Does Audit Risk Affect The Audit Fee?

Ahmad Muhajir

Faculty of Economics & Business, Universitas Airlangga, Surabaya, Indonesia

ahmdmhjrmd@gmail.com

Keywords: Audit Fees, Control Risk, Detection Risk, Inherent Risk, Risk Assessment.

Abstract: The risk assessment procedure is the most significant procedure in a general audit. Risk assessment is

commonly used to assess the risks of any potential material misstatement. In assessing risk, an auditor

considers three major components consisting of inherent risk, control risk, and detection risk. This research

aims to examine empirically whether these three audit risk components significantly affect the audit fee.

The three components of audit risk can be considered by an auditor at a public accountancy firm in

performing audit planning, such as determining the time and budget plan, the number of auditors assigned to

the fieldwork, and the audit scope to collect relevant audit evidence. Therefore, the auditor at a public

accounting firm can determine the audit fee suitable for the job. This study used managers and partners from

a public accounting firm in East Java that are registered on the public accounting firm directory published

by IICPA. The samples taken for this study are from 86 audit managers and audit partners. This study used

inherent risk, control risk, and detection risk as independent variables and the audit fee as the dependent

variable. In this research, a T-test was used to identify the effect of independent variables on the dependent

variable with the assistance of SmartPLS 3.0 for Windows.

1 INTRODUCTION

Certified public accountants provide assurance

services related to management assurance of

financial statements and are licensed by the Minister

of Finance with the issuance of the Regulation of the

Minister of Finance No. 17/PMK.01/2008 and later

supported by The Public Accountants Act No. 5 of

2011, which discusses public accountants. A public

accountant is required to always follow current

information including changes to the general

financial accounting standards and professional

standards of certified public accountants issued by

professional organizations and other official

regulations.

As of January 1

st

, 2013, Indonesia has used

International Standards on Auditing (ISA) in

determining the professional standards of certified

public accountants to be used by Indonesian

auditors. The ISA considers risks involved in

carrying out the audit fieldwork. Tuanakotta (2013)

divides audit risk into three main parts, namely

inherent risk, control risk, and detection risk.

Inherent risk is the vulnerability of an assertion to a

material misstatement. It relates to internal or

external events or circumstances arising from the

entity’s purpose, the nature of the entity’s operations

or the scope of the entity’s industry, the client’s

location, and the complexity of the client’s business.

The control risk emerges from the client’s

inadequate internal control. The third component is

detection risk meaning the material misstatement is

not detected by the auditor due to improper selection

and implementation of audit procedures.

At the audit planning stage, the auditor identifies

audit risks that may occur. A complex audit process

may be caused by a high audit risk. Audit risk plays

a significant role in the determination of audit fees

by public accounting firms. However, the audit risk

may not affect the audit fees since the fee

determination generally considers other factors such

as business competition among public accounting

firms.

The Institut Akuntan Publik Indonesia is the

official body that regulates Certified Public

Accountants (CPA) and legally empowers it to set

auditing standards and ethical standards as well as

publish the rules regarding audit fees; No.

KEP.024/IAPI/VII/2008 was updated on

Management Regulation No. 2 in 2016 regarding the

determination of audit fees.

Muhajir, A.

Does Audit Risk Affect The Audit Fee?.

In Proceedings of the Journal of Contemporary Accounting and Economics Symposium 2018 on Special Session for Indonesian Study (JCAE 2018) - Contemporary Accounting Studies in

Indonesia, pages 37-42

ISBN: 978-989-758-339-1

Copyright © 2018 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

37

There are some researchers who have

investigated studies closely related to this research.

In a study conducted by Simunic (1980) entitled

“The Pricing of Audit Services: Theory and

Evidence”, the independent variables used were

entity size, audit risk based on the current ratio,

quick ratio, debt-to-equity ratio, litigation risk, and

audit complexity. Meanwhile, the dependent

variable used was the audit fee. The results of this

study indicate that entity size, audit risk based on the

current ratio, quick ratio, debt-to-equity ratio,

litigation risk, and audit complexity have a positive

effect on the audit fee.

The second study was conducted by Suharli and

Nurlaelah (2008) with the title “Auditor

Concentration and Determination of Audit Fee:

Investigation at State Enterprise”. This study

examined the effect of concentration ratio, size of

the public accountancy firm (KAP), auditee size, and

subsidiary company against the audit fee. The results

obtained from this study indicate that concentration

ratio and auditee size have a significant relationship,

while the size of the CPA firm and the number of

subsidiaries have no significant relationship to the

audit fee.

Next, Herawaty (2011) conducted a study

entitled “The Influence of Internal Control and the

Time Budget of Audit on Audit Fee”. The results

obtained from this study reveal that partial internal

control has a positive influence on the audit fee.

Another study was conducted by Kusharyanti

(2012) with the title “Analysis of the Factors

Determining the Audit Fee”. The independent

variables used in this study were client size, audit

complexity, audit risk, audit committee, client’s

financial condition, size of the public accounting

firm, audit tenure, and audit specialization, while the

dependent variable used was audit fee. The results of

this study suggest that client size, audit complexity,

audit risk, audit committee, client’s financial

condition, and size of the public accounting firm

have a significant effect on the determination of the

audit fee, while audit tenure and audit specialization

do not have any significant effect in determining the

audit fee.

Jemada and Yeniartha (2013) conducted a study

entitled “Influence of Time Budget Pressure,

Complexity of Duties, and Reputation of Auditor to

Audit Fee at Public Accounting Firm in Bali”. The

results of this study show that time budget pressure,

task complexity, and the reputation of the auditor

positively and significantly affect the audit fee at a

public accounting firm in Bali.

Finally, Akhtarudin et al. (2016) examined

internal control deficiencies, opportunity investment,

and audit fees. The results show that the increment

of audit fee designates a supplemental cost that firms

should bear when they are growing and the internal

control mechanism is reported ineffectual.

Audit risk consideration is required in

international audit standards but the focus of this

research is whether components in audit risk such as

inherent risk, control risk, and detection risk are

respectively the responsibility of the auditor or

auditee because there are some risks that are

inherent to the auditor, and risks to which the

auditee is responsible, therefore, researchers want to

discuss this topic.

Therefore, this research intends to find out

whether audit risks such as inherent risk, control

risk, and detection risk can affect the amount of

audit fees offered by CPA firms.

2 THEORETICAL

BACKGROUND

2.1 Agency Theory

Agency theory is a theory composed by Jensen and

Meckling in 1976 that defines that there is an agency

relationship between two parties in which the first

party, as the principal, delegates the decision-

making authority to the second party, that is, the

agent. Agency theory refers to three basic

assumptions of humans: self-centeredness, limited

thought about the view of the future, and risk

aversion (Eisenhardt, 1989).

As Fachriyah (2011) assumes, an auditor is

trusted by the community as an independent party

who can provide assurance for client’s financial

statements. Since companies use the services of

auditors through public accounting firms in

providing independent opinions on financial

statements, there is a monitoring cost in the form of

external audit fees.

2.2 Audit Concept

An audit is an accumulation of evaluation activities

on evidence and information in determining and

reporting the level of conformity between stable

information and criteria, and audit procedures are

required to be performed by third parties who adhere

to the professional code of ethics (Arens et al.,

2011).

JCAE Symposium 2018 – Journal of Contemporary Accounting and Economics Symposium 2018 on Special Session for Indonesian Study

38

The general purpose of auditing, according to

Boynton and Johnson (2006), is to express an

opinion on fairness in all material respects, financial

position, and business results in accordance with

generally accepted accounting principles. The

purpose of the audit is specifically based on the

assertions that have been made and signed by the

management listed in the financial statements.

In preparing an audit plan, the auditor should

consider what audit risks are. Tuanakotta (2015)

defines audit risk as the risk of providing an

inappropriate audit opinion on mismanaged financial

statements.

According to SAS 47 (audit risk and materiality

in conducting an audit), audit risk is a risk arising

because the auditor unwittingly did not modify his

or her opinion properly on a financial statement

containing material misstatements.

The audit fee is defined as the amount of the

service fee received by the external auditor for the

performance of the audit work. The reward is related

to the amount of time spent in completing their

work.

In Indonesia, the Indonesian Institute of Certified

Public Accountants (IAPI) published the rules

regarding audit fees, No. KEP.024/IAPI/VII/2008. It

is explained that in setting the audit fee, CPA firms

must consider client needs, legal duties and

responsibilities (statutory duties), independence,

level of expertise and responsibilities attached to the

work performed, as well as the complexity of the

work and the amount of time required by members

and staff to complete the work.

2.3 Hypotheses Development

2.3.1 Inherent Risk and Audit Fees

According to Arens (2006), the correlation between

inherent risk and audit evidence is directly

proportional. The higher the inherent risk that the

client’s entity has, the more audit evidence it

obtains. Accordingly, the fee received by public

accounting firms also increases. Simunic (1980)

indicates that entity size, audit risk based on the

current ratio, quick ratio, debt-to-equity ratio,

litigation risk, and audit complexity have a positive

effect on audit fee.

H1: High inherent risk is associated with higher

audit fees.

2.3.2 Control Risk and Audit Fees

Akhtarudin (2016) suggests that internal control

affects the audit fee. Internal control is a component

of assessing control risk. When the control risk

obtained by the client’s internal control is getting

higher, the audit scope becomes more complicated.

Therefore, the audit fee obtained by CPA firms

should also be higher.

H2: High control risk is associated with higher

audit fees.

2.3.3 Detection Risk and Audit Fees

Detection risk is a risk of material misstatement that

auditors fail to detect due to improper use of audit

procedures. High detection risk can be prevented by

adequate planning and supervision and also the

implementation of audit engagement in accordance

with the professional standards of the CPA.

Adequate supervision and implementation of the

audit in accordance with the standards of quality

control are obtained from internal training and

participation in continuous professional training

provided by professional organizations and higher

costs are paid by CPA firms. Therefore, the audit fee

should also be higher.

H3: High detection risk is associated with higher

audit fees.

3 RESEARCH METHODOLOGY

The approach in this study is a quantitative

descriptive method through associative research.

The researcher decided to use the associative

research method to find correlations and causal

relationships among variables (Sulistyanto et al.,

2006). According to Sugiyono (2005), associative

research has the ability to discover the relationship

between two variables or more.

3.1 Population and Samples

The population used in this study includes auditors

working at CPA firms in East Java, Indonesia. Using

a purposive sampling method, 86 auditors in

manager and partner positions filled and returned a

questionnaire so data could be processed further.

3.2 Operational Definitions

3.2.1 Inherent Risk

Inherent risk is the risk of vulnerability to the

assertion, including transaction type, account

balance, or disclosure of material misstatement

before considering related controls (Tuanakotta,

Does Audit Risk Affect The Audit Fee?

39

2015). Inherent risk measurement uses a Likert scale

of 1–5 to indicate the level of agreement to a

statement. We are using a few indicators such as the

nature of the client’s business, findings from

previous audits, transactions with related parties,

non-routine transactions, consideration of some

accounts, the client’s financial condition, and client

integrity.

3.2.2 Control Risk

Control risk is a risk of vulnerability to the assertion,

including transaction type, account balance, or

disclosure of material misstatement that is not

prevented or detected and corrected by the client’s

internal control (Tuanakotta, 2015). Control risk

measurement is conducted on a Likert scale of 1–5

to indicate the level of agreement to a statement.

Control risk is measured by how far the auditors

gain knowledge and understanding of an entity’s

internal control and also perform tests of

effectiveness on these internal controls.

3.2.3 Detection Risk

Detection risk is a risk of material misstatement that

auditors fail to detect due to improper selection and

implementation of audit procedures. High detection

risk can be prevented by adequate planning,

supervision, and implementation of audit

engagement in accordance with the CPA’s

professional standards (Tuanakotta, 2015). The

measurement uses a Likert scale of 1–5 to indicate

the level of agreement to a statement. Detection risk

is measured by auditors misapplying audit

procedures, misinterpreting the audit results, or not

picking the testing method properly.

3.2.4 Audit Fees

According to Al-Shammari et al. (as cited in

Fachriyah, 2011), the audit fee is defined as a

remuneration received by the CPA firm for the audit

engaged by the auditor. The audit fees are influenced

by several factors including client size, profitability,

complexity, client internal control, or auditor factors

such as location, size, and auditor’s reputation. The

measurement uses a Likert scale of 1–5 to indicate

the level of agreement to a statement.

3.3 Data Analysis Method

The researcher proposed a causality model for the

data analysis method. To test this model, the

researcher used a causality analysis technique, a

structural equation model by using base variance or

partial least square (PLS). The researcher used the

PLS model because it shows the causality

relationship between a dependent variable and three

independent variables when one or two of the

variables have at least one indicator.

3.4 Outer Model Measurement

In the PLS analysis technique, the measurement uses

an outer model and inner model. In this research,

outer model measurement was used with a loading

factor value for each indicator. The reflective size

was correlated when the value was more than 0.7

with the high construct. The researcher used a 0.5

outer loading value for the initial stage of the

development of the measurement scale; an outer

loading value of 0.50 to 0.60 is considered sufficient

by Chin (1998).

3.4.1 Validity Test

A measurement scale is valid if the measurement

scale performs what should be performed and

measures what should be measured (Kuncoro,

2003). Validity can be assessed by comparing the

square root of the average variance extracted (AVE)

values for each construct, then the AVE value must

be greater than 0.30 (Formel & Larcker, 1981).

3.4.2 Reliability Test

The testing technique is composite reliability, which

measures a construct and can be measured by two

different sizes: 1) internal consistency, 2)

Chronbach’s Alpha (Ghozali, 2006). If the reliability

is above 0.70, the statement or indicator can be

declared reliable.

3.5 Inner Model Measurement

This testing method defines how big the influence of

the independent and dependent variables are. The R-

square value (R

2

) is used in this measurement.

3.6 Hypothesis Testing

The hypothesis test design proposed by the

researcher is based on the research objective of the

hypothesis T-test whose function is to assess the

influence of independent variables separately. The

confidence level used is 95%, so the level of

precision or limit of inaccuracy is α = 5% = 0.05

with table value. Hypotheses 0 is accepted and

JCAE Symposium 2018 – Journal of Contemporary Accounting and Economics Symposium 2018 on Special Session for Indonesian Study

40

Hypotheses a is rejected if the p-value is smaller

than the α value. On the other hand, Hypotheses 0 is

rejected and Hypotheses a is accepted if the p-value

is greater or equal to the α value.

4 RESULTS AND DISCUSSION

4.1 Outer Model Measurement Result

4.1.1 Validity Testing

All tested variables had a discriminant validity value

greater than 0.30 and a p-value less than the

significant level of 0.05. It can be concluded that all

variables are valid and reliable.

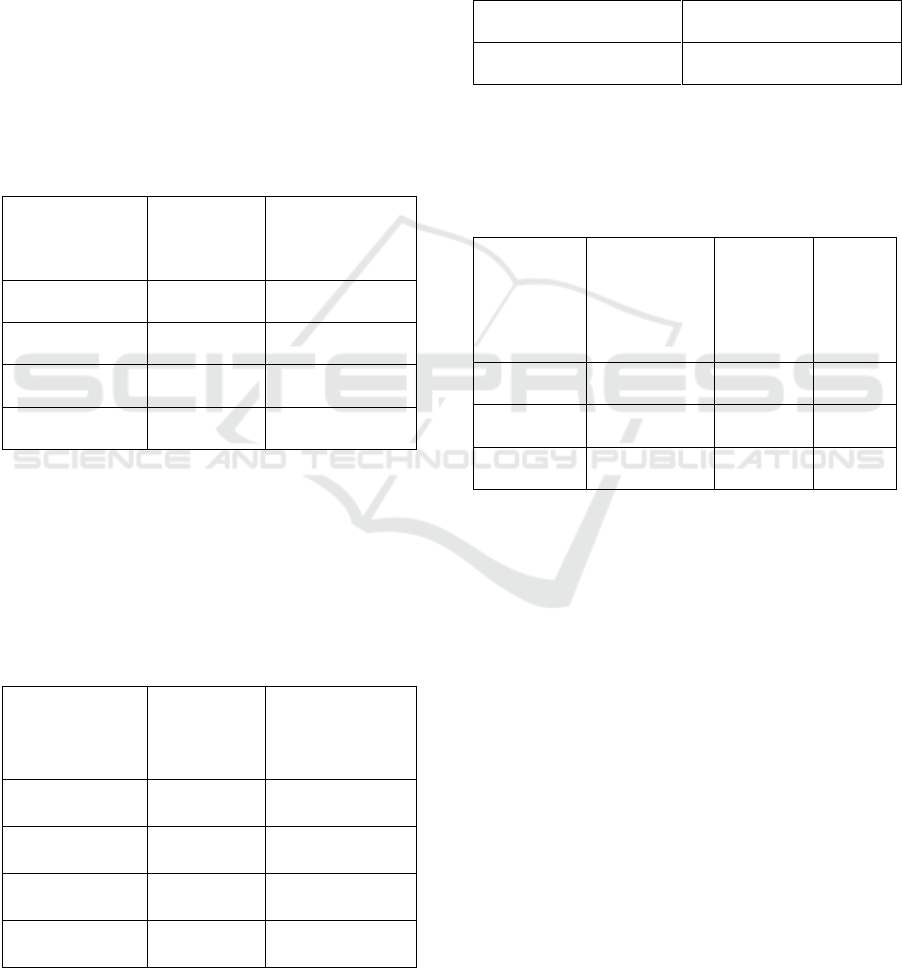

Table 1: Discriminant validity measurement results.

Variable

Original

Sampling

P-values

Inherent Risk

0.405

0.000

Control Risk

0.725

0.000

Detection Risk

0.701

0.000

Audit Fee

0.576

0.000

4.1.2 Reliability Testing

All tested variables had a composite reliability value

greater than 0.70 or had a p-value smaller than the

significant level of 0.05. Accordingly, it can be

concluded that the overall variables tested are

reliable for further testing and analysis.

Table 2: Composite reliability measurement results.

Variable

Original

Sampling

P-values

Inherent Risk

0.859

0.000

Control Risk

0.888

0.000

Detection Risk

0.874

0.000

Audit Fee

0.890

0.000

4.2 Inner Model Measurement Result

The audit fee variable had an adjusted R

2

value of

0.239. This figure shows that the audit fee service

variable can be explained by as much as 23.9% by

the independent variables used by the researcher

such as inherent risk variable, control risk variable,

and detection risk variable.

Table 3: Adjusted R

2

Value

Endogenous Variable

Adjusted R

2

Value

Audit Fee

0.239

4.3 Hypothesis Testing Results and

Discussion

Table 4: Statistical Test Results of Inter-Variable

Relationships.

Hypothesis

Original

Sample (O)

t-statistic

(|O/STER

R|)

p-

values

H1

0.217

2.292

0.022

H2

0.280

2.526

0.012

H3

0.183

1.687

0.092

In the PLS analysis technique based on the t-

statistic test, it can be concluded that the inherent

risk variable influences the audit fee based on p-

values of 0.022 (which is under 0.05). This result is

supported by Simunic’s (1980) studies. The second

variable tested is the control risk variable. It can be

concluded that the control risk affects the audit fee

based on p-values of 0.012, which is below the 0.05

significance level. According to the regression

coefficient value result of 0.280, it can be concluded

that control risk has a positive effect on the audit fee.

The same results are also supported by Akhtarudin’s

(2016) research. The last variable tested is the

detection risk variable. It can be stated that detection

risk does not affect the audit fee. This is because the

p-values are 0.092 (below 0.05). It can be concluded

that the detection risk has no effect on the audit fee.

This indicates that the third hypothesis that states the

detection risk has an effect on the audit fee is not

proven.

Does Audit Risk Affect The Audit Fee?

41

The results of this study indicate that inherent

risk and control risk affect the determination of audit

fees. This proves that inherent risk and control risk

become crucial factors in determining audit fees.

High control risk causes auditors difficulties in

detecting material misstatement due to a limitation,

that is, the weakness of the client’s internal control

system. Inadequate internal control implies that the

client has a high control risk. Hence, public

accounting firms should set a higher fee for a client

with higher level of control risk than for a client

with a moderate or low level of control risk.

On the other hand, the detection risk does not

affect the determination of the audit fee. The

detection risk arises from the failure of the auditor to

detect a material misstatement. Detection risk is

controlled entirely by the auditor. Therefore, the

auditor should reduce the detection risk to the

reasonable level since the detection risk is the

responsibility of the auditor.

5 CONCLUSIONS

The results of this study indicate that inherent risk

and control risk affect the determination of audit

fees. This proves that inherent risk and control risk

become crucial factors in determining audit fees. On

the other hand, detection risk does not affect the

determination of the audit fee. The detection risk

arises from the failure of the auditor to detect a

material misstatement.

Meanwhile, this study has several limitations.

First of all, the researcher only used samples from

CPA firms in East Java, so the results cannot be

generalized to other CPA firms. Secondly, not all

CPA firms in East Java were willing to fill out the

questionnaire. Moreover, the researcher only used

inherent risk, control risk, and detection risk as

independent variables in determining the audit fee,

while there are other factors that may also influence

the amount of the audit fee that are not included

such as client business risk, time budget pressure,

and auditor reputation.

REFERENCES

Akhtarudin, M. and Jonathan, O. (2016). Internal control

deficiencies, investment opportunities, and audit fees.

Int. J. Accounting and Finance. 6 (2).

Arens et al. (2012). Auditing and assurance services: An

integrated approach. 14

th

edn. New Jersey: Pearson –

Prentice Hall Inc.

Chin, W. (1995). Partial least square is to LISREL as

principal components analysis is to common factor

analysis. Technology Studies, 2, 315-319.

Eisenhardt, M. (1989). Agency theory: An assessment and

review. Academy of Management Review. 14 (1), 57-

74.

Fachriyah, N. (2011). Faktor-faktor yang Mempengaruhi

Penentuan Fee Audit oleh Kantor Akuntan Publik di

Malang. Unpublished thesis. Malang: Universitas

Brawijaya.

Ghozali, I. (2006). Aplikasi analisis multivariate dengan

program SPSS. Semarang: Badan Penerbit Undip.

Herawaty, N. (2011). Pengaruh pengendalian intern dan

lamanya waktu audit terhadap fee audit (Studi kasus

pada KAP Kota Jambi dan Palembang). Jurnal

Penelitian Universtas Jambi Seri Humaniora ISSN

0852-8349. 13 (1), Januari-Juni 2011, 07-12.

Jemada, V. and Yaniartha, S. (2013). Pengaruh tekanan

anggaran waktu, kompleksitas tugas, dan reputasi

auditor terhadap fee audit pada kantor akuntan publik

(KAP) di Bali. E-Jurnal Akuntansi Universitas

Udayana ISSN 2302-8556. 3 (3), 132-146.

Jensen, C. and Meckling, H. (1976). The theory of the

firm: Managerial behavior, agency cost, and

ownership structure. Journal of Financial Economics.

3(4), 305-360.

Keputusan Institut Akuntan Publik Indonesia Nomor:

024/IAPI/VII/2008 tentang Kebijakan Penentuan Fee

Audit. Tanggal 2 Juli 2008.

Kusharyanti. (2012). Analysis of the factors determining

the audit fee. Jounal of Economics, Business, and

Accountancy Ventura. 16 (1), April 2013, 147-160.

Simunic, A. (1980). The pricing of audit services: Theory

and evidence. Journal of Accounting Research. 22 (3),

161-190.

Sugiyono. (2005). Metode penelitian pendidikan:

Pendekatan kuantitatif, kualitatif, dan R&D. Bandung:

ALFABETA.

Sulistiyanto, S. and Susilawati, C. (2006). Pedoman

penulisan skripsi. Semarang: Penerbit Universitas

Soegijapranata dan Pusat Pengkajian dan

Pengembangan Akuntansi.

Suharli, M. and Nurlaelah. (2008). Konsentrasi auditor

dan penetapan fee audit: Investigasi pada BUMN.

JAAI. 12 (2), Desember 2008, 133-148.

Tuanakotta, T. (2013). Audit berbasis ISA. Jakarta:

Salemba Empat.

Tuanakotta, T. (2015). Audit kontemporer. Jakarta:

Salemba Empat.

JCAE Symposium 2018 – Journal of Contemporary Accounting and Economics Symposium 2018 on Special Session for Indonesian Study

42