Designing System for Employee Performance Allowance Calculation

using Pay for Performance

Sari Harto Kusumo

1

and Trisacti Wahyuni

1

1

Faculty of Economics and Business, Universitas Indonesia, Jakarta-Indonesia

Keywords: Management Accounting Control System, Pay for Performance, Employee Performance Allowance

Abstract: This study aims to propose the calculation of employee performance allowance system design using Pay for

Performance (PFP) at Agency X. PFP helps in producing reliable data in evaluating employee performance

such as the existence of supporting evidence for the performance performed by employees and must be

included to meet criteria promotion based on the credit number unit specified in the applicable rules.

Agency X is a work unit that is responsible to the Minister through the Secretary General and headed by the

Chief. Agency X itself has the task of carrying out guidance and management of information systems, data

management, and analysis and presentation of data and information. The non-optimal employee

performance allowance payment will result in an inefficient payment system for employee salaries. If the

agency's performance is not effective but the costs paid are high, it can be said that the agency is not

efficient in managing its costs. There are some employees who have not received a promotion even though

they have exceeded a certain period of work because the employee has not fulfilled the determined

performance but receives a full performance allowance. PFP is part of the Management Accounting Control

System (MACS). MACS helps decision makers in determining whether strategies, objectives, levels of

organization, business, and operations can be fulfilled. PFP can be applied as a control system to overcome

the problem of the gap of interests faced by Agency X. This study uses qualitative methods with a case

study approach. Data collection and analysis using research instruments, interviews, documentation, and

content analysis. The benefit of this research is to evaluate and provide solutions to the causes of problems

and provide a basis for making decisions to change the current employee performance allowance calculation

system to be more efficient.

1 INTRODUCTION

Reforms carried out in the field of planning and

budgeting began in 2005 with reference to Law

Number 17 of 2003 concerning State Finance and

Law Number 25 of 2004 concerning the National

Development Planning System. The reformation was

to emphasize that work plans and budgets must be

prepared using a performance-based budgeting

approach by considering the suitability of funding

(Cost) with the expected results to provide

information about the effectiveness and efficiency of

activities. This study discusses the Institution X,

namely a stakeholder in one of the sectors

contributing the largest PBD in the Indonesian

economy. The performance of the sector is

generated from the support of the provision of data

and information as a basis for making decisions and

policies to adjust business activities in the sector.

Employees at Institution X are Functional

Officials who are Civil Servants (PNS) that are

given full duty, responsibility, authority and rights

by the authorized officials to carry out activities

based on certain expertise and / or skills and are

independent. The performance of functional officials

is measured using credit point units. Credit points

are units of value for each item of activity and / or

accumulated values of items of activity that must be

achieved by functional office holders for established

career guidance (PP 16, 1994). Institution X

Employee Performance Allowance that has been

compiled is not in accordance with the expected

results that are predetermined employee

performance. This was also supported by the results

of interviews which stated that there were several

1122

Kusumo, S. and Wahyuni, T.

Designing System for Employee Performance Allowance Calculation using Pay for Performance.

DOI: 10.5220/0009505711221127

In Proceedings of the 1st Unimed International Conference on Economics Education and Social Science (UNICEES 2018), pages 1122-1127

ISBN: 978-989-758-432-9

Copyright

c

2020 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

employees who had not received a promotion even

though they had exceeded a certain period of work

because these employees had not fulfilled the set

performance and in that period they received full

Performance Allowance. There are also complaints

that the current performance allowance calculation

system is considered unfair because these employees

feel that they have different performance from one

another, but the performance they mean is not seen

in the performance allowance calculation system.

With the broad scope of responsibilities and the

variety of mandated assignments, Institution X has

the urgency to implement a control system that can

reduce interest gaps and improve employee

performance in accordance with agency expectations

that is a Pay for Performance system. With the

calculation of employee performance allowance

costs that will be adjusted to the performance

produced so that unit costs to produce performance

will be reduced when compared with without using

the Pay for Performance control system.

2 THEORICAL FRAMEWORK

In the control process that has meaning and

credibility, the organization must have the

knowledge and ability to be able to improve the

uncontrolled situation. If this is not done, then

control does not have a goal (Atkinson, 2012). The

scope of MACS must be comprehensive and cover

all activities throughout the organization's value

chain. For example, many MACS measure and

assess performance only in one part of the value

chain of the actual production process or process. In

this case, supplier performance, design activities,

and post-production activities related to products

and services are neglected. Without a comprehensive

set of information, managers can only make limited

decisions (Atkinson, 2012).

The term "Pay for Performance" (hereinafter

abbreviated as PFP) refers to a payment strategy in

which performance evaluations performed by each

employee in the organization have a significant

influence on the amount of salary increases or

bonuses given to each employee itself. However,

institutions should not rely solely on monetary

motivational abilities to improve the performance of

individuals or organizations because with more and

more employees motivated by these monetary

factors (Merit Systems Protection Board, 2006).

By motivating individual employees, incentive

schemes are expected to increase performance

satisfaction, improve interpersonal relations, lower

absenteeism and material waste or capital, and

reduce turnover rates. It must also be able to produce

long-term effects on company performance. (Bryson

al, 2012. In order for PFP to work efficiently in two

processes, compensation management and

performance management must function properly.

Not only separately but also can operate together as

an integrated system. Compensation management

requires an accurate assessment of the performance

management system to realize its maximum

potential. Whereas to achieve the full benefits of

performance management a well-managed

compensation system is needed. (Summers, 2005).

Before we can implement PFP systems in

organizations, according to the Merit Systems

Protection Board (2006) there are several steps or

general questions that must be understood by the

organization to be able to design the system

optimally. The steps include:

1. What is the purpose of implementing the PFP

system?

2. Who should receive the PFP payment?

3. When is the right time to implement the PFP

system?

4. What should be given as a form of appreciation

for its performance?

5. How should employees be rewarded for their

performance?

6. Who provides input on employee performance

ratings?

7. How can institutions facilitate the integrity of the

PFP system?

Government Agency Performance

Accountability System (SAKIP) is carried out in the

framework of preparing Performance Reports in

accordance with the provisions of the law. The

implementation is carried out simultaneously and in

accordance with the implementation of Government

Accounting Systems (SAP), control procedures, and

evaluation of the implementation of development

plans. The implementation of SAKIP in state

ministries / institutions is carried out by Performance

Accountability entities in stages with entity levels

Accountability for Work Unit Performance,

Organizational Units and State Ministries /

Institutions (PP No. 29, 2014).

The State Civil Apparatus (hereinafter

abbreviated as ASN) in Indonesia consists of several

types namely Civil Servants (PNS) and Government

Employees with Employment Agreements (PPPK).

Civil servants themselves are ASN employees who

are appointed as permanent employees by the

Personnel Development Officer and have a national

employee ID number (NIP). In functional positions,

office holders are classified back into two parts,

namely functional positions in terms of expertise and

Designing System for Employee Performance Allowance Calculation using Pay for Performance

1123

functional positions of skills (UU No. 5, 2014,

Article 18).

The work performance appraisal of civil servants

is carried out to ensure the objectivity of the PNS

career development and system based on the work

performance system (PP No. 46, 2011 Article 2, 3

and 4). The performance appraisal of civil servants

is carried out based on principles that are objective,

measurable, accountable, participatory and

transparent. The performance appraisal of civil

servants themselves consists of two elements, that

are:

a) SKP; and

b) work behavior.

Employee Work Objectives (hereinafter

abbreviated as SKP) are a work plan and targets to

be achieved by a civil servant. Every civil servant

must prepare SKP based on the agency's annual

work plan where the SKP contains all activities on

the assignment of tasks and targets that must be

achieved in a measurable period of time, which is set

every year in January. The prepared SKP must be

approved and determined by the appraisal official

(PP No. 46, 2011 Article 5).

As if management in a company in managing its

resources, the Indonesian government system also

regulates the management of ASN especially for

civil servants for the continuity of government

activities. ASN management is a management

system in a government system that functions to

produce professional ASN employees, have basic

values, professional ethics, free from political

intervention, clean from the practices of corruption,

collusion and nepotism (UU No. 5, 2014 article 1).

The work performance appraisal of civil servants is

carried out to ensure the objectivity of the PNS

career development and system based on the work

performance system (PP No. 46, 2011 Article 2, 3

and 4).

3 RESEARCH METHOD

This study uses a qualitative approach with a case

study method, that the approach is carried out to get

information in more depth and detail on the object of

research. The case study approach according to Yin

(2012) aims to explain the present situation to

answer how and why of a phenomenon. Subandi

(2006) states that case studies are one type of

qualitative research that fully and deeply

comprehends a case.

This research was conducted in Institution X

which is a work unit that is responsible to the

Minister through the Secretary General and led by

the Chief. Institution X itself has the task of carrying

out guidance and management of information

systems, data management, and analysis and

presentation of data and information. In this study,

Institution X employees became the object of

research and the unit of analysis was the actual

source of information both for companies,

organizations, individuals, and so on.

Data collected is primary and secondary, where

the data is available from search results and the

process of further collection of data that can be

accessed or which is not accessible to the public.

The research instruments used in this study were

observation, interviews, documentation, and content

analysis. Content analysis important to be done

because in the document regarding rules and

procedures for giving employee incentives, an

analysis is still needed to obtain the information

needed in order to evaluate and propose the design

of a pay for performance system for the Institution

X.

4 ANALYSIS

This study aims to produce a system implementation

design for the calculation of performance allowance

costs. The application of the system uses the Pay for

Performance method which will be carried out at

Institution X with several stages, those are:

a. The purpose of implementing the Performance

Based Incentive system.

b. Parties who receive payment for Performance

Based Incentives.

c. The right timing in implementing a Performance

Based Incentive system.

d. What actions should be given as a form of

appreciation for performance.

e. The process of awarding employee

performance.

f. Parties who can provide input on employee

performance ratings.

g. Procedures carried out by the institution in

facilitating the integrity of the Performance

Based Incentive system.

4.1 The Purpose of Implementing the

Performance based Incentive System

It is also important to remember that the impact of

changing systems into PFP will affect organizational

UNICEES 2018 - Unimed International Conference on Economics Education and Social Science

1124

culture because it is important for organizations to

maintain harmony between organizational values

and performance payment strategies. The purpose of

implementing incentives based on performance in

Agency X is to equalize the interests of employees

and employers. The expectation of the employer is

the achievement of the performance produced by the

employee, while the expectation of the employee is

the provision of incentives in the form of monthly

allowances. So that with the implementation of the

system for calculating the performance allowance,

the provision of incentives is based on the

performance produced by employees.

4.2 Parties Who Receive Payment for

Performance based Incentives

To select appropriate coverage, the organization

needs to decide what message the PFP system wants

to be delivered to employees, including what must

be measured and how. Calculation of costs for

Institutional X performance benefits is based on

several components, the first is employee work

discipline with a weight of 60%. This gives the

message that discipline is one of the important

indicators for employers of employees. The second

component is the achievement of credit numbers set

by the employer with a weight of 40%. Credit

numbers are units of value for each item of activity

and / or accumulated values of items of activity that

must be achieved by Functional Officials in the

context of career development. This shows that

performance achievements are also important things

to be achieved by employees in order to get their

rights to incentives every month.

4.3 The Right Timing in Implementing a

Performance based Incentive System

Simultaneous application may look better if the

organization is able to convey dramatic messages of

organizational change and foster a sense of

solidarity. Implementing a PFP system

simultaneously can also avoid confusion and

difficulties that arise related to the administrative

system in an organization. The system of calculating

the performance allowances can be applied to all

existing Functional Officers but in this case the

application should be carried out in stages using a

pilot project by functional statistics officials where

the group of employees is the employee in charge of

providing data and information relevant to

Institution X decision making.

4.4 What Actions Should Be Given as a Form

of Appreciation for Performance

Evaluation of the criteria for performance standards

of Agency X employees on the calculation of

performance allowance costs can be described in the

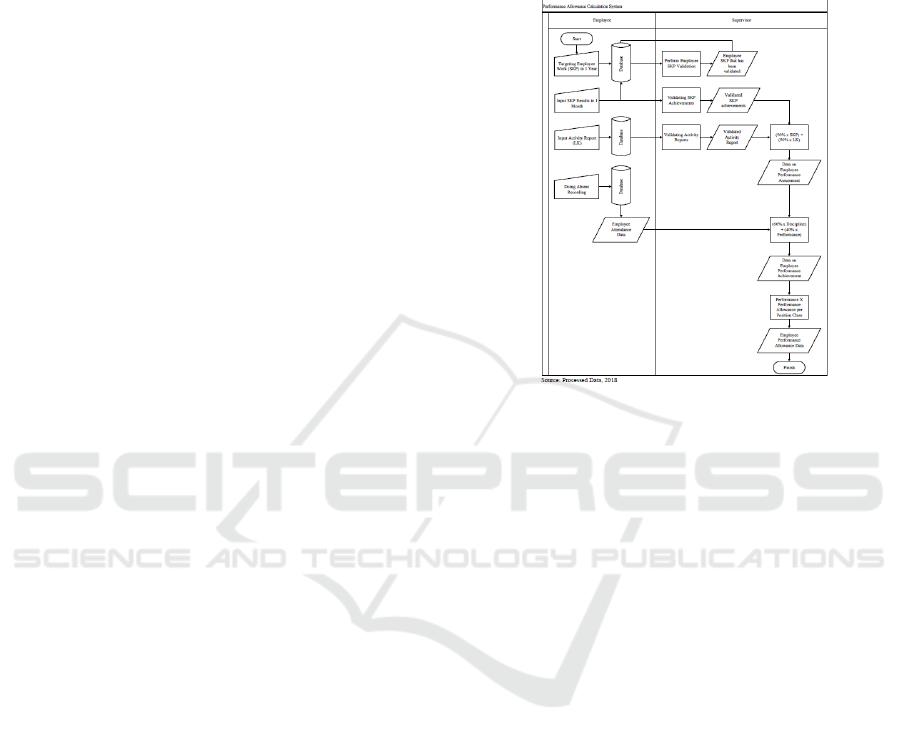

flowchart in Figure 1.

Figure 1: Current Institution X Performance

Allowance Calculation System

In the flowchart, it explains how the overall cost

calculation process and the value components that

affect the receipt of incentives are in the form of

Employee Performance Allowance. The flowchart is

a general description of the process that is currently

in effect and is still practiced to date, and will further

be reviewed both the details and weaknesses of the

system which can have a negative impact on the

organization. There are weaknesses that arise in the

current system, that is, the monthly SKP

achievement target is determined in units of

percentages which causes information that is not

reliable because it is not supported by sufficient

evidence. This is of course a factor that can increase

the negative risk for the interests of the organization

because the organization cannot objectively assess

the truth of the employee SKP that is actually done,

so that the assessment of employee performance

becomes biased.

4.5 The Process of Awarding Employee

Performance

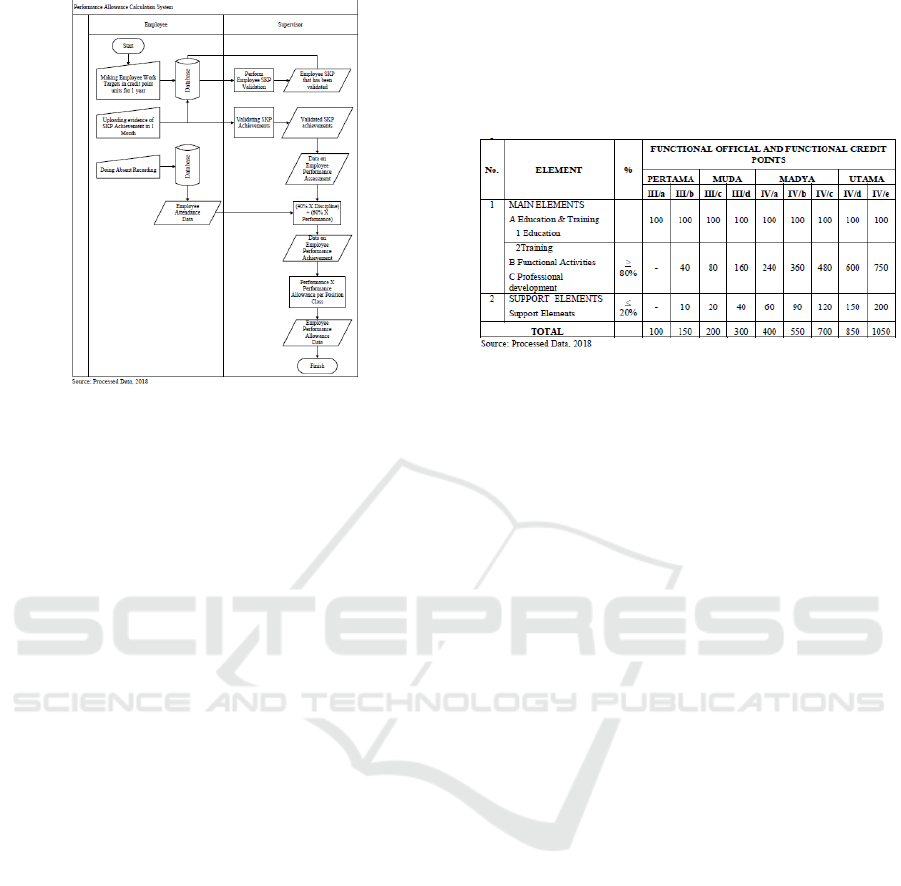

Figure 2 Proposed Performance Allowance

Calculation System Institution X which is the

proposed flowchart for the calculation of the

Institution X's current performance allowance costs

described earlier in Figure 1.

Designing System for Employee Performance Allowance Calculation using Pay for Performance

1125

Figure 2: Proposed Performance Allowance

Calculation System Institution X

In Figure 2 describes some solutions to the

weaknesses that arise in the current calculation

system. The solution includes removing the grading

system using a percentage of activity reports that are

considered not transparent. In addition, the proposal

to use credit numbers is used as an evaluation tool

that can be justified because it is accompanied by

supporting evidence in the form of uploading actual

activity documents. In addition, the weight of the

SKP value is the dominant factor in determining the

value of employee performance benefits which is

equal to 60%.

4.6 Parties Who Can Provide Input on

Employee Performance Ratings

Such input can come through various levels

including first-level supervisors, second-level

managers, employee colleagues and customers, also

directly from employees. This can be achieved by

using a 360-degree feedback instrument that

includes input from higher levels of staff,

colleagues, subordinates, and / or scorecards that

include the results of assessments and feedback that

can help ensure the organization that input from

various parties becomes so meaningful and cannot

be ignored.

At Institution X, the instrument that fits in

covering the overall performance of employees is

using a score card. Scorecard can be a tool that is

transparent, objective, and reliable in displaying

overall employee performance. Before knowing how

to form a scorecard in accordance with the

implementation of employee performance at

Institution X, first it will be explained about the

number of cumulative credit points in Table 1.

Table 1: Number of Cumulative Credit Points for

Promoting Functional Official with Bachelor (S1) /

Diploma IV Education.

The table shows that in order to get promotions

regularly, each employee must collect credit points

for the cumulative credit point for higher level

positions minus the cumulative credit point of the

current position level which is generally taken for

four years with a minimum value of 80% for the

element main and maximum 20% for supporting

elements. So, for each year each employee must

collect 25% of the total credit amount that must be

collected for four years and must be paid in

installments every month where the monthly

performance allowance will be given according to

the performance achievements of each employee.

4.7 Procedures Carried Out by the Institution

in Facilitating the Integrity of the

Performance based Incentive System

Organizations can take a number of steps to evaluate

the integrity of their compensation system, even

when significant oversight policies have been built

into the structure. Therefore, building protection

from within the system from the start is very

important for the long-term acceptance and

feasibility of the PFP system.

Based on the explanation of several important

aspects in the performance appraisal, the first thing

that can be done objectively by the appraiser or in

this case Institution X is the direct supervisor as the

appraiser, the first is to use the basic rules that apply

to credit numbers. Second, the assessment is carried

out transparently and accountably because it is

carried out in the system and well documented so

that each party can evaluate each other. It also serves

to eliminate the statement of employees who feel the

performance appraisal is done unfairly. Third, the

results of the results must be monitored and

validated by the direct supervisor. Fourth, at the end

of the credit collection period for promotions, an

independent team evaluates the adequacy of the

UNICEES 2018 - Unimed International Conference on Economics Education and Social Science

1126

requirements for the promotion of the employee

concerned.

5 RESULTS

After conducting research to find out how the

application of the performance allowance cost

calculation system at Institution X uses the Pay for

Performance method, it can be concluded that

Institution X still needs system renewal in

determining the standard of performance allowance

calculation for each employee. The standard that can

be used for functional officials is to use a system

credit point. The credit point system is considered

capable of describing various activities that must be

fulfilled by employees in fulfilling and improving

their performance. With the increase in performance,

the institution's goals can be fulfilled so that the

awarding of employee performance can be better

realized. Therefore, the PFP is considered competent

enough in measuring the performance of Institution

X employees for the future.

6 CONCLUSIONS

The development of a performance-based incentive

system can be a solution to the problems faced by

Institution X. In the analysis of performance-based

incentives in Analysis, the development of a

calculation system is expected to overcome a variety

of problems, especially complaints related to the

calculation of performance appraisals and

performance allowances that are not reliable,

inaccuracies in the calculation of the activities to

fulfill employee promotion and the gap of interest

between employees and employers. Information that

was previously not accountable and not in

accordance with applicable rules became easily

accepted and accountable after the system

development was implemented later.

The performance-based incentive system

designed in Analysis equires consistency with the

institution's compliance with the applicable rules,

one of which is a calculation based on the credit

point unit in evaluating performance in order to

determine the amount of performance allowances to

be received by employees. This system requires

consistency by system users, that are employees and

supervisors at Institution X. An incentive system

based on performance also helps Institution X to

produce reliable data in evaluating employee

performance such as the existence of supporting

evidence for the performance that has been

performed by employees and must be included for

fulfillment the criteria for promotion are based on

the credit point unit specified in the applicable rules.

REFERENCES

Atkinson, Anthony A, Robert S. Kaplan, Ella Mae

Matsumura, & S. Mark Young. (2012). Management

Accounting. Sixth Edition. Pearson.

Bryson, Alex, Richard Freeman, Claudio Lucifora,

Michele Pellizzari, & Virginie Perotin. (2012). Paying

for Performance: Incentive Pay

Schemes and Employees'Financial Participation. Centre

for Economic Performance, London School of

Economics and Political Science.

Merit Systems Protection Board. (2006). Designing an

Effective Pay for Performance Compensation System.

Subadi, Tjipto (2006). Metode Penelitian Kualitatif.

Cetakan kedua. Surakarta; Penerbit Universitas

Muhammadiyah.

Summers, Lynn. (2005). Integrated Pay for Performance:

The High-Tech Marriage of Compen-sation

Management and Performance Management.

Compensation Benefits Review. 37(1).

Yin, Robert K. (2012). Case Study Research: Design and

Method. Fifth Edition. Sage Publications.

Designing System for Employee Performance Allowance Calculation using Pay for Performance

1127