Effect of Audit Knowledge, Work Experience, and Gender on Audit

Quality in Jakarta City

Yosevin Karnawati

1

, Ahmad Sururi Afif

1

, Sri Handayani

1

and Jusuf

1

1

Faculty of Economics and Business, Esa Unggul University, Jakarta, Indonesia

Keyword: Audit knowledge, work experience, gender, audit quality

Abstract: Auditor quality is an important thing in maintaining the reliability of financial statements. This study aims

to analyze the factors that affect the quality of audits on Public Accountants and to determine the most

dominant factors affect audit quality. The subject of this research is auditors who work in anaccountant

public company in Jakarta Barat. This study uses data from questionnaires. Data collection using purposive

sampling where there are certain criteria in sampling research. The analysis tool used is multiple regression

analysis with consists of F test and t-test. The result of this research concludes that the variable of audit

knowledge affects audit quality while work experience and gender do not affect audit quality. A person with

more experience in a substantive field has more things stored in his memory and can develop a good

understanding of events. If the auditor understands well the profession, then the auditor will be free to

perform audit tasks properly.

1 INTRODUCTION

Today the company needs the preparation of good

financial statements. However, in order to have a

good financial report, an auditing section is required

because a good financial report must meet auditing

standards established by the Indonesian Institute of

Accountants (IAI). Auditing for the company is

quite important because it gives a big influence on

the activities of the company concerned. At the

beginning of its development, auditing is only

intended to find and find fraud and mistakes, then

developed into the examination of financial

statements to provide opinions on the correctness of

the presentation of corporate financial statements

and also become one of the factors in decision

making.

As the company grows, the audit function

becomes increasingly important, and the need arises

from governments, shareholders, financial analysts,

bankers, investors and the public to assess the

quality of management's operating results and

achievements of managers. To address these needs,

management audits arise as a reliable means of

assisting the implementation of their responsibilities

by providing analysis, assessment, recommendation

on activities that have been undertaken. To produce

a good financial report, the quality of the audit

should be considered. Audit quality is defined as the

probability that an auditor finds and reports about a

violation in its client's accounting system. The

probability of finding an offence depends on the

auditor's ability and level of auditor independence.

In Indonesia, in November 2013 the Directorate

for Economic and Special Crimes of the Police

Bareskim summoned five auditors of customs and

duties related to the bribery case of the Head of

Customs and Excise Sub Directorate, Heru

Sulastyono.In a similar case, Finance Minister Sri

Mulyani suspended permits 2 public accountants

Rutlan Effendi and AP Muhamad Zen and 1 public

accounting firm Atang Djaelani for violating

Auditing Standards - Accounting Standards of

Public Accountants (SPAP) during an audit at PT.

Bumi Resources Minerals Tbk (BRMS).

Audit quality can be achieved if the auditor has

good competence. Competence consists of two

dimensions of experience and knowledge. Auditors

as the spearhead of the implementation of audit tasks

should always improve the knowledge that has been

owned for the application of knowledge can be

maximized in practice. Application of maximum

knowledge will certainly be in line with the

increasing experience owned.

The public accountant has the responsibility to

determine each competency or to assess whether the

Karnawati, Y., Sururi Afif, A., Handayani, S. and Jusuf, .

Effect of Audit Knowledge, Work Experience, and Gender on Audit Quality in Jakarta City.

DOI: 10.5220/0009951905190524

In Proceedings of the 1st International Conference on Recent Innovations (ICRI 2018), pages 519-524

ISBN: 978-989-758-458-9

Copyright

c

2020 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

519

education, experience and considerations required

are adequate for the responsibilities it must fulfil.

Competence indicates the achievement and

maintenance of a level of understanding and

knowledge that allows a member to provide services

with ease and ingenuity, in the case of professional

assignment exceeding the competence of a member

or company, a member shall consult or deliver the

client to a more competent competitor. Competence

consists of two dimensions of experience and

knowledge. Auditors as the spearhead of the

implementation of audit tasks should always

improve the knowledge that has been owned for the

application of knowledge can be maximized in

practice. Application of maximum knowledge will

certainly be in line with the increasing experience

owned.

The level of knowledge that the auditor has is

very important that can affect the auditor in making

decisions. With a high level of knowledge owned by

an auditor, the auditor will not only be able to

complete an audit job effectively but will also have a

broader view of things. Auditors with a high level of

knowledge can detect an error. Experience also

gives impact to every decision taken in the

implementation of the audit so that expected every

decision taken is the right decision. It indicates that

the longer the work of the auditor will be the better

the quality of audit generated. Previous studies

related to audit quality include Harvita and Pamudji

(2012) research, on independence giving results that

independence has no significant effect on audit

quality, while from Alim et al. (2007) research that

independent, Gender and biological sex are

fundamentally differentiated. Gender is divided into

two that is male and female which is absolute at

human being when born. Gender as an illustration of

the nature, attitudes and behavior of men and

women. A personality and behavior differentiated

between masculine and feminine types. Feminine

has characteristics such as warm in interpersonal

relationships, affiliation, compromise, sensitivity,

taste, pleasure in group life while masculine has less

characteristic to express warmth, less responsive,

risk-taking.

The purpose of research conducted in this

research is as follows: 1) To analyze whether Audit

Knowledge, Work Experience, and Gender jointly

affect the Audit Quality Improvement; 2) To analyze

whether Audit Knowledge has an effect on

Improving Audit Quality; 3) To analyze whether

Work Experience has an effect on Improving Audit

Quality; 4) To analyze whether Gender affects

Quality Audit Improvement.

2 LITERATURE REVIEW

2.1 Audit

The audit is an activity to collect and evaluate

evidence from information to determine and report

the level of suitability between information and

predetermined criteria (Staciokas and Rupsys, 2005;

Skaerbaek, 2009; Popović et al., 2015). The audit

process must be carried out by competent and

independent people

2.2 Quality Audit

It is a probability that an auditor finds and reports

about infringement in the client's accounting system.

The results of his research indicate that large KAPs

will seek to present greater audit quality than small

KAPs.

2.3 Audit Knowledge

Audit knowledge is defined by the level of the

auditor's understanding of a job, conceptually or

theoretically (Sari and Mardisar, 2007; Yanti et al.,

2018). Differences in knowledge among auditors will

affect the way auditors complete a job. Further

explained that an auditor would be able to complete a

job effectively if supported by the knowledge it has.

2.4 Work Experience

The more experience, the auditor can generate more

assumptions in explaining the audit findings. A

person with more experience in a substantive field

has more things stored in his memory and can

develop a good understanding of events. Meaningful

work is a fundamental aspect of workplace

spirituality that consists of having the ability to feel

the deepest meaning and purpose of one's work. This

dimension represents how workers interact with

their work day by day on an individual level.

2.5 Gender

Gender and biological sex are fundamentally

differentiated. We are born as women or men who

are the absolute gift, then the biological interpretation

by culture gives way that makes us masculine or

feminine. Gender is thought of as a costume and

mask in a theatre that describes to others about

ourselves feminine or masculine. It forms the gender

roles that include appearance, dress, attitude,

personality, work inside or outside the home,

sexuality, family responsibilities and so on.

ICRI 2018 - International Conference Recent Innovation

520

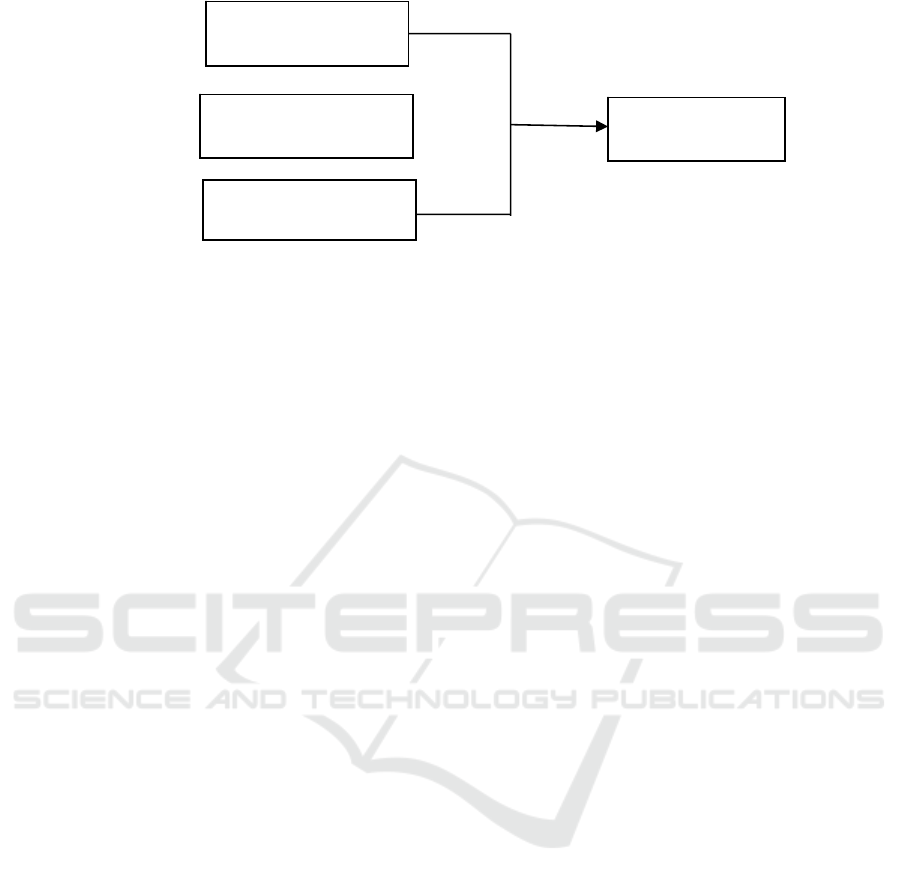

Figure 1: Research Model

Based on Figure 1 and the existing theoretical basis,

the hypothesis proposed to be tested is as follows:

Ha1: There is a positive and significant influence

between audit knowledge, work experience, gender

with audit quality.

Ha2: There is a positive and significant influence

between audit knowledge and audit quality.

Ha3: There is significant influence between work

experience and audit quality.

Ha4: There is significant influence between gender

and audit quality.

3 RESEARCH METHOD

The population in this study is a senior auditor who

works in a public accounting firm in West Jakarta.

The population was taken as many as 19 offices,

with a total population of 95 senior auditors.

Determination of this sample is done by purposive

sampling, the population to be sampled this study is

to meet the criteria of a particular sample by the

desired researcher, and then selected based on

certain considerations tailored to the purpose of

research. The criteria for the sample are senior

auditors who work in West Jakarta Public

Accounting Firm. Selected sample of 19 public

accounting firms and by using Slovin formula

(Tejada and Punzalan, 2012; Khalifa and Alswailem,

2015), the total sample size used in this study was 77

auditors.

While the operational definition of variables is

following:

a. Independent Variables

In this study, the independent variables are:

1) Audit Knowledge (X1)

Audit knowledge is the level of the auditor's

understanding of a job on a conceptual or

theoretical basis.

2) Work Experience (X2)

Experience is a skill and knowledge acquired

by someone after doing something.

Experience variables will be measured using

the length of working indicators, the

frequency of inspection work, and more.

3) Gender (X3)

Gender is one of the non-technical factors

that affect the quality of the audit. According

to Mikkola (2005) Gender is defined as a

description of the nature, attitudes and

behavior of men and women. A personality

and behavior differentiated between

masculine and feminine types. Feminine has

characteristics such as warm in interpersonal

relationships, affiliation, compromise,

sensitivity, taste, pleasure in group life while

masculine has less characteristic to express

warmth, less responsive, risk-taking.

b. Dependent Variable (Y)

Audit quality is the attitude of the auditor in

performing its duties as reflected in the results of its

reliable examination by applicable standards. In the

operationalization of variables, researchers identify

dimensions and indicators of each variable

measured.

The multiple regression equations for testing

this hypothesis are:

Y = β

0

+ β

1

X

1

+ β

2

X

2

+ β

3

X

3

+ ε (1)

β0 = constants

β1-3 = regression coefficient

X1 = audit knowledge

X2 = work experience

X3 = gender

ε = error

To analyze the above model using a multiple

linear regression technique. Furthermore, in testing

the hypothesis will be used F test and T-test,

Audit Knowledge

Gender

WorkExperience

Audit Quality

Effect of Audit Knowledge, Work Experience, and Gender on Audit Quality in Jakarta City

521

whether an independent variable (audit knowledge,

work experience and gender) simultaneously or

partially have a positive influence in becoming a

predictor of the dependent variable (audit quality).

Multiple linear regression analysis is used to

measure the influence between the independent

variable and the dependent variable. Basic decision

making:

a. if P-Value (sig) <α (5%), then Ha is accepted

b. if P-Value (sig)> α (5%), then Ha is rejected

4 RESULTS AND DISCUSSION

4.1 Descriptive Statistics Variable

From the results of descriptive statistical tests known

that audit knowledge has the lowest value of 1.22;

the highest value of 5.00; the average value of

3.9617 means that when viewed from the average of

the highest and lowest score of 31.1% and compared

with the resulting average of 39.6% it can be

concluded that many auditors in KAP West Jakarta

have extensive audit knowledge. This is because the

auditor handles many cases in audit firms.

Work experience has the lowest score of 1.00;

the highest value of 5.00; the average score of

4.0024 means that when viewed from the highest

and lowest average of 30% and compared with the

generated average of 40% it can be concluded that

auditors in KAP West Jakarta have many audit

experience. This is due to high auditor flight hours.

The gender that has the lowest value of 0.00; the

highest value of 1.00; an average score of 0.5862.

The number 1 shows the number of the feminine as

many as 34 respondents with the percentage of

58.6% and number 0 indicates the masculine number

of 24 respondents with the percentage of 41.4%.

Then it can be concluded that auditors are more

likely to have femininity properties. This is because

when auditors conduct an audit, they also consider

personal assumptions in making decisions.

Audit quality that has the lowest value of 1.21;

the highest value of 5.00; the average value of

3.9353 means that when viewed from the average of

the highest and lowest value of 31.05% and

compared with the resulting average of 39.35% it

can be concluded that the auditor auditing quality in

West Jakarta KAP good. This is because the quality

of audits achieved have the good competence and

can compete with the KAP outside West Jakarta.

4.2 Test Data Normality

From the normality test by One-Sample

Kolmogorov-Smirnov test, showed the significance

level of several variables greater than 0.05, can be

seen from the sig value of 0.492. If sig value> 0,05

then data is said normal. Thus, based on the results

of testing the normality of data proved that the data

in this study is normally distributed.

4.3 Multicollinearity Test

From the calculation results obtained that on the

collinearity statistics, the Variance Inflation Factor

(VIF) on the independent variable audit knowledge

2.689 <10, work experience 2.627 <10, and gender

1.045 <10. Can be concluded all the independent

variables in this study there are no symptoms of

multicollinearity.

4.4 Heteroscedasticity Test

In the scatterplot image, it is seen that it cannot be a

particular pattern in the image. The point on the

image also spread randomly (random) either above

or below the number 0 on the Y-axis. So it can be

concluded that there is no heteroscedasticity on this

regression model.

4.5 Autocorrelation Test

The Durbin-Watson test results show a value of

2.005, α = 0.05 n = 58, k = 3, yielded du = 1.6860,

with the criteria du <dw <4 - du, ie 1.6860 <2.005

<2.314. From the results of this test can be said that

this regression model is free from autocorrelation.

4.6 Test of Validity and Reliability of

Research Instruments

While the reliability test used Cronbach alpha

(Santos, 1999; Tavakol and Dennick, 2011). Test

results validity of each item in the questionnaire

declared valid with a value above 0.3 and reliable

with the value of Cronbach alpha above 0.7.

4.7 Hypothesis Testing

Audit knowledge has a regression coefficient of

0.668 states each increase of audit knowledge of 1

value hence, audit quality increased by 0.668 but a

significant level of audit of 0, this indicates that the

coefficient of audit knowledge variable has a

positive effect on audit quality with a significant

ICRI 2018 - International Conference Recent Innovation

522

level of 0.000. This means that the more knowledge

owned by auditors, the higher the quality audit.

Work experience has a regression coefficient of

0.11 denotes each increase in work experience of 1

value hence, audit quality increases by 0.11 but a

significant level of work experience of 0.147;

thisindicates that the variable of the work experience

does not affect the quality of the audit because the

significant level of0.147 is far from the significant

level of 0.05.

Gender has a regression coefficient of 0.101

stating each gender increase of 1 value hence, audit

quality increased by 0.101 but gender significant

level of 0.205; this indicates that the gender variable

does not affect audit quality because the significant

level of 0.205 is far from the significant level of

0.05.

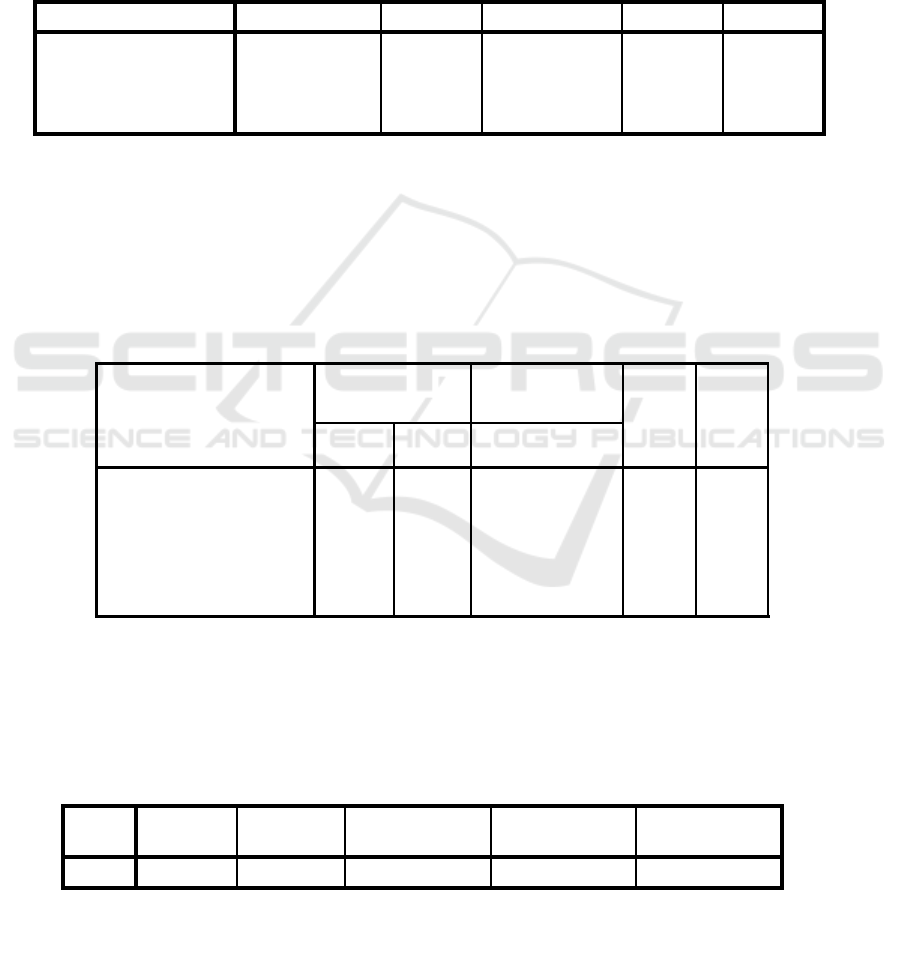

Table 1. F-test (ANOVA)

Model Sum of Squares Df Mean Square F Sig.

1 Regression 13.364 3 4.455 69.774 .000

a

Residual 3.384 53 .064

Total 16.748 56

a. Predictors: (Constant), work experience, gender, audit knowledge

b. Dependent Variable: auditquality

Based on the F test result as shown in Table 1, F-

test value 69,774 and obtained probability (level of

significance) 0.000. Therefore, the probability is

0.000 <0.05. So, from the results obtained can be

said that Ho is rejected and Ha accepted. So that it

can be interpreted audit knowledge, work experience

and gender together affect the quality of the audit.

Table 2. Multiple Linier Regression (Coefficients

a

)

Model

Unstandardized

Coefficients

Standardized

Coefficients

T Sig. B

Std.

Error Beta

1

(Constant) -0.004 0.033

-0.127 0.899

Audit _knowledge 0.668 0.085 0.798 7.881 0.000

work_experience 0.101 0.078 0.128 1.284 0.205

Gender 0.11 0.075 0.093 1.472 0.147

a. Dependent Variable: audit quality

Based on Table 2, the result of T, it is known that

the value of audit knowledge significance of 7.881>

1.673 then Ho is rejected and Ha accepted.

Significance value for work experience is 1.284

<1.673 then Ho accepted and Ha rejected and

significance value for gender equal to 1,472 <1.673

then Ho accepted and Ha rejected.

Table 3. Coefficient Determination

Model R R Square Adjusted R Square

Std. Error of the

Estimate Durbin-Watson

1 .187

a

.035 .017 .54705 2.005

a. Predictors: (Constant), audit knowledge, work experience, gender

b. Dependent Variable: audit quality

Effect of Audit Knowledge, Work Experience, and Gender on Audit Quality in Jakarta City

523

Based on the results of data processing in Table

3, the value of the adjusted coefficient of

determination (Adjusted R Square) is equal to 0.017.

This means that 1.7% of the dependent variable of

audit quality is explained by the independent variable

consisting of audit knowledge, work experience and

gender. The rest of 98.3% is explained by other

variables outside the variables used.

5 CONCLUSIONS

From the research that has been done, obtained the

result that audit knowledge has a significant

influence on audit quality. Influence of 0.000 which

means that the knowledge possessed by an auditor

affect the quality audit, while the work experience

does not have a significant effect on audit quality.

Influence caused by 0.205> 0.05, so the experience

of an auditor does not affect the audit quality

generated by the auditor.

Gender variables do not have a significant effect

on audit quality, the effect of 0.147> 0.05; masculine

characters are basically more rational, use more logic

while feminine characters are more emotionally

oriented, this can be linked to gender with audit art

and science gives the meaning that audit as a craft

(art) and as a science. So the gender character of an

auditor does not affect the audit quality generated by

the auditor.

From the result of the research simultaneously it

is known that audit quality at auditor at Public

Accountant Office in Jakarta can be determined by

audit knowledge factor, work experience and gender

in determination coefficient R2 is 1.7% and the rest

98.3% is determined by other factors outside

research model this.

The results can be understood that to improve the

quality of the auditors. If the auditor understands

well the profession, then the auditor will be free to

perform the audit tasks properly.

The subject of the study is an only limited auditor

who works in the public accountant firm of Jakarta

Barat, so for further research is expected in doing

further research to expand the sample area and in

subsequent research is also expected to add other

variables that allegedly affect the quality audit

REFERENCES

Alim, M. N., Hapsari, T., and Purwanti, L. (2007).

Pengaruh kompetensi dan

independensiterhadapkualitas audit denganetika

auditor sebagaivariabelmoderasi. Simposium Nasional

Akuntansi X, 26-28.

Harvita, Y.A., Pamudji, S. (2012). Pengaruh Pengalaman

Kerja, Independensi, Obyektifitas, Integritas, dan

Kompetensi Terhadap Kualitas Hasil

Audit.Diponogoro Journal of Accounting, 1(2): 1-10.

Khalifa, M., and Alswailem, O. (2015). Hospital

information systems (HIS) acceptance and satisfaction:

a case study of a tertiary care hospital. Procedia

Computer Science, 63: 198-204.

Mikkola, A. (2005). Role of Gender Equality in

Development-A Literature Review. University of

Helsinki, RUESG and HECER. Available at:

https://helda.helsinki.fi/bitstream/handle/10138/16660/

roleofge.pdf?sequence=1&origin=publication_detail

Popović, S., Tošković, J., Majstorović, A., Brkanlić, S.,

and Katić, A. (2015). The Importance of Continuous

Audit of Financial Statements of the Company of

Countries Joining the EU. Annals of' Constantin

Brancusi'University of Targu-Jiu. Economy Series.

Santos, J. R. A. (1999). Cronbach’s alpha: A tool for

assessing the reliability of scales. Journal of extension,

37(2): 1-5.

Sari, R. N., and Mardisar, D. (2007). The Effect of Task

Complexity on Quality of Auditor’s work: The Impact

of Accountability and Knowledge. Jurnal Bisnis dan

Akuntansi, 9(3): 223-236.

Skaerbaek, P. (2009). Public sector auditor identities in

making efficiency auditable: The National Audit

Office of Denmark as independent auditor and

modernizer. Accounting, Organizations and Society,

34(8):971-987.

Staciokas, R., and Rupsys, R. (2005). Internal audit and its

role in organizational government. Management of

Organizations: Systematic Research, 33: 169-180.

Tavakol, M., and Dennick, R. (2011). Making sense of

Cronbach's alpha. International journal of medical

education, 2: 53.

Tejada, J. J., and Punzalan, J. R. B. (2012). On the misuse

of Slovin’s formula. The Philippine Statistician, 61(1):

129-136.

Yanti, L., Abdullah, S., and Djalil, M. A. (2018). Influence

of Competence, Professional Skeptism and Audit

Knowledge on Financial Decrease Detection (Study on

Inspectorate Aceh). BRAND. Broad Research in

Accounting, Negotiation, and Distribution, 9(2): 13-21.

ICRI 2018 - International Conference Recent Innovation

524