Analysis of the Implementation of the COSO Internal Control

Structure for Provision of Credit at PT. Bank Perkreditan Rakyat

Ferry Laurensius

1

, Sumini

1

and Melisa Sirait

1

1

Politeknik Wilmar Bisnis, Indonesia

Keywords: COSO, Internal Control Structure, Provision of Credit

Abstract: Uncollectible credit risk or bad credit may impede BPR operations. Risk can be avoided or minimized by

executing consistent internal control structures. If the internal control structure is sufficient in the provision

of credit, the implementation of credit provision can be controlled and able to prevent the occurrence of errors

that can inflict jeopardy on the bank. Object of this research is PT. BPR located at Tembung. This study aims

to determine whether the internal control of the credit systems in PT. BPR are in accordance with internal

control elements based on COSO and provide input or improvement that may be applied related to internal

control system. The research method is applied research using comparative method in data analyses. Data

collection by interview, observation and documentation. The research outcomes indicate that the

implementation of internal control system in PT. BPR is quite good, but there are still certain points which

are less suitable with the internal control system based on COSO and BI which need to be improved.

1 INTRODUCTION

The banking sector plays an important role in

supporting the running of the economy and national

development of a country by contributing to

providing loans to sectors that need funds. This can

occur because of the function of banks as

intermediary institutions where banks collect funds

from the community in the form of deposits and

channeling to the community in the form of credit and

or other forms. People's Credit Banks (BPR), which

is one type of banking, have a role in driving the

progress of economic equality and micro-economic

growth. The role of BPR in supporting Indonesia's

current national economic growth through increasing

access to credit or financing from banks. The problem

that often occurs in giving credit is bad credit. Bad

credit brings a threat to the continuity of BPR such as:

cash turnover slows down because cash availability

decreases, profits decline, liquidity ratio, solvency

and profitability are directly or indirectly affected.

This shows the influence on the health of BPR, where

the most tragic is that customers have no more trust.

PT. BPR X Tembung is a bank-shaped business entity

people's credit which has the main function to save

and channel funds (credit) to the community in the

Tembung area. Based on Law No. 10 of 1998, credit

is the provision of money or equivalent claims, based

on an agreement or agreement between banks and

other parties that requires the borrower to repay the

debt after a certain period of time with interest. PT.

BPR X Tembung also experienced a classic problem

faced by BPRs in general, namely non-performing

loans. At PT. BPR X Tembung itself, the level of non-

performing loans or bad loans has always increased

by almost 2% from 2014 to 2016. Even in 2016 the

NPL level shows that the NPL has exceeded the

prescribed limit. Bank Indonesia sets a limit for BPR

NPLs of 5%(Bank Indonesia, 2013).

To prevent the risks of bad credit that can hinder

the operations of the BPR, BPR is very necessary to

pay attention to the effectiveness of the internal

control structure in the BPR. Risks can be avoided or

minimized by implementing the internal control

structure consistently. If the internal control structure

is sufficient in providing credit, the implementation

of credit provision can be controlled and can prevent

the occurrence of errors that can harm the bank.

This study aims to determine whether the internal

control of the lending system at PT. BPR X Tembung

is in accordance with the elements of internal control

according to COSO and provides input or

1006

Laurensius, F., Sumini, . and Sirait, M.

Analysis of the Implementation of the COSO Internal Control Structure for Provision of Credit at PT. Bank Perkreditan Rakyat.

DOI: 10.5220/0009500810061010

In Proceedings of the 1st Unimed International Conference on Economics Education and Social Science (UNICEES 2018), pages 1006-1010

ISBN: 978-989-758-432-9

Copyright

c

2020 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

improvements that may be applied related to the

internal control system.

2 THEORICAL FRAMEWORK

The main source of income for rural banks (BPR) is

interest income derived from lending. When

distributing credit, BPRs face the risk of credit

collection where errors in the procedure for lending

can cause non-performing loans. The factors that

cause non performing loans are as follows (Fransisca

Claudya Mewoh, Sumampouw and Tamengkel,

2016):

a. External factors of the bank

1. There is doubtful intentions from debtors who

are in doubt.

2. There are difficulties or failures in the liquidity

process of the credit agreement that has been

agreed between the debtor and the bank.

3. Conditions of the management and business

environment of the debtor.

4. Disasters (for example: fire, natural disasters) or

business failures.

b. Internal bank factors

1. Lack of knowledge and skills of credit managers.

2. There is no credit policy at the bank concerned.

3. Provision and supervision of credit carried out by

banks deviates from established procedures.

One way to reduce the risk of non-performing

loans from the internal side is to design and

implement internal controls in the process of lending.

Bank Indonesia in its Guidelines for Internal Control

Standards for Commercial Banks (2003) states that an

effective internal control system is an important

component in bank management and is the basis for

healthy and safe financial operations. Internal control

is a supervisory mechanism established by

management on an ongoing basis, with a purpose

(Bank Indonesia, 2003):

1. Maintain and secure bank assets.

2. Ensure the availability of more accurate reports.

3. Improve compliance with applicable regulations.

4. Reducing financial / loss, the impact of

irregularities including fraud / fraud, and

violation of aspects of prudence.

5. Increasing organizational effectiveness and

increasing cost efficiency.

Elements of the Internal Control System The

COSO (Committee of Sponsoring Organizations of

the Treatway Commission) introduces five internal

control components that are interconnected with each

other, namely(Tampubolon, 2005):

1. Control Environment

2. Risk Assessment

3. Control Activities

4. Informasi dan Komunikasi

5. Monitoring

Weak internal control systems in banking institutions

can cause (Bank Indonesia, 2003)

lack of oversight mechanisms, unclear

accountability of Bank management and failure

in developing a culture of internal control at all

levels of the organization;

Inadequate implementation of the identification

and assessment of risks from the Bank's

operational activities;

the absence or failure of a principal control of the

Bank's operational activities, such as the

separation of functions, authorization,

verification and review of the risk exposure and

performance of the Bank;

lack of communication and information between

levels in the Bank's organization, especially

information at the take-up level

decision about the decrease in the quality of risk

exposure and

application of corrective actions;

inadequate or ineffective internal audit program

and other monitoring activities;

lack of commitment by the Bank's management

to carry out internal control processes and

enforce strict sanctions

3 RESEARCH METHOD

This type of research method is applied research that

uses comparative methods in analyzing data. The

object of research is the internal control system of

providing credit to PT. BPR X Tembung. The type of

data used in this study is qualitative data. The data

sources used in this study are:

Primary data, obtained directly from the object of

research in the form of data relating to the

procedure of lending and control.

Secondary data, obtained from the company in

the form of data and documents at PT. BPR X

Tembung and from other sources such as books,

journals, financial service authority regulations

(OJK) and Bank Indonesia.

The data collection techniques used by the authors in

this study are:

Observation, namely making direct observations

of activities or procedures for granting credit to

PT. X Tembung, with the aim of getting the data

needed in this study.

Analysis of the Implementation of the COSO Internal Control Structure for Provision of Credit at PT. Bank Perkreditan Rakyat

1007

Documentation, which is collecting data based

on documents and other related written reports

directly with this study.

Interviews, namely conducting interviews with

employees and Directors at BPR X Tembung.

4 ANALYSIS

Lending by BPR X Tembung in 3 consecutive years

has resulted in net profit, non-performing loans and

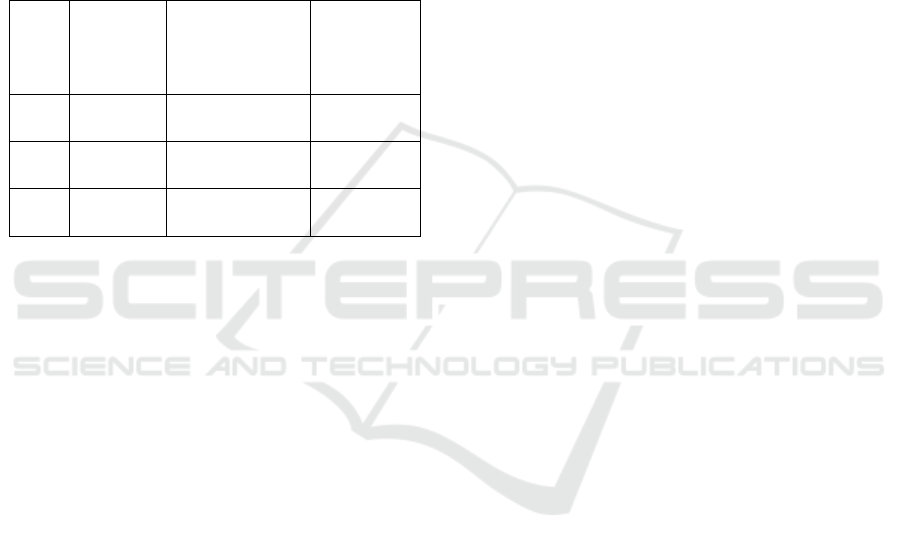

loan to deposit ratio as shown in the following table:

Table 1: Lending by BPR X Tembung

Year

Loan to

Deposit

Ratio

(LDR)

Bad Credit NPL

2014 83,78 % Rp 154.148.200 0,8881 %

2015 67,62 % Rp 73.442.300 2,48 %

2016 66,80 % Rp 205.297.600 5,66 %

From the table it can be seen that the LDR is very

large, the total channeled loans increase, but the net

profit decreases, and the condition of the NPL on

BPR X Tembung has increased sharply over the past

3 years. This can occur because of the abundant third

party funds indicated by the percentage of LDR.

Because third party funds are abundant and there

is a huge opportunity to get profits from lending,

credit is also being intensified to make a profit.

However, credit is experiencing congestion in

payments of principal and interest, so that it can affect

BPR income. In order to obtain optimal profit with

minimal bad credit risk, it can be achieved, it is

necessary to have a controlled and optimal credit

management through an internal control system in

granting credit. If the internal control structure that is

owned is consistent and adequate in granting credit,

then the implementation of credit provision can be

controlled and can prevent the occurrence of errors

that can be detrimental. Analysis of the internal

control system of PT. BPR X can be described as

follows according to COSO:

1. Control Environment

PT. BPR X Tembung has an organizational structure,

job description and decree that clearly explains the

division of tasks, responsibilities and work

relationships. However, there is still an

implementation that is not in accordance with the

organizational structure, namely the existence of

vacant positions (bill monitoring section).

In terms of integrity and ethical values, PT. BPR

X does not yet have a code of ethics guideline that

directs the ethical behavior of every employee,

especially employees in lending. Ethics and integrity

are carried out only based on Bank Indonesia

guidelines

In human resource policies, PT. BPR X Tembung

has procedures for the acceptance of new employees,

training, promotions, compensation. PT. BPR X also

has training activities & other motivational activities.

2. Risk assessment

PT. BPR X Tembung has not carried out a

comprehensive risk assessment and has no risk

universe and risk register. In credit distribution, only

5 C debtors are assessed. Important risk assessment is

carried out to design and implement internal controls

that are still needed in lending.

3. Control Activities

There are performance reviews conducted by top

management namely directors in terms of achieving

credit targets every month, against the target bills that

must be achieved every month and debtor payment

reports from month to month.

PT. BPR X Tembung also has and runs credit

policies and procedures contained in the Guidelines

for BPR (PKPB), and BPR X Tembung Credit

Guidelines (PP).

Segregation of duties in the procedure of lending

is carried out by several related functions. In the

credit process there are multiple functions, namely

survey functions and analysis functions carried out by

the same person from AO Lending which can cause

fraud where analysis is not carried out based on the

actual condition of the debtor. In terms of monitoring

bills there is a double duty. The task of monitoring

bills is carried out by other parts randomly, no special

unit is set to run).

There are certain controls or functions to check the

accuracy, completeness and feasibility of authorizing

all transactions credit, namely the internal control

department.

Credit distribution is carried out when authorized

by the authorities.

Credit documents are prenumbered.

Recording in journal is based on evidence of

incoming credit that has been authorized by the

authorized function and enclosed by a complete

document.

UNICEES 2018 - Unimed International Conference on Economics Education and Social Science

1008

In terms of physical control of assets, BPR X

performs physical matching between credit

documents, collection documents, proof of cash

receipts and debtor books. This is done by the Internal

Audit Function

4. Information and communication

There is an accounting information system that

includes methods and records in order to identify,

classify, analyze, classify, record / record and report

bank transactions contained in the PKPB & PP BPR

X Tembung. PT. BPR X also owns and runs a credit

management information system in the form

electronic or not electronic or system manuals using

forms / books / notes.

5. Monitoring

Monitoring should be carried out continuously

through the implementation of internal audits or

annual audits conducted by external auditors. Even

though it has an SPI function, based on the results of

the study, information is obtained that no audit has

been carried out in the process of lending, which

includes evaluation of risks and internal controls.

Monitoring in the BPR is only on checking

documents and administration related to the

implementation of lending by internal control by 1

person. Credit monitoring is carried out by taking into

account the debtor's loan deadline which must be

immediately visited or levied. Giving a warning to the

debtor if the installments or interest that are due are

not paid on time there are 3 times. Giving warnings

using the desk call and sms blast that has been

automated, and a letter for the third warning.

5 RESULTS

From the results of the analysis it was found that the

increase in bad credit at PT. BPR X Tembung can be

seen from the increase in the ratio of Non Performing

Loans, where the NPL of BPR X increased to 5.66%

in 2016. The increase in NPL could be caused by

external factors and internal factors. One of the

internal factors that influence the increase in problem

loans is the weak application of the Internal Control

Structure. Based on the results of the analysis, the

internal control of PT. BPR X must be addressed

immediately to reduce the risk of non-performing

loans. Some recommendations from the results of the

analysis of the Internal Control Structure of PT. BPR

X Tembung is:

1. Improve organizational structure and complete

with clear job descriptions and performance

targets in lending. Empty positions must be filled

immediately so that responsibility for managing

functions can be established.

2. Implement comprehensive risk management and

risk assessment in the function of lending.

Extensive risk assessment on the function of

lending must be followed by self assessment

(CSA) so that the risks of lending can be

immediately anticipated with adequate internal

controls.

3. The segregation of duties in lending is carried out

by separating the functions of the survey and

analysis so that the giving credit more leverage

and prevent fraud.

4. In terms of monitoring bills, it is recommended

that a special unit be assigned to carry out the

task of monitoring bills so that there is no

duplication of tasks that can cause fraud and

hinder other work.

5. Add personnel to the Internal Control department

and further develop the Internal Control program

or establish a special work unit for active

monitoring of the overall implementation of

lending (Audit Committee). Internal Audit /

Audit Committee will usually carry out analysis,

assessment and submission of suggestions. Audit

helps implement systematic, disciplined

evaluations & enhances the effectiveness of risk

management, control & regulatory processes,

and organizational management. This internal

audit is an added value that enhances BPR

operations.

6. Monitoring economic developments and

competing business debtors when current loans

can help BPR anticipate events that will occur on

loans. So that the relationship that wants to be

built between BPR and debtors that are not just

money and bank relations can be realized, thus it

can also create loyalty, and the family

atmosphere desired by BPR can be achieved.

6 CONCLUSIONS

Based on the discussion and analysis described

previously, the authors concluded that:

1. BPR X Tembung has an organizational structure

that is not suitable for its implementation, namely

the existence of vacant positions (bill monitoring

section). PT. BPR X should always make

adjustments and improve organizational

structures so that channels or information flows

are adequate, the objectives and processes

implemented are in line.

Analysis of the Implementation of the COSO Internal Control Structure for Provision of Credit at PT. Bank Perkreditan Rakyat

1009

2. BPR X Tembung does not carry out risk

management thoroughly. BPR X Tembung only

assesses the risk of the debtor (principle 5C).

BPR X should carry out risk management as a

whole because it can affect the achievement of

goals or objectives.

3. In the credit process there is a multiplication of

functions, namely the survey function and

analysis function carried out by the same person

from AO Lending which can cause fraud. BPR X

should separate the multiple functions that are in

the lending process, namely credit surveys and

analyzes conducted by people who are different

from AO lending.

4. In terms of monitoring bills there is a duplicate

of tasks (the task of monitoring bills is done by

other parts randomly, no special unit is set to run)

which can cause fraud and inhibit other work.

BPR X should reassign the bill monitoring

function unit, so that there is no duplication of

duties.

5. BPR X only monitor the completeness of

documents and administration related to the

implementation of lending by internal control by

1 person only and there is no stipulation or

establishment of a special work unit to actively

monitor the overall implementation of lending.

BPR X should add personnel to the Internal

Control section and further develop the internal

control program or establish an Audit Unit or

Audit Committee to actively monitor the overall

implementation of lending (monitoring

objectives, achievement strategies, financial

reporting, compliance with regulations, internal

controls, and recruitment and supervision).

REFERENCES

Bank Indonesia (2003) Pedoman Standar Sistem

Pengendalian Internal bagi Bank Umum dan Surat

Edaran No.5/22/DPNP, Bank Indonesia.

Bank Indonesia (2013) Pedoman Kebijakan dan Prosedur

Perkreditan Bagi Bank Prekreditan Rakyat dan Surat

Edaran No.14/26/DKBU, Bank Indonesia.

Fransisca Claudya Mewoh, Sumampouw, H. J. and

Tamengkel, L. F. (2016) ‘ANALISIS KREDIT

MACET (PT. BANK SULUT, TBK DI

MANADO)’, Jurnal Administrasi Bisnis, 4 (1).

Tampubolon, R. (2005) Risk and Systems Based Internal

Audit. PT.Elex Media Komputindo.

UNICEES 2018 - Unimed International Conference on Economics Education and Social Science

1010