The Internal Audit Unit, Budgetary Participation, and Intellectual

Capital Effect to Good University Governance through Internal

Control

Rulyanti Susi Wardhani

1

, Taufik Marwa

2

, Luk Fuadah

2

, Saadah Siddik

3

, Rita Martini

4

, Ahmad

Maulana

5

, and Nurkadina Novalia

5

1

Bangka Belitung University, Bangka Belitung, Indonesia

2

Sriwijaya University, Palembang, Indonesia

3

Muhammadyah University, Palembang, Indonesia

4

Sriwijaya State Polytechnic, Palembang, Indonesia

5

IBA University, Palembang, Indonesia

rulyantiwardhani67, lukluk.fuadah, martinirita65, maulanaahmad, nurkardinanovalia (@gmail.com),

Keywords: Internal audit unit, budgetary participation, intellectual capital, internal control, good university governance.

Abstract: This research aims to analyze the influence of internal audit unit, budgetary participation, intellectual capital

(IC), on good university governance (GUG) through internal control at the Southern Sumatra State

University. The number of universities studied was Sriwijaya University, Bangka Belitung University,

Lampung University, Jambi University, Lampung State Polytechnic, Sriwijaya State Polytechnic, Bangka

Belitung Manufacturing Polytechnic, Sumatra Technology Institute and Bengkulu University. The results

showed that there was a direct influence of internal audit units, negatively and significant. The participation

in budgeting and internal control has a positive and significant influence on GUG. However, IC does not

directly affect GUG. The results for indirect influences indicate that the internal audit unit, participation in

the budget and intellectual capital compilation of GUG through internal control.

1 INTRODUCTION

Higher education is a character from an

institution that must be confident in improving the

management of the institution's internal management

intensely. Looking forward, universities must be

able to produce resources that can answer the wishes

and challenges of the community. According to

(Lee, 2001) the tendency of strengthening and

improving quality in the field of education through

various policies such as education that has been

implemented in several countries such as; Britain,

America, Japan and Korea are proof of the

awareness of the governments of these countries

towards the pressure of high levels of competence in

the era of globalization. The existence of

globalization will bring human civilization to a

society that is knowledgeable agains GUG through

internal control (Coaldrake et al, 2003).

Kennedy (2003) and Kickbusch & Gleicher

(2012) stated that policy issues in the 21st century

focused on the public sector in the management of

universities. Higher education institutions, both

private and public, are expected to provide the

maximum possible service to the community,

therefore higher education requires the concept of

good governance (Goodwin, 2003; Dewi & Apandi,

2012). The implementation of the concept of good

governance in universities in Indonesia as well as

other developing countries, there are basic

challenges namely improving quality, relevance,

equity, efficiency, and governance, where the

position of higher education is a moral force to assist

in directing democratization in society and socio-

political reform. The existence of basic challenges in

State Universities (PTN) resulted in the emergence

of new challenges namely understanding the

knowledge economy, increasing internationalization

and competition between countries (Nizam, 2006).

546

Susi Wardhani, R., Marwa, T., Fuadah, L., Siddik, S., Martini, R., Maulana, A. and Novalia, N.

The Internal Audit Unit, Budgetary Participation, and Intellectual Capital Effect to Good University Governance through Internal Control.

DOI: 10.5220/0008442405460554

In Proceedings of the 4th Sriwijaya Economics, Accounting, and Business Conference (SEABC 2018), pages 546-554

ISBN: 978-989-758-387-2

Copyright

c

2019 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

The new challenge caused the Indonesian

government to issue Government Regulation

Number 4 of 2014 and this regulation is in line with

the study of Zaman (2016) regarding the autonomy

of higher education. The autonomy of tertiary

institutions in question is the autonomy of the

academic and non-academic fields. Non-academic

autonomy whose activities include the establishment

of operational, financial, student, labour and

infrastructure norms and policies for its management

carried out through the principles of Good

University Governance (Government Regulation No.

4 of 2014). The results of the examination of the

Financial Examination Agency of the Republic of

Indonesia (2015) states that there are still many

problems and weak management of PTN caused by

weak internal controls and still not compliant laws

and regulations in managing PTN in Indonesia. The

existence of higher education autonomy will open up

areas of improvement and competition, but these

conditions are still limited by state-driven higher

education policies and increasing interventions

related to external quality assurance (Hénard &

Mitterle, 2010). Actuality from Indonesian education

providers has experienced a number of obstacles,

both in terms of policy, implementation, supervision,

and evaluation. This condition requires that

optimization of the application of the GUG

principles and maximize the function of the Internal

Audit Unit (SPI), this causes according to Aisyah et

al (2013) that the need for SPI formation is not

based on the needs of the SPI role, but more in the

administrative complementary organizational

structure, many SPI teams, especially those that have

not been Public Service Agencies (BLU), cannot

function properly because SPI is in an inappropriate

form in terms of the number of human resources

allocated, the qualifications of the chairperson and

members of the SPI, and the funding of program

activities and internal audit activity. Systematic

budgeting is expected to be able to accommodate the

interests of each unit in activity activities.

Implementation of budgeting requires the

participation of the organization (Ompusunggu and

Krisler, 2006) but in reality, the budget preparation

in universities involves only a few elements, so the

budget is not an appropriate target. Incorrectly

arranged budgets can cause dysfunctional behaviour

and negative behaviour among organizational

members (Kennis, 1979; Argyris, 1952; Syahputra,

2014). Management in PTN is inseparable from

aspects of human resources because it is a very

important aspect of every organization. The most

valuable resource in the university is the expertise of

the faculty and staff, namely it’s IC (Jones et al,

2009).

The reason for state universities in Southern

Sumatra was due to the findings of the Republic of

Indonesia Supreme Audit Agency (2016), namely

weak internal control, lack of compliance with

legislation, as well as budget targets not yet found in

the Southern Sumatra PTN. This study refers to the

research of Azwar (2013), Fredrick and Narkiso

(2014), Gina et al (2014), Karagiorgos et al (2010),

Kusmayadi (2012), Radjagukku et al, 2014),

Puspitarini (2012), Suyono and Hariyanto (2012),

Sukirman (2012) where efforts to achieve good

governance, in this case, are GUG, PTN requires an

internal supervision unit or internal auditor to

support the GUG, which is currently the main

component in management or improve universities

effectively and efficiently based on the principles of

good governance. SPI or audit has a positive effect

on the achievement of GUG which means that the

better the role of the internal supervision unit, the

better the achievement or good corporate. Amilin

(2016) budgeting participation has not encouraged

the principles of GUG. Studies by Cadara & Saidin

(2013) state that internal control influences the

effectiveness of internal audit and Ramírez's (2013)

research states that the presentation of information

related to Intellectual Capital (IC) is important in

higher education institutions, especially because

knowledge is the main output both through research

and teaching. Aristanti (2016) show that the

increasing IC owned, the more it can increase GUG,

which means IC has a positive effect on GUG.

Based on previous research related to good

corporate governance, most of the research was

carried out on private companies and the public

sector such as the financial sector (Handley-

Schachler et al, 2007). Good in the public sector

(Stewart-Weeks and Kastelle, 2015). Previous

research still discusses partially or separately the

influence of SPI, participation in budgeting, IC,

internal control and GUG, so that this study tries to

combine several of these variables and SPI

indicators in accordance with the Regulation of the

Minister of National Education of the Republic of

Indonesia Number 47 of 2011 and the existence of

internal control variables as mediating variables

which are the novelty in this study. Previous

research also has not shown consistency in the

results of research, therefore, it needs to be reviewed

in depth in accordance with the above phenomenon,

or the phenomenon above, the purpose of the study

is to analyse the direct and indirect influence of

internal supervision units, budgeting participation,

The Internal Audit Unit, Budgetary Participation, and Intellectual Capital Effect to Good University Governance through Internal Control

547

intellectual capital on good university governance

with internal control as an intervening variable in the

Southern Sumatra Region PTN.

The theory used in this research is that

Stewardship theory views management as a party

that can be trusted to act as well as possible for the

public interest or stakeholders, for the interests of

the principal (community and government).

Stewardship theory describes a situation or condition

in which management is not motivated by individual

goals but rather prioritizes the interests of the

organization (Davis et al, 1991). The theory assumes

that there is a strong relationship between

organizational satisfaction and success.

Organizational success describes maximization

utility of principals and management groups. The

utility maximization of this group will ultimately

maximize the interests of individuals within the

group of organizations.

Good governance can guarantee an organization

(Learmount, 2004; Martini, 2015) so that: 1) able to

provide goods, services or programs effectively and

efficiently, 2) able to create good performance, and

3) able to meet legal, regulatory requirements

published. GUG is actually a derivative of a more

general governance concept, namely good

governance (Azwar, 2013). The purpose of the GUG

is to realize an accountable of higher education.

Some of the principles in GUG are as follows: a)

Governance structure b) autonomy c) Accountability

d) Leadership e) Transparency (Effendi, 2016;

Nurhasanah, 2016; RI BPK, 2008).

Internal control of the COSO version is an

internal control framework by integrating all aspects

of the company's operations and finances, including

between leaders (top executives) and employees

(employees), business objectives and risks, and

covering all organizational activity units. Form of

irregularities that might occur, improvements in the

quality of financial reports and compliance with

regulations. The internal control concept issued by

COSO, states that internal control consists of

policies and procedures designed to provide

management with reasonable certainty that the

organization has achieved its goals and objectives.

These policies and procedures are often called

controls, and collectively shape the entity's internal

controls (A. Arens et al, 2012). The core of COSO's

report consists of five components (Hadisantoso,

2017; Kiabel, 2012; Moeller, 2012; Sawyer's, 2005;

Bill et al, 1997; Bruynseels et al, 2006, SPIP, 2008),

namely: 1) The Control Environment; 2) Risk

Assessment; 3) Control Activities; 4) Information

and Communication; and 5) Monitoring. Budget

participation is mainly carried out by middle-level

managers who hold accountability centre by

emphasizing their participation in the process of

preparing and determining budget targets that are

their responsibility. Brownell and McIness (1986),

Kennis (1979) and Marfuah and Amanda (2014)

define participation in budgeting as the extent of

managers involved in preparing the budget and the

magnitude of the manager's influence on the

organizational unit's budget goals.

Activities in the PTN scope need to be monitored

and evaluated in advance by internal parties, in this

case, the internal supervision unit. SPI has the duty

to carry out supervision of the implementation of

duties in the work unit, so that the understanding is

the entire process of audit activities, reviews,

evaluations, monitoring and other supervisory

activities on the organization of tasks and functions

aimed at controlling activities, securing assets and

assets, carrying out financial statements good,

improve effectiveness and efficiency, and detect in

detail the occurrence, irregularities and non-

compliance with the provisions of the legislation

(Regulation of the Minister of National Education of

the Republic of Indonesia Number 47 of

2011).Various definitions of IC are found in several

kinds of literature Edvinsson (2013) states IC as a

knowledge that can be converted into values. Huang

et al (2007) state that IC is a knowledge that is in the

organization and raised at the personal and

organizational level, where Personal level includes

temporary skills and knowledge at the organizational

level, things like specific databases for each client,

organizational and cultural technologies and

methods. Rastogi (2002) states IC is the entire

ability of an organization to constantly face and

respond to existing and potential challenges

creatively and effectively. IC can be concluded as all

organizational resources, which are sourced from

capital, employees in the form of knowledge,

experience, and thinking power, and sourced from

the organization itself in the form of knowledge,

rules, systems, corporate culture, databases, or other

forms of intellectual property such as brands, patents

and others. Ramírez (2013) measures IC with human

capital, structural capital and relational capital.

Based on the theoretical review and the results

of empirical research above, hypotheses can be

formulated in this study: the internal audit unit,

budgetary participation, and intellectual capital

affect GUG through internal control of state

university in the Southern Sumatra region.

SEABC 2018 - 4th Sriwijaya Economics, Accounting, and Business Conference

548

2 METHODOLOGY

The type of explanatory research is to analyze

the causality relationship the influence of the

internal audit unit (SPI), budgetary participation and

IC on GUG with internal control as an intervening

variable. The approach used to analyze is a

quantitative approach, which includes quantitative

analysis as the main method and qualitative

explanation. This research will be conducted at state

universities (PTN) in Southern Sumatra Region. The

state universities are Jambi University, Bengkulu

University, Lampung University, Bangka Belitung

University, Sriwijaya University, Sumatra Institute

of Technology, Sriwijaya State Polytechnic, and

Bangka Belitung Manufacturing State Polytechnic.

The data used in this study include secondary data

and primary data. Secondary data collected relates to

the description of PTN in the Southern Sumatra

Region obtained from the publication and profile of

the PTN. The primary data used by questionnaires

were filled in by leaders of the Southern Sumatra

Regional PTN namely the chancellor, vice

chancellor, dean, deputy dean, director, deputy

director, and SPI.

The method used to collect data in this study is

questionnaire distribution. The collected data is then

carried out a measurement and scoring scale. The

measurement scale used in this study is the Likert

scale, which is from 1 to 5. The technique used is

Structural Equation Modeling (SEM), the use of

SEM is inseparable from assumptions (Byrne, 2016;

Ferdinand, 2014; Gudono, 2011), these assumptions

include: sample size, b) normality test, and c) outlier

test. . Steps to use SEM according to (Ferdinand,

2014) as follows:

1. Development of a theoretical model.

2. Arrange the path diagram, in the research the

relationship between variables is described in the

path diagram as follows:

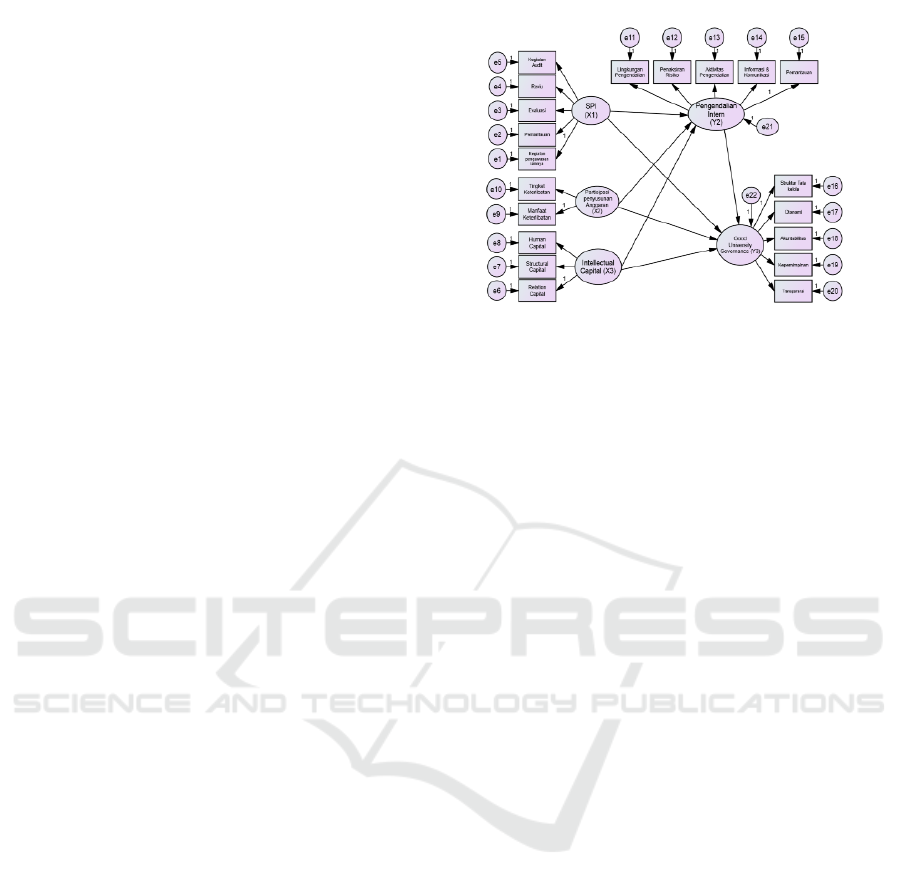

Figure 1: Inter Variable Relations Flow Chart

3. Correcting path diagrams in the form of

equations. The aim is to state the causality

relationship between various constructs. The

equation is:

endogenous variable = exogenous variable +

endogenous variable + error

Testing the proposed hypothesis is formed

mathematical functional equations in the

simultaneous model namely SEM as follows:

PI fSPI PPA IC ……….(1)

GUG fPI SPI PPA IC…....(2)

Where: PI (Internal Control), GUG (Good

University Governance), SPI (Internal Audit Unit),

PPA (Budgeting Participation), IC (Intellectual

Capital).

The function that has been formed above, will

produce the following equation model:

Model GUG

0

1

2

3

4

2

……………..(3)

Where: direct effect

1

= Effect of internal control on GUG

2

= The influence of SPI on GUG

3

= Effect of budgetary participation on GUG

4

= The influence of intellectual capital on GUG

indirect effect

0

1

1

1

2

1

3

……… ( 4)

Where

1

1

= Influence of SPI through internal control of

GUG

1

2

= Effect of budgetary participation through

internal control of GUG

1

3

= Effect of intellectual capital through internal

control of GUG

The Internal Audit Unit, Budgetary Participation, and Intellectual Capital Effect to Good University Governance through Internal Control

549

3. Select the input matrix and estimation model or

technique

4. Assessing the identification problem where the

identification problem has the principle that the

problem of inability of the model developed to

produce a better estimate. If each time an

estimation is made, an identification problem

appears, so the model should be reconsidered by

developing more constructs.

5. Model evaluation is based on the criteria of

goodness of fit:

3 DISCUSSION

This research uses a survey method with the

questionnaire instrument. Questionnaires are

distributed to 5 universities, 3 polytechnics and 1

institution with the number of respondents 250

namely chancellor, vice chancellor, director, deputy

director, dean, vice dean, and internal audit units and

the results are as follows:

Table 1: Response Rate

Description

Number of

Respondents

Percentage

(%)

Questionnaire sent

250

100

Questionnaires were

entered

230

92

The questionnaire that

cannot be processed

4

2

Questionnaire processed

226

90

Source: data processed (2018)

As many as 226 respondents who were processed

in which the total universities added up consisting of

Sriwijaya University, Jambi University, Lampung

University, and Bengkulu University 145

respondents, polytechnics and institutions amounted

to 76 respondents while the Intern audit unit

numbered 5 respondents.

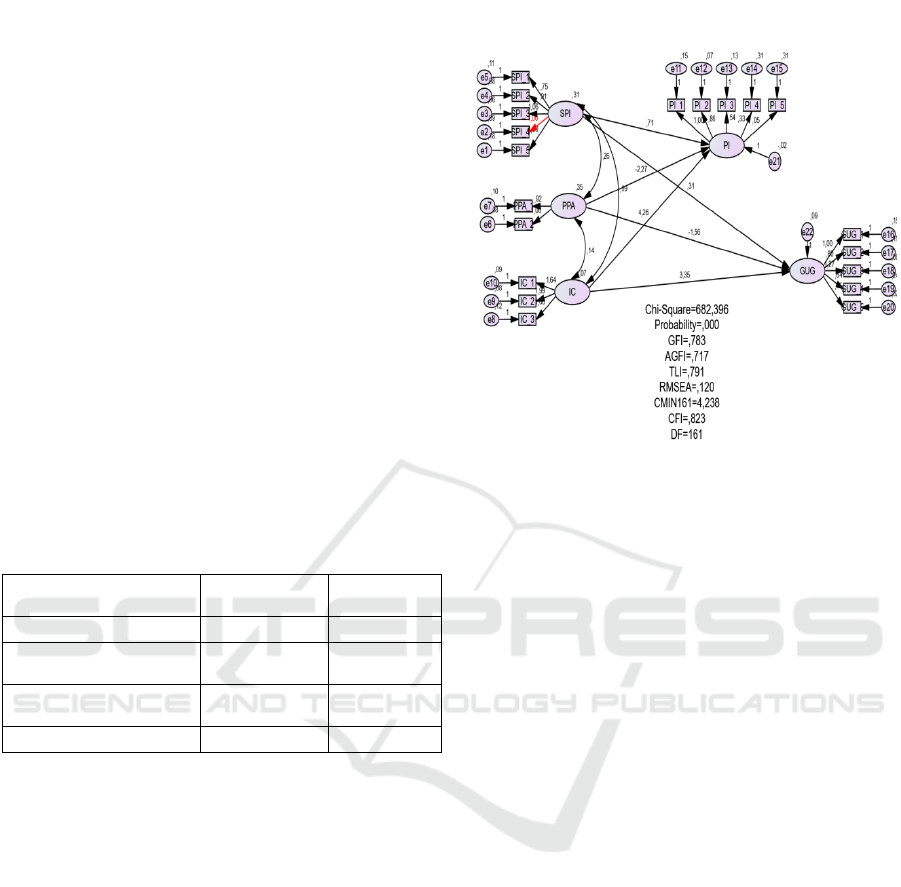

The results of the measurement and structural

model in the form of a full model path diagram

which is hypothesized are obtained by the

calculation of the model seen in the figure 2:

Figure 2: Complete Model Path Diagram (Full Inter-

Variable Model)

The sample size of the sample is 226 there is no

standard provision for criteria than the sample, it is

recommended that the sample is 200-400 so that the

criteria of the sample size in this study have been

fulfilled. The assumption of normality can be tested

by looking at the value of Skewness and kurtosis of

the data obtained. If the CR value ranges between ±

2.5, then the data can still be stated as the normal

distribution. Data processing results show that

overall (Multivariate) distribution is not normal,

because the multivariate numbers are 20,087>2.58.

Likewise, the cr kurtosis value obtained is not

normally distributed because the value is> 2.58. But

the overall cr Skewness value is below the 2.58

value. A data includes multivariate outliers if the

values of p1 and p2 are less than 0.05 (Singgih,

2011). Based on the output, multivariate outliers

were detected, but in this study, the outliers were

maintained because if the outliers were removed it

would cause other outliers. Thus, the next process is

the estimation of the SEM model with the maximum

likelihood (ML) method.

The suitability test of the overall model is done

by using SEM which is also used to analyze the

proposed hypothesis. Based on the results of the

processed data, it can be seen that all constructs used

to form a research model have not met the

requirements of the goodness of fit set out in Figure

2 above. Then the modification of the model is done

with the aim to improve the fit of a model, which is

from a model that is less/not fit to be a fit model

(Yamin and Kurniawan, 2009). If the model is not

fit with the data, the following actions can be done

SEABC 2018 - 4th Sriwijaya Economics, Accounting, and Business Conference

550

by modifying the model by adding or removing

connection/line relationships, adding variables (if

data is available) and reducing variables. Model

modification carried out in this study is based on the

theory described by Arbuckle which discusses how

to make modifications by looking at modification

indices which provide several recommendations for

adding a connection/connection that can reduce chi-

square (r

2

) so that the model becomes more fit or

good. The following is the output modification

indices that provide recommendations for

connection lines that can be connected to obtain

better results seen in Figure 3:

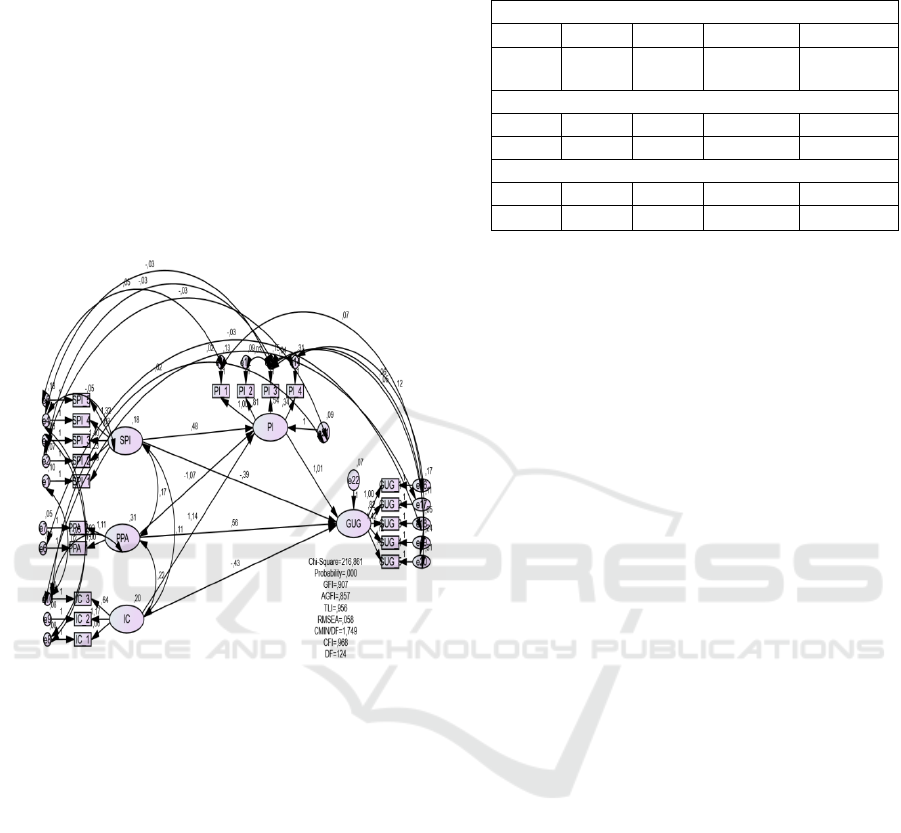

Figure 3: Model After Modification

Of the twelve testing the suitability of the whole

model, there are ten test results that show the model

is of good value or meets the criteria so that it is

concluded that the SEM model.

Structural Equation from the GUG model

a. Direct influence equation

1008 0394 0561

0430

2

Structural equations for GUG can be concluded

that internal control and budgeting participation

have a positive and significant influence each of

1.008 and 0.561. For internal audit units have a

negative and significant effect of 0.394 on good

university governance. But intellectual capital does

not affect the good university governance. Whereas

to find out the results of the formulation of indirect

effects, it can be seen from the standardized direct

effect output, the standardized indirect effect and the

standardized total effect in the following table:

Table 2: Standardized Direct Effect, Standardized Indirect

Effect, and Standardized Total Effect

Standardized Direct Effect

IC

PPA

SPI

PI

GUG

1,259

-0,449

-1,471

0,729

0,510

-0,395

0,000

0,953

0,000

0,000

Standardized Indirect Effect

0,000

0,000

0,000

0,000

0,000

1,201

-1,403

0,486

0,000

0,000

Standardized Total Effect

1,259

-1,471

0,510

0,000

0,000

0,752

-0,674

0.090

0,953

0,000

Source: Source: data processed (2018)

Based on the indirect effect table, it can be

calculated that there is an indirect effect between IC

on GUG of 1.201 (0.953 x 1.259), which means that

internal control is an intervening variable for the

influence of IC on GUG. The same thing with

internal audit unit variable of 0.486 (0.953 x -1.477)

and budgeting participation variable has an indirect

effect of -1.403 (0.953 x -1.497) on GUG means that

all independent variables are mediated by internal

control of GUG.

Testing of the previously proposed hypothesis

where the value of CR with its critical value uses t

count value, which is 1.96 at the significance level

of p <0.05, then the proposed hypothesis is accepted.

However, if the CR value has not been able to reach

its critical value at the significance level of p <0.05,

the proposed hypothesis is rejected. For this study,

the hypothesis (H

1

) internal supervision unit, IC,

budgeting participation affects the GUG through

internal control in PTN in the Southern Sumatra

Region.

Directly the internal supervision unit, budgetary

participation in GUG is influential, but intellectual

capital has no effect on good university governance

in PTN in the Southern Sumatra Region. But the

internal supervision unit, budgetary participation,

and intellectual capital indirectly influence the GUG

through internal control. The hypothesis of this

study was received with a large internal control unit

of 1,201, budgetary participation -1,403, the

intellectual capital was 0.486 so that the internal

control unit had the most dominant indirect

influence compared to other variables.

The results of this study that the internal audit

unit and participation influence the GUG and do not

support the research of Azwar (2013), Fredrick and

Narkiso (2014), Gina et al (2014), Karagiorgos et al

(2010), Kusmayadi, (2012), Radjagukku et al

(2014), Puspitarini (2012), Suyono and Hariyanto

(2012), Sukirman (2012) where efforts to achieve

The Internal Audit Unit, Budgetary Participation, and Intellectual Capital Effect to Good University Governance through Internal Control

551

good governance, in this case, GUG, PTN require

internal supervision units or internal auditor in

supporting the GUG, which is currently a major

component in managing or improving higher

education institutions effectively and efficiently

based on the principles of good governance.

Because the internal audit unit has a negative and

significant influence on the GUG, it means that the

role of the internal supervision unit in PTN Southern

Sumatra Region to realize the GUG is still only a

formality, there are still many state universities in

the Southern Sumatra Region have not optimized

where the SPI is also constrained by human

resources or lack of knowledge related to the role of

SPI and the lack of strong leadership commitment to

the existence of the SPI.

In contrast to Amilin (2016) that there was no

influence of budgeting participation on government

good university, this study found that budgetary

participation had an effect on GUG. This is due to

the fact that PTN in Sumatra Region generally

involves all parts of the university, so that the

achievement of the planned target is what is desired

in the use of the budget. Internal control influences

the GUG supported by the study (Handley-

Schachler, Juleff, and Paton, 2007) and (Stewart-

Weeks and Kastelle, 2015) that university

governance is a public sector with the hope that the

community gets good service quality in the public

sector, it cannot be separated from internal control

because the findings of the BPK-RI are still not

compliant with PTN in Indonesia or in the Southern

Sumatra Region for internal control.

Intellectual capital has no effect on GUG does

not support Ramírez's (2013) research and states that

the presentation of information related to Intellectual

Capital (IC) Widyaningsih (2016) is important in

higher education institutions, especially because

knowledge is the main output both through research

and teaching. Not optimal elements of intellectual

capital are considered to be applied in PTN in the

Southern Sumatra Region, it is seen that there are

still elements of recruitment of employees and

lecturers in a transparent manner and elements of

kinship in the recipients of employees and lecturers

are still thick. Overall the findings of this study

support Stewardship theory view management as a

party that can be trusted to act as well as possible for

the public interest or stakeholders.The implication of

the stewardship theory in this study is that the

steward (in this case is the management of higher

education) will work as well as possible for the

principal's interests (community and government).

organizational interests. But for internal supervision

units and intellectual capital does not support the

stewardship theory of Davis et al (1991), meaning

that governance arrangements in universities or

known as GUG which is a series of processes,

habits, policies, and regulations that are directed and

controlled have not affected intellectual capital and

internal supervision units must be in line for the

application of the GUG in the Southern Sumatra

Region PTN. This study found new findings, namely

that the participation of the participants turned out to

have an effect on the management of state

universities and SPI has a negative effect, which

means that the better the SPI, the GUG will not

materialize, while intellectual capital has no effect

on GUG in the Southern Sumatra Region.

4 CONCLUSION

Research results that the internal control unit has

a direct negative and significant influence but

internal control and budgetary participation have a

direct and positive influence on GUG of state

university in the Southern Sumatra Region. The

internal audit unit, budgetary participation,

intellectual capital influence the GUG through

internal control at state university in Southern

Sumatra. The intellectual capital variable does not

affect the GUG.

It is recommended to increase the role of the

internal audit unit to assist or provide advice and

recommendations to the leadership with the

leadership's commitment to place internal audit units

not just a formality, because there are several state

universities in the South Sumatra Region. SPI

workplaces are not yet feasible and programs that

have been approved not implemented yet. It is

expected that the effective role of the SPI will

embody GUG.

Increasing the intellectual capital that consists of

Human Capital, Structural Capital, and Relational

Capital by cooperating with other universities both

at home and abroad. There needs to be a policy from

the government, especially the Ministry of Research

and Technology, to continue to improve the more

innovative learning systems in universities such as

learning curriculum and improve the ability of

students or as soon as possible to implement cyber

university which is a solution to reach quality higher

education. For further research with the same theme

to be able to add leadership commitment variables,

alliance strategies and dimensions of GUG with

justice.

SEABC 2018 - 4th Sriwijaya Economics, Accounting, and Business Conference

552

This study has limitations, among others, that the

factors that apply GUG are not only SPI, budgetary

participation, intellectual capital and internal control,

but there are still many other factors that influence

GUG such as organizational culture and leadership

commitment. The population used in subsequent

studies can expand state universities including state

universities throughout Indonesia so that they are

close to the results that are closer to the actual

conditions. If necessary, compare between new state

universities and those who have long been

established.

REFERENCES

A Arens, Randal, E., & Beasly, M. S (2012). Auditing and

Assurance Services : An Integrated Apporach.

Fourteenth Edition.

Aisyah, Husaini, Halimatusyadiah, A. (2013). Peran

Satuan Pengawasan Intern (SPI) di Perguruan Tinggi

Negeri Indonesia. Laporan Akhir Penelitian

Universitas Bengkulu.

Aisyah, Husaini, Halimatusyadiah, A. (2013). Peran

Satuan Pengawasan Intern (SPI) di Perguruan

Tinggi Negeri Indonesia. Laporan Akhir Penelitian

Universitas Bengkulu.

Amilin. (2016). Dampak Penerapan Good Universuty

Governance Terhadap kinerja Manajerial Melalui

Implementasi Anggaran berbasis Partisipatif. Jurnal

Akuntansi Universitas Tarumanagara, XX(03),

330–344.

Anwar Azwar. (2013). Peran SPI Terhadap Pencapaian

Opini WTP Dan Pencegahan Korupsi Melalaui

PEnerapan GUG (Analisis Studi Pustaka). Ikhtiyar,

Volume 11 N0.1 Januari-Maret 2013, 11(1).

Argyris, C. (1952). The Impact of Budgets on People.

New York: The Controllership Foundation.

Badara, M., & Saidin, S. (2013). Impact of the effective

internal control system on the internal audit

effectiveness at local government level. Journal of

Social and Development Sciences, 4(1), 16–23.

Bill, B. B. M., Barry, L., & Roebuck Petter. (1997).

Global Competency Frame Work For Internal

Auditing Project. In The Institude of Internal

Auditor.

BPK RI. (2008). Peraturan Pemerintah RI Nomor 60

Tahun 2008, Tentang Sistem Pengendalian Intern

Pemerintah.

Brownell, P., & Mclness, M. (1986). Budgetary

Participation, Motivation, and Manajerial

Performance. The Accounting Review, LXI(4), 587-

600

Bruyneels, L., Knechel, W. R., & Wilekens, M. (2006).

Do industry specialists and business risk auditors

enchance audit reporting accurary? Dtew -

Afi_0610, 1-37.

Byrne, B. M. (2016). Structural Equation Modeling

with AMOS. Structural Equation Modeling (Third

Edit).

Choong, K. (2008). Intellectual capital: definitions,

categorization and reporting models. Journal of

Intellectual Capital, 9(4), 609–638.

Coaldrake, P., Stedman, I., & Litte, P. (2003). Issues in

Australian University Governance.

Davis, J. H., Schoorman, F. D., & Donaldson, L.

(1991). Toward a Stewardship Theory of

Management Toward A Stewardship Theory Of

Management. Academy of Management Review,

22(1), 20-47.

Dewi, R., & Apandi, N. N. (2012). Gejala Fraud dan

Peran Auditor Internal dalam Pendeteksian Fraud di

Lingkungan Perguruan Tinggi. SNA XV

Banjarmasin, 1–28.

Edvinsson, L. (2013). Developing Intellectual Capital at

Skandia Understanding Knowledge Management.

Long Range Planning, 30(3), 366–373.

Effendi, M.A. (2016). The Power of Good Corporate

Governance Teori dan Implementasi.

Ferdinand, A. (2014). Metode Penelitian Manajemen,

(5th ed.). Semarang: Universitas DIponegoro Press.

Fisher, J. (1998). Contingency theory, management

control system and firm outcomes: past results and

future directions. Behavioral Research in

Accounting, 10, 47-64.

Gina, O., Adeghe, R., & Kingsley, O. O. (2014).

Internal Control As A Potential Instrument For

Corporate Governance. IOSR Journal of Economics

and Finance (IOSR-JEF), 2(6), 66–70.

Goodwin, J. (2003). The Relationship Between the

Audit Committee and the Internal Audit Function:

Evidence from Australia and New Zealand.

International Journal of Auditing Int. J. Audit,

7(April), 263–278.

Gudono. (2011). Analisis Data Multivariat (Pertama).

Yogyakarta: BPFE UGM.

Hadisantoso, E. (2017). The Influence of

Profesionalism and Competence of Auditors

towards the Performance of Auditors. Scientifics

Research Journal, V(I), 10-14

Hénard, F., & Mitterle, A. (2010). Governance and

Quality Guidelines in Higher Education: A review

of Governance Arrangements and Quality

Assurance Guidelines. OECD.

Huang, C. C., Luther, R. G., & Tayles, M. E. (2007).

An evidence-based taxonomy of intellectual capital.

Journal of Intellectual Capital, 8(3), 386-408.

Jaramillo, A., & Zaafrane, H. (2014). Benchmarking

university governance in the MENA region. Higher

Education Management and Policy, 24(3), 7-36

Jones, N., Meadow, C., & Sicilia, M.-A. (2009).

Measuring intellectual capital in higher education.

Journal of Information and Knowledge

Management, 8(2), 113–136.

Karagiorgos, T. D., Gotzamanis, E., & Tampakoudis, L.

(2010). Internal Auditing As an Effective Tool For

Corporate Governance. Journal of Business

Management.

The Internal Audit Unit, Budgetary Participation, and Intellectual Capital Effect to Good University Governance through Internal Control

553

Kennedy, K. J. (2003). Higher Education Governance

as a Key Policy Issue in the 21st Century.

Educational Research for Policy and Practice, 2(1),

55–70.

Kennis, I. (1979). Effect of Budgetary Goal

Characteristic on Managerial Attitudes and

Performance. The Accounting Review, LIV(4).

Kiabel, D. (2012). Internal Auditing and Performance

of Governance of Government Enterprises: A

Nigerian Study. Global Journal of Management

and Business Research, 12(6),6.

Kickbusch, I., & Gleicher, D. (2012). Governance for

Health in The 21st century. Who, 1–106.

https://doi.org/15 January, 2016

Kusmayadi, D. (2012). Determinasi audit internal

dalam mewujudkan good corporate governance

serta implikasinya pada kinerja bank. Jurnal

Keuangan Dan Perbankan, 16(1), 152.

Learmount, S. (2004). Corporate Governance: What

Can Be Learned From Japan? Corporate

Governance: What Can Be Learned From Japan?

Lee, J. (2001). School reform initiatives as balancing

acts:Policy variation and educational convergence

among Japan, Korea, England and the United

States. Education Policy Analysis Archives.

Marfuah dan Amanda. (2014). Pengaruh Partisipasi

Anggaran Terhadap Senjangan Anggaran Dengan

Menggunakan Komitmen Organisasi, dan Informasi

Asimetri Sebagai Variabel Pemoderasi.

EKBISI,VII(2), 200-218

Martini, R. (2015). Analisis Penerapan Good University

Governance Melalui Efektifitas Pengendalian Intern

dan Komitmen Organisasional. SNA XVII,

Sumatera Utara.

Moeller, R. R. (2012). Brink's Modern Internal

Auditing. Brink's Modern Internal Auditing : A

Common Body of Knowledge: Seventh Edition.

Nauli Radjagukku, Ramantha, Mimba, M. (2014).

Pengaruh Peran Satuan Pengawasan Intern dan

Komite Audit Terhadap Tingkat Penerapan Good

Corporate Governance Pada PT Pengembangan

Pariwisata Bali (Persero)BTDC. E-JUrnal Ekonomi

Dan Bisnis Universitas Udayana, 3(7), 391–402.

Nizam. (2006). Indonesia: The Need for Higher

Education Reforms. Higher Education in Southeast

Asia, 35–68.

Nurhanasah. (2016). Efektivitas pengendalian internal,

audit internal, karakteristik instansi dan kasus

korupsi. Tata Kelola & Akuntabilitas Keuangan

Negara.

Odoyo, F. S., Omwono, G. A., & Okinyi, N. O. (2014).

An Analysis of the Role of Internal Audit in

Implementing Risk Management-a Study of State

Corporations in Kenya. International Journal of

Business and Social Science, 5(6), 169–176.

Ompusunggu, Krisler, I. (2006). Pengaruh Partisipasi

Anggaran dan Job Relevant Information terhadap

Informasi Asimetris. In Simposium Nasional

Akuntansi IX Padang.

Otley, D. T. (1980). The contingency theory of

management accounting: Achievement and

prognosis, Accounting, Organization and Society,

5(4), 413-428

Peraturan Pemerintah No 4 Tahun 2014. (2014).

Penyelenggaraan Penddikan Tinggi dan

Pengelolaan Perguruan Tinggi.

PP 4 Tahun 2014, (1989). Penyelenggaraan Pendidikan

Tinggi Dan Pengelolaan Perguruan Tinggi, 53,

160.

Puspitarini, N. D. (2012). Peran Satuan Pengawasan

Intern Dalam Pencapaian Good University

Governance Pada Perguruan Tinggi Berstatus Pk-

Blu. Accounting Analysis Journal, 1(2).

Rafiee, M., & Mosavi, M. (2010). Formulating and

Elaborating a Model for the recognition of

Intellectual Capital in Iranian universities. In

Proceedings of 2010 International Conference on

Innovation, Management and Service (pp. 14–23).

Ramírez-Córcoles, Y. (2013). Intellectual capital

management and reporting in European higher

education. Intangible Capital, 9(1), 1–19.

Rastogi, P. N. (2002). Knowledge management and

intellectual capital as a paradigm of value creation.

Human System Management, 21, 229-240.

Rizal, M. T. (2013). Governance Perguruan Tinggi.

Direktorat Kelembagaan Dan Kerjasama Ditjen

Pendidikan Tinggi.

Rosca, I. G., Nastase, P., & Mihai, F. (2010).

Information System Audit for University

Governance in Bucharest Academy of Economic

Studies. Informatica Economica, 14(1), 21-31. R.

Sawyer's. (2005). Audit Internal Sawyer (Edisi

Keli). Jakarta: Salemba Empat

Stewart-Weeks, M., & Kastelle, T. (2015). Innovation

in the Public Sector. Australian Journal of Public

Administration, 74(1), 63-72

Sukirman, & Sari, P. M. (2012). Peran Internal Audit

dalam Upaya Mewujudkan Good University

Governance di Unnes. Jurnal Dinamika Akuntansi,

4(1), 64–71.

Suryani, I. (STIE G. W. B. (2015). Good University

Governance. Jurnal Riset Akutansi, VII(2).

Suyono, E., & Hariyanto, E. (2012). Relationship

Between Internal Control, Internal Audit and

Organization Commitment With Good Governance

Indonesian Case. Business Review, 11(9), 1237–

1245.

Sveiby, K.-E. (2001). A knowledge-based theory of the

firm to guide in strategy formulation. Journal of

Intellectual Capital, 2(4), 344–358.

Syahputra, Z. (2014). Budget Participation on

Managerial Performance : Related Factors i n that

influenced to Government’s Employee ( Study of

Indonesian Local Government ), 5(21), 95–100.

Zaman, K. (2015). Quality guidelines for good governance

in higher education across the globe. Pacific Science

Review B: Humanities and Social Sciences, 1(1), 1–7.

SEABC 2018 - 4th Sriwijaya Economics, Accounting, and Business Conference

554