Strategy and Performance Measures of Information Technology

in the Enhancement of Financial Management Internal Control,

Ministry of Public Works and Housing

Obeth Simatupang

1

and Binsar Simanjuntak

1

1

Faculty of Economics and Business, Universitas Indonesia, Jakarta-Indonesia

Keywords: Information Technology Strategy and Performance Measures, Internal Control of Financial Management

Abstract: To be able to survive amid intense organizational competition, Small Medium Entrepreneurs (SMEs)

require strategies to improve the quality of products/services offered. Quality improvement is clearly needed

so that companies have high competitiveness. Good product/services can be produced by good internal

processes. ISO 9001 Quality Management System is a framework that has been used extensively by SMEs

to ensure the quality of the process. But not a few SMEs have successfully implemented and obtained QMS

certification. Many factors influence the process of implementing ISO 9001 QMS, especially in the context

of SMEs that have many limitations. This study aims to test the validity and reliability of scale for

implementing ISO 9001’s Critical Factors in SMEs level. The method used is a quantitative survey of four

SMEs that have successfully implemented and obtained ISO 9001 certification. Data from the survey were

analysed using the Aiken approach to show the level of validity and reliability. The results showed that of

the 20 items tested, only 19 items were met the criteria. Item of Employee Acceptance was eliminated from

scale because the implementation of ISO 9001 is mandatory for all stakeholders so the factors could be

ignored.

1 INTRODUCTION

Government continues to give attention to build

public works and housing infrastructure in

Indonesia. It gives impact to the increasing budget of

Ministry of Public Works and Housing (PUPR) from

year to year. The budget of PUPR for 2018 has

increased 91% compared to 2011 (State Law, 2017).

PUPR implements internal control in carrying out its

duty, it includes in the field of financial

management.

The audit result from Indonesian Supreme Audit

Institution (BPK-RI) has pointed that there are still

weaknesses in the financial management internal

control of PUPR. One of the causes is the utilization

of Information Technology (IT) not yet optimal in

the financial management at PUPR.

IT can be used to improve quality of financial

management internal control, because IT can make

financial management more effective and efficient.

Currently, the benefit of IT is not yet optimal in

financial management, because target and

performance measures of IT have not yet align with

the target and performance measures of financial

management. This study was conducted to determine

strategy and performance measures of IT Division in

order to improve financial management internal

control at PUPR.

2 THEORICAL FRAMEWORK

Balanced Scorecard (BSC) discovered by Kaplan

and Norton for the very first time, is a new method

in measuring organizational performance in a

balanced manner and it is replacing performance

measurement method that only focus on financial

perspective (Kaplan and Norton, 1992). Performance

measurement is conducted by measuring

organizational performance toward its strategic

objectives in various perspectives which are aligned

with the mission, value and vision of the

organization. Kaplan and Norton complement the

performance measures produced by BSC with a

748

Simatupang, O. and Simanjuntak, B.

Strategy and Performance Measures of Information Technology in the Enhancement of Financial Management Internal Control, Ministry of Public Works and Housing.

DOI: 10.5220/0009504407480753

In Proceedings of the 1st Unimed International Conference on Economics Education and Social Science (UNICEES 2018), pages 748-753

ISBN: 978-989-758-432-9

Copyright

c

2020 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

strategy map to show organization strategy in

achieving organization mission through causality

between strategic objectives that must be achieved

by the organization (Kaplan and Norton, 2004).

BSC can be used to inherit strategy of parent

organization to other organizations which are part of

parent organization. BSC also can be used to align

strategy and performance measures of IT Division

which is part of the organization. Van Gembergen

and Saul have shown that strategy and performance

measures of IT can be aligned with the strategy and

performance measures of parent organization by

deriving the strategy and performance measures of

IT from the strategy and performance measures of

parent organization (Van Gembergen and Saull,

2001).

BSC can be used by IT Division in an

organization to measure the performance of IT

management toward perspectives in the parent

organization’s BSC namely: 1) financial; 2)

customer; 3) internal process; and 4) learning and

growth (Addo, Chow and Haddad, 2004). IT BSC

also can be used during IT strategic planning,

consisting of: 1) aligning IT strategy and business

strategy; 2) IT performance evaluation; 3) IT

strategic plan; 4) IT implementation plan; and 5)

socialization of IT strategic plan (Tonneli, Bermejo,

and Zambalde, 2014).

3 RESULT & DISCUSSIONS

The study was conducted with a qualitative approach

using a case study method. Case study was used in

this study to be able to explain in detail and

comprehensive about strategy and performance

measures of IT in improving the quality of financial

management internal control.

Primary data collection was conducted by semi-

structured interview. Researchers carried an

interview guideline consisting of basic questions to

guide researchers in collecting data to answer

research problems. Interviews were conducted by

asking open questions to informants who were

executers of financial management and IT

management at PUPR. Secondary data collection

was conducted by collecting documents related to:

1) regulation of financial management and IT

management; 2) strategic plan document of financial

management and IT management; 3) BPK-RI audit

results; and 4) government instance performance

report.

Data collected then analyzed to be used in the

formulation of strategy and performance measures.

Public organization can determine perspective,

strategic objectives, and strategy map as well as

performance measures if they already have mission,

values and vision (Niven, 2003). The method used in

structuring the strategy map and performance

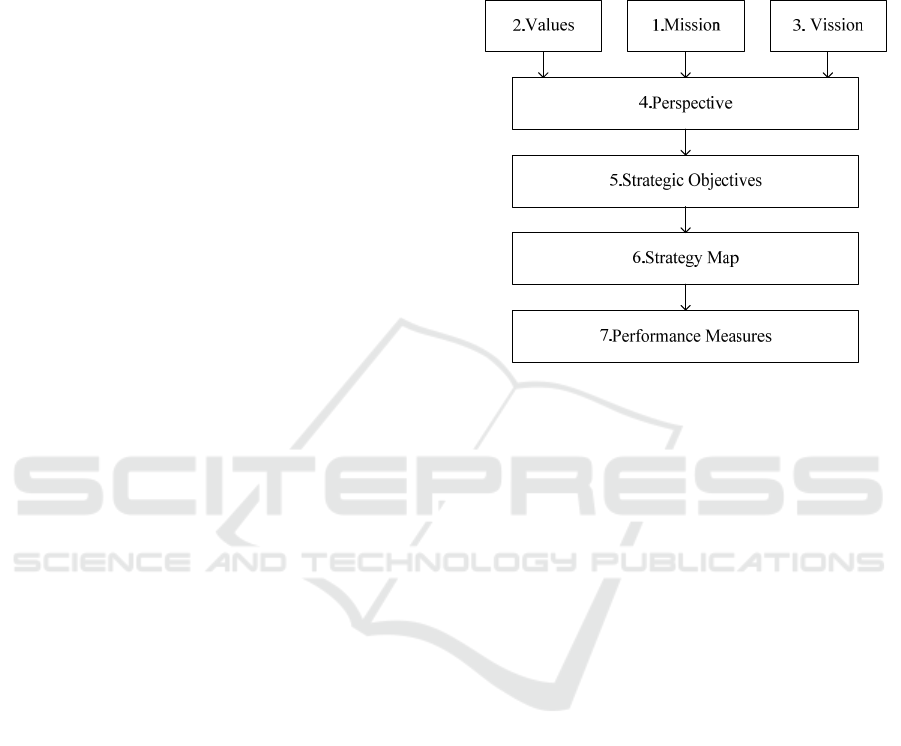

measures in this study is as shown in Figure 1.

Figure 1: The Structuring of Strategy Map and

Performance Measures

3.1 Strategy And Performance Measures Of

Budget /Goods User

a. Strategy of Budget/Goods User

President authorizes the authority of state financial

management to Ministries/Agencies as

Budget/Goods User to use budget and goods to

conduct government programs in their respective

Ministries/Agencies (State Law, 2003). The mission

of Budget/Goods User at PUPR is to use the budget

effective, efficient, accountably and transparently as

well as to use state-owned property (BMN)

optimally to support the implementation of reliable

infrastructure development of public works and

housing.

The Budget/Goods User at PUPR has values that

must be implemented by all PUPR employees

namely: integrity, professional, mission oriented,

visionary; and ethical. The vision of Budget/Goods

User at PUPR is to become a Budget/Goods User

with integrity, professionalism and responsibility to

support the realization of reliable infrastructure of

public works and housing. Perspective will help

Budget/Goods User to translate mission, values and

vision into strategic objectives that must be achieved

from various important perspectives in a balanced

manner.

Budget/Goods User uses the customer's

perspective to determine the value that can be

generated in the form of products and services

Strategy and Performance Measures of Information Technology in the Enhancement of Financial Management Internal Control, Ministry of

Public Works and Housing

749

desired by customer from Budget/Goods User

associated with the mission, values and vision of

PUPR. The customer of Budget/Goods User consists

of: 1) President; 2) House of Representatives (DPR);

3)BPK-RI; 4) related Ministries/Agencies; 5) public;

and 6) other related parties. Customer wishes

Budget/Goods User to: 1) provide budget,

goods/services, and financial report; 2) comply with

regulations; 3) accept non-tax state revenues

(PNBP); and 4)utilize BMN.

Budget/Goods User determines strategic

objectives toward customer’s expectation that has

been explained in the customer perspective. Table 1

shows strategic objectives of Budget/Goods User in

customer perspective.

Budget/Goods user uses an internal process

perspective to determine processes that must be

executed perfectly by Budget/Goods User in order to

provide maximum value to customer. To be able to

provide value to customer, processes which must be

conducted by Budget/Goods User are namely: 1)

preparing budget; 2) implementing budget; 3)

holding responsible over budget; 4) reviewing PNBP

potential; 5) conducting procurement of BMN; 6)

implementing security and maintenance to BMN; 7)

administering BMN; and 8) supervising state

financial management.

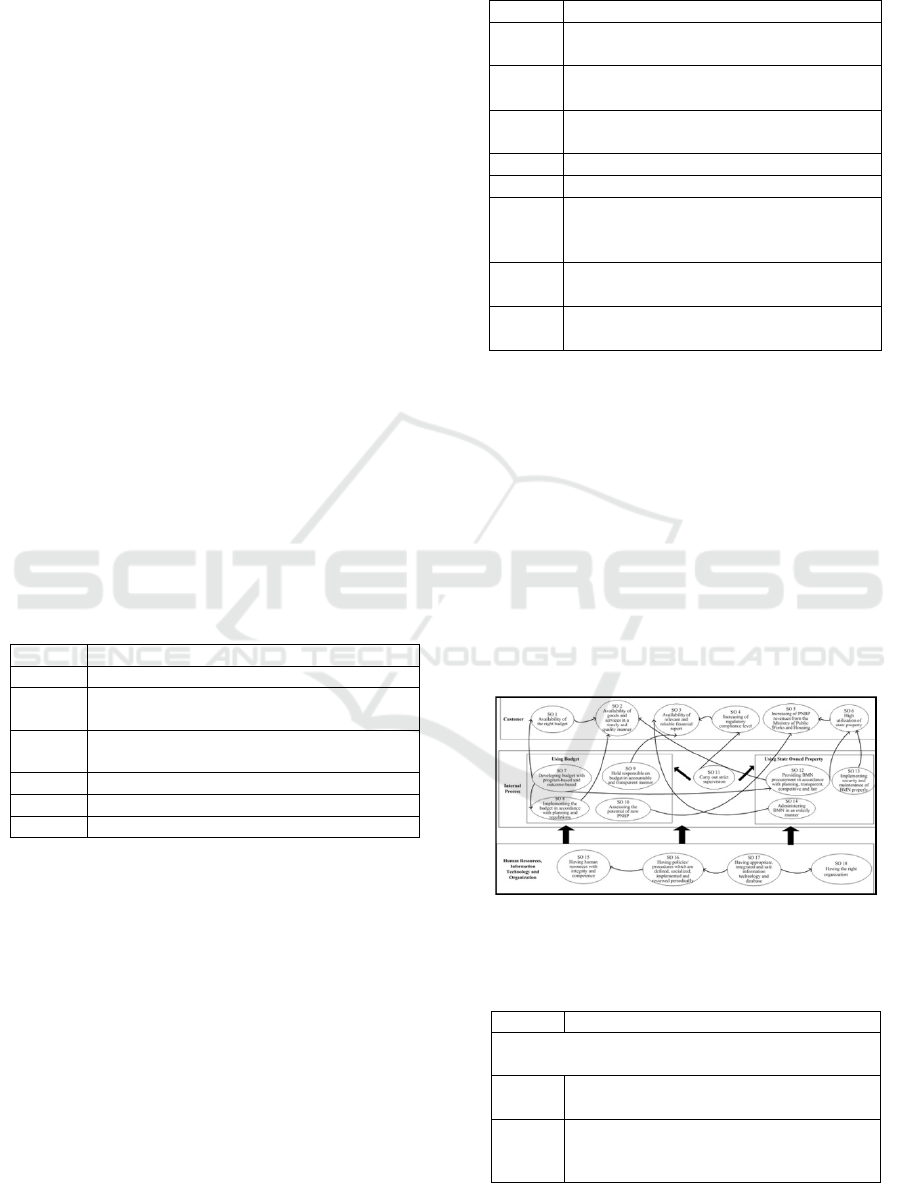

Table 1: Strategic Objectives of Budget/Goods User

in Customer Perspective

SO Strategic Objective

SO1 Availability of the right budget

SO2 Availability of goods and services in a

timely and quality manner

SO3 Availability of relevant and reliable

financial statement

SO4 Increasing of regulatory compliance level

SO5 Increasing of PNBP revenues from PUPR

SO6 High utilization of BMN

Budget/Goods User determines strategic

objectives based on the processes already described

in the internal process perspective. Table 2 shows

strategic objectives of Budget/Goods User in

internal process perspective.

Budget/Goods user uses the perspective of

human resources, information technology and

organization in determining resources that must be

owned by Budget/Goods User in order to carry out

internal process providing value to customer.

Budget/Goods user needs human resources that have

a certain quality, appropriate information technology

and the right form of organization in order to carry

out the needed internal process.

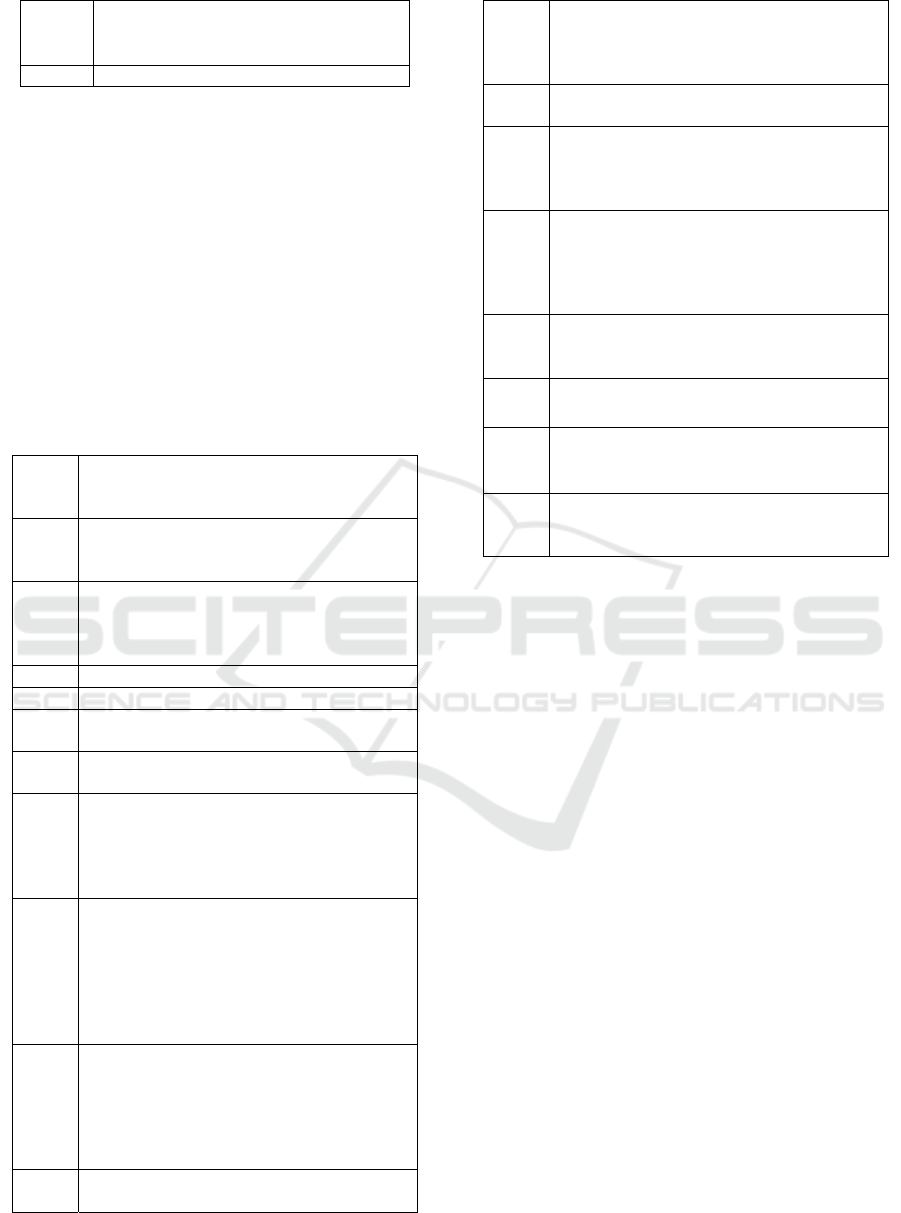

Table 2: Strategic Objectives of Budget/Goods User

in Internal Process Perspective

SO Strategic Objective

SO7 Develop budget with program-based and

outcome-based

SO 8 Carry out the budget in accordance with

planning and regulations

SO 9 Holding responsible over budget in

accountable and transparent manner

SO 10 Assesssing the potential of new PNBP

SO 11 Carry out strict supervision

SO 12 Providing BMN procurement in

accordance with planning, transparent,

competitive and fair

SO 13 Implementing security and maintenance

of BMN properly

SO 14 Administering BMN in an orderly

manner

Budget/Goods User determines strategic

objectives based on needs of human resources

described in the perspective of human resources,

information technology and organization. Table 3

shows strategic objectives of Budget/Goods User in

perspective of human resources, information

technology and organization.

Each strategic objective in the strategy map of

Budget/Goods User must have causality with other

strategic objective both in the same perspective and

different perspective. Causality shows strategy of

Budget/Goods User to achieve mission, values and

vision of Budget/Goods User.

The strategy map of Budget/Goods User is

illustrated in Figure 2.

Figure 2. Strategy map of Budget/Goods User

Table 3: Strategic Objectives of Budget/Goods User

in Human Resources, Information Technology and

Organization Perspective

SO Strategic Objective

Human Resources, Information Technology

and Organization Perspective

SO 15 Having human resources with integrity

and competence

SO 16 Having policies/procedures which are

defined, socialized, implemented and

reviewed periodically

UNICEES 2018 - Unimed International Conference on Economics Education and Social Science

750

SO 17 Having appropriate, integrated and safe

information information technology and

database

SO 18 Having the right organization

b. Performance Measures of Budget/Goods User

Budget/Goods user has determined strategic

objectives and described causality between strategic

objectives contained in the strategy map describing

strategy from Budget/Goods User to achieve

mission, values and vision of Budget/Goods User.

Budget/Goods user must measure their performance

towards strategic objective that have been

determined with the right performance measure.

Budget/Goods user has strategic objectives that must

be determined its performance measures as it is

shown in Table 4.

Table 4: Performance Measures of Budget/Goods

User at PUPR

SO Performance Measures /

Data Source

SO1 Performance Evaluation Value / Budget

Performance Accountability Report

(LAKIP)

SO2 Goods and services that are completed and

can be received on time / Contract

document, and Minutes of Handover

(BAST) of work

SO3 BPK-RI opinion / BPK-RI Audit Report

SO4 State losses / BPK-RI Audit Report

SO5 Level of PNBP revenues / Treasurer

Accountability Report (LPJ)

SO6 BMN used, utilized, and granted / BMN

Report

SO7 Amount of DIPA revision and differences

between plan and work result / Revision

Document of Budget Implementation List

(DIPA), Term of Reference, and BPK-RI

Audit Report

SO8 Percentage of budget realization, Amount

of late payment, Amount of over budget

realization, Amount of payment refusal /

Budget Realization Report Document,

Invoice Document, Payment Warrant

(SPM), and Fund Disbursement Warrant

(SP2D).

SO9 Percentage of responsibility

comprehensiveness over budget utilization,

Obedience in the submission of financial

statement / Evidence of budget utilization,

Reconciliation Minutes of Financial

Statement

SO10 Amount/number of PNBP type/ Study

document of PNBP

SO11 Number of work unit supervised, Number

of work implementation supervised /

Aocument of audit implementation

planning by internal auditor.

SO12 Number Procurement objection / Bidders'

objection document

SO13 Amount of BMN used by unauthorized

parties, amount of severely damaged BMN

/ BMN Condition Report and BMN

Inventory Report

SO14 Percentage of BMN that has been revalued

on time, Abedience in the submission of

BMN report / BMN Report, BMN

revaluation report, and BMN procurement

document

SO15 Amount of certified HR, amount of training

/ Implementation report of training and HR

certification.

SO16 Assessment result of quality management

system / Quality management document

SO17 Support index of IT and database /

document of IT and database needs,

document of IT and database management

SO18 Organizational Index / Analysis document

of organization form and the applicable

organizational form document

3.2

Strategy And Performance Measures Of

Division

On the Strategy Map of Budget/Goods User at

PUPR, as it is shown in Figure 2, there is the 17th

strategic objective (SO 17) found in the perspective

of HR, IT and organizational, namely Budget/Goods

User must have appropriate, integrated and safe

information technology and database. IT Division

has a role in financial management at PUPR to

support Budget/Goods User in reaching SO 17, so

that the mission of IT Division is to provide

information system and database that are reliable,

integrated and safe to support the use of budget in

effective, efficient, accountable, and transparent

manner, as well as optimal use of BMN.

IT Division at the PUPR has values that must be

implemented by all PUPR employees, namely

integrity, professional, mission oriented, visionary

and ethical. The vision of IT Division in the

financial management at PUPR is to become reliable

and innovative information technology and database

manager, in order to support integrated, professional

and responsible Budget/Goods User.

The perspective used by IT Division to develop

BSC of IT Division in the financial management of

PUPR is a perspective that can be used to translate

the mission, values and vision of IT Division in

financial management at the PUPR. The perspective

used is the perspective of Budget/Goods User as

Strategy and Performance Measures of Information Technology in the Enhancement of Financial Management Internal Control, Ministry of

Public Works and Housing

751

user of IT services, internal process perspective, as

well as learning and growth perspective.

The perspective of Budget/Goods User is used to

determine the values expected by Budget/Goods

User from IT Division. Budget/Goods User expects

IT Division to provide information system, database

and IT infrastructure that can be used to achieve

their strategic objectives.

IT Division determines strategic objectives

toward Budget/Goods User expectation. Table 6

shows strategic objectives of IT Division in

Budget/Goods User perspective.

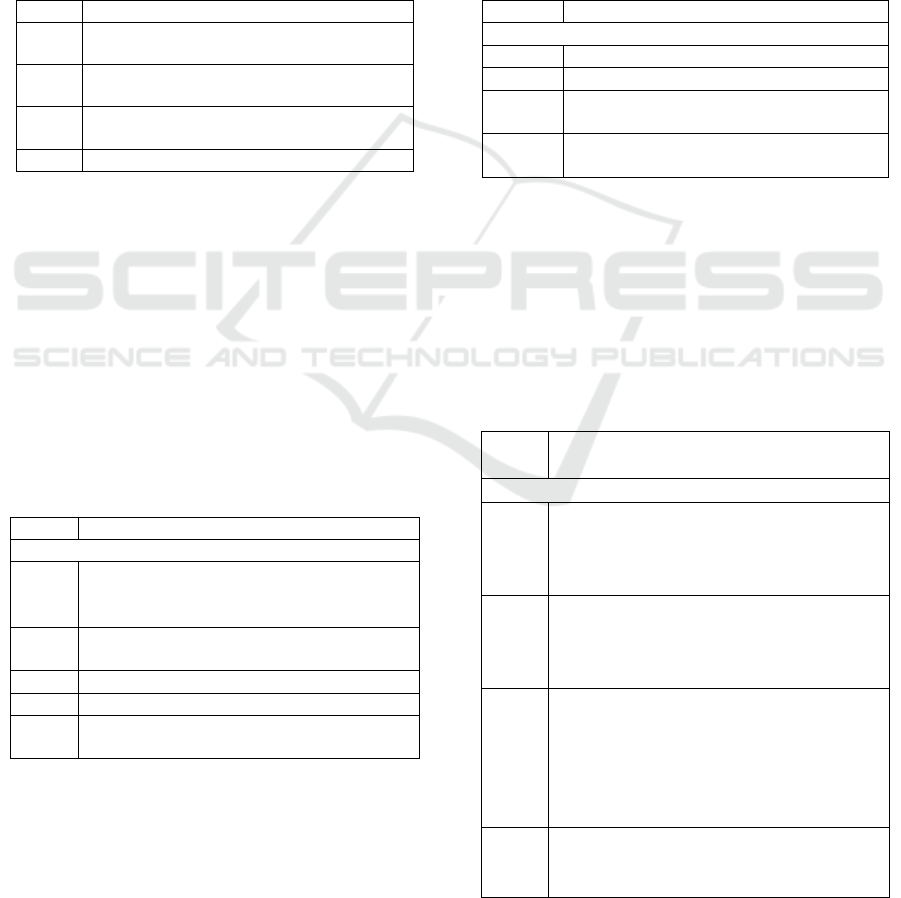

Table 5: Strategic Objectives of IT Division in

Budget/Goods User Perspective

SO Strategic Objectives

SO1 Availability of information system and

database which are according to needs

SO 2 Availability of integrated information and

database system

SO 3 Availability of a secure information and

database system

SO 4 Availability of adequate IT infrastructure

The internal process perspective describes what

processes that must be done well in order to provide

value to the Budget/Goods User. The prioritized

internal processes to be implemented are namely: 1)

analyzing the information system requirement, data

and infrastructure; 2) developing information

system, 3) collecting data; 4) organizing IT

infrastructure; and 5) implementing IT operation. IT

Division determines strategic objectives toward

internal process which is important to be

implemented. Table 6 shows strategic objectives of

IT Division in internal process perspective.

Table 6: Strategic Objectives of IT Division in

Internal Process Perspective

No Strategic Objectives

Internal Process Perspective

SO 5 Analyzing the needs of information system,

IT infrastructure data which are according

to needs

SO 6 Developing information systems with good

development standard

SO 7 Collecting and verifying data

SO 8 Implementing the right IT infrastructure

SO 9 Carrying out effective and efficient

information technology operation

Learning and Growth Perspective explains the

resources that IT Division must have in order to be

able to carry out internal processes perfectly. IT

Division must have HR, training, lesson learned and

follow technological development. IT Division

determines strategic objectives toward resources that

must be owned. Table 7 shows strategic objectives

of IT Division in Learning and Growth Perspective.

IT Division compiles a strategy map to describe

process to achieve mission, values and vision of IT

Division in financial management at PUPR. On the

strategy map of IT Division in financial management

at PUPR, there is causality between each of the

strategic objectives in the strategy map. This

relationship illustrates the process on how IT

Division can achieve their mission, values and

vision in implementing financial management at

PUPR as it is shown in Figure 2.

Table 7: Strategic Objectives of IT Division in

Learning and Growth Perspective

No Strategic Objectives

Learning and Growth Perspective Perspective

SO 10 Having competent human resources

SO 11 Having sufficient amount of training

SO 12 Record, analyze, and use lessons learned

SO 13 Having a study of information technology

development

b. Performance Measures of IT Division in

Financial Management

IT Division sets performance measures for strategic

objectives to be achieved. Performance measures are

used to measure performance of IT Division towards

strategic objectives to be achieved. as it is shown in

Table 8.

Table 8: Performance Measures of IT Division in

Financial Management at PUPR

SO Performance Measures /

Data

Customer Perspective

SO1 Level of participation in IT forums,

Budget/Goods User Satisfaction / IT

Forums Report, Budget / Goods User

Satisfaction Survey

SO2 Number of stand alone information

system, total number interface /

Information system and database

architecture

SO3 Number of IS and database infiltration

incident, percentage of corrupt IS and

database / Information system and

database operation report, information

system error report and database

corrupt report

SO4 IT infrastructure index / report of IT

infrastructure needs, and report of

available IT inventory

UNICEES 2018 - Unimed International Conference on Economics Education and Social Science

752

Internal Process Perspective

SO5 Percent of IS projects with a negotiated

plan with Budget/Goods User /

Business Case

SO6 Percent resources devoted to

applications development / Schedule

data and Budget data

SO7 Data entry error rates, age data /

Database, Data warehouse

SO8 Project performance meets or exceeds

baseline expectations / Scope

performance data

SO9 Total number of direct labor hours,

cost/unit of service / Employee

assignment report, IT cost report

Learning and Growth Perspective

SO10 Number of employees with

certification / Employee expertise

certification

SO11 IT training and development budget as

a percent of overall IT budget, Percent

of technical training goals met / IT

Budget, training report.

SO12 Percent of projects with lessons

learned in database / database

SO13 Number of new IT study / IT study

document.

4 CONCLUSIONS

After carried out all stages of this study, several

conclusions can be conveyed by the researcher are:

1) organization must have good mission, values and

vision before developing organizational strategy; 2)

strategy and performance measures of IT Division

must be derived from strategy and performance

measures of organization.; and 3) strategy map can

be a tool for compiling, implementing and

communicating strategy.

Several suggestions can be conveyed by the

researcher are: 1) preparation of strategy and

performance measures require commitment from all

parties; 2) preparation of strategy and performance

measures should use benchmark with similar

organization; and 3) performance measures that are

already been prepared are followed up with

determining right objectives and activities to achieve

performance measures target and strategic objectives

target.

REFERENCES

State Law (2017) ‘Undang-Undang No. 15 Tahun 2017

Tentang Anggaran dan Pendapatan Belanja Tahun

2018’.

Tonelli, A.O.;Bermejo P.; and Zambalde A. (2014) 'Using

the bsc for strategic planning of it (information

technology) in brazilian organizations.', Journal of

Information Systems and Technology Management ,

vol 11, pp.361-378.

Addo, T. B.; Chow W. C.; and Haddad, K. M. (2004)

'Development of an IT Balanced Scorecard', Journal of

International Information Management, Vol. 13,

Article 1.

Kaplan, R. and Norton, D. (2004) 'Strategy maps:

converting intangible assets into tangible outcome',

Boston, Harvard Business School Press.

R. Niven, Paul. (2003) 'Balanced Scorecard Step-by-Step

for Government and Nonprofit Agencies, P.R. Niven.

Undang-Undang (2003) ‘Undang-Undang No. 17 Tahun

2003 Tentang Keuangan Negara’.

Kaplan, R. and Norton, D. (1992) 'The Balanced

Scorecard—Measures That Drive Performance',

Boston, Harvard Business Review

Strategy and Performance Measures of Information Technology in the Enhancement of Financial Management Internal Control, Ministry of

Public Works and Housing

753