that without fully understanding a firm’s

background and situation, the Government pressure

cannot be accurately identified. Also, its position

has an influence on its political dependence (Chen

and Wang, 2011). Future research is encouraged by

them to better understand the contingencies

affecting firms’ political dependence and linked

pressures. However, our empirical research results

have indicated a slightly different from previous

study. We will discuss our findings on the structure

of our conceptual model. In the following sub-

section, we will be derived to demonstrate this

phenomenon in rich discussion.

6 CONCLUSION

CSR has gathered raising momentum of discussion in

today’s society. However, empirical studies on the

relationship between CSR and Corporate Financial

Performance based on the Triple Bottom Line are

remains low in the context of China. It is even fewer

researches which are specific to any industry related

to CSR. The media constantly expose unethical

business behaviors which it is caused by the impact

of the triple bottom line principle on business

operation is not obvious, and the impact of the triple

bottom line principle on the economic performance of

enterprises is not understood. In conclusion, we

found that participants believed that TBL-EMS had

an impact on Top management, and TML was not

important for the adjustment between EMS and the

CFP. In other words, the CFP could not be affected

by EMS through TML, and this is because there may

be other stakeholders more influential than TML

among manufacturing SMEs under Chinese context.

REFERENCE

Aguinis, H., & Glavas, A. (2012). What we know and don’t

know about corporate social responsibility: A review

and research agenda. Journal of Management, 38(4),

932–968. doi:10.1007/s10551-015-2776-0.

Barla, P. 2007, ISO 14001 ‘Certification and Environmental

Performance in Quebec’s pulp and Paper Industry’.

Journal of Environmental Economics and Management

Vol. 53 (3), 291–306.

China Briefing, 2011, ‘Political Influence in China’s

Biggest Companies Almost 100%’, China Briefing, 25

April, viewed 29 June 2016, <http://www.china-

The Impact of Triple Bottom Line-oriented Environmental Management System on Firms’ Performance in China: Evidence from Yangtze

River Delta

67

briefing.com/news/2011/04/25/political-influence-in-

chinas-biggest-companies-almost-100.html>

Chen, C & Torstensson, P 2015, ‘Environmental

Management System’s Impact on Corporate Social

Responsibility’ viewed May 17, 2018 <http://www.

diva-portal.org/smash/record.jsf?pid=diva2%3A79406

6&dswid=-5219>

Chen, H., & Wang, X. (2011). Corporate social

responsibility and corporate financial performance in

China: An empirical research from Chinese firms.

Corporate Governance: The International Journal of

Business in Society, 11(4), 361–370. doi:10.1108/

14720701111159217.

China Jiangsu. (2016), “The 2015 socio-economic

development report of Jiangsu Province”, 25 February.

Available at: http://jsnews.jschina.com.cn/system/

2016/02/25/027935497.html (In Chinese)

China Jiaxing. (2016), “The report of economy

development of Yangtze River Delta region in 2015”, 1

April 2018. Available at: http://www.jiaxing.gov.

cn/stjj/tjxx_6433/tjfx_6436/201604/t20160401_58464

4.html (In Chinese) (accessed 16 April, 2018).

Cohen, M. 2010, ‘The narrow application of Rawls in

business ethics: A political conception of both

stakeholder theory and the morality of markets’,

Journal of Business Ethics, vol. 97, no. 4, pp. 563-579.

Coles, J. L., Daniel, N. D., & Naveen, L. (2008). Boards:

Does one size fit all? Journal of Financial Economics,

87(2), 329–356. doi:10.1016/j.jfineco.2006.08.008.

Duggan, J. 2014, ‘China’s Polluters to Face Large Fines

Under Law Change’ the Gurdian, 25 April 2013,

viewed 30 may 2016, <https://www.theguardian.com/

environment/chinas-choice/2014/apr/25/china-environ

ment-law-fines-for-pollution>

Feng, T., Keller, L. R., Wu, P., Xu, Y., 2014. An empirical

study of the toxic capsule crisis in China: risk

perceptions and behavioral responses. Risk Anal.: Int.

J. 34 (4), 698–710.

Freeman, R. E. (1984). Strategic management: A

stakeholder approach. Englewood Cliffs, NJ: Prentice-

Hall.

Gefen, D., Straub, D., Boudreau, M.-C., 2000. Structural

equation modeling and regression: guidelines for

research practice. Commun. Assoc. Inf. Syst. 4 (7), 2–

76.

Globerman, S., Peng, M. W., & Shapiro, D. M. (2011).

Corporate governance and Asian companies. Asia

Pacific Journal of Management, 28(1), 1–14.

Guan, J. 2011, ‘Guanxi: The Key to Achieving Success in

China’. Viewed 15 Oct 2016 <http://sino-

platonic.org/complete/spp217_guanxi.pdf >

Hair, J. F., Black, W. C., Babin, B. J., Anderson, R. E.,

2014. Multivariate Data Analysis: Pearson New

International Edition, seventh ed. Pearson Education

Limited, Essex. Hand, C.M., Van Liere, K.D., 1984.

Religion, mastery-over-nature, and environmental

concern. Social Forces 63 (2), 555–570.

iFeng. (2016), “Status quo and reason of the recession of

Hong Kong economy”, 14 February. Available at:

http://finance.ifeng.com/a/20160214/14214957_0.sht

ml (In Chinese) (accessed 5 May, 2018).

Jensen, M. C., & Meckling, W. H. (1976). Theory of the

firm: managerial behavior, agency costs and ownership

structure. Journal of Financial Economics, 3(4), 305–

360. doi:10.1016/ 0304-405X(76)90026-X.

Kiron, D. 2015, Joining Forces: Collaborative Leadership

for Sustainability, viewed 21 May 2016, <https://hbr.

org/product/joining-forces-collaborative-leadership-

for-sustainability/ROT277-PDF-ENG>

Kriz, A., Gummesson, E., & Quazi, A. (2014).

Methodology meets culture: Relational and guanxi-

oriented research in China. International Journal of

Cross Cultural Management, 14(1), 27–46.

Marquic, C. & Qian, C. 2013, ‘Corporate Social

Responsibility in China: Symbol or Substance?’

‘organization science’ vol. 25, no. 1, pp.127-148.

Marquis, C., & Qian, C. (2014). Corporate social

responsibility reporting in China: Symbol or substance?

Organization Science, 25(1), 127–148.

Michelon, G., & Parbonetti, A. (2012). The effect of

corporate governance on sustainability disclosure.

Journal of Management and Governance, 16(3), 477–

509. doi:10.1007/s10997-010-9160-3.

Mitchell, M., Curtis, A. & Davidson, P. 2008. ‘Evaluating

the Process of Triple Bottom Line Reporting:

Increasing the Potential for Change’, Local

Environment, Vol. 13 (2), 67-80.

Moura-Leite, C & Padgett, C 2011. ‘Historical Background

of Corporate Social Responsibility’, Social

Responsibility Journal, Vol. 7 No: 4, pp.528 - 539

Quazi, A. and O’Brien, D. 2000, ‘An empirical Test of a

Cross-national Model of Corporate Social

Responsibility’, Journal of Business Ethics, 26, 33-51.

Quazi, A. M., 2003. Identifying the determinants of

corporate managers’ perceived social obligations.

Management Decision, 41(9), pp.822-831.

Quinn, L. & Baltes, J. 2007, ‘Leadership and Triple Bottom

Line’, center for creative leadership, North America.

Slaper, F. & Hall J. 2011. ‘The Triple Bottom Line: What

is it and How Does it Work?’, Social Responsibility

Journal, Vol. 7 (4), 528-539.

Xinhua. (2016b), “The 2015 GDP ranking among Chinese

cities”, 21 January. Available at: http://www.

tj.xinhuanet.com/news/2016-01/21/c_1117847129.htm

(In Chinese) (accessed 28 April, 2018).

XJTLU. (2013), “XJTLU Postgraduate Prospect 2013”. Xi’

an Jiaotong Liverpool University.

Yin, J & Quazi, A 2016, ‘Business Ethics in the Greater

China Region: Past, Present, and Future Research’,

Journal of Business Ethics, doi: 10.1007/s10551-016-

3220-9.

Zhai, Q., Lindorff, M., & Cooper, B. (2013). Workplace

Guanxi: Its dispositional antecedents and mediating

role in the affectivity– job satisfaction relationship.

Journal of Business Ethics, 117(3), 541–551.

FEMIB 2019 - International Conference on Finance, Economics, Management and IT Business

68

APPENDIX

Measurement items.

Measurement

name

Article Author Year

TBL-EMS Environmental Management System’s Impact on Corporate Social Responsibility Chen et al 2016

TML Ideology and the micro-foundations of CSR: why executives believe in the

business case for CSR and how this affects their CSR engagements

Hafenbradl and

Waeger

2017

CSR policy Performance implications for the relationships among top management leadership,

organizational culture, and appraisal practice: testing two theory-based models of

organizational learning theory in Japan

Jung and

Takeuchi

2010

An analysis of Islamic CSR concept and the opinions of Malaysian managers Siwar and

Hossain

2009

CFP Relations between transformational leadership, organizational learning,

knowledge management, organizational innovation, and organizational

performance: an empirical investigation of manufacturing firms

Noruzy et al. 2012

Gov.

connection

Political connections and entrepreneurial investment: Evidence from China's

transition economy

Wubiao Zhou 2012

The Eects of Business and Political Ties on Firm Performance: Evidence from

China

Zhou and Li 2011

Kept items.

Construct Items used in structural model

TBL-EMS Direct contribution to the society

Monitoring CSR of the partners

5 years changing environmental performance

5 years changing environmental performance

TML Human must live in harmony with nature in order to survive.

Humans are severely abusing the environment.

The Earth is like a spaceship with only limited room and resources.

CSR policy I am always courteous even to people who are disagreeable.

Our firm has clear policy statements urging environmental awareness in every area of operations.

Environmental preservation is a central corporate value of our firm.

The firm I stay with is like an extended family.

CFP In the past 5 years, OP measured by return on assets has increased.

In the past 5 years, OP measured by return on equity has increased.

In the past 5 years, OP measured by Growth of sales in its main products and markets has increased.

The Impact of Triple Bottom Line-oriented Environmental Management System on Firms’ Performance in China: Evidence from Yangtze

River Delta

69