Does the Risk Profile, Liquidity Ratio, Good Corporate Governance and

Intellectual Capital Able to Affect the Financial Performance of Islamic

Banks in Indonesia?

Abdurrahman

1

, Ahmad Rodoni

2

and Muhammad Yusuf

3

1

University

Of Esa Unggul

2

UIN Syarif Hidayatullah

3

University Of Sahid

Keywords: Risk Profile, Liquidty Ratio, Good Corporate Governance, Intelectual Capital

Abstract: Financial performance is one consideration for investors in investing in a bank. The decline in financial

performance can affect banks in obtaining future earnings. the prospect of a bank is highly dependent on the

ability of management in managing risk, the level of liquidity, banking governance, and managing

intangible assets. The sample in this study were all Islamic commercial banks operating in Indonesia, the

observation period of this study was 2012 to 2016. The variables used were Performance measured through

the Return On Asset approach, Risk Profile measured through the Non Performance Financing ratio,

Liquidity through Capital Adequacy Ratio ratio approach, Good Corporate Governance through the IPCG

index approach, and Intellectual capital through the Value Added Capital Employed approach, Value Added

Human Capital, and Structural Capital Value Added. This study uses Multiple Regression as an analytical

tool. The results of this study indicate that only the risk profile, level of liquidity and Intellectual capital of

Value Added Capital Employed have influence while Good Corporate Governance, Intellectual capital from

Value Added Human Capital and Structural Capital Value Added have no influence over financial

performance of Islamic Banking in Indonesia.

1 INTRODUCTION

Financial performance is one of the big

cnsiderations for investors in investing in a bank.

The decline in financial performance can affect

banks in obtaining future earnings. the prospect of a

bank is highly dependent on the management's

ability to manage risk, the level of liquidity, banking

governance, and managing intangible assets.

Financial system (financial system) is a

collection of institutions. market. provisions of

legislation. law / regulations. and ways or techniques

where securities (securities) are traded. interest rates

are determined and financial services are produced

and offered to all corners of the world (A.Rose et.al

2006). Financial experts agree that in the financial

system there are seven important main functions,

namely the savings function. wealth function.

liquidity function. credit function. payment fuction

function. risk function and policy function.

Banking systems in Indonesia are the largest part

of the financial system. Its role is very strategic and

significant in accelerating national economic

growth. The interaction between the financial system

and the real sector has actually occurred in various

business cycles. Although in general the financial

system is only a derivation of the real sector but in

reality what happens is that both of them influence

each other in forming a long-term balance. The

development of the financial sector through

improving the structure and integration of financial

markets within it is certainly expected to be able to

increase the acceleration of economic activity in the

community and accelerate the turnaround of the

national economy.

The need for banks is vital because all activities

carried out by the community are always related to

money, and money is always related to the world of

banking. In Indonesia the majority of the population

is Muslims also need banking services. Started in

1992 but only fully operational in 1998 The first

Sharia Bank was operational, namely Bank

Abdurrahman, ., Rodoni, A. and Yusuf, M.

Does the Risk Profile, Liquidity Ratio, Good Corporate Governance and Intellectual Capital Able to Affect the Financial Performance of Islamic Banks in Indonesia?.

DOI: 10.5220/0009495812231228

In Proceedings of the 1st Unimed International Conference on Economics Education and Social Science (UNICEES 2018), pages 1223-1228

ISBN: 978-989-758-432-9

Copyright

c

2020 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

1223

Mualamat, Tbk and was followed by 12 other

Islamic banks until 2018. The development of

sharia-based banks indicated that the Islamic

economy had developed in Indonesia Falikhatun and

Assegaf, 2012).

The banking business is a business of trust,

where banks must have very much Human

Resources, which have a role as intermediaries

between those who have excess funds and those who

lack funds and institutions that function to facilitate

payment flow, as well as the Sharia banking needs to

be trusted in carrying out its activities. This can be

seen from the 2016 data which states that the market

share of Islamic banking is only 5.33% of

Indonesia's national banking.

Growth and development of profitability (Return

On Asset) from 2011-2016 in Islamic banking in

Indonesia tends to fluctuate.

Figure 1: Growth and development

The future and prospects of the organization,

especially banking management, are highly

dependent on the ability of management to manage

risk, manage liquidity, and how management's

ability to increase company value. The role and

standard of Risk profile, Liquidity level, Good

Corporate Governance and Intellectual Capital are

very significant in influencing the performance of

Islamic banking so it is interesting to be investigated

further.

2 THEORICAL FRAMEWORK

The decision making role of the firm has progressed

from the neoclassical standpoint of profit

maximization to sales maximization, utility

maximization, and satisficing. From the Operation

Research point of view. The ideal picture is that

someone, presumable the firm that hires the

operations researcher, hands him, on a silver platter,

an objective function. By talking to the engineers, or

by looking into a few scientific laws, he determines

the policy alternatives available and also the model.

(Arrow, 1984).

Resource Based Theory (RBT)

Resource Based Theory is a theory that illustrates

that a company can increase its competitive

advantage by developing resources so that it can

direct the company to survive in the long term. The

key to the RBT approach is the strategy of

understanding the relationship between resources,

capabilities, competitive advantage, and profitability

in particular to be able to understand the mechanism

by maintaining competitive advantage over time.

This model requires the use of unique characteristics

of the company.

This theory was first put forward by Wernerfelt

(1984) in his work entitled "A Resource-based view

of the firm". But much of the reference research is

articles by Barney (1991) "Firm Resource and

Sustained Competitive Advantage". Firm resource

explained helps companies improve the efficiency

and effectiveness of the company's operations.

Furthermore, competitive competitiveness can be

understood by instilling an understanding that the

company consists of heterogeneous and immovable

elements. Steps to maximize competitive advantage,

companies must meet four criteria, namely valuable,

awareness, inimitability and non-substitutability.

Risk Profile

The bank's risk profile is a description of the main

risks that exist in bank activities. Banks in running a

business contain a variety of risks. The risk profile is

a summary that provides an overview for risk

management what needs attention.

The risk profile is measured by identifying the

inherent risks in various business activities, or the

risks inherent in bank activities, and evaluating the

quality of controls, and the plan to improve quality

control.

Bank Indonesia makes the risk category

consisting of credit risk, market risk, liquidity risk,

operational risk, compliance risk, strategic risk,

reputation risk and legal risk. For the eight risks, it

can be determined what risks need to be prioritized

by management's attention to be managed properly,

because they are seen as potentially harming the

bank. (Bank Indonesia Regulation Number: 13/1 /

PBI / 2011)

Liquidity Level

The term liquidity is basically a term absorbed from

English, namely the word liquid which means liquid.

This term usually indicates the level of liquidity of

funds or wealth owned by a company organization.

According to KBBI (Indonesian dictionary)

itself, the definition of liquidity is the position of

1.79

2.14

2.00

0.41

0.49

0.63

‐

1.00

2.00

3.00

2011

2012

2013

2014

2015

2016

ROA of Islamic Banking 2011-2016 (%)

ROA

UNICEES 2018 - Unimed International Conference on Economics Education and Social Science

1224

money or cash of a company and its ability to fulfill

obligations that are due on time; ability to fulfill

obligations to pay debts on time.

The company's liquidity level is usually

indicated in the form of certain numbers such as fast

ratio numbers, current ratio numbers, and cash ratio

figures. The whole number in these three ratios is a

comparison between the level of current assets and

the amount of liabilities held by the company.

Good Corporate Governance

Good Corporate Governance (GCG) is the principle

that directs and controls the company in order to

achieve a balance between the strength and authority

of the company in providing its accountability to the

shareholders in particular, and stakeholders in

general. Of course this is intended to regulate the

authority of Directors, managers, shareholders and

other parties related to the development of

companies in certain environments.

The Center for European Policy Studies (CEPS)

has another formula. GCG, said the center of study,

is an entire system formed from rights, processes,

and controls, both within and outside the

management of the company. For the record, rights

here are the rights of all stakeholders, not limited to

shareholders only. Rights are the various strengths

that individual stakeholders have to influence

management. The process, meaning the mechanism

of these rights. Control is a mechanism that allows

stakeholders to receive the information needed about

various company activities.

Meanwhile, ADB (Asian Development Bank)

explained that GCG contains four main values,

namely: accountability, transparency, predictability

and participation. Another understanding came from

the Finance Committee on Corporate Governance in

Malaysia. According to the agency, GCG is a

process and structure used to direct and manage the

business and business of the company towards

increasing business growth and corporate

accountability. The ultimate goal is to increase the

value of shares in the long term but still pay

attention to the various interests of other

stakeholders.

Intellectual Capital

In There are many corporate valuation methods.

Nevertheless, studies find contradictory results, and

the corporate finance community is not even close to

a universal methodology of company valuation.

Different methods have different advantages in

different situations, and some capture important

aspects of valuing a business, which are not

recognized by others. Traditional company valuation

methods pay more attention to either historical

figures (based on the balance sheet, income or cash

flow statement) or inexact forecasting [for example,

free cash flow and weighted average cost of capital

(WACC) for subsequent periods]. These methods

are mostly taking into consideration the physical

assets of the company, while in the knowledge-

based economy more emphasis is put on employees

and intellectual capital. Therefore, afore mentioned

corporate valuation methods are not suitable in

today’s world.

Intellectual capital has been recognized as

knowledge applied to practice, reflecting

organizations ability to perform and not just

calculating the value of knowledge in financial

terms. The application of knowledge in innovation

and agility to succeed in business is what

differentiates today's organizations, i.e., the

distinctive capacity of these organizations is their

'knowledge in action' (Davenport and Prusak, 1998).

For this knowledge to be reflected, organizations

should disclose an IC report showing the

transactions on knowledge, as the annexto financial

statements reflects the transactions within the

accounting system (Mouritsen, 2006).

We live in an economy where dematerialization

of production, and information and communication

echnologies, especially the internet, have a leading

role, creating a network economy with intensive use

of knowledge and innovation in the production of

goods and services. Knowledge is then the main

factor of production and competitive pressures have

made innovation the key factor for businesses

survival. The type of IC disclosure is valuable

information for investors, as it can help them

reducing the uncertainly of the bank’s future

prospect and facilitate in valuing the bank. Table 1

provides the main contributions of some of the IC

disclosure models available in the literature.

3 RESULT METHODS

This study examines the level of influence of

Independent variables (X) in this case are Non

Performance Finance (NPF), Capital Adequacy

Ratio (CAR), Good Corporate Governance (GCG)

and Intellectual Capital (Value Added Capital

Employed-VACA, Value Added Human Capital-

VAHU, and Structural Capital Value Added-STVA)

on the dependent variable (Y) in this case is Return

On Assets (ROA). The design of this study is

causality. The type of data used is quantitative data

Does the Risk Profile, Liquidity Ratio, Good Corporate Governance and Intellectual Capital Able to Affect the Financial Performance of

Islamic Banks in Indonesia?

1225

data in the form of numbers that have been

processed from the financial statements of Islamic

banks sourced from the site www.bi.go.id and

www.ojk.go.id.

The research population is Islamic banking

registered at Bank Indonesia for the period from

2012 to 2016. The samples in this study were 11

(eleven) Islamic banks in Indonesia. The operational

definitions in this study are as follows:

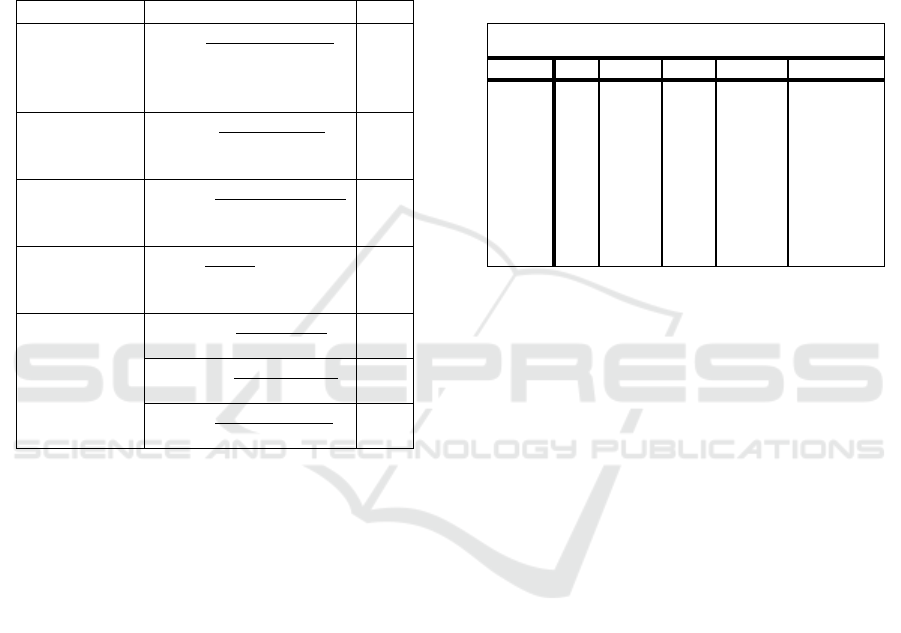

Table 1: Operating Variable

Variable Formula Scale

Return on Asset

(ROA)

ROA = Earning Before Tax x

100%

Total Credit

%

Risk Profile (

NPF)

NPF = Problem Credit x

100%

Total Credit

%

Good Corporate

Governance

(GCG)

IPCG = Item scor disclosure

x 100%

Maximum scor

%

Capital

Adequacy Ratio

(CAR)

CAR = Capital x 100%

ATMR

%

Intellectual

Capital (VAIC)

VACA = Value Added x

100% Capital Employed

%

VAHU = Value Added x

100% Human Capital

%

STVA = Structural Capital x

100% Value Added

%

The data analysis technique in this study uses

multiple linear regression techniques using statistical

software. The following is the data technique used in

this study, namely: 1). Descriptive statistics are used

to give an overview of variables and data seen from

the mean, standard deviation, maximum, minimum,

variance and so on. 2). Classical Assumption Test

which includes normality test, multicollinearity,

autocorrelation and heteroscedasticity. and 3).

Hypothesis Test consists of F Test and t Test 4)

Determinant Coefficient Test.

4 ANALYSIS

This study shows the results in the form of

descriptive statistics, the results of testing the quality

of data and the results of statistical tests for

hypotheses that are suitable or not in accordance

with the theory used by researchers in this study

Descriptive statistics

Descriptive statistics provide an overview of

research data in the form of Non-performance

Financing (NPF), Good Corporate Governance

(GCG), Capital Adequacy Ratio (CAR), Intellectual

Capital (Value Added Capital Employed-VACA,

Value Added Human Capital-VAHU, and Structural

Capital Value Added-STVA) and Return On Assets

(ROA). As stated in table 1. The following

descriptive statistics:

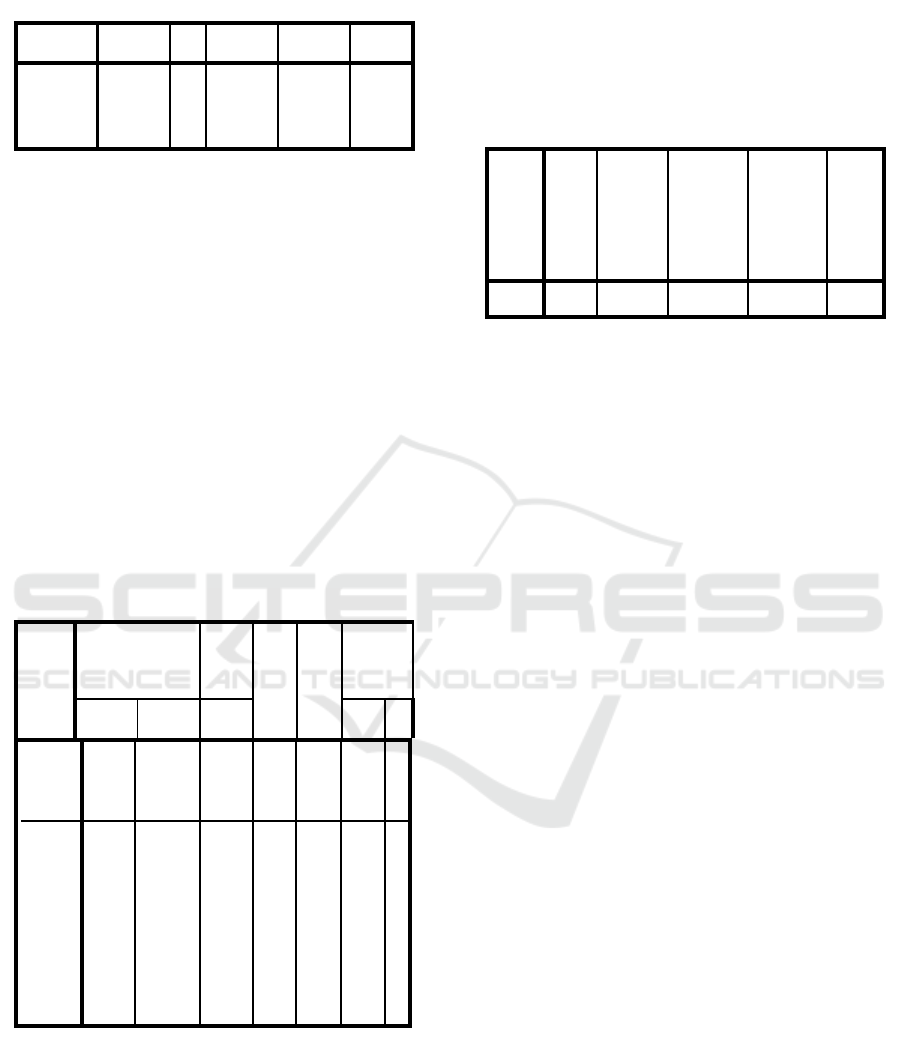

Table 2: Deskriptive Statistics

Descriptive Statistics

N Min Max Mean S. Deviation

NPF 55 .10 13.00 4.5864 7.32093

GCG 55 11.63 77.91 48.3721 17.06835

CAR 55 7.91 89.16 23.9973 17.57944

VACA 55 -.48 .92 .2376 .22478

VAHU 55 -12.52 4.24 1.1425 2.22429

STVA 55 -5.90 3.07 .2091 1.12440

ROA 55 -5.57 4.31 .5566 1.35334

Valid N

(listwis

e)

55

Based on table 2 that this study has 55 sample data.

The variables discussed are as follows: NPF shows

an average of 4.5864%, which means that Islamic

banking has a risk that is close to the maximum

value set by Bank Indonesia which is 5% so that it

can be said that Islamic banking still has high risk,

GCG shows an average amounting to 48.37% which

means that Islamic banking is still not serious in

implementing GCG, CAR shows an average of

23.99%, which means that Islamic banking has a

good level of liquidity, while Intellectual Capital

including VACA shows an average of 0.2376 or

23.76% meaning that the ownership of a sharia

banking company has a pretty good added value,

VAHU shows 1.1425 or 114.25%, which means that

Islamic banking gets a considerable value added

from employees, and STVA shows an average of

0.2091 or 20.91% which means that structural

capital has a contribution for value added banking

sharia and ROA show an average of 0.5566 or

55.66%, which means that Islamic banking has a

performance that can be said to be good because it is

able to manage its assets well in earning profits.

F Test

The F test is used to determine the extent to which

the independent variables are able to explain

together the dependent variable.

UNICEES 2018 - Unimed International Conference on Economics Education and Social Science

1226

Table 3: F Test Output

ANOV

A

a

Sum of

Squares df

Mean

Square F Sig.

Regressi

on

70.808 6 11.801 20.163 .000

b

Residual 28.095 48 .585

Total 98.903 54

Based on the table above shows a significant value

of 0.000 <0.05. meaning independent variables are

able to influence together Dependent Variables. It

can be concluded that the variables are Non-

performance Financing (NPF), Good Corporate

Governance (GCG), Capital Adequacy Ratio (CAR),

Intellectual Capital (Value Added Capital

Employed-VACA, Value Added Human Capital

VAHU, and Structural Capital Value Added-STVA )

able to explain together the ROA variable.

t Test

This test is used to find out whether the regression

coefficient has a partial or significant influence

between the independent variable (X) on the

dependent variable (Y)

Table 4: t Test Output

Coefficients

a

Unstandardized

Coefficients

Standar

-dized

Coeffi-

cients

t Sig.

Collinearit

y

Statistics

B

Std.

Error Beta Tol

VI

F

(Constan

t)

-.881 .420

-

2.100

.041

N

PF

-.130 .049 -.239

-

2.679

.010 .741

1.3

50

GCG

-.000 .006 -.006 -.073 .942 .887

1.1

27

CAR

.031 .007 .404 4.340 .000 .684

1.4

62

VACA

4.582 .694 .761 6.599 .000 .445

2.2

47

VAHU

.065 .060 -.107 1.090 .281 .611

1.6

37

STVA

-.074 .097 -.061 -.760 .451 .908

1.1

01

a. Dependent Variable: ROA

Based on the table above it can be concluded that

NPF is able to influence ROA, GCG is not able to

influence ROA, CAR is able to influence ROA,

VACA is able to influence ROA, VAHU is unable

to influence ROA, and STVA is unable to influence

ROA

Determinant Coefficient Test

The coefficient of determination is used to find the

contribution of the independent variable (X) to the

dependent variable (Y)

Table 5: Determinant Coefficient Test Output

Based on table 5 shows that the number of

coefficients (R) is 0.846 which indicates that the

relationship between the independent variable and

the dependent variable is strong because it has R>

0.5. The R2 value is 0.716, indicating that 71.6% of

the dependent variable variation (ROA) can be

explained by variations in the independent variables

(NPF, CAR, GCG, VACA, VAHU, and STVA) in

this study. While the remaining 28.4% is explained

by other variables outside the model.

5 RESULT

The results of this study indicate that basically a

sharia banking company is one company that is

categorized as an industry that has so many

provisions in its operational management that are not

immune from risk management, capital adequacy,

good corporate governance, and management of

intangible assets.

However, in this study it can be explained that

only risk management, capital adequacy and the

management of intangible assets of value added

capital employed have an influence on the

performance of Islamic banking.

Risk management is important in banking

performance given that Islamic banking is a

company engaged in services. Whereas the level of

liquidity is an absolute provision for a bank to

operate in Indonesia, and Intellectual Capital in

Value Added Capital Employed (VACA) is

important because in VACA it consists of physical

capital and financial assets. This means that Islamic

banking companies must be efficient in running the

company by optimally utilizing existing assets.

Model Summary

b

Mo

del R

R

Square

Adjusted

R Square

Std.

Error of

the

Estimate

Durbi

n-

Watso

n

1 .846

a

.716 .680 .76506 2.192

a. Predictors: (Constant), STVA, VACA, GCG, CAR, VAHU, NPF

5. Dependent Variable: ROA

Does the Risk Profile, Liquidity Ratio, Good Corporate Governance and Intellectual Capital Able to Affect the Financial Performance of

Islamic Banks in Indonesia?

1227

6 CONCLUSIONS

This study concludes as follows: where the research

model is feasible because the independent variables

in this study jointly influence the performance of

Islamic banking. while the results of the partial test

found that only NPF, CAR and Intellectual Capital

in VACA were able to influence the Performance of

Islamic Banking while GCG, Intellectual Capital in

VAHU and STVA were not strong enough to

influence the performance of Islamic banking. the

relationship between independent variables and the

dependent variable is quite high and the contribution

of independent variables in explaining the dependent

variable is also quite high.

REFERENCES

Arrow, Kenneth J. (1984). Collected Papers, vol. 4: The

Economics of Information. Oxford: Basil Blackwell.

A.Ross, Stephen, Randolp W. Westerfield, dan Bradford

D. Jordan. (2006). Fundamentals of Corporate

Finance. New York: McGraw-Hill Irwin.

Bank Indonesia, (2011), Surat Edaran No.13/24/DPNP

Date 25 Oktober 2011, regarding the guideline for the

rating system for commercial banks ", accessed on 11

November 2018 from www.bi.go.id.

Bank Indonesia, (2011), Surat Edaran No.13/1/PBI/2011

Date 05 Januari 2011, regarding the assessment of the

soundness level of commercial banks ", accessed on

11 November 2018 from www.bi.go.id.

Barney, J. B.(1991). ‘Firm Resources and Sustained

Competitive Advantage.’Journal of Management

17(1):99–129

Bontis, Nick & Chua Chong Keow, William &

Richardson, Stanley, (2000), Intellectual Capital and

Business Performance in Malaysian Industry. Journal

of Intellectual Capital. 1. 85-100.

Davenport, T. H., Prusak, L, (1998). Working knowledge:

How organizations manage what they know, Harvard

Business School Press, Boston.

Falikhatun and Assegaf, 2012, Bank Syariah Di

Indonesia: Ketaatan Pada Prinsip-Prinsip Syariah Dan

Kesehatan Finansial. Accounting and Management

(CBAM).Vol. 1 No. 1 December 2012, 245 –254

Gozali, Imam, 2011, Aplikasi Analisis Multivariate

dengan program SPSS. Semarang, universitas

Diponegoro

Jan Mouritsen, 2006 "Problematising intellectual capital

research: ostensive versus performative IC",

Accounting, Auditing & Accountability Journal, Vol.

19 Issue: 6, pp.820-84

Otoritas Jasa Keuangan, 2016, Statistik Perbankan

Indonesia accessed on 07 October 2018 from

www.ojk.go.id

Sahara Ayu Yanita, (2010), Analisis Pengaruh Inflasi,

Suku Bunga BI, dan Produk Domestik Bruto terhadap

Return On Asset (ROA) Bank Syariah di Indonesia.

Jurnal Ilmu Manajemen, Vol 1 No.1 Januari 2013.

Umum, Ihyaul, (2008), Pengaruh Intellectual capital

terhadap kinerja keuangan perusahaan perbankan di

Indonesia. Pontianak: Call for paper symposium

Nasional Akuntansi XI, Ikatan Akuntan Indonesia,

Wernerfelt, B. (1977), 'An information based theory of

nlicroeconomics and its consequences for corporate

strategy', Unpublished Dissertrrtion, Harvard

University, Graduate School of Business

Administration.

UNICEES 2018 - Unimed International Conference on Economics Education and Social Science

1228