Good Governance Problem at Local Level: Study of Village Funds

Management Accountability in Madura, West Java

Haniah Hanafie

1

and Masrul Huda

1

1

Universitas Islam Negeri Syarif Hidayatullah Jakarta, Indonesia

Keywords: good governance, accountability, village funds.

Abstract: The purpose of this paper to explain the issues of good governance at the local level, especially the study of

accountability in the management of Village Funds in Madura, East Java. Use of theory the Good

Governance perspective focuses on one of the principles of good governance is accountability. The

accountability which is used as a reference in this study includes vertical, horizontal, local and social

accountability. This study uses a qualitative approach, data collection techniques are interviews, document

review and observation. Techniques of data analysis is qualitative descriptive. The results has found that

accountability of Good Governance in management of village funds at Madura was still weak. Term of

Vertical Accountability, independence in making reports does not yet exist, because it is made by The Third

Parties. Horizontal Accountability it is also still weak, because the BPD does not provide supervision the

development funded by the Village Funds. Local Accountability is also weak, because the BPD and the

village head have no cooperation in development planning. Social Accountability is still low, because the

involvement of community participation in development has not done well. Conclusion, The accountability

of good governance at the local level (Madura) has not yet done properly.

1 INTRODUCTION

The Village Funds (Dana Desa) becomes an

important issue and draws the attention of wider

community due to the recent implementation of new

policy that has been taken from Indonesian budget

(Anggaran Pendapatan dan Belanja Negara) policy

which was done by the government.

The allocation of the Village Funds (Dana Desa)

has continued to increase by 2015 with Rp. 20.76

trillions to Rp. 46.9 trillions in 2016 continued in

2017 by Rp. 60 trillions, and currently the budget is

on Rp. 120 trillions.

Several studies have shown that the Village

Funds (Dana Daerah) program has resulted a

positive impact, as Daraba (2017: 52) suggests that

village participation can be enhanced by the Village

Funds (Dana Daerah) program. In contrast to

Daraba, the result of the research that was conducted

by Sari and Abdullah (2017: 46-47) (Sari, 2017),

shows that the Village Funds (Dana Daerah) has

succeeded in reducing local poverty. Tangkumahat,

Panelewen, and Mirah (2017: 341-342)

(Tengkumahat, 2017), noticed that the Village Funds

program in Pineleng Sub-district can also improve

the local economy as the infrastructure has been

built from the Village Funds Program.

Indonesia has 74,093 villages, and 20,168

villages (27.22%) are in underdeveloped condition.

Distribution of Village Funds (Dana Desa) is based

on the number of villages: the level of geographical

difficulty and population, area, poverty rate, and cost

of living index. However, 90% is divided equally to

all villages and 10% is taken into the variables.

Thus, the more villages the region has, the larger the

Village Funds is, and the greater the accountability

will be.

Based on the results of studies and coordination

and supervision activities from the Corruption

Eradication Commission (KPK) (Directorate of

Research and Development (R & D), 2015), it turns

out that the accountability of the financial

management in the regions is still weak. Therefore,

in order to enhance the accountability, the local

government should provide supervision or assistance

to the village government in managing the village

funds.

Hanafie, H. and Huda, M.

Good Governance Problem at Local Level: Study of Village Funds Management Accountability in Madura, West Java.

DOI: 10.5220/0009932816211628

In Proceedings of the 1st International Conference on Recent Innovations (ICRI 2018), pages 1621-1628

ISBN: 978-989-758-458-9

Copyright

c

2020 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

1621

According to the Regulation of the Minister of

Home Affairs (Kementerian Dalam Negeri)

(Regulation of the Minister of Home Affairs

(Pemendagri) on Management of Village Finance,

2014), Village Fund (Dana Daerah) should be

managed on the basis of transparency, accountable,

participatory principles and carried out in an orderly

and budgetary discipline. In fact, these principles

have not been well implemented by every village

resulting in ineffectiveness of the village funds

management.

The conclusion of Farida's research (2015: 118)

(Farida, 2015) show that HR causes the inefficacy of

the village financial management since the

authorities are unable to generate an accountable

financial administration. Ade Irma (2015: 136)

(Irma, 2015) in Dolo Selatan District, Sigi District,

discovered that the local government calls for

support from the local authorities due to the

deficient situation of the administration.

Astri Furqani (2010) (Furqani, 2010) stated in

her research in Kalimo Village, Kalianget District,

Sumenep Regency, that financial management does

not fulfill the principle of the accountability because

there are several processes that are not in accordance

with Minister of Home Affairs Regulation

(Kementerian Dalam Negeri) No. 37/2007. One of

the examples is the absence of the Board of Local

Advisor (BPD) during the meeting made it

impossible to have transparency from planning to

executing.

Likewise, with the research in Desa Aglik

(Putriyanti, 2012), it was found that the low of

reinforcement of the Village Government in Aglik

because the people were slow in responding the

information of the Village Implementation Report

and the lack of supervision to the accountability of

the village government.

Likewise, with the research in Desa Aglik

(Putriyanti, 2012), it was found that the reasons of

the low reinforcement of the local government in

Aglik are because of responsiveness of the local

people and the lack of supervision in the

accountability of the regional bureaucracy. The

problem of ineffectiveness of the village financial

management shows that both the central and local

government are not aware of the development of the

villages. (Series Discussion Institute of Civilization,

2015)

Some villages have received training and

assistance by district governments and NGOs, hence

development is possible to achieve. In contrast with

villages that did not receive adequate training and

assistance, they are still struggling to improve the

quality of the village.

The village is believed to be one of the

spearheads of the government organization and seen

as the success factor of one nation. Partial

perspective is still related to the government

authorities which indicates that proper management

has not been able to be implemented at the local

level.

The research of Sudarno Sumarto, Asep

Suryahadi and Alex Arifianto (2004: 5) (Sumarto,

2004), revealed that donor countries believe the

foreign aid cannot reduce the poverty in the

developing countries. Therefore, to be able to

eliminate destitution, the country needs professional

and reliable management from the government. In

this case, Village funds can help the local

administration to use the natural resources to provide

welfare prosperity for the local people.

The implementation of good governance, both

central and local levels, can better the situation of

local people, especially in the rural areas if only the

accountability of the village funds management is

well implemented.

Many types of research that had been taken

mainly focused on the accountability in the general

spectrum. Thus, as expected by The Villages,

Disadvantaged Regions and Transmigration

Ministry, this paper aims to dig into more detailed

and focused on 4 types of accountability, namely

vertical, horizontal, local and social accountability

(Jafar, 2015). The main reason for choosing these 4

types of accountability is as a focus of study in the

management of Village Funds because the four

accountabilities must be conducted by the local

government.

This paper examines the problem of good

governance at the local level: Village Funds

Accountability Study in Madura, East Java. this

paper discusses the 4 types of accountability and

will be using a qualitative approach to describe the

phenomenon of the accountability in the village

funds management in the context of a good

governance.

2 PLANNING AND

IMPLEMENTATION OF

VILLAGE FUNDS

MANAGEMENT

The islands of Masalembu District is located in

Sumenep Regency. Sumenep Regency is one out of

ICRI 2018 - International Conference Recent Innovation

1622

29 districts in Madura. This district has 4 villages

named Karamian, Masalima, Masakambing, and

Sukajeruk. These four villages have received village

funds from the district government. The amount of

budget each village received in 2016 was Rp.

2.618.609.019 and in 2017 Rp. 3.342.655.700.

Thereby, the number of village funds received per

village has increased as can be seen in the following

table:

Table 1: Number of Village Funds Received by

Masalembu Sub-district

No

Name

Villages

Years 2016 Years 2017 Total Rp.

1

Masalima

Village

692,501,65

1

884,658,10

0

1,557,159,751

2

Karamian

Village

631,899,24

0

806,211,30 1,438,110,540

3

Masakam

bing

Village

624,660,278

796,840,80

0

1,421,501,078

4

Sukajeru

k Village

669,547,85

0

854,945,50

0

1,524,493,350

Total 2.618.609.019 3.342.665.700 5.961.264.719

Source: Secondary Data from Kemendesa PDTT RI, 2017

The source of the village fund is from Indonesian

Budget (Anggaran Pendapatan dan Belanja Negara

Indonesia), and transferred to the District

Government Treasury and eventually to the Village

Government's treasury. Once the Village Funds is

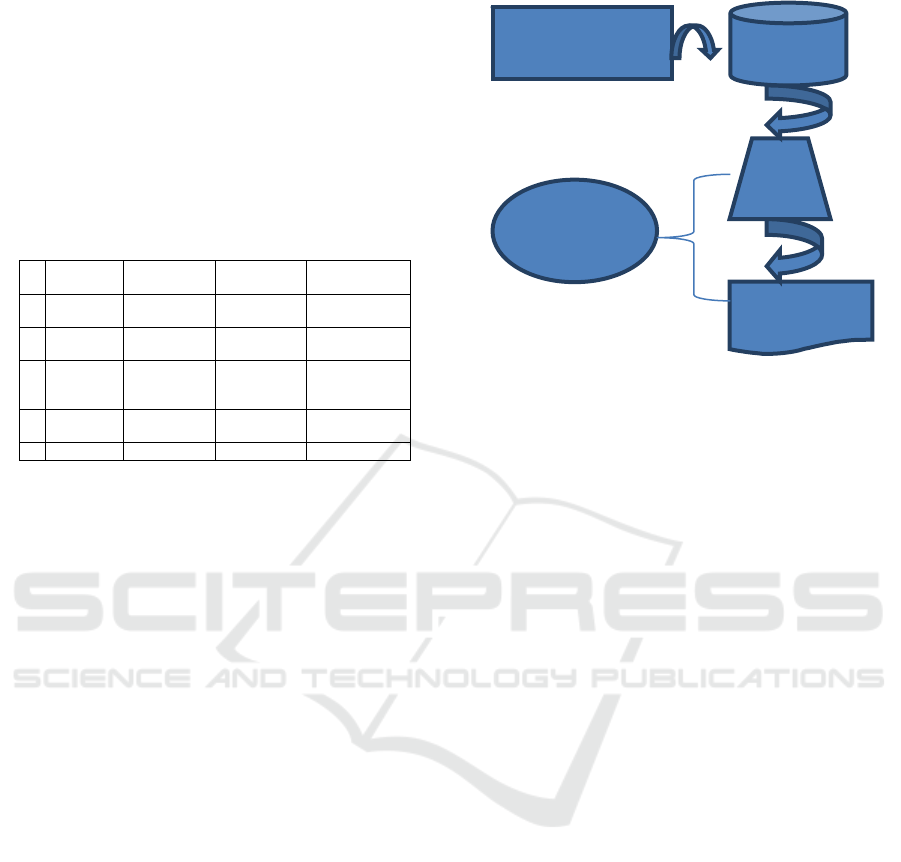

received, the village government must make a plan.

The planning stage consists of 1). Determination of

Priority of Development Sector, 2). Priority of

Empowerment Field, 3). Agreed and decided in

Village Deliberation, 4). Preparation of the Village

Government Work Plan (RKP Des), 5) Budgeted in

APB Des (Village Revenue Expense Village), 6).

Village RKP and Village APB must be established

in Village Regulation (Perdes). The flow chart is as

follows (Village Development Planning Ministry of

Village PDDT RI, 2017):

Figure 1.

The study result in Madura indicates that the

procedure of planning stages has been properly

performed by the local government, in Karamian,

Masalima, Masakambing, and Sukajeruk.

The improvement of the village fund is more

focused on the infrastructure development (roads,

beach embankments, ditches,etc), while the

betterment in the area has not received attention.

This means the provision in PP no. 60 of 2014

(Government Regulation on Terms of Use of Village

Funds, 2014) and Minister of Finance Regulation

No. 247 of 2015 (Regulation of the Minister of

Home Affairs (Pemendagri) on Management of

Village Finance, 2014) prioritize community

development and empowerment, but the objective of

the village funds has not been justly applied by the

local authority.

The development of the Village Funds Program

Planning needs to make Musyawarah Dusun

(Musdus) before holding Village Deliberation

(Musdes) meeting. In the process of Village

Deliberation (Musdes) assembly, not all members of

the community are involved in the Village

Deliberation Community (BPD) meeting as the

Chairman of the neighborhood (RT), and the

Chairman of the hamlet have represented them in the

conference.

The absence of all members of the BPD in the

Musdes indicates that the village head ignored the

suggestion to hold the Musdes along with the BPD.

Besides, the BPD (Pemendagri on Village Financial

Managemet) is an institution that must obtain a

written statement of government administration at

DEVELOPMENT AND

EMPOWERMENT

PRIORITY

MUSDE

S

RKP

DESA

APB

DESA

DECIDED

ON PERDES

Good Governance Problem at Local Level: Study of Village Funds Management Accountability in Madura, West Java

1623

the end of the fiscal year of the village head (Law on

Village, 2014).

Musdes produces Village Government Work

Plan (RKP Des) which becomes the basis of Village

Revenue Expenditure Budget (APBDesa). After

RKP Des and APBDes are drawn up, it is stipulated

in Perdes (Village Regulation) by the village head.

Although it must be established with Village

Regulation (Perdes) However, the research team has

never received the Perdes which made by the village

head since the Local Village Assistant (PLD) is

responsible for the existence of Perdes.

Unfortunately, the PLD is unable to show the Perdes

to the board research team..

In addition to the Perdes, Village Budget Plan

(RAPBDesa) also should not be broadcasted to the

community, including to the Research Team. The

attitude of the village head and PLD indicates that

transparency of information is very difficult to

realize. Hence, transparency becomes one of the

principles in village governance that must be

implemented by the village head in organizing the

government (Law on Village, 2014). The village

success management can automatically enforce good

governance at the local level. Therefore, all of the

village government officials should be perspicuous,

professional and free from Corruption and Nepotism

(KKN) (Law on Village, 2014).

Although the Village Funds Program has been

planned to accommodate community proposals

through Musdus and Musdes from the beginning,

that does not mean all the village community

proposals can be met. Since the development of the

Village Funds Program is aimed only at the location,

residence of the village head; village officials and

village head supporters, the outcome of the Village

Funds development is considered to be uneven and

discriminating,

In addition to the low quality of development,

the construction of coastal embankments has always

been damaged, and the development of Village

Funds is considered to be unuseful as it only builds

sub-district signboards that are not directly

beneficial to the community.

The transparency and participation principles of

good governance in village financial management,

as outlined in the Minister of Home Affairs

Regulation No. 113 of 2014 (Regulation of the

Minister of Home Affairs (Pemendagri) on

Management of Village Finance, 2014) are not fully

implemented in Madura. Because the villagers are

skeptics about the amount of the village funds and

the lack of involvement from the community in the

development planning or even in the public

dialogue.

The Implementation of the transparency and

participation is still infirm: there are geographic and

demographic inhibiting factors. The area of

Masalembu Subdistrict is geographically isolated

and situated on an island off the coast of Java Sea,

adjacent to South Kalimantan and South Sulawesi.

The intensity of departure only twice a week and the

journey takes 16 hours by ship. When the weather is

terrible, the boat trip is often canceled.

The condition of the remoteness hinders the

process of coaching, empowerment, assistance, and

supervision given by the central, provincial and

district governments to streamline the management

of village funds. At the time of the interview with

auxiliary experts at Sumenep Regency, the

geographical condition of Masalembu Sub-district

was recognized as a significant obstacle, so the co-

chairs had never been to Masalembu for assistance.

The geographical barrier also affects

demographic conditions, the population of

Masalembu Sub-District is 23.75 people, the

majority of 18,640 people or 78% do not graduate

from elementary school (SD). The demographic

condition also influences the weakness of the

authorities in managing the government including

the village funds. The activities of empowerment

and assistance that should be done by a higher

government are not conducted because of the

constrained natural conditions

.

3 ACOOUNTABILITY OF

VILLAGE FUNDS

MANAGEMENT

3.1 Vertical Accountability

Accountability is the responsibility of the village

government given by the government above it

(district government) in the management of village

funds. In this paper, we examine four types of

accountability, namely vertical accountability,

horizontal accountability, local accountability and

social accountability.

To obtain information on how vertical

accountability in Village Funds (DD) management

in Masalembu district, the indicator used is how the

accountability report of Village Funds (DD)

management is made and given by the Village

Government to the superiors (Sumenep District

Government).

ICRI 2018 - International Conference Recent Innovation

1624

Meanwhile, the Village Funds Reporting

Procedure and responsibility are held by the Village

Head as the holder of

the village financial

management authority. The reporting procedures of

the Village Funds are related to the APBDesa, and

the realization is submitted to the Mayor

(Pemendagri on Village Financial Managemet), in

the form of (a) First-semester report; and reports for

the end of the year. (b) The first-semester reports is a

report on the realization of Village Funds

(APBDesa). (c) The realization report of Village

Fund (APBDesa) implementation should be

submitted no later than the end of July of the current

year. (d) The final semester report is filed no later

than the end of January of the following year.

The village head submits the accountability

report of the realization of the APBDesa

implementation to the Regent / Mayor at the end of

the fiscal year. The accountability report for the

understanding of APBDesa implementation, the

elements of the income, expenditure, and finance.

Village Regulation determines the accountability

report for the realization of APBDesa

implementation.

Although the village head holds the power of

village financial management, it does not mean the

village head and the apparatus who make their

accountability report. The village head received and

entirely handed over the report to the PLD (Local

Village Assistant) because of those whom so-called

"brokers" (consultants, third parties) from the district

or regency. Nevertheless, vertical accountability will

remain in place if the village head does not report

the liability for the use of the Village Funds

(APBDes) reports on usage, and the next phase of

the Village Funds will not be lowered. Therefore,

reports on the usage of APBDesa must be made and

sent to the district while the problem is the village

government does not make the report.

The Village Funds accountability report is part of

the realization of the APBDesa implementation, but

it does not

separate itself from the village

governance report and submit

it to the regent/mayor

through the sub-district head or other designation.

This report can be informed to the public in written

or information media that is accessible for everyone.

The media information can be varied from bulletin

boards, community radio, and other media

information.

However, in reality, there are different types of

information regarding Village Funds, and some of

the data is not fully shared to the research team even

the RAB Desa (Budget Plan) should not be informed

to the community, including the research team. The

transparency of the information is very difficult to

obtain, let alone the data collection which

coincidently happened with the case of Pamekasan

Regent related to corruption of Village Funds.

Therefore, the village government is worried about

providing information, because it is believed that

clean and free from corruption and nepotism

environment is still challenging to implement yet.

It can be said that the local government has

fulfilled vertical accountability, only the

independence in making the accountability report is

not yet apparent because the village administration

just received the "transparent" report, without much

effort to make it.

The downside of the village government lies in

the human resources which cannot fulfill and

understand the task appropriately. According to

Tangkumahat et al., 92017: 340) (Tengkumahat,

2017)

: The village government's human resources

are still unable to comprehend the process of

implementing the Village Funds Program, and the

delay in reporting due to the lack of knowledge and

skills of PTPKD. Besides, the lack of technical

guidance from the PLD and the availability of third

parties as the middleman make the village head feel

secured as well as deny the responsibility

.

3.2 Horizontal Accountability

Horizontal Accountability is the accountability

provided by an authorized institution/body/

organization that has authority, and the supervision

given by the Village Consultative Body (BPD).

Surveys have shown that the supervision of BPD

has not been optimally implemented because during

the Village Deliberation (Musdes), not all official

BPD officials were invited to discuss the Village

Funds (Dana Desa) Program, as what had been

experienced in Masalima Village. The Secretary of

BPD was not included in the Musdes, as it does not

support the village head, that is why the decision on

the Village Funds is vague. Meanwhile, in Karamian

Village the Chairman of BPD was involved in the

Musdes, but the supervision was not optimally done

since the wife of the Chairman of BPD also acts as

the staff of the village head, therefore the decision

made by the village head is entirely supported by the

chairman of BPD.

Mostly, local BPDs are not independent and do

not have the power to supervise village heads

because of the absence of their supervisory during

the planning, development and implementation

process. Whereas in Law No. 6 of 2014 on villages

it is said that BPD will receive reports on the

Good Governance Problem at Local Level: Study of Village Funds Management Accountability in Madura, West Java

1625

administration of the village head (Law on Village,

2014). There must be cooperation between the

village head and BPD, so BPD is expected to

intensify its control over the village administration.

Cooperativeness plays a vital role to generate the

harmonious relationship between the village head

and BPD so the supervision will not get weaker and

there will be no room for fear of corruption and

nepotism (KKN) in the system.

3.3 Local Accountability

Local Accountability is done internally within a

particular region, for example, in this case, it is

undergone by village government along with BPD to

plan and evaluate the development of the village.

The results of the research show that the

existence of BPD is considered to be one-sided,

because not all BPD managers join in the discussion

of the Village Funds in the Musdes. The initial

meeting initiatives merely come from the village

head, that is why BPD does not have the power to

initiate a discussion related to village funds. The

village head only cooperates with members or

administrators of BPD who can follow the rule and

term that are implemented by the village head. while

members who are not in line with the leadership of

the village head will be excluded from the assembly.

It is difficult to create a strong relationship

between the village head and the overall BPD

officials to do the planning and evaluation of the

Village Fund Program. In Permendagri No. 110 of

2016 on Village Consultative Body (BPD)

(Permendagri on Village Consultative Body (BPD),

2016) it is written that members of BPD are

representative of villagers and elected

democratically through direct election process or

deliberative consideration. Thus, the BPD can be

considered as people's representative (Village

Parliament), and the aspirations of village

communities can be represented and submitted by

BPD, both in the planning and evaluation of the

Village Funds Program. Therefore, establishing

cooperation with BPD can be interpreted as having

served the people of the village.

According to Alexander Abe (2002) in Daraba

(2017: 57) (Daraba, Influence of Village Funds

Program on Community Participation Level of

North Galesong Sub-district, Takalar Disrict, 2017),

there are two forms of participatory planning,

namely direct planning prepared with the

community and plan developed through

representative mechanisms. In Masalembu district,

specifically the second participatory planning, the

village head does not adequately discuss the village

funds program since all members of BPD, as the

legitimate representative institution, are not invited

to the discussion.

3.4 Social Accountability

Social accountability is the accountability that must

be provided to the community by involving the

citizens in the planning, supervision and social audit

in the process of village development in particular in

the management of the Village Funds (village

finance).

Citizens have made their involvement in

planning which their participation only presented by

the representative. In Sukajeruk Village, the village

head does not include RT, RW, and BPD either in

planning, supervision or social audit, therefore it is

difficult for the local people to supervise and audit

the program impartially. According to Geddesian in

Daraba (2017: 57) (Daraba, Influence of Village

Funds Program on Community Participation Level

of North Galesong Sub-district, Takalar Disrict,

2017) from the planning stage, communities can

actively involve through Musdus and Musdes.

In the planning stage through legitimate

representatives, e.g., BPD, according to Alexander

Abe (2002) in Daraba (2017:57) (Daraba, 2017),

stated that society should not remain silent, but still

provide input, criticism, and control, so that people's

aspiration can be heard and actualized.

The research concluded that despite the protest

made by one member of Sukajeruk Village

community on the quality of coastal embankment

construction and its construction site being built, the

village officials did not respond to it. Furthermore,

the RAB (Budget Plan) on the development of

Village Funds should not be published and

broadcasted to the public to frightened the public in

doing an upcoming protest.

Social accountability is getting more difficult to

achieve due to the lack of community involvement

in village funds development especially in planning,

monitoring, and social auditing. None of the

mentioned accountability above can be implemented

sufficiently in Masalembu sub-district, for one of the

principles of village law No.6 of 2014 on Villages

(Law on Village, 2014) has not been correctly

applied and used into the process of village

improvement.

In terms of financial accountability, it is claimed

that Mohamad et al. (2004) (Fajri), accountability

which includes financial statements consisting of

revenue, storage, and expenditure cannot be

ICRI 2018 - International Conference Recent Innovation

1626

accomplished by the village government

administrators independently because a third party

still assists it, and incompetent human resources

becomes one of the reasons.

Concerning the benefit accountability (Fajri), the

accountability that includes the achievement of

objectives following the procedure to achieving the

effectiveness of the purposes. One of the prominent

obstacles stand in However, it has not been taken

into account due to the lack ofinvolvement from the

community and BPD. The most important thing

from achieving the objective is effectiveness, not yet

well said, because the procedure that should be done

by involving the community and BPD is not fully

realized. The alignment of the village head to the

community or the BPD Board in line has become

one of the obstacles.

Similarly, from the side of procedural

accountability (Fajri), accountability relating to the

procedures implementation concerning the

principles of ethics, morality and legal certainty, is

not fulfilled thoroughly since the ethical and moral

issues have not yet been upheld by village

government apparatus. It can only be accomplished

by reducing the quality of development and

essential mechanism. By lowering the variety of

construction and significant procedures that should

be passed.

4 CONCLUSION

From the above description, it can be concluded that:

1. The implementation of vertical, horizontal, local

and social accountability in the management of

village funds should be taken into serious

consideration, in this way the officiated chairman

of the village can acknowledge the central issue

to create a sustainable system in the government

in the local level. So that automatically good

governance at the local level can be realized.

2. The intensity of assistance from the Local

Village Assistants (PLD) and the District

Assistant should be intensified to the specific

degree to achieve the target of the village in its

development.

3. The local government need to consider the

competency of the human resources in the

village financial system.

REFERENCES

(n.d.). Retrieved July 23, 2018, from www.kemenkeu.com

Law on Village, No. 6 (2014).

Law on Village, No.6 (2014).

Law on Village, No. 6 (2014).

Regulation of the Minister of Home Affairs (Pemendagri)

on Management of Village Finance, No. 113 (2014).

Terms of Use of Village Funds, PP No. 60 (2014).

Village Financial Management, No. 113 (Permendagri

2014).

(2015, October 20). Retrieved from

https://www.kompas.com

Proceduring of Appropiation, Distribution, Use,

Monitoring and Evaluation of Village Funds, No. 247

(Regulation of the Minister of Finance (PMK) 2015).

Series Discussion Institute of Civilization. (2015, February

25).

Permendagri on Village Consultative Body (BPD), 110

(2016).

(2017, August 19). Retrieved July 20, 2018, from

https://www.merdeka.com

Secondary Data from the Ministry of Village PDTT RI

(2017).

Daraba, H. D. (2017, March 1). Influence of Village Funds

Program on Community Participation Level of North

Galesong Sub-district, Takalar Disrict.

Sosiohumaniora Journal, 19.

Daraba, H. D. (n.d.). Influence of Village Funds Program

on Community Participation Level of North Galesong

Sub-district, Takalar District. Journal of

Sosiohumaniora, 19.

Directorate of Research and Development (R & D).

(2015).

Fajri, R. E. (n.d.). Village Government Accontability in

Village Fund Allocation Management (ADD) (Study

at Ketindan Village Office, Lawang Sub-district,

Malamg Regency). Journal of Public Administration

(JAP), 3.

Farida. 2015. Transparency and Accountability of Village

Revenue and Expenditure Budges (APBDesa).

Journal of Accounting Science & Research, 4.

Furqani, A. 2010. Village Finance Management in

Achieving Good Governance (Study on teh Village

Government of Kalimo, Kalianget District of Sumenep

Regency). e-Journal.

Irma, A. 2015, January 1. Accountability Management of

Village Fund Allocation (ADD) in Dolo Selatan

District, Sigi Regency. e-Journal of Cataloging, 3.

Jafar, M. 2015. Series Discussion Institute of Civilization.

Pemendagri on Village Financial Managemet, No. 113

(2014).

Putriyanti, A. 2012. Implementation of Regional

Autonomy in Strengthening the Accountability of

Village Governance and Community Empowerment in

Aglik Village, Grabag Sub-district, Purworejo District.

Good Governance Problem at Local Level: Study of Village Funds Management Accountability in Madura, West Java

1627

Sari, I. M. 2017, June 1. Economic Analysis of Village

Fund Policies on Village Poverty in Tulungagung

District. Journal of Development Economics, 15.

Sumarto, S. A. 2004, March. Government Governance and

Poverty Reduction Preliminary Evidence of

Decentralizationin Indonesia. SMERU Research

Institute. Support from AusAID and Ford Foundation

and DFID.

Tengkumahat, F. V. 2017. Impact of Village Funds

Program on Improving Development and Economy in

Peneleng Sub-district, Minahasa. Journal of Agri

Socio Economic Unsrat, 13.

Village Financial Management. 2014. Regulation of the

Minister of Home Affairs (PERMENDRAGI). Village

Financial Management.

Village Fund, PP 22.

ICRI 2018 - International Conference Recent Innovation

1628