Effect of Budgeting Factors on Budgetary Slack in Indonesia

Universities

Sandra Aulia

Accounting Laboratory, Vocational Education Program, Universitas Indonesia, Indonesia

Keywords: Budgetary slack, participation, accountability, information asymmetry, individual behaviour.

Abstract: This study aims to investigate the effect of budgeting factors on budgetary slack in Indonesia Universities.

A quantitative research methodology is used in this study. We used 63 respondents with structural position

universities in Indonesia. A questionnaire was conducted, and structural equation modelling was used to test

the proposed models among the constructs and related hypotheses. This research found that accountability

has a significant effect on Budgetary Participation, Information Asymmetry and Individual Behavior, but no

significant effect on Budgetary Slack. Budgetary participation has no significant effect on Information

Asymmetry. Information Asymmetry has no significant effect on Individual Behavior. Individual behaviour

has no significant effect on Budgetary Participation. Budgetary Participation and Information asymmetry

have no significant effect on Budgetary Slack, but Individual behaviour has a significant effect on

Budgetary Slack when preparing to budget in universities. This paper contributes to existing research on

budgetary slack in extent on previous work by identified the factors affecting the budgetary slack. The most

factor affects the budgetary slack is participation among individual who gives information to budgeting and

asymmetry information. The findings of this study suggest that universities should give target that the

department or division to achieved.

1 INTRODUCTION

The budget has a vital role in carrying out the

university’s strategic plan, which is a benchmark for

accountability and performance. It is expected that

the budget can be adjusted to the needs of each part

under its control. Based on input from each section,

all information is obtained and does not result in

information asymmetry, thereby reducing budgetary

slack. Budgeting that involves all parties will

influence individual behaviour in organising to

implement a strategic plan to achieve the stated

vision and mission.

The budget can reflect economic and social

policies in the form of decisions to determine what

funds are used to use (Lewis, 2006). The budget is

the basis for financial negotiations with funders,

which describes the expected cost of an activity

package when the activities are carried out, so there

is a change from the top part of the Mango budget

(2006). Hansen et al. (2003) stated that the budget

aims to increase long-term profit in a relatively short

period which is used for various purposes including

planning and coordinating various organisational

activities, allocating resources, and motivating, but

their use is far from perfect. Concern about using the

budget for planning and performance evaluation.

Budgets inhibit the allocation of organisational

resources for their best use and encourage decision

making.

Kahar et al. (2016) get strong evidence in

analysing the relationship between participatory

budgeting and budgetary slack. There is a

relationship between participatory budgeting on

individual performance and job satisfaction as an

intervening variable. According to Fitri (2004),

Budget control lacks the presence of information

asymmetry and budgeting participation. The way

managers are involved in the strategy process

determines the creation of slack budgets. When

trying to influence the behaviour of subordinate

budgeting managers, top management must take a

holistic approach and consider the elements of the

planning process (Baerdemaeker, 2015). Strategic

Business Unit Managers participate in determining

the objectives of their specific unit budget and have

several levels of influence on their final budget. The

use of budget refers to the use of budget information

526

Aulia, S.

Effect of Budgeting Factors on Budgetary Slack in Indonesia Universities.

DOI: 10.5220/0010700800002967

In Proceedings of the 4th International Conference of Vocational Higher Education (ICVHE 2019) - Empowering Human Capital Towards Sustainable 4.0 Industry, pages 526-533

ISBN: 978-989-758-530-2; ISSN: 2184-9870

Copyright

c

2021 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

by business unit managers to measure unit

performance (Hoque et al., 2016).

Chong et al. (2015) stated that budgetary slack

causes subordinates to be honest in disclosing

personal information about performance. When

budgets are applied to innovation policies, managers

will have simple policies, not only to improve

efficiency but also to improve product quality.

Budgetary slack has an impact on the quality of

customer relations and organisational performance

(Chen et al., 2016).

Previous studies examined the factors that

influence budgeting for budgetary slack with

different outcomes except for budgetary

participation factors. The difference between this

research and the previous one is combining the

factors used in the previous research into one using

the Structural Equation Model. This study examines

the effect of budgetary participation, accountability,

information asymmetry, and individual behaviour as

a factor in budgeting in universities in Indonesia

against budgetary slack.

2 LITERATURE REVIEW

2.1 Budget

Budget is a vital economic policy instrument that

reflects policy priorities in the form of a decision to

determine the funds to be used (Lewis, 2006).

Budgeting is used to achieve objectives such as the

planning and coordination of the various activities of

the organisation, the allocation of resources power,

motivating employee (Hansen et al., 2003). A

university budget is a must and essential to do to

achieve the goals of the university. It is also an

indicator to measure the achievements of a study

program and the university as a whole.

2.2 Budgetary Slack

Duck et al. (1998) stated that slack is intent to

establish income and ability of production are much

lower, or fees and use of sources of power are much

higher. Slack is the difference between the amount

that is budgeted to cost and expense that should

(Duck and Perera, 1997). Chow et al. (1988) stated

that slack as the difference between performance is

expected with that reported in the budget.

In budgetary slack, subordinates are allowed to

provide information related to its work on the

standards specified which later would become the

basis of the evaluation of performance that can

improve the satisfaction of work and performance

(Young, 1985). Schriff and Lewin (1970) stated

budgetary slack is the mechanism that is used

managers to set a budget that can be in trying to

accomplish as a way managers to achieve its

interests alone. To conclude, a mechanism should

achieve individual interests to establish a budget.

They are achieved if there is a difference between

the amount of budget and the expected expenditures.

Budgetary slack associated with budgetary

participation, namely the participation of managers

or subordinates in participating in the preparation of

the budget can influence the outcome and process of

budgeting (Duck, 1995). Stevens (1998) in Fitri

(2004) stated that budgetary slack occurs because of

the asymmetry of information, the uncertainty of

performance, the interests of personal and conflict

between agent and principal. Slack is created by

lower-level managers who know the conditions in

the field so that managers can set targets that can be

achieved (Van der Stede, 2000). The inconsistency

in the results of research before giving ideas for

researchers to give a contribution to the research.

2.3 Accountability

Kilby (2004) stating accountability is divided into

two so that rating giver (upward accountability) and

vote by the community (downward accountability).

Their demands of accountability would lead to

control over the budget that is tight so that directors

and managers will be careful in preparing the budget

related to the reports that should they accountable

(Van der Stede, 2001). Hopwood (1972) in Otley

and Fakiolas (2000) stating the demands will be

accountability rigour in the assessment of

performance-based budget (rigid budgetary control

syle). The results of previous studies are negatively

related, and some are positively related. Dunk

(1993) and Van der Stede (2001) find increased

social pressure on achieving budget targets reducing

the amount of slack. Thereby also control which

emphasises on the results of the end, will lead to

declining slack. However, Merchant (1985) found

the relationship positive between budgetary slack

with accountability through control strict of top

management. Structural in the University High will

seek to be careful in preparing the budget because it

relates to the budget that must be accounted for.

Hanson (1996) and Van der Stede (2001) have found

that accountability has a positive effect to budgetary

participation, but Ebdon et al., (2016) found that no

significant relationship between accountability and

Effect of Budgeting Factors on Budgetary Slack in Indonesia Universities

527

budgetary participation. Young (1985) and Van der

Stede (2001) found that accountability has a positive

effect on asymmetry information. Commann (1979)

found that accountability has a positive effect on

individual behaviour, but Otley (1978) found no

effect between accountability and individual

behaviour. Van der Stede (2001) An overview back

to the budget in detail and the achievement of the

target budget requires a level of participation that is

higher to go on an exchange of information to carry

out control over the budget. So it can be said that the

higher the accountability, the higher the need for

participation. Their control is tight against the

budget required information that is sufficient so that

their tendency to conceal information. The

university has supervision from various parties so

that the structure will be more careful in preparing

the budget because of accountability.

2.4 Budgetary Participation

Individual participation in the preparation of the

budget is used to see how much opportunity is given

to choose the desired action. The most contributions

of activity budgeting are when a subordinate or

subordinates participate in the preparation of the

budget. Therefore, employees feel concerned with

the attainment of the target budget. According to

Atkinson et al. (2001), budgetary participation is

determination budgets are together to agree on a

target budget. Welsch et al. (2000) budgetary

participation has impacted positively, namely

reducing the asymmetry of information within the

organisation and increase the commitment of

individuals within the organisation to achieve the

target that is specified. Bianca et al. (2017) state that

the relationship between participation and

performance matrix forms the perspective of

individuals participating in budgeting to encourage

better employee performance. The relationship

between participation and budget performance

shows a good relationship (Stammerjohan and

Lopez, 2008). The results of previous studies were

varied. Some findings have had negative

participation results on budgetary slack, and some

have the opposite. The results which stated

positively related means participation caused a

decrease in budgetary slack. These findings are

stated in research (Fitri, 2004), (Van der Stede,

2001), (Dunk 1998), while those who argue

otherwise state participation provides a slack

opportunity. Young (1985) find that a subordinate

who participates will set a standard that is relatively

easy to achieve. Onsi (1973) budgetary participation

has a positive effect to budgetary slack, Young

(1985) has a negative effect, Dunk (1993) has a

negative effect, Daumoser (2018) has a positive

effect, and Kahar et al. (2016) budgetary

participation harm budgetary slack with job

satisfaction. Browell and Mcinnes (1986) found that

budgetary participation harms asymmetry

information, but Van der Stede (2001) found a

positive relationship between them. Previous study

History of the hypothesis of the research is seeing

the effect of budgetary participation impacting

positively on budgetary slack which means

increasingly higher levels of participation will lead

to a further reduction in budgetary slack.

2.5 Information Asymmetry

Asymmetry of information is a condition that there

is a party which gained the advantage on the cost of

the others because it has information that is better

than with the others (Scott, 2003). Asymmetry of

information in university higher among parties that

provide funding to the program of study that is

preparing the budget for implementing the program

is planned. Parties have information that is either not

need to take the opportunity to perform budgetary

slack because the life of the parties are sufficiently

provided information bias or hide most of the

information which they possess in pure, 2004. The

donor fund has a standard maximum of the costs

arising that can be proposed in the budget by a

percentage certain of the total cost of the program

(Lewis, 2006) as the maximum budget is used to pay

salaries not be more than 50% of the total budget.

Fitri (2004) found that information asymmetry did

not have a significant impact on budgetary slack.

Daumoser (2018) asymmetry information has a

positive effect on budgetary slack. Young (1985) has

no significant effect (2016), Dunk (1993) has a

positive effect, and Chong and Ferdiansah (2011)

result negative effect, tested with trust factor and

Chong (2016) asymmetry information has a negative

effect with leader’s reputation variable. Young

(1985) and Chow et al. (1988) found that asymmetry

information harms individual behaviour. In

Universities, each program of study is to know the

conditions are encountered. Setting a budget that is

stiffer than on enabling structural perform budgetary

slack.

ICVHE 2019 - The International Conference of Vocational Higher Education (ICVHE) “Empowering Human Capital Towards Sustainable

4.0 Industry”

528

2.6 Individual Behaviour and

Budgetary Slack

George and Jone (2002) state that behaviour is a

collection of feelings, beliefs and thoughts about

how to act about work and the organisation where he

works. Young (1985) find a subordinate who has

behavioural avoid the risk will increase the slack. In

universities, regulations regarding the budget are

more rigid and so individual behaviour encourages

individuals to achieve university goals. There is a

final sacrifice between budget and trust, and there is

a contrary sacrifice between budget and distrust.

Trust motivates managers to invest their efforts,

while distrust encourages middle managers to reduce

their efforts (Susana, 2016). Schciff and Lewin

(1970) and Brownell and Melnnes (1986) found that

individual behaviour has a positive effect on

budgetary participation. Chruch (2018) and Chong

(2016) their research result individual behaviour

harms budgetary slack.

3 METHODOLOGY

The research sample is structural in Higher

Education in Indonesia involved or participating in

the preparation of the budget such as deans, vice

deans, head of study programs and heads of

laboratories. This study uses a questionnaire survey

method using a four-point Likert scale. Of the 75

questionnaires sent, only 63 were returned.

Table 1: Demographics of the respondents

Descri

p

tions Res

p

ondent %

Gende

r

- Women 35 56%

- Men 27 43%

Statu

-PTN 39 62%

-PTS 24 38%

Structural Position

-Dean 9 14%

-Vice Dean 2 3%

-Head of study

Program / Head of lab

52 83%

Universitas Indonesia GU 16

Universitas Pad

j

ad

j

aran GU 3

Univesitas Ga

j

ah Mada GU 2

Unversitas Jembe

r

GU 1

Universitas Negeri Malang GU 3

Universitas Sumatera Utara GU 1

Universitas Negeri Makasa

r

GU 2

Universitas Ne

g

eri Medan GU 1

Universitas Airlangga GU 2

Universitas Halu Oleo GU 2

Politeknik Manado GU 1

Universitas Matara

m

GU 2

Universitas Ben

g

kulu GU 2

Universitas Negeri Jakarta GU 2

Politeknik UNS GU 1

Universitas Atmajaya PU 2

Universitas Mercu Buana PU 2

Universitas Perbanas PU 2

Universitas BSI PU 2

Universitas Pamulang PU 1

YKPN PU 1

Politeknik TEDC PU 2

Politeknik Hara

p

an Bersama PU 1

Politeknik LPP Yo

gy

aPU 3

Universitas Pakuan PU 2

Universitas Trisakti PU 2

STIESIA PU 2

3.1 Operationalisation of Variables

This study uses SEM with the LISREL8 application

program. Minimum data of five respondents for the

Maximum Likelihood or ten respondents for the

estimation of Weighted Least Square has been

fulfilled in this study. Latent variables (endogenous

and exogenous latent) are vital variables that are the

focus of this study which are abstract concepts that

can only be observed indirectly and imperfectly

through their influence on the observed variables

(Wijayanto, 2016). Endogenous latent variables are

variables that are bound to at least one equation in

the model even though in other equations are

independent variables. Endogenous variables in this

study are budgetary slack, budgetary participation,

information asymmetry and individual behaviour.

Exogenous latent variables are free variables in all

equations, namely demands accountability.

Indicators are variables that are observed and can be

measured empirically.

This study uses questions developed by Maria

(2007), the higher the score, the greater the

information asymmetry and accountability. Onsi

(1993) individual behaviour shows the higher the

score, the greater the pressure perceived by

individuals and influence behaviour. Eight questions

for Budgetary Participation, eight questions for

Accountability Demands, six questions for

information asymmetry, five questions for individual

behaviour and nine questions for budgetary slack.

The pretest is done for all observed variables and

all latent variables with Cronbach’s alpha value of

0.768 means that all questions in the questionnaire

Effect of Budgeting Factors on Budgetary Slack in Indonesia Universities

529

can be understood by respondents. Internal

consistency reliability test results to see the

correlation and consistency between items are

getting better because the coefficient is close to 1

(Sekaran, 2003).

4 ANALYSIS AND RESULTS

4.1 Confirmatory Test (Confirmatory

Analysis)

Testing using the Confirmatory Factor Analysis

(CFA) or also called the measurement model match

test is carried out to test the validity and reliability as

well as the contribution given to the observed

variables in measuring latent variables. The

measurement model match test is carried out on each

latent variable that is related to several observed

variables separately through an evaluation of the

validity and an evaluation of the reliability of the

measurement model. An evaluation of the validity of

the observed variables is carried out regarding the

standardised loading factor. Meanwhile, the

evaluation of the reliability of the measurement

model is done by referring to the value of the

Construct Reliability (CR) and Variance Error (VE)

of the measurement model. After evaluating the

validity and reliability of the measurement model,

indicators that have excellent reliability and validity

are obtained.

Table 2: Confirmatory Test Results.

Item

Loading Factor

≥ 0.50

AVE ≥

0.50

Construct

Reliability

≥ 0.70

BP1 0,69

0,425 0,772

BP2 0,71

BP3 0,05

BP4 0,94

BP5 0,79

BP7 0,24

IA1 0,87

0,638 0,912

IA2 0,85

IA3 0,87

IA4 0,81

IA5 0,53

IA6 0,81

IB1 0,78

0,270 0,512

IB2 0,31

IB4 0,61

IB5 0,05

BS1 0,76 0,178 0,493

Item

Loading Factor

≥ 0.50

AVE ≥

0.50

Construct

Reliability

≥ 0.70

BS3 0,10

BS4 0,49

BS6 0,27

BS7 0,23

BS9 0,34

AK1 0,86

0,306 0,766

AK2 0,36

AK3 0,60

AK4 0,45

AK5 0,60

AK6 0,37

AK7 0,54

AK8 0,48

Based on the results of the CFA test shows that

most of the indicators in the research sub-variables

are valid because they have a loading factor value ≥

0.7. Besides, three research variables have met the

standard values of both Construct Reliability (CR)

and Variance Extracted (VE) values, which are more

significant than 0.7 for CR and greater than 0.5 for

VE. Thus this shows that all items in the variable

have the same answer in measuring the latent /

construct variable so that it can be used for further

analysis.

4.2 Overall Model Fit

4.2.1 Absolute Measurement Model Match

The results of the Absolute Measurement Model

match size can be seen in the following table:

Table 3: Absolute Measurement Model Match Size

Results.

Measuremen

t (GOF)

Target of FIt Result

Level of

fit

Absolute Fit Measure

Statistic Chi

Square (X

2

)

P

Lower than

P ≤ 0,05

520,76

P=0,001

Poor fit

RMSEA

RMSEA ≤

0,08

0,067 Good fit

0,08 ≤

RMSEA <

0,10

RMSEA ≥

0,10

GFI 0,0 – 1,0 0,63

Marginal

f

i

t

AGFI ≥ 0,9 0,56

Marginal

f

i

t

ICVHE 2019 - The International Conference of Vocational Higher Education (ICVHE) “Empowering Human Capital Towards Sustainable

4.0 Industry”

530

CFI ≥ 0.95 0,92 Good fit

NFI ≥ 0,9 0,74

Marginal

f

i

t

NNFI ≥ 0,9 0,91 Good fit

IFI ≥ 0,9 0,92 Good fit

RFI 0,0 – 1,0 0,71

Marginal

f

i

t

Based on the results above, it appears that four

GOF sizes show an excellent fit match, 4 GOF sizes

that are marginal fit, and 1 GOF size that is a poor

fit. Therefore it can be concluded that the overall fit

of the model in this study is a good fit. Based on

these results, it can be concluded that the

measurement model generally meets the suitability

requirements, and it is decided to move forward in

the next step, namely the interpretation of the

estimated results.

Based on these results, it can be concluded that

the measurement model generally meets the

suitability requirements, and it is decided to move

forward in the next step, namely the interpretation of

the estimated results. The following figure shows the

path diagram of the estimation results of the model

based on the LISREL output.

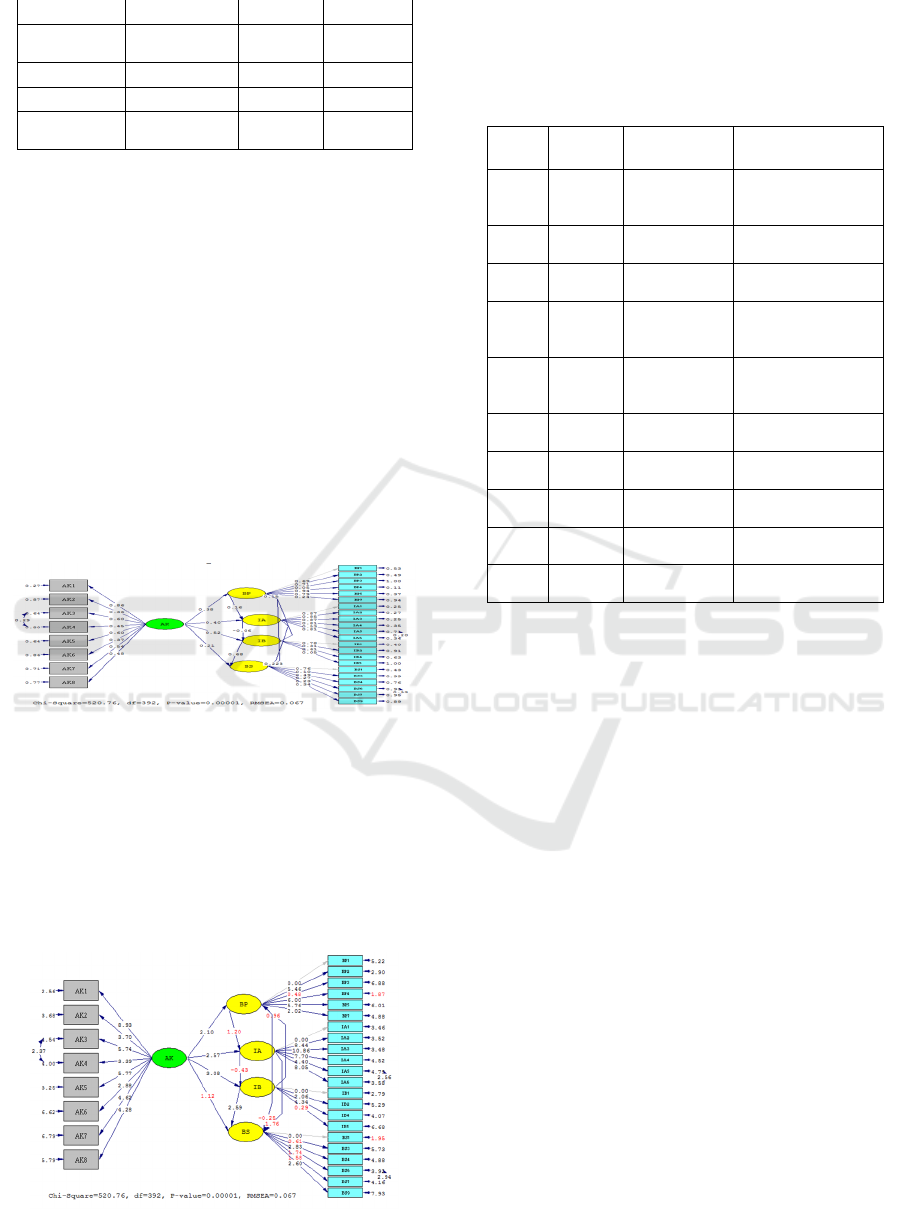

Figure 1: Standardised Solution Model SEM.

4.3 Structural Model Analysis

The structural model analysis is related to the

coefficients or parameters that show the effect of the

relationship between latent variables and other latent

variables. The following is a picture of the results of

basic model research.

Figure 2: T-Value Model SEM.

Based on the picture above, the results of the

structural model analysis are summarised in the

following table:

Table 4: Structural Model Analysis Results.

Path T-Value Cut off Value Conclusion

AK

→

BP

2,10 1,96 hypothesis accepted

AK

→ IA

2,57 1,96 hypothesis accepted

AK

→ IB

3,08 1,96 hypothesis accepted

AK

→

BS

1,12 1,96 hypothesis rejected

BP

→

BS

-0,25 1,96 hypothesis rejected

BP

→ IA

1,20 1,96 hypothesis rejected

IA →

BS

1,76 1,96 hypothesis rejected

IA →

IB

-0,43 1,96 hypothesis rejected

IB →

BS

2,59 1,96 hypothesis accepted

IB →

BP

0,96 1,96 hypothesis rejected

Accountability has a significant effect on

Budgetary Participation, Information Asymmetry

and Individual Behavior, but accountability has no

significant effect on Budgetary Slack. Universities

obtain funds from the public, have governance,

vision and mission that must be achieved and

obeyed by the entire academic community and

overseen by many parties, especially for state

universities. So this research shows that

accountability has an influence on participation in

budgeting which is the basis of all activities and

achievement of the university’s vision, mission,

goals and strategies. Accountability will give more

transparent information influence in the preparation

of the budget, and accountability does not affect the

behaviour of individuals in the preparation of the

budget.

This research found that Budgetary Participation

has no significant effect on Information Asymmetry.

Information Asymmetry has no significant effect on

Individual Behavior. Individual behaviour has no

significant effect on Budgetary Participation.

Budgetary Participation and Information asymmetry

have no significant effect on Budgetary Slack, but

Individual behaviour has a significant effect on

Budgetary Slack in Universities.

Effect of Budgeting Factors on Budgetary Slack in Indonesia Universities

531

5 CONCLUSIONS

This research found that accountability has a

significant effect on Budgetary Participation,

Information Asymmetry and Individual Behavior,

but no significant effect on Budgetary Slack.

Budgetary participation has no significant effect on

Information Asymmetry. Information Asymmetry

has no significant effect on Individual Behavior.

Individual behaviour has no significant effect on

Budgetary Participation. Budgetary Participation and

Information asymmetry have no significant effect on

Budgetary Slack, but Individual behaviour has a

significant effect on Budgetary Slack in preparing to

budget in universities in Indonesia.

The researcher did not separate the type of

Universities and the structural level that filled out

the questionnaire and the number of respondents in

each university which was not balanced between

government university and Private University. The

sample does not represent the number of

Universities in Indonesia, causing the SEM model to

become less fit. Marginal results may be due to

errors in measurement because many questions are

ultimately not used.

Future studies can examine the measurement

variables in order to get better measurements.

Increase the number of respondents representing all

universities in Indonesia so that the research results

are improved.

Separating types of Universities, namely

Government Universities (BHMN, BLU and Satker)

and Private Universities as well as structural that fill

out the Dean’s questionnaire, deputy dean, head of

the study program and head of the laboratory and

separate the size of Universities because in

determining the budget each university has a

different policy.

This paper contributes to existing research

on budgetary slack in extent on previous work by

identified the factors affecting the budgetary slack.

The most factor affects the budgetary slack is

participation among individual who gives

information to budgeting and asymmetry

information. The findings of this study suggest that

universities should give target that the department or

division to achieved.

REFERENCES

Bianca A., Groen. A., Wouters, M.J.F., Wilderom, C.P.M.

2016. “Employee participation, performance metrics,

and job performance : A survey study based on self-

determination theor. Management Accounting

Research, 36, 51-66.

Chow, Chww W., Cooper, J.C., and Waller, W.S. 1998.

“Participative Budgeting: Effects of the Truth-

Inducing Pay Scheme and Information Asymmetry on

Slack and performance”, The Accounting Review,

Vol.63, No.1 (January), 111-122.

Chong, V. K., & Ferdiansah, I. 2011. The effect of trust-

in-superior and truthfulness on bud- getary slack: An

experimental investigation. Advances in Management

Accounting, 19, 55-73.

Chong, V.K and Loy, Chanel Y. 2015. The effect of a

Leader’s Reputation on budgetary slack. Advances in

Management Accounting. Volume 23, 49-102.

Der Fa Chen, Chun Hsu Lu, Alvin Chang, Hsieh His Liu,

Kuo Chih Cheng. 2016. The Relationships Among

Budgetary Slack, Customers’ Relationship Quality and

Organisational Performance. 5th IIAI International

Congress on Advanced Applied Informatics

Dunk, Alan S. 1993. “The effect of Budget Emphasis and

Information Asymmetry on the Relation between

Budgetary Participation and slack”, The Accounting

Review, Vol.68, Ni.2 (april), 400-410.

Duck, AS and Perera, H. 1997. “The Incidence of

Budgetary Slack: A Field Study Exploration”,

Accounting, Auditing and Accountability Journal, 10

(mei), 649-664.

Dunk, Alan S. and Hossein Nouri. 1998. “Antecedents of

Budgetary Slack: A Literature Review and Synthesis”,

Journal of Accounting Literature, 17, 72-96.

Daumoser, C., Hirsch, B, Sohn, M. 2018. Honesty in

budgeting : a review of morality and control aspects in

the budgetary slack literature. Journal Management

Conttol. Germany. https://doi..org/10./1007/s00187-

018-0267

Ebdon, C., Jiang, Y., Franklin A.L. 2016. Elected

Officials’ Perceptions of Governance Relationships

and Budget Participation Mechanisms. Journal of

Public Budgeting, Accounting & Finance

Management, 28 (1), 103-124.

Fitri, Y. 2004. “Pengaruh Informasi asimetri, partisipasi

penganggaran dan komitment organisasi terhadap

timbulnya kesenjfangan anggaran : Studi empiris pada

universitas swasta di Kota Bandung » Seminar

Nasional Akuntansi, 581-597

George, J.M., & Jone, G.R.J. 2002. “Organisational

Behaviour”, Prentice Hall, International Edition, 3

rd

Edition.

Hansen, S.C.,.Otley, DT, and Van der Stede, W.A 2003.

“Practice Developments in Budgeting in Public

Accounting, An Overview and Research Perspective“,

Journal of Management Accounting Research.

Hossein Nouri and Larissa Kyj. 2015. “An Experimental

Examination Of The Combined Effects Of Normative

And Instrumental Commitments On Budgetary Slack

Creation: Comparing Individuals Versus Group

Members“. Advances in Management Accounting,

Volume 22, 225–260

Baerdemaeker, J.D, Bruggeman, W. 2015. “The impact of

participation in strategic planning on

ICVHE 2019 - The International Conference of Vocational Higher Education (ICVHE) “Empowering Human Capital Towards Sustainable

4.0 Industry”

532

managers’creation of budgetary slack : the mediating

role of autonomous motivation and effective

organisational commitment“. Volume 29. Page 1-12

Lewis, D. 2006. “Understanding the Budget’, Women’s

Issues Networkof Belize (April, 2016)

Kahar, S. H.A., Rohman, A, Chariri, A. 2016.

Participative budgeting, budgetary slack and Job

satisfaction in The Public Sector. The Journal of

Applied Business Research. Vol 31 Number 6, 1663-

1674

Kilby, P. 2004. “Accountability for Empowerment:

Dillemas Facing Non-Govermental Organization”.

Working Paper of The Asia Pacific School of

Economics and Government, The Australian National

University, Januari, 1-23.

Mango. 2006. “Money-Budgeting, Accounting and Fund-

Raising“. 1-21

Merchant, K. A. 1985. “Budgeting and The Propensity to

create budgetary slack”, Accounting, Organisation and

Society, 10, 201-2010.

Onsi, M. 1973. “Factor Analysis of Behavioural Variable

Affecting Budgetary Slack”, The Accounting Review,

Vo.48, No.3 (July), 535-548.

Otley, D. & Fakiolas,A. 2000. “Reliance on Accounting

Performance Measures: Dead End or New

Beginning?’, Accounting, organisation and society,

25, 497-510.

Schriff, M. & AY. Lewin. 1968. “Where Traditional

Budgeting Fails”, Financial Executive (Mei), 50-62.

Scott, W. R. (2003). Financial Accounting Theory”, Edisi

Kedua, Prentice Hall Canada Inc., Scarborough,

Ontario.

Sekaran, U. 2003. “Research Methods for Business: A

Skill Building Approach”, Edisi Keempat, John Wiley

and Sons, Inc., USA

Susana, G.R. 2016. Effects of trust and distrust on effort

and budgetary slack : an experiment. Mnagement

Decisiopn. Volume 54, Issue 8

Chong, V.K. & Loy, C.Y. 2015. “The Effect Of A

Leader’s Reputation On Budgetary Slack“. Advances

in Management Accounting, Volume 25, 49102

Van der Stede,W.A. 2001. Measuring “tight budgetary

control’. Management Accounting Research. Vol 12,

119-137.

Wijayanto, S.H. 2006. “Struktur Equation Modeling

dengan LISREL”, FEUI Pascasarjana Ilmu

Manajemen, Agustus.

Stammerjohan, W.W., López, MAL Auburn University

Montgomery, Claire Allison Stammerjohan. 2008.

“The Effects of Power Distance on the Budgetary

Participation/Performance Relationship“.

Young, S.M. 1985. “Participative Budgeting: The Effect

of Risk Aversion and Asymmetric Information on

Budgetary Slack”, Journal of Accounting Research,

23, 829-842.

Zahirul Hoque and Peter Brosnan. 2015. “Industrial

Relations, Budgetary Participation And Budget Use:

An Empirical Study“. Advances in Management

Accounting, Volume 21, 119–147

Effect of Budgeting Factors on Budgetary Slack in Indonesia Universities

533