How to Research into Accounting using Semiotic Approaches by de Saussure,

Barthes, and Baudrillard?

Sri Pujiningsih

*

, Sawitri Dwi Prastiti

, Ika Putri Larasati

Accounting Department, Economics Faculty. Universitas Negeri Malang

Keywords: Semiotics, Accounting, Saussure, Barthes, and Baudrillard.

Abstract: This paper aims to provide practical guidance on how to research into accounting with semiotic approaches.

The first discussion is about the comparison of concepts and examples of semiotic accounting research from

de Saussure, Roland Barthes, and Jean Baudrillard. De Saussure developed the concepts of the signifier,

signified, syntagmatic and paradigmatic. Roland Barthes's semiotic concept includes forms, concepts,

denotations, connotations, and myths. Meanwhile, the concept of Jean Baudrillard is simulacrum and hyper-

reality. The second is to provide a technical understanding of the research method including data selection

and analysis techniques as well as the discussion of research results.

1 INTRODUCTION

This paper intends to discuss the semiotic

approaches in accounting research including

concepts and methodologies. The discussion begins

with an understanding of the semiotic theories

developed by de Saussure, Roland Barthes and Jean

Baudrillard. This first discussion contains the

examples of semiotic research. The second is about

semiotic research methods, which include data, data

analysis, and discussion of research result. The third

is a conclusion that contains the practical

contribution and limitations of this paper.

2 LITERATURE REVIEW:

SEMIOTIC THEORIES BY DE

SAUSSURE; BARTHES, AND

BAUDRILLARD IN

ACCOUNTING RESEARCHES

What is Semiotics? Semiotics is a sign of language

(Belkauoi, 2004). Why can accounting be studied

with semiotics? As Accounting is the language of

business. Accounting is a communication medium

(Parker and Ghutrie, 2009; Breton, 2009; Davison,

2011). Semiotics is divided into syntactic, semantic,

and pragmatic. Syntax in Accounting refers to the

structure of accounting, for example, the

construction of accounting income coming from

revenues minus expenses (Riduwan et al., 2009).

Semantics in Accounting is the meanings of

Accounting itself, for example, accounting is a

reflection of financial performance (Pujiningsih et

al., 2017), Accounting is a tool of management

legitimacy (Crowther et al., 2006; Pujiningsih et al.,

2014) and accounting is an annual ritual (Crowther

et al., 2006). Meanwhile, Accounting, pragmatically,

is the basis for decision-making (Clatworthy and

Jones, 2003; Ross, 1977). Furthermore, what is the

purpose of semiotic research in accounting?

Semiotic accounting research is to gain a better

understanding of financial statements (Breton,

2009).

The accounting researchers use semiotic

approaches from several semiotic experts, including

Structuralist, de Saussure; poststructuralist, Barthes;

and Postmodernist, Jean Baudrillard. The examples

of researches using de Saussure’s semiotics include

Yussof and Lehman (2009) regarding reports of

social disclosure in two countries and Pujiningsih et

al. (2017) about the financial reports of two

universities. The examples of researches with

Barthes’s semiotics include the myth of financial

statements (Pujiningsih et al., 2018); Myth of photo

images in financial statements (Davison, 2007);

accountant photography (Ewing et al., 2001); and

accountant film (Dimnik and Felton, 2006).

Meanwhile, the examples of researches with

90

Pujiningsih, S., Prastiti, S. and Larasati, I.

How to Research into Accounting using Emiotic Approaches by de Saussure, Barthes, and Baudrillard?.

DOI: 10.5220/0008786600900096

In Proceedings of the 2nd International Research Conference on Economics and Business (IRCEB 2018), pages 90-96

ISBN: 978-989-758-428-2

Copyright

c

2020 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

Baudrillard's semiotics are simulacrum and hyper-

reality financial reports (Machintos et al., 2000)

Which semiotic concept distinguishes between

Saussure, Barthes, and Baudrillard? Who is de

Saussure? Ferdinand de Saussure is a French

philosopher who introduced the term of semiology

(Hoed, 2007). According to Saussure, the sign is

divided into two, the signifier (a form of the sign), a

material aspect and signified (its meaning), a mental

concept. For example, the financial report is a sign,

the financial ratio is a signifier, and the reflection of

financial performance is signified (Pujiningsih,

2017). Furthermore, each sign will be organized

paradigmatically and syntagmatically. Paradigmatic

is a sign, which can distinguish from others (Hoed,

2007). Meanwhile, syntagmatic is a structure of

interagency links that can form meaning (Audifax,

2007), or intertextuality of the messages (Yussof and

Lehman, 2009).

To understand the syntagmatic and paradigmatic

concepts, Saussure gave an analogy to the building

poles. Poles relate to other parts of the building, as

syntagmatic understanding which is horizontal.

While the relation to other types of poles belongs to

paradigmatic understanding, which is vertical. For

example, the differences in reports between

Malaysian and Singapore Corporate Social

Responsibility (CSR) companies (Yussof and

Lehman, 2009) and the differences in the Notes of

Financial Statements (CaLK) of two universities in

Indonesia (Pujiningsih et al, 2017). Table 1 explains

the semiotic concept of the "Sign" by de Saussure.

Table 1: Sign Concept of de Saussure’s Semiotics

Sign

Signifier

Paradigmatic (vertically

understanding)

Syntagmatic (horizontally

understanding)

Signified

Who is Roland Barthes? Roland Barthes is a

semiology author born on November 12, 1915, in

Cherbourg, Normandy. Barthes is Saussure's

successor. In his lecture compilation, Barthes used

the term of Semiology taken from the concept of a

sign from de Saussure. Barthes uses the term "form"

instead of “signifier” and "concept" instead of

"signified". Barthes's presence modified and

criticized de Saussure's thoughts. In his mythological

work, Barthes defined de Saussure's "sign" as the

primary sign order (denotation) and secondary sign

order (connotation). In this second one, myth is

found (Barthes, 1972). Myths can be used to

propagate ideological meaning (Barthes, 1977a). It

can also be a synonym for ideology (Barthes,

1977c).

Furthermore, Barthes explained that photo

images belong to messages (Barthes, 1977b). If the

images are originally interpreted as captured by the

camera, this message belongs to encode message in

the sense of denotative meaning. Conversely, if the

photo images have a coded message, it can be

categorized as connotative meaning. The

connotative meaning of photographic images

depends on the socio-cultural context and how

someone produces them. The connotative meaning is

more ideological which contains intentions or not

(McGoun et al., 2007). The examples of denotation

in financial statements are the reality of an

organization's financial performance. Meanwhile,

the examples of connotation in financial statements

are going concern image and good governance

(Pujiningsih et al., 2018). The examples of myths in

financial statements are hyper-reality (Pujiningsih et

al., 2018). The following table 2 explains the

meaning level in Roland Barthes's semiotic

perspective.

Table 2: Sign Concept of Barthes’s Semiotics

Sign

Types

Form

Concept

Sign I

Denotative

Sign

II

Connotative 1

(intention)

Connotative 2

(no intention)

Sign

III

Myths

Who is Jean Baudrillard? Jean Baudrillard is a

postmodernist author who criticized Sassure's

thoughts about sign categories (Pilliang, 1999;

Machintos et al., 2000; O'Donnell, 2009; Callinicos,

2009). Like Saussure, Baudrillard also emphasizes

sign relations, but the relation refers to the variety of

signs in the level of simulacrum and hyper-reality

(Machintos et al., 2000). Simulacrum is a sign,

image, model, and so on. While hyper-reality occurs

when simulacrum is no longer associated with

reality. For example, financial statements as "signs"

have denotative meaning in Saussure's semiotics as a

reflection of the reality of the organization's

financial performance (Pujiningsih et al., 2017).

Meanwhile, the example of simulacrum financial

report as an "image" in Barthes’s connotative

meaning is the image of going concern and good

governance (Pujiningsih et al., 2018) and the image

of organizational sustainability (Machintos et al.,

2000). The example of hyper-reality is income

management (Machintos et al., 2000). Income

How to Research into Accounting using Emiotic Approaches by de Saussure, Barthes, and Baudrillard?

91

management is if "income" no longer refers to real

income and expenses. Therefore, income

management is called hyper-reality. This "income"

is only an "information model" that has no subject to

the postmodernist world. The guise of "ideology" as

described by Barthes about "myth" becomes invalid

(Callinicos, 2008).

Baudrillard divides the three stages of the

signing process. First, the sign is a reflection of

reality. The second stage, the sign of close and the

absorption of reality, called simulacrum. All three

simulacrums no longer refer to reality (Machintos et

al., 2000). According to Baudrillard, the stages of

signs are in table 3 below.

Table 3: Sign Stages of Baudrillard’s Semiotics

Sign Stages

Description

First

The sign is a reflection of reality

(denotative)

Second

Sign of closed and absorption of

reality (simulacrum)

Third

Simulacrum no longer refers to reality

(hyper-reality)

Therefore, it can be concluded that similarity of

Baudrillard and de Saussure are when interpreting

the signs at the first level, denotation. The similarity

with Roland Barthes' theory is on the meaning of the

second level, the connotation meaning, which

belongs to simulacrum in Baudrillard's theory.

Meanwhile, the meaning at the third level with a

new concept is called hyper-reality. Hyper-reality is

actually part of Barthes' myth characteristics, in

which the "concept" distorts the form, so the

meaning in the first level system (denotative

meaning) no longer refers to the actual facts

(McGoun et al., 2007). Here is the similarity of

mythical meaning according to Barthes and the

hyper-reality according to Baudrillard.

From the three semiotic theories by de Saussure,

Barthes, and Baudrillard, it can be concluded that

the concept of de Saussure's "sign" is the basis of

Barthes's critical thinking and Baudrillard's

postmodernism. Saussure defines the sign as a

reflection of reality or the meaning of denotation.

Barthes interpreted Saussure's denotation critically

as the connotation and myth meaning as ideological

criticism. While, Baudrillard transcends the meaning

of denotation, connotation, and myth with the terms

of simulacrum and hyper-reality. Although if traced

deeper, Barthes' connotation meaning is almost

similar to Baudrillard's simulacrum. The distortive

nature of Barthes' myth actually also attaches to the

characteristics of hipper-reality. An important point

distinguishing myth and hipper-reality is a myth as a

critique of ideology that has a capitalist subject,

while hipper-reality is without a subject. According

to Baudrillard, the sign is no longer a guise of

ideology as Barthes intended, but a sign is a hipper-

reality without a subject. Baudrillard explains that

the world of hyper-reality is a world filled with

alternating reproduction of simulacrum objects

deprived of their past social realities, or no a social

reality as their reference (Piliang, 1999: 90).

Table 4 below explains the differences of

semiotic concepts, thought paradigm, and also

examples of researches by de Saussure, Barthes, and

Baudrillard.

Table 4: Comparison of Semiotic Concepts Fromde

Saussure, Barthes, dan Baudrillard

Semiotics

de

Saussure

Roland

Barthes

Jean Bau-

drillard

Concepts

Sign,

signifier,

signified,

syntagmatic

,

paradigmati

c

Sign, form,

concept,

denotation,

connotation,

myth

Sign,

simulacru

m, hyper-

reality

Paradigm

Structuralis

t

Poststructuralis

t (critical)

Postmoder

nist

Research

Examples

Yussof dan

Lehman

(2009);

Pujiningsih

et al.

(2017)

Pujiningsih et

al. (2018);

Davison

(2007); Ewing

et al (2001);

Dimnik and

Felton (2006);

Walton (1993);

McGoun et al.

(2007)

Machintos

et al.,

2000

3 DISCUSSION: HOW DOES

SEMIOTIC RESEARCH

METHOD WORK?

Research methods relate to approaches, data, and

techniques of data analysis. Semiotic research

belongs to qualitative research (Hoed, 2003: 7). The

researchers can use a paradigm or research

perspective according to the research focus. The

structural paradigm can use Saussure theory,

poststructuralist or critical paradigm use Barthes and

postmodernist can use Baudrillard’s theory. Those

semiotic theories are used as methodologies and

medium of the data analysis.

What kinds of data are used in semiotic research?

The data used in semiotic research is text (Hoed,

IRCEB 2018 - 2nd INTERNATIONAL RESEARCH CONFERENCE ON ECONOMICS AND BUSINESS 2018

92

2003: 7). The text is divided into two groups. First is

text representing experience which is analyzed by a

systematic elicitation technique and text analysis

that bases on words or text as a sign system.

Systemic elicitation technique is identifying text

elements that are part of a culture and examining the

relationships between these elements. Second is the

text as an object of analysis by analyzing

conversation, narration, parole, or grammatical

structure. How to analyze texts? Text analysis uses

texts-based analysis content (Chariri, 2009).

What kind of accounting data can be used in

semiotic research? All texts related to accounting

can be used as data, including financial statements

(Hopwood, 1996; Masocha and Weetman, 2007;

McGoun et al., 2007; Pujiningsih et al., 2017); Notes

of Financial Statements (CALK), organizational

strategic plan (renstra), auditor opinion (Pujiningsih

et al., 2017); CSR reports (Yussof and Lehman,

2009; Chariri and Nugroho, 2009), financial

statements (Machintos et al., 2000); results of

interviews with accountant and non-accountant

authors (Riduwan et al., 2009); photo images in

financial statements (Davison, 2007); accountant

photography (Ewing et al., 2001); accountant films

(Dimnik and Felton, 2006); annual reports (Beattie

et al., 2004; Freedman and Stagliano, 2002;

Davison, 2011); and income announcements

(Cooper, 1995).

How to analyze “accounting text"? To analyze

the accounting texts, the researchers should adjust to

the focus and semiotic theory used in the study. For

example, accounting research using de Saussure's

semiotic theory, the steps should begin with

determining the sign and identify the sign into the

signifier and signified. Second is interpreting the

signifier and signified relationships. The third is

analyzing syntagmatically and paradigmatically. For

example, research by Pujiningsih et al. (2017) uses

the text of the strategic plan, financial statements,

and Notes of The Financial Statements (NFS) of the

university as research data. The examples of data

analysis are described in the following tables 5 and

6.

Table 5: Analysis of Syntagmatic Financial Statements in

University X

Sign

Signifier

Signified and

Interpretation

Strategic

Plan

Corporate

Principe,

Autonomy,

Accountable,

transparent,

sustainable

quality, effective-

efficient, ISO

management,

imaging, income

generating

Clarification as

university

managing

corporately

Interpretation:

transformation

State

University into

Corporate

University

Financial

Statements

Improving

liquidity,

solvability, stable,

improving

activity, fluctuated

profitability

Financial

performance.

Interpretation:

a reflection of

financial

performance

via accounting

Notes of

Financial

Statements

Imhere, Corporate

accounting, actual

accounting,

accountability,

imaging

Financial

support of

Imhere project

in organizing

corporate State

University and

its accounting

practice

Interpretation:

the success of

Imhere project

implementation

in forming

corporate State

University and

its accounting

practice

Sources: (Pujiningsih et al., 2017).

The example of a discussion of the strategic plan

texts for "sustainable quality" is as follows:

This 'continuous quality improvement' text is also

a term in the commercial industry. The text was

previously a sign in a commercial organization.

However, the term has become a new sign in

corporate State University (PTN BLU) (Watkins and

Arrington, 2007). A sign either as a form of the sign

(signified) or its meaning (signifier) could be that

the relationship between them does not change.

Instead, the relationship between the form of the

sign and its meaning can change. This happens as

social production allows the sign to be used and

interpreted (Rabber and Bud, 2003). Like de

Saussure’s statement (Rabber and Bud, 2003“The

How to Research into Accounting using Emiotic Approaches by de Saussure, Barthes, and Baudrillard?

93

kind of change that can and does occur over time is

“a shift in the relationship between the signified and

signifier” (de Saussure, 1959, pp. 74-5). The results

indicate that the relationship between the form of the

sign and its meaning changes. This means that the

signifier of "college" transforms into a "corporate"

signifier.

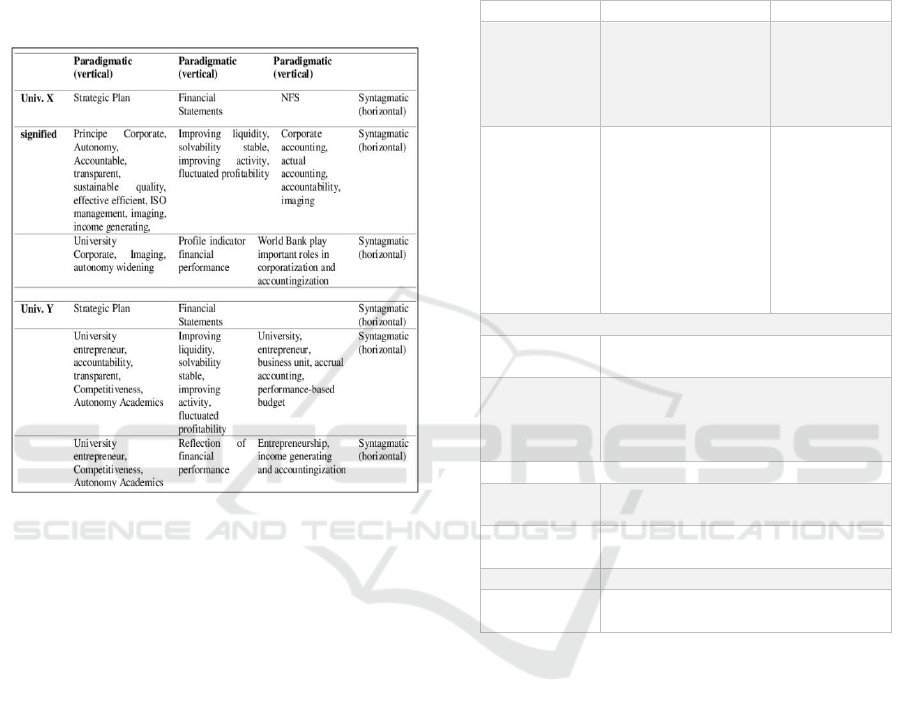

Table 6: Paradigmatic Analysis of University X and Y

Sumber: Pujiningsih et al., (2017)

The examples of paradigmatic discussions are as

follows:

"Paradigmatically, the sign of strategic plan and

CaLK is those that can distinguish between

corporate university X (PT BLU X) and corporate

university Y (PT BLU Y). PT BLU X from the sign

belongs to a corporate university to improve the

organization's image. Organizational imaging aims

to gain legitimacy (Nugroho and Chariri, 2009).

Meanwhile, the similar sign of PTN BLU Y is a

competitive entrepreneur university. This

paradigmatic analysis confirms the results of Yusoff

and Lehman's (2009) research on the differences in

CSR reports between Australian and Malaysian

companies ". (Source: Pujiningsih et al., 2017).

How to analyze the texts using Barthes' semiotic

theory? The steps taken include, first, determining

the sign and identifying the sign into the form and

concept. Second is finding the first connotation

meaning (without intention) and the second one

(with intention) basing on the denotation meaning.

The third is finding myths from the connotation

meaning as ideological criticism. Table 7 describes

the meaning of denotation, connotation, and myth of

financial statements.

Table 7: Meaning Of Denotation, Connotation, And Myth

in University X

Sign

Form

Concept

Financial

Statements

Improving liquidity,

solvability stable,

improving activity,

fluctuated

profitability

Financial

performance

reflection

NSF

Imhere, Corporate

accounting, accrual

accounting,

administration,

transparent,

accountability,

imaging

Project

financial

support of

Imhere in

organizing

PSA and its

accounting

practice.

Denotative meaning

Financial

Statements

Reflection of financial performance

NSF

the success of Imhere project

implementation in forming corporate

State University and its accounting

practice

Connotative meaning

Financial

Statements

going concern images

NSF

good governance images and

capitalism colonization

Myth

Financial

Statements

Hyper-reality, legitimating, and

existence

Sources: Pujiningsih et al. (2018)

The example of a discussion about hyper-reality

myth is as follow:

"Financial statement is a distortive myth if the

relation of financial ratios forms no longer refers to

the actual facts. As known, syntactically income,

expenses, debt, and equity are elements of the

construction of financial statements. While the

concept of the element itself is tentatively

constructed by humans. The financial statement

replaces the organization itself as a reality. This is

indicated by the ratio of liquidity, solvency, and

profitability at the University X and Y. The number

of the ratio has replaced the organization reality.

Here is the role of creating myths from financial

statements. Therefore, financial statements get

hyper-reality (Crowther et al., 2006). Hyperreality of

financial statements occurs when financial

IRCEB 2018 - 2nd INTERNATIONAL RESEARCH CONFERENCE ON ECONOMICS AND BUSINESS 2018

94

statements are no longer associated with

organizational realities, as they are only replaced by

financial statements (Mchintosh et al., (2000). The

hyper-reality of financial statements is one example

of a distortive myth". (Source: Pujiningsih et al.,

2018).

How to analyze data using Baudrillard semiotic

theory? The steps taken include firstly determining

the sign and finding the denotative meaning. Second

is finding the meaning of simulacrum or imaging.

Last is finding the meaning of hyper-reality.

The following table explains the stages of sign

based on Baudrillard's semiotic theory.

Table 8: Sign Stages of Baudrillard’s Semiotics

Sign Stages

meaning

First

(denotative)

reflection of organizational

financial performance reality

(Pujiningsih et al., 2017)

Second

(simulacrum)

Financial statements are going

concern image and good

governance (Pujiningsih et al,

2018)

Third

(hyperreality)

Income management Machintos

et al. (2000)

Adapted from Machintos et al., (2000)

4 CONCLUSION

This paper has revealed the main focus of how to

examine accounting with semiotic theories by de

Saussure, Roland Barthes, and Jean Baudrillard.

Before conducting the research, firstly, the

researchers should understand those semiotic

concepts. The semiotic theories are used as an

analytical instrument and methodology. Secondly,

the researchers can choose the research methods

including research paradigms, data, and techniques

of data analysis that are in accordance with the

research focus or problem. This paper provides

practical contributions for researchers and researcher

candidates who are interested in the semiotic

approaches in accounting researches. This paper

hasn’t provided a comprehensive discussion,

especially in examining the three semiotic theories.

Further papers on how to research accounting

semiotics with other semiotic authors such as Pierce

and Derrida can be conducted by the next

researchers.

REFERENCES

Audifax (2007), Semiotik Tuhan, Penerbit Pinus,

Yogyakarta

Barthes, R. (1972), Mythologies, Jonathan Cape, London,

trans. by Lavers, A.

Barthes, R. (1977a), “From work to text”, Image, Music,

Text, Fontana Press, London, pp. 155-64, trans. by

Heath, S..

Barthes, R. (1977a), “The death of the author”, Image,

Music, Text, Fontana Press, London, pp. 142-8, trans.

by Heath, S..

Barthes, R. (1977b), “The photographic message”, Image,

Music, Text, Fontana Press, London, pp. 15-31), trans.

by Heath, S..

Barthes, R. (1977c), “The third meaning”, Image, Music,

Text, Fontana Press, London, pp. 52-68, trans. by

Heath, S..

Beattie, V. (2004). Accounting narratives and the

narrative turn in accounting research: Issues, theory,

methodology, methods and a research framework. The

British Accounting Review 46:2, 111-134

Belkaoui, A.R. (2004), Accountinh Theory. Fifth Edition.

London: Thomson Learning.

Breton, G.(2009), From Folk-Tales ToShareholder-Tales:

Semiotics Analysis of The

Annual Report, Society and Business Review, Vol. 4 No.

3, Pp. 187-201

Callinicos, A. (2008), Menolak Postmodernisme. Resist

Book: Yogyakarta

Chariri, A. dan A. F. Nugroho (2009), Retorika Dalam

Pelaporan Corporate Social

Responsibility: Analisis Semiotik Atas Sustainability

Reporting Pt Aneka Tambang Tbk, prosiding

Simposium Nasional Akuntansi (SNA), XII

Palembang 4-6 November

Chariri, A. (2009) “Landasan Filsafat dan Metode

Penelitian Kualitatif”, Paper disajikan pada Workshop

Metodologi Penelitian Kuantitatif dan Kualitatif,

Laboratorium Pengembangan Akuntansi (LPA),

Fakultas Ekonomi Universitas Diponegoro Semarang,

31 Juli – 1 Agustus

Clatworthy, M.A. and Jones, M.J. (2003), “Financial

reporting of good and bad news: evidence from

accounting narratives”, Accounting and Business

Research, Vol. 33 No. 3, pp. 171-85.

Cooper, C. (1995), “Ideology, hegemony and accounting

discourse”, Critical Perspectives on Accounting, Vol.

6, pp. 175-208.

Davison, J. (2007), “Photographs and accountability:

cracking the codes of an NGO”, Accounting, Auditing

and Accountability Journal, Vol. 20 No. 1, pp. 133-58.

Davison, J. (2011), Barthesian perspectives on accounting

communication and visual images of professional

accountancy. Accounting, Auditing and Accountability

Journal 24:2, 250-283

Dimnik, T. and Felton, S. (2006), “Accountant stereotypes

in movies distributed in North America in the

twentieth century”, Accounting, Organizations and

Society, Vol. 31, pp. 129-55.

How to Research into Accounting using Emiotic Approaches by de Saussure, Barthes, and Baudrillard?

95

Freedman, M. and Stagliano, A.J. (2002), “Environmental

disclosure by companies involved In initial public

offerings”, Accounting, Auditing and Accountability

Journal, Vol. 15No. 1, pp. 94-105.

Hopwood, A. (1996), “Making visible and the

construction of visibilities: shifting agendas in the

design of the corporate report: introduction”,

Accounting, Organizations and Society, Vol. 21 No. 1,

pp. 55-6.

Macintosh, N.B., Shearer, T., Thornton, D.B. and Welker,

M. (2000), “Accounting as simulacrum and

hyperreality: perspectives on income and capital”,

Accounting, Organizations and Society, Vol. 25 No. 8,

pp. 13-50.

Masocha, W. and Weetman, P. (2007), “Rhetoric in

standard setting: the case of the going-concern audit”,

Accounting, Auditing and Accountability Journal, Vol.

20 No. 1, pp. 74-100

McGoun, E.G., Bettner, M.S. and Coyne, M.P. (2007),

“Pedagogic metaphors and the nature of accounting

signification”, Critical Perspectives on Accounting,

Vol. 18 No. 2, pp. 213-30.

O’Donell, K. (2009). Posmodernisme. Penerbit Kanisius:

Yogyakarta

Piliang, Y. A. (1999). Hiperirealitas Kebudayaan. LkiS:

Yogyakarta

Parker, L. and Guthrie, J. (2009), “Championing

intellectual pluralism”, Accounting, Auditing and

Accountability Journal, Vol. 22 No. 1, pp. 5-12.

Pujiningsih, S.; I. Triyuwono; A. Djamhuri; and

Sukoharsono.E. G. (2014). Anggaran Emansipatoris

Berdimensi Ketuhanan Sebagai Kritik Ideologi

Anggaran Berbasis Kinerja (Studi Kasus Perguruan

Tinggi Negeri Di Indonesia). Prosiding Simposium

Nasional Akuntansi (SNA) XVII, Lombok, 24-27

September

Pujiningsih, S. (2014) Globalisasi Ekonomi: Korporatisasi

Perguruan Tinggi (Peran Akuntansi dalam Tinjauan

Teori Kritis Habermas, Dinamika Akuntansi

Keuangan dan perbankan. Vol. 3, No. 1 hal. 1-9

Pujiningsih, S.; S.D. Prastiti dan D.Syariati. (2017). Kajian

Semiotik de Saussure Laporan Keuangan Perguruan

Tinggi, Laporan Penelitian Fakultas Ekonomi

Universitas Negeri Malang tidak diterbitkan.

Pujiningsih, S. Prastiti, D.P dan Larasati, I. P. (2018) Myth

of Financial Statement in Indonesian College From

Barthesian’s Semiology, working paper presented in

International Conference Economics, Business,

Entepreneurship and Finance (ICEBEF) Universitas

Pendidikan Indonesia, Bandung, 19 september.

Ross, S. (1977)”The Determintation of Financial Structure

The Incentive-Signaling Approach. Journal off

Economics, Vol. 8, Issue 1, pp 23-40

Riduwan, A.; I. Triyuwono, G. Irianto dan U. Ludigdo

(2009), Semiotika Laba Akuntansi:

Studi Kritikal-Posmodernis Derridean, Prosiding,

Simposium Nasional Akuntansi (SNA) XII,

Palembang, 4-6 November

Yusoff, H. dan G. Lehman (2009), Corporate

environmental reporting through the lens of Semiotics,

Asian Review of Accounting Vol . 17 No. 3, pp. 226-

246

IRCEB 2018 - 2nd INTERNATIONAL RESEARCH CONFERENCE ON ECONOMICS AND BUSINESS 2018

96