Analysis of the Factors That Affect the Acceptance of Accounting

Information Systems in Business Firms in Jakarta

Darmansyah

1

, Yosevin Karnawati

1

, Retna Suliati

1

and Royhisar Martahan S

1

1

Faculty of Economics and Business, Department of Accounting, Universitas Esa Unggul, Jakarta, Indonesia

Keywords: Performance Expectancy, Effort Expectancy, Social Influence, Facilitating Conditions, Acceptance of

Accounting Information System.

Abstract: The company needs an accounting information system in order to provide information to users of financial

statements. Accountants within the company must quickly adapt to changes in information systems and

technologies applied to the company. This study aims to determine the factors that affect the acceptance of

accounting information systems in management accountants who work in business enterprises. The

population of this study is a management accountant working in West Jakarta. While the unit of analysis is a

management accountant, who works on the business company and uses accounting information technology

in its financial reporting process. Data retrieval is done by distributing questionnaires on respondents who

meet the criteria as a management accountant who uses accounting information systems in his work. The

research design used is explanatoris causal. processing. The analytical tool used is multiple regression

analysis. The results show that the accountant uses the importance of accounting information systems to

support many works. Performance expectancy has a significant positive effect on the acceptance of

accounting information system. With high performance expectancy, accountants have been able to

experience Effort expectancy has a significant negative effect on the acceptance of the accounting

information system. Effort Expectancy has a significant negative effect on the acceptance of the accounting

information system.

1 INTRODUCTION

The development of information technology has a

significant impact on the accounting information

system (AIS) within a company. The real perceived

impact of the existence of an AIS is the processing

of data that changes from the manual system to the

computer system and the emergence of software for

accounting that can facilitate the making of

financial statements. The software includes Oracle,

Microsoft SQL server, Deceasay, Peachtree, Zahir

and Myob. The advances in information technology

affect the development of accounting information

systems (SIAs) in terms of data processing, internal

control, increasing the number and quality of

information in financial reporting.

The user of a system is a human (man) who

psychologically has a certainbehavior attached to

him so that the aspects of behavior in the human

context as the user (brainware) of IT becomes

important as a decisive factor on everyone who runs

IT. Research on interest in behaving in the use of

technology is done using the Technology

Acceptance Model (TAM). TAM is based on the

Theory of Reasoned Action (TRA) which was

proposed by Ajzen et al. (1980). TRA states that a

person will receive a computer if the computer

provides benefits to the wearer. TAM is specifically

used in the field of information systems to predict

acceptance and use in individual user jobs

(Jogiyanto: 2007). This model places the attitude

factor of each user behavior with four variables:

perceived ease of use, perceived usefulness, attitude

towards using, and behavioral tendency to keep

using (behavioral intention to use). These four

variables have high determinants and validity that

have been tested empirically to predict the picture

on the behavioral aspects of information technology

users (Chau: 1996).

The acceptance of information technology can

be defined as the use of workers' technology, as

their way of life. A study in the field of information

systems to assess the acceptance of its users in

ways: the frequency or computer system used, the

506

Darmansyah, ., Karnawati, Y., Suliati, R. and Martahan S., R.

Analysis of the Factors That Affect the Acceptance of Accounting Information Systems in Business Firms in Jakarta.

DOI: 10.5220/0009951505060511

In Proceedings of the 1st International Conference on Recent Innovations (ICRI 2018), pages 506-511

ISBN: 978-989-758-458-9

Copyright

c

2020 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

duration of use and the number of uses of different

computer applications (Schillewaert et al., 2000).

The TAM model developed from psychological

theory explains the behavior of computer users,

which is based on belief, attitude, intention and user

behavior relationship (Fahmi: 2004). The user's

attitude towards the computer can also be

demonstrated by the user's optimistic attitude that

the computer is very helpful and useful to overcome

problems or work (Nur Indriantoro: 2000).

UTAUT (Unified Theory of Acceptance and

Use of Technology) is a model to explain user

behavior towards information technology. This

model is a combination of eight models that have

been successfully developed before. The UTAUT

model shows that the intention to behave

(behavioral intention) and behavior to use a

technology (use behavior) is influenced by

performance expectancy, effort expectancy, social

influence and facilitating conditions.

This study will analyze the behavior of system

users by using the UTAUT model framework that

examines the determinants of user acceptance and

user behavior, namely performance expectancy,

effort expectancy, social influence and facilitating

conditions. Furthermore, Chin and Todd (1995)

convey that the usefulness of information

technology will make the work easier, useful,

increase productivity, enhance effectiveness, and

improve performance and job performance.

Nasir (2013) stated that performance expectancy is

defined as the degree to which a person believes

that using a system will help him achieve a

performance advantage in his work. Effort

expectancy is defined as the level of ease associated

with system usage. Social influence is defined as

the degree to which a person perceives that the

person, he deems important, believes that he should

use the new system. Facilitating conditions are

defined as the extent to which a person believes that

the existing organizational and technical

infrastructure supports the use of the system.

Research Objectives to be achieved are as follows

1) analyze the determinants of Accounting

Information System Acceptance and performance of

individuals in the Business Company.

2 LITERATURE REVIEW AND

HYPOTHESES

DEVELOPMENT

2.1 Accounting Information System

According to Bordnar and Hopewood (2001), the

notion of an accounting information system is, "A

collection of resources, such as human and

equipment, which is set to transform data into

accounting information." This information is

communicated to its users for various decision-

making. Accounting Information System is a

functional information system that underlies other

functional information systems. This shows that a

company that will build a management information

system, it is advisable to build an accounting

information system first. Important functions formed

by SIA in an organization include collecting and

storing data about activities and transactions.

2.2 Unified Theory of Acceptance and

Use of Technology (UTAUT)

The Unified Theory of Acceptance and Use of

Technology (UTAUT) model is a theory developed

by Venkatesh et al. (2003) combines the successful

features of eight leading technology acceptance

theories into one theory. The constructs underlying

the Unified Theory of Acceptance and Use of

Technology are as follows:

a. Performance Expectancy

Venkatesh et al.(2003) define Performance

Expectancy as the level at which a person

believes by using the system will help the person

to gain performance on the job. The variables

are: 1) perceived usefulness, 2) extrinsic

motivation, 3) job fit, 4) relative advantage, 5)

outcome expectations.

b. Effort Expectancy

Effort expectancy is a level of ease of use system

that will be able to reduce the effort (energy and

time) of individuals in doing their work. The

variables are formulated based on 3 constructs on

the previous model or theory of Perceived Easy

Of Use (PEOU) of the TAM model, the

complexity of the model of PC utilization

(MPCU), and the ease of use of the diffusion

theory of innovation (Venkatesh et al., 2003).

c. Social Influence

Social influence is defined as the degree to which

an individual assumes that the other person

assures him that he or she should use the new

Analysis of the Factors That Affect the Acceptance of Accounting Information Systems in Business Firms in Jakarta

507

system. Herbert Kelman (1958) identifies three

broad varieties of social factors, which include 1)

Compliance, 2) Identification and 3)

Internalization. In this concept, there is a

combination of variables derived from the

previous research model on the model of

acceptance and use of technology. The variables

are subjective norms, social factors (social

factors) and image (image).

d. Facilitating Conditions

The theory of attitude and behavior of Triandis

(1980) in Tjhai (2003) states that the use of

information technology by workers is influenced

by individual feelings (affect) on the use of

personal computers, social norms in workplaces

taking into account the use of personal

computers, habits related to computer use,

consequences of personal computer use, and

facilitating conditions in the use of information

technology.

2.3 Acceptance of IT

The use of information systems, the utilization of

information technology by individuals, groups, or

companies is a core variable in information systems

research. The use of information technology systems

is a major variable affecting managerial performance

(Sharda et al., 1998; Davis, 1989). Iqbaria (1994),

Nelson (1996), Luthans (1995) also mentioned that

individually or collectively acceptance of use can be

explained from the variation of the use of a system

because it is believed the use of an IT-based system

can develop individual performance or

organizational performance.

Several studies have identified IT acceptance

indicators, where it is generally known that IT

acceptance is seen from system usage and frequency

of computer usage (Soh.et.al:1992) and others are

looking at user satisfaction aspects

(Iqbaria.et.al:1997). Research conducted by

Adam.et.al (1992) and Davis.et.al (1989) make use

of the system as a key indicator of user acceptance.

While Imam Yuadi (2010) explains that 3

dimensions determine the acceptance of technology,

namely aspects of trust, attitude, and user goals.

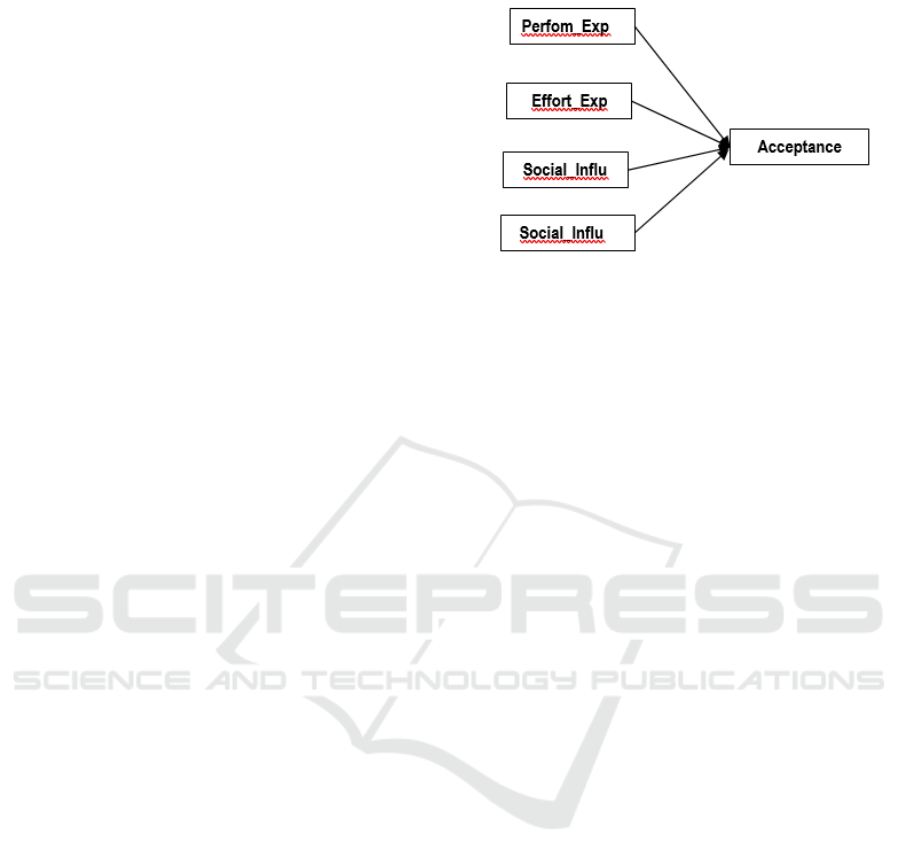

The research model used as the basis for

preparing the hypothesis is as follows:

Figure 1. Research Model

Performance expectancy in the form of easy

access to accounting data in various formats,

flexibility to communicate with leaders and peers,

flexibility report format, Positive experience in the

form of ease of using features and systems that are

user friendly, Social influence in the form of advice

and direction from the leadership and peers, greeting

the use of system and facilitating condition in the

form of system facilities provided by the company

proved to increase their acceptance in using

accounting information system.

Hypothesis 1: Performance Expectancy, Effort

Expectancy, Social Influence and

Facilitating Condition affect the

Acceptance of Accounting

Information System

The impact of the use of an information system

on the individual users of the system is defined as

the degree to which a person believes that using the

system can improve its performance. Seddon (1997)

defines the performance of individuals as individual

perceptions of the use of information systems they

use can improve their performance in

organizing.Acceptance of a good system will make

accountants tend to feel comfortable during work so

they will feel helpful in completing the work. The

higher the level of user satisfaction of information

systems, the higher their performance.

Hypothesis 2: Acceptance of Accounting

Information System influence

toward individual performance.

Performance Expectancy, Effort Expectancy,

Social Influence and Facilitating Condition provide

net benefits so that it can be a reference to the extent

to which information systems can contribute to the

success of individuals and organizations.Factors

ICRI 2018 - International Conference Recent Innovation

508

Performance Expectancy, Effort Expectancy, Social

Influence and Facilitating Condition give impact to

user satisfaction system, so as to increase individual

performance (Seddon, 1997).

Hypothesis 3: Performance Expectancy, Effort

Expectancy, Social Influence and

Facilitating Condition

influencetoward individual

performance.

3 RESEARCH METHOD AND

INSTRUMENTS

The population in this study is a management

accountant working for a business company in West

Jakarta. The number of samples determined in this

study is 5 times the number of indicators as many as

110. Hypothesis testing of this research using Path

Analysis (Analysis of Path) by using 2S OLS (Two

Stage Ordinary Least Square) to analyze the pattern

of relationship between variables with the aim to

determine the direct or indirect effect with the

pattern of causality.

1. Empirical results and discussion

a. Performance Expectancy, Effort Expectancy,

Social Influence and Facilitating Condition on

Acceptance of Accounting Information System

1) Simultaneous Test (F Test)

This test is used to determine whether

there is influence simultaneously between

Performance Expectancy, Effort Expectancy,

Social Influence and Facilitating Condition to

Acceptance of Accounting Information

System.F test results can be seen as follows:

Table 1 Simultaneous Test Results Model 1

ANOVA

a

Model

Sum of

Squares

df

Mean

Square

F Sig.

1

Regre

ssion

8.106 4 2.026

6.77

8

.000

b

Resid

ual

31.392 105 0.299

Total 39.497 109

Then Ha1 is accepted, because when viewed

from the results of significance, it is found that the

significance value of 0.000 <α (0.05) means that

simultaneously Performance Expectancy, Effort

Expectancy, Social Influence and Facilitating

Condition affect Acceptance of Accounting

Information System. This can be due to the

accountant already aware of the importance of

accounting systems that support his work.

Performance expectancy in the form of ease of

accessing accounting data in various formats,

flexibility to communicate with leaders and peers,

flexibility report format, positive experience of

effort expectancy in the form of ease of use features

and systems that are user friendly, social influence in

the form of advice and direction from the leadership

and colleagues greeting the use of system and

facilitating condition in the form of system facilities

provided by the company proved to increase their

acceptance in using accounting information system.

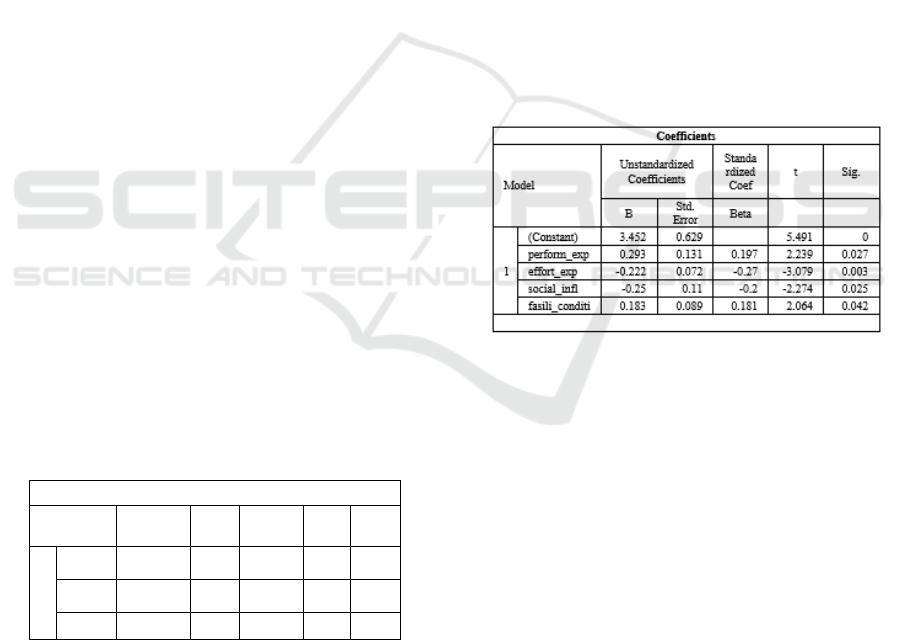

2) Partial Test (t test)

The t test is performed to prove the

partial influence between the independent

variables consisting of Performance

Expectancy, Effort Expectancy, Social

Influence and Facilitating Condition

influencing Acceptance of Accounting

Information System.

Table 2 Partial Test Results Model 1

Performance Expectancy has a significant

positive effect on Acceptance of Accounting

Information System. This is because Performance

expectancy is a UTAUT construct aimed at

measuring a person's confidence level that using a

system can assist a person in achieving job

performance (Vekantesh et al., 2003).With high

Peformance expectancy, accountants have been able

to experience significant benefits after using a

system (Adenan, 2013).With these perceived

benefits, then the level of acceptance of accounting

information systems will increase.

Effort Expectancy has a significant negative

effect on Acceptance of Accounting Information

System. Effort Expectancy has a significant negative

effect on Acceptance of Accounting Information

System. Effort expectancy is the level of effort of

each individual in the use of a system to support his

work (Venkatesh et al., 2003) and is a level of ease

of use of the system that will reduce the effort

Analysis of the Factors That Affect the Acceptance of Accounting Information Systems in Business Firms in Jakarta

509

(energy and time) of individuals in doing their work.

As stated by Adenan (2015), that effort expectancy

refers to how easily one thinks in using a system, it

can be said that accountants within the company

have not felt that the system is capable of supporting

their work and it requires effort and time to be able

to use,thus with the system makes the acceptance of

accounting information systems to be down.

According to Venkatesh and Davis (2000), social

influence has an impact on individual behavior

through three mechanisms of compliance,

internalization, and identification. It can be

concluded that the more influence an environment

gives to the prospective users of information

technology to use new information technology, the

greater the interest arising from potential personal

users in using the information technology because of

the strong influence of the surrounding environment.

Social influence can negatively affect the acceptance

of the system may be due to the desire of

individuation, namely the need to maintain our

individuality. Most of us have a desire for

individuation to be differentiated from others in

some ways.Also, it is possible because of the desire

to maintain control over the events in his life. The

stronger the individual needs for personal control,

the less likely they are to comply with social

pressure.

Facilitation Condition has a significant positive

effect on Acceptance of Accounting Information

System. The conditions that facilitate the use of

information technology are the extent to which one

believes that organizational and technical

infrastructure exists to support the use of the system.

If the facilities provided to use the system more

complete, then the acceptance of the system will

increase.

4 CONCLUSIONS AND

IMPLICATIONS

The conclusion of this research is that the

acceptance of the accounting information system

due to management accountant has realized the

importance of an accounting system to support the

work.This is becauseof ease of accessing accounting

data in various formats, flexibility to communicate

with leaders and peers, flexibility report format,

positive experience and systems that are user-

friendly. Acceptance of an accounting information

system makes accountants tend to feel comfortable

during work so they will feel helpful in completing

the work.

Some of the limitations of this study lead to

many things that can not be explained more deeply,

especially the discussion of the causal factors of

individual performance improvement from

individual control over their work and their belief in

self-efficacy. Then further research can be proposed

to add the variables locus of control in order to

improve the performance of individual accountant

management about the acceptance of the accounting

information system

REFERENCES

Budi Santoso(2010),Pengaruh Perceived Usefulness,

Perceived Ease Of Use, Dan Perceived Enjoyment

Terhadap Penerimaan Teknologi Informasi (Studi

Empiris Di Kabupaten Sragen)Jurnal Studi Akuntansi

Indonesia Fakultas Ekonomi Universitas Sebelas

Maret Surakarta

Christina Jimantoro Dan Elisa Tjondro (2014), Analisis

Niat Penggunaan E-Filing Di Pt “X” Dan Pt”Y”

Surabaya Dengan Structural Equation Modeling Tax

& Accounting Review, Vol 4, No 2, 2014 Program

Akuntansi Pajak Program Studi Akuntansi Universitas

Kristen Petra

Haris Pamugar, Wing Wahyu Winarno & Warsun Najib

(2014), Model Evaluasi Kesuksesan Dan Penerimaan

Sistem Informasi E-Learning Pada Lembaga Diklat

Pemerintah Scientific Journal Of Informatics Vol. 1,

No. 1, Mei 2014 Jurusan Teknologi Elektro Dan

Teknologi Informasi, Fakultas Teknik, UGM,

Yogyakarta

I Komang Ari Diksani, Ni Kadek Sinarwati, Nyoman Ari

Surya Darmawan(2010),Pengaruh Keyakinan Diri

Atas Komputer, Keinovatifan Personal, Persepsi

Kegunaan, Dan Persepsi Kemudahan Penggunaan

Terhadap Penggunaan Sistem Informasi Akuntansi

(Studi Pada Kantor Cabang Utama Bank Central Asia

Di Singaraja), Jurusan Akuntansi Program S1

Universitas Pendidikan Ganesha Singaraja, Indonesia.

I Made Suarta Dan Iga Oka Sudiadnyani (2012), Studi

Faktor Penentu Penerimaan Dan Penggunaan Sistem

Informasi Akuntansi Pada Lembaga Perkreditan

DesaJurusan Akuntansi, Politeknik Negeri Bali Jln.

Kampus Bukit Jimbaran, Badung, Bali.

Ni Made Sugiartini Ida Bagus Dharmadiaksa (2016),

Pengaruh Efektivitas Teknologi Sistem Informasi

Akuntansi Pada Kinerja Individu Dengan Budaya

Organisasi Sebagai Pemoderasi Issn: 2302-8559 E-

Jurnal Akuntansi Universitas Udayana.14.3 (2016)

Hal: 1867-1894 1867

Ni Made Sri Rukmiyati I Ketut Budiartha (2016),

Pengaruh Kualitas Sistem Informasi, Kualitas

Informasi Dan Perceived Usefulness Pada Kepuasan

Pengguna Akhir Software Akuntansi (Studi Empiris

ICRI 2018 - International Conference Recent Innovation

510

Pada Hotel Berbintang Di Provinsi Bali).E-Jurnal

Ekonomi Dan Bisnis Universitas Udayana 5.1 (2016) :

115-142

R. Kristoforus Jawa Bendi, Sri Andayani (2013)Analisis

Perilaku Penggunaan Sistem Informasi Menggunakan

Model Utaut Seminar Nasional Teknologi Informasi &

Komunikasi Terapan 2013 (Semantik 2013) Isbn: 979-

26-0266-6 Semarang, 16 November 2013

Ribka Armanda Suwardi Bambang Hermanto (2015),

Analisis Faktor Penerimaan Dan Penggunaan

Teknologi Dalam Sistem Informasi Akuntansi Dengan

Pendekatan Tam Sekolah Tinggi Ilmu Ekonomi

Indonesia (Stiesia) Surabaya Jurnal Ilmu & Riset

Akuntansi Vol. 4 No. 3 (2015)

Sri Hartini (2011), Pengembangan Model Tam :Expertice

Dan Innovativeness Sebagai Variabel Moderator Studi

Pada Penggunaan E Banking Journal Of Business

And Banking Volume 1, No. 2, November 2011, Pages

155 – 164

Taufik Saleh, Darwanis, Usman Bakar (2014), Pengaruh

Kualitas Sistem Informasi Terhadap Kualitas

Informasi Akuntansi Dalam Upaya Meningkatkan

Kepuasan Pengguna Software Akuntansi Pada

Pemerintah Aceh, Magister Akuntansi Pascasarjana

Universitas Syiah Kuala Banda Aceh Fakultas

Ekonomi Universitas Syiah Kuala, E-Journal S1 Ak

Universitas Pendidikan Ganesha (Volume: 2 No. 1

Tahun 2014)

Vivi Ani Susanti (2008), Teknologi Tugas Yang Fit Dan

Kinerja Individual Staf Pengajar Fakultas Ekonomi

Unika Widya Mandala, Surabaya

Wiwin Agustian Rusmin Syafari (2015),Pendekatan

Technology Acceptance Model (Tam) Untuk

Mengidentifikasi Pemanfaatan Internet Usaha Kecil

Dan Menengah Sumatera Selatan Universitas Bina

Darma

PalembangUniversitas@Mail.Binadarma.Ac.Id

Analysis of the Factors That Affect the Acceptance of Accounting Information Systems in Business Firms in Jakarta

511