Potential Implementation of Goods and Services Tax as a Substitute

for Value Added Tax in Indonesia

Naufalia Dinar Primacita

1

and Khoirunurrofik

2

1

Ministry of Finance, DG Custom, Indonesia

2

Institute for Economic and Social Research (LPEM), Faculty of Economics and Business, Universitas Indonesia,

Keywords: Goods and services tax, gross regional domestic product, surcharge, value added tax.

Abstract: This research aims to analyze the feasibility of implementing a goods and services tax as a substitute for

value added tax in Indonesia during the period 2005 to 2015. It also estimates the potential revenues made at

both central and local government levels. This study uses a panel data method prepared through descriptive

and econometric analysis. The unit of analysis is between provinces in Indonesia, with the findings

correlated to Stiglitz’s theory. The findings show that goods and services tax (GST) has the potential to be

feasibly applied in Indonesia as an alternative to value added tax (VAT), and that it would provide a greater

potential tax revenue than VAT. Consequently, if GST were to be implemented at a regional level,

interprovincial equity could be achieved by empowering fiscal equity through a local surcharge tax system.

1 INTRODUCTION

Fiscal strains are occurring in Indonesia and the

efficiency and effectiveness of revenues from

various taxes implemented are not optimal. The Data

from Central Bureau of Statistics (Badan Pusat

Statistik or BPS) in 201) confirms that the country’s

tax ratio to gross domestic product (GDP) is still

relatively low in comparison with countries of both

the ASEAN bloc and worldwide, at around 11% to

13% (Worldbank). Figure 1 shows the fluctuation in

the tax ratio in Indonesia over the period 2010 to

2016, and this is a condition that affects the

government’s funding sources for carrying out

development and achieving welfare objectives for

the population. In relation to expansion of the tax

base, fiscal policy has an important role to play in

the government’s plans for sustainability of the

economy, and high tax revenues will provide more

sources of funding for the country’s development.

During the five years to 2016, value added tax

(VAT) was the second-highest contributor to tax

revenue after income tax, with an increasing trend

every year. However, while its contribution was

constantly increasing it did not have a significant

impact on improving the ratio of tax to GDP. Thus,

as an indirect tax, VAT is not seen to be impacting

state tax revenues effectively. In addition, the VAT

elasticity value of 0.82 (Nurhidayati, 2013) indicates

that VAT is not very elastic with reference to the tax

base. Accordingly, the government should review its

existing policies both in terms of intensification and

intensification.

Taxation of the service sector (“taxable

services”) as well as taxable goods should be

explored as a potential tax revenue source. As a

developing country, Indonesia faces structural

transformation that causes a transition of production

activity from the primary sector to the secondary

sector. Agrarian countries such as Indonesia focus

on agricultural production in terms of products such

as raw materials or processed ingredients consumed

in the community. However, with the impact of

global competition the agricultural sector has

declined in recent years while the manufacturing and

services sectors have grown. This may lead to

technological improvements and shifting consumer

preferences which will bring about structural

transformation in Indonesia and transfer attention to

the service sector.

102

Dinar Primacita, N. and Khoirunurrofik, .

Potential Implementation of Goods and Services Tax as a Substitute of Value Added Tax in Indonesia.

DOI: 10.5220/0008437301020111

In Proceedings of the 4th Sriwijaya Economics, Accounting, and Business Conference (SEABC 2018), pages 102-111

ISBN: 978-989-758-387-2

Copyright

c

2019 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

Figure 1. Realization of domestic tax revenue in Indonesia 2010–2016

Source: BPS, 2017

To tackle this issue, the Indonesian government

has begun to review the possibility of changing VAT

into a goods and services tax (GST). This tax reform

is being analyzed by the Ministry of Finance as a

revision aspect of VAT Act No.42 of 2009. This

policy aims to expand the tax base and increase the

ratio of tax revenue to GDP (the “tax ratio”). Even

though GST is more widely implemented in

developed countries, Indonesia as a developing

country could also apply this type of tax. In previous

studies, discussions have related to tax revenues at a

national level; the question therefore arises of

whether tax revenue at the regional level, such as

provinces and cities, can also be similarly analyzed

and changed. However, since GST is focused at the

central level, it will not have a significant impact on

the equitable distribution of income between

provinces.

When looked at from the administration aspect,

the collection system for GST is more convenient

than VAT because the administration of VAT

revenues and VAT expenditures creates high

accounting costs. In addition, the potential

occurrence of “overpayments” and “underpayment”

create inefficiency in VAT administration. One of

the steps toward developing efficiency in fiscal

policy by optimizing tax revenue at both central and

provincial level is the use of an surcharge tax

(opsen) approach. This can provide potential

taxation opportunities that can be used by both

central and local governments to increase gross

regional domestic product (GRDP). Indeed, it could

lead to improvement in the income distribution

between each local government on an aggregate

basis. Therefore, the objective of this study is to

analyze the feasibility of implementing GST as a

substitute for VAT in Indonesia, and to estimate the

potential revenues of GST application for central

government, and for local governments if a

surcharge system is applied.

2 LITERATURE REVIEW

GST has been widely implemented in developed

countries with a range of objectives. There are at

least five countries––Australia, Canada, India,

Malaysia and Singapore––presently changing their

taxation systems toward GST, and these are the main

reference countries for this study.

2.1 Goods and services tax (GST)

By definition, GST is one of the indirect tax types

which is levied on individuals who engage in

consumption activities at each business level.

Consequently, there is no need to wait for goods or

services to acquire added value before they can be

taxed. Based on World Bank information, the tax

percentage levied as GST is lower than for VAT,

with the standard GST level charged being 6%.

Moreover, taxable goods which are taken directly

from their sources are also able to be taxed, such as

in the mining and extraction sectors. There are,

however, tax exemptions for primary goods, such as

11.30

12.3

11.90

11.9

11.40

10.7

12.20

10

10

11

11

12

12

13

0

200

400

600

800

1 000

2010 2011 2012 2013 2014 2015 2016

persen

Trillion Rupiah

PPh PBB+PBHTB

PPN+PPnBM Cukai

Pajak Perdagangan Internasional Pajak Lainnya

Rasio Pajak

Potential Implementation of Goods and Services Tax as a Substitute of Value Added Tax in Indonesia

103

for micro, small, and medium (UMKM) units, and

for agricultural products, health goods, education

sectors, and housing for those with low income. This

aims to provide incentives where needed and to

protect primary sectors to avoid shocks to the

economy.

2.2 Stiglitz’s theory

Stiglitz’s theory (2000) states that a good tax policy

achieves at least five principles of taxation:

efficiency, administrative simplicity, flexibility,

political responsibility, and fairness. In this study,

these five principles will be used as evaluation

indicators in analyzing the feasibility of potential

GST revenues compared to potential VAT revenues.

Efficiency is defined as a tax system that has the

potential to improve economic efficiency. Efficiency

in the tax system refers to the allocation of economic

resources to achieve optimal tax revenue, the

minimization of deadweight loss that occurs in tax

revenue, and a ratio between tax revenue and the

cost of tax officers’ salaries of greater than 1.

The second principle is administrative simplicity.

Along with the delivery of simple administrative

costs and cheap compliance costs, this is also one of

the principles which makes it easier for the taxpayer

to perform their obligations.

The tax system must also be flexible, enabling it

to respond to changes in the state of the economy by

being easily adapted to meet changes in economic

conditions.

Another principle is the responsibility of

stakeholders, in this case the government (political

responsibility). A high level of political

responsibility will demonstrate transparency

between the government and the taxpayer. The

applied tax base and the amount of tax rate to be

paid should also be clearly known, so that taxpayers

can be sure of the exact amount of tax to be levied

and can evaluate how accurately the system has been

applied.

The last principle is fairness. The tax system

should embrace principles that treat individuals

fairly. Equity is divided into aspects: horizontal

equity and vertical equity. Horizontal equity occurs

in a tax imposed on individuals with the same

economic circumstances, so that people are treated

the same and are subject to the same percentage of

tax burden. In contrast, vertical equity is the

imposition of taxes with different percentages of tax

burden in accordance with the ability to pay of

individuals; thus, it can create equality among

taxpayers.

Another important element to take into account

in analyzing tax effectiveness is the nature of the

changes that occur in tax revenue. Rosen and Gayer

(2010) state that the tax burden of a taxing unit is

affected by the elasticity of demand and supply of

the taxed goods and services. This can be used to

estimate the productivity of tax revenues. In

considering these elements, the principles of Stiglitz

will be used as benchmarks of the potential

feasibility of the implementation of GST as the

transition taxation for VAT. The results will be

explained through a descriptive analysis method.

Study of GST has been carried out by previous

researchers, some of whom have analyzed the

causation and descriptive nature of tax reform

through the implementation of GST tax policies. A

study by Jenkins and Khadka (1998) investigated

how Singapore modified its taxation system to meet

changes in the country’s economy. The findings of

this study are that by using GST Singapore managed

to grow its export competitiveness and minimize the

transitional and compliance costs that arose from the

shift from the previous tax regime to the new one.

GST was implemented in Singapore as a transition

from a tax policy that previously embraced sales tax

to one based on GST. In spite of having the same

objectives, the implementation of these two tax

types is different. Taking advantage of its strategic

business location as the largest cargo-handling port

in Asia, Singapore decided to transition its taxation

policy from sales taxes to GST, and has been able to

maintain its collection of tax during this transition.

Likewise to Singapore, India is the first developing

country to introduce GST which can be said to be

successful in its application. In his study, Ramesh

(2015) examines the challenges and opportunities of

the implementation of dual GST, namely central

GST and state GST. By applying a GST tax rate of

2% gradually increasing to 12% as a first step of

implementing GST, India has been able to

implement this consumption tax policy. The findings

of Ramesh’s (2015) study reveal the minimization of

cascading effect, the renewal of tax revenues, and

increasing economic growth by creating integration

between regions through a uniform tax rate.

A study by Valadkhani (2005) examined the

impact of GST in Australia on the prices of goods

and services including on the consumer price index

(CPI) basket. It found that there were no significant

changes in the CPI basket. The reason Australia

began to implement a GST policy was to increase

the competitiveness of its country’s exports, given

that, as a country producing enough raw materials,

the Australian government wanted to optimize its

SEABC 2018 - 4th Sriwijaya Economics, Accounting, and Business Conference

104

sectors. The result of the transition proves that

Australia was able to keep its inflation level steady

as seen from CPI from before to after GST was

applied. There was also a study by Grady (1990)

into the effects of GST implementation on the

distribution of income in Canada. Equal distribution

of income can help those with low to middle

income. Meanwhile, Palil and Ibrahim (2011)

investigated the impact on those with lower middle

income in Malaysia of the implementation of GST,

using the analysis of variance (ANOVA) method.

The results of these findings indicate that exemption

taxes were used. A rise in tax credit is used as an

incentive for the implementation of the introduction

of GST. Furthermore, Mansor and Ilias (2013)

provided an argument for the benefit of GST

application for Malaysian’s people in strengthening

the economy and improving the public’s quality of

life.

The practical base for applying GST in these

countries is to impose tax burdens on taxpayers at

every level of economic activity with a lower tax

rate than the rate for VAT. The strategies undertaken

by the five countries in the literature referenced

above are relatively similar, such as controlling CPI

to avoid inflation, especially during the introduction

of GST. In addition, to avoid double taxation, the tax

base should be clearly established so as not to cause

cascading effects across output tax and income tax,

which would lead to high accounting costs. As a

result, inefficiency would occur in terms of

admissibility. Furthermore, increasing the GST rate

gradually and decreasing corporate income tax can

be used as an incentive for business actors in the

introductory period. Finally, tax exemptions in

certain sectors, such as education, health,

agricultural products, and non-profit local

transportation, can be included. The studies

referenced above can strengthen the authors’

arguments regarding the implementation of GST as

seen from the acceptance and accuracy of the

applied taxation principles.

3 RESEARCH METHODOLOGY

This paper applies two approaches to the research

questions. First, we carry out descriptive analysis to

examine the feasibility of GST application. For the

comparison of GST and VAT described, this

research conducts a calculation model that describes

the tax base of the tax-type model-building process.

Descriptive analysis is conducted to answer the first

research question, that is, an examination of the

feasibility of applying GST in Indonesia. In this

case, GST acceptance at the central level is the same

as for the existing VAT. Second, we will perform

econometric estimation of the potential tax revenue

from GST in Indonesia as determined by several tax

basis variables, as follows:

3.1 Equity ratio

The level of the equity ratio can be seen by

calculating the ratio of tax receipts to acceptance

nationally. In this case, the authors compare the

potential ratios of VAT and the estimated potential

of GST acceptance for domestic revenue and GDP:

A =

𝑽𝑨𝑻

𝐃𝐨𝐦𝐞𝐬𝐭𝐢𝐜 𝐑𝐞𝐯𝐞𝐧𝐮𝐞

; B =

𝑽𝑨𝑻

𝐆𝐃𝐏

(1)

and

𝐂 =

𝑮𝑺𝑻

𝑫𝒐𝒎𝒆𝒔𝒕𝒊𝒄 𝑹𝒆𝒗𝒆𝒏𝒖𝒆

; 𝐃 =

𝑮𝑺𝑻

𝑮𝑫𝑷

𝐚𝐥𝐬𝐨

𝐄 =

𝑮𝑺𝑻

𝑽𝑨𝑻

The greater the value of A, B, C, D, and E the

greater the equity. In contrast, the smaller the value

of the ratio, the lower the spread equity. To evaluate

the feasibility of GST implementation, the authors

focus on the value of the E ratio, which identifies the

ratio of potential GST revenues to potential VAT

revenues. If the value is greater than 1, GST is

feasible for implementation in Indonesia, and vice

versa.

3.2 Potential GST calculation

Estimated potential GST receipts are based on total

consumption expenditures, composed of both

household and private sectors, multiplied by a GST

rate of 6%. This approach is one of three GST

acceptance theories used in India and adapted from

previous research (Rao & Chakraborty, 2013). The

scale of the analysis used in this case is national and

annual, and the estimation equation is therefore as

follows:

𝑮𝑺𝑻

𝒕

= 𝚺

(

𝒄𝒐𝒏𝒔𝒑𝒆𝒓𝒌𝒂𝒑𝒊𝒕𝒂

𝒊𝒕

∗ 𝒑𝒐𝒑𝒖𝒍𝒂𝒕𝒊𝒐𝒏

𝒊𝒕

∗ 𝟏𝟐 ∗

𝟔%

)

+ (𝒄𝒐𝒏𝒔

𝒑𝒓𝒊𝒗𝒂𝒕𝒆

𝒊𝒕

∗ 𝒏𝒖𝒎𝒃𝒆𝒓 𝒐𝒇

𝒑𝒓𝒊𝒗𝒂𝒕𝒆

𝒊𝒕

∗ 𝟔%)

(2)

Equation 2 indicates that GST would be affected by

total consumption activities in both the individual

Potential Implementation of Goods and Services Tax as a Substitute of Value Added Tax in Indonesia

105

household and private sectors, multiplied by a GST

standard rate of 6% per year.

3.3 VAT potential calculation

The GST value used in the estimation is the potential

value. So that like-for-like comparability can be

achieved, the VAT calculation also uses the

potential rather than the actual value. The potential

for VAT revenues is based on the value of GDP by

expenditure for household and private consumption

at a tax rate of 10%, because by definition VAT and

GDP are similarly based on value added.

𝑷𝑷𝑵

𝒑

=

𝟏𝟎

𝟏𝟎𝟎

∗

𝚺(𝑪

𝒉𝒐𝒖𝒔𝒆𝒉𝒐𝒍𝒅

+𝑪

𝒑𝒓𝒊𝒗𝒂𝒕𝒆

)

𝒕

(3)

Equation 3 indicates the potential VAT value from

the sum of value added of goods and services

multiplied by the VAT rate implemented.

3.4 Empirical estimation

Six variables are used in the model, representing

aspects expected to have an effect on potential tax

revenue from GST. The first variable (a targeted

variable in this study) is GRDP. The amount of

regional revenue can be estimated from the value of

GRDP and domestic income as a basis for tax

collection. Since, the characteristics of provinces in

Indonesia are different and making the potential for

regional income also different, so this GRDP

variable is used to identify the potential for regional

revenues, including the potential for GST revenue.

To analyze price changes in goods and services,

as well as to identify the difference in inflation

before and after GST implementation (transitional

condition), the value of the consumer price index is

symbolized by CPI and quadratic CPI (SQCPI). This

variable is used as an adaptation of the method used

in the study by Valadkhani (2005), which analyzed

CPI basket changes resulting from the transition to

GST in Australia.

Consumption by the government as well as

household and private consumption are taxed. This

variable is used as a control variable in the model to

identify potential tax revenue that can be levied from

the consumption activity of economic actors in a

country. Not only is government spending

referenced in terms of its effect on GST, as

symbolized by GOVEXP, but also the total

population of a region. A large population living in

an area is expected to affect the potential for tax

revenues from GST by assuming that each

individual has a consumptive nature, so that buying

and selling transactions may increase. Because of

this, a population variable is used to identify this

factor. This variable was adapted from the study by

Grady (2009) on the impact of GST distribution in

Canada as seen from demographic factors including

population size.

In addition, the level of individual education is

also thought to have an effect on tax revenues. In

line with this view, Ibrahim (2013) used educational

variables as a control in his research into GST

practice in Malaysia. Thus, in this present research,

educational-level variables are adapted to analyze

the effect of education levels on individuals’

consumption patterns. In this study, the education of

individuals to a minimum of senior high school level

is symbolized by senior high school (SHS). As a

justification of this choice of variable, individuals

who have high school education in Indonesia tend to

have job opportunities which are better in terms of

income.

The final control variable is the trade sector of

the sectoral GDP of each province. Trading activity

has relevance for consumption activity, so this

variable is considered to be linked closely to the

potential for GST implementation.

In this research, the economic model used is

ordinary least square (OLS) regression estimation

with a panel data method. The analytical unit used is

the provincial level, to enable the analysis of the

magnitude of potential tax revenues in terms of the

GRDP of the various provinces. The reason this

model was chosen rather than other models is that it

can reduce the occurrence of different specific

province errors in each region for constant variables

over time, such as cultural and geographic factors.

This method is therefore able to describe variable

changes over time by minimizing error in estimating

the impact of independent variables on dependent

variables. In addition, the movement of continuous

variables can more easily be illustrated by using the

data panel method compared with, for instance, the

maximum likelihood method.

Regression is performed by setting a GST rate of

6%, based on the GST standard rate applied

worldwide. The determination of this GST rate is

based on international regulatory reviews and

scientific literature. Also, this study adds control

variables related to demographic and economic

factors and will compare the results of potential tax

revenue between GST and VAT in order to increase

tax revenue. The specification model to estimate the

potential of GST as follows:

SEABC 2018 - 4th Sriwijaya Economics, Accounting, and Business Conference

106

𝒍𝒏𝑮𝑺𝑻

𝒊𝒕

= 𝜷

𝟎

+ 𝜷

𝟏

𝒍𝒏𝑮𝑫𝑹𝑷

𝒊𝒕

+ 𝜷

𝟐

𝑪𝑷𝑰

𝒊𝒕

+ 𝜷

𝟑

𝑺𝑸𝑪𝑷𝑰

𝒊𝒕

+ 𝜷

𝟒

𝒍𝒏𝑮𝑶𝑽𝑬𝑿𝑷

𝒊𝒕

+ 𝜷

𝟓

𝒍𝒏𝑷𝑶𝑷

𝒊𝒕

+ 𝜷

𝟔

𝒍𝒏𝑺𝑯𝑺

𝒊𝒕

+ 𝜷

𝟕

𝒍𝒏𝑻𝑹𝑨𝑫𝑬

𝒊𝒕

+ 𝜺

𝒊𝒕

(4)

Equation 4 is log-log model indicator for each 1%

change in the independent variable to dependent

variables. It is used to examine the hypothesis

variables which reference GST revenue, and allows

for the possibility that those variables would affect

potential GST revenue. A classical assumption test

was conducted to evaluate whether the parameters

generated by the regression model derived from the

OLS method are best linear unbiased estimators.

Thus, the classical assumption test used covers three

aspects: multicollinearity, heteroscedasticity, and

autocorrelation.

4 RESULTS AND DISCUSSION

4.1 Descriptive analysis

In general, the percentage of the revenue potential of

GST in provinces in Indonesia increased from 2005

to 2015. The decrease seen in 2008 was due to the

global subprime mortgage crisis that hit the United

States, but in the following years, the potential GST

acceptance rate shows a positive trend. It can be

concluded that, in light of the pattern of increasing

consumption activities by both households and the

private sector in Indonesia, there is the potential

nationally for a positive response to the

implementation of GST-type taxation in the country.

Figures 2 and 3 show the changes in the

potential distribution of GST in 33 provinces in

Indonesia for each year. In viewing this movement,

the authors only sampled for 2005 and 2015. To

achieve interprovincial equity, equitable distribution

of regional income is required.

Figure 2. Geographical distribution of potential GST tax revenues in 33 provinces in 2005

Source: Authors, from information from GEODA

Figure 3. Geographical distribution of potential GST tax revenues in 33 provinces in 2015

Source: Authors, from information from GEODA

Potential Implementation of Goods and Services Tax as a Substitute of Value Added Tax in Indonesia

107

Figures 2 and 3 show geographical locations if

GST is implemented at a regional level in Indonesia,

based on custom breaks. The use of custom breaks is

based on the classification of values within the

group (province) into five class intervals. The first

class contains areas that have potential GST revenue

of fewer than Rp30 trillion per year; the second

consists of regions with potential GST revenues of

between Rp31 and 60 trillion per year; the third is

regions with a potential GST revenue of Rp61 to 90

trillion per year; the fourth class interval contains

regions with potential tax revenue from GST of

Rp91 to 120 trillion and the final class interval

includes the regions with potential for annual GST

revenues of over Rp120 trillion.

In 2005, the highest GST revenue potential was

in West Java while the lowest was in Gorontalo, at

18.83% and 0.26% of total GST revenue potential

for the year, respectively. In this year, 97% of

provinces in all regions had a potential value of GST

revenues of less than Rp30 trillion. However, in

2015 there was a widening of distribution from

previously only the centralized West Java province.

There was an expansion of potential GST revenues

in other provinces, such as Banten, DKI Jakarta,

Central Java and East Java, with an average increase

of 54%. Although still concentrated in the island of

Java, there was an increase in GST acceptance

potential outside Java, although still in the same

interval class.

Furthermore, there was an increase in the

average potential GST acceptance nationally of

57.56%. Although still centered on the island of

Java, the study found interesting conditions occurred

in the province of North Sumatra that shows

significantly increased of GST revenue from 2005 to

2015. This condition is supported by the main

economic sector in the area, which is rich in natural

resources in the form of natural gas in the area of

Binjai and Langkat oilfields. Thus, the distribution

of potential GST revenues from 2005 to 2015 has a

positive trend, with a national average of Rp6 trillion

in 2005 increasing to Rp21 trillion per year by 2015.

Therefore, GST in Indonesia has the potential for

encouraging tax revenues in terms of both the ratio

of taxes and overall domestic revenues, as well as

contributing to the improvement of regional income

distribution.

4.2 Comparison of the strengths and

weaknesses of VAT and GST

Each type of tax has advantages and disadvantages,

both administratively and in practice. This

comparison aims to identify the efficiency and

welfare effects of the differences between the VAT

and GST. Table 1 presents a comparison of the

advantages and disadvantages of these two taxes.

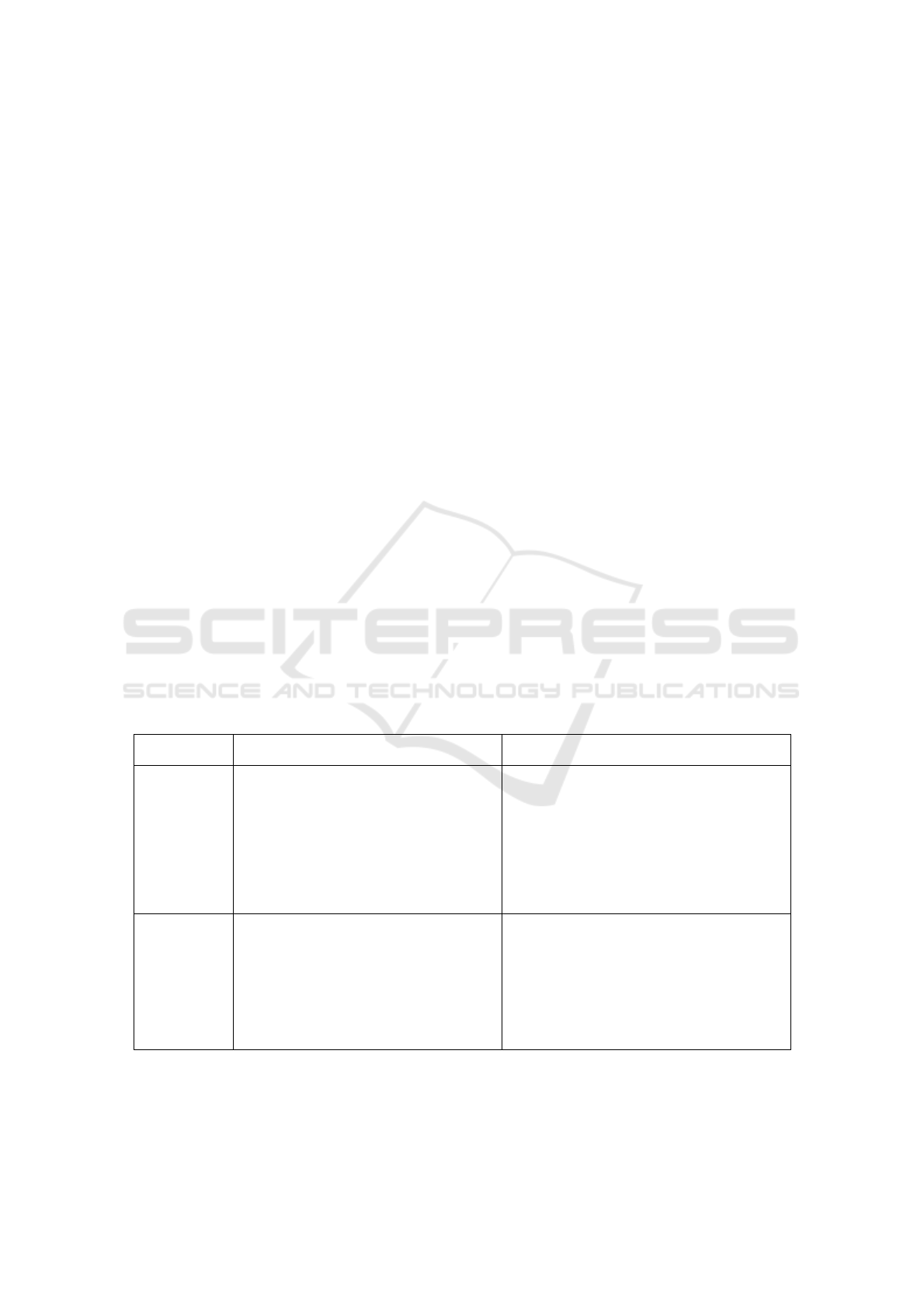

Table 1. Comparison of the strengths and weaknesses of VAT and GST

TAX TYPE

STRENGTHS

WEAKNESSES

Value added

tax

(VAT)

Only taxed once, so there is no double

taxation

Uses a flat tax

Tax base is based on value added in

goods and services

VAT is charged on any transactions

involving the transfer of taxable goods or

taxable services in certain regions of the

country

VAT input and VAT output requirements

increase accounting cost

VAT is implemented at a central level

only, so there can be no fiscal

decentralization

Goods and

services tax

(GST)

An easier administrative system, thus

reducing tax avoidance and tax evasion

Reduces lost revenue opportunities by

tightening supervision at an early stage

in the production and distribution chain

There can be GST refunds for foreign

tourists

Minimizes economic distortion

The potential for double taxation

Reduces people’s incentives to consume

Source: (Le, 2003)

SEABC 2018 - 4th Sriwijaya Economics, Accounting, and Business Conference

108

4.3 Empirical results

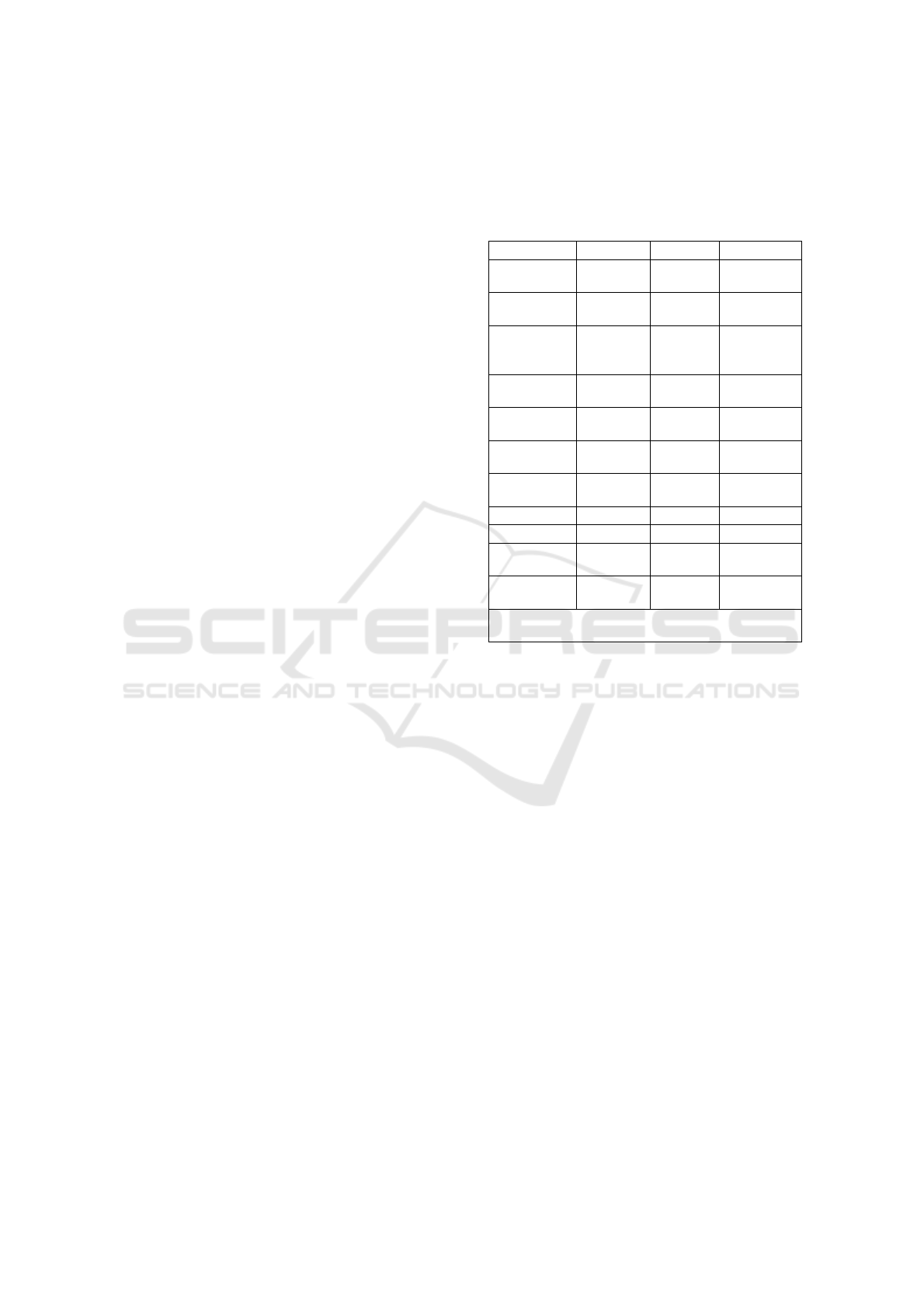

Table 2 shows that, in general, each variable for

model 1, model 2, and model 3 has constant value

changes with varying significance levels of 1%, 5%

and 10%. In general, it can be concluded that every

major variable and control variable in the model has

been tested in accordance with the theory of

robustness with constant value changes and with

various control variables added. The best model is

model 2, which is the model with the main control

variable being the population having an education

level of at least SHS. This reflects the majority of

workers in Indonesia being SHS graduates. This

model has an adjusted R-squared value of 0.9520,

which means that the dependent variable in the

model can be explained by an independent variable

of 95.2%.

For variables related to wealth and income in the

regional economy, GRDP for all three models is

consistent, suggesting that the value of GRDP based

on expenditure has a positive correlation trend and is

significant for the percentage of potential GST. This

can be seen from the significance value of 5% for

the default. It can therefore be concluded that

increase in revenue of GRDP of 1% in an area will

increase the potential of GST acceptance by 5%,

ceteris paribus. This result is in accordance with the

theory that the greater the regional income, the

greater the tax revenue. In model 2, the percentage

of GRDP has the best level of significance, with a p-

value of 0.019 from adding a variable related to a

demographic factor, in this case, the education level

of its population.

For CPI and quadratic CPI (SQCPI) variables,

CPI has a positive and significant impact on the

percentage of potential GST revenues with a 99%

confidence interval. However, this impact does not

occur in long-term balance. It indicates that the

effect of GST on inflation shows that impacts occur

only at the time of the initial introduction of GST

and when it has just been implemented, ceteris

paribus. This is due to a small shock to the economy

and the unfamiliarity of the market with a new type

of taxation, known as transitional cost, which

increases the price of goods and services. For local

government expenditure variables (GOVEXP), it

can be seen that all three models show consistent

results suggesting that local government expenditure

has a positive and significant correlation with the

percentage of potential GST acceptance. This is in

line with Adolf Wagner's theory which states that

the greater the economic income of a country, the

greater the government spending to balance the

development of the state and the needs of society.

Table 2. Estimation Result for Fixed Effect Model of

potential GST Revenue

Variable

Model 1

Model 2

Model 3

lnGDRP

0.040**

(0.018)

0.033***

(0.018)

0.028

(0.019)

CPI

0.043***

(0.003)

0.043***

(0.003)

0.042***

(0.003)

SQCPI

-

0.000***

(0.000)

-

0.000***

(0.000)

-0.000***

(0.000)

lnGOVEXP

0.046**

(0.019)

0.039**

(0.019)

0.039**

(0.019)

lnPOP

0.710***

(0.043)

0.708***

(0.042)

0.708***

(0.042)

lnSHS

0.113***

(0.038)

0.113***

(0.038)

lnTRADE

0.040**

(0.023)

Prob>F

0.0000

0.0000

0.0000

N

363

363

363

Within R-

square

0.9553

0.9565

0.9569

Adjusted R-

square

0.9500

0.9510

0.9520

Note: *** Significant at 1% level; ** Significant at

the 5% level; * Significant at the 10% level

Source: Authors’ Calculation.

From Table 2, the results for model 1 indicate

that an increase in government spending of 1% will

lead to an increase in the potential of GST

acceptance of 0.046%, ceteris paribus. In addition, in

model 1, local government spending is also

significant and has a positive correlation trend with

the percentage potential for GST, in which the

coefficient value will be smaller with the increase in

control variables. This is in line with the theory that

revenues and expenditures have a cointegration

relationship with each other. Demographic-related

variables such as total population deliver constant

results with potentially positive relationships with a

potential percentage of GST acceptance. With a 99%

confidence level, the size of provincial populations

is significant for the increasing percentage of

potential GST acceptance. Therefore, in model 1,

ceteris paribus, for every 1% increase in provincial

population, the potential for GST acceptance will

increase by 0.710%.

In addition, models 2 and 3 show similar results,

with a significance level of 1%. Therefore, by

assuming that each individual engages in

consumption activity, this is consistent with the

Potential Implementation of Goods and Services Tax as a Substitute of Value Added Tax in Indonesia

109

theory that consumption is positively correlated

with implementation. Another demographic variable

is SHS education level, reflecting the level of

education of workers in Indonesia. The justification

of this variable is that people who have graduated

from high school have income to spend. This is

supported by statistics for workers in Indonesia

which show that the majority of workers are high-

school educated, and it can therefore be assumed

that they carry out consumption activities. In the

regression estimate, the SHS variable has a

potentially positive and significant relation at a 99%

confidence interval for potential GST acceptance in

provinces in Indonesia. It can therefore be said that

for every 1% increase in the population of high

school graduates, ceteris paribus, the potential of

GST acceptance will increase by 0.113%.

Meanwhile, the economic-sector-related

variables used as other controls are the trade sectors.

Table 2 shows that, with the entry of TRADE

variables, the value of GRDP becomes insignificant.

This is because this variable only includes trade

activities that are highly relevant to the imposition of

GST. GRDP covers not only consumption activities

but also other components, such as gross domestic

fixed capital formation and inventory changes that

are less relevant to GST. Consequently, the p-value

of GRDP decreases. Therefore, it can be interpreted

that for every increase in GDP of the trade sector by

1%, ceteris paribus, the potential of GST acceptance

will increase by 0.023%. Thus, it can be stated that

although each variable used has a different level of

significance, for GRDP in each province CPI and

quadratic CPI and government spending have met

the hypothesis proposed in this study.

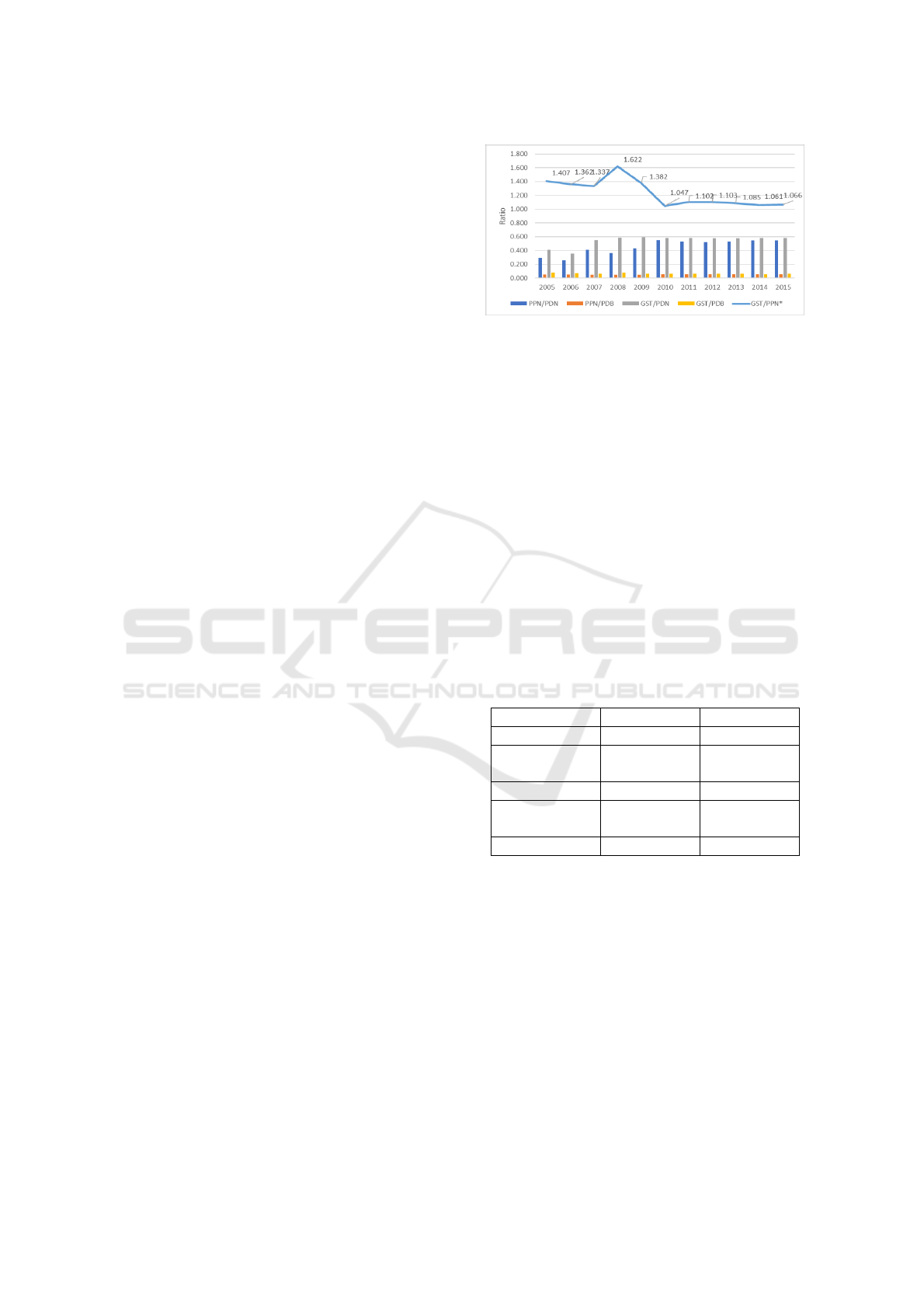

Figure 4 describes the potential tax revenue of

GST and VAT for domestic product and GDP from

2005 to 2015. Using a GST tax rate of 6% (the

world standard), GST revenue potential in Indonesia

is almost twice as great as the tax revenue potential

for VAT at a 10% rate. If the government plans to

implement a GST with value of revenue equal to the

potential of VAT revenue as it has been

implemented thus far, it should charge a GST rate of

at least 5%. Thus, this difference of 1% is a revenue

advantage in the potential implementation of GST

rather than VAT. The world standard rate of 6% has

a larger revenue estimate with an upward trend each

year than the potential VAT revenue at the 10% rate

as currently applied. As a result, for a GST rate of

6%, the potential for receipts is the same as for

VAT at a 10% rate.

Figure 4. GST and VAT potential revenue ratio in terms of

domestic revenue and GDP 2005–2015

Overall, the study can assess feasibility based on

Stiglitz’s (2000) tax principles. One of the principles

focused on in this research is the comparative

efficiency of VAT and GST. This factor can be

determined from comparison of the value of the tax

revenue ratio for each, supported by empirical

analysis of the panel data regression between

regions. In summary, the estimated potential GST

revenue can be evaluated based on the Stiglitz’s

theory of tax principles as described above. Table 3

shows a comparison of VAT and GST for

descriptive and econometric analyses performed in

accordance with the taxation principles. In short,

GST-type tax has met the rules to be considered to

be a good tax policy.

Table 3. Evaluation framework for the Stiglitz taxation

principles for VAT and GST

Principle

VAT

GST

Efficiency

No

Yes

Administrative

simplicity

No

Yes

Flexibility

Yes

Yes

Political

responsibility

Yes

Yes

Fairness

Yes

Yes

5 CONCLUSION

This research proposes the use of a provincial

panel data method with an surcharge (opsen) system

as a new method to obtain best assignment rules for

the distribution of tax revenue collected to

strengthen fiscal capacity. Based on the analysis

from the OLS panel data model at a regional level,

GST can be seen to have a significant potential to

increase tax revenues. In summary, GST has

potential applicability in Indonesia, evident from the

ratio of GST revenue (as compared to that for VAT)

SEABC 2018 - 4th Sriwijaya Economics, Accounting, and Business Conference

110

of greater than 1, thus meeting the rules of Stiglitz's

theory. Furthermore, the potential GST revenue in

Indonesia is greater than the potential for VAT by an

average amount of Rp60 trillion each year. As a

result, greater efficiency is expected if GST is

implemented in Indonesia rather than the current

VAT regime. We were aware that this research has

some limitations. The variable used to describe

consumption level, in this case education level, was

not very specifically focused on describing

household expenditure levels.

Further research should improve on certain

aspects: first, it would be beneficial to conduct more

microlevel research to more accurately measure

consumer readiness, perceptions, and acceptance of

GST and to investigate how it would affect

household expenditure and income inequality and

poverty level; second, the research should measure

the role of regional government in supporting policy.

ACKNOWLEDGEMENT

Authors thank to Hibah PITTA Universitas

Indonesia for partly and financially support to

rewrite and publish the first author’s undergraduate

thesis that is submitted to Department of Economics,

Faculty of Economics and Business, Universitas

Indonesia. All remaining errors are our own.

REFERENCES

Grady, P. (2009). An analysis of the distributional impact

of goods and services tax. Munich PErsonal RePEc

Archive Paper, 13144. https://mpra.ub.uni-

muenchen.de/13144/1/MPRA_paper_13144.pdf

Ibrahim, M. R. (2013). The impact of goods and services

tax on middle-income earners in Malaysia.

International Journal of Economics Business and

Management Studies, 2(1), 12–19.

Jenkins, G., & Khadka, R. (1998). Tax reform in

Singapore. (Development Discussion Paper 644).

Harvard Institute for International Development.

http://jdintl.econ.queensu.ca/publications/qed_dp_129.

pdf

Le, T. M. (2003). Value-added taxation: Mechanism,

design, and policy issues. (World Bank course on

Practical Issues of Tax Policy in Developing

Countries). Washington DC.

http://siteresources.worldbank.org/INTTPA/Resources

/TuanPaper.pdf

Mansor, N. H. A., & Ilias, A. (2013). Goods and services

tax (GST): A new tax reform in Malaysia.

International Journal of Economics Business and

Management Studies, 2(1), 12–19.

Nurhidayati. (2013). Estimating elasticity and buoyancy of

Value Added Tax (VAT) in Indonesia: Aggregate and

Sectoral Basis Analysis Unplublished Tesis,

University of Indonesia.

Palil, M. R., & Ibrahim, M. A. (2011). The impacts of

goods and services tax (GST) on middle income

earners in Malaysia. World Review of Business

Research, 1(3), 192–206.

Ramesh, A. (2015). Gst in India - Challenges and

opportunities. Perquisa Journal, 1(1). Munich

Personal RePEc Archive Paper, 13144.

Rao, R. K., & Chakraborty, P. (2013). Revenue

Implications of GST and Estimation of Revenue

Neutral Rate: A State Wise Analysis. National Institute

of Public Finance and Policy, New Delhi.

Rosen, H. S., & Gayer, T. (2010). Public Finance (9th ed).

New York, NY: McGraw-Hill.

Stiglitz, J. E. (2000). Economics of the public sector (3rd

ed). New York, NY: W.W. Norton & Company.

Valadkhani, A. (2005). Goods and services tax effects on

goods and services included in the consumer price

index basket: Australia. The Economic Record, 81,

104–114.

WorldBank.. Tax Revenue (% of GDP). Retrieved from

http://databank.worldbank.org/data/reports.aspx?sourc

e=2&series=GC.TAX.TOTL.GD.ZS&country=IDN,

MYS,SGP,AUS,CAN#

Potential Implementation of Goods and Services Tax as a Substitute of Value Added Tax in Indonesia

111