Analysis of Cost Calculation System at X Hospital based on

Traditional Costing and Time Driven Activity based Costing: Study

at Unit Cost Hemodialysis Services

Novia Rizki

1

and Dwi Hartanti

1

1

Faculty of Economics and Business, Universitas Indonesia, Jakarta -Indonesia

Keywords: TDABC, Traditional Costing, hospital, hemodialysis services

Abstract: The purpose of this research was to show an analysis of unit cost calculation based on traditional costing

and time driven activity based costing methods and also to analyze costs and benefits of time driven activity

based costing method’s implementation at X Hospital. This Hospital was chosen as a sample because it does

not have a good cost system yet so far. X Hospital uses tariff which is determined by the regional

government. This study was conducted using qualitative and study case approach. It focused on the unit cost

of hemodialysis services at X Hospital. The result of the study showed that unit cost calculation using time

driven activity based costing is higher than by using traditional costing. Both methods used a different

driver, in which traditional costing method used the number of patients driver and time driven activity based

costing method used time as driver. Time driven activity based costing system reflected more the activities

that are consumed by hemodialysis services, and more importantly, human resources of X Hospital are

ready to implement this method.

1 INTRODUCTION

A hospital’s revenue from a certain service is a total

of the unit cost of services and the expected surplus.

Unit cost of a hospital consists of direct cost and

indirect cost. A direct cost will be charged to each

service, meanwhile, the indirect cost will be

allocated later. There are some methods that can be

used to allocate the indirect cost such as traditional

method and activity-based costing method.

Traditional method and activity-based costing

method are differed in their allocation aspect of

indirect costs, in which activity-based costing uses

activities as the base of its allocation. According to

Popesko and Nová (2014) an organization that runs

their operational activities with high complexity and

high proportion of indirect costs such as hospital

will be suitable to use activity-based costing method.

This method will give a more detail costs

information regarding the hospital’s activities.

Having known of this, yet health organizations such

as a hospital rarely uses activity-based costing

method; hospitals in Indonesia are not exception.

Therefore, this study was motivated in analyzing the

implementation of activity-based costing method in

a hospital or a health unit in Indonesia. The chosen

sample for this study is X hospital which is located

in West Nusa Tenggara.

The activity-based costing method is also not yet

implemented at X hospital. This hospital had

experienced a deficit on their operational activities

in the last couple of years, even though the recorded

increase in their income is quite high. The number of

patients at X hospital in 2017 is 160.757 patients.

The highest number of patients that are received by

the hospital is outpatients with the number of

125.403 patients, while services with the lowest

number of visits received is intensive care unit with

the number of 1.281 patients. X hospital offers

various types of services in which every service uses

different resources, therefore, it is advised that X

hospital uses activity-based costing method that

emphasizes the allocation of indirect costs on

activities.

Additionally, X hospital does not have a clear

system of costs accountancy because they are using

a tariff format that is decided by the regional

Rizki, N. and Hartanti, D.

Analysis of Cost Calculation System at X Hospital based on Traditional Costing and Time Driven Activity based Costing: Study at Unit Cost Hemodialysis Services.

DOI: 10.5220/0009504010791084

In Proceedings of the 1st Unimed International Conference on Economics Education and Social Science (UNICEES 2018), pages 1079-1084

ISBN: 978-989-758-432-9

Copyright

c

2020 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

1079

government. There are a lot of changes that have

been experienced by X Hospital from 2015 to 2017,

but unit cost and tariff calculation were last done in

2015. Based on the information gathered through

interview, it showed that X hospital did not

categorized the costs based on the general principles

stated on the cost accounting, such as direct

material, direct labor, and overhead. The fact that

they are still using the traditional method in deciding

the unit cost and in counting the proposed tariff to

regional government has led the researcher to doubt

the accuracy of the computation system that they

use. Therefore, the time driven activity-based

costing method is proposed as the method for

computation.

Time driven activity-based costing method is

simpler and easier to be applied compared to

activity-based costing method. This method is

considered easier and reasonably cheaper. Time

driven activity-based costing method uses time

driver to allocate resources to products. In addition,

this study will also analyze the proposal to

implement time driven activity-based costing

method to calculate unit cost of hemodialysis

services that is a part of one day care service of X

hospital. There is no recorded health service unit in

Indonesia that implements unit cost calculation

using time driven activity-based costing method.

Research that discusses the proposal to apply this

method is also scarce and limited. The formulated

questions for this study are as follow:

1. What is the existing system in determining tariff

of services at X hospital and how is calculation

of the total costs of hemodialysis services at X

hospital based on traditional costing?

2. How is calculation of the total costs of

hemodialysis services at X hospital based on

time driven activity-based costing?

3. How is the calculation comparison of the total

costs of hemodialysis services at X hospital

based on traditional costing and time driven

activity based costing?

4. How is the readiness of human resources as well

as advantages and costs if time driven activity-

based costing is implemented as method to

calculate the unit cost of services at X hospital?

2 THEORICAL FRAMEWORK

Traditional Cost Accounting

There are five unit-level drivers which are generally

used in traditional costing method i.e. unit produced,

direct labor hours, direct labor dollar, machine

hours, and direct material dollar. In this system,

there are two methods in deciding cost driver for

overhead cost, i.e. plantwide rates, which is deciding

overhead cost rate using one driver. Another one is

departmental rates, which is deciding overhead cost

rate based on each production department. However,

both methods do not function well and in truth they

can cause a serious distortion in product costs,

especially, for a company with significant overhead

costs and for a company with high variety of

products which consumes varied resources (Hansen

and Mowen, 2015).

Activity based Costing System

Activity based costing is a system of costs

determination by allocating indirect costs toward a

cost object based on activity driver, not the volume

driver. This is because it is believed that the cause

for the rise in costs is the activity, not the quantity of

the product. Baker (1998) stated that an activity can

have some cost drivers which relate to that activity.

In a world of health services, an activity almost

always possesses many cost drivers. The right

implementation of cost driver will have a positive

influence toward the success of an organization.

However, activity-based costing method is

considered quite difficult because it requires detailed

interview and survey. It also needs substantial costs

in its implementation (Kaplan and Anderson, 2007).

Time Driven Activity based Costing

Time driven activity-based costing method assumed

that time is the prime mover of costs since most of

resources such as personnels and equipments have

the capacities that can be easily measured with the

number of available times to do the job (Kaplan and

Anderson, 2007). Time driven activity-based costing

method is the most agreeable with companies

dealing in service industry. This is because service

industry focuses more on providing services which

will be more accurately calculated with the time

spent to do the service activity (Szychta, 2010).

Time driven activity-based costing method in its

calculation needs predictions from two components

i.e. unit costs for the available capacity and the time

that is needed to do the transaction or activity

(Kaplan dan Anderson, 2007).

Formula for calculating costs based on time

driven activity based costing method:

capacity cost rate

cost of capacity supplied

practical capacity of resources sepplied

UNICEES 2018 - Unimed International Conference on Economics Education and Social Science

1080

3 RESEARCH METHOD

This study used qualitative and case study

approaches. The data collection techniques used in

this study were interview and field study. Primary

data that was used in this study was the finance

reports period 2016 and 2017, installation data

recapitulation of patients’ medical records period

2017, and data from the field study and interview

which were conducted since May 2018 until October

2018.

This study was a single case study that was

conducted on a single unit analysis; a hemodialysis

unit at X hospital. The period that was used to

calculate the unit cost at X hospital was one year; a

year of 2017.

Based on the results of the interview and the

primary data that had been gathered, researcher did

an analysis about the system of tariff determination

which was currently used by the hospital. After that,

the researcher designed a traditional costing system

to calculate the unit cost of hemodialysis services

and compared them with the existing costs

calculating system. Next is designing time driven

activity-based costing system to the same unit cost

service and compared the calculation results of

traditional costing method dan time driven activity

based costing method. The researcher did the

calculation of unit cost using time driven activity

based costing method by referring to Kaplan and

Anderson (2007).

4 ANALYSIS

4.1 The Current Tariff Determination System

at X Hospital in Relation to Their Unit

Cost Calculation of Hemodialysis Service

using Traditional Method

X hospital has established a specific tariff team to

formulate the unit cost calculation and the selling

price or the real tariff which are applied to general

patients. The real tariff has included the 20% surplus

and the real unit cost. There are some changes in the

X hospital from 2015 to 2017 which supposedly

influence the changes in the unit cost formulation

and the tariff of services. Some of them are the rise

in the number of patients’ visit, followed by the

trend of the rise in number of the average patients’

visits which is 3.5% per year, the development of

heart services and integrated blood vessels/cathlab

center which was inaugurated on November 9

th

2016, the enhancement of the supporting service

facilities, the number of new services at the

Radiology unit, the inauguration of independent

policlinic facility, education-training unit (skill lab),

research unit (Litbangkes Institution), and

accommodation (guest house).

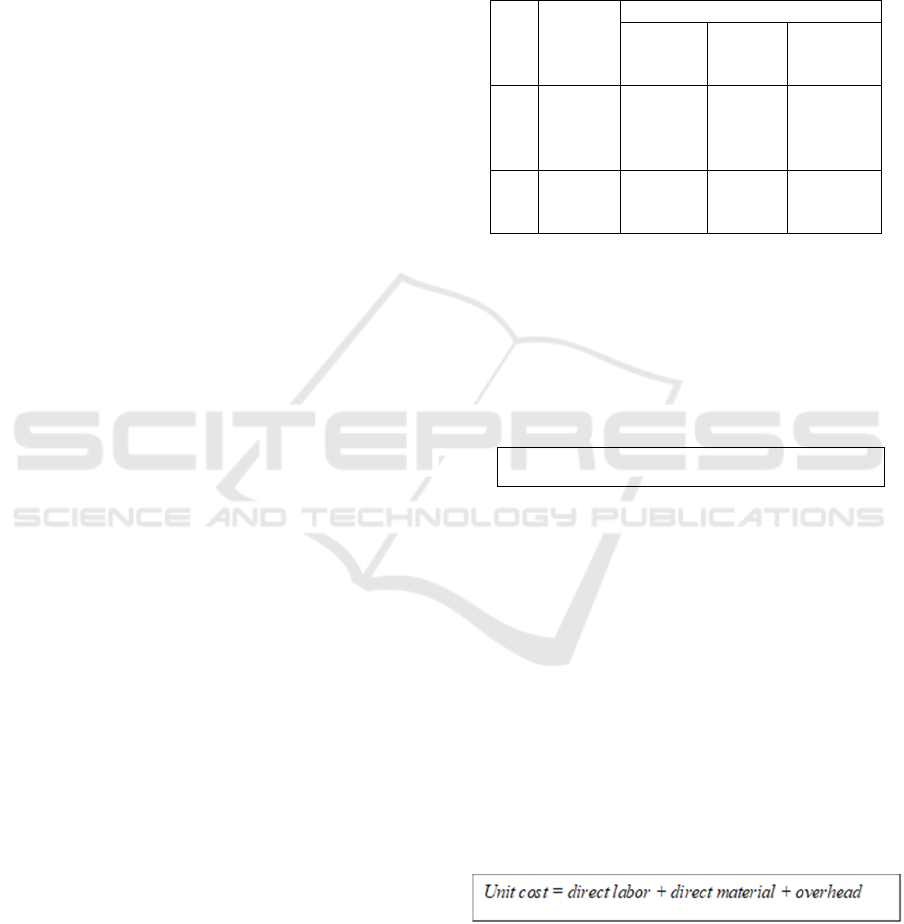

Table 1: Hemodialysis Services Tariff at X Hospital

2017

No. Types

of

Services

Class an

d

VIP (IDR)

Service

Facilitie

s

Service Tariff

1 HD

single-

use

Service

960,000 408,00

0

1,368,00

0

2 HD

Reuse

Service

840,000 240,000 1,080,000

Source: X Hospital (2017)

Referring to the result of the interview, service

facilities consist of direct material for one treatment

or one service, overhead cost, and mark-up.

Meanwhile, service consists of direct labor cost and

indirect labor cost.

Unit cost of hemodialysis services based on the

calculation of X Hospital is as follow:

Based on the above formula, then unit cost for

each hemodialysis service which was taken as

sample in this study was:

a. Unit cost of HD single-use service = IDR

1,140,000

b. Unit cost of HD re-use service = IDR 900,000

The following is the calculation of hemodialysis

services unit costs based on traditional costing

method which was designed by the researcher. The

calculation would be done based on one-year data to

eliminate the possibility of numbers’ fluctuation

each month. This calculation was based on the

analysis result of finance reports year of 2017,

interview, and observation that has been conducted.

Below is the explanation of each costs which

was used to calculate hemodialysis services unit cost

period of 2017:

1. Direct labor

The total direct labor cost of hemodialysis unit in

one year which is the year of 2017 was IDR

Unit cos

t

= Real tariff

–

mark up 20%

Analysis of Cost Calculation System at X Hospital based on Traditional Costing and Time Driven Activity based Costing: Study at Unit

Cost Hemodialysis Services

1081

661,412,000. If this figure were to be divided by the

number of hemodialysis services in one year which

is 12.123, then the direct labor costs for one-time

hemodialysis service, either for single use or re-use

is IDR 54,558.

2. Direct Material

Direct material consists of consumables material,

other equipment, medicines, safety equipment,

machinery equipment and HD set. The difference

between the single use and re use hemodialysis

services is only in the HD set that is used,

meanwhile, other components from the two types of

services consume the same resources.

a. The total number of consumables goods,

medicines, and hemodialysis unit equipment

for the year of 2017 is IDR 2,092,938,966. If

this number were to be divided with the

number of hemodialysis services in a year

which is 12.123, then the cost of consumables

goods for one-time hemodialysis service is

IDR 172, 642 for both single use or re-use

hemodialysis services.

b. HD Set package for each types of

hemodialysis services:

1) Single Use package is IDR 517,550. -

2) Reuse package is IDR 373,830.-

3. Overhead Cost

Overhead costs and indirect costs are the costs

that do not directly influence the service activities

and are consumed by variety of production

activities. The total overhead cost of X Hospital in

the year of 2017 is IDR 92,847,527,177.

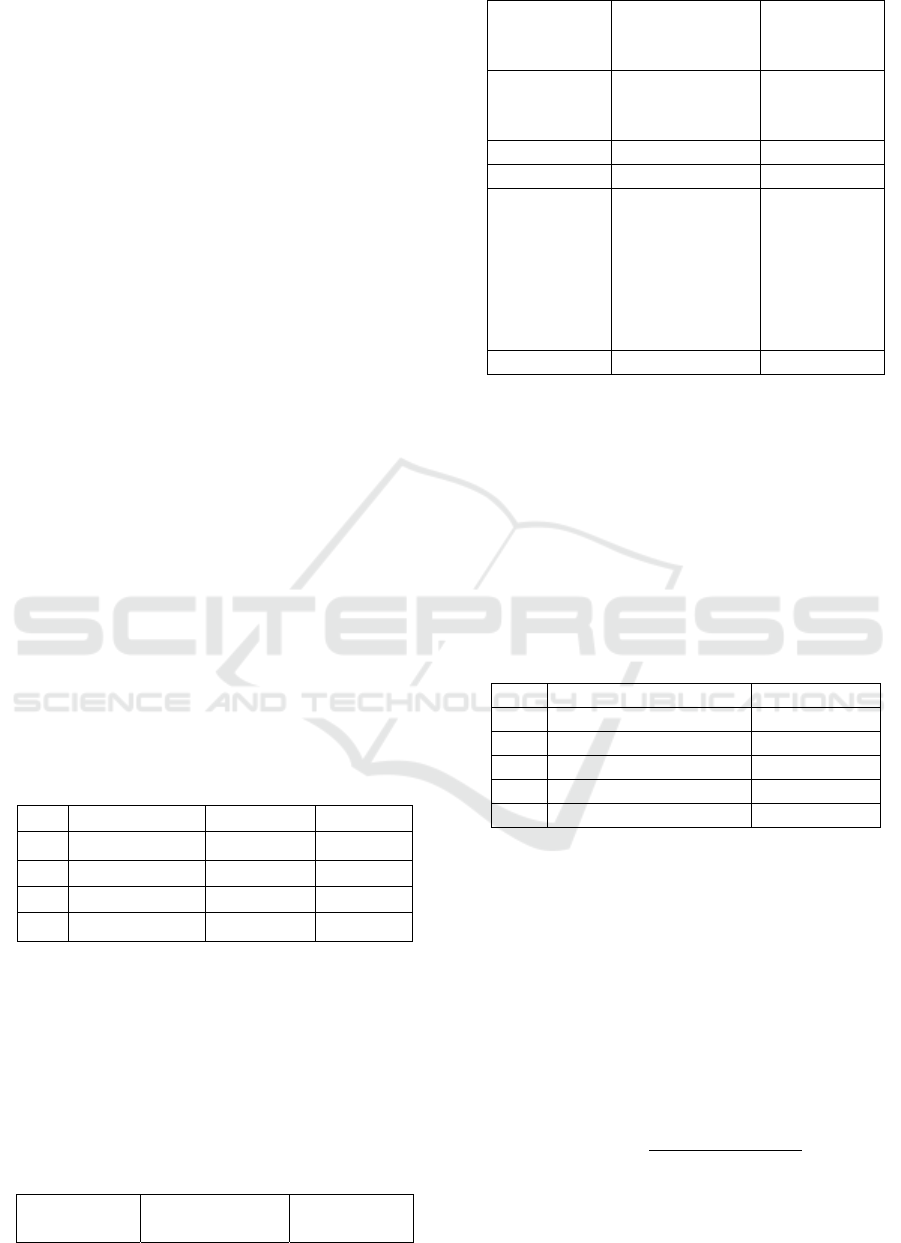

Table 2 : Unit Cost of Hemodialysis using

Traditional Costing

No Types of costs Single Use Re-Use

1. Direct Labor 54.558 54.558

2. Direct Material 690.192 546.472

3. Overhead 577.564 577.564

4. Total 1.322.314 1.178.594

Table 2 above showed the total unit cost for each

hemodialysis services using traditional costing

calculation method by applying components of the

hospital’s costs for the year of 2017. The difference

in both services is only found in the direct material

components, specifically for the HD set that is used.

Table 3 : Comparison of Hemodialysis services Unit

Cost (Traditional Costing) with the Hospitals’ Tariff

Calculation

Metho

d

Single Use

(IDR)

Re-use

(IDR)

Hospital

Unit cost

calculation

1.140.000 900.000

Unit cost

traditional

costin

g

1.322.314 1.178.594

Gap (182.314) (278.594)

Tarif RS 1.368.000 1.080.000

Traditional

costing

tariff (unit

cost

traditional

costing +

mark up)

1.586.776 1.414.313

Gap (218.000) (334.313)

Source: X Hospital (2017), has been reprocessed

4.2 Design of Hemodialysis Services Unit Cost

using Time Driven Activity based Costing

Method

Time driven activity based costing method would be

used as the method for the allocation of indirect

costs or overhead costs. The first phase is the

activities’ grouping in hemodialysis unit’s service,

and then counting the capacity cost rate.

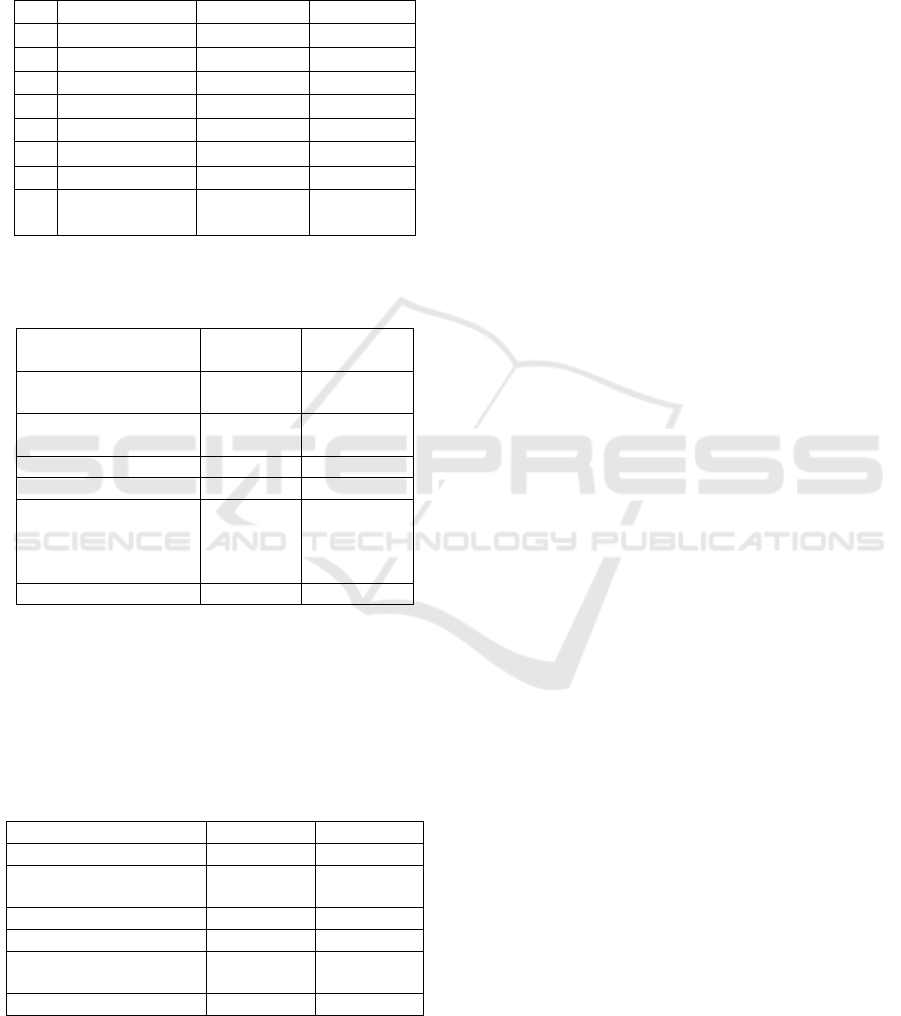

Table 4 : Grouping Activities of Hemodialysis

Services

N

o Outlines of Activities Time

1 Administration 30 minutes

2Pre Dial

y

sis 55 minutes

3 HD Process 302 minutes

4 Post HD 30 minutes

Total 417 minutes

Source: Respondent Interview (2018), has been

reprocessed

Capacity cost rate or cost per unit of time can be

counted by dividing the costs of the available

capacities with practical capacities. The available

capacity cost is a total cost of overhead, meanwhile

the practical capacity in this study refers to indirect

labor hours in a year.

The practical capacity of one indirect staff in a

year is 108.060 minutes. The number of the indirect

staffs is 532 people, then the total practical capacity

is 54.487.920 minutes.

cost per unit time

Rp 92.847.527.177

54.487.920 minutes

cost per unit time Rp 1.704/minute

UNICEES 2018 - Unimed International Conference on Economics Education and Social Science

1082

Based on the group of activities, the

hemodialysis service is divided into 4; they are

administrative group, pre-dialysis, HD process, and

post HD.

Table 6 : Unit Cost of Hemodialysis Services Based

on Time Driven Activity Based Costing

No Cost Single Use Re Use

1. Direct labor 54.558 54.558

2. Direct material 690.192 546.472

3. Administration 327.504,92 327.504,92

4. Pre HD 54.481,58 54.481,58

5. HD Process 298.905,58 298.905,58

6. Post HD 29.675,92 29.675,92

Total Unit Cost 1.455.318 1.311.598

Tariff (mark-up

20%)

1.746.381 1.573.917

Table 7 : Comparison of Hemodialysis Services Unit

Cost (Time Driven Activity Based Costing) with the

Hospital’s Tariff

Calculation Method Single Use

(IDR)

Re-use

(IDR)

Hospital calculation

of Unit cost

1.140.000 900.000

Unit cost time driven

activit

y

based costin

g

1.455.318 1.311.598

Ga

p

(

315.318

)

(

411.598

)

Hospital Tariff 1.368.000 1.080.000

Tariff of time driven

activity based coting

(unit cost traditional

costin

g

+ mark u

p)

1.746.381 1.573.917

Gap (378.381) (493.917)

Source: X Hospital (2017), has been reprocessed

4.3 Comparison of Unit Cost and Tariff based

on Traditional Costing dan Time Driven

Activity based Costing

Table 8 : Comparison of Unit Cost and Tariff Based

on Traditional Costing dan Time Driven Activity

Based Costing

Metho

d

Sin

g

le use Re-use

Traditional Costing 1.322.314 1.178.594

Time Driven Activity

Based Costin

g

1.455.318 1.311.598

Gap (133.004) (133.004)

Traditional Costing 1.586.774 1.414.313

Time Driven Activity

Based Costin

g

1.746.381 1.573.917

Gap (159.603) (159.604)

4.4 The Readiness of Human Resources,

Advantages, and Costs of Implementing

Time Driven Activity based Costing as a

Calculation Method of Service Unit Cost in

a Hospital

X hospital has possessed SPO for treatment at every

service that is provided in every unit, accompanied

with normal time or standard realization time of

every activity at that service. This indicates that X

hospital is ready to use time driven activity based

costing method when we looked at its human

resources aspect since they have gotten used to the

existing SPO. The SPO that they have had included

the understanding of action (treatment), objectives,

policies and procedures that are detailed in steps,

and the relevant units i.e. unit or installation as well

as labors who work in the activity.

The benefit of time driven activity based costing

method to X hospital is it gives information about

the costs of hemodialysis services more accurately

and gives information about the activities of every

service product. Meanwhile, in term of cost, if this

method is implemented, the tariff cannot be changed

directly. There are some things that need to be

considered such as getting approval from relevant

stakeholders, considering the purchasing capability

of the community around the area, and the

dependency toward the external stakeholders in

relation to the regional government regulations.

Even though it is quite complicated, at the end,

the calculation of unit cost for every service has to

be done in order to increase the finance management

of X hospital. Holding status as BLUD, X hospital is

expected to manage its own finance.

5 RESULTS

There was a difference calculation result of unit cost

between X hospital calculation and the traditional

costing calculation that was conducted in this study.

This difference might happen because X hospital did

not have cost system and did not do any cost

analysis. Also importantly, the unit cost calculation

formula that the hospital has been using was

obsolete and was not suitable anymore with the

current condition of the hospital.

In terms of comparison of unit cost and

hemodialysis services tariff using time driven

activity based costing method with unit cost, it

showed that there was undercosting case based on

the result of hospital’s calculation i.e. at the single

use and re use hemodialysis service. This needs to

Analysis of Cost Calculation System at X Hospital based on Traditional Costing and Time Driven Activity based Costing: Study at Unit

Cost Hemodialysis Services

1083

be X hospital’s concerns since the interview has

shown that the number of patients subjected to the

re-use hemodialysis was higher than single use

hemodialysis patients in 2017.

There was a significant difference in the result

of calculation using traditional costing and time

driven activity based costing for both types of

hemodialysis services. The result of unit cost

calculation using both methods had a significant

difference in which the result of the unit cost

calculation using traditional costing was IDR

133.004 lower than the result of unit cost calculation

using time driven activity based costing method. The

difference laid on the overhead cost calculation only,

meanwhile the charges calculation for direct

material and direct labor used the same calculation.

This difference was caused by the use of different

allocation methods for both methods i.e. traditional

costing used number of patient driver and time

driven activity based costing method allocated the

overhead cost based on the time for every group of

activities in hemodialysis services which consumed

the overhead cost component.

6 CONCLUSIONS

From the tariff calculation by adding mark-up 20%,

traditional costing and time driven activity based

costing methods had resulted in a higher tariff

compared to the current hospital’s tariff for both

types of hemodialysis services i.e. single use and re-

use. X hospital is highly advised to apply a better

unit cost calculation. The unit cost calculation will

be useful in making an informed decision regarding

the tariff that will be charged to the consumers. The

unit cost calculation is proven to be executed better

using time driven activity based costing method. It is

believed that by using the method, the resources’

allocation will be more accurate. Moreover, the

implementation of time driven activity based costing

is considered easier than activity based costing

method, which will also cost significant time and

money.

From the human resources point of view that are

available at X hospital, they can be considered ready

to implement the time driven activity based costing

method. This is supported by the existing SPO

system, in which every unit has informed counts of

the standard time to perform the given services.

Therefore, when the time driven activity based

costing method is introduced to them, it will not

change their regular activity drastically. The

implementation of time driven activity based costing

as a method for calculating the unit cost of services

also gives benefit to X hospital i.e. giving

information about hemodialysis services cost more

accurately and giving information about activities of

every service products. However, we need to keep in

mind that the changes in the tariff of services, when

time driven activity based costing method has been

implemented, cannot be done abruptly without

considering relevant factors and stakeholders.

REFERENCES

Baker, J. Judith. (1998). Activity Based Costing and

Activity Based Management for Health Care.

Gaithersburg, Maryland: Aspen Publisher, Inc.

Hansen, Don R., and Mowen, Maryanne M. (2015)

Cornerstones of Cost Management Third Edition.

South-Western: Cengange Learning.

Kaplan, Robert S and Anderson, S. R. (2007). Time

Driven Activity Based Costing. Boston,

Massachusetts: Harvard Business School Press.

Popesko, B., & Nová, P. (2014). Implementation of the

Process-Oriented Costing System in a Hospital

Department, 5(1).

https://doi.org/10.7763/IJTEF.2014.V5.345

Szychta, A. (2010). Time-Driven Activity-Based Costing

in Service Industries Time-Driven Activity-Based

Costing in Service Industries, (March).

UNICEES 2018 - Unimed International Conference on Economics Education and Social Science

1084