The Analysis of Financial Reporting Disclosure through Internet

Financial Reporting on E-Government: Further Evidence from Local

Government of Indonesia

Arthaingan Mutiha

Vocational Education Program of Universitas Indonesia, UI Campus Depok, Indonesia

Keywords: Internet Financial Reporting, E-Government, Financial Disclosure Index

Abstract: The purpose of this research is to compare the quality of financial reporting disclosures through e-government

called Internet Financial Reporting. The research population is local government in Indonesia which is

divided into two groups. The first group is all provincial government in Indonesia, while the second group is

the district/city government selected one in each province. In the second group, the sample selection method

used is a purposive sampling method with the criteria of having the broadest area size, the most populated

and has the most substantial regional income. The index used to assess the quality of disclosure is using

disclosure parameters based on the Instruction of the Minister of Home Affairs No.188.5/1797 / SJ in 2012

concerning Transparency of Regional Budget Management and the index used has been modified following

research needs. There are four parameters used in this research; (A) The existence of the local official

government website, (B) The existence of a content menu with the name "Regional Budget Management

Transparency", (C) Availability of latest data (the data of 2018), (D) Availability of previous data (the data

of 2017), and (E) The presentation of budget information. Data were collected through observation with

internet media on the availability of parameters determined in this study. Two groups of samples were

analyzed on each parameter using the Mann-Whitney test to examine whether there is a significant difference

between the two groups of samples. The result of this research is that there are no significant differences of

financial disclosure between provincial government and city government on parameter A, B and E, and there

are significant differences of financial disclosure between provincial government and city government on

parameter C and D.

1 INTRODUCTION

Periodically, the organization will issue reports both

financial and non-financial reports. Periodic and

annual financial statements will be issued

periodically. As time and development progress,

rapid changes in the market and society cause this

reporting to become obsolete. Today's high

competition demands the provision of more up-to-

date information to enable management to adapt

quickly to opportunities and provide solutions to

problems that occur (Inês Pinto,2016). Organizations

need an information system that will help them

produce the financial information or reporting

needed. For this reason, computerized Accounting

Information Systems (AIS) has brought opportunities

for companies to perform accounting functions more

effectively and efficiently. This opportunity is

because the use of computerized SIA has resulted in

significant savings in terms of time and cost.

(Maziyar Ghasemi, 2011). Time and cost savings

allow companies to do other, more valuable things,

such as conducting financial reporting analysis. This

analysis is possible with the development of

technology. The use of technology in the accounting

process has increased as a result of the development

of computer technology in producing information for

corporate administration. At the same time, the use of

e-accounting (electronic accounting) in the company

has begun to expand (Aysel Guney, 2014).

Technology allows everything to be done quickly and

effectively. The results of the use of technology will

result in improvements in the means of

communication, transaction processing, and

information exchange will be more effective. In

addition, the use of technology will affect every

aspect of life, will consistently revolutionize the way

544

Mutiha, A.

The Analysis of Financial Reporting Disclosure through Internet Financial Reporting on E-Government: Further Evidence from Local Government of Indonesia.

DOI: 10.5220/0010704400002967

In Proceedings of the 4th International Conference of Vocational Higher Education (ICVHE 2019) - Empowering Human Capital Towards Sustainable 4.0 Industry, pages 544-551

ISBN: 978-989-758-530-2; ISSN: 2184-9870

Copyright

c

2021 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

communication between humans, even the way

people interact with the government (Jin Sangki,

2018). With the rapid development and increasingly

widespread use of the internet, organizations have

obtained highly useful communication tools to

present information to stakeholders. The use of the

internet in communicating information to

stakeholders enables the dissemination of

information in a more timely, cheaper and more

interactive manner. (Tatjana Dolinsek, 2014)

In addition, the Application of Information

Technology (IT) has a different impact on how work

is done. The purpose of implementing IT is to provide

a significant positive impact on the work done (Wan

Zuriati Wan Zakaria, 2017). As with the purpose of

financial statement distribution, the application of IT

makes a significant contribution in this regard.

Initially, the distribution was done manually, but now

it is done using internet technology. The rapid growth

of the internet in the past decade has enabled

companies to use new tools to disclose and

disseminate financial information to stakeholders.

(Inês Pinto,2016)

Public sector financial disclosure or reporting

using government web sites (e-government) is called

IFR (Internet Financial Reporting). Internet Financial

Reporting (IFR) is the disclosure of financial

information through the company's website (Inês

Pinto, 2016). Financial reports can be published

quickly with a broader range of coverage by using

IFR media to all interested users of financial

statements. This demand is clearly outlined in Law

No. 14 of 2008 concerning Public Information

Disclosure, Article 9 paragraph 4, that the obligation

to disseminate public information is conveyed in a

way that is easily accessible to the public, one of

which is through e-government. Based on this, the

local government should make use of the website as

an official means of delivering public information.

Law No. 14 of 2008 concerning Public

Information Disclosure has mandated that every

Public Agency must announce public information

regularly, and one of them is the information about

financial statements. This law also mandates that the

obligation to disseminate public information is

delivered in a way that is easily accessible to the

public in easily understood languages. This demand

is clearly outlined in this Act in article 9 paragraph 14

that the obligation to disseminate public information

is conveyed in a way that is easily accessible to the

public, one of which is through e-government.

To follow up on Law No. 14 of 2008, the Ministry

of Home Affairs issued Minister of Home Affairs

Instruction No. 188.52/1797/SC/2012 concerning

Regional Budget Management Transparency

(TPAD). The Minister of Home Affairs' instruction

instructs the provincial and district/city governments

to prepare a menu called Regional Budget

Management Transparency on the official

government website (e-government) and publish the

latest data on the context menu.

The Minister of Home Affairs' instruction

requires the Governor to instruct the Regents /

Mayors in their respective regions to implement the

following:

1. Provide facilities in the official regency/city

government websites. This facility was required

to be implemented no later than May 31, 2012.

2. Prepare a context menu with the name "Regional

Budget Management” in the official regency/city

government websites. This menu e was required

to be implemented no later than May 31, 2012.

This study aims to compare the quality of financial

statement disclosure or IFR (Internet Financial

Reporting) between provincial and district/city

governments in Indonesia by using disclosure

parameters based on the Instruction of the Minister of

Home Affairs No.188.5/1797 / SJ in 2012 concerning

Transparency of Regional Budget Management. The

parameters used in this research has been modified

following research needs.

The parameters used in this study are:

- Availability of official government websites

- Availability of a content menu with the name

“Regional Budget Management Transparency.”

- Availability of the latest data

The latest data used in this research is the data of

2018.

- Availability of data in the previous year

The data for the previous year is the data of 2017.

- Presentation of Budget Information Presentation

2 REVIEW OF LITERATURE

2.1 Literature Review

Implementation of Law no. 32 of 2004 concerning the

Regional Government and Law no. 33 of 2004

concerning Financial Balance between the Central

and Regional Governments marked the entry of

regional autonomy in Indonesia. The enactment of

regional autonomy requires the independence of local

governments in managing their budgets in order to

reduce their dependence to the central government. In

the context of agency problems, principal and agent

The Analysis of Financial Reporting Disclosure through Internet Financial Reporting on E-Government: Further Evidence from Local

Government of Indonesia

545

relations can occur in the government structure in

Indonesia, where the central government is the

principal and the regional government acts as an

agent. Fadzil and Nyoto (2011) also state that there is

a principal-agent relationship between the

government agency fund centre. In the context of

signalling theory, the government obliged to provide

an excellent signal to the people (Evans and Patton,

1987). The goal is that people can continue to support

the current government. Financial reports can be used

as a means to signal to the public. Excellent

government performance needs to be informed to the

people both as a form of accountability and

promotion for public purposes.

Disclosure of financial reporting using local

government websites (e-government) is commonly

called the Internet Financial Reporting (IFR).

Publication of regional budget information on the

local government website will make it easier for the

public to access regional budget information if it is

available wholly and correctly.

The development of the website used by the

district/city government began with the issuance of

Presidential Instruction No. 6 of 2001. The instruction

discusses the development and utilization of

telematics in Indonesia which is then clarified by

Presidential Instruction No. 3 of 2003 concerning

national development policies and strategies for E-

Government. In May 2008, the Indonesian

government passed Law No. 14 of 2008 concerning

Public Information Disclosure, which mandates that

every public body is obliged to open access for every

applicant to obtain public information, except for

certain information concerning the country's

resilience.

2.2 Research Method

Parameters used in this research is based on Minister

of Home Affairs Instruction No.188.52 / 1797 / SJ /

2012. There are five parameters consist of :

1. Availability of official government websites

a) The provincial and district/city governments

have an official go.id address and the address can

be accessed directly (becoming the first page)

when searched from Google / Yahoo

b) The website can be accessed properly (not in the

stage of under repair)

c) The website displays public information

2. Availability of a content menu with the name

"Regional Budget Management Transparency."

a) "Financial Transparency" menu is available on the

first page of the provincial or district/city

government website

b) The menu uses names under the Ministry of Home

Affairs Instruction, namely "Transparency of

Regional Budget Management."

c) The menu can be clicked, and there is available

clickable budget information

3. Availability of the latest data (in 2018)

The latest data referred to in this study is the data of

2018. According to the Ministry of Home Affairs

Instruction, ten documents must be included in e-

government websites, namely:

1. Summary of Work Plans and Budgets of

Regional Work Units (Summary of RKA –

SKPD)

2. Summary of Work Plans and Budgets of

Regional Financial Management Officers

(Summary of RKA – PPKD)

3. Draft Regional Regulation concerning Regional

Revenue and Expenditure Budget (RAPERDA

about APBD)

4. Draft Regional Regulation concerning Changes

in Regional Revenue and Expenditure Budget

(RAPERDA about The Exchange of APBD)

5. Regional Regulation on Regional Revenue and

Expenditures Budget (PERDA about APBD)

6. Regional Regulation on Changes in Regional

Budget Revenue and Expenditures

(PERDA about The Exchange of APBD)

7. Summary of Regional Government Work Unit

Budget Implementation Documents

(Summary of DPA SKPD)

8. Summary of Regional Budget Management

Official Budget Implementation Documents

(Summary of DPA PPKD)

9. Budget Realization Report for all Regional Work

Units (LRA of all SKPD)

10. Budget Realization Report of the Regional

Financial Management Officer (LRA PPKD)

4. Availability of data in the previous year (2017)

The previous year's data used in this study is 2017.

According to the Ministry of Home Affairs

Instruction, the previous year's data that must be

available in all of the data mentioned in point 3 above,

plus two data, which consists of:

1) The Regional Government Financial Report

audited by the Supreme Audit Agency (LKPD

already audited) and

ICVHE 2019 - The International Conference of Vocational Higher Education (ICVHE) “Empowering Human Capital Towards Sustainable

4.0 Industry”

546

2) The Opinion of the Supreme Audit Board on the

Local Government Financial Report (BPK

Opinion on LKPD).

This condition is because these two reports can only

be produced in the coming year after the current year

has passed.

5. Presentation of Budget Information Presentation

Presentation of budget information presentation can

be done in various ways that make it easy for readers.

The data can be presented in PDF format that can be

downloaded, or presented in graphical and

infographic form.

The scores are given to each parameter to assess

the five parameters mentioned above. Each

parameter is given value of 20 points. Therefore, the

total value of all parameters is 100 points. The scores

are summarized in the following table:

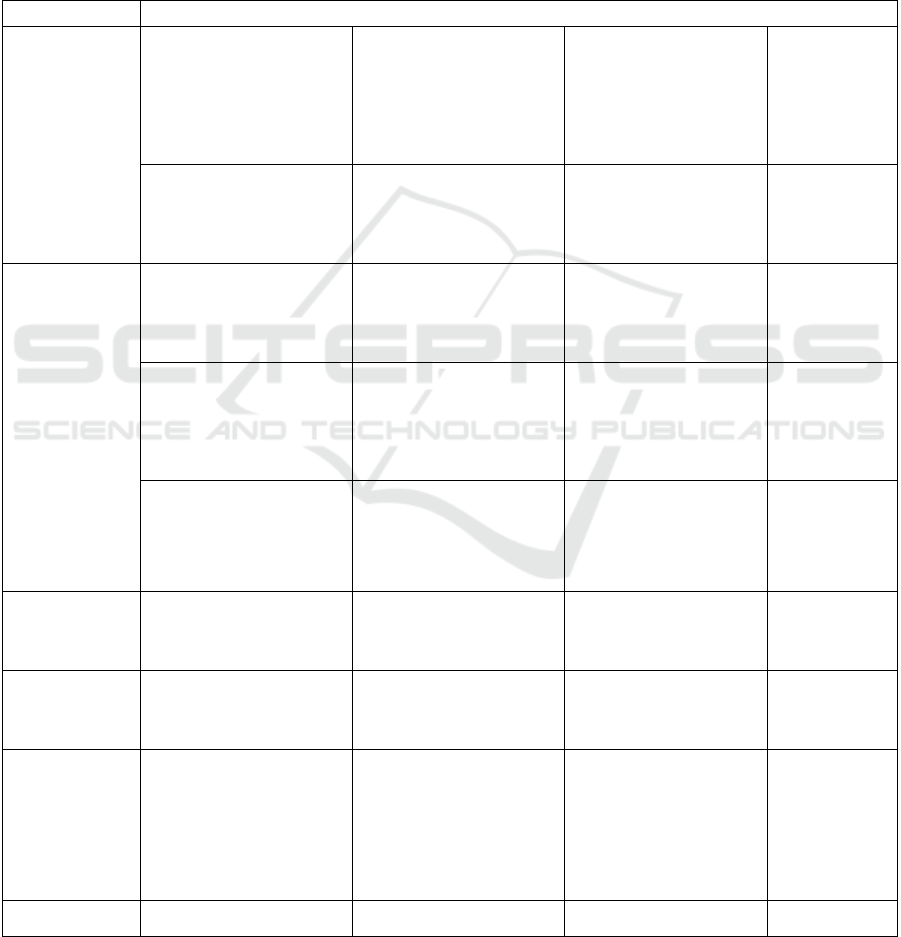

Table 3. Internet Financial Reporting Index

PARAMETER POINT

The existence of

official local

government

websites (A)

There is an official go.id

address and can be accessed

directly (becoming the first

page) when searched from

Google / Yahoo

(10 points)

There is an official go.id

address but it cannot be

accessed directly (not being

the first page) when searched

from Google / Yahoo (2- 4

clicks)

(8 points)

There is an official go.id

address but it cannot be

accessed directly (being the

first page) when searched

from Google / Yahoo (> 4

clicks)

(5 points)

There is no

official address

with go.id

(0 points)

A website can be accessed

properly (no interference)

and display public

information

(10 points)

The website can be accessed

properly but does not display

public information

(7 points)

The website cannot be

adequately accessed or has

a problem

(5 points)

The existence of a

content menu

with the name

"Regional Budget

Management

Transparency."

(B)

A financial transparency

menu/banner is available on

the first page of the local

government website

(7 points)

The menu/banner is found

on three or fewer mouse

clicks

(5 points)

The menu/banner is found

through four or more

mouse clicks

(3 points)

No menu at all

(0 points)

The menu/banner uses the

name that matches the

"Regional Budget

Management Transparency."

(7 points)

There are a menu and

information, but the name is

not suitable, for example,

"Budget transparency,

budget information."

(5 points)

There are menus and

information and use

completely inappropriate

names

(4 points)

The menu can be clicked,

and there is budget

information that can be

clicked

(6 points)

The menu can be clicked,

but there is no budget

information in it

(5 points)

The menu cannot be

clicked at al

(3 points)

Latest data

availability (up to

date) (C)

The latest data for the current

year is available and

complete (10 items)

(20 points)

The latest data for the

current year is available and

complete (6-9 items)

(15 points)

The latest data for the

current year is available

and complete (1- 5 items)

(10 points)

There is no data

at all

(5 points)

Availability of

previous year's

data (D)

Data for the previous year is

available and complete (12

items)

(20 points)

Data for the previous year is

available (7-11 items)

(15 points)

Data for the previous year

is available (7-11 items)

(10 points)

There is no data

at all

(5 points)

Presentation of

budget

information

presentation

(E )

Data is presented in the

format:

PDF that can be downloaded

Graphs available

Infographics available

(20 points)

Only available graphics and

PDFs that can be

downloaded

(15 points)

Only available PDF that

can be downloaded

(10 points)

There is only a

table

(5 points)

100 point 75 point 50 point 25 point

*The total score is 100 points

The Analysis of Financial Reporting Disclosure through Internet Financial Reporting on E-Government: Further Evidence from Local

Government of Indonesia

547

2.3 Sample Selection and Methodology

The population in this study are all local governments

in Indonesia, where the study sample is divided into

two groups. The first group is all provincial

governments in Indonesia, while the second group is

district/city governments that are selected based on

individual or purposive sampling method. The

specific criteria used to select the district/city are; in

each province, one district/city government will be

chosen with the criteria such as the area with the

broadest category, the most population, and with the

highest income.

The number of provinces in Indonesia is 34

provinces. Meanwhile, the total sample of

regencies/cities is 33, excluding five administrative

cities and an administrative district in Jakarta

Data were collected through observation with

internet media on the availability of parameters

determined in this study. Two groups of samples were

analyzed using the Mann-Whitney test to examine

whether there is a significant difference between the

two groups of samples.

3 RESULT

Based on the results of the study, the highest score for

the parameter is the category of availability of the

official website of the provincial and city

government. Then, followed by the availability of

financial transparency menu in the second score, then

the category of last year's data availability, the

availability of the latest year data then the percentage

of budget information presentation.

The analysis shows that all provincial governments

already have an official website with the address go.id

and 97% of the website can be accessed properly and

display public information. Meanwhile, 68% of

provincial governments already have a menu called

Budget of Transparency on their official website.

However, only 58% of the website, have names

according to the rules, namely “Regional Budget

Management Transparency" Regarding the provision

of data/information in the year of 2018, only 37% of

the province have already provided complete data.

While for the previous year's data provision, only

40% of the province already provided complete data.

Furthermore, only 28% of the provincial government

presents data in pdf format that can be downloaded,

or in the form of tables and infographics.

The results of the analysis for the city government

showed that there are two city governments which do

not yet have an official city government website (as

of the date of these observations performed) namely

Tanjung Selor and Sofifi. Meanwhile, 60% of the city

governments have already Budget Transparency

menu. However, only 49% of the cities have named

the menu in accordance with the rules, namely

“Regional Budget Management Transparency".

Regarding the provision of data/information in 2018,

only 27% of cities provide complete data. While for

the previous year's data provision, only 26% of cities

provide complete data. Furthermore, only 29% of the

city government presents data in pdf format that can

be downloaded, or in the form of tables and

infographics.

Based on Table 2, North Kalimantan received the

highest score among the other provinces. Then the

second score and highest third, obtained by South

Kalimantan and Central Java. For the city group,

Banda Aceh received the highest score among other

cities. Then proceed by the city of Bandung and the

city of Ambon

Table 2. Financial Disclosure Index

No Province Score No Cities Score

1 Kalimantan Utara 90 1 Banda Aceh 80

2 Kalimantan Selatan 78 2 Bandun

g

68

3 Jawa Tengah 73 3 Ambon 61

4 Kalimantan Ten

g

ah 73 4 Medan 60

5 Jawa Barat 71 5 Bandar Lampung 60

6 Banten 68 6 Gorontalo 60

7 Gorontalo 68 7 Padan

g

58

8 Jambi 67 8 Yogyakarta 58

9 Sulawesi Barat 66 9 Suraba

y

a 58

10 Kalimantan Barat 65 10 Palembang 57

11 Maluku 63 11 Ku

p

an

g

57

12 Pa

p

ua 63 12 Makasa

r

57

13 Kepulauan Bangka Belitung 62 13 Jambi 56

14 Bengkulu 60 14 Banjarmasin 55

ICVHE 2019 - The International Conference of Vocational Higher Education (ICVHE) “Empowering Human Capital Towards Sustainable

4.0 Industry”

548

15 Aceh 58 15 Mamuju 55

16 Lam

p

un

g

55 16 Pekanbaru 52

17 DKI Jakarta 55 17 Semarang 52

18 Sulawesi Selatan 55 18 Tanjung Pinang 51

19 DI Yogyakarta 51 19 Pontiana

k

48

20 Riau 50 20 Den

p

asa

r

47

21 NTT 49 21 Samarinda 47

22 Sulawesi Utara 47 22 Palangkaraya 45

23 Sumatera Selatan 46 23 Manokwari 42

24 NTB 43 24 Ben

g

kulu 35

25 Kalimantan Timur 43 25 Pangkal Pinang 30

26 Jawa Timu

r

35 26 Serang 30

27 Sumatera Utara 30 27 Manado 30

28 Sumatera Barat 30 28 Kendari 30

29 Ke

p

ulauan Riau 30 29 Ja

y

a

p

ura 30

30 Sulawesi Ten

g

ah 30 30 Palu 28

31 Sulawesi Tenggara 30 31 Matara

m

25

32 Maluku Utara 30 32 Tanjung Selor 0

33 Pa

p

ua Barat 30 33 Sofifi 0

34 Bali 15

Following are the results of the Mann Whitney Test

statistical test to compare the five parameters between

two sample groups, namely the provincial and city

governments.

Table 4. Summary of The Result

Parameter N

Mean

Rank

Sum of

Ranks

Mann-

Whitne

y

Wilcoxon

W Z

Asymp.

Sig (2

tailed)

The existence of

official local

government

websites

Provincial

35,53 1208

509 1.070 - 1,430 0,152

Cit

y

32,42 1070

The existence of a

content menu with

the name

"Regional Budget

Management

Trans

p

arenc

y

"

Provincial

35,66 1212,5

504,5 1065,5 - 0,721 0,471

Cit

y

32,29 1065,5

Latest data

availability (up to

date

)

Provincial

37,66 1280,5

436,5 997,5 - 2,092 0,036

Cit

y

30,23 997,5

Availability of

previous year's

data

Provincial

39,85 1355

362 923 - 3,150 0,002

City 27,97 923

Presentation of

budget

information

Provincial

33,46 1137,5

542,5 1.137,5 - 0,257 0,797

Cit

y

34,56 1140,5

The existence of official local government websites

(A)

From table 4, it can be seen that the mean value for

the provincial government is greater than the city

government, while the value of Asymp.Sig (2 tailed)

is 0.152> 0.05. This value can be concluded that Ho

is accepted which means that there is no significant

difference regarding the existence of the official local

government website between the provincial

government and the city government.

The existence of a menu with the name "Regional

Budget Management Transparency" (B)

From table 4, it can be seen that the mean value for

the provincial government is greater than the city

government, while the Asymp. Sig (2 tailed) value is

0.471> 0.05. This value can be concluded that Ho is

The Analysis of Financial Reporting Disclosure through Internet Financial Reporting on E-Government: Further Evidence from Local

Government of Indonesia

549

accepted which means that there is no significant

difference regarding the existence of the menu

“Regional Budget Management Transparency”

between the provincial government and the city

government.

Latest data availability (C)

From table 4, it can be seen that the mean value for

the provincial government is lower than the city

government, while the Asymp.Sig (2 tailed) value is

0.036< 0.05. This value can be concluded that Ho is

not accepted which means that there is a significant

difference regarding the availability of the latest

regional government data between the provincial

government and the city government.

Availability of previous year's data (D)

From table 4, it can be seen that the mean for the

provincial government is greater than the city

government, while the value of Asymp.Sig (2 tailed)

is 0.002 <0.05. This value can be concluded that Ho

is rejected, which means that there is a significant

difference regarding the availability of the previous

year’s data between the provincial government and

the city government.

Presentation of budget information (E)

From table 4, it can be seen that the mean for city

government is greater than the provincial

government, while the value of Asymp.Sig (2 tailed)

is 0.575> 0.05. This value can be concluded that Ho

is accepted, which means that there is no significant

difference regarding the presentation of local

government information between the provincial

government and the city government.

4 CONCLUSION

Based on the results of research conducted, it can be

concluded that all provincial governments already

have official government websites while there are two

cities (at the time this data is accessed), do not yet

have official government websites. The lowest

category that has not yet been fulfilled by the

provincial or city government is the provision of data

both the latest and last year's data, such as financial

report data, audit opinion by the Supreme Audit

Board, and other data required by regulations.

Likewise, for the presentation category of budget

presentations, both the provincial and city

governments still have low scores. The three

provincial governments that have the highest scores

in a row are North Kalimantan, South Kalimantan and

Central Java while the three highest scores for the city

government are Banda Aceh, Bandung and Ambon.

The result of this research is that there are no

significant differences of financial disclosure

between provincial government and city government

on parameter A, B and E, and there are significant

differences of financial disclosure between provincial

government and city government on parameter C and

D.

REFERENCES

Antonio Trigo. (2016). Accounting Information System:

Evolving Towards A Business Process Oriented

Accounting. Procedia Computer Science

Aysel Guney. (2014). Role of Technology in Accounting

and E-Accounting. Procedia-Social and Behavioral

Sciences.

Caludiu Brandas. (2015). Global Perspectives on

Accounting Information System: Mobile and Cloud

Approach. Procedia Economics and Finance.

Evans, J & Patton. (1987). Signalling and Monitoring in

Public Sector Accounting. Journal of Accounting and

Research

Fadzil, Faudziah Hanim, and Nyoto, Harryanto (2011).

Fiscal Decentralization after implementation of Local

Government Autonomy in Indonesia. World Review of

Business Research.

Fernando Belfo. (2013). Accounting Information System:

Tradition and Future Directions.Procedia Technology

Ines Pinto, Winnie Ng Picoto.(2016). Configurational

Analysis of Firms Performance: Understanding The

Role of Internet Financial Reporting. Journal of

Business Research.

John J. Morris. (2011).The Impact of Enterprise Resources

Planning Systems on the Effectiveness of Internal

Control over Financial Reporting. Journal of

Information Systems.

Jin Sangki, (2018). The vision of Future E-Government via

New Government Maturity Model: Based on Korea’s E-

Government Practises. Telecommunication Policy.

Kajian Akses Warga atas Informasi Anggaran Daerah.

(2014). Penabulu Alliance

Law No. 14 of 2008. Public Information Disclosure.

Indonesia

Maziyar Ghasemi. (2011). The Impact of Information

Technology (IT) on Modern Accounting Systems.

Social and Behavioral Sciences.

Noemi Pena Miquel. (2018). New Accounting Information

System: An Application for A Basic Social Benefit in

Spain. Spanish Accounting Review.

Paolo Quattrone. (2016). Management Accounting Goes

Digital: Will The Move Make It Easier. Management

Accounting Research.

Presidential Instruction No. 3 of 2003. National

Development Policies and Strategies for E-

Government. Indonesia

Presidential Instruction No. 6 of 2001. Telematika.

Indonesia

ICVHE 2019 - The International Conference of Vocational Higher Education (ICVHE) “Empowering Human Capital Towards Sustainable

4.0 Industry”

550

Tatjana Dolinsek. (2014). The Determinants of Internet

Financial Reporting in Slovenia. Emerald Insight

Verawaty. (2014). Analisis Komparasi Indeks Internet

Financial Reporting Pemerintah Daerah di Indonesia.

SNA Mataram

Wan Zuariati Wan Zakaria, Norazlina Illias. (2017). A

Survey on The Impact of Accounting Information

System on Task Efficiency: Evidence from Malaysian

Public Sector Agencies. International Review of

Management and Marketing.

The Analysis of Financial Reporting Disclosure through Internet Financial Reporting on E-Government: Further Evidence from Local

Government of Indonesia

551