Practice of Disclosure Accounting Social Responsibility

Dimita Purba

1

, Duma Megaria Elisabeth

1

, Syafruddin Ginting

2

and Iskandar Muda

2

1

Student Postgraduate, Faculty Economic and Business, Universitas Sumatera Utara, Medan Indonesia

2

Lecture Faculty Economic and Business, Universitas Sumatera Utara, Medan Indonesia

Keywords: Accounting Social Responsibility, Profitabilitas, Disclosure

Abstract: PT. Toba Pulp Lestari is a paper production company founded in 1983 in Porsea sub-district. PT. Toba Pulp,

one of the companies that applies Corporate Social Responsibility, is a company's commitment to build a

better quality of life together with related parties, especially the surrounding communities and the social

environment in which the company is located in an integrated manner with its business activities in a

sustainable manner. The purpose of this study was to determine the application of Corporate Social

Responsibility (CSR) and the impact on the profitability of PT. Toba Pulp Lestari, Tbk. The method of data

collection used is documentation and literature study. The research method used in the study was

descriptive. The results of the study show that PT. Toba Pulp Lestari, Tbk, which every year pays for CD

(Community Development) / CSR funds by 1% of net sales. To implement CSR means the company issues

a number of costs. Final costs will be burdensome which reduce perceptions as high as profitability of

companies will decrease. Still, by implementing CSR, the corporate image will increase both the loyalty of

consumers to the highest level. This results in a level of profitability that will affect the indirect results.

1 INTRODUCTION

In maintaining its existence, the company should be

separated from the community as its external

environment. There is a reciprocal relationship

between the company and the community. Every

company around the world will prepare various

planned activities to improve the existence of the

company and become a Good Bussiness company.

One of them is by implementing Corporate

Social Responsibility (CSR) activities. CSRis an

agreement from The World Business Council for

Subtainable Development (WBCSD) in South Africa

in 2002 aimed at encouraging all companies in the

world to create sustainable development

CSR is transparent in expressing activities which

is conducted by companies related to social

activities, where disclosure is only limited to

company financial information, but is also expected

to provide information about the impacts caused by

company activities, especially those related to the

environment and problems social

Guaranteed sustainability of the company if the

company conducted by its responsibilities is not

only limited to shareholders but the company must

also pay attention to the social and the environment

that becomes the company's operations

The community will give a negative response to

the company that is considered not to pay attention

to the economic, social and environmental

conditions. This negative response from the

community will threaten the sustainability of the

company.

At present economic decisions are taken only by

considering the performance of the financial

information which is realized to be irrelevant by

investors and company management. The purpose of

this study is to determine the social responsibility

accounting at PT. Toba Pulp Lestari, Tbk and

recognize of social responsibility activities. And

recognize the impact of Corporate Social

Responsibility (CSR) on profitability at PT. Toba

Pulp Lestari, Tbk.

Purba, D., Elisabeth, D., Ginting, S. and Muda, I.

Practice of Disclosure Accounting Social Responsibility.

DOI: 10.5220/0009508911851189

In Proceedings of the 1st Unimed International Conference on Economics Education and Social Science (UNICEES 2018), pages 1185-1189

ISBN: 978-989-758-432-9

Copyright

c

2020 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

1185

2 THEORICAL FRAMEWORK

2.1 Stakeholder Theory

Friedman (1962) in (Ghozali, Imam, dan Chariri,

2007) stated that the company's main goal is to

maximize the prosperity of its owners. So according

to him, stakeholders are only defined as owners. In

the end, the Stakeholder Theory emerged by

Freeman (1983) in (Ghozali, Imam, dan Chariri,

2007) which explained the involvement and role of

stakeholders in promoting CSR towards the

company. According to him, stakeholders consisting

of customers, competitors, merchant associations,

media, environment, distributors, government,

consumer protection institutions, local communities,

and business people have active participation that is

very much needed in the successful implementation

of CSR. This makes the existence of a company

strongly influenced by the support provided by

stakeholders to the company (Ghozali, Imam, dan

Chariri, 2007)

Stakeholder theory considers the position of

stakeholders more powerful. This stakeholder group

is the main consideration for companies in

disclosing and / not disclosing information in

financial statements. In view of stakeholder theory,

companies have stakeholders, not shareholders

(Belkaoui, Ahmed Riahi, 2006).

Corporate Social Responsibility is a corporate

strategy to satisfy the desires of stakeholders, the

better disclosure of Corporate Social Responsibility

by the company, the stakeholders will be more

satisfied and will give full support to the company

for all its activities aimed at raising performance and

achieving profit.

2.2 Legitimacy Theory

The legitimacy theory and stakeholder theory are

theoretical perspectives that are within the

framework of the theory of political economy.

Because the influence of the wider community can

determine the allocation of financial resources and

other economic sources, companies tend to use

environment-based performance and disclosure of

environmental information to justify or legitimize

corporate activities in the eyes of the public (Gray,

Rob, 1995)

(Ralf, 2007) revealed that the explanation of the

strength of the organization's legitimacy theory in

the context of corporate social responsibility in

developing countries is twofold; First, the capability

to place profit maximization motives makes a clearer

picture of the motivation of the company to increase

its social responsibility. Second, the legitimacy of an

organization can be to include cultural factors that

form different institutional pressures in different

contexts. Legitimacy can provide a powerful

mechanism for understanding voluntary disclosures

for the environment and social activities carried out

by the company, and this understanding will lead to

critical public debate, furthermore the legitimacy

theory shows researchers and the wider community

of ways to be more sensitive to the content of

disclosure company (Tilling, 2004)

Corporate Social Responsibility practices carried

out by the company aim to align themselves with

community norms. With good disclosure of

Corporate Social Responsibility, it is expected that

the company will gain legitimacy from the

community so that it can improve performance

aimed at achieving corporate profits.

2.3 Signaling Theory

According to (Harahap, 2007) signal theory

(signaling theory) explains why companies have the

urge to provide financial reports to external parties.

The company's push to provide information is

because there is information asymmetry between

company management and outsiders (investors)

The company will present an annual report on the

company's CSR activities or reports on the

implementation of GCG (Good Corporate

Governance) in the company.

The purpose of this additional report is to provide

additional information about the company's activities

as well as a means to provide signals to stakeholders

on other matters, for example providing signals

about the company's concern for the surrounding

area, or a sign that the company is not only provide

information based on regulatory provisions but

provide more information for stakeholders. These

signals are expected to be positively accepted by the

market so as to be able to influence the company's

market performance reflected in the market price of

the company's shares.

According to Morris in (Harahap, 2007),

information asymmetry can occur if one party has a

more complete signal of information than the other

party. Information asymmetry occurs if management

does not convey all information obtained in full so

that it affects the value of the company reflected in

changes in stock prices because the market will

respond to existing information as a signal.

According to (Drever, 2016) signaling theory

emphasizes that the reporting company can increase

the value of the company through its reporting.

2.4 Corporate Social Responsibility (CSR)

Conceptually, there are many notions of social and

environmental responsibility, better known as

Corporate Social Responsibility (CSR).

According to Lako in the book CSR and Reform

of the Business & Accounting Paradigm (Lako,

UNICEES 2018 - Unimed International Conference on Economics Education and Social Science

1186

2011), CSR is a continuing commitment of a

company to be economically, legally and ethically

responsible for the impacts of its economic actions

on the community and the environment and

proactively make efforts sustainable efforts to

prevent potential negative impacts on society and the

environment and improve social and environmental

quality

A world organization The World Business

Council for Sustainable Development (WBCSD) in

(Belkaoui, Ahmed Riahi, 2006) defines CSR as

follows:

“Continuing Commitment by business to be

have ethically and contribute to economic

development while improving the quality of life of

the workforce and their families as well as of the

local community and society at large.”

According to the CSR Study Circle, the

definition of CSR is the earnest effort of business

entities to minimize negative impacts and maximize

the positive impact of their operations on all

stakeholders in the economic, social and

environmental spheres to achieve sustainable

development goals.

According to (Agus, 2011) that corporate

responsibility is not only limited to economic

responsibility, namely how to maximize profits to

increase shareholder equity, but also must be

socially responsible and environmentally (

environmental responsibility) integrally.

2.5 Corporate Social Responsibility Reporting

CSR disclosure itself is interpreted as part of the

social responsibility accounting that communicates

social information to stakeholders. The disclosure or

reporting of CSR implementation is reported in the

Sustainability Reporting. Sustainability reporting is

a practice of measurement, disclosure and

accountability efforts of organizational performance

in achieving sustainable development goals.

Sustainability reporting must provide a balanced and

reasonable picture of the sustainability performance

of an organization, both positive and negative

contributions

Nationally applicable guidelines are regulations

that apply in Indonesia. Corporate Social

Responsibility has been ratified as the company's

obligation in Article 74 of Law Number 40 of 2007

concerning Limited Liability Companies (Company

Law) on July 20, 2007 (UU Perseroan Terbatas No.

40 Tahun 2007, 2007) and Government Regulation

No. 47 of 2012 concerning Social Responsibility and

Environment of Limited Liability Companies (PP

47/2012)

According (Harahap, 2007), explained three (3)

form corporate social responsibility, “(a) Corporate

Philanthoropy, (b) Corporate Responsibility, dan (c)

Corporate Policy”.

In addition there are 5 (five) possible areas where

social responsibility is located, namely (1) Net Profit

Contributions, (2) Donations to the environment, (3)

Public Donations, (4) Donations to Human

Resources, (5) ) Product or Service Contribution.

According to Thomas W Zimmerer in a book

written by Suryana (2006: 18) there are several

kinds of accountability, namely: "

1) Responsibility to the environment,

2) Responsibility to employees,

3) Responsibility to customers,

4) Responsibility to investors,

5) Responsibility to the community "

Corporate Social Responsibility (CSR) is a

mechanism for an organization to voluntarily

integrate attention to the environment and socially

into its operations and its interactions with

stakeholders, which exceeds organizational

responsibility in the legal field. The company's

social responsibility is expressed in a report called

Sustainability Reporting. Sustainability Reporting is

reporting on economic, environmental and social

policies, the influence and performance of

organizations and their products in the context of

sustainable development.

3 RESEARCH METHOD

The data used by the author is secondary data,

namely annual report PT. Toba Pulp Lestari, Tbk in

2014-2017, company profile, company brief history,

company organizational structure. Sources of data

obtained through various sources, namely literature,

articles, internet sites relating to research conducted.

Data collection techniques in this study are

library documentation and study.The variable and

operational definition variable on this study is as

follows:

1. Corporate Social Responsibility (CSR) is a

concept that organizations, especially (but not

only), companies are having various forms of

responsibility towards all stakeholders,

including consumers, employees, shareholders,

communities and the environment in all aspects

company operations that cover economic, social

and environmental aspects

2. Profitability or ability to obtain profits is a

measure of the percentage used to measure the

extent of the firm to produce a level that can be

received. On research profitability is proxied by

ROA (Return on Assets)

Practice of Disclosure Accounting Social Responsibility

1187

The data analysis technique used in this study is

descriptive data analysis technique, which is an

analytical method that describes a situation

objectively, so as to obtain a solution to a problem

faced by the company.

4 ANALYSIS

The approach and stages of the PT CSR program.

Toba Pulp Lestari, Tbk namely Joint Community

Planning:

1. Hold a Meeting with Community Leaders and

Village Representatives.

2. Make an agreement on the type of program as

needed: Integrated Agriculture Program (IFS),

namely: livestock, fisheries, agriculture;

infrastructure; education; health and others.

3. Implement the program in accordance with the

agreement with the community.

The form of Corporate Social Responsibility

implemented by PT Toba Pulp Lestari is Community

Development

CSR program activities in 2014-2016:

- Community relation

- Community services

PT Toba Pulp Lestari's assistance in education in the

form of assistance in the right to grant scholarships

to outstanding students, and repair of elementary

school buildings in Pangombusan village, Siruar

Village, in Tangga Batu I village and development

of PAUD schools in North Siantar Village

-Community Empowering

Implementation programs related to providing wider

access to the community to support their

independence, such as the formation of cooperatives

managed by the community. And providing direct

assistance to the community such as giving

livestock, and assistance in agriculture.

The company management, sets the social costs

incurred by PT. Toba Pulp Lestari Tbk which is

equal to 1% of net sales. Comparison of social costs

to net sales from 2014 - 2016 can be seen in table 1

below:

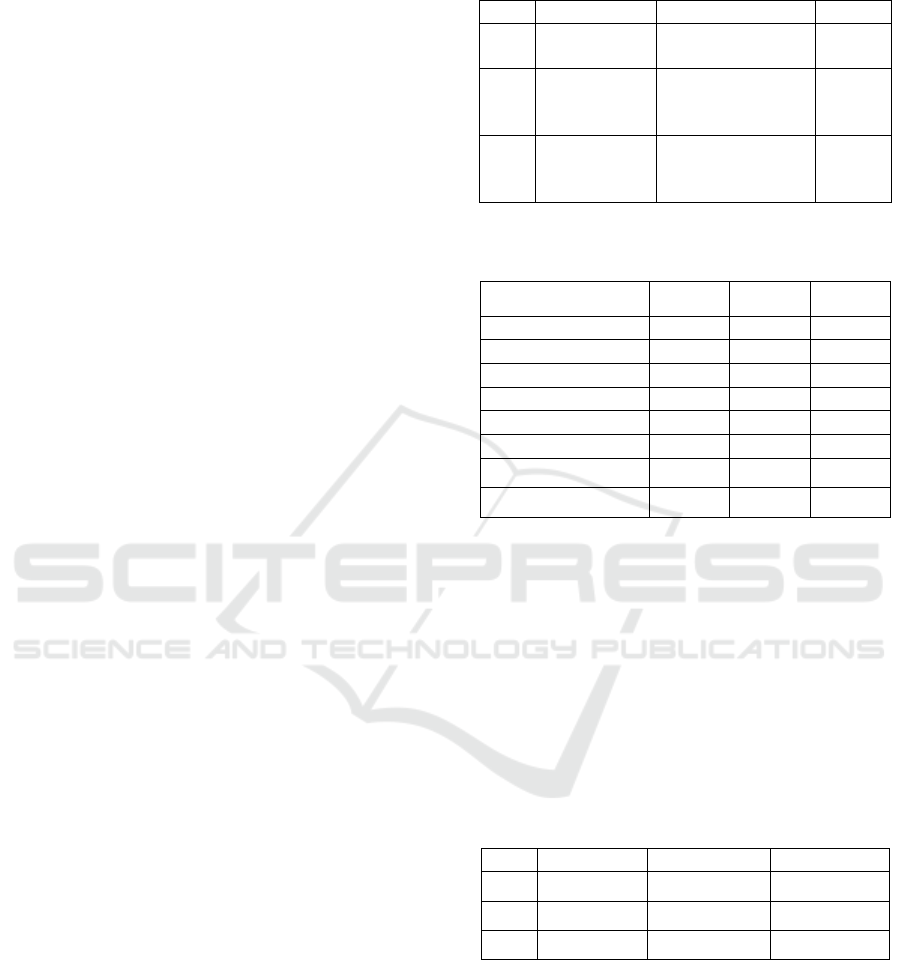

Tabel 1: PT. Toba Pulp Lestari, TbkComparison of social

costs to net sales Tahun 2014 – 2016

Year Net Sales Social Cost Proporsi

2014 Rp. 1.503.505.

018.608,99

Rp.

15.035.050.186,089

1 %

2015 Rp.

1.327.644.239.

093,14

Rp.

13.276.443.390,913

1 %

2016 Rp.

1.157.635.388.

115,83

Rp.

11.576.353.881,158

1 %

Tabel 2: CSR Disclosure PT. Toba Pulp Lestari, Tbk

2014-2016

Descriptions 2014 2015 2016

Economics 5 6 5

Environment 9 17 19

Labour 3 7 11

Human rights 0 0 0

Social 1 1 1

Product 0 0 1

Total 18 31 37

Index CSR 0.22 0.39 0.46

Of the overall indicators above, the results

obtained in 2014 were 18, 2015 had an increase of

31, and in 2015 had an increase of 37. For the CSR

Index obtained by the company in 2014 was 0.22. In

2015 it began to increase to 0.39. In 2016 also had

an increase from the previous year to 0.46

To measure company profitability by using

Return On Assets (ROA). ROA gives an idea of how

much efficient management is in using its assets to

generate profits

Tabel 3: Calculation of ROA at PT. Toba Pulp Lestari,

Tbk

Year Net Profit Total Aset ROA

2014 USD 1.575 USD 330.234 0,47 %

2015 (USD 2.752) USD 333.904 (0,824 %)

2016 USD 37.492 USD 339.428 11,046 %

Source : PT Toba Pulp Lestari, Tbk

5 RESULTS

PT Toba Pulp Lestari Tbk has been established since

1983 under the name of PT Inti Indorayon Utama in

Parmaksian District, this company is engaged in the

manufacture of pulp. Since the establishment of this

company, there have been many conflicts with the

UNICEES 2018 - Unimed International Conference on Economics Education and Social Science

1188

community. This happens because the company does

not carry out its corporate social responsibility

Since operating again in 2003 to become PT

Toba Pulp Lestari this company has a new paradigm

that will be run by the company. The company

implements Corporate Social Responsibility starting

from a commitment in the new paradigm in 2003

namely:

1. Use of environmentally friendly technology

2. Sustainable management of forest resources

3. Social responsibility:

a. Prioritizing the son of the local area

b. Cooperating with business partnerships

with local communities

c. Set aside funds for social contributions for

community development by 1% of Net

Sales per year

4. Accepting independent institutions to oversee

the implementation of the company's new

paradigm.

To implement CSR means the company will

spend a number of costs. Same is the case with PT.

Toba Pulp Lestari, Tbk, which annually issues CD /

CSR funds of 1% of net sales. This results in a level

of profitability that will affect and also affect the net

profit (loss) of the company.

The accounting treatment for the Company's

CSR is the CSR costs incurred by the company

listed in the company's profit and loss report which

shows that it is recorded as other expenses in the

company's profit and loss statement.

6 CONCLUSIONS

1. In general, CSR at PT. Toba Pulp Lestari has

been implemented based on the applicable

provisions, namely the provisions of Law

Number 40 of 2007 concerning Limited

Liability Companies as a regulation that covers

the implementation of CSR corporate social

responsibility in Indonesia and Government

Regulation Number 47 of 2012 concerning

Social and Environmental Responsibilities of

Limited Liability Companies as regulations

implementation.

2. The implementation of the PT. Toba Pulp

Lestari, Tbk with a variety of programs

implemented, namely the use of

environmentally friendly technology,

sustainable forest resource management,

prioritizing local area sons to become company

employees, conducting business partnerships

with local communities, setting aside funds

contributing an average of 1% of net sales per

year as social costs incurred

3. The CSR of PT Toba Pulp Lestari has a role in

community welfare including:

a. Through Community Relations

b. Through Community Service

c. Through Community Empowering

4. Implementation of corporate social

responsibility or CSR of PT. Toba Pulp Lestari

as a whole has had a positive influence on the

community, both communities around the area

of the company operate

5. It can be concluded that social accounting or

accounting for social responsibility is a report or

new obligation that must be included in the

financial statements of each company which

will be a reflection or description of the

condition of the company in the short term and

especially the long term.

REFERENCES

Agus, S. dan C. A. (2011) Etika Bisnis dan Profesi.

Jakarta: Salemba Empat.

Belkaoui, Ahmed Riahi, 2006. (2006) Accounting Theory.

5th edn. Jakarta: Salemba Empat.

Drever, M. S. P. and M. G. S. (2016) ‘Contemporary

Issues in Accounting’, in Mehmet Huseyin Bilgin,

Hakan Danis, Ender Demir, U. C. (ed.) Eurasian

Studies in Business and Economic. London: Springer,

p. 55. doi: 10.1007/978-3-3-19-22596-8.

Ghozali, Imam, dan Chariri, A. (2007) Teori Akuntansi.

4th edn. Semarang: Badan Penerbitan Universitas

Diponegoro.

Gray, Rob, R. dan S. L. (1995) ‘Corporate Social and

Enviromental Reporting’, Emerald Insight Journal,

8(2), pp. 47–77. doi: https://doi.org/10.1108/

09513579510146996.

Harahap, S. S. (2007) Teori Akuntansi. 4th edn. Jakarta:

Raja Grafindo Persada.

Lako, A. (2011) Dekonstruksi CSR dan Reformasi

Paradigma Bisnis dan Akuntansi. Jakarta: Erlangga.

Ralf, B. (2007) Legitimacy as A Key Driver and

Determinant of CSR in Developing Countries.

Amsterdam.

Tilling, M. V (2004) Refinements to Legitimacy Theory in

Social and Environmental Accounting. 1441–3906.

UU Perseroan Terbatas No. 40 Tahun 2007 (2007).

Indonesia: www.legalitas.org.

Practice of Disclosure Accounting Social Responsibility

1189