Environmental Management Accounting, Quality of Decision

Influence on Environmental Performance in Indonesia

Luk Luk Fuadah, Rochmawati Daud, and Burhanuddin

Universitas Sriwijaya

Keywords: environmental management accounting, quality of decision, environmental performance

Abstract: The aim of this study is to examine the link between environmental management accounting, quality of

decision and environmental performance. The data is obtained from the survey. The natural resource based

view theory and decision theory used in this study. The results research show both environmental

management accounting and quality of decision have a positive and significant effect on environmental

performance. The more companies implementation environmental management accounting, the higher

environmental performance. This is similar to the higher quality of decision, higher environmental

management accounting. The first limitation of this study is a low response rate supports this idea, even

though the company contacted in this study is all ISO 14001 certified companies that have achieved

environmental management system standards. Future research should research qualitative research. Second,

this study only focuses on two variabels impacts on environmental performance. Future research can use

other variables.

1 INTRODUCTION

The company's social and environmental

responsibility has been the focus of attention by the

media and globally in currently, because the

company concerns about environmental hazards,

such as climate change, greenhouse gas emissions

and partly because the company's current

performance is measured in not only financial

performance but also environmental performance

(Stefan Schaltegger, Gibassier, & Zvezdov, 2013).

Thus, stakeholders encourage managers to focus

more on environmental issues and evaluating

environmental performance (Burritt, Schaltegger, &

Burritt, 2010; Rodrigue, Magnan, & Boulianne,

2013).

Environmental Management Accounting is "a

technique for improving, analyzing and using

financial and non-financial information, with the aim

of improving the environment and corporate

environment, economic performance and

contributing to sustainable business" (Schaltegger,

Bennet, Burrit, & Jasch, 2009).

The Government, through the Environment and

Forestry Ministry since 2002, formed a Corporate

Performance Rating Assessment Program in

Environmental Management (PROPER). Initially

PROPER was one of the policy tools developed by

the Environment and Forestry Ministry in order to

encourage compliance with the business and / or

activity responsible for various laws and regulations

in the environmental field. PROPER provides

information about the performance of each company

to all stakeholders on a national scale (mnlh.go.id).

Staniskis & Stasiskiene, (2006) research

environmental management accounting in Lithuania.

The finding reveals there is a positive relationship

between environmental management accounting and

environmental performance. The companies used

environmental management accounting to improve

their decision making including environment and

economics (Staniskis & Stasiskiene, 2006).

Environmental management accounting is useful for

monitoring environmental costs and environmental

performance recordings (Burritt & Saka, 2006).

Furthermore, Henri & Journeault (2010) conclude

that managers depend on indicators of

environmental performance in the evaluation of

performance and decision making.

The implementation of ISO 14001, the standard

used by companies to implement, maintain and

improve their environmental management systems

(Solovida & Latan, 2017).

Fuadah, L., Daud, R. and Burhanuddin, .

Environmental Management Accounting, Quality Decision Influence on Environmental Performance in Indonesia.

DOI: 10.5220/0008440003390346

In Proceedings of the 4th Sriwijaya Economics, Accounting, and Business Conference (SEABC 2018), pages 339-346

ISBN: 978-989-758-387-2

Copyright

c

2019 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

339

Indonesia is a country in Southeast Asia and has

a complex geographical environment; Deforestation

problems are serious according to a 2013 report

from the Indonesian Ministry of Environment and

Forestry. However, research in Southeast Asia and

Indonesia is still rarely carried out that reflects the

empirical gap (Derchi, Burkert, & Oyon, 2015).

This shows that environmental issues in Indonesia

are very important to study.

This research focuses on the link environmental

management accounting, quality of decision and

environmental performance to companies listed in

Indonesia Stock Exchange especially for companies

received ISO 14001 certification.

2 LITERATURE REVIEW

2.1 Natural Resources Based View

Theory

Natural resources based view theory, argues

competitive advantage can be maintained only if the

company has the ability to realize profits that are

supported by resources that are difficult for

competitors to follow (Hart & Dowell, 2011). Hart

& Dowell, (2011) to evaluate the theory of Natural

Resources Based View Theory based on existing

empirical research and conclude that most of Hart,

(1995) propositions are supported. However, there

has been no further exploration of how the

combination of company resources affects

environmental performance.

Natural Resources Based View Theory proposed

by (Hart, 1995; Hart & Dowell, 2011), which

determines that the company's strategy will improve

its environmental performance. Thus, this study uses

the Natural Resources Based View as a theory that

explain the influence of environmental management

accounting on the environmental performance

(Aragón-Correa, Hurtado-Torres, Sharma, & García-

Morales, 2008; Christ & Burritt, 2013).

Natural Resources Based View Theory argues

that competitive advantage can be maintained only if

there is the ability to create profits that are supported

by resources that are not easily duplicated by

competitors. This consists of three interrelated

strategies, namely: (1) pollution prevention; (2)

product stewardship; and (3) sustainable

development. They have different driving force in

the environment, which builds different key

resources, and they have different sources of

competitive advantage. For example, removing

pollutants from the production process can increase

efficiency by (a) reducing the input needed, (b)

simplifying the process, and (c) reducing costs and

compliance obligations Hart & Dowell, 2011)

2.2 Decision Theory

Decision theory is a theory about a decision.

Based on decision theory that highlights the

important role of information in decision making

processes (Hansson, 2005). In particular, with the

use of Environmental Activity Management will

facilitate better environmental assessment and

decision quality because of the provision of more

detailed and accurate environmental information that

is likely to assist the manager's decision-making

process, thereby increasing the quality of

environmental decisions, and in turn, leads to

improved environmental performance. Thus, in this

study propose the link between quality of decision

and environmental performance.

Based on decision theory there are two central

questions, namely the prescriptive and descriptive

approach. First, our prescriptive (rational) approach

asks how rational decisions must be made. Second,

with a descriptive approach (behavior) we model the

actual decisions made by individuals (Hens &

Rieger, 2016). Furthermore, decision theory that

studies choices between alternatives that involve risk

and uncertainty. Risk means here that decisions lead

to consequences that cannot be predicted precisely,

but follow a known probability distribution.

Uncertainty or ambiguity means that this probability

distribution is at least partially unknown to the

decision(Hens & Rieger, 2016).

2.3 Environmental Management

Accounting

Environmental Management accounting has

received considerable attention for academic,

international organization, professional accounting

organizations and business entities. It is reflected in

many scientific journals articles, books and also

working papers (Stefan Schaltegger et al., 2013).

There are several potential benefits associated

with the use of Environmental Management

Accounting. These include reducing costs,

increasing product prices, attracting human

resources, and increasing reputation (Burrit, Rogger,

Hahn, & Schaltegger, 2002). The study also notes

that the implementation of environmental

management accounting usually benefits

organizations by giving them different information

SEABC 2018 - 4th Sriwijaya Economics, Accounting, and Business Conference

340

for decision making (Burrit et al., 2002). Such

information can reveal hidden opportunities, such as

better waste management processes, energy

reduction and consumption of materials or

opportunities for material recycling. From an

environmental perspective, this information can also

be used in developing more efficient processes and

thus leading to innovation.

Burrit, Rogger, Hahn, & Schaltegger, (2002)

reveals that environmental management accounting

is distinguished between ad hoc and routine

information when focusing on past, present or future

time frames and short and long term. Based on this

environmental management accounting information

dimension, Burrit, et.al., (2002) have suggested a

framework of environmental management

accounting. Furthermore, Business entities use

environmental management accounting can improve

environmental and financial performance (Gibson &

Martin, 2004)

Burritt & Saka, (2006) investigate the link

between environmental management accounting and

eco-efficiency measurement in Japan. They

promoted to business entities in Japan to concern to

the environment on their process and consumption

of their products. Moreover, Staniskis & Stasiskiene

(2006) imply SMEs in Lithuanian implement

environmental management accounting and

innovation of Cleaner production. They also report

base on projects of cleaner production and increase

concern from policy makers, industrialists and

practitioners.

There are no regulations on environmental

disclosure in Spain, but this study reveals that the

elaboration of a large number of environmental

accounting information used by internal parties is

useful for decisions on the implementation of

environmental management systems (Masanet-

Llodra, 2006). The use of environmental

management accounting can improve the companies

performance, one of that is environmental

performance (Tsui, Christophor, Lee, & Kee, 2014).

It is also better to manage the cost of environment

and improve process of production (Tsui et al.,

2014).

Solovida & Latan (2017) the use of

environmental management accounting as an

intangible asset has benefited companies by

providing information on their operational activities,

especially as related to the environment and the

results of good environmental performance. Qian et

al., (2018) reveals that the implementation of

environmental management accounting has a

significant positive impact on the company's carbon

management and the quality of its disclosure.

2.4 Environmental Performance

The Government, through the Environment and

Forestry Ministry since 2002, formed a Corporate

Performance Rating Assessment Program in

Environmental Management (PROPER). The

Company Performance Rating Program (PROPER)

is a program used by the Indonesian Environment

and Forestry Ministry together with the Environment

Agency to monitor and assess the company's

environmental performance. Initially PROPER was

one of the policy tools developed by the Ministry of

Environment and Forestry in order to encourage

compliance with the business and / or activity

responsible for various laws and regulations in the

environmental field. PROPER is closely related to

the dissemination of information on the performance

of each company to all stakeholders on a national

scale (mnlh.go.id).

Solovida & Latan (2017) explained that

PROPER (Program of the corporate performance

rating) members are assessed on a 5 (five) color

scale ranging from the highest, gold, down to green,

blue, red, and black. Gold and green rating gave to

companies that go beyond mere compliance and

include three criteria: (1) implementing an

environmental management system, one of that is

the certificate of ISO 14001, (2) using resources, and

(3) carrying out community development.

2.5 Hypothesis Development

2.5.1 Environmental management

accounting (EMA) and environmental

performance (EP)

Environmental management accounting is one of

the tools of environmental management that is useful

for tracking environmental costs as well as physical

environmental flows (Burritt & Saka, 2006). Based

Natural Resources Based View Theory argue that

there is the combination of company resources

affects environmental performance (Hart, 1995).

One of the company resources is environmental

management accounting. In this study proposed that

environmental management accounting has relation

with environmental performance. The higher

environmental management accounting implement

in the company, the higher environmental

performance.

Environmental Management Accounting, Quality Decision Influence on Environmental Performance in Indonesia

341

Previous studies include Aragón-Correa,

Hurtado-Torres, Sharma, & García-Morales (2008),

and Henri & Journeault (2010) showed that eco-

efficient practices are positively related to company

performance. Henri & Journeault (2010) use 303

respondents for their analysis. Empirical evidence

shows that the use of environmental management

accounting has a positive and significant on

company's environmental performance (Solovida &

Latan, 2017). Solovida & Latan (2017) analyzed

from 68 respondents from the survey conducted.

The more sophisticated the use of management

accounting practices, namely environmental

management accounting, the better the process of

control and decision making influences the

environmental management control system on

environmental performance (Solovida & Latan,

2017).

Furthermore, other study revealed that there is a

positive and significant influence between

organizational resources, the use of environmental

management accounting, and the company's

environmental performance (Latan, Chiappetta

Jabbour, Lopes de Sousa Jabbour, Wamba, &

Shahbaz, 2018). Latan, Chiappetta Jabbour, Lopes

de Sousa Jabbour, Wamba, & Shahbaz (2018)

analyzed 107 respondents using an online survey.

Based on the argument above, the hypothesis

proposed is in the following:

H1: Environmental Management Accounting

have a positive impact on Environmental

Performance.

2.5.2 Quality of decision (QD) and

Environmental performance

Quality of decisions are decisions taken

accurately and in detail specifically related to the

environment in this study. Decision theory is a

theory about a decision. Based on decision theory

that highlights the important role of information in

decision making processes (Hansson, 2005). Thus,

better environmental assessment and decision

quality due to the provision of more detailed and

accurate environmental information that is likely to

assist the manager's decision-making process,

thereby increasing the quality of environmental

decisions, and in turn leads to improved

environmental performance. The higher quality of

decision, the higher environmental performance.

Phan, Baird, & Su (2018) reveal that the

management of environmental activities towards the

quality of decisions and environmental performance

of the company. The study was conducted in

Australia to test the management of environmental

activities related to Activity Based Costing. The

more sophisticated the use of management

accounting practices (in this case environmental

management accounting), the better the process of

control and decision making and the more solid the

impact of environmental management control

system on the company's environmental

performance. Phan, Baird, & Su (2018) research

environmental activity based costing and

environmental performance through the quality of

decision.

It is expected that the quality of their

environmental decisions will be improved, which in

turn will have a positive impact on environmental

management in terms of improving environmental

performance. One of the main difficulties in

environmental management is the identification and

calculation of the costs of organizational activities

and processes (Sarkis, Meade, & Presley, 2006). The

higher quality of decision, the higher environmental

performance as well. Thus, our hypothesis is

proposed in the following:

H2: Quality of decision have a positive effect on

environmental performance.

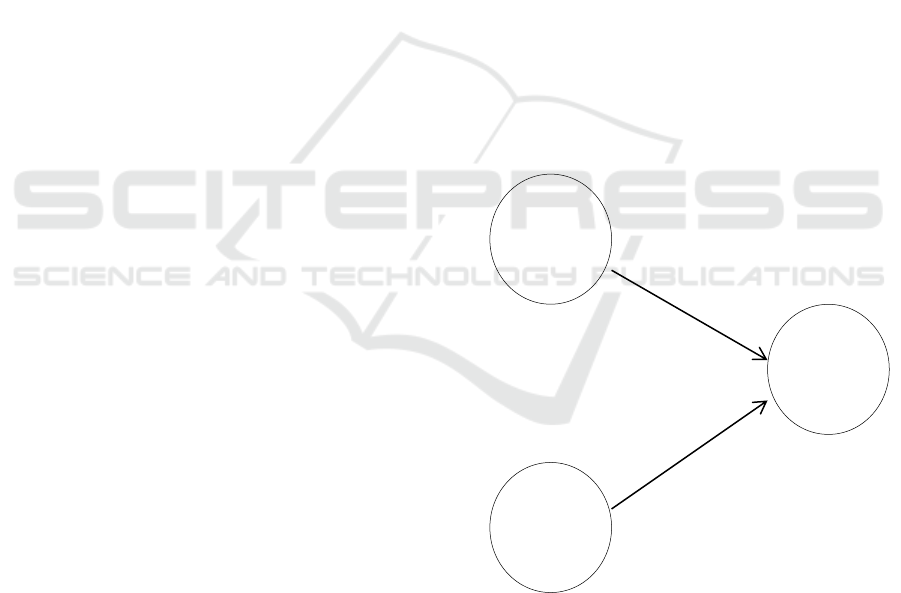

Figure 1: Research Framework

Environmental

Management

Accounting

Quality

of

Decision

Environmental

Performance

H1

H2

SEABC 2018 - 4th Sriwijaya Economics, Accounting, and Business Conference

342

3 METHOD

3.1 Sample

The sample in the study are all companies that

have ISO 14001 certification. This is because the

company is more concerned than other companies

about environmental issues and tends to have a

strong commitment to environmental responsibility.

The sample in this study as respondents were

general managers, operations managers, financial

managers and environmental managers in the sample

company.

3.2 Instruments

3.2.1 Environmental management

accounting

This study uses environmental management

accounting instruments are 12 items of

environmental management accounting (Ferreira,

Moulang, & Hendro, 2010). This study uses seven

Likert point scales which indicate 1 "do not do it at

all" up to 7 "has been done".

3.2.2 Decision Quality

The measure for decision quality is a five-item

instrument derived from (McIntyre, 1982). This

study uses seven Likert point scales which indicate

that from 1 "not at all applied" to 7 "very applied".

3.2.3 Environmental Performance

This study uses 13 environmental performance

instruments of the company (Henri & Journeault,

2010). This study uses seven Likert point scales

which indicate 1 "do not at all" up to 7 "to great

extent".

3.3 Data Collected Technique

The collection technique is by collecting by the

survey. Before the survey was conducted, a pilot

test has been carried out. Data obtained from an

online survey to companies received ISO 14001

certificate listed Indonesian Stock Exchange. The

total company received ISO 14001 around 200

companies. The data use in this study is 56

respondents from the result of the survey.

3.4 Analysis

The hypotheses developed were examined by

using Partial Least Square (PLS).

The model of this study is:

EPi,t = α + β1 EMAi,t, + β2 QDi,t + t

(1)

Where:

i, t = sector i, Year t,

= intercept

Β = independent variable coefficient

= error term

EMA = Environmental Management Accounting

QD = Quality of decision

EP = Environmental performance

4 RESULT AND DISCUSSION

4.1 Result

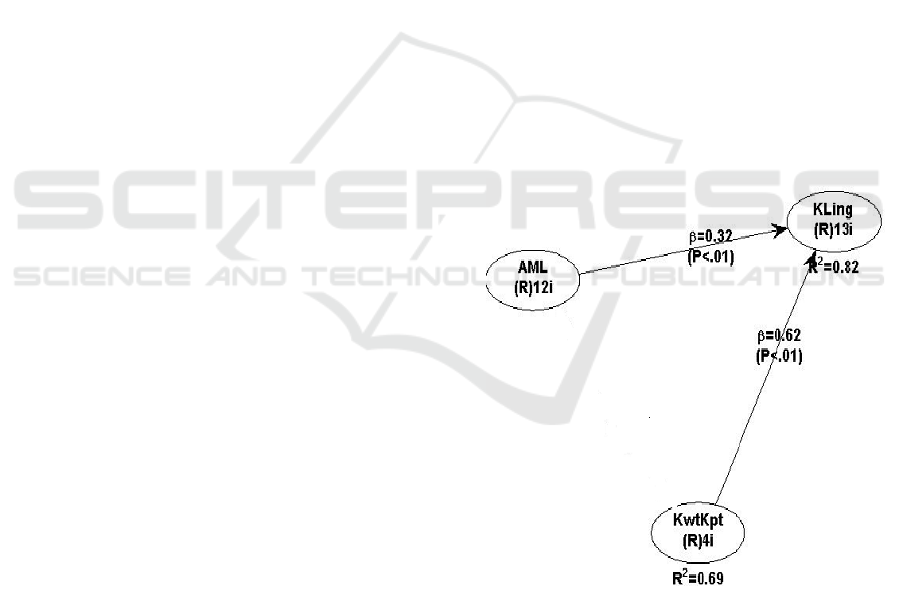

Figure 1: The result of research

Environmental Management Accounting, Quality Decision Influence on Environmental Performance in Indonesia

343

Table 1: The hypothesis Result

Hypothesis

Coefficient

p Value

Result

H1

0,32

< 0.01

Supported

H2

0,62

< 0.01

Supported

It can be seen in figure 1 and table II. Based on

the results the explanation in the following:

1. The first hypothesis, the link between

environmental management accounting and

environmental performance. It shows that p= <

0.01. It means that the first hypothesis is

accepted at the level below 1 %. The

coefficient 0,32. It shows a positive

relationship.

2. The second hypothesis states quality of

decision has a positive effect on environmental

performance. It is also suported. Because p= <

0.01, it is less than 1%. The coefficient (β =

0,62). It means the quality of decision has a

positive link with environmental performance

4.2 Discussion

The first hypothesis (H1) which states

environmental management accounting have a

positive effect on environmental performance.

Result research shows H1 is accepted. The results of

this analysis indicate that the company's

environmental performance is influenced by

environmental management accounting. The more

often environmental management accounting is used

in a company, the higher the environmental

performance of the company. This finding is in line

with previous studies by (Aragón-Correa, Hurtado-

Torres, Sharma, & García-Morales, 2008). The

finding support Natural resource base view theory.

This finding in line to Solovida & Latan (2017);

Latan, Jabbour, Lopes de Sousa Jabbour, Wamba, &

Shahbaz, (2018).

The argument for the acceptance of the first

hypothesis is as follows; the implementation of

environmental management accounting has

encouraged companies to improve their

environmental performance. The finding supports

the Natural Resources Based View Theory, that

explain the influence of environmental management

accounting on the environmental performance

(Aragón-Correa, Hurtado-Torres, Sharma, & García-

Morales, 2008; Christ & Burritt, 2013).

The second hypothesis (H2) which states

Decision Quality has a positive effect on

Environmental performance. The result of the

research shows H2 is accepted. The findings

indicate that the quality of decisions has an impact

on environmental performance. In particular,

information on environmental costs is very

important in assisting internal decision makers in

various production decisions and resource allocation

(Deegan, 2008). Therefore, it is very important for

organizations to assess correctly environmental costs

to provide better product cost estimates with

increasing costs Environmental protection must be

passed on to customers through an accurate pricing

policy. This finding support (Phan et al., 2018).

The argument for the acceptance of the second

hypothesis is as follows; the quality of decision

improves their environmental performance. This

study supports the decision Theory.

5 CONCLUSION

Both environmental management accounting and

decision quality have a positive impact on

environmental performance. The more companies

implementation environmental management

accounting, the higher environmental performance.

The higher the quality of decision, the higher

environmental management accounting.

One of the roles of environmental management

accounting on business in a company is to disclose

both financial information and non-financial

information. In addition, it is to improve information

about the environment and the corporate

environment, the economic performance of the

company. This environmental management

accounting also contributes to sustainable business.

However, the quality of decision is a decision taken

by a company that has the quality where in decision

making requires information not only financial

information but also non-financial information

especially information related to the environment in

company.

This study support two theory that used includes

Natural Resources Based View Theory and decision

theory. This research also has important implications

for the management of the company with regard to

environmental management accounting and the

quality of decisions that can improve environmental

SEABC 2018 - 4th Sriwijaya Economics, Accounting, and Business Conference

344

performance. The actions that can be taken by

companies is managing waste and improving all

activities that are environmentally friendly which

can contribute to environmental performance.

There are several limitations in this study that

must be considered. First, this study uses a relatively

small sample: many companies are reluctant to

provide it information related to environmental

performance, because most companies treat this

information as "confidential." Information relating to

the strategy, use of environmental management

accounting and environmental performance are thus

not known to the public. A low response rate

supports this idea, even though the company

contacted in this study is all ISO 14001 certified

companies that have achieved environmental

management system standards. Second, this study

only focuses two variables impacts on

environmental performance. Future research can use

other variables.

Acknowledgment

Author thank to Universitas Sriwijaya, we can

get Competitive Research grant (Penelitian

Unggulan Kompetitif Universitas Sriwijaya) in

2018.

REFERENCES

Aragón-Correa, J. A., Hurtado-Torres, N., Sharma, S., &

García-Morales, V. J. (2008). Environmental strategy

and performance in small firms: A resource-based

perspective. Journal of Environmental Management,

86(1), 88–103.

https://doi.org/10.1016/j.jenvman.2006.11.022

Burrit, Rogger, L., Hahn, T., & Schaltegger, S. (2002).

Towards a comprehensive framework for

environmental management accounting - Links

between business actors and environmental

management accounting tool. Australian Accounting

Review, 12(2), 39–50. https://doi.org/10.1111/j.1835-

2561.2002.tb00202.x

Burritt, R. L., & Saka, C. (2006). Environmental

management accounting applications and eco-

efficiency: case studies from Japan. Journal of

Cleaner Production, 14(14), 1262–1275.

https://doi.org/10.1016/j.jclepro.2005.08.012

Burritt, R. L., Schaltegger, S., & Burritt, R. L. (2010).

Sustainability accounting and reporting : fad or trend ?

https://doi.org/10.1108/09513571011080144

Christ, K. L., & Burritt, R. L. (2013). Environmental

management accounting: The significance of

contingent variables for adoption. Journal of Cleaner

Production, 41, 163–173.

https://doi.org/10.1016/j.jclepro.2012.10.007

Deegan, C. (2008). Environmental costing in capital

investment decisions: Electricity distributors and the

choice of power poles. Australian Accounting Review,

18(1), 2–15. https://doi.org/10.1111/j.1835-

2561.2008.0002.x

Derchi, G. B., Burkert, M., & Oyon, D. (2015).

Environmental management accounting systems: A

review of the evidence and propositions for future

research. Studies in Managerial and Financial

Accounting (Vol. 26). Emerald Group Publishing

Limited. https://doi.org/10.1108/S1479-

3512(2013)0000026006

Ferreira, A., Moulang, C., & Hendro, B. (2010).

Environmental management accounting and

innovation: an exploratory analysis. Accounting,

Auditing & Accountability Journal, 23(7), 920–948.

https://doi.org/10.1108/09513571011080180

Gibson, K. C., & Martin, B. A. (2004). Demonstrating

value through the use of environmental management

accounting. Environmental Quality Management,

13(3), 45–52. https://doi.org/10.1002/tqem.20003

Hansson, S. O. (2005). Decision Theory A brief

introduction. Sweden: Upsala University. Swedia:

Upsala University.

https://doi.org/10.4324/9780203112991

Hart, S. (1995). A Natural-Resource-Based View of the

Firm. Academy of Management Review, 20(4), 986–

1014. https://doi.org/10.5465/AMR.1995.9512280033

Hart, S. L., & Dowell, G. (2011). A natural-resource-

based view of the firm: Fifteen years after. Journal of

Management, 37(5), 1464–1479.

https://doi.org/10.1177/0149206310390219

Henri, J. F., & Journeault, M. (2010). Eco-control: The

influence of management control systems on

environmental and economic performance.

Accounting, Organizations and Society, 35(1), 63–80.

https://doi.org/10.1016/j.aos.2009.02.001

Hens, T., & Rieger, M. O. (2016). Decision Theory. In

Financial Economics (pp. 15–88). London, UK:

Springer Text Book in Business and Economics.

https://doi.org/10.4324/9780203932025

Latan, H., Chiappetta Jabbour, C. J., Lopes de Sousa

Jabbour, A. B., Wamba, S. F., & Shahbaz, M. (2018).

Effects of environmental strategy, environmental

uncertainty and top management’s commitment on

corporate environmental performance: The role of

environmental management accounting. Journal of

Cleaner Production, 180, 297–306.

https://doi.org/10.1016/j.jclepro.2018.01.106

Masanet-Llodra, M. J. (2006). Environmental

management accounting: A case study research on

innovative strategy. Journal of Business Ethics, 68(4),

393–408. https://doi.org/10.1007/s10551-006-9029-1

McIntyre, S. H. (1982). An Experimental Study of the

Impact of Judgment-Based Marketing Models.

Management Science, 28(1), 17–33.

https://doi.org/10.1287/mnsc.28.1.17

Phan, T. N., Baird, K., & Su, S. (2018). Environmental

activity management: its use and impact on

environmental performance. Accounting, Auditing and

Environmental Management Accounting, Quality Decision Influence on Environmental Performance in Indonesia

345

Accountability Journal, 31(2), 651–673.

https://doi.org/10.1108/AAAJ-08-2016-2686

Qian, W., Hörisch, J., & Schaltegger, S. (2018).

Environmental management accounting and its effects

on carbon management and disclosure quality. Journal

of Cleaner Production, 174, 1608–1619.

https://doi.org/10.1016/j.jclepro.2017.11.092

Rodrigue, M., Magnan, M., & Boulianne, E. (2013).

Stakeholders’ influence on environmental strategy and

performance indicators: A managerial perspective.

Management Accounting Research, 24(4), 301–316.

https://doi.org/10.1016/j.mar.2013.06.004

Sarkis, J., Meade, L., & Presley, A. (2006). An activity

based management methodology for evaluating

business processes for environmental sustainability.

Business Process Management Journal, 12(6), 751–

769. https://doi.org/10.1108/14637150610710918

Schaltegger, S., Bennet, M., Burrit, R. L., & Jasch, C.

(2009). Eco-Efficiency in Industry and Science

Environmental Management Accounting for Cleaner

Production. Vienna: Springer.

Schaltegger, S., Gibassier, D., & Zvezdov, D. (2013). Is

environmental management accounting a discipline? A

bibliometric literature review. Meditari Accountancy

Research, 21(1), 4–31.

https://doi.org/10.1108/MEDAR-12-2012-0039

Solovida, G. T., & Latan, H. (2017). Linking

environmental strategy to environmental performance

Mediation role of environmental. Sustainability

Accounting, Management and Policy Journal, 8(5),

595–619. https://doi.org/10.1108/SAMPJ-08-2016-

0046

Staniskis, J. K., & Stasiskiene, Z. (2006). Environmental

management accounting in Lithuania : exploratory

study of current practices , opportunities and strategic

intents. Journal of Cleaner Production, 14, 1252–

1261. https://doi.org/10.1016/j.jclepro.2005.08.009

Tsui, C. S. K., Christophor, Lee, S. K. T., & Kee, S.

(2014). A Literature Review on Environmental

Management Accounting (EMA) Adoption. Web

Journal of Chinese Management Review, Vol. 17(3),

No. 3.

Tsui, (2014), A literature review on Environmental

Management Accounting, (EMA) adoption, Chinese

Management Review, Vol. 17, No. 3, 1- 19.

www.mnlh.go.id

SEABC 2018 - 4th Sriwijaya Economics, Accounting, and Business Conference

346