Analysis and Design AIS for Raw Materials Inventory

and Finished Goods Inventory in Accordance with ISO 9001:2015 at

Frozen Food Company

Syahni Tiska

1

and Yudho Giri Sucahyo

1

1

Faculty of Economics and Business, Universitas Indonesia, Jakarta -Indonesia

Keywords: Accounting information system, Inventory Control, ISO 9001:2015, FAST, Inventory, Contingency Theory

Abstract: The purpose of this study is to analyze and design accounting information system for raw materials

inventory and finished goods inventory in accordance with ISO 9001:2015 at PT. XYZ which is engaged in

frozen food industry. Data collection methods that have been used are interviews, observations and

literatures while the analysis method that has been used is qualitative research method. In this study, the

types of data used are primary and secondary data. Designing an accounting information system for raw

materials inventory and finished goods inventory at PT. XYZ will use FAST method (Framework for the

Application of System Thinking). In this study, there will be also explained about contingency theory,

accounting information systems, inventory control, system design tools, inventory, FAST, ISO and ISO

9001: 2015. The problem in this company is the differences between inventories recording and physical

stocks which is caused by manually inventories recording and unclear of segregation of duties. The results

of this study are expected to provide a design of accounting information systems for raw materials inventory

and finished goods inventory in accordance with the provisions of ISO 9001: 2015 (clause 8.5.1) that can be

used by the company to smooth inventories recording and the company's production process.

1 INTRODUCTION

In PSAK No. 14 (2015), inventories are assets

available for sale for business activities, assets in the

production process for the sale or assets in the form

of materials or equipment for use in the process of

production or service delivery. In a company,

inventory has an important role because it will affect

the level of production and the level of sales. There

are two problems in inventory that are very

important to note because of their relation to

production efficiency and sales optimization, namely

controlling raw materials inventory and finished

goods inventory.

PT. XYZ is a company engaged in the frozen

food industry. This company has been established

and operating since 2013. In this company, there are

two types of inventory, namely raw materials

inventory and finished goods inventory. As stated by

the Director of PT. XYZ, the company still manages

raw material and finished goods inventory data

manually. All activities in and out of raw materials

and finished goods are recorded using a stock card,

so that the inventory balance must be adjusted every

month after the stock taking.

Director of PT. XYZ also stated that inventory

activities often experience delays in reporting and

there are often errors in recording the transfer of

goods because there are various types of raw

materials and finised goods inventory. In addition,

the authorization of the entry and exit of inventory

should also be separated so that accountability

becomes clearer on inventory. Raw materials often

run out, even though there are still a lot of inventory

in stock card. This often makes raw materials

purchased not from major suppliers and prices often

change due to the impromptu purchase.

Designing accounting information system for raw

materials and finished goods at PT. XYZ is needed

because of the management of raw materials

inventory and finished goods inventory of PT. XYZ

is still manual. In designing AIS for the supply of

raw materials and finished goods in the company,

the author will follow the provisions in clause 8.5.1

on ISO 9001: 2015 related to "Production and

Provision of Service Control". ISO 9001: 2015 is an

Tiska, S. and Sucahyo, Y.

Analysis and Design AIS for Raw Materials Inventory and Finished Goods Inventory in Accordance with ISO 9001:2015 at Frozen Food Company.

DOI: 10.5220/0009506811411148

In Proceedings of the 1st Unimed International Conference on Economics Education and Social Science (UNICEES 2018), pages 1141-1148

ISBN: 978-989-758-432-9

Copyright

c

2020 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

1141

international standard for the implementation of

quality management, which is a strategic decision

for a company that can help to improve its overall

performance and become a strong basis for

sustainable development initiatives.

Therefore, the purpose of this study is to analyze

inventory control procedures that exist at PT XYZ

and design accounting information systems for raw

materials and finished goods inventory according to

ISO 9001: 2015.

2 THEORICAL FRAMEWORK

The main theory used in this study is contingency

theory. According to Duncan and Moores (1989),

contingency theory is a function of the compatibility

between the system and the environment an

organization operates. In addition, according to

Nicolaou (2000), contingency theory can support the

formation of the effectiveness of accounting

information systems. The effectiveness of an

information system is influenced by the effects of

technology, organizational structure and

environment. The effect of technology is closely

related to the use of information systems in an

organization and the effects of the environment and

organizational structure related to the performance

of employees working in an organization.

According to Diana and Setiawati (2011),

accounting information systems are systems that aim

to collect and process data as well as, report

information relating to financial transactions. On the

other hand, according to Krismiaji (2015),

accounting information systems are systems that

process data and transactions to produce information

that is useful for planning, controlling and

processing business. This is useful to be able to

produce information needed by decision makers.

System modeling consists of Use Case

Diagrams, Data Flow Diagrams (DFD) which are

translated into Context Diagrams, Level 1 and 2

Diagrams, Functional Decomposition Diagrams

(FDD), Entity Relationship Diagrams (ERD), and

user interface designs.

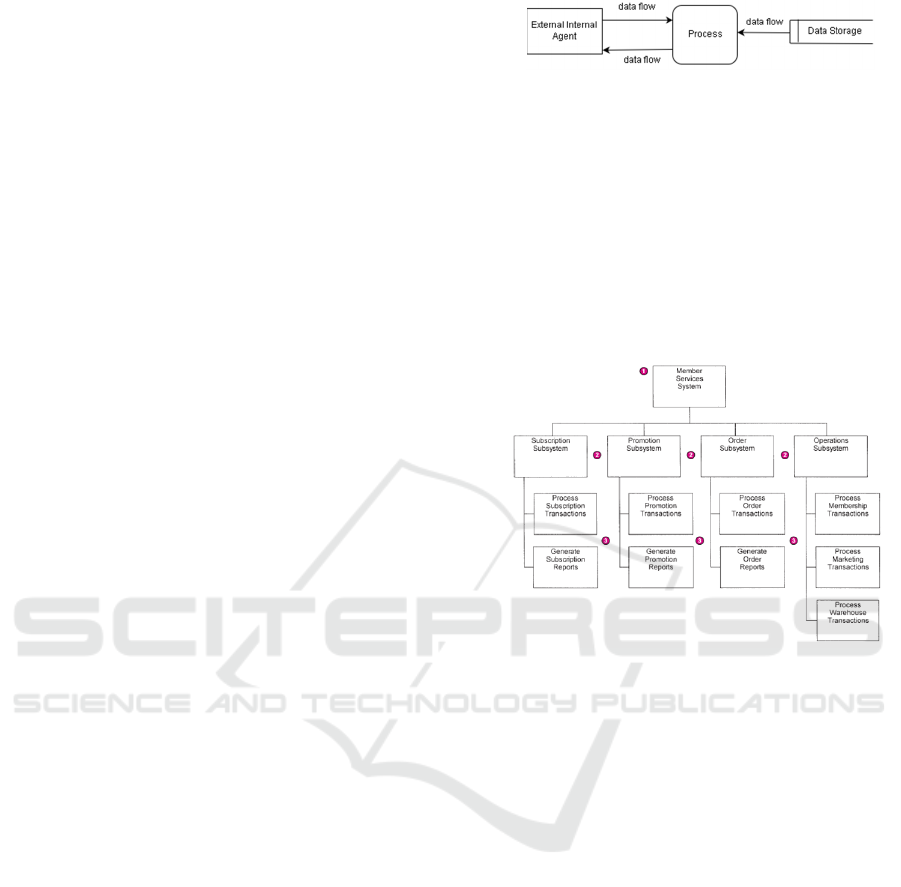

Data Flow Diagrams (DFD) is a process model

that is used to describe the flow of data in a system

that works supported by the system. All parties

involved in this system can see all systems working

continuously through DFD. DFD is indicated by a

context diagram which is then developed in a level 0

diagram. Figure 1 shows example of DFD:

Source: Bentley, Whitten & Dittman (2007)

Figure 1: Data Flow Diagram

Context Diagram is part of the Data Flow

Diagram which functions to map environmental

models represented by a single circle representing

the entire system.

Functional Decomposition Diagram (FDD) is a

tool used to describe the decomposition of functions

or activities of a system. Decomposition is breaking

a system into small partials or also called

subsystems. Figure 2 shows example of FDD:

Source: Bentley, Whitten & Dittman (2007)

Figure 2: Functional Decomposition Diagram

Entity Relationship Diagram is a data model that

uses many notations or also called cardinality

notations to describe data of an entity and the

relationships that occur between entities with each of

these data.

According to Romney and Steinbart (2011),

internal control is a process that is carried out to

provide adequate guarantees so that the control

objectives have been achieved. Internal control of

inventory becomes a difficult thing in management,

because the many threats that can cause inventory

cannot be calculated properly.

For the design of the system used FAST method

which according to Bentley, Whitten & Dittman

(2007) here are 8 phases namely Scope definition,

Problem analysis, Requirement analysis, Logical

design, Decision analysis, Physical design and

integration, Construction and Testing, Installation

and Delivery.

Viewed from the site iso.org, ISO (International

Organization for Standardization) is an international

standard setting body consisting of representatives

from the national standardization bodies of each

UNICEES 2018 - Unimed International Conference on Economics Education and Social Science

1142

country. ISO establishes world industrial and

commercial standards. One of them is ISO 9001.

ISO 9001 has undergone several revisions. The

latest ISO 9001 is ISO 9001:2015 and ISO was ISO

9001: 2008. As can be seen from the ISO 9001:2008

and ISO 9001:2015 documents issued by Badan

Standardisasi Nasional (2008) and Badan

Standardisasi Nasional (2015), there are clearly

visible differences from ISO 9001:2015 with ISO

9001:2008, which are neater clauses because they

are well grouped and attempt to eliminate the

impression that the application of ISO 9001 only

relies on making SOPs or procedures.

The focus of this research is using ISO

9001:2015 clause 8.5.1 where ISO 9001:2015 is also

called a quality management system which is a

strategic decision for a company or organization that

can help to improve its overall performance and as a

solid basis for initiatives for sustainable

development. Whereas clause 8.5.1 is a clause that

describes "Control of production and service

provision".

3 RESEARCH METHOD

This study uses qualitative research methods and a

case study approach in order to analyze and answer

the phenomenon in detail. The definition of

qualitative research is research that is used to

investigate, find, describe, and explain the quality or

features of social influences that cannot be

explained, measured or described through a

quantitative approach (Saryono, 2010).

In this study, data collection was carried out

through interviews, observation and documentation

(Fathoni, 2006).

Observations of company activities are carried

out especially in the supply of raw materials and

finished goods, to find out how the procedure for

recording inventory at PT. XYZ. Then, interviews

conducted with the operation staff, production staffs,

warehouse staffs, to find out more about matters

relating to inventory activities of raw materials and

finished goods. As well, interviews were also

conducted with the director of PT. XYZ, so that the

writer knows the comparison of information on the

existing conditions and the wishes of the company's

management of inventory accounting information

systems. Formal interviews that are allowed by the

company are only interviews with the operation staff

and director. In addition, documentation is carried

out to collect data or documents of PT XYZ, as well

as collect various references from books related to

accounting information systems for the supply of

raw materials and finished goods according to ISO

9001:2015.

The design of inventory information system at

PT XYZ applies FAST approach (Framework for the

Application of System Thinking). Generally, FAST

has 8 phases, but in this study will only use 4 phases,

namely (Bentley, Whitten & Dittman, 2007):

1. Phase Scope Definition, in this phase the

scope or boundaries of the project are

determined.

2. Phase Analysis Problem, in this phase we

study the existing system and analyze the

findings to provide the project team with a

deeper understanding of the problems that

trigger the project.

3. Phase Requirement Analysis, in this phase

the analyst approaches the users to find out

what they need or what they want from the

new system.

4. Phase Logical Design, in this phase

translation of business requirements into

system models is carried out. The system

model is a picture of a system that

represents the desired reality.

4 ANALYSIS

4.1 Analysis of PT XYZ's Raw Material and

Finished Goods Inventory Control

Procedures

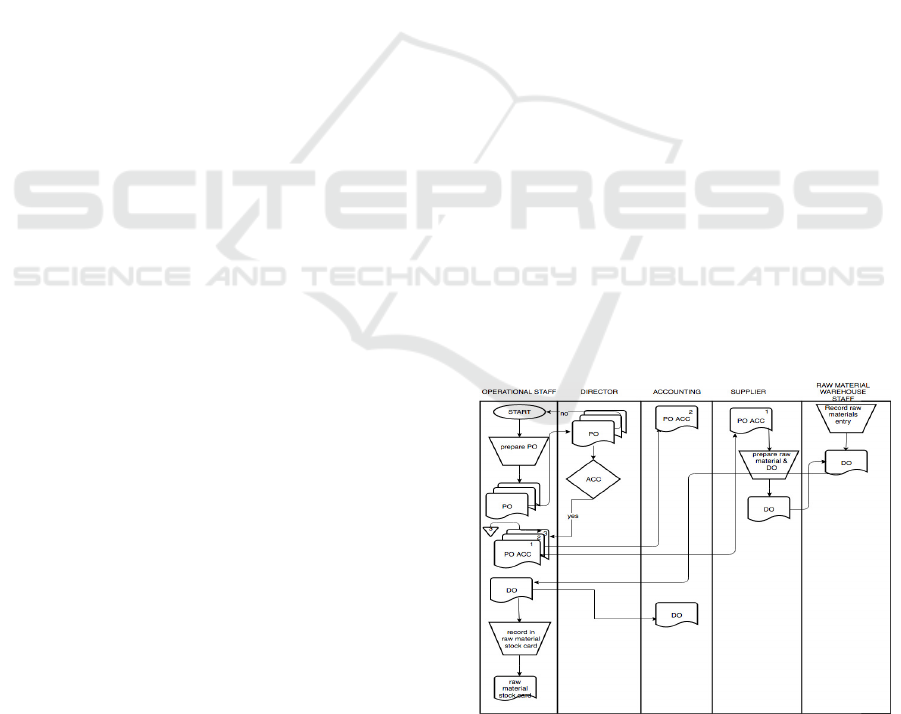

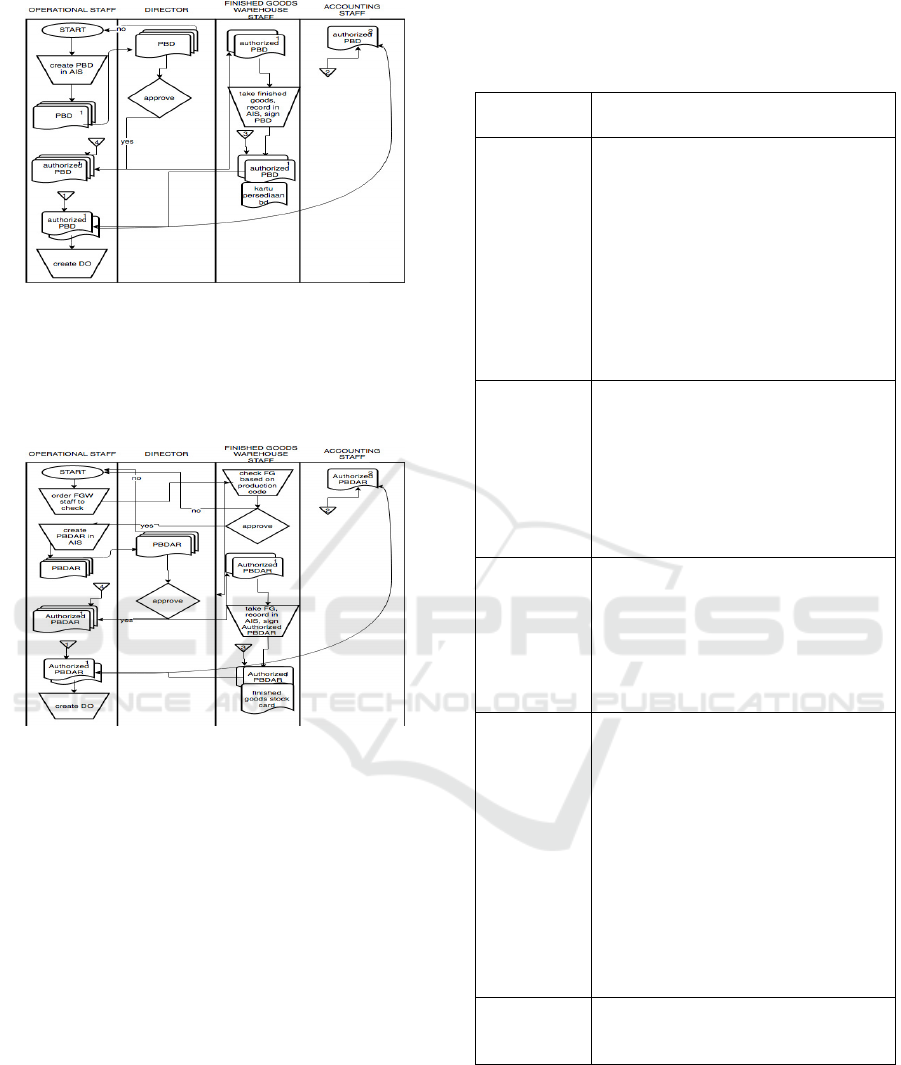

Figure 3 shows the procedure for Demanding raw

materials to supplier:

Figure 3:Procedure for Demanding Raw Materials to

Supplier

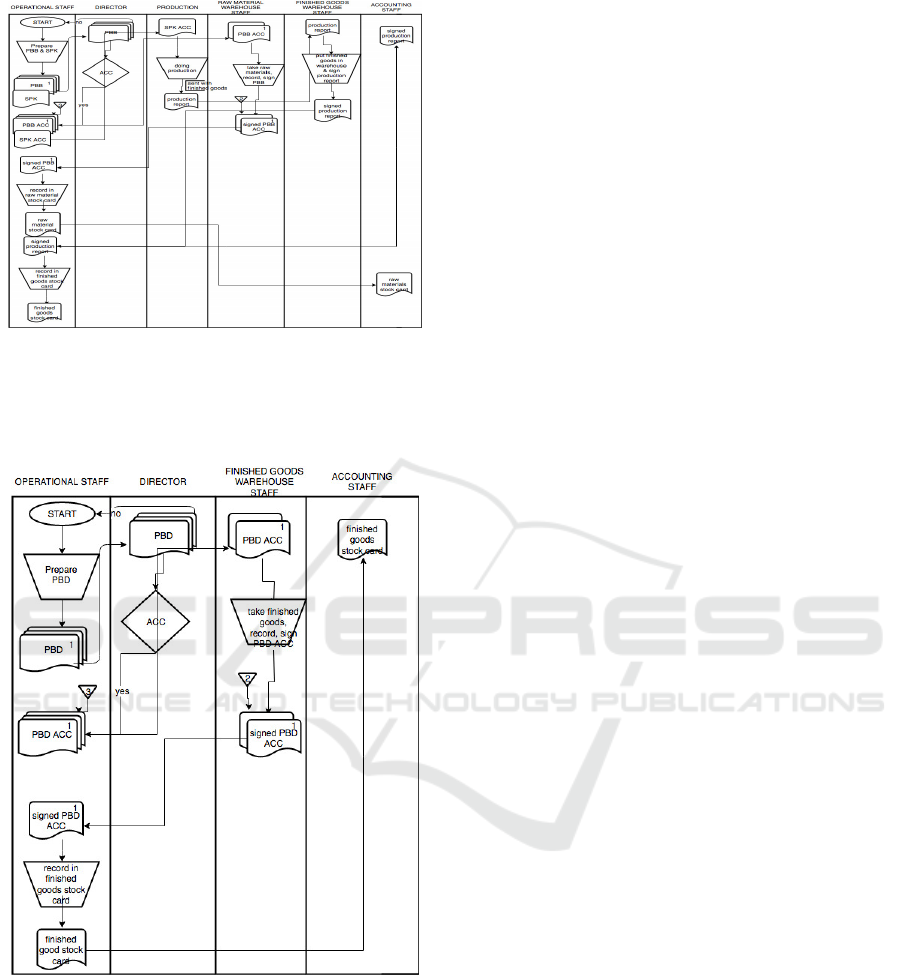

Figure 4 shows the procedure for Demanding raw

materials for production :

Analysis and Design AIS for Raw Materials Inventory and Finished Goods Inventory in Accordance with ISO 9001:2015 at Frozen Food

Company

1143

Figure 4: Procedure for Demanding Raw Materials

for Production

Figure 5 shows the procedure for Demanding

finished goods inventory:

Figure 5: Procedure for Demanding Finished Goods

Inventory

4.2 PT XYZ's Raw Material and Finished Goods

Inventory Control Procedure in Accordance

with ISO 9001: 2015

Before designing SIA for raw materials and

finished goods inventory at PT XYZ, we must first

pay attention to ISO 9001: 2015 clause 8.5.1 relating

to inventory control because this clause discusses

"control of production and service provision". The

organization must implement production and service

provision under controlled conditions, where

controlled conditions must include, as applicable:

o Availability of defining documented information

(product and service characteristics, results

achieved): For this condition, PT XYZ already

has a list of products with packaging,

documented criteria, and raw materials used also

have details for each product produced. Thus, the

SIA that will be designed will be made a

database of the amount of raw materials used, the

products produced and the results to be achieved,

all of which can be seen from the Daily

Production List (DPH) document. For product

characteristics without preservatives and halal,

details of suppliers that have passed the criteria

are listed in the system and orders can be made.

o Availability and use of monitoring in accordance

with the measurement of resources: PT XYZ has

carried out appropriate monitoring and

measurement of its resources properly, but they

were still less effectively and efficiently. Valid

resources for measurement are three things that

must be considered, namely measuring

instruments, inspectors and the environment.

First, the measuring instrument, the company

already has a prescription and the target of

production for each production, it's just still

manual so that there is a high probability of an

error. In AIS, a supplier database will be

designed in which the supplier that has passed

the criteria for halal products and BPOM

certified and its products without preservatives

are registered in the system. In addition, product

prescription databases are also made to ensure

that the products released from the raw material

warehouse and the results achieved are in

accordance with existing measurements.

The second thing is the inspector. The division of

work that is still unclear makes mistakes more

common. So, in this study a flowchart will be

made that shows the workflow and data for each

part so that the division of work is clearer.

Third thing, environment. The company already

has an environment that is suitable for everything

needed by inventory and production, such as dry

warehouses, cold warehouses and factories. It's

just that there are no restrictions on the access of

unauthorized parties to enter.

o Implementation of monitoring and measurement

activities at the appropriate stage to verify that

the criteria for controlling processes or output,

and acceptance criteria for products and services,

have been fulfilled: To meet these conditions, the

UNICEES 2018 - Unimed International Conference on Economics Education and Social Science

1144

AIS will have access restrictions in accordance

with the authority which each part has at each

stage.

o The use of infrastructure and environment that is

suitable for the operations of existing processes:

PT XYZ is divided into 4 buildings in the

company. Building 1 is the office where the

director, operation, accounting, and marketing

work. Building 2 is a factory where the

production department works. Building 3 is a

Cooling Warehouse. Building 4 is a Dry

Warehouse / Spice Warehouse. With the

existence of these 4 buildings, each part is given

different authority according to the existing

processes. Those who can only enter each

building are those who have the authority and of

course those who have access to the AIS system

that will be created only those who have

authorization.

o Appointment of competent people, including the

required qualifications: The selection of

employees in this company is of course through a

separate procedure in which each employee has

been given training according to their respective

positions. For the use of SIA, of course the

person appointed is who is able to use the

computer well and get certain trainings. In

addition, for product quality, the company also

has a nutritionist who monitors every product

produced.

o Periodic validation and re-validation, for the

ability to achieve planned results from processes

and service provision, where the output produced

cannot be verified by monitoring or

measurement: Stock taking activities are always

carried out by the company once every three

months. For stock taking activities, the running

process is still efficient and effective to be

carried out for the next few years, considering

the amount of costs that will be used if the stock

operation uses an RFID or barcode system.

Therefore, SIA is not designed for stock taking

activities. Stock taking activities will follow the

existing path where after the Accounting Staff

and Operation Staff perform stock taking

accompanied by the Warehouse officers, then the

inventory report is processed by Accounting staff

to see the difference with the existing inventory.

Then, Accounting staff makes a letter of

application for outgoing goods or incoming

goods so that the Operation staff create forms for

goods in or out. Furthermore, it will follow the

flow of goods demand in and out without having

to take or enter goods into the warehouse.

o Implementation of measures to prevent human

error: To fulfill this condition, an inventory

accounting information system is needed. With

SIA Inventory is expected to reduce the presence

of human error.

o Implementation of expenditure, shipping and

post-shipping activities: To meet these

conditions, SIA inventories will be designed to

document expenditure activities and post-

shipment activities.

5 RESULTS

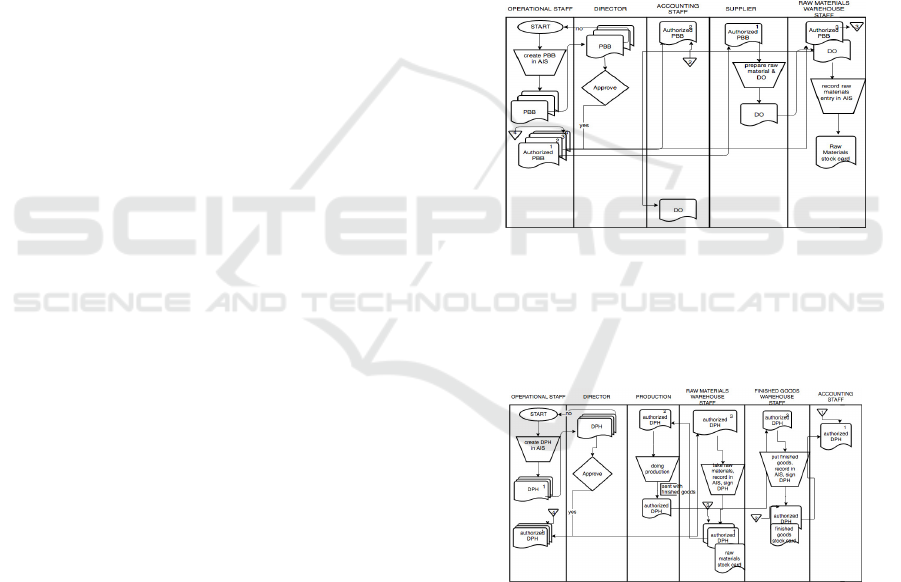

Figure 6 shows the procedure for ordering raw

materials to suppliers that are in accordance with

ISO 9001: 2015:

Figure 6: Procedure for Ordering Raw Materials to

Suppliers that are in accordance with ISO 9001:2015

Figure 7 shows the procedure for Demanding raw

materials for production that are in accordance with

ISO 9001: 2015:

Figure 7: Procedure for Demanding Raw Materials

for Production That are in Accordance with ISO

9001:2015

Figure 8 shows the Procedure for Demanding

Finished Goods for Production in accordance with

ISO 9001: 2015:

Analysis and Design AIS for Raw Materials Inventory and Finished Goods Inventory in Accordance with ISO 9001:2015 at Frozen Food

Company

1145

Figure 8: Procedure for Demanding Finished Goods

for Production in accordance with ISO 9001: 2015

Figure 9 the Procedure for Demanding Return of

finished goods according to ISO 9001:2015:

Figure 9: Procedure for Demanding Return of

finished goods according to ISO 9001:2015

Design of PT XYZ's Raw Material

Inventory and Merchandise

In the scope definition phase, the analysis was

conducted to identify problems and opportunities at

PT XYZ. Based on the results of discussions with

the Director and operational staff, the author

summarizes the problems faced by the company

using the PIECES framework (Performance,

Information, Economics, Control, Efficiency,

Service).

At the stage of problem analysis,

misinformation regarding the supply of raw

materials and finished goods is actually caused by a

manual recording system and the separation of work

that is still not appropriate. Therefore, the design of

an accounting information system that is in

accordance with ISO 9001: 2015 must be able to

store data accurately, eliminate the system of

recording manually and provide proper separation

on its part in the company to be able to access and

input data in the system.

Table 1: PIECES framework

Performance Calculation of raw material and

finished goods inventory automatically

Information (1) Information regarding the

amount of raw materials and

finished goods inventory is

inaccurate

(2) Information regarding the total

rupiah of raw material and

finished goods supplies is

inaccurate

(3) Data is inflexible – it is not easy

to meet new information needs

from stored data

Economics (1) Costs arising from the difference

in the calculation of raw

material and finished goods

inventories

(2) Cost arising from error in the

estimation of the repurchase of

raw materials which causes a

purchase not to fixed supplier

Control (1) The absence of accurate

information about the supply of

raw materials and finished

goods can trigger errors in

decision making

(2) Avoid fraud in the supply of raw

materials and finished goods

Efficiency (1) Without a system, it takes a lot

of people in charge and

documentation to produce

accurate information about the

supply of raw materials and

merchandise

(2) Without a system, costs arise

from the existence of a

difference in inventory value

(3) Without a system, costs arise

from the existence of errors in

decision making.

Service Accounting information systems are

expected to be compatible so that they

can help all parts of the company.

In the Needs Analysis Phase, Functional

Decomposition Diagrams (FDD) are designed to

describe the required components contained in the

system and sub-systems separately.

UNICEES 2018 - Unimed International Conference on Economics Education and Social Science

1146

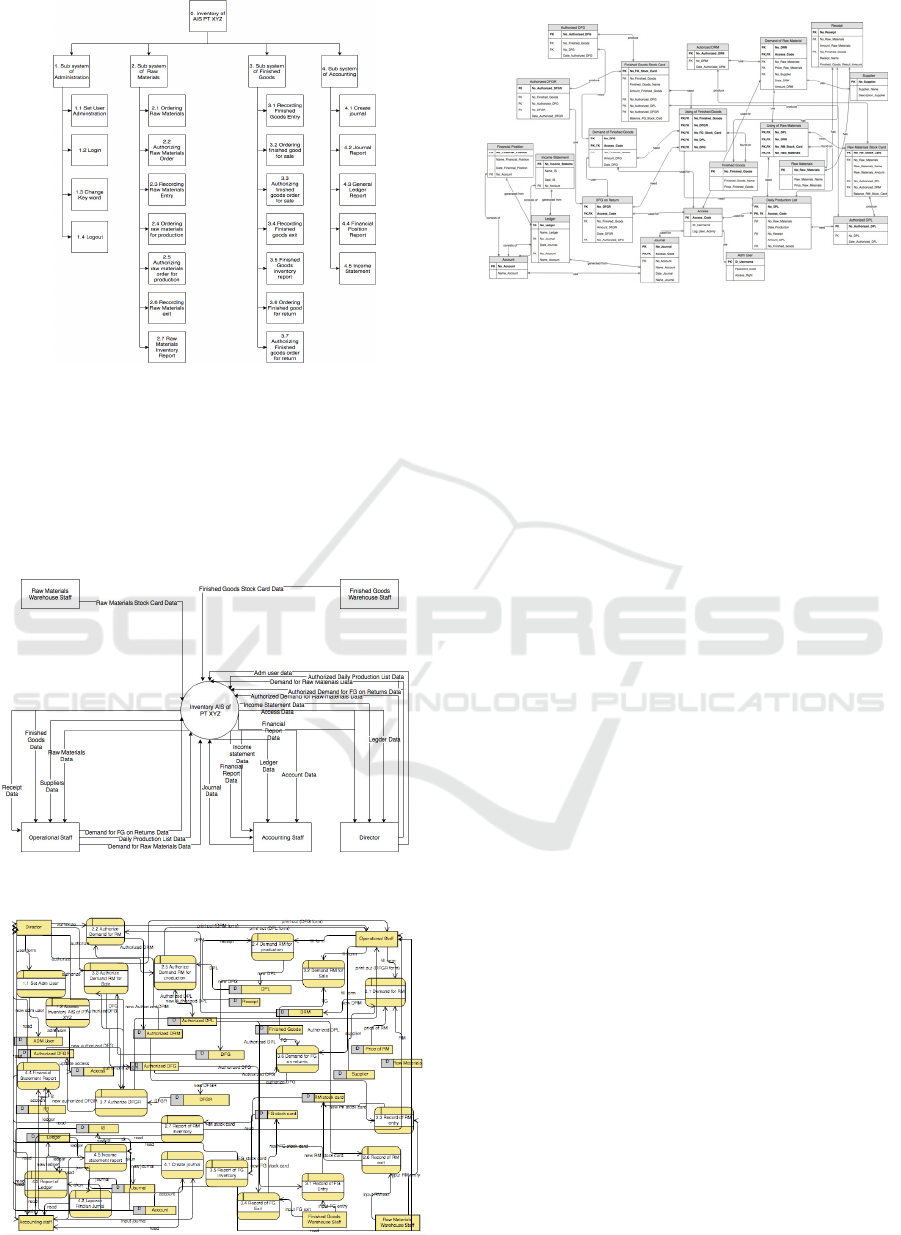

Figure 10: FDD of Inventory AIS PT XYZ

The logical design phase translates business

requirements into a system model. The system

model consists of logical data models that describe

business process requirements, data and information

needs, and interface needs.

1. Context Diagram

Figure 11: Context Diagram of Inventory

2. Data Flow Diagram

Figure 12: DFD of Inventory AIS PT XYZ

3. Entity Relationship Diagram (ERD)

Figure 13: ERD of Inventory AIS PT XYZ

6 CONCLUSIONS

The design of the inventory accounting

information system was made as one of the solutions

to the problems faced by PT XYZ in the company's

inventory control. In PIECES analysis, the

development of accounting information systems is

expected to overcome various problems, especially

those related to information. Information about the

supply of raw materials and finished goods is

expected to be more accurate and the data more

flexible, in order to become easily obtained after the

system is developed.

The inventory accounting information system

that have been designed certainly requires resources

for its operation. The system also requires a lot of

data that must be entered in accordance with the

section and its authorization, namely, the

Operational Staffs, Raw Material Warehouse Staffs,

Trade Warehouse Staffs, Accounting Staffs, and

Director.

The tool for documentation of system

requirements consists of FDD, DFD and ERD which

illustrates the need for inventory recording systems

to be developed for PT XYZ. However, of course

this does not rule out the possibility that other parties

or other similar companies use the results of

documentation of system requirements in this final

work. The system design can be changed according

to the user needs of the system and business

processes that exist in the system user organization.

REFERENCES

Badan Standardisasi Nasional. (2015). Sistem Manajemen

Mutu ISO 9001:2015. Jakarta: SNI.

Badan Standardisasi Nasional. (2008). Sistem Manajemen

Mutu ISO 9001:2008. Jakarta: SNI.

Analysis and Design AIS for Raw Materials Inventory and Finished Goods Inventory in Accordance with ISO 9001:2015 at Frozen Food

Company

1147

Bentley, L., Whitten, J. and Dittman, K. (2007). System

Analysis & Design for Global Enterprise. 7th ed. New

York: McGraw Hill.

Diana, A & LS. (2011). Sistem Informasi Akuntansi.

Yogyakarta: Andi Offset.

Duncan, Keith, Moores K., (1989). Residual Analysis: A

Better Methodology for Contingency Studies in

Management Accounting. Journal of Management

Accounting Review.

Fathoni, Abdurrahmat. (2006). Metodologi Penelitian dan

Teknik Penyusunan Skripsi. Jakarta: PT Rineka Cipta.

ISO. (2018). Standards. [online] Available at:

https://www.iso.org/standards.html [Accessed 18 Nov.

2018].

Krismiaji. (2015). Sistem Informasi Akuntansi. Jakarta:

Salemba Empat.

Nicolaou, Andreas I. (2000). A Contingency Model of

Perceived Effectiveness in Accounting Information

Systems: Organizational Coordination and Control

Effects. Journal of Accounting Information Systems

Vol 1, Issue 2.

Romney, M. B., Steinbart, P. J. (2011). Accounting

Information System (12

th

ed.). New Jersey: Pearson

Prentice Hall.

Saryono. 2010. Metodologi Penelitian Kualitatif dalam

Bidang Kesehatan. Yogyakarta: Nuha Medika.

UNICEES 2018 - Unimed International Conference on Economics Education and Social Science

1148