The Effects of Environmental Performance and Environmental

Information Disclosure on Financial Performance in Companies

Listed on the Indonesia Stock Exchange

Msy. Mikial

1

, Taufiq Marwa

2

, LukLuk Fuadah

2

, Inten Meutia

2

1

Faculty of Economics, Tridinanti University, Palembang, Indonesia

2

Faculty of Economics, Universitas Sriwijaya, Palembang, Indonesia

Keywords: Environmental Performance, Environmental Information Disclosure, Financial Performance

Abstract: The purpose of this study is to examine the effects of environmental performance and environmental

information disclosure on financial performance in companies listed on the Indonesia Stock Exchange. The

sample in this study only 20 companies listed on the Indonesia Stock Exchange, issued an Annual Report and

Sustainability Report and included in the Sustainability Disclosure Database of the Global Reporting Initiative

(GRI). The data used in the form of secondary data obtained from annual reports and sustainability reports of

companies listed on the Indonesia Stock Exchange from 2013 to 2016. The analysis technique used was Partial

Least Square (PLS). The results of this study show that environmental performance has a positive but not

significant effect on financial performance, environmental information disclosure has a negative and

significant effect on financial performance. Disclosure of environmental information is more equipped and in

accordance with the disclosure guidelines, the cost is not small so that it will reduce financial performance.

Future research can develop other variables for a more comprehensive dimension, with a longer span of time

and a greater number of companies in publishing Sustainability Reporting.

1 INTRODUCTION

Indonesian public awareness on the importance of

the environment starts to grow slowly. People who

believe that the environment carried out by the

company focuses more on using technology as

efficiently as possible and unwittingly ignoring

environmental aspects. The government has also

established regulations on environmental

management, but there are still many companies that

contribute to the problem of environmental pollution.

In recent years, the concept of sustainability has

become a major issue of the company's development.

This concept arises due to the demands and

expectations of the community about the company's

role in society. Sustainability Reporting is a trend and

need for companies to inform about economic, social

performance and its environment at the same time to

all stakeholders of the company. Sustainability

Reporting contains not only financial performance

information but also non-financial information

consisting of information on social and

environmental activities that enable companies to

grow sustainably.

Environmental performance can be measured by

how effective the company's expenditure is to prevent

and protect the environment. In fact, most companies

have not fully disclosed the environmental costs of

the company and are usually only included in indirect

costs (factory overhead). This results in high

production costs, resulting in incorrect profit margins

and ultimately an impact on the profitability of the

company. The company will consider the costs and

benefits that will be obtained when they decide to

disclose environmental information including

environmental costs. If the benefits obtained by

disclosure of information are greater than the costs

incurred, the company will voluntarily disclose the

information and if the benefits are not too much, the

company will not disclose that information. Usually

large companies that are very interested in disclosing

environmental information through annual reports,

sustainability reports, and websites, because of the

guidance of most stakeholders on environmental

information.

Mikial, M., Marwa, T., Fuadah, L. and Meutia, I.

The Effects of Environmental Performance and Environmental Information Disclosure on Financial Performance in Companies Listed on the Indonesia Stock Exchange.

DOI: 10.5220/0008442105250532

In Proceedings of the 4th Sriwijaya Economics, Accounting, and Business Conference (SEABC 2018), pages 525-532

ISBN: 978-989-758-387-2

Copyright

c

2019 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

525

The company has an interest in improving

environmental performance with the ultimate goal to

increase the profits gained, as stated by Nakao,

Amano, Matsumura, Genba, & Nakano, (2007),

Suratno, Darsono, & Mutmainah, (2006) and

Earnhart & Lizal, (2010) there is a positive influence

of the company's environmental activities

(environmental performance) on financial

performance. According to Moneva & Ortas (2010)

companies with good environmental performance

will be followed by a good financial position, because

it increases efficiency, consolidates the financial

situation and meets the demands of the company's

stakeholders. Improved environmental performance

will lead to the use of cost-effective organizational

resources so that businesses that are environmentally

responsible will be able to report higher returns that

lead to enhanced value than companies that are less

responsible (Porter & Linde, 1995). Contrary to the

research of Walker & Wan, (2012) and Horváthová,

(2010) who found that environmental performance

has a negative effect on financial performance.

Likewise with the results of Dragomir, (2010)and

Gibson Nyirenda, (2013) research which states that

no relationship was found between performance

environments with financial performance.

Information on environmental performance needs

to be disclosed to the community, in these case

stakeholders, although the nature of its disclosure is

still voluntary. With the disclosure of environmental

information, the company's image is expected to

increase and increase stakeholder perceptions, which

will further improve the company's financial

performance. Oba, Fodio, (2012), Ong, Tho, Goh,

Thai, & Teh, (2016) and Mahmes, (2016) state that

there was a positive and significant relationship

between the quality of environmental information

disclosure on financial performance, while

Malarvizhi, (2016) find out no significant relationship

between the level of environmental disclosure and the

company's financial performance.

The novelty in this study is to measure

environmental performance based on outcomes,

namely environmental costs incurred by the

companyin accordance with the guidelines in Global

Reporting Initiates G4 - En 31.The cost of a well-

managed environment will improve environmental

performance because there are efficient use of

resources. In the end it will improve the company's

financial performance. Companies with good

environmental performance will disclose

environmental information to meet stakeholder

demands.

The objective of this study is to analyze and

examine empirically the effect of environmental

performance and environmental information

disclosure on financial performance at companies on

the Indonesia Stock Exchange that publish

Sustainability Reporting. This research was

developed through explanation and justification of

data collected and continued with results and

implications.

2 LITERATURE REVIEW,

DEVELOPMENT OF THEORY

AND HYPOTHESES

2.1 Stakeholder Theory

Stakeholder theory is used as a basis for analyzing

groups for companies to be responsible. Stakeholder

theory introduced by Freeman (1984) states that the

company is an organ that deals with other interested

parties, both inside and outside the company. So the

success of a company depends heavily on the success

of management in managing relationships with its

stakeholders.

The concept of stakeholders is described by Evan

and Freeman (1993) as the following two principles:

1. The principle of company legitimacy.

Corporations must be managed for the benefit of

stakeholders: customers, suppliers, owners,

employees and local communities. The rights of

these groups must be ensured, and furthermore,

groups must participate, in a sense, in decisions

that substantially affect their welfare.

2. Fiduciary principles of stakeholders. Management

bears fiduciary relationships to stakeholders and

corporations as abstract entities. In this case it

must act in the interests of the stakeholders as

their agent, and must act in the interests of the

corporation to ensure the survival of the company,

maintain their existence in the long term.

2.2 Environmental Performance!

Bennett and James (1999) emphasize

environmental performance as the company's

achievement in managing any interaction between the

company’s activities, products or services and the

environment.

Enviromental performance is measured by

environmental costs, namely company expenditures

for mitigation and environmental protection show

how effectively organizations use resources to

SEABC 2018 - 4th Sriwijaya Economics, Accounting, and Business Conference

526

improve performance. These expenditures allow

organizations to assess the value of investments for

complex organizations or technologies (GRI, 2013).

Environmental costs can be expressed as costs to

minimize environmental impacts caused by the

company's business activities and costs associated

with it. Environmental costs include all costs incurred

due to the use of inputs (energy, water, materials) and

the disposal of non-product outputs (waste and

emissions) plus other costs associated with efforts to

protect the environment. Environmental costs are

basically related to the costs of important products,

processes, systems or facilities for better management

decisions (Ikhsan, 2009).

2.3 Environmental Information

Disclosure

Environmental information disclosure are:

"Environmental disclosure was taken to comprise

disclosure relating to the company's attitude, policy

or behavior towards its environmental impact,

emissions, pollution, cleaning up (after pollution), re-

landscaping or energy efficiency (that was not

intended as an explicit economic

message)"(Campbell, 2004)

The disclosure of environmental information in

the annual report is one of the effective disclosure

methods because this report is the main source of

information for investors, creditors, customers,

employees, environmental groups and government

(Patten, 1992). This report is also a medium for

companies to publish all information about

companies that need to be known by the company to

the public, including information about the

environment, which is issued periodically, made by

almost all companies, and easy to read and compare.

Wang, (2016) states that the disclosure of

environmental information is beneficial for relevant

government authorities, practitioners, and academics

in helping to understand the value relevance of

environmental information disclosure and corporate

governance in decision making for various purposes

such as investment, financing, consumption, and

labor supply.

The Sustainability Reporting Guidelines, also

referred to as the Global Reporting Initiative (GRI),

are the most widely used guidelines for

environmental information disclosure. Global

Reporting Initiative (GRI) G4 is an ongoing reporting

guideline that contains the latest disclosure of

environmental information. Sustainability reporting

helps organizations to set goals, measure

performance, and manage change in order to make

their operations more sustainable. A sustainability

report conveys disclosures about the impact of the

organization - whether positive or negative - on the

environment, society and the economy. In an effort to

make it happen, sustainability reporting makes

abstracts real and concrete, thus helping in

understanding and managing the impact of

sustainable development on organizational activities

and strategies. Disclosures and metrics that are agreed

internationally allow information contained in

sustainability reports to be accessed and compared, so

as to provide additional information to stakeholders

to make decisions (GRI, 2013).

2.4 Financial Performance

Financial performance is a description of the

company's financial condition in a certain period of

both aspects of fund raising and channeling of funds,

which is usually measured by indicators of capital

adequacy, liquidity and profitability (Werner et al.,

2013).Financial performance describes the work

performance that has been achieved by the company

in a certain period and contained in the company's

related financial statements. Return on Investment

(ROI), Return on Assets (ROA), and Return on

Equity (ROE) are the most commonly used measures

of profitability. ROI and ROA are often used

interchangeably because they refer to the same thing,

namely the ratio between earnings and assets owned,

while ROE refers to the amount of the company's

equity.

Ezejiofor, (2016) found that environmental costs

have no effect positive on the income of corporate

organizations in Nigeria. In addition, environmental

costs also positively influence the formation of

corporate earnings, and there is a significant influence

of sustainability policies, strategies and operations on

financial performance. Birkin & Woodward, (1997)

state that there is a relationship between

environmental performance and financial

performance through cost efficiency generated by

good environmental performance.Nakao et al., (2007)

research results stated that the company's

environmental performance has a positive influence

on its financial performance and is verified more

clearly when information about the company's

response to business Environmental services are

included with information about environmental

management activities. Clarkson, Overell, &

Chapple, (2011) research shows that not only

companies with higher pollution trends reveal more

environmental information, poor environmental

performance (high pollutant companies) make

The Effects of Environmental Performance and Environmental Information Disclosure on Financial Performance in Companies Listed on

the Indonesia Stock Exchange

527

voluntary disclosure on environmental performance.

Thus, high environmental reporting does not

necessarily mean high environmental performance.

The results of Nor, Bahari, Adnan, Kamal, & Ali,

(2016) state that there is a significant relationship

between total environmental disclosure and profit

margins. Disclosure of environmental information

will benefit the market and the ability to benefit from

investments in environmental improvement.

However, the findings for the other three variables,

namely ROA, ROE, and EPS show no significant

relationship between total environmental disclosure.

2.5 Development of Theory

Contemporary economists state that companies

not only create profit or welfare for shareholders, but

also provide welfare to all stakeholders. This means

that companies are not only oriented to maximizing

profits to shareholders, but companies are also

required to contribute and commit to social and

environmental activities to their stakeholders.

Stakeholder theory assumes that the existence of a

company is determined by its stakeholders.

According to stakeholder theory,

organizations/companies will voluntarily disclose

information about environmental and social

performance. Companies have a tendency to satisfy

stakeholders because they need support to improve

company performance and continue operations. To

meet the demands of stakeholders for

environmentally friendly products, the company

strives to make environmental cost efficiency efforts

that reflect the company's environmental

performance, and try to disclose its environmental

information with the aim of meeting stakeholder

demands. The company seeks to improve

environmental performance and disclose

environmental information in sustainability reports

with the aim of gaining legitimacy from the

community.

Hypothesis :

H1 :Environmental performance have a positive

effect on financial performance in companies

listed on the Indonesia Stock Exchange.

H2 : Environmental information disclosurehave a

positive effect on financial performance in

companies listed on the Indonesia Stock

Exchange.

3 METHODOLOGY

3.1 Data Sources and Data Collection

Data sources in the form of secondary data come

from electronic publications that are accessed from

internet. The data collection method used in this study

is documentation. Data obtained from various sources

include data from sustainability reports and company

annual reports on the Indonesia Stock Exchange and

in the Sustainability Disclosure Database of the

Global Reporting Initiative (GRI), from literature,

journals and other sources related to problems in

research.

3.2 Population and Sample

The population of this study is all companies

registered in the 2013-2016 Indonesia Stock

Exchange Which have following criteria:

(1) Issue full Annual Report and Suitability Report

(2) Having data regarding disclosure of

environmental information

(3) Having data on environmental costs

(4) Included inthev Sustainability Disclosure

Database from the Global Reporting Initiative

(GRI)

Table 1: List of Companies Registered on the IDX in 2017

No

Code

Company Name

1

ANTM

Aneka Tambang (Persero) Tbk

2

ASII

Astra International Tbk

3

ELSA

Elnusa Tbk

4

INCO

Vale Indonesia Tbk

5

INDR

Indo Rama Synthetic Tbk

6

INTP

Indocement Tunggal Prakasa Tbk

7

ITMG

Indo Tambangraya Megah Tbk

8

PTBA

Tambang Batubara Bukit Asam

(Persero) Tbk

9

PTRO

Petrosea Tbk

10

SMCB

Holcim Indonesia Tbk

11

SMGR

Semen Indonesia (persero) Tbk

12

TINS

Timah (Persero) Tbk

13

WTON

Wijaya Karya Beton Tbk

14

PGAS

Perusahaan Gas Negara (Persero)

Tbk

15

UNTR

United Tractors Tbk

16

BBNI

Bank Negara Indonesia Tbk

17

BMRI

Bank Mandiri (persero) Tbk

18

GIAA

Garuda Indonesia (persero) Tbk

19

BNII

PT Bank Maybank Indonesia Tbk

20

BBRI

Bank Rakyat Indonesia (persero)

Tbk

Source : www.idx.co.id

SEABC 2018 - 4th Sriwijaya Economics, Accounting, and Business Conference

528

Based on the predetermined criteria, the sample

only 20 companies registered in the Indonesian

Securities Exchange, publishes the Annual Report

and Sustainability Report and is included in the

Sustainability Disclosure Database of the Global

Reporting Initiative (GRI) for the period 2013-2016

(4 years), resulting in 80 observations.

3.3 Operational Definition and Variable

Measurement

The variables in this study consisted of:

1. Environmental performance (X

1

)

Environmental performance is activities carried

out by companies that are directly related to the

surrounding natural environment. This variable is

measured using environmental costs, namely costs to

minimize environmental impacts caused by the

company's business activities and costs associated

with it. Environmental costs are measured by the

company's total environmental expenditure and

investment protection based on guidelines from GRI

G4 En-31.

2. Disclosure of environmental information (X

2

)

Disclosure of environmental information is a set

of past, present and future information regarding

company activities and environmental performance

including information about financial implications

resulting from environmental management decisions

or actions by the company. This variable is measured

by disclosures based on the dimensions and indicators

of Global Reporting Initial G4 (2013) as many as 34

indicators, which consist of aspects of material,

energy aspects, water aspects, biodiversity aspects,

emissions aspects, effluent and waste aspects, product

and service aspects, compliance aspects,

transportation aspects, other aspects, and aspects of

supplier assessment on the environment. By using a

checklist compiled based on disclosure indicators to

calculate how much was disclosed compared to what

should be disclosed.

3. Financial Performance (Y)

Finance is a measure of the company's success in

monetary units. The indicator used to measure

financial performance is the company's profitability,

namely Return on Equity (ROE), which describes the

profit ratio obtained with equity owned by the

company.

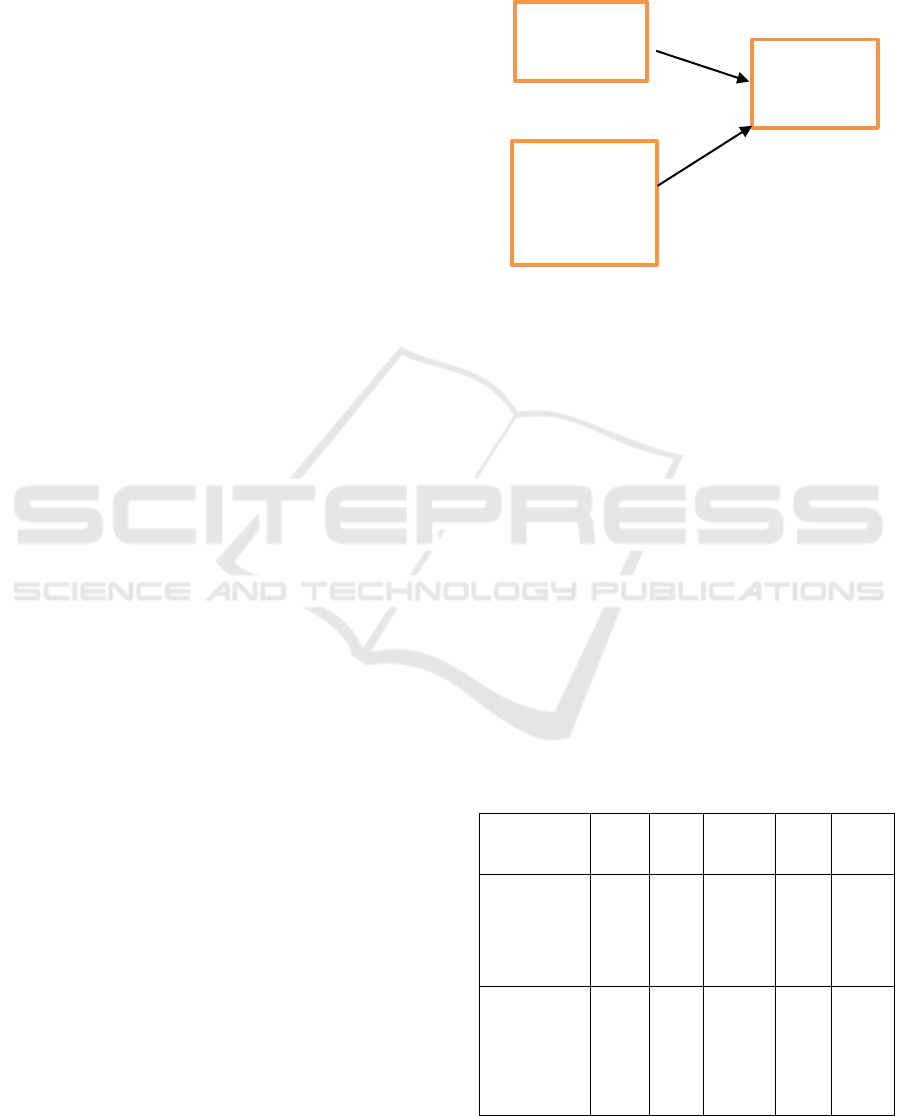

3.4 Technique of Analysis

The research model submitted to be tested is as

follows:

Enviromental

Performance

β

1

(X

1

) Financial

Performance

(Y)

β

2

Enviromental

Information

Disclosure

(X

2

)

Equation:

Y = β

1

X

1

+ β

2

X

2

+ ε(1)

The analytical tool uses Smart PLS software.

Partial Least Square (PLS) software is an analytical

method that is soft modeling because it does not

assume the data must be with a certain measurement

scale, which means the number is small (under 100

samples).The data in this study amounted to 80, so it

was suitable to use PLS

4 RESULT

4.1 Path Coefficient

The efficiency of exogenous variable paths to

endogenous variables can be seen in the Table 2

below:

Table 2: Path Coefficient

Original

Sample

(O)

Sample

Mean

(M)

Standard

Error

(STERR)

t-

Statistics

(|O/STE

RR|)

P Values

Enviromental

Performance

(X1) ->

Financial

Performance

(Y)

0,139

0,146

0,098

1,426

0,077

Environment

alInformation

Disclosure

(X2) -

>Financial

Performance

(Y)

-0,265

-0,270

0,090

2,944

0,002

The Effects of Environmental Performance and Environmental Information Disclosure on Financial Performance in Companies Listed on

the Indonesia Stock Exchange

529

4.2 The Effects of Environmental

Performance on Financial

Performance

Based on the estimation results shown in Table 2,

it can be seen that Environmental performance (X

1

)

does not affect financial performance (Y). This

condition is characterized by a statistical t value of

1.426 and a p value of 0.077 significant at the level of

α 5%. The direction of its influence is negative.

The results of this study were not in line with

some of the results of previous studies which stated

that environmental performance has an effect on

financial performance, such as the results of research

by Nakao et al. (2007), Suratno et al. (2006), Earnhart

& Lizal, (2010a) and Moneva & Ortas, (2010b). The

results of their research can explain that companies

with better environmental performance will increase

profitability.

The results of previous studies to measure

environmental performance use many measures of

compliance with regulations, while this study uses an

outcomes approach in the form of environmental

costs incurred by the company covering total

environmental expenditure and investment protection

as environmental performance. In this study the

environmental performance with proxy

environmental costs issued by the company

apparently cannot affect financial performance. The

results of this study are in line with the research

conducted by Dragomir, (2010) and Nyirenda et al.,

(2013) which states that no relationship was found

between environmental performance and financial

performance.

In fact, not many companies are aware of the

importance of environmental performance to be able

to improve the company's financial performance.

Companies in Indonesia in particular, not many

separate the costs associated with the environment in

individual items in the cost group and still include

them in factory overhead costs, so that company

management will experience difficulties when

making decisions relating to environmental

conservation. In reality environmental management

accounting facilitates the management of

environmental costs and reduces costs through

making connections between costs and the underlying

activities (Noodezh & Moghimi, 2015).

The environmental cost approach with the

environmental quality cost model adopted by the

quality cost model by Hansen, Don R; Mowen,

(2007) allows companies to prioritize prevention of

environmental damage before it occurs compared to

handling if environmental damage has occurred. This

is also in line with Al-Tuwaijri et al, (2004) which

states that managers must change their strategies

regarding environmental performance, namely from

the emphasis on the costs of handling pollution and

environmental damage (pollution abatement costs) to

be costs for prevention of pollution and

environmental damage (pollution prevention costs).

Moneva & Ortas, (2010b) states that companies with

good environmental performance have good financial

performance in the future. This is because good

environmental performance can improve efficiency,

consolidate financial situations and meet the demands

of corporate stakeholders. Thus, if managers ignore

environmental factors when designing strategic

policies, the company will lose competitiveness in the

long run. This is in accordance with stakeholder

theory which states that a company is an organ that

deals with other interested parties, both inside and

outside the company, so the existence of the company

is determined by stakeholders.

4.3 The Effects of Environmental

Performance and Environmental

Information Disclosure on Financial

Performance

Disclosure of environmental information (X

2

)

affects financial performance (Y). This condition is

marked by a statistic value of 2.944 and a p value of

0.002 <0.05. The direction of its influence is negative,

meaning that the more complete the disclosure of

environmental information, the financial

performance will decrease.

This condition indicates that environmental

information disclosure causes the declining

components of financial performance. In the initial

and short-term stages, disclosure of environmental

information weighs on the company so that it incurs

additional costs and disrupts the company's financial

performance.

The results of this study are not in line with the

previous research conducted by Mahmes, (2016) and

Nor et al., (2016) that there is a significant influence

/ relationship between total environmental disclosure

and profit margins. By disclosing information about

the environment the company will gain market

benefits and the ability to benefit from investments in

environmental improvement, so that its financial

performance increases. Stakeholder theory states that

information is one of the media to obtain support and

manage relationships with stakeholders (Gray, 1994).

Environmental information disclosure is often used

by companies to create a good image in the eyes of

stakeholders, especially customers and investors. If

SEABC 2018 - 4th Sriwijaya Economics, Accounting, and Business Conference

530

the customer has a good image about the company, it

is likely that it will affect his behavior in buying

company products so that it is expected to improve

financial performance through increased sales(Ling,

2007). Previous theory and research cannot be proven

in this study because of the fact that even companies

with very low levels of environmental information

disclosure can increase sales. This study supports

research from Malarvizhi, (2016) whose results show

that there is no significant relationship between the

level of environmental disclosure and company

performance. Companies that do not generate large

profits also disclose information about the

environment. In order to maintain a global

environment, companies must disclose

environmental information even though their

financial performance is not good.

5 CONCLUSIONS, LIMITATIONS

AND RECOMMENDATIONS

5.1 Conclusions

Based on the formulation of the problem, the

formulation of the hypothesis and the results of the

study, the following conclusions can be drawn:

Environmental performance has positive but not

significant effect on financial performance, while

environmental information disclosure has a

significant effect on financial performance. In fact,

not many companies are aware of the importance of

environmental performance to be able to improve the

company's financial performance. The disclosure of

environmental information has a negative effect on

financial performance, it shows that if environmental

information disclosure is more completed it will

reduce financial performance. This condition

indicates that disclosure of environmental

information causes the deciding component of

financial performance. Disclosure of environmental

information in the initial stages burdens the company

with additional costs and this can reduce the

company's financial performance.

5.2 Limitations

The first limitation of this study is the difficulty in

obtaining environmental cost data because the

company has no obligation to disclose environmental

costs so that the sample is limited to companies listed

on the IDX that have a Sustainability Report and are

included in the Sustainability Disclosure Database of

the Global Reporting Initiative (GRI). The second

limitation, this study only focuses two environmental

variables influence financial performance.

5.3 Recommendations

Based on the conclusions, it is expected that

Indonesian Accounting Association as an accounting

profession organization in Indonesia is expected to be

able to formulate measurement and reporting

standards for environmental cost information so that

reporting and disclosure can be generated separate

and standardized environmental information. For

other researchers who are interested in researching

environmental accounting can develop other

variables such as environmental regulation,

environmental audit, organizational commitment, and

others with a more comprehensive dimension and

with a longer span of time and a greater number of

companies in publishing Sustainability Reporting.

REFERENCES

Al-tuwaijri, S. A., Christensen, T. E., & Ii, K. E. H. (2004).

The relations among environmental disclosure ,

environmental performance , and economic

performance : a simultaneous equations approach.

Society, 29(801), 447–471.

https://doi.org/10.1016/S0361-3682(03)00032-1

Bennett, M and James, P. 1999. Sustainable measures:

evaluation and reporting of environmental and social

performance. Greenleaf Publishing.

Birkin, F. K., & Woodward, D. G. (1997). Accounting for

the sustainable corporation. Environmental

Management and Health, 8(2), 67–72.

https://doi.org/10.1108/09566169710166557

Campbell, D. (2004). A longitudinal and cross-sectional

analysis of environmental disclosure in UK companies

- A research note. British Accounting Review.

https://doi.org/10.1016/j.bar.2003.09.001

Clarkson, P. M., Overell, M. B., & Chapple, L. (2011).

Environmental Reporting and its Relation to Corporate

Environmental Performance. Abacus.

https://doi.org/10.1111/j.1467-6281.2011.00330.x

Dragomir, V. D. (2010). Environmentally sensitive

disclosures and financial performance in a European

setting. Journal of Accounting & Organizational

Change, 6(3), 359–388.

https://doi.org/10.1108/18325911011075222

Earnhart, D., & Lizal, L. (2010). The Effect of Corporate

Environmental Performance on Financial Outcomes –

Profits , Revenues , and Costs : Evidence from the

Czech Transition Economy * Dietrich Earnhart # The

Effect of Corporate Environmental Performance on

Financial Outcomes – Profits ,. Environmental &

Resource Economics, European Association of

The Effects of Environmental Performance and Environmental Information Disclosure on Financial Performance in Companies Listed on

the Indonesia Stock Exchange

531

Environmental and Resource Economists, 46(3), 1–44.

Epstein, E. M., Freeman, R. E., Carroll, L., Pitman, C. C.,

& Freeman, O. R. E. (n.d.). MANAGEMENT

CONSULTING EDITOR.

Evan, W. M. and Freeman, R. E. , 1993 ‘A Stakeholder

Theory of the Modern Corporation: Kantian

Capitalism’, in T. L. Beauchamp and N. E. Bowie

(eds.), Ethical Theory and Business. Englewood CliVs,

NJ: Prentice-Hall

Ezejiofor, R. A. (2016). Effect of Sustainability

Environmental Cost Accounting on Financial

Performance of Nigerian Corporate Organizations.

International Journal of Scientific Research and

Management, (April).

https://doi.org/10.18535/ijsrm/v4i8.06

Freeman, R. Edward, 1984. Strategic Management : A

stakeholder Approach. Pitman Boston.

Gibson Nyirenda. (2013). No Title.

Gray, R. H. (1994). Corporate Reporting for Sustainable

Development: Accounting for Sustainability in

2000AD. Environmental Values, 3(1), 17–45.

https://doi.org/10.3197/096327194776679782

GRI. (2013). Pedoman Pelaporan Keberlanjutan G4.

Global Reporting Initiative. Retrieved from

www.globalreporting.org

Hansen, Don R; Mowen, M. M. (2007). Managerial

Accounting. aaajournals.org.

https://doi.org/10.1111/j.1751-908X.2002.tb00883.x

Horváthová, E. (2010). Does environmental performance

affect financial performance? A meta-analysis.

Ecological Economics, 70(1), 52–59.

https://doi.org/10.1016/J.ECOLECON.2010.04.004

Ikhsan, Arfan. 2008, Akuntansi Lingkungan &

Pengungkapannya. Edisi Pertama Yogyakarta : Graha

Ilmu.

Ikhsan, Arfan. 2009. Akuntansi Lingkungan Lingkungan.

Edisi Pertama Yogyakarta : Graha Ilmu.

Jumingan, 2011, Analisis Laporan Keuangan, Jakarta,

Bumi Aksara

Ling, Q. (2007). Competitive strategy, voluntary

environmental disclosure strategy, and voluntary

environmental disclosure quality. ProQuest

Dissertations and Theses.

Mahmes, K. (2016). Corporate Environmental Disclosure

and Economic Performance of Companies in the

Libyan Manufacturing Sector. International Journal of

Economics and Finance Studies, 8(2), 1309–8055.

Retrieved from

http://www.sobiad.org/ejournals/journal_ijef/archieves

/IJEF-2016_2/kemal.pdf

Malarvizhi, P. (2016). Link between Corporate

Environmental Disclosure and Firm Performance –

Perception or Reality. Accounting, Organizations and

Society, 5(3), 1–34.

Moneva, J. M., & Ortas, E. (2010). Corporate

environmental and financial performance: a

multivariate approach. Industrial Management & Data

Systems, 110(2), 193–210.

https://doi.org/10.1108/02635571011020304

Nakao, Y., Amano, A., Matsumura, K., Genba, K., &

Nakano, M. (2007). Relationship between

environmental performance and financial performance:

An empirical analysis of Japanese corporations.

Business Strategy and the Environment.

https://doi.org/10.1002/bse.476

Noodezh, H. R., & Moghimi, S. (2015). Environmental

Costs and Environmental Information Disclosure in the

Accounting Systems. International Journal of

Academic Research in Accounting Finance and

Management Sciences, 5(1), 13–18.

https://doi.org/10.6007/IJARAFMS/v5-i1/1412

Nor, N. M., Bahari, N. A. S., Adnan, N. A., Kamal, S. M.

Q. A. S., & Ali, I. M. (2016). The Effects of

Environmental Disclosure on Financial Performance in

Malaysia. Procedia Economics and Finance,

35(October 2015), 117–126.

https://doi.org/10.1016/S2212-5671(16)00016-2

Oba, Fodio, S. (2012). The Value Relevance of

Environmental Responsibility Information Disclosure

...: EBSCOhost. Acta Universitatis Danubius:

Oeconomica., 8(6), 99–112.

Ong, T. S., Tho, H. S., Goh, H. H., Thai, S. B., & Teh, B.

H. (2016). The relationship between environmental

disclosures and financial performance of public listed

companies in Malaysia. International Business

Management.

https://doi.org/10.3923/ibm.2016.461.467

Patten, D. M. (1992). Intra-industry environmental

disclosures in response to the Alaskan oil spill: A note

on legitimacy theory. Accounting, Organizations and

Society. https://doi.org/10.1016/0361-3682(92)90042-

Q

Porter, M. E., & Linde, C. van der. (1995). Toward a New

Conception of the Environment-Competitiveness

Relationship. Journal of Economic Perspectives, 9(4),

97–118. https://doi.org/10.1257/jep.9.4.97

Suratno, I. B., Darsono, & Mutmainah, S. (2006). Pengaruh

Environmental Performance Terhadap Environmental

Disclosure dan Economic Performance (Studi Empiris

pada Perusahaan Manufaktur yang Terdaftar di Bursa

Efek Jakarta Periode 2001-2004). Simposium Nasional

9 Padang.

Walker, K., & Wan, F. (2012). The Harm of Symbolic

Actions and Green-Washing: Corporate Actions and

Communications on Environmental Performance and

Their Financial Implications. Journal of Business

Ethics, 109(2), 227–242.

https://doi.org/10.1007/s10551-011-1122-4

Wang, M. C. (2016). The relationship between

environmental information disclosure and firm

valuation: the role of corporate governance. Quality

and Quantity, 50(3), 1135–1151.

https://doi.org/10.1007/s11135-015-0194-0

Werner, M., Rusdiana, Purwanto, Jumingan, Juliana, John,

… Fahmi, I. (2013). Analisa Laporan Keuangan.

Jurnal Of Business And Banking.

SEABC 2018 - 4th Sriwijaya Economics, Accounting, and Business Conference

532