Optimal Design of Production Systems: Metaoptimization with

Generalized De Novo Programming

Helena Brožová

1

and Milan Vlach

2

1

Czech University of Life Sciences, Faculty of Economics and Management, Department of Systems Engineering,

Kamýcká 129, Prague 6, Czech Republic

2

Charles University, Faculty of Mathematics and Physics, Department of Theoretical Computer Science and

Mathematical Logic, Malostranské náměstí 25, Prague 1, Czech Republic

Keywords: De Novo Programming, Model Conditions, Capacity Constraints, Requirement Constraints, Multi-Objective

Optimization, Optimal Design.

Abstract: Milan Zelený, in a number of papers, proposed and developed specially structured LP model called De Novo

Programming. This approach uses, in an essential way, a transformation of the original problem to continuous

knapsack problem, and it concerns only models with capacity constraints and some implicit assumptions about

the problem data. Here we extend this methodology to cases involving not only capacity constraints but also

requirement and balance constraints. This extension is based on the methodology of Zelený and uses some

principles of the STEM methods. We present an example of an adaptation of De Novo approach for models

with both capacity, requirement and balance constraints.

1 INTRODUCTION

Optimization of systems means finding "best

available" values of some criterion given a defined

input and output of this system. Optimal design of

systems means "best available" setting of proposed

system. Process of system design requires

understanding the content of three system approach

phases – reality, model and metamodel. In the first

phase the inquiring system is used for description and

understanding the real problem. If we do not

understand the reality, we cannot solve its problems

properly. In the second phase, inquiring system for

creating the model of problem solved is important.

The proper selection of the model is important for

obtaining the good results. In the third phases the

inquiring system of abstract process of model

creation, metamodel is studied (Gigch, 1991).

Production system optimization, in business and

marketing, is methodology for decision process,

which leads to the optimal production mix under the

defined criterion (criteria). Very often the

mathematical programming, especially the linear

optimization model is used to find the optimal

solution. As Zelený (1986, 1990a, 1990b)

emphasises, the already formulated model implicitly

contains the optimal solution. Therefore, the decision

is given by the set parameters of the model. The

crucial problem is how to formulate this model

correctly, respectively, how to choose the best input

data? The question of the best design or formulation

of the model can be seen as a metamodeling process.

A model is the first abstraction of the real-world

problem, and then a metamodel can be seen as the

second abstraction, highlighting and optimizing the

properties of the model itself. Metamodeling typically

involves studying the input, output relationships, and

then fitting right models to represent that behaviour.

Metamodeling identifies the underlying modelling

process and provides tools and techniques for model

development that will allow the proper application to

real problems. In this process, Zelený (1990a, 1990b)

suggests De Novo programming for optimal design of

production systems described by the linear

optimization model with the constraints of the “”

type. This approach is used in practical applications

for instance by Babic and Pavic, (1996), Huang,

Tzeng, (2007) and Zhang et al., 2009. Fiala (2011)

describes the future development and possible

applications of various modifications of De Novo

programming.

The main aim of this paper is to generalize the De

Novo approach for finding of optimal design of

Brožová, H. and Vlach, M.

Optimal Design of Production Systems: Metaoptimization with Generalized De Novo Programming.

DOI: 10.5220/0007682404730480

In Proceedings of the 8th International Conference on Operations Research and Enterprise Systems (ICORES 2019), pages 473-480

ISBN: 978-989-758-352-0

Copyright

c

2019 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

473

production system so that more types of constraints

are possible, in particular “≥” and “=”.

2 DE NOVO PROGRAMING

To motivate the De Novo approach to optimal design

of production systems, Zelený (1986, 1990a; 1990b,

2005, 2010) starts with considering the standard

linear programming model for allocating given

resources to possible activities in order to achieve a

given economic objective. If only one criterion is

considered and the objective is to maximize it, then

we have the problem

→ s.t.

,0 (1)

where is a real

,

-matrix, is a real -vector,

and is a real -vector.

When multiple criteria are involved, we have to

solve the multiple objective problem

→ s.

t

.

,0

(2)

where is a real

,

-matrix of coefficients of

objective functions.

An important question is what happens to the

optimal solution if the resource allocation changes.

Therefore, since the early days of linear

programming, both practitioners and theorists have

been interested in behaviour of solutions if

coefficients of the problem vary. Such questions have

led to the emergence of

• Sensitivity analysis (investigation of changes in

the individual coefficients which cause an optimal

solution to become non-optimal);

• Parametric programming (investigation of

changes when some of the coefficients are

functions of parameters);

• Robust optimization (investigation of solutions

under uncertainty that is represented as

deterministic variability in the value of the

parameters);

• Inverse optimization (investigation of solutions

with goal objective value when some of the

coefficients are parameters);

• De Novo programming (investigation of budget

allocation to individual resources which results in

optimal system structure) (Zelený, 1990a, 1990b,

2005, 2010).

The De Novo methodology (Zelený, 1990b) allows

for changes in some of the input data, particularly,

with changes in the components

of the right-hand

side vector of model (1) or (2). Clearly, such

changes describe changes in resources allocation;

modify the system design, and, therefore, the set of

feasible solutions, which may change the optimal

solution. In contrast to the sensitivity analysis and

parametric programming, De Novo programming

similarly as Robust or Inverse optimization requires

some additional exogenous data. De Novo

programming requires specification of cost of

resources and level of available budget.

According to Zelený (1990a, 1990b), if denotes

a given -vector of unit cost of resources and

denotes a given available budget, then De Novo

approach gives to the freedom to vary freely in the

region given by

0.

(3)

To indicate that the components of are now real

variables we change the notation and use the letter

instead of . Now it should be clear that instead

considering the general linear programming problem

(1), (2) resp., we deal with a special linear

programming problem with one objective function

→

s.t.

0

0,0.

(4)

resp. with multiple objective functions

→

s.t.

0

0,0.

(5)

To refer to the special structure of these problems, we

say that we are considering (De Novo) optimal design

problems with single, resp. multiple objective

functions.

Originally, the De Novo approach employs the

fact that, for each feasible solution

,

of problem

(4), is also a feasible solution of the problem

→

s.t.

0

(6)

where stands for the -vector

.

This is a continuous linear knapsack problem

whose optimal solution we can easily obtain by the

following procedure, provided all components of c

and V are positive: Let k be such that

⁄

⁄

,

⁄

,…,

⁄

.

Then the components of the optimal solution are

given by

,

⁄

, and

0 otherwise. Using ,

we set and

=. The resulting triple

ICORES 2019 - 8th International Conference on Operations Research and Enterprise Systems

474

,,

is called the optimal system design for De

Novo problem (4). It is clear that, in this simple case

with one objective function, we have

.

For the decision making under multiple criteria,

the De Novo approach first proceeds by solving

single objective optimization problems (replacing

by ,1,…,). Let

∗

be the -vector of optimal

values of individual objective functions over the set

of feasible solutions, which is the same as in problem

(4). Then

∗

is used to define an auxiliary problem,

called the meta-optimization problem, which is

formulated as the minimization problem (Zelený

1990b)

→

s.t.

∗

0.

(7)

Let x

*

be an optimal solution of this problem and

define

∗

and

∗

by

∗

∗

and

∗

∗

. It is

easy to see that

∗

and that the value

∗

is the

minimum budget for obtaining at least

∗

by using

∗

and

∗

. The model (7) is often (Zelený, 1986, 2005)

defined using equations in the form

→

s.t.

∗

0.

(8)

The fraction

∗

∗

is called the optimum path ratio

(Shi (1995), Zelený (1990b)) for approaching

∗

with

respect to given budget , and the ordered triple

∗

∗

;

∗

∗

;

∗

∗

is called the optimal system design

for the De Novo problem (5).

Shi (1995) proposes some variations of Zelený’s

approach, and introduces several (formally

uncountable many) optimum path ratios for enforcing

different budget levels of resources, which leads to

alternative optimal system designs. However, it turns

out that most of the proposed alternatives are not real

alternatives. To see it clearly let us consider Shi's

proposal in more detail.

Unlike the Zelený procedure, which is based on

∗

;

∗

;

∗

, Shi’s uses triple

∗∗

;

∗∗

;

∗∗

. The

solution

∗∗

is defined by the non-zero components of

the

∗

(

∗

) different single objective optimal

solutions

,1,…,

∗

. Without loss of generality,

for each solution

we suppose

⁄

, and

0, otherwise. Hereupon Shi defines synthetic

solution

∗∗

,

,…,

∗

∗

,0,…,0

, and

respective values

∗∗

∗∗

and

∗∗

∗∗

Then

∗∗

;

∗∗

;

∗∗

is used to define the following

optimum-path ratios.

∗

∗∗

,

∗∗

,

∑

∗

∗∗

,

∗

,

∑

∗

∗

,

∑

∗

,

(9)

where

∗∗

∗∗

,

, 0

1,

and

∑

1.

However, simple computations show that all

are equal to . Thus, for each ,

are equal

(Zelený’s ratio). The following equalities also apply

;

;

=1.

The question of solvability of problem (4) by

transforming it into a knapsack problem is mentioned

only in Zelený (1990b). Almost none of other

published articles mentions the prerequisites for using

the classical De Novo Programming approach. Some

of the usually tacitly assumed conditions are

discussed in Vlach and Brožová, (2018). Let us

noticed that:

• The model construction supposes only the

constraints of type , so called the capacity

constraints, which ensure compliance with

resource capacity.

• The transformation of the model (4) to the

knapsack problem (6) requires the positivity of

components of

. The positivity of

is

guaranteed if matrix is nonnegative and has no

zero-column and all components of vector are

positive.

• It is also necessary to find out whether the system

of equations

∗

or

∗

is solvable, as

required in Zelený (1990b).

• This approach can easily be extended to situations

with upper bounds on the components of .

3 DESIGN OPTIMIZATION OF

GENERAL PRODUCTION

SYSTEM

The system design optimization using a linear

optimization model should be based on several tasks:

The optimal choice of the type of constraints and

their number;

The optimal choice of criterion or criteria;

The optimal choice of the model data values.

The De Novo standard procedure supposes only

constraints of type

, called the capacity

constraints. The objective of these conditions is to

maintain the consumption of resources below the

Optimal Design of Production Systems: Metaoptimization with Generalized De Novo Programming

475

given limits. De Novo also supposes, that the unit cost

of these resources is known and total cost of these

resources is known, also.

In the linear optimization models, often other

types of constraints appear. For example, the

constraints of type

, so called the definitional

or binding constraints, serve to meet a particular

demand. Or, the so-called balance constraints, that is,

the constraints of type

0,

(

are positive values and

are negative values)

assure the balance between production and

consumption perhaps with a surplus or lack

allowed. Moreover, the constraints of type

,

so called the requirements constraints, guarantee the

required amount of production for sale. In practical

applications, it is often necessary to assume the cost

of such requirements (the cost of the contract signed).

The typical multiple objective linear optimization

model with the all types of mentioned constraints can

be written as follows

→

→

s.t.

0

(10)

where

,

are coefficients from the capacity

constraints,

,

are coefficients from constraints in the

equational form,

,

are coefficients from the requirements

constraints, and

,

are coefficients of objective functions.

The (criteria) optimization means to find the optimal

values of objective functions. Using De Novo

approach, the system design optimization means to

find the optimal values of capacities and requirements

under the given budget.

Consider now the values of all capacities and

requirements (right hand side values) as variables and

reformulate constraints into form of equations as

follows:

capacity constraints with unknown capacities

0 (11)

equational constraints with unknown definitional

value

0 (12)

requirements constraints with unknown

requirements

0

(13)

cost of necessary capacities and possible

requirements has to be less than or equal to the

given budget

(14)

where

,

,

are unknown values of

capacities and requirements,

,

,

are the cost of

capacities and requirements and is the available

budget.

Optimal system design means optimal budget

allocation and it means looking for optimal necessary

capacities and possible requirements. If these values

are known, the constraints of type (11), (12) and (13)

can be seen as the equations (Zelený, 1986). Into this

relaxed model, the budget constraint (14) has to be

added. In order to ensure finding of a non-trivial

solution, it is necessary to assume that the entire

budget will be used, i.e. the condition (14) will be in

the form of an equation. New model formulation will

be

→

→

s.t. 0

,0

(15)

The feasible solution exists if

0. The optimal

solutions of model (15) are found individually for

each objective function and these ideal values of all

objective functions create the ideal vector

,…,

(16)

The problem of optimal system design is now to find

the values of capacities and requirements under the

minimal necessary budget that guarantee at least the

ideal values of objective functions. The general

formulation of this meta-optimum model should be

(Zhuang and Hocine, 2018)

→

s.t.

0

,0

(17)

After solving model (17), the minimal budget

∗

for

achieving at least ideal objective functions values, the

optimal solution

∗

,

∗

and the corresponding

values of objective functions

∗

∗

are received.

Generally, this minimal budget

∗

can be either

smaller or larger than available budget . The

optimum path ratio for achieving the best

performance for a given budget can be defined

using

∗

. By using optimum path ratio , the

ICORES 2019 - 8th International Conference on Operations Research and Enterprise Systems

476

following data for optimal system design can be

received:

Optimal right-hand side values

∗

Optimal values of variables

∗

Optimal values of objective functions

∗

The optimal system design is done by equations

,

,

(18)

Unfortunately, this approach cannot be used for all

problems because there is no guarantee that there

exists a solution of the system of criterial constraints

as inequalities

(19)

or a solution of the system of criterial constraints as

equations

(20)

Therefore, some principles of the method STEM

(Benayoun et al., 1971, Roostaee et al., 2012) for

multiple objective optimization can be utilized. We

suggest not to solve inequalities (19) or equations

(20) but to find minimal weighted deviations from

the goal values)

,1,…,

,1,…,

(21)

where the additional signs min or max mean the type

of objective optimization.

This idea generally could allow to decision-maker

to change the goal values, which have to be reached.

4 GENERALIZED DE NOVO

PROGRAMMING

To solve the general linear optimization model (10)

to optimize the system design we suggest the

Generalized De Novo optimization approach. This

methodology of system design consists of the

following four steps.

Suppose now we look for a solution of the model

(10) under the possibility to change the values of

with

,

,

as the cost of capacities and

requirements while respecting budget .

1) Model Reformulation.

To allow the change the values of , the model

reformulation (15) with unknown variables

represents unknown values of capacities and

requirements while respecting budget will be used.

2) Partial Optimization.

Model (15) is now solved separately for the

individual objective functions. Received solutions are

filled into the decision matrix containing all values of

individual objective functions for single optimal

solutions of model (15)

⋯

⋮

⋱

(22)

Besides the vector of ideal values

(16) which

contains the best values from each column in the

decision matrix (22), the nadir vector is created

,…,

(23)

which contains the worst values of each objective

function in the decision matrix (22).

3) Metaoptimization.

The solution with the minimal deviations from the

ideal values of the criteria is found by solving the

following single objective model.

→

s.t.

0

,1,…,

,1,…,

,,0

(24)

Weights

are calculated based on the ideal and

nadir values as normalized values

2

2

.

1

∑

(25)

Such values of weights allow comparisons of the

deviations from ideal values of objective functions

without affecting their size.

The solution of this problem is

∗

,

∗

and

achieved values of objective functions

∗

∗

Remarks: Similarly as in the STEP method, the

decision maker could change the required goal values

and repeat the metamodel optimization.

4) Metametaoptimization.

Minimal necessary budget is found by solving the

following optimization model with one objective

function

→

s.t.

0

∗

∗

,0

(26)

Optimal Design of Production Systems: Metaoptimization with Generalized De Novo Programming

477

Solution of the model (26) exists, because the solution

of the model (24) exists.

Let the solution of problem (26) is

∗∗

,

∗∗

,

values of objective functions

∗∗

∗

and minimal

necessary budget is

∗∗

.

5) Solution – Optimal System Design.

By using optimum-path ratio

∗∗

, the following

solution of the optimal system design is received:

Optimal right hand side values

∗∗

Optimal values of variables

∗∗

Optimal values of objective functions

∗∗

The optimal system design

,

,

(27)

Remark: It is possible to suppose that not all resources

or requirements as RHS values (or corresponding

constraints) are subject of optimization of system

design. Such constraints of model (9) are not

transformed for system design optimization. In such

case the model (15) would have the following form

→

→

s.t.

0

,0

(28)

where

consists of the coefficients from the

constraints for which the optimal RHS have to be find

and

consists of the coefficients from the

constraints with fixed RHS values .

The steps of the suggested methodology then are

used accordingly. However, the model (28) may not

have a feasible solution with the budget constraints in

equation or inequality form.

5 EXAMPLE

The question of this problem is how many pieces of

three products have to be produced to fulfil the

contracts and minimized the labour cost and

maximized the profit under the production system

constraints. Problem with three products P1, P2, and

P3, two capacity constraints R1 and R2 (limited

recourses), three requirements constraints C1, C2 and

C3 (contracts with minimal supply), and two criteria

(minimization of the labour cost, maximization of the

profit) will be solved. The initial formulation of the

model is in Table 1 together with the price of the

resources and contracts and the total budget.

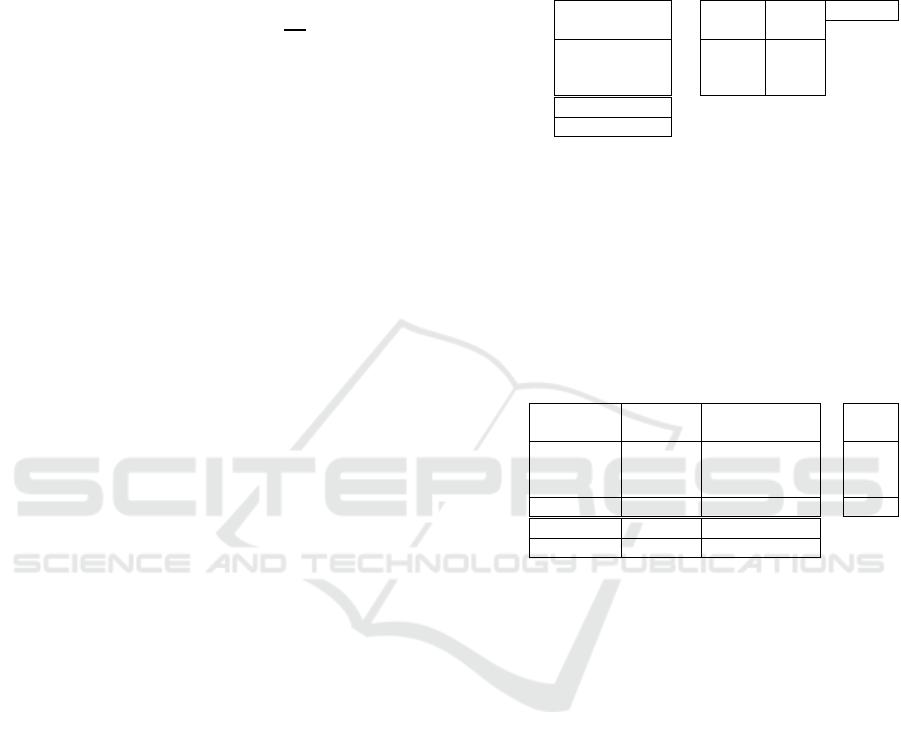

Table 1: Model of the three products problem.

P1 P2 P3

RHS Price

Total

b

udge

t

R1 2 0 1 ≤ 25 5 206

R2 1 1 1 ≤ 20 3

C1 1 ≥ 10 1

C2 1 ≥ 3 1

C3 1 ≥ 4 2

L. costs 1 1 8 MIN

Profi

t

236 MAX

Ideal values of objective functions of this model

are in the vector

65;45

.

1) Model Reformulation.

The model is reformulated using 5 unknown variables

,…,

representing unknow values of capacities

and requirements while respecting budget . The new

formulation of model is in Table 2.

Table 2: Reformulated model.

P1 P2 P3

y

R1

y

R2

y

C1

y

C2

y

C3

R1

2 0 1 -1 0 0 0 0

=

0

R2

1 1 1 0 -1 0 0 0

=

0

C1

1 0 0 0 0 -1 0 0

=

0

C2

0 1 0 0 0 0 -1 0

=

0

C3

0 0 1 0 0 0 0 -1

=

0

Budget

0 0 0 5 3 1 1 2

=

206

L. cost

1 1 8 0 0 0 0 0 MIN

Profit

2 3 6 0 0 0 0 0 MAX

2) Partial Optimization.

Ideal solutions are found solving two single objective

optimization models received by reformulation of the

initial model according to the (15).

The solution of minimization of the labour cost is

to produce only 14.71 pcs of the product P1 with

necessary 29.43 units of resource 1 and 14.71 units of

resource 2. This system design allows to closed only

the first contract. The minimal labour cost is 14.71

thous. CZK and maximal profit is 29.43 thous. CZK.

The solution of maximization of the profit is to

produce only 51.5 pcs of the product P2 with

necessary 51.5 units of resource 2. This system design

allows to closed only the second contract. The

minimal labour cost is 154.5 thous. CZK and

maximal profit is 51.5 thous. CZK.

Ideal values of objective functions under budget

are in the vector

14.71;154.5

.

3) Metaoptimization.

Based on the ideal and nadir objective function values

the following weights are used for calculation of

metaoptimization model (Table 3)

ICORES 2019 - 8th International Conference on Operations Research and Enterprise Systems

478

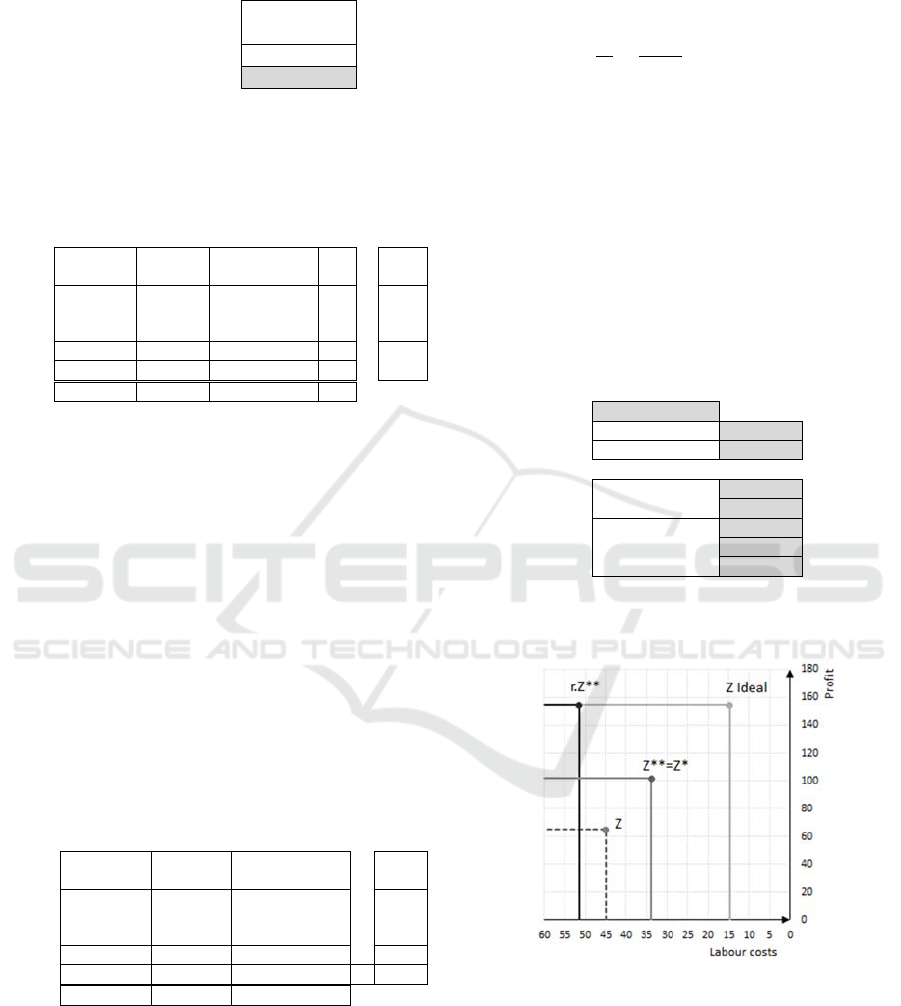

Table 3: Normalized weights.

Cost Profit

14.71 154.5

51.5 29.43

Average 33.11 91.96

Normalized weights 0.73 0.27

The formulation of the metaoptimization model

minimizing the deviation of ideal values is in Table 4.

Table 4: Formulation and solution of metaoptimization

model.

P1 P2 P3 yR1 yR2 yC1 yC2 yC3

R1

2 0 1 -1 0 0 0 0 0 = 0

R2

1 1 1 0 -1 0 0 0 0 = 0

C1

1 0 0 0 0 -1 0 0 0 = 0

C2

0 1 0 0 0 0 -1 0 0 = 0

C3

0 0 1 0 0 0 0 -1 0 = 0

L. cost

1 1 8 0 0 0 0 0 -1.4 = 14.7

Profit

2 3 6 0 0 0 0 0 3.8 = 154.5

Dev.

0 0 0 0 0 0 0 0 1 MIN

Its optimal solution is to produce only 33.82 pcs

of the product P2 with necessary 33.8 units of

resource 2. This system design allows to closed only

the second contract. The minimal labour cost is 33.82

thous. CZK and maximal profit is 101.44 thous. CZK.

The vector

∗

is

33.82;101.44

4) Metametaoptimization.

With the best obtainable values of both criteria is

solved the metametamodel to find the minimal

necessary budget. Similarly, as in the STEP method,

the decision maker could change these values and

repeat the metamodel optimization from the previous

step. Now the minimal budget is calculated with

objective functions values of the optimal solution of

metaoptimization model (Table 5).

Table 5: Metametaoptimization model.

P1 P2 P3

y

R1

y

R2

y

C1

y

C2

y

C3

R1

2 0 1 -1 0 0 0 0

=

0

R2

1 1 1 0 -1 0 0 0

=

0

C1

1 0 0 0 0 -1 0 0

=

0

C2

0 1 0 0 0 0 -1 0

=

0

C3

0 0 1 0 0 0 0 -1

=

0

L. cost

1 1 8 0 0 0 0 0 ≤ 33.8

Profit

2 3 6 0 0 0 0 0 ≥ 101.4

Budget

0 0 0 5 3 1 1 2 MIN

The optimal solution of metametaoptimization

model is equal to the solution of the previous

metaoptimization model, so we receive

∗∗

∗

33.82;101.44

. The minimal necessary budget

is

135.26 thous. CZK, what is less then we suppose to

invest to production. So, it is possible to extend the

production process.

4) Optimal System Design.

Optimal production structure under optimal design of

production system and available budget allows

expansion according to the optimal path ratio which

is equal to

∗

.

1,523.

The optimal system design (Table 6) allows

producing 51.5 pcs of the product P2 with necessary

51.5 units of resource 2. This system design allows to

closed only the second contract on 51.5 pcs of

products of products sold. The minimal labour cost is

51.5 thous. CZK and maximal profit is 154.5 thous.

CZK;

∗∗

51.5;154.5

. This means that there is

no need for resource 1 but higher consumption of

resource 2, e. g. 51.5 units. Also, there is only one

optimal contract, the contract C2 with 51.5 pcs of

product 2.

Table 6: Optimal system design.

P1 P2 P3

0 51.5 0 Solution

L. costs 118 51.5

Revenue 2 3 6 154.5

Inpu

t

data

Resource R1 2 0 1 0 25

Resource R2 1 1 1 51.5 20

Contracts C1 1 0 0 0 10

Contracts C2 0 1 0 51.5 3

Contracts C3 0 0 1 0 4

In the figure 1 the objective functions values of

selected models are shown.

Figure 1: Values of labour costs and profit for selected

solutions of three products problem.

It is possible to say, that the optimal system design

has resulted in significantly higher profit but with the

highest labour cost. Optimal system design results in

necessity to product only one type of product and

allocate the whole budget for the second resource and

the contract for the optimal type of products.

Optimal Design of Production Systems: Metaoptimization with Generalized De Novo Programming

479

6 CONCLUSIONS

In this paper, we continued our previous discussion of

De Novo Programming; see Vlach and Brožová

(2018). We briefly recalled the original approach of

Zelený, rectified some oversights in the alternative

proposal by Shi. Then we presented adaptation of De

Novo methodology for models with capacity,

requirement, and balance constraints, where the

transformation to continuous knapsack problem is not

possible.

Our proposal for Generalized De Novo

Programing is a way to optimize the system design in

more general settings. In particular, it is possible to

deal with more types of constraints and more types of

criteria.

REFERENCES

Babic, Z., Pavic, I., 1996. Multicriterial production

planning by De Novo programming approach.

International Journal of Production Economics, 43(1),

59–66.

Benayoun, R., de Montgolfier, J., Tergny, J., 1971. Linear

Programming with Multiple Objective Functions:

STEP Method (STEM). Mathematical Programming 1,

366-375.

Vlach, M., Brožová, H., 2018. Remarks on De Novo

approach to multiple criteria optimization. In:

Proceedings of the 36th Conference on Mathematical

Methods in Economics. Prague: Faculty of

Management, University of Economics, 618-623.

Fiala, P., 2011. Multiobjective De Novo Linear

Programming. Acta Univ. Palacki. Olomuc., Fac. rer.

nat., Mathematica, 50(2), 29–36.

Huang, Ch.Y., Tzeng, G.H., 2007. Post-Merger High

Technology R&D Human Resources Optimization

through the De Novo Perspective. In: Advances in

Multiple Criteria Decision Making and Human Systems

Management: Knowledge and Wisdom, Ed. Y. Shi et

al., IOS Press, 47-64.

Gigch, J.P., 1991. System Design Modeling and

Metamodeling. Plenum Press: New York and London.

Roostaee, R. Izadikhah, M. Hosseinzadeh Lotfi F., 2012.

An Interactive Procedure to Solve Multi-Objective

Decision-Making Problem: An Improvement to STEM

Method, Journal of Applied Mathematics [online].

Accessible from: https://www.hindawi.com/journals/

jam/2012/324712/.

Shi, Y., 1995. Studies on Optimum-Path Ratios in De Novo

Programming Problems. Computers and Mathematics

with Applications, 29(5), 43–50.

Zelený, M., 2010. Multiobjective Optimization, Systems

Design and De Novo Programming. In: Zopounidis C.,

Pardalos P. M. (eds.): Handbook of Multicriteria

Analysis, Berlin: Springer.

Zelený, M., 2005. The Evolution of Optimality: De Novo

Programming. In: Proceedings of EMO 2005, LNC

3410, ed. C.A. Coello Coello et al., Springer-Verlag,

Berlin-Heidelberg, 1-13.

Zelený, M., 1990a. De Novo Programming. Ekonomicko-

matematický obzor, 26(4), 406–413.

Zelený, M., 1990b. Optimal Given System vs. Designing

Optimal System: The De Novo Programming

Approach. International Journal of General System,

17(4), 295–307.

Zelený, M., 1986. Optimal system design with multiple

criteria: De Novo programming approach. Engi-

neering Costs and Production Economics, 10(2), 89-94.

Zhang, Y. M., Huang, G. H., Zhang, X. D., 2009. Inexact

de Novo programming for water resources systems

planning. European Journal of Operational Research,

199, 531–541.

Zhuang, Z.Y., Hocine, A. 2018. Meta goal programing

approach for solving multi-criteria de Novo programing

problem. European Journal of Operational Research,

265, 228–238.

ICORES 2019 - 8th International Conference on Operations Research and Enterprise Systems

480