Analysis of Development Revenue Cycle Information System for

Broadcasting of Television Media Advertisement: Case Study - PT XYZ

Anggiani Nyssa Clarissa

1

and Aria Farah Mita

1

1

Faculty of Economics and Business, Universitas Indonesia, Jakarta -Indonesia

Keywords: Accounting System Information, Revenue Cycle, FAST

Abstract:

This study aims to analyze the development of an information system of revenue cycle for the

broadcasting of television media advertisement at PT XYZ. Right now, there are two information

systems that used by PT XYZ and have not integrated yet with each other; those are Broadcast

Management System (BMS) as an advertisement production system and Oracle Finance

(ORAFIN) as an Enterprise Resource Planning (ERP) system. Moreover, there are is no main

feature integrated yet in the system that caused several problems that affect the performance of

the related divisions. As a result, it can make a different values of an advertisement billing

because the current system does not meet the user needs. This research is a case study with a

qualitative method. The research methodology is using Participatory Action Research (PAR),

where researchers use users of information systems directly PT XYZ to identify information of

information systems that exist nowaday and analyze their subsequent needs. Data was acquired

by interview, documents analysis, and observation at PT XYZ. The method used to develop

information systems of revenue cycle is FAST (Framework for the Application of System

Technique) method. The result of this study provides a new revenue cycle information system

that can integrate the existing system to minimize the billing error and provide the reliable

information as based on decision making.

1 INTRODUCTION

Nowadays, television media is one of the media that

has great potential of influencing public opinion of

an issue. Television media is still considered as an

information center for most people in the world,

include in Indonesia.

Along with the number of private television

stations that have sprung up, then advertisement has

become something that must be on every television

broadcast in Indonesia. Furthermore, advertisement

is one of the most effective marketing

communication media and is one of the biggest

supporters in operational activities that can increase

company profits.

In this era, the development of information

systems and the application of information

technology is increasingly rapid. This situation is the

basis for a company or organization to develop more

professionally in terms of performance effectiveness

and efficiency. Each company has a different

strategy from other companies for reaching the

expected targets. Therefore, in order to achieve

company goals, each company is required to

implement and develop an information system that

can support the company's internal control as a

support in the right decision-making process. With

the support of a well-designed information system,

the information produced will be precise and

accurate so that the company is superior in

competing with other companies.

Moreover, the development of the current

business environment clearly great affects the

company's workflow and business cycle that

requires them to be able to provide services quickly

and accurately. Therefore, company that operates in

the media industry are advised to use qualified

information technology, so that the wishes of

corporate stakeholders can be fulfilled properly and

optimally.

For television companies, advertisement is the

main requirement for the continuity of broadcast

Clarissa, A. and Mita, A.

Analysis of Development Revenue Cycle Information System for Broadcasting of Television Media Advertisement: Case Study - PT XYZ.

DOI: 10.5220/0009498409550962

In Proceedings of the 1st Unimed International Conference on Economics Education and Social Science (UNICEES 2018), pages 955-962

ISBN: 978-989-758-432-9

Copyright

c

2020 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

955

production. Without advertisement, the television

station will have difficulties to face a business

competition in media industry. Those advertisements

that appear on televisions are become company’s

main income to run the wheels of business, that is

for finance any production including production

costs for broadcast the programs and show on that

television.

To be able to display advertisments on television,

a company of products, services, or place of

business must be contact the television. The aim is

to arrange retated matters of advertising, such as

how much the advertisement costs per second, when

the advertisement will appear, in what program the

advertisement will appear and so on. Therefore, an

information system and technology are needed to

arranging and processing all related matters of the

advertisement serving. Starting from the request to

make an advertisements, advertisement serving, until

payment billing of advertisement that become

revenue for television Company.

In this research, the author will examine

information and technology systems of revenue

cycle that is in one of the television media

companies in Indonesia, namely XYZ Company. At

present the information system applied to XYZ

Company still has several weaknesses, there is does

not yet has several features that are integrated in the

system, thus raises several problems that affect the

performance of related divisions within the

company.

This research has two research questions, the

first is how to control the current revenue cycle

information system for advertisement serving

activities and how the design of revenue cycle

information system development in the new

advertisement serving activity at XYZ Company.

The purpose of this research is to analyze the

control of current revenue cycle information system

and provide recommendations for system

development design in advertisement serving on

XYZ Company called the Smart Intelligence

Broadcasting Orchestration System.

2 THEORICAL FRAMEWORK

According to Romney and Steinbart (2015), internal

control is a process carried out to providing adequate

guarantees for the purposes of internal control,

including safeguarding assets, managing records

with good detail to report company assets fairly and

accurately, providing information that is reliable and

trustworthy, prepare financial reports that are in

accordance with predetermined criteria, improving

operational efficiency, encouraging compliance with

predetermined managerial policies, and complying

with applicable laws and regulations.

Meanwhile, internal control according to

Mulyadi (2002) is a series of actions that are

pervasive and become an inseparable part, not only

as an addition, from the entity’s infrastructure.

Romney and Steinbart (2015) stated that

accounting information system is about of

collecting, recording, storing, and processing data to

produce information for decision makers. This

system includes people, procedures and instructions,

data, software, information technology

infrastructure, as well as internal controls and

security measures.

There are six components of the accounting

information system, namely:

a) People who use the system;

b) Procedures and instructions used to collect,

process and store the data;

c) Data about the organization and its business

activities;

d) Software used to process data;

e) Information technology infrastructure, including

computers, peripheral devices, and

communication network devices used in

Accounting Information System (AIS);

f) Internal controls and security measurements that

store AIS’s data.

According to Romney and Steinbart (2015),

revenue cycle is a series of business activities and

continuous processing of related information

processing that provides commodities and services

for costumer and receive cash as payment for the

sales.

The thinking framework used in conducting this

research begins with determining the background for

choose a research topic, then proceeding to

determine the problem in the study, the purpose of

the research, the contributions of the research, the

limitations of the research and the methodology

used, and systematics in this study. Furthermore, a

collection of various literature related to this study

was also conducted. The two stages above are stages

in the planning section.

Then when the planning has been carried out, the

next stage is the analysis phase. At this phase of the

analysis, the data needed is a general description of

the company along with its vision and mission. In

addition, information is also needed is about the

company's business processes, so that problems can

be analyzed and how to recommend solutions for

future needs. From the various data that have been

UNICEES 2018 - Unimed International Conference on Economics Education and Social Science

956

obtained, the analysis will be carried out using the

theoretical literature in this study. Theoretical

literature used is, the theory of internal control,

information systems, revenue cycle and the method

of developing information systems that used, there is

FAST (Framework for the Application of Systems

Technique).

In the design phase, recommendations for

solutions proposed in the analysis phase must be

present in system design according to the FAST

(Framework for the Application of Systems

Technique) approach developed by Whitten and

Bentley (2007).

For the system development, an agile method –

FAST (Framework for the Application of Systems

Technique) – was used because its comprehensive

approach (Whitten and Bentley, 2007). FAST

method consists of phases as follows (this research

used four early phases):

(1) Scope definition. The purpose of the scope

definition phase is twofold. First, it answers the

question, “Is this problem worth looking at?”

Second, and assuming the problem is worth looking

at, it establishes the size and boundaries of the

project, the project vision, any constraints or

limitations.

(2) Problem analysis. This phase studies the

existing system and analyze the findings to provide

the project team with a more thorough understanding

of the problems that triggered the project.

(3) Requirements analysis. This phase defines

and prioritizes the business requirements. Simply

stated, researcher approaches the users to find out

what they need or want out of the new system.

Logical design. This phase translates business

requirements into system models. The logical design

will use system design tools like functional

decomposition diagram (FDD), data flow diagram

(DFD), entity relationship diagram (ERD), and user

interface design.

3 RESEARCH METHOD

This research was conducted in order to answer

existing research questions, those are:

a) How to control the current revenue cycle

information system of advertisement serving

activity at XYZ Company?

b) How is the design of the revenue cycle

information system development in the new

advertisement serving activity at XYZ

Company?

This research is a case study with a qualitative

method using primary and secondary data. The

method used to obtain these data is as follows.

a) Interviews and Observations

Field research was conducted directly at XYZ

Company to obtained data and information

needed by observation. This observation aims to

study current operational activities. Primary data

is obtained by interviewing related divisions of

account receivable flow, those are the Sales

Division, Traffic Division, Billing Division and

Collection Division at XYZ Company.

Meanwhile, secondary data is obtained by

studying the Standard Operational Procedure

(SOP) that applies to each related divisions.

b) Participatory Action Research (PAR)

According to Yoland Wadworth in Agus Afandi

(2013) Participatory Action Research (PAR) is a

research method which implemented in a

participatory manner among a group of people in

a community. This research involves all relevant

parties in actively examining together the current

actions or conditions (which they experience as

problems) in order to change and correct them.

In this research, the researchers directly

involved the revenue cycle users information

system at XYZ Company to directly identify the

problems and weaknesses of the existing

accounting information system and analyze their

subsequent needs.

Researcher in this research act as authors and

actors of the system, because researcher in this

case are actively involves in the company's

business processes. Information about the current

problems is identified by conducting interviews

with several respondents from related divisions.

Those are, the Sales Division, the Traffic

Division, the Billing Division and the Collection

Division as the users of the revenue cycle

accounting information system.

The result of the interview that have been

conducted will be summarized and concluded as

the main problems that experienced by system

users.

4 ANALYSIS

4.1 System Analysis

In this phase, an analysis of the current business

process description of the company will be carried

out. Then, it will explain the problems faced in

Analysis of Development Revenue Cycle Information System for Broadcasting of Television Media Advertisement: Case Study - PT XYZ

957

implementing the business process. Those problems

will be analyzed on the implementation of the

revenue cycle accounting information system that is

still ongoing today and formulated the right solution

for system improvement so that it can overcome

these problems.

4.1.1 Scope Definition Phase

To analyze the accounting information system of

XYZ Company, it begins by determining the scope

using the PIECES framework (Performance,

Information, Economics, Control, Efficiency,

Service) developed by James Wetherbe in Whitten

and Bentley (2007). The following is a table that

shows the problems faced by XYZ Company and

opportunities for solutions that can be applied to

determine the scope of system development.

Information in this table is obtained from direct

observation and direct interviews with all relevant

parts at XYZ Company.

Table 1: The Framework of PIECES

No Existing Problems The Opportunities

Performa

nce

(1) In the sales process,

the income report

has not been

monitored

systemically.

The income report

can be monitored

continuously and

automated.

(2) The company has

trouble to manage

the cash flow for

other importance

activities.

The company can

manage cash flow if

the income report

information can be

known reliably.

(3) Less effective and

efficient in the entire

real time collecting

information.

The company can

caries out the

production activity

and finances report

effectively and

efficiently if there is

a new information

system

development.

Informati

on

(4) This time the

information about

sales data should be

imported manually

from BMS system to

ORAFIN system.

Sales data is updated

and imported

automatically.

(5) The data have not

integrated well and

it is not easy to

fulfill the new

information needed.

All data is well

integrated and can

fulfill the other new

information needed.

Economi

cs

(6) There are

differences value of

The incorrect

collection of

an advertisement

billing.

advertisement

billing can be

minimized by the

development of new

information system.

(7) Income cannot be

accurately identified

Income can be

accurately identified

Control

(8) The unavailability of

information about

advertisement detail

can trigger errors

differences value of

an advertisement

billing.

The incorrect

collection of

advertisement

billing can be

minimized by the

development of new

information system.

(9) The company has

trouble to manage

the cash flow for

other importance

activities.

Information on

advertisement

revenue will help to

make the right

decision on XYZ

Company’s cash

inflows and cash

outflows.

Efficienc

y

(10) The existing system

still not fulfill the

user needs so that

need a excessive

effort to produce the

accurate revenue

information

periodically.

The production

process and

recording off all

broadcast activities

and its conversion

are more effective

and more efficient if

there is a new

system

development.

Service

(11) The employee and

management have

difficulties to get a

reliable information.

(a) Facilitate the

employee in

doing any

broadcast

production

activity and

reporting.

(b) Facilitate the

management to

access the

existing report.

(c) Facilitate all of

divisions to find

the source of

trouble because

every activity has

been recorded in

the system.

4.2 Problem Analysis Phase

The goal of the problem analysis phase is to study

and understand the problem domain well enough to

thoroughly analyze its problems, opportunities, and

constraints (Whitten and Bentley, 2007).

In this phase, an analysis is carried out on the

problems that arise in the business process because

there is no development of information systems that

appropriate with the user needs. As identified in the

PIECES framework, from the results of the

UNICEES 2018 - Unimed International Conference on Economics Education and Social Science

958

interview with several related divisions in the

company, those are: the Sales, Traffic, Billing and

Collection divisions, table 2 describe some of the

solutions proposed in overcoming the problems that

occur in the revenue cycle information system

development process PT XYZ.

Table 2: The analysis of cause and effect previous

system and solutions for new system

No Inhibitor Effect Proposed

Solution

1. Broadcast

Manageme

nt System

(BMS) as

the system

used to

process the

advertisem

ent

broadcasti

ng is not

directly

integrated

with

ORAFIN

as an ERP

system.

1. Sales data must be

imported from BMS to

ORAFIN at the end of

each month. The risk is

that if there is an

incomplete processing

then the data will not

imported entirely so it

must be re-imported

continuously until the

data can be moved

entirely into the ORAFIN

system.

2. Another thing is if one of

the clients requests an

invoice before the XYZ

Company’s specified

date, then the billing

division must import the

client’s sales data one by

one over the client’s sales

data to issuance an

invoice.

An

information

system that

can integrate

BMS with

ORAFIN is

needs to be

made. So, all

of sales data

can be

updated

realtime.

2 The

making of

package

order is

still done

manually

by using

Ms. Excel.

It is done

by the

Marketing

Division.

The Traffic Division

cannot supervise the

system over the client

budget which used in

certain month, whether or

not the budget is

appropriate with the

package that has been

approved.

An

information

system that

can provide

the create

package

order feature

that

integrated

with the

other

programs in

the system is

needs to be

made.

3 The

making of

media

order is

still done

manually

by using

Ms. Excel.

It is done

by the

Sales

Division.

1. Traffic Division have to

input the manual media

order to the BMS system.

2. If there are additional

orders, it will probably

trigger errors in the

number of billing to

client because the

additional order cannot

be automatically updated

by the system.

An

information

system that

can provide

the create

media order

feature that

integrated

with the

other

programs in

the system is

needs to be

made.

4 The

existing

system

does not

has a

detailed of

database

advertisem

ent

serving.

The Collection Division

cannot know the real

value of the broadcast

when billing clients each

month. So, there is a

difference between the

value stated on the

package or media order

and the value in the

system because the sales

1. An

information

system that

can provide

the database

of the

advertiseme

nt or

programs

broadcast

value has not been

updated automatically.

detail is

needs to be

made. So,

the

Collection

Division can

reconciliatio

n if there is a

difference in

the nominal

value of the

bill.

2

. This system

information

is also can

provide the

Intelligent

Alert feature

on the

changes that

occur during

the

broadcasting

process.

Therefore,

when there

is a shift in

broadcast

time, then it

will

automaticall

y give

notification

on emails to

the Account

Executive

(AE) so the

AE can

immediately

inform this

shift to the

client who

coordinating

the next

client

request.

5 There is no

online

database

system for

storing

billing

documents

files.

The Collection Division

must look for invoices file

and its completeness such

as sales packages, tax

invoices, log proof, and

other related documents

to invoice’s storage

warehouse.

Provides an

online

database to

store the

invoices and

their

completeness

combined in

one folder

according to

the invoice’s

number.

4.3 Requirement Analysis Phase

After analyzing the existing problems and doing a

more detailed understanding, an analysis is carried

out to determine the user's needs for the

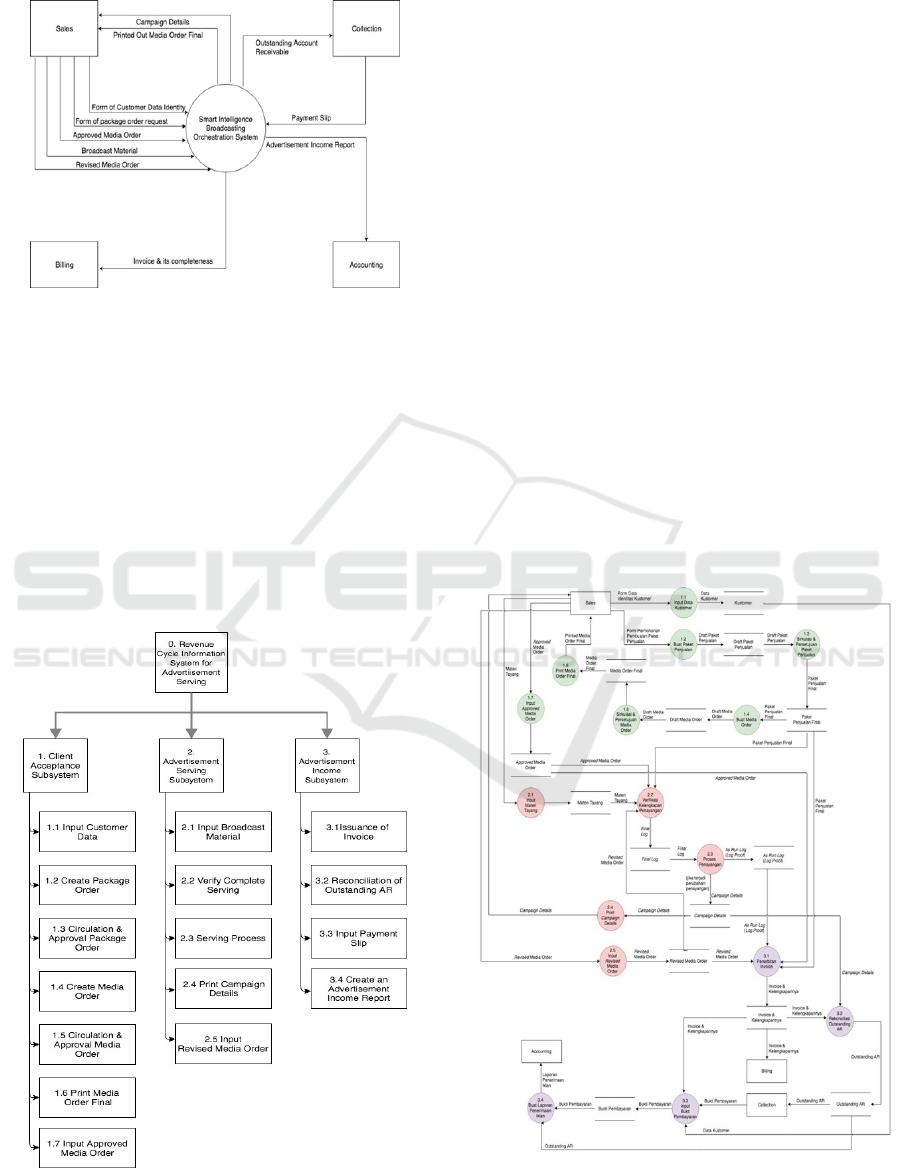

development of the system by making a context

diagram. Context diagram is a diagram that can

describe the relationship between the system and the

business as a whole. The related relationship is

described as the flow of information and data that

enters the system and exits the system. The

information system context diagram for

Analysis of Development Revenue Cycle Information System for Broadcasting of Television Media Advertisement: Case Study - PT XYZ

959

advertisment serving revenue cycle can be seen in

the following figure.

Figure 1: Context Data Flow Diagram

After creating a context diagram, then the Functional

Decomposition Diagrams is arranged. According to

Whitten and Bentley (2007), Functional

Decomposition Diagrams (FDD) are made with the

aim of describing the components contained in the

system and sub-systems separately. Decomposition

diagram shows top-down functional decomposition

or system structure. FDD is the first step in making

a diagram flow. From the FDD compiled, later Data

Flow Diagrams (DFD) can be created. FDD

Information system for advertisement serving

revenue cycle can be seen in the following figure.

Figure 2: Functional Decomposition Diagram (FDD)

4.4 Logical Design Phase

This stage of logical design will transform the

business requirements into a system both in the

process and process data model. The purpose of this

logical design is to obtain a more detailed picture of

the information needed to develop an information

system for the advertisement serving revenue cycle.

Process modelling will be described by Data Flow

Diagrams (DFD), while data modelling will be

described by using the Entity Relationship Diagram

(ERD).

4.4.1 Process Modelling

According to Whitten and Bentley (2007) process

modelling is a technique used to organize and

document the structure and flow of data from a

system or logic, policies, and procedures so that it

can be implemented by the system process.

To do process modelling, one technique that can

be used is Data Flow Diagrams (DFD). DFD is a

tool in modelling that allows system analysis to

describe the system as a network of functional

processes that are connected to each other by the

flow of data, both manually and computerized. Data

Flow Diagram Information system of advertising

revenue cycle can be seen in the following picture.

Figure 3: Data Floxew Diagram

UNICEES 2018 - Unimed International Conference on Economics Education and Social Science

960

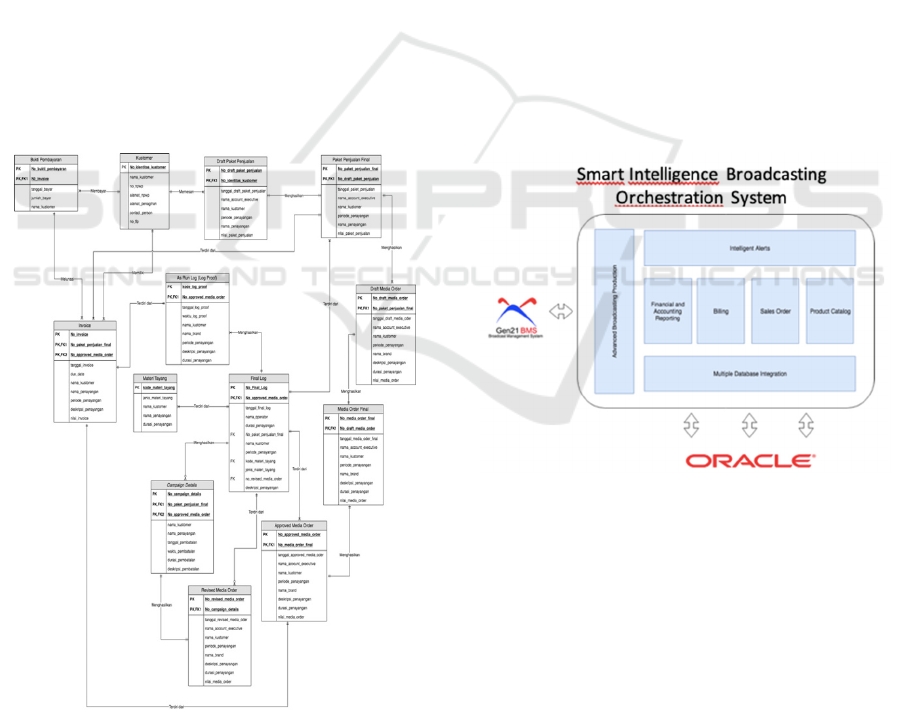

4.4.2 Data Modelling

Data modelling is a technique in organizing and

documenting the data that the system has. Often

referred to as database modelling. The first step in

modelling data is to determine the entities contained

in the system. Information system database entity of

XYZ Company’s revenue cycle is determined by

looking at the requirements of the system. After

determining the entities contained in the system,

then the next analysis is carried out to determine the

relationships between entities. Relationships are

natural business relationships between one or many

entities (Whitten and Bentley, 2007). Next, an

analysis is carried out to determine the cardinality

between entities. Cardinality is the minimum and

maximum number of occurrences of an entity and its

relation to the emergence of other entities. After

analyzing the relationship and cardinality between

entities in the revenue cycle information system, the

entity as a whole can be described in a fully attribute

data model diagram in the form of an entity

relational diagram. Figure 4 shows the Entity

Relationship Diagram data model for XYZ

Company's advertising revenue cycle information

system.

Figure 4 Fully Attribute Entity Relationship

Diagram

4.5 Designing the User Interface

In designing this advertisement serving revenue

cycle information system, the author uses

middleware device technology, which is to integrate

two different systems, those are the Broadcast

Management System (BMS) as a processing system

for displaying advertisements or programs in the

television industry with Oracle Finance (ORAFIN)

as an Enterprise Resources system Planning (ERP)

used by XYZ COMPANY to be able to

communicate between one and the other in

processing data in realtime. In this case, the

middleware device also provides features to create

integrated sales and media order packages and

access to approve that sales documents. In addition,

the Intelligent Alert feature is also provided, where

this feature serves to provide automatic e-mail

notifications to the Account Executive (AE) for

changes in impressions that occur and save the

changes in the database provided.

The following is the information system design

of the advertisement serving revenue cycle, named

the Smart Intelligence Broadcasting Orchestration

System, which was recommended by the author to

XYZ COMPANY.

Figure 5: Smart Intelligence Broadcasting

Orchestration System Design

5 RESULTS

The result of this research are the solution for XYZ

Company in the form of a revenue cycle information

system that has been integrated with the BMS and

ORAFIN systems. In this system, a sales package

and media order feature has been provided, the

database of advertisement or program broadcast

details, and an online database for storing invoices

and other equipment. In addition, this system has the

intelligent alert feature in the form of e-mail

Analysis of Development Revenue Cycle Information System for Broadcasting of Television Media Advertisement: Case Study - PT XYZ

961

notifications to the relevant Account Executive (AE)

for changes in impressions that occur during the

broadcasting process. With the creation of an

revenue cycle information system, it is expected to

minimize the occurrence of advertisement billing

error and provide reliable information as based on

decision making.

6 CONCLUSIONS, SUGGESTION

& LIMITATION

6.1 Conclusions

From the result of analysis and data collection that

has been conducted by the authors, conclusions can

be taken as follows:

1. The information system of the advertisement

serving revenue cycle that has been designed

allows companies to minimize advertisement

billing error. With the availability of the main

features that have been integrated, it will make it

easier for companies to carry out their activities.

2. Beside that, the revenue cycle information

system designed is an information system based

on realtime so that all changes that occur during

advertisement serving can be identified and can

be handled quickly.

6.2 Suggestion

Based on these conclusions, the author has

suggestions that can be considered for the

improvement and progress of the company, there is

the implementation of revenue cycle information

systems development is expected to help companies

to dealing with the problems that has been identified

in chapter 4. However, to reach the objectives to be

achieved, when implementing the revenue cycle

information system for the advertisement serving the

company must take appropriate steps. Companies

need to do a systematic way and follow existing

rules, such as proceeding to the phase of system

physical design, system testing, and maintenance of

the system. Although this does not guarantee the

success of implementing a system, work that follows

the rules will bring closer results.

6.3 Research Limitation

The limitations of this study are only using the 4

stages of the FAST method, which only reaches the

logical design stage. Research also has limited

coverage because the analysis carried out only on

the revenue cycle information system of the

advertisement serving regardless of the

organization's needs for other systems. In addition,

the design of this system can also be developed

through the development of a better architecture so

that system users can easily operate this system.

REFERENCES

Afandi, Agus. (2013). Modul Participatory Action

Reseacrh (PAR). IAIN Sunan Ampel Surabaya:

Lembaga Pengabdian Masyarakat (LPM).

Mulyadi. (2002). Auditing. Jakarta: Salemba Empat.

Romney, M. B., & Steinbart, P. J. (2015). Accounting

Information Systems (13rd ed.). New Jersey: Pearson

Education, Inc.

Whitten, J.L, dan Lonnie D. Bentley (2007). System

Analysis and Design Methods. 7

th

Edition. McGraw-

Hill Company, New York.

UNICEES 2018 - Unimed International Conference on Economics Education and Social Science

962