The Role of Islamic Microfinance to Support the Growth of

Small – Medium Enterprises: Case Study of SMEs in Jakarta, Depok,

Bogor and Tangerang

Amanda Riany Putri

1

, Irfani Fithria Ummul Muzayanah

1

and Rahmatina Awaliyah Kasri

1

1

Faculty of Economics and Business, Universitas Indonesia, Jakarta-Indonesia

Keywords: Islamic microfinance, SMEs, OLS

Abstract: The role of Small and Medium Enterprises (SMEs) become prominent in the economic development of a

country. However, despite of their importance, SMEs have less access to formal source of external finance.

The rise of Islamic microfinance is expected to overcome the financial constraint facing by SMEs.

Accordingly, this study aims to investigate the role of islamic microfinance on the growth of small -medium

enterprises. The sample comprised of 160 customers of four islamic microfinance institution located in

Jakarta, Bogor, Depok, dan Tangerang. The regresion results empirically show that islamic microfinance

variables used in this research are positively related with the growth of small – medium enterprises in the

samples. Trainings and loan frequency are significant to affect the growth of SMEs.

1 INTRODUCTION

Globally, SMEs have proven to contribute

significantly to GDP and also to employment

(EdinburghGroup,2014). As a developing country,

MSMEs certainly have a very important role for the

Indonesian economy (Sarwono,2015). In the last five

years, the contribution of the MSME sector to

Indonesia's Gross Domestic Product increased from

57.84% to 60.34% (Kemenperin,2018).

However, SMEs globally have a major problem

that is the limitations of capital (Christopher,2010).

Lack of access to financial support has been identified

as one of the main problems for the growth of SMEs

globally, also in Indonesia (Sarwono,2015). There are

about 60-70% of MSMEs in Indonesia have not been

able to get access to financing or credit from banks

(Sarwono,2015). This is based on the fact that there

are still few banks that can reach the remote areas of

UMKM throughout Indonesia. In addition, there are

also administrative constraints of MSMEs that do not

meet the requirements. Therefore, the existence of

Micro Finance Institution and Sharia Micro Finance

Institution in Indonesia is a solution to reduce the

problem of capital limitations to MSMEs. The

success of microfinance institutions has been proven

and successful in Muslim-majority countries such as

Indonesia, Bangladesh, Pakistan, Turkey and others

(Rokhman,2013). However, this product does not

meet the needs of all Muslim clients.

Today, sharia financial institutions are a

growing industry worldwide. This is because Islamic

financial institutions have their own attractiveness

that is the practice in accordance with Islamic

principles and theories (Amin et al.,2011). In

Indonesia, the growth of sharia financial institutions

is an interesting phenomenon. Not only sharia

banking, shariah micro-finance institutions are also

growing and increasing in number. Referring to the

market potential and the important role of of Islamic

Microfinance Institution, therefore,

Research from Rokhman (2013) showed that

microfinance has an important role in increasing

income levels, children's education, and business

progress. However, Babajide (2012) revealed an

inverse result that microfinance in Nigeria did not

increase the growth of MSMEs. Hence, this study

aims to investage whether islamic financing can

support MSMEs’ growth.

950

Putri, A., Muzayanah, I. and Kasri, R.

The Role of Islamic Microfinance to Support the Growth of Small – Medium Enterprises: Case Study of SMEs in Jakarta, Depok, Bogor and Tangerang.

DOI: 10.5220/0009497609500954

In Proceedings of the 1st Unimed International Conference on Economics Education and Social Science (UNICEES 2018), pages 950-954

ISBN: 978-989-758-432-9

Copyright

c

2020 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

2 LITERATURE REVIEW

In general, Islam supports the rotation or transfer of

wealth from surplus units to deficit units that will

assist in the development of socio-economic welfare

of the needy (Ali et al.,2015). Financing in Islam has

two main goals. First, financing in Islam has the goal

of channelling resources and wealth from surplus

units to deficit units. Second, to meet human needs

and enable Muslims to improve their welfare (Kahf

and Khan,1992). Basically, Islam does not encourage

someone to carry debt. Every debt must be based on

real needs, therefore as much as possible Islam

regulates its people to have no debt. (Amin et

al.,2011).

A numerous of empirical studies has been

conducted to investigate the role of microfinance in

supporting the growth of SMEs. Adnan & Ajija

(2015) investigate the effectiveness of Baitul Maal

wat Tamwil (BMT) in reducing poverty. The

empirical results show that financing from BMT is

significant in reducing poverty. The findings confirm

that most respondents experiencing an increase in the

level of income after receiving financing from BMT.

Other BMT’s products, especially mudharabah, have

positive contribution to empower the poor in various

productive programs and also able to reduce the level

as well as the severity of poverty.

While Awuah and Addaney (2016) provide

another empirical evidence to support the argument

that there is positive relationship between

microfinance and SMEs growth in Kenya. This study

is a survey – based approach and employ data from

152 respondents. After getting financing from

microfinance, there is an evident that the level of

revenue, profit and assets of the respodents have

increased. Furthermore, the results also provide that

non – financial services and products of the

microfinance institution such as managerial training

and business consultation services also significant as

major contribution in increasing the growth of SMEs.

Thuo (2015) investigates the effect of

microfinance services on growth of SMEs in Nairobi.

The variables used in the estimation consist of the

amount of microloan, number of training, total

savings done by the SMEs in microfinance

institutions and legal composition. The results show

that microfinance services (the amount of financing,

training and savings) have a positive effect on SME

growth. The result find an interesting result that the

amount of microloan alone has a negative impact.

However, this study concludes that there is a strong

positive relationship between combined microfinance

services and company growth.

In addition, Mohamed and Al-Shaigi (2017)

analyze the effect of microfinance on poverty

reduction using the case of Sudan. The study using

primary data gathered from interview and

questionnaires. They use three dimensions to evaluate

the performance of microfinance : outreach,

sustainability and business development. The result

show that business development is positively

influenced by microfinance in the sense that it can

increase the level of employment, while microfinance

only contribute a moderate effect on outreach to the

poor and sustainability.

The study of Siyad (2013) examines how lending

from microfinance institution influence the growth of

small and medium enterprises in Somalia. The result

also corroborates the existing studies that

microfinance’s lending play as significant factor in

affeting the growth of SMEs in Somalia. Moreover,

Aldesta (2014) using multiple regression approach

finds that microfinance variables proxied by the

frequency of financing, duration of business, and the

amount of financing have a positive and significant

effect on business development.

Antonio (2011) argue that Baitul Maal wat

Tamwil (BMT) has potential role as a strategic

community – based micro lending initiative. The

study emphasizes that islamic microfinance play as an

alternative source of finance for SMEs in Indonesia.

3 RESEARCH METHOD

The data in this study is used primary data sources,

namely original data obtained directly by researchers

for purposes related to the problem being studied

(malhotra, 2010). Furthermore, the primary data used

in this study was obtained from field research (survey

– based approach) using a questionnaire. The

questionnaire was distributed to respondents who

were customers of islamic microfinance institutions

in Jakarta, Bogor, Depok, and Tangerang. This study

employs a questionnaire distributed through door to

door to the location of business / home of the

respondent to obtain the data.

Respondents in this study are customers who

were getting a sharia microfinance scheme islamic

microfinance institutions. The product of islamic

microfinance here is also specific which refers to

productive financing such as credit financing. This

study utilizes customers who had used islamic

microfinance services and loan, therefore, the

influence of islamic financing could be clearly seen

and analyzed.

The questionnaire was adapted from past studies.

A total of 160 survey questionnaires were distributed

to customers who are taking islamic micro financing

scheme from 4 islamic microfinance institution

located in Jakarta, Bogor, Depok, and Tangerang.

The Role of Islamic Microfinance to Support the Growth of Small – Medium Enterprises: Case Study of SMEs in Jakarta, Depok, Bogor

and Tangerang

951

Institution consists of 2 Baitul Maal wa Tamwil and

2 Bank Pembiayaan Rakyat Syariah (BPRS). The

total samples in this research are consist of 160

respondents.

In this study, the method used in sampling is

nonprobability sampling, and using convenience

sampling technique. Convinience sampling or

incidental is a sample determination technique

selected by chance, ie anyone who accidentally meets

the researcher and can be used as a suitable sample

for the data source (Sugiyono, 2017).

The independent variables are financing

frequency, average amount of financing, duration of

financing, and also training. There are also control

variables such as age, education, marital status,

gender, business age, and business location. While

dependent variable used in this study is profit growth

after receiving islamic microfinace to proxy thr

growth of SMEs. Using multiple regression, this

study estimate the following estimation :

𝑔𝑟𝑜𝑤𝑡ℎ 𝛼0 𝛽𝑖 𝑆𝐶 𝛽𝑗𝐵𝑢𝑠𝑖𝑛𝑒𝑠𝑠

𝛽𝑘 𝑀𝑖𝑐𝑟𝑜𝑓𝑖𝑛𝑎𝑛𝑐𝑒 𝜇

where :

growth : business growth

SC : vector of respondents’s socio – demographic

factors

Business : vector of respondent’s business

characteristics

Microfinance : vector of islamic microfinance

variables

The detail of the definition of each variables are given

in the following table :

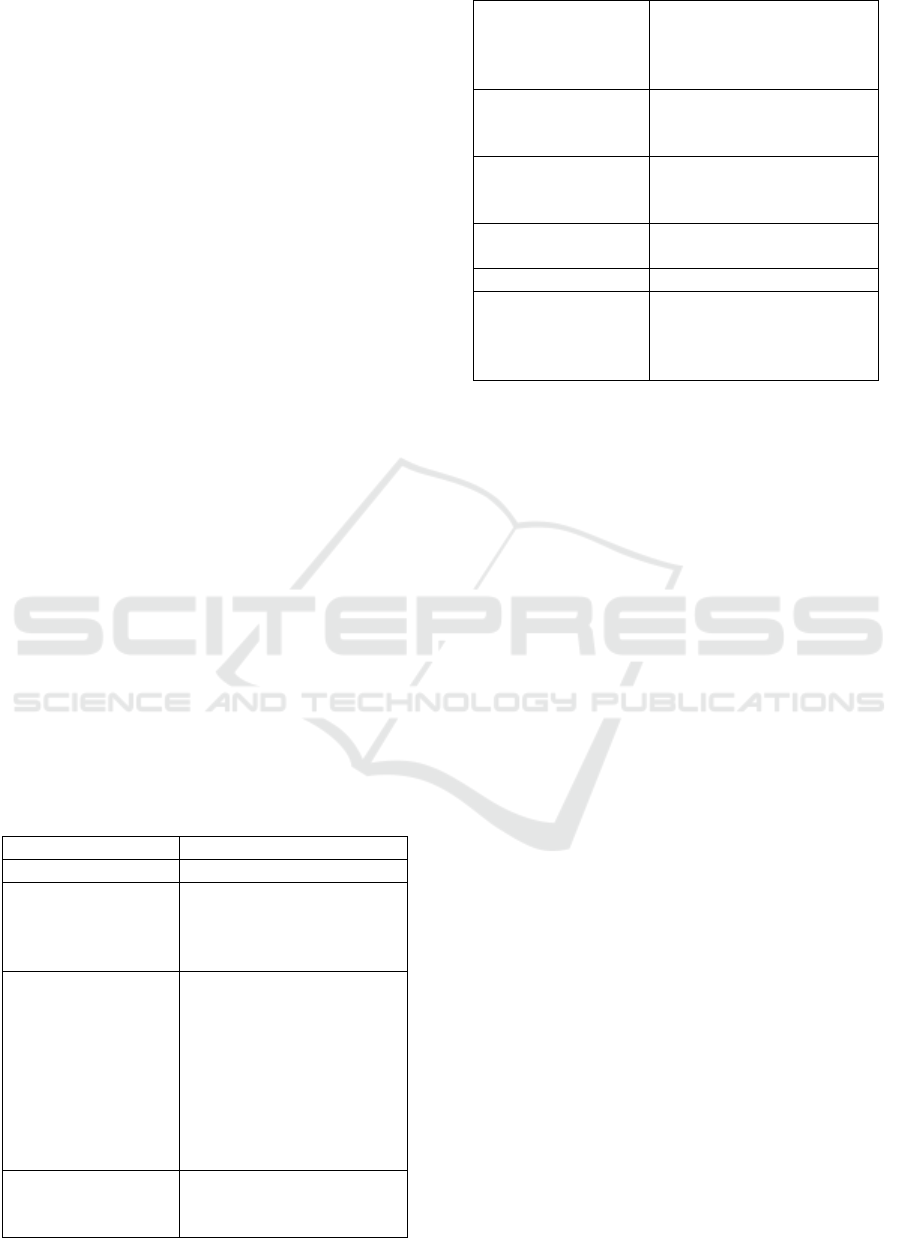

Table 1: Variable Definition

Variable Definition

Growth

p

rofit

g

rowth

Socio –

demographic

variables :

Age

Age of the

respondents

Education Education category :

1 = unschooled

2 = primary school

= junior high

school

= high school

= diploma

= undergraduate

Marital status

Gender

1= if married; 0=

otherwise

1= man;0=otherwise

Business

characteristics

:

Bizage

Age of business

Bizloc Location of business

1=commercial/market

0=otherwise

Islamic

microfinance :

FD

Financing duration

FS The average amount

of financing

FF Financin

g

frequenc

y

Trainin

g

Receive managerial

training

1=if yes

0 otherwise

4 RESULT

Descriptive Statistics

This study employ promary data with total number of

samples are 160 rrespondent. The data shows that 100

out of 160 respondents are man, and the rest

respondents are woman. Therefore, the proportion of

the samples are 62% man and around 38%

respondents are women. Accordingly, customers who

use islamic microfinance are dominated by men. The

reason behind this might occur because man plays a

the head of the family and usually they responsible

for owning and running the business. While 46% age

of the respondents are ranging from 35 – 44 years old.

While the level of education of the respondents

are dominated by respondents who graduated from

high school. Total 83 respondents are graduated from

high school or this number represents 51.88% from

total samples. The second highest level of education

is junior high school which represent 24.38%.

From the data, it also can be seen that as many as

53 respondents or around 33.13% have monthly

income in the range of Rp. 5,000,001-10,000,000,

followed by income groups Rp. 1,000,001-5,000,000,

totaling 47 people (29.38%). These two range of

income are the two highest among other income

categories. Meanwhile, most of respondents or

41.25% respondents run their business mostly taken

place in market, the next business locations are

located in commercial area which represent 31.88%

and 26.88% run their business from home as they

located in residential area.

Empirical Results

After fulfilling the classic assumptions requirements,

the empirical result is presented in the following table

UNICEES 2018 - Unimed International Conference on Economics Education and Social Science

952

Table 2: Regression Results

Profit Growth

A

g

e -0,064

(0,3680)

Education 0.009

(0.0780)

Marital status 0.810*

(0.2959)

Gender -0.1254

(0.1724)

Biza

g

e -0.0553

(0.1480)

Bizloc 0.1101

(0.1763)

FD -0.06574

(0.1219)

FS 0.0321

(0.0580)

FF 0.0585*

(0.01968)

Trainin

g

0.5999*

(0.2341)

Number in parentheses : standard eror

Indicates 90% of signifinace level

The regression result show that only three variables

are significant in influencing the growth of SMEs.

One variable consists of socio – demographic factor

namely marital status, while the islamic microfinance

variables proxied by financing frequency and training

are significant.

Marital status is significant probably because it

can be related to the happiness index which in turn

affecting the level of productivity. Sunar (2012) that

married workers have fewer absenteeism, lower

worker turnover. The results of the study are also

supported by the study of Hermawan (2012) and

which indicate that marital status affects the increase

in business income.

The results obtained from the regression result

also indicate that the training received by respondents

will lead to increased profit growth. This might

happen because the training will provide new

knowledge to the entrepreneurs that in turn will lead

to an increase in repondent’s productivity and

knowledge to run the business better. Thuo (2015)

show that training provides business and financial

skills that are very important for making business

decisions.

Financing frequency also find to significantly

affect the profit growth of the SMEs. Respondents

who receive more credit or loan from islamic

microfinance tend to experience an increase in profit

growth. This results indicate that along with the use

of Islamic microfinance programs taken by

respondents, it will open opportunities for respective

respondent to increase their business profits. This can

be explained since the more often rspondent take the

financing, the faster the business turnover will be.

This result is also supported by research of

Perwitasari (2014) who find that there is a positive

influence on the frequency of financing with the large

development of SMEs turnover.

5 CONCLUSIONS

Overall, the empirical result from this study support

the argument that islamic microfinance is significant

to affect the growth of SMEs. Specifically, only

financing frequency and training as proxy for islamic

microfinance variables are significant and positively

related with the profit growth of SMEs. In addition,

marital status variables also positively related to

profit growth.

However, there are still much room of

improvement in this study. The number and the scope

of the samples used in this study is limited and might

not represent a bigger samples. Better approach and

methodology may improve the result and can be done

for further research.

REFERENCES

Adnan, M. A., & Ajija, S. R. (2015). The effectiveness of

baitul maal wat tamwil in reducing poverty the case of

indonesian islamic microfinance institution.

Humanomics, 31(2), 160–182. https://doi.org/10.1108/

H-03-2012-0003

Amin, H., Rahim, A., Rahman, A., Sondoh, S. L.,

Magdalene, A., & Hwa, C. (2011). Determinants of

customers ’ intention to use Islamic personal financing

The case of Malaysian Islamic banks. Journal of Islamic

Accounting and Business Research, 2(1), 22–42.

https://doi.org/10.1108/17590811111129490

Ali, M., Raza, S. A., & Chin-hong, P. (2015a). Factors

affecting intention to use Islamic personal financing in

Pakistan: Evidence from the modified TRA model.

Munich Personal RePEc Archive Factors.

Ali, M., Raza, S. A., & Chin-hong, P. (2015b). Islamic

home financing in Pakistan: A SEM based approach

using modified TPB model. Munich Personal RePEc

Archive Factors, (67877).

Antonio, Muhammad Syafii. (2011). Islamic Micro Finance

Initiatives To Enhance Small and Medium Enterprises

in Indonesia. Journal of Indonesian Islamic; ISSN1978-

6301

Awuah, S. B. and Addaney, M., (2016). The interactions

between microfinance institutions and small and

medium scale enterprises in the Sunyani municipality

of Ghana. Asian Development Policy Review, 4(2). pp.

51-64

The Role of Islamic Microfinance to Support the Growth of Small – Medium Enterprises: Case Study of SMEs in Jakarta, Depok, Bogor

and Tangerang

953

EdinburghGroup. (2014). Growing the global economy

through SMEs. The Edinburgh Group. Retrieved from

http://www.edinburgh-

group.org/media/2776/edinburgh_group_research__gr

owing_the_global_economy_through_smes.pdf

Khan, R. A. G., Khan, F. A., & Khan, M. A. (2011). Impact

of Training and Development on Organizational

Performance. Global Journal of Management and

Business Research, 11(7), 63–69.

https://doi.org/10.1017/CBO9781107415324.004

Malhotra, N. K. (2010). Marketing Research: An Applied

Orientation. Pearson International Education: Limited.

Mohamed, H. A. and Al-Shaigi, R. S. M., (2017). The role

of microfinance in reducing poverty rate in Sudan: A

case study of saving & social development bank.

International Journal of Science, Environment and

Technology, 6(2), pp.1460 – 1475

Perwitasari, A. N., & Tunas. (2014). Analisis Pengaruh

Pembiayaan Syariah Terhadap Perkembangan Usaha

Mikro Kecil Menengah Di Kota Depok. Jurnal Ilmu

Syariah dan Hukum.

Rokhman, W. (2013). The Effect of Islamic Microfinance

on Poverty Alleviation: Study in Indonesia. Journal of

Economics and Business, XI(2), 21–31

Sarwono, H. A. (2015). Profil Bisnis Usaha Mikro, Kecil

Dan Menengah (UMKM). Bank Indonesia dan LPPI.

Sugiyono. (2017). Metode Penelitian Kuantitatif,

Kualitatif, dan R&D. Bandung: Alfabeta

Thuo, M. W. (2015). The Effect of Microfinance Services

on Growth Of Small and Micro Enterprises in Nairobi’s

Informal Settlements.

UNICEES 2018 - Unimed International Conference on Economics Education and Social Science

954