Analysis Internal Control In Order To Design Standard Operating

Procedure (Sop) For Fixed Assets Procurement And Management

Activites: Case Study on PT ABC

Triyanda Agustin Ginting

and Siti Nurwayuningsih Harahap

Department of Accounting, Faculty of Economic and Business, University Indonesia, Jakarta, Indonesia

triyanda.agustin@gmail.com, nungharahap@yahoo.com

Keywords: Control Activity, Fixed Assets, Fixed Assets Procurement and Management Activities, Identify Risk,

Internal Control.

Abstract: This research aims to analyze internal control system and propose a design of standard operating procedures

(SOP) for fixed asset procurement and management activities in PT ABC. This is a qualitative research with

case study method at PT ABC which is engaged in rental fixed assets for supporting education facilities. We

have interviewed the management of PT ABC, conducts observation, and analysis internal documents.

Based on those data, we analyze the internal control system that has been implemented by PT ABC related

with procurement and management activities of fixed assets, including identifying risk in those activities as

the basis for the analysis of the ongoing internal control system. The results show that there are some

weakness on internal control system, especially related to fixed assets management activities. Therefore,

some risks have not been mitigated yet. In addition, the Company has not formalized internal control

procedure yet, which caused unstructured implementation. Therefore, this research provides

recommendation for improvement in internal control activities and proposed a design of standard operating

procedure (SOP) related to procurement and management activities of fixed assets that tailored with the PT

ABC needs.

1 INTRODUCTION

Companies use assets as one of the resources to

support the company's operational activities in order

to achieve company goals. Fixed assets are generally

important for to the company due to its significant

value and long-term usage to achieve company’s

goals. Based on Indonesian GAAP 16 (IAI, 2014)

states that property, plant and equipment are held for

use in the production or supply of goods or services,

for rental to others, or for administrative purposes

and expected to be used for more than one period. In

addition to its value, information related with assets

are important for both companies and stakeholders

for decision-making. Lansiluoto, Jokipii, Eklund

(2016) stated in their research if firm does not have

effective internal control, it is possible that the

firm’s financial statement contains a material

weakness. Hence, it is critical for management to

have and establish appropriate policies and controls

surrounding fixed assets. With appropriate policies

and controls, it is expected that the company will

have a reliable financial statement with no material

misstatements in fixed assets.

PT ABC engaged in education services, (school

operated under foundation) for children under 3

years old (early childhood education) up to 18 years

old (high school), with market share is middle to

upper class families. Until now school has 6 (six)

branches (later call as site) in Jakarta and 1 (one)

branch in Surabaya with total student reaching 1,500

students. One of the services is rental fixed assets for

supporting education facilities at XYZ foundation.

PT ABC is act as a holding and record all fixed

assets and receive fee payment from XYZ

foundation in the form of rental fee.

Assets remain important for PT ABC because

fixed assets play a significant role in business

activities, have a material value (65.58% of total

assets of PT ABC in 2016), and the value of fixed

assets is used as the basis for calculating rental fees.

The rental fee is based on the fair value of total fixed

assets, with tariff charged based on agreement is 4%

from total fair value of fixed assets. The business

364

Ginting, T. and Harahap, S.

Analysis Internal Control In Order To Design Standard Operating Procedure (Sop) For Fixed Assets Procurement And Management Activites: Case Study on PT ABC.

In Proceedings of the Journal of Contemporary Accounting and Economics Symposium 2018 on Special Session for Indonesian Study (JCAE 2018) - Contemporary Accounting Studies in

Indonesia, pages 364-370

ISBN: 978-989-758-339-1

Copyright © 2018 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

process of PT ABC also has an unique characteristic,

which is PT ABC owned the fixed asset then renting

the fixed asset to XYZ Foundation. The procurement

process of fixed assets was done by PT ABC based

on XYZ Foundation needs, while the management

of assets is in the hands of XYZ Foundation.

Therefore, it is important for PT ABC to have

adequate internal control related with fixed asset

procurement and management activities, due to

ineffectiveness in internal control can lead to

inaccurate of total fixed assets. Inaccurate of total

fixed assets may cause a risk that is potential loss of

income for PT ABC, as well as incomplete

information of assets will impact in improper

decision making. Other than that, this is also poses a

potential risk for PT ABC that is fixed assets are not

suitable with the needs of site if the procurement

process is not done properly and loss of fixed assets

or fixed assets more quickly damaged if the XYZ

foundation does not manage fixed assets properly.

Management has plans for expansion by opening

several new schools in several major cities on Java

and Sumatera with foreign investors, with the

nearest project is in early 2018 with opening new

branches in Bandung and Pekanbaru. Through this

expansion the value of the company's fixed assets

will be even greater and the presence of foreign

investment requires the company to be able to

provide reliable financial reports.

With the things mention above, the objectives of

this research are to understand the internal control

system that has been implemented by PT ABC

related with procurement and management activities

of fixed assets, identify risks related to procurement

and management activities of fixed assets PT ABC's

as a basis for internal control analysis of the ongoing

system, and provide recommendation in the form of

proposed a design of SOP procurement and

management activities of fixed assets so that control

activities can run effectively and efficiently.

2 LITERATURE REVIEW

2.1 Internal Control

Committee of Sponsoring Organizations of The

Treadway Commission (2013) defined internal

control as a process, effected by an entity’s board of

directors, management, and other personnel,

designed to provide reasonable assurance regarding

the achievement of objectives relating to operations,

reporting, and compliance. Romney and Steinbart

(2015) stated internal control as the process

implemented to provide reasonable assurance that

control objectives are achieved, including safeguard

assets. COSO’s Internal Control—Integrated

Framework (2013) enables organizations to

effectively and efficiently develop systems of

internal control that adapt to changing business and

operating environments, mitigate risks to acceptable

levels, and support sound decision making and

governance of the organization. Internal control

consists of five integrated framework that is control

environment, risk assessment, control activity,

information and communication, and monitoring.

2.2 Internal Control of Fixed Assets

Control activity of fixed assets can fall into the

several categories (Romney and Steinbart, 2015).

Proper authorization of transaction and activities,

can be done since the procurement process up to

managing fixed assets. authorizations are required

when request for order fixed assets, transfer of fixed

assets, ulitization asset, and write-off fixed assets.

Segregation of duties, done with segregation duties

employee for record, custody, receive, and buy and

payment the fixed assets. Design and use of

documents and records, ensuring documents or

records used in controlling fixed assets are adequate

and all activities are well documented. Safeguarding

assets, records, and data, done by creating and

enforce appropriate asset policies and procedures,

maintain accurate asset records of all assets, restrict

access to assets, and protect records and documents.

Independent checks on performance, done with

regularly perform physical check.

There are two essential elements of internal

control when we are dealing with Property, Plant,

and Equipment (PP&E). One is knowing what you

are supposed to have, which is the purpose of the

fixed-asset register or master file. The other is being

able to locate the actual assets, to provide assurance

that the property register represents what is

physically present (King, 2011).

One of control activities to achieve the

company's goal is to have the design and use of good

documents and records (Romney and Steinbart,

2015). One form of documentation is to have a

standard operating procedure (SOP). Standard

Operating Procedure (SOP) based on United States

Environmental Protection Agency (2007) is a set of

written instructions that document a routine or

repetitive activity followed by an organization. The

development and use of SOPs are an integral part of

a successful quality system as it provides individuals

with the information to perform a job properly, and

Analysis Internal Control In Order To Design Standard Operating Procedure (Sop) For Fixed Assets Procurement And Management

Activites: Case Study on PT ABC

365

facilitates consistency in the quality and integrity of

a product or end-result.

They document the way activities are to be

performed to facilitate consistent conformance to

technical and quality system requirements and to

support data quality. SOPs are intended to be

specific to the organization or facility whose

activities are described and assist that organization

to maintain their quality control and quality

assurance processes and ensure compliance with

governmental regulations (United States

Environmental Protection Agency, 2007).

Dini (2013) in her research, do analysis

effectiveness internal control of fixed asset

management in North Jakarta Administration City

Government, that using COSO criteria and Peraturan

Pemerintah No. 60/2008 tentang Sistem

Pengendalian Intern Pemerintah as well as the

PERMENDAGRI No. 17/2007 tentang Pedoman

Teknis Pengelolaan Barang Milik Daerah as a

valuation guide. The results show that the

implementation of the internal control system in

general is quite good but not as effective as it still

has weaknesses. the difference with previous

research is researcher not stop in provide

recommendation for weaknesses in internal control

but also provide recommendation in the form of

proposed design of standard operating procedure.

3 RESEARCH METHODOLOGY

3.1 Research Methods

This research is a qualitative research with case

study approach. Qualitative research is multi-method

in focus, involving in interpretive, naturalistic

approach to its subject matter. This means that

qualitative researchers study things in their natural

settings, attempting to make sense of, or interpret

phenomena in the terms of the meanings people

brim to them (Wahyuni, 2015). This method is

choose due to this research is aim to gain deeper

understanding of the process or experience or

phenomena from a person or group that occur in the

field then make conclusion of the pattern or

phenomenon that occurs. Other than that, qualitative

research is choose due to data that researcher use for

processing data is not numerical data, but using data

from observation, interview results, analysis

documents.

This research is case study approach on fixed

assets procurement and management activities at PT

ABC in consideration total fixed assets is use as

basis for calculation rental fee, which is this rental

fee is income for PT ABC. Income is an important

aspect because it affects the going concern of an

entity. Thus, the researcher considers that this

research will give a large enough impact for the

object of research.

Data collection method that use in this research

are observation, interview, and analysis internal

documents. Observation was conducts in Head

Office and site Serpong (choose because has the

biggest total fixed asset). Researcher get a chance to

know how the management of fixed assets done,

such as the process of receive fixed assets, delivery

fixed asset to other site, and how safeguarding asset

run head office and site. Interview conducts to know

business environment and business process of

company and components of internal control for

procurement and management activities of fixed

assets PT ABC, which allows new questions to gain

a deeper understanding. Interviews conducts by the

researcher involve general affair general manager,

general affair manager, procurement manager,

finance staff and some general affair site staff.

Researcher also analyze Company’s internal

documents to know the adequacy of documents.

3.2 Unit Analysis

The procurement and management activities of fixed

assets PT ABC was involve the General Affairs

department. General affair department divided into

general affair head office (in PT ABC) and general

affair site (under XYZ Foundation and located in

every school/site). General affair site is responsible

to general affair head office (PT ABC) related with

the fixed assets management activities in each site.

Procurement activities involves ordering fixed

assets, supplier or vendor selection, and receiving

fixed assets process. Management activities of fixed

assets involves recording fixed asset, transfer fixed

asset, disposal fixed asset, receiving assets from

donors, and monitoring fixed assets process.

3.3 Data Analysis

Research is carried out with understanding the

business environment and business processes of the

company by doing interview with management PT

ABC. To gain deeper understanding related with

fixed asset procurement and management activities,

researcher conducts interviews with people from

general affair department such as general affair GM,

GA and procurement manager and GA staff and

other department that related with general affairs

JCAE Symposium 2018 – Journal of Contemporary Accounting and Economics Symposium 2018 on Special Session for Indonesian Study

366

such as finance staff. Research analyze internal

documents to determine the adequacy of documents,

whether it is in accordance with the needs of fixed

asset procurement and management activities

Then researcher make analysis related with

company's internal control system using the COSO’s

internal control framework, including identifying

and analyzing the risks associated with the

procurement and management of fixed assets,

analyzing ongoing internal control system and

provide recommendation of existing internal

controls weakness.

4 RESULT

4.1 Internal Control Analysis on Fixed

Asset Procurement and

Management Activities at PT ABC

Components of internal control to be tested include

the control environment, risk assessment, control

activity, information and communication, and

monitoring.

1. Control Environment.

Researcher do the analysis where the criteria

examined are management’s philosophy and

operating style, commitment to integrity and ethical

value, organizational structure, assigning authority

and responsibility, and policy and practice of human

resource development. The results show that vision

and mission Company not written in any media and

employees are not aware of their role in terms of

internal control. Therefore, researcher provide

recommendation to including vision and mission in

the employee guidebook. Also, Company provides

an overview of internal controls, the importance of

internal controls for the company and what role

employees should do in order for internal controls

proceed effectively. Including control activities as

one of the employee performance appraisal points.

2. Risk Assessment.

Researcher do the analysis where the criteria

examined are establishment of overall company

objectives, goal setting at level activity, risk

identification, risk analysis, and risk management.

The results show that Company not yet do identify

and analysis risk, assessment risk and manage risk.

Therefore, researcher do identify and analyze risk, to

help Company to start doing risk assessment.

3. Control Activity.

researcher do the analysis where the criteria

examined are proper authorization of transaction and

activities, segregation of duties, safeguard assets,

accurate and timely recording of transaction, control

over management information system,

documentation of transaction, and activities

independence check of performance, and training

employee. Following were weakness that associated

with criteria that mentioned above:

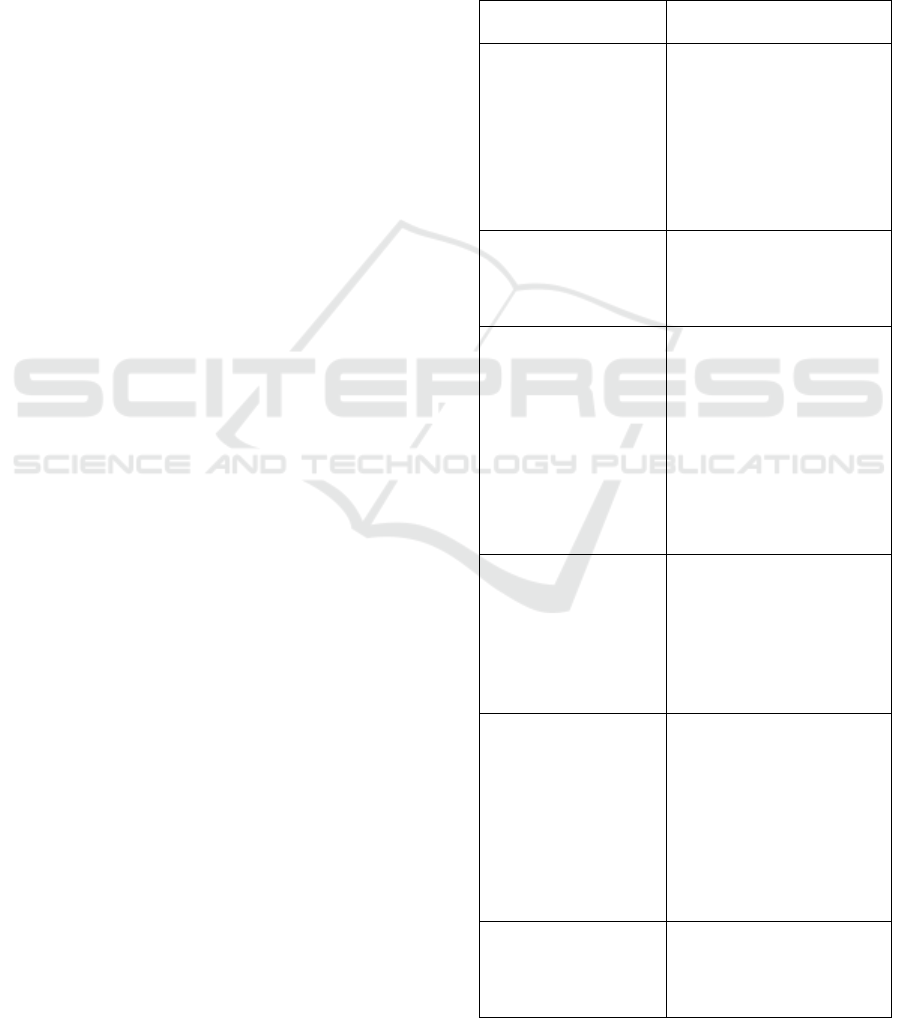

Tabel 1: Problem Identification and Recommendation

Control Activities

Problem

Identification

Recommendation

Site coordinator not

routine in making

"pertanggungjawaban"

report, can be delayed

up to 2 weeks

GA department must be

routine in making an

"pertanggungjawaban"

report (at least once a week,

adjusted with the frequency

of receipt goods) and give

penalties or punishment if

treporting exceeds the

specified time.

General affair and

finance department

never reconciles fixed

asset data

Perform reconciliation

(check and balance)

between GA and finance at

least once a month.

Company has not yet

applied technology

information system in

recording fixed assets

Begin to use information

systems technology to

record the assets of PT

ABC. This system can be

purchased or built alone

(depending on the maturity

of the company's IT) and to

be effective must be

integrated with all

procurement and asset

management activities.

Transfer of assets

(borrowed or

permanently

transferred) is not well

documented.

Transfer of assets whether

borrowed (temporary) or

transferred (permanent)

must have clear procedures,

with supporting documents

and approved by the GA

Director/GM.

General affair never

informs the finance

department for assets

that permanently

transferred or

disposed.

Inform finance for transfer

or disposal assets, therefore

fixed asset in finance

always update. This can be

done by regularly perform

reconciliation between GA

and finance. Provide

punishment if it fails in

performing its duties

(informing disposal).

Company does not

have a regular

schedule for physical

checks.

Company has a fixed

schedule for physical

checking of fixed assets

head office and site, at least

Analysis Internal Control In Order To Design Standard Operating Procedure (Sop) For Fixed Assets Procurement And Management

Activites: Case Study on PT ABC

367

annually.

4. Information and Communication.

Researcher do the analysis where the criteria

examined are information and communication and

form and tools communication. The result show that

Company does not have standard operating

procedure, therefore researcher provide propose

design of standard operating procedures (SOPs) for

fixed assets procurement and management activities

at PT ABC with the aim of providing guidance to

employees and facilitate employees in carrying out

their duties.

5. Monitoring.

Monitoring is an evaluation to assess whether each

element of internal control has been implemented

and functioning as it should. The results show there

are fixed assets that directly send to site without re-

checking from GA head office. Therefore,

researcher provide recommendation that require GA

to re-checking fixed assets sends directly to site, at

least for fixed assets that have a material nominal

and have regular schedule to perform physical

checks.

4.2 Risk Assessment and Control Activity

Analysis on Procurement and

Management Activity of Fixed

Assets PT ABC

Based on internal control analysis above, Company

never conduct risk assessment. Therefore, researcher

do risk assessment in order to help Company. Risk

assessment start with identify risk that related with

fixed asset procurement and management activities,

then researcher determine ideal control activities for

those activities. Researcher then compare current (on

going) control activities with the ideal control

activities, for those activities that find doesn’t have

proper control activities, researcher will provide

recommendation.

Based on analysis, there are several activities that

find not have proper control activities, for those

weaknesses researcher provide recommendation,

please find below:

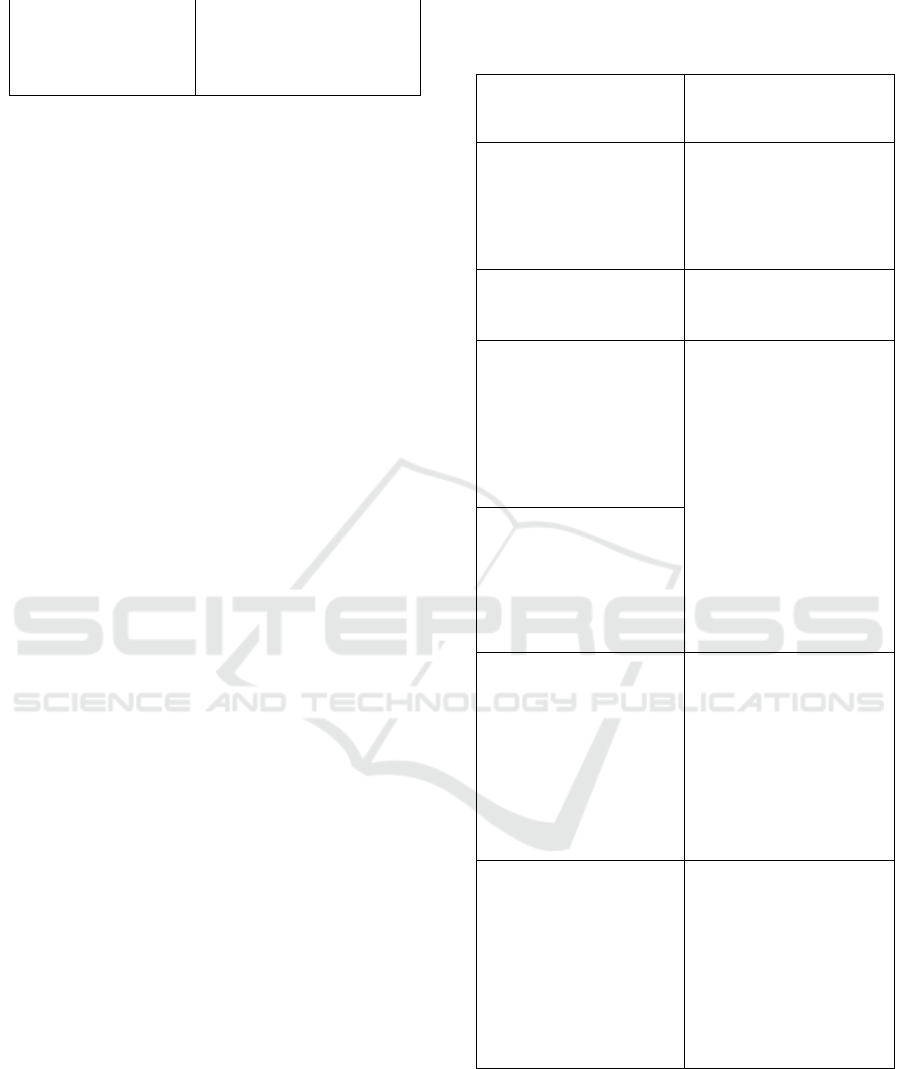

Table 2: Recommendation Control Activity for

Procurement and Management Activity of Fixed Assets

PT ABC

Analysis (Risk and

Current Control

Activities)

Recommendation

Risk: kickbacks.

-There are no job rotation

rules and obligation to

take holidays or leave in

procurement department.

Obligation to take holiday

or leave as Company

rules.

Analysis (Risk and

Current Control

Activities)

Recommendation

Risk: Receive assets not

accordance with the

specifications.

-Not all sites receive

purchase order from head

office, seldom based on

verbal info from head

office.

Copy of purchase order

must be given to the site

(if the goods are directly

received at the site).

Risk: Mistake in

accounting.

-Not all sites receive

purchase order from head

office, seldom based on

verbal info from head

office.

Risk: Loss of fixed

assets.

-For items received

directly on site, head

office never performs

physical checks.

GA department should be

routine in making

"pertanggungjawaban"

report (at least once a

week, adjusted with the

frequency of receipt

goods) and give penalties

or punishment if

reporting exceeds the

specified time.

Risk: Records of fixed

assets are not accurate.

-Company still using

excel to record assets.

-Never done checks and

balances process.

-Started using technology

information systems to

record the assets of PT

ABC, integrated with all

procurement and

management activities of

PT ABC's fixed assets.

- Routinely perform

check and balance assets

between GA and finance.

JCAE Symposium 2018 – Journal of Contemporary Accounting and Economics Symposium 2018 on Special Session for Indonesian Study

368

Risk: Assets are lost and

asset records are not

accurate.

-Not all fixed assets that

come out from site are

issued delivery order.

-Transfer of fixed assets

between sites is not

documented (no special

documents, only verbally

or via email) and not

communicated to the

finance department.

- Authorized verbally by

GA GM.

-Transfer of fixed assets

either borrowed

(temporary) or transferred

(permanent) must have

clear procedures, with

supporting documents

and approved by GA

Director/GM.

- Establish standard

operating procedure

(SOP) related to

management activities of

Company's fixed assets.

Analysis (Risk and

Current Control

Activities)

Recommendation

Risk: Records of fixed

assets not accurate.

-The write-off of fixed

assets (discarded, sold, or

donated) is not

communicated to

finance.

- The removal of fixed

assets (discarded, sold,

donated) that still have

book value must first

obtain GM Finance

approval and all removed

assets must be

communicated to the

finance department to

update the company's

fixed asset records.

- Establish standard

operating procedure

(SOP) related the

management activities of

Company's fixed assets.

Risk: Records of fixed

assets not accurate.

-GA does not have a

fixed schedule to perform

physical checks.

-Not all fixed assets

companies have tagging

and number assets in

each site has a different

format (not

standardized).

-Company has fixed

schedule for physical

checking FA head office

and site, at least annually.

-All of the company's

fixed assets must have

tagging (sticker or

barcode) and number

assets on each site should

be standardized.

- Establish standard

operating procedure

(SOP) related to

management activities of

the Company's fixed

assets.

4.3 Proposed Design of Standard

Operating Procedure (SOP) for

Fixed Asset Procurement and

Management Activities at PT ABC.

Based on internal control and risk assessment

analysis above, the Company does not have internal

control that is formalized therefore the procurement

and management activities of fixed assets are still

running not effectively. Therefore, researcher

provide proposed standard operating procedure

(SOP) and related documents that can support the

smooth those activities.

Researcher proposed 7 (seven) design standard

operating procedure related with fixed asset

procurement and management activities, that is

procurement fixed asset, utilization fixed asset,

stocktaking fixed asset, borrow fixed asset, transfer

fixed asset, retirement fixed asset, and loss fixed

asset.

Each proposed SOP is design with PT ABC needs

and consist of:

1. Approval of SOP by top management and related

senior management.

2. Objective and scope.

3. Responsibility, stated people or department that

responsible for those process.

4. Definitions, identifying any acronyms,

abbreviations, or specialized terms used.

5. Conditions, explain definition and classification

of fixed assets and authorization for each

process.

5. Process, explanation for each process.

6. Flowchart, showing the step or workflow that

explain in process.

7. Documents related process, stated documents

that needs for each process.

Based on analysis on transfer assets process it is

found that this process is not documented well

enough, therefore researcher also design documents

related to borrow and transfer asset.

5 CONCLUSION

Based on the results of the analysis and discussion

that has been discussed in the previous section, it

can be concluded that PT ABC already has internal

controls related to procurement and management

activities of fixed assets but internal controls are still

not formalized and still found some problems in the

implementation of such control. For any weaknesses

that found in the internal controls, the researcher

propose recommendation.

Based on the results of risk analysis related to

procurement and management activities of fixed

assets PT ABC still found some risks that have no

control activities.

Based on the results of risk analysis and control

activities, researcher provide proposed design of

Analysis Internal Control In Order To Design Standard Operating Procedure (Sop) For Fixed Assets Procurement And Management

Activites: Case Study on PT ABC

369

standard operating procedure (SOP) related to

procurement and management activities of fixed

assets that tailored with PT ABC needs.

Research has several limitations that are the

evaluation of internal controls focuses on

procurement and the management activities of fixed

assets PT ABC and does not cover the entire system

of PT ABC and the proposed standard operating

procedure (SOP) is limited to procurement and

management activities of fixed asset.

REFERENCES

Committee of Sponsoring Organization of the Treadway

Commission (2013). Internal Control-Integrated

Framework: Executive Summary. July 23, 2017.

https://na.theiia.org/standards-

guidance/topics/Documents/Executive_Summary.pdf

King, A. M. (2011). Internal Control of Fixed Assets: A

Controller and Auditor’s Guide. New Jersey: John

Willey & Sons, Inc.

Ikatan Akuntan Indonesia. (2015). Standar Akuntansi

Keuangan. Jakarta: Salemba Empat.

Länsiluoto, Aapo., Jokipii, Annukka., Eklund, Tomas.

(2016). Internal control effectiveness – a clustering

approach, Managerial Auditing Journal, Vol. 31 Issue:

1, pp.5-34. Retrieved from https://remote-

lib.ui.ac.id:4611/10.1108/MAJ-08-2013-0910

M.B. Romney and P.J. Steinbart. (2015). Accounting

Information Systems (13th Ed.). England: Pearson

Education Limited

Paramita, Dini. (2013). Evaluation of effectiveness of

internal control systems in fixed asset business process

in order to improve financial reporting reliability at

North Jakarta Administration City Government. Tesis,

Magister Akuntansi, Universitas Indonesia. Retrieved

from http://lib.ui.ac.id/detail?id=20365137&lokasi=

lokal.

United States Environmental Protection Agency. (2007).

Guidance for Preparing Standard Operating

Procedure (SOPs). July 21, 2017.

https://www.epa.gov/sites/production/files/2015-

06/documents/g6-final.pdf

Wahyuni, Sari. (2015). Qualitative Research Method:

Theory and Practice (2nd Ed.). Jakarta: Salemba

Empat.

JCAE Symposium 2018 – Journal of Contemporary Accounting and Economics Symposium 2018 on Special Session for Indonesian Study

370