The Development of Practicum Teaching Materials based on IFRS to

Improve Learning Outcomes of Accounting Students’

Erny Luxy D. Purba

1

and Yulita Triadiarti

1

1

Faculty of Economics, Universitas Negeri Medan, Medan -Indonesia

Keywords: Accounting, IFRS-Based Accounting, Teaching Material

Abstract: The research problem is that the business environment and Indonesian accounting standards are changing

rapidly. Therefore, the development of material in practical introductory accounting textbooks must reflect

new developments in accounting standards as well as practical business. Since 2012, PSAK refers to the

International Financial Reporting Standards (IFRS) which became effective from January 1, 2009.

Indonesia's commitment is to support IFRS standards as accounting standards that are accepted globally and

continue with the process of convergence of IFRS standards, to minimize gaps between SAK and IFRS.

This is the reason for the need for international accounting standards to eliminate barriers to international

capital flows by reducing differences in financial reporting provisions, reducing financial reporting costs for

multinational companies and costs for financial analysis. The subjects of this study were first semester

students majoring in accounting who took introductory accounting practice courses. Data analysis in this

study used quantitative descriptive analysis. All collected data were analyzed by descriptive statistical

techniques which were quantitatively separated according to categories to sharpen judgments in drawing

conclusions. Qualitative data in the form of very inadequate, inadequate, moderate, feasible and very

feasible statements are converted into quantitative data with a scale of grades 1 to 5. The results are

averaged and used to assess the quality of learning media. Media criteria will be converted into values on a

scale of five using Scale Likert. The results of the study obtained that the development of teaching materials

was deemed feasible to use and able to improve student learning independently.

1 INTRODUCTION

At present the curriculum used by Universitas

Negeri Medan is based on the Indonesian National

Qualifications Framework (KKNI) which requires

the determination of learning outcomes for four

aspects namely attitudes, general skills, special

skills, and knowledge mastery in order to be able to

answer and shape graduates who answer the needs

of users, who need energy professional. One way to

realize the achievement of the effectiveness of the

implementation of learning is to form a Study

Lecturer Group (KDBK) based on the alignment of

studies in the course. One of the KDBK in the

Department of Accounting is the Financial

Accounting KDBK which is a forum for developing

professionalism and lecturer performance, especially

developing lecturer competencies in developing

teaching preparation such as developing learning

processes and materials in financial accounting

KDBK courses, each lecturer can discuss and help

each other if there is a special difficulty in the

implementation of accounting practice courses

which are part of KDBK financial accounting.

Renewal of the learning process and teaching

materials must be done to improve the quality of

learning itself and ultimately will be able to improve

the quality of graduates. The renewal of the learning

process and introductory accounting practicum

materials, especially in the business environment

and Indonesian accounting standards change rapidly.

Therefore researchers want to develop material in

practice accounting interventions to reflect new

developments in accounting standards as practical

business. This is in accordance with the Statement of

Financial Accounting Standards (PSAK) issued by

258

Purba, E. and Triadiarti, Y.

The Development of Practicum Teaching Materials based on IFRS to Improve Learning Outcomes of Accounting Students’.

DOI: 10.5220/0009495602580265

In Proceedings of the 1st Unimed International Conference on Economics Education and Social Science (UNICEES 2018), pages 258-265

ISBN: 978-989-758-432-9

Copyright

c

2020 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

the Accounting Standards Board (DSAK IAI) under

the auspices of the Indonesian Institute of

Accountants or IAI. Since 2012, the PSAK refers to

International Financial Reporting Standards (IFRS)

which are effective since January 1, 2009.

Indonesia's commitment is to support the IFRS

standard as an accepted accounting standard globally

and continue with the IFRS standard convergence

process, to minimize the gap between financial

accounting standards (FAS) and IFRS

The question arises why adopt International

Financial Reporting Standard (IFRS)? Practically

speaking, adoption of IFRS is not an option for

Indonesia, but a necessity, with hope, foreign

investment will continue to enter or even increase

and we are not excluded from international relations

and even get maximum recognition from the

international community. Companies in the world

have been and are in the process of adopting IFRS

with very impressive developments. Most G20

member countries are also IFRS adopters. This is the

reason for the need for international accounting

standards to remove barriers to international capital

flows by reducing differences in financial reporting

provisions, reducing financial reporting costs for

multinational companies and costs for financial

analysis for analysts and improving financial

comparability in providing quality information on

international capital markets.

(http://maiyasari.wordpress.com, 2012)

The development of IFRS-based introductory

accounting practicum teaching materials is one of

the efforts taken to be able to improve the ability of

student practicum in accordance with new

developments in international accounting standards,

because accounting is one of the fields of science

that is not sufficiently studied only in terms of

theory, but accounting is easier to understand with

real bookkeeping practices.

2 LITERATURE REVIEW

Definition of Teaching Materials

One of the tasks of educators is to provide a pleasant

learning atmosphere. One way to make learning fun

is to use fun teaching materials too. (Prastowo Andi,

2011) Teaching materials are basically all materials

(both information, tools, and texts) that are arranged

systematically, which displays the complete figure

of the competencies that will be mastered by

students and used in the learning process with the

objectives of planning and reviewing the

implementation of learning.

Teaching materials that are well designed by

lecturers will be able to make learning more

effective and students' understanding of accounting

increases. The results of Demaja W's research in

(Pujiati, 2007) show that: Learning outcomes of

PAK learning strategies between students who use

teaching materials for Dick and Carey models with

students using traditional teaching materials differ

significantly. It was found that the learning

outcomes of PAK learning strategies for students

who use teaching materials compiled by researchers

are higher than students who use traditional teaching

materials.

Usually teaching materials are "independent",

meaning that they can be studied by students

independently because they are systematic and

complete. (Paulina, Pannen, 2001). Further

explained that:

"Teaching materials designed

and developed based on good

instructional principles will be

able to: 1) assist students in the

learning process, 2) assist

lecturers to reduce material

presentation time and increase

lecturer guidance time for

students, 3) assist universities in

completing curriculum and

achieving goals instructional

with the time available.

"(Paulina, Pannen, 2001.)

Independent learning shows that students are not

dependent on continuous supervision and lecturer

direction, but students also have their own creativity

and initiative, and are able to work alone by

referring to the guidance they obtain (Self Directed

Learning, Knowles, 1975 in (Paulina, Pannen,

2001). The main role of the lecturer in independent

learning is as a consultant and facilitator, not as an

authority and the only source of knowledge.

(Wadjadi Faried, 2004) explained that good

teaching materials are materials that: (1) can arouse

students' interest in learning, (2) have instructional

purpose clarity, (3) present material with good

structure, (4) provide opportunities for students to

practice and provide feedback to students, and (5)

create two-way communication. In addition to the

above to stimulate students' creativity and interest in

learning, instructional materials are designed as

attractive as possible including the use of color,

shape, font size and thickening of letters, lacing and

lines are also needed to clarify the contents of the

message. Like Leshin, Pollock, and Reigeluth,

(1992: 280) describes the tools used to be able to

The Development of Practicum Teaching Materials based on IFRS to Improve Learning Outcomes of Accounting Students’

259

create the focus of the attention of the following

readers :

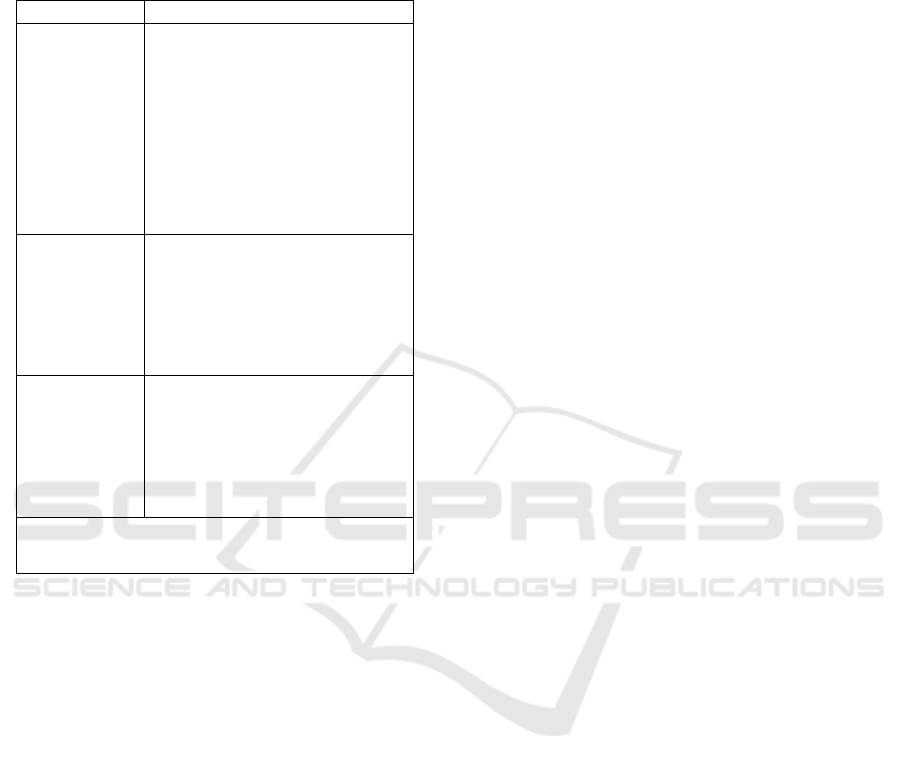

Table 1: Tools used for attention-centering

Equipmen

t

Usa

g

e Description

Color

Use color as a pointing

device to pay attention

directly to something

important.

Always be consistent in

using color when giving

emphasis on key words or

items that are important.

Font Style

Use letters that attract the

eye, italics, or bold to

emphasize keywords or

naming. Use of italics is

recommended.

Boxes and

lines

Staining to surround

important information.

Do not use the underscore

as a pointing device; this

makes words harder to

read.

Note: Avoid excessive use of equipment as a

pointing device

Adapted from Guidelines, Using Tools For

Emphasis (Leshin, Pollock, and Reigeluth, 1992:

280 in (Pujiati, 2007)

International Financial Reporting Standards

(IFRS) International Financial Reporting

Standards

The SFAS has gradually changed according to

International Financial Reporting Standards (IFRS)

and International Accounting Standards (IAS) from

2008 to 2011. The application of this revised PSAK

early in corporate accounting and education is

strongly recommended, because on January 1, 2012

all new PSAK MUST be implemented. This change

in PSAK requires changes in accounting books, both

in universities and vocational high schools (SMK)

majoring in accounting. (Linda S, 2011)

In December 2008, the Indonesian Institute of

Accountants (IAI) has launched a full PSAK to

IFRS convergence in 2012. Since 2009, the

Financial Accounting Standards Board - Indonesian

Accountants Association (DSAK-IAI) has carried

out work programs related to the convergence

process up to year 2011.

It is targeted that in 2012, all PSAK will not

have material differences with IFRS which will be

effective as of January 1, 2009. After 2012, PSAK

will be updated continuously as changes in IFRS.

Not only adopting IFRS that has been published,

DSAK-IAI is also determined to play an active role

in the development of world accounting standards.

International Financial Reporting Standards

(IFRS) is indeed a global agreement on accounting

standards supported by many countries and

international bodies in the world. The popularity of

IFRS at the global level is increasing over time. The

G-20 Agreement in Pittsburg on September 24-25,

2009, for example, stated that the authorities that

oversee international accounting rules must raise

global standards in June 2011 to reduce the rule gap

among G-20 member countries. Through global

participation, IFRS is indeed expected to become a

high-quality theory and principle-based accounting

standard. The application of the same accounting

standards throughout the world will also reduce

problems related to comparability in financial

reporting.

Rosita also added that the IFRS 2012

convergence challenge is the readiness of

practitioners of management accountants, public

accountants, academics, regulators and other

supporting professions such as actuaries and

assessors. Public Accountants are expected to be

able to immediately update their knowledge

regarding changes in IFRSs, update SPAP and adjust

audit approaches based on IFRS. Management/

Company accountants can anticipate by immediately

forming the IFRS convergence success team in

charge of updating Management Accountant

knowledge, conducting gap analysis and developing

IFRS convergence road maps and coordinating with

other projects to optimize resources. Academics/

University Accountants are expected to form IFRS

convergence success team to update Academics'

knowledge, revise curriculum and syllabus and

conduct various related studies and provide input/

comments on ED and Discussion Papers published

by DSAK and IASB. (Linda S, 2011)

Based on some of the opinions above, it can be

concluded that there is a need to develop

introductory accounting practicum materials that suit

student needs, curriculum demands, international

financial accounting standards in this case IFRS,

business environment, target characteristics and

learning problem solving demands.

UNICEES 2018 - Unimed International Conference on Economics Education and Social Science

260

3 RESEARCH METHOD

This research uses research and development

approach (R & D). Development of Practical

Learning Materials Introduction to Accounting

follows the Dick and Carey model, using a system

approach, because it emphasizes the relationship

between each component. The system approach can

also increase the opportunities for integrating all the

variables that affect learning in learning design.

These steps are not the standard things that must be

followed; the steps taken can be adjusted to the

needs of the researcher. To produce interactive

teaching material products, planning, learning design

is needed

.

The steps for developing teaching materials

according to the models of (Dick, W., Carey, L. and

Carey, 2005) are as follows: (1) identifying general

objectives, (2) conducting instructional analysis, (3)

identifying initial behavior / entry behavior lines, (4)

formulating performance goals, (5) developing

reference test items, (6) developing instructional

strategies, (7) developing and selecting instructional

materials, (8) designing and implementing formative

evaluations, and (9) designing and implementing

summative evaluations, (10) revising instructional

activities

The development of material substance in

accordance with International Financial Reporting

Standards (IFRS) and International Accounting

Standards (International Accounting Standards /

IAS) will be integrated in the following steps:

1. Conduct preliminary research, which includes:

a. Identify learning needs and determine

Competency standards for introductory

An accounting practice courses.

b. Conduct an analysis of learning material that

Has been given to introductory accounting

courses (literature studies).

c. Conduct an analysis of learning that has been

done so far in introductory accounting practice

courses.

d. Identify the characteristics and initial behavior

of students in practical courses in accounting,

namely students in accounting semester 1.

e. Write basic competencies and indicators.

f. Write a benchmark reference test.

g. Develop learning strategies that consist of,

(1). Explanation of instructional goals; (2).

Explanation of the relevance of the contents of

the lecture, (3). Explanation of subject matter

Or concepts, principles, and procedures that

students will learn, (4). Formative tests and

feedback, (5). Follow up.

2. conducting the development stage, which

Includes:

a. Preparation of draft teaching materials

b. Make Prototypes teach

c. Material expert assessment

d. Revision 1

e. Small group trials

f. Revision 2

g. Design and media assessment

h. Revision 3

3. Conduct testing of product effectiveness

a. Pre Test-Post Test control design

b. Revision 4

c. Field trials (large groups)

d. Revision 5

e. Final product teaching material

Data analysis in this research used qualitative

data and quantitative descriptive analysis. All data

were collected by analysis with descriptive statistical

techniques that were quantitatively separated

according to categories to sharpen the judgment in

drawing conclusions. Qualitative data in the form of

statements that were very inadequate, less feasible,

moderate, feasible and very feasible were changed to

quantitative data with a value scale of 1 to 5.

However, in frequent measurements, the tendency of

respondents to choose more in category 3 is to avoid

the likert scale being modified by only using the

choice of 4 choices, 4 (Very good); 3 (Good); 2

(Enough); 1 (Less) (Direktorat Pembinaan Sekolah

Menegah atas Dirjen Manajemen Pendidikan Dasar

dan Menengah Atas, 2008). The data analysis

technique in this study uses percentage descriptive

analysis through exposure to data or conclusions of

data processed using percentage techniques which

are divided into four categories with the following

formula:

Percentage of eligibility (%) =

Observe score/expected score x 100 %

The collected data is processed by summing,

compared with the expected number and obtained by

the percentage (Arikunto, 1996).

The product of developing practical teaching

materials introducing accounting requires feedback

in the context of formative evaluation. The

feedbacks were obtained from subjects consisting of

1 learning design expert, 1 material expert, 1

instructional media expert, and product user, namely

first semester students majoring in Accounting

Faculty of Economics, Medan State University

consisting of 8 students to test try small groups and

24 students for big group trials.

The Development of Practicum Teaching Materials based on IFRS to Improve Learning Outcomes of Accounting Students’

261

4 RESULT AND DISCUSSION

Product Development Results

This research and development aims to produce

practical teaching material introducing accounting

based on IFRS. The development in this study uses a

development model adopted from Dick, Carey and

(Suparman, Atwi, 2012). The stages of

implementation of development consist of: a)

Preliminary Research b) Product development and c)

Test the effectiveness of the product

a. The stage of conducting preliminary research

At the preliminary research stage, FGD was held

with the introductory lecturer in accounting and

practicum introductory accounting to identify

learning needs including: a) determining learning

achievement standards and learning outcomes in the

field of knowledge introducing accounting practice

in accordance with the KKNI curriculum by

conducting an analysis of learning which had been

done so far in introductory accounting practice

courses; b) Identifying the characteristics and initial

behavior of students in accounting introductory

practical courses, namely students in accounting

semester 1; c) Writing basic competencies,

indicators and developing learning strategies

consisting of, 1. Explanation of general and specific

instructional objectives, 2. Explanation of the

sequence of subject matter needed in developing

teaching materials, concepts, principles, and

procedures that are in accordance with reporting

standards international finance (IFRS) that will be

studied by students. 3. Explanation of benchmark

reference tests to measure student mastery of the

overall material between accounting and improve

student knowledge to solve accounting cases /

questions in the introductory accounting practice. 4.

Explanation of learning strategies to create a more

lively learning process so as to encourage students to

think more critically by making cases or looking for

the latest cases discussed in the class.

b. Product Development Phase

At this stage the sources of teaching materials or

literature are collected, preparation and making

teaching materials by holding FGDs with lecturers

of accounting introductory subjects and accounting

introductory practicum’s and design experts. At this

stage, reviewing the entire introductory teaching

accounting material by synchronizing introductory

accounting and practicum accounting material so

that students can more easily understand the material

/ concepts in theory and master accounting practices.

The entire material is adjusted to the latest

applicable international financial reporting

standards. In general in Indonesia (IFRS). Making

teaching materials must pay attention to colors,

images, language and design (display) to stimulate

students' minds, attention and reading interest and

certainly encourage students to learn more

independently.

c. The stage of testing the effectiveness of the

Product

The stage of product effectiveness testing

(introductory accounting practice teaching material)

that will be developed first is carried out the analysis

phase of data processing that has been obtained from

observations to find out the learning materials based

on the assessment of material experts, design

experts, media experts, small group trials, and trials

large groups. Then product revisions / improvements

are made and conclusions are drawn

1. Data Description Test Material Effectiveness

(field of study)

Test the effectiveness of material experts including

aspects of content feasibility, language feasibility,

and graphic feasibility. The due diligence process is

carried out to find out whether the material

presented in the teaching material is in accordance

with the semester learning plan, the language used is

appropriate and graphics are in accordance with the

subject matter and to get advice and input on

introductory accounting teaching material to be

developed. These suggestions and inputs are then

analyzed and used to develop practical introductory

accounting teaching materials that are in accordance

with IFRS-based introductory accounting material so

that they can improve student learning outcomes and

answer the needs of stakeholders who have made /

produced financial reports in accordance with IFRS.

The effectiveness test data of the practicum

Materials experts introducing IFRS-based

accounting in the development of learning media

with case-based / problem-based approaches can be

seen in the following table:

UNICEES 2018 - Unimed International Conference on Economics Education and Social Science

262

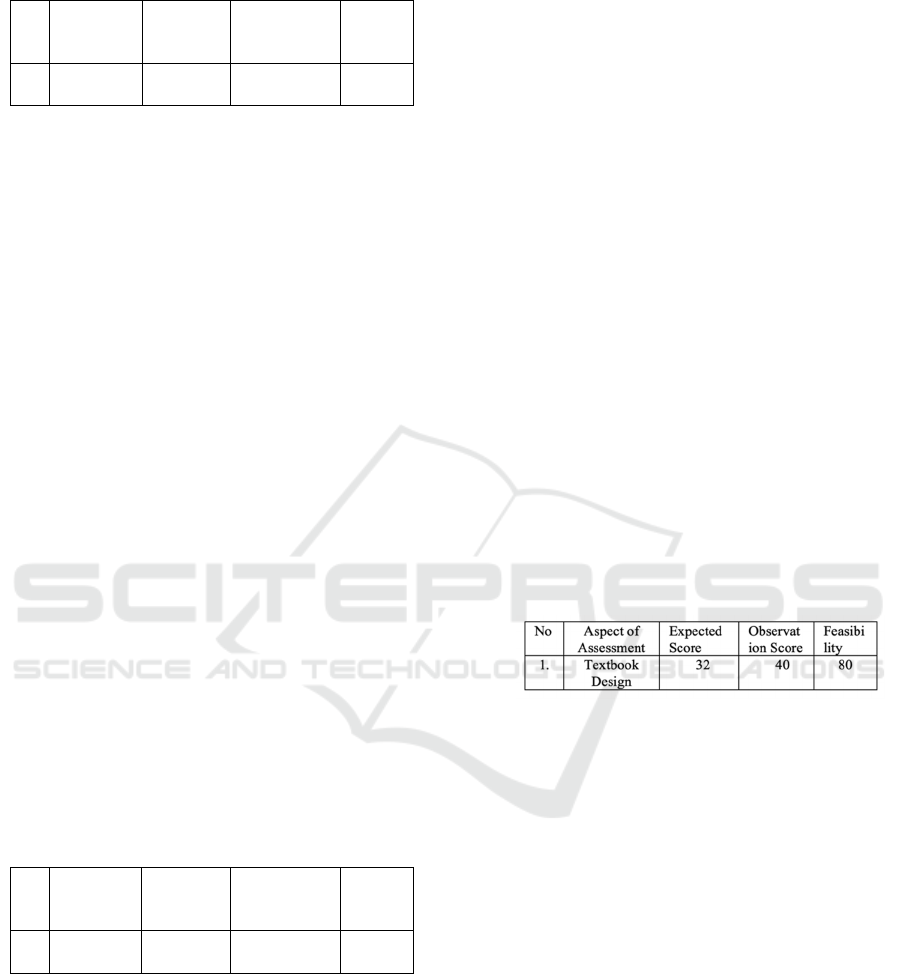

Table 2: Scores of Material Assessment

Based on table 2 above, the average total assessment

of this learning material expert obtained 83.92%

results. In accordance with the percentage scale the

results fall into the category of "proper to use".

The things suggested by material experts are

1) There needs to be other sources for learning (in

the form of an IFRS based accounting book); 2)

More transactions are made to sharpen students'

understanding of the journal; 3) More varied level of

difficulty of questions / cases to sharpen students'

ability to solve accounting cases / questions

2. Description of Data Test the Effectiveness of

Designers

Test the effectiveness of Learning media design

experts aims to get input and suggestions regarding

the design of practical teaching books for

accountants in developing practical teaching

materials introducing IFRS-based accounting to

improve understanding of concepts/material and

mastering accounting practices in making/producing

financial reports on accounting introductory

practical courses in accounting study programs non

education-faculty of Economics Universitas Negeri

Medan. The input is then analyzed and used to

revise the design of the practical introductory

accounting textbook so that it can increase students'

interest in reading interest so that it will improve

student learning outcomes.

Table 3: Design Expert Assessment Score

Based on table 3 above, the average total

Assessment of learning design experts about the

Design of the introductory practical accounting

Textbook is 80.76%. In accordance with the

Percentage scale the results fall into the the category

of "proper to use".

The things suggested by design experts are 1) the

need for image clarity and image function; 2) Need

to clarify the compatibility between tables and

material; 3) Need to pay attention to the accuracy of

color selection, and need to pay attention to the

number of tables to facilitate student work.

3. Data Description Test the Effectiveness of

Media Experts

Test the effectiveness of instructional media experts

includes aspects of non-visual communication that

can lead to reciprocal benefits so as to be able to

solve a problem because teaching materials become

the center of the development of knowledge of

understanding a material / concept for students. The

results of the effectiveness test aim to get input and

suggestions regarding taxation textbooks as a

medium that will be developed with the approach of

working on questions / cases to improve the function

of the textbook as a practicum media that can

improve conceptual understanding / material and

mastery of accounting practices in accounting

introductory practical courses in Universitas Negeri

Medan Faculty of Economics. The input is then

analyzed and used to revise accounting practice

teaching books so that it can improve the quality of

textbooks that are very feasible to use which will

result in high student learning outcomes

Table 4: Media Expert Assessment Scores

Based on table 4. above, the average total

assessment of learning design experts about the

design of textbooks with problem solving obtained

80% results. According to the percentage scale these

results fall into the category of quite feasible /

attractive / motivated to use.

The things suggested by media experts are 1)

need to pay attention to aspects of typos and pages

that are missing; 2) the concept should be equipped

with examples to facilitate student understanding.

4. Small group test results followed by

revisions and large group trials followed by

revisions

Small Group Test Result

After the effectiveness of teaching materials

products is tested by material experts, design experts

and media experts, then revised according to

suggestions or comments from the valuators. The

revised product then enters the testing phase of

students as end product users. Teaching materials

developed were tested on 9 students called small

N

o

Aspect of

Assessm

ent

Expected

Score

Observation

Score

Feasib

ility

1 Contents

Material

47 56 83,92

N

o

Aspect of

Assessm

ent

Expected

Score

Observation

Score

Feasib

ility

1. Textbook

Design

42 52 80,76

The Development of Practicum Teaching Materials based on IFRS to Improve Learning Outcomes of Accounting Students’

263

groups representing non-first semester accounting

students who took accounting introductory practical

courses with the criteria of 3 high, medium and low

ability students. The assessment aspects given in the

small group trials included aspects of the feasibility

of content, aspects of graphics, and aspects of

benefits. This small group test was conducted to get

input or suggestions from prospective users

(students) based on the use of practical teaching

materials so far. Small group test score scores by

students are presented in the table below:

Table 4.4 Student Assessment Scores

Based on table 4.4 above, the average total

assessment of learning design experts about the

design of textbooks with this problem solving

obtained 83.47% results. In accordance with the

percentage scale the results fall into the appropriate

category for use.

Large Group Test Results

This large group test was conducted to get input or

suggestions from prospective users (students) based

on the results of the assessment on the questionnaire.

The respondents of this large group test were taken

randomly as many as 24 of UNIMED's economics

faculty business education students who took

taxation courses in semester V of the 2018/2019

academic year with categories of 8 high, medium

and low ability students respectively. The percentage

of large group test assessment data by students is

presented in the table below:

Based on table 5 below, the average total

assessment of learning design experts about the

design of textbooks with this problem solving

obtained 83.71% results. In accordance with the

percentage scale the results fall into the appropriate

category for use.

Table 5: Student Assessment Scores

5 CONCLUSIONS AND

RECOMENDATION

5.1 Conclusions

Based on the results of research and product

development introductory accounting practice

teaching materials that have been stated previously,

it can be concluded as follows:

1. From the results of the assessment according to

material experts it is "feasible to use" with a

score of 83,92,%. The assessment results

according to the design expert are "worthy of

use" with a score of 80.76%; while the results

of evaluations from media experts are "feasible

to use" with a score of 80%

2. The use of teaching material products by

students shows a score of 83.47% for small

groups and large groups 83.71%. This means

that the use of instructional materials products

developed is deemed feasible to use and able to

improve student learning independently, high

questioning ability and the better understanding

of the transaction settlement cases in

accounting material.

5.2 Recommendation

Based on the results of this research and

development, it is recommended

1. For lecturers, product introductory practical

teaching materials can be used as a source of

learning for Universitas Negeri Medan Faculty

of Economics students, especially accounting

majors.

2. For students, it can be used as an alternative

source of independent learning

3. Development of this product is recommended to

pay attention to more attractive packaging

including matching colors

4. Development of this product is recommended to

add transaction and case questions to simplify

and sharpen student understanding.

5. The research and development products in the

form of teaching materials need to be conducted

in a larger field trial for student subjects in the

accounting department before being used by all

students to improve the quality of the products

produced.

REFERENCES

Arikunto. (1996). Prosedur Penelitian. Rineka Cipta :

Jakarta.

Dick, W., Carey, L. and Carey, J. O. (2005) T. systematic

N

o

Aspect of

Assessme

nt

Expected

Score

Observa

tion

Score

Feasibility

1 Content

Feasibility

720 864 83,33

2 Integrity 481 576 83,50

3 Benefits 326 384 84,89

Total 1527 1824 83,71

UNICEES 2018 - Unimed International Conference on Economics Education and Social Science

264

design of instruction. P. and B. (2005). The

systematic design of instruction. Pearson/Allyn and

Bacon.

Direktorat Pembinaan Sekolah Menegah atas Dirjen

Manajemen Pendidikan Dasar dan Menengah Atas,

T. P. (2008). Panduan Pengembangan Bahan Ajar.

Jakarta : Depdiknas.

Paulina, Pannen, P. (n.d.). penulisan-bahan-ajar.pdf.

Jakarta : PAU-PPAI, Universitas Terbuka.

Prastowo Andi. (2011). Panduan Kreatif Membuat Bahan

Ajar Inovatif : Menciptakan Metode Pembelajaran

yang Menarik dan Menyenangkan. Yogyakarta:

Diva Pres.

Pujiati. (2007). Pengembangan Bahan Ajar Praktikum

Pengantar Akuntansi Untuk Mahasiswa Jurusan

Akuntansi. Jurnal Ekonomi & Pendidikan, Volume

4 N, 36–53.

Suparman, Atwi, M. (2012). Desain Instruksional

Moderen. Erlangga : Jakarta.

Wadjadi Faried. (2004). Pengaruh Pemberian Bahan

Belajar Terhadap Hasil Belajar pada Mata Kuliah

Rangkaian Dasar Listrik (Suatu Studi di Jurusan

Teknik Elektro UNJ). Jurnal Teknodik, No. 15/VII,

105.

The Development of Practicum Teaching Materials based on IFRS to Improve Learning Outcomes of Accounting Students’

265