Making the Cloud Work for Software Producers: Linking

Architecture, Operating Cost and Revenue

Pierangelo Rosati

1

, Frank Fowley

1

, Claus Pahl

2

, Davide Taibi

3

and Theo Lynn

1

1

Irish Centre for Cloud Computing and Commerce, Dublin City University, Dublin, Ireland

2

Faculty of Computer Science, Free University of Bozen-Bolzano, Bolzano, Italy

2

Laboratory of Pervasive Computing, Tampere University of Technology, Tampere, Finland

Keywords: Cloud Migration, Total Cost of Ownership, Monetization, Architecture Migration, Software Producer.

Abstract: Cloud migration is concerned with moving an on-premise software system into the cloud. In this paper, we

focus on software producers adopting the cloud to provide their solutions to enterprise customers. Their

challenge is to migrate a software product, developed in-house and traditionally delivered on-premise, to an

Infrastructure-as-a-Service or Platform-as-a-Service solution, while also mapping an existing traditional

licensing model on to a cloud monetization model. The analysis of relevant cost types and factors of cloud

computing generate relevant information for the software producers when deciding to adopt cloud computing,

and defining software pricing. We present an integrated framework for informing cloud monetization based

on operational cost factors for migrating to the cloud and test it in a real-life case study. Differences between

basic virtualization of the software product and using fully cloud-native platform services for re-architecting

the product in question are discussed.

1 INTRODUCTION

Cloud computing is increasingly the computing

paradigm of choice for enterprises worldwide. Cloud

computing is particularly attractive from a business

perspective since it requires lower upfront capital

expenditure, and improves operational and organiza-

tional efficiencies and agility (Armbrust et al., 2010;

Leimbach et al., 2010; Marston et al., 2011; Berman

et al., 2012). Similarly, from a technical perspective,

the benefits of the cloud are well documented

including on-demand, self-service, resource pooling

and rapid elasticity (Armbrust et al., 2010).

Notwithstanding these benefits, cloud computing

adoption also generates significant challenges for

software producers (SPs), particularly for those

offering a Software-as-a-Service (SaaS) model. SPs

typically migrate their software to a third-party

platform (Infrastructure-as-a-Service – IaaS – or

Platform-as-a-Service – PaaS) and their customers

access it from this new multi-tenant architecture. In a

cloud environment both SPs and their customers are

typically charged on a pay-per-use or subscription

basis. Furthermore, SPs do not have control of

customers’ service usage; in such a context, it is

crucial for SPs to identify the right architectural

configuration to meet service level agreement (SLA)

obligations at the minimum cost. Being charged on a

per-use basis also represents a radical change in the

producers’ cost and revenue models and introduces

additional uncertainty in cash flow forecasting

(Dillon et al., 2010). Furthermore, the actual cost of

the migration process might be substantial for SPs

and for their legacy customers, while nonexistent for

cloud-native SPs. According to the Cloud Native

Computing Foundation, modern cloud-native

systems have the following properties:

container-packaged;

dynamically managed by a central

orchestrating process;

microservice-oriented.

Cloud-native architectures have technical

advantages in terms of isolation and reusability, thus

reducing cost for maintenance and operations. PaaS

clouds with their recent support for containerized

microservice architectures are the ideal environments

to create cloud-native systems.

While the service and payment/revenue model are

the same in both scenarios, the total cost of ownership

(TCO) is substantially different due to the migration

costs. Rationally, SPs should offer their software at a

higher price to compensate their migration costs,

364

Rosati, P., Fowley, F., Pahl, C., Taibi, D. and Lynn, T.

Making the Cloud Work for Software Producers: Linking Architecture, Operating Cost and Revenue.

DOI: 10.5220/0006679303640375

In Proceedings of the 8th International Conference on Cloud Computing and Services Science (CLOSER 2018), pages 364-375

ISBN: 978-989-758-295-0

Copyright

c

2019 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

however this may not always be competitively

feasible or desirable.

While architectural challenges in migration have

been ad-dressed (Jamshidi et al., 2013; Pahl and

Xiong, 2013), research exploring the link between

cloud architecture and TCO, and therefore on pricing

cloud services from an SP perspective is lacking.

The main objective of this paper is to explore the

impact of two cloud architectural options, IaaS (basic

virtualization) and PaaS (cloud-native), on SPs’

operating costs. We present an initial framework for

operating cost factors and dependencies, and a

practical process for architecture-related cost

estimation.

This paper is organized as follows. Section 2

reviews related work and presents the cloud migration

context. Section 3 introduces the overall framework

and process. Sections 4 and 5 focuses on the IaaS- and

PaaS-based cost calculation respectively. In Section

6, we validate and illustrate our contribution using a

case study. We end with some conclusions and

observations for future research.

2 ARCHITECTURE MIGRATION

CONTEXT

2.1 Context and Related Work

Traditionally, enterprise software was licensed under

a packaged, perpetual or server license, and

customers were typically required to purchase

technical support and maintenance packages for a

predefined period (Ferrante, 2006). The cost of

software development, production and marketing was

offset against the license fees, typically paid upfront

by the customer.

The introduction of cloud computing accelerated

the adoption of two new licensing models:

subscription and utility-based licensing. The former

involves an enterprise customer purchasing a license

for a pre-defined time period whereas the latter

involves charging the customer on a pay-per-use

basis. Key advantages for the enterprise customer

include (i) less upfront expenditure in licensing and

(ii) no additional fees for fixes, upgrades or feature

enhancements (Ferrante, 2006). The shift from a

product orientation to a service orientation is a

significant disruption for SPs, not only from a

strategic perspective but also from a cost- and

revenue- recognition perspective. Cost and revenues,

indeed, are spread over time and producers do not

receive additional fees for upgrades. This resulted in

a significant business model readjustment (DaSilva et

al., 2013). Such changes do not apply to cloud-native

SPs such as start-ups. Giardino et al. (2015) observe

that cloud computing is particularly beneficial for

start-up companies since it significantly lowers the

initial investment in IT infrastructure.

Cost savings are a major factor in cloud adoption

(CFO Research, 2012; Bain and Company, 2017),

however ex-ante TCO estimation is not

straightforward due to the presence of long-term and

hidden costs of operating in the cloud which tend to

be ignored or underestimated (ISACA, 2012). From

an SP perspective, this represents a major concern

since properly mapping the costs of the cloud

represents the basis for adequate and effective pricing

strategies. This process has become more and more

important for SPs due to increasing competition in the

cloud environment, where SPs are sometimes forced

to deliver services whose costs exceed revenues

(Durkee, 2010).

TCO is the most adopted costing model in both

research and practice (Strebel and Stage, 2010) and

has been defined as “a procedure that provides the

means for determining the total economic value of an

investment, including the initial capital expenditures

(CapEx) and the operational expenditures (OpEx)”

(Filiopoulou, 2015, p. 278). TCO estimation

frameworks used for traditional on-premise

infrastructure need to be adapted to the cloud world

to reflect different cost drivers (Martens et al, 2012;

Walterbusch et al, 2013).

Strebel and Stage (2010) applied a TCO-based

decision model for business software application

deployment, while running simulations on hybrid

cloud environments. The decision model only

included a comparison of operational IT costs, such

as server and storage expenses and the external

provisioning by means of cloud computing services.

Reference (Li et al., 2009) formulated a TCO model

and identified the factors involved in the utilization

cost. This model consists of the total cost of all

servers and resources used to provide the service.

Cloud implementation and operating costs were

divided into eight different categories that mainly

represent fixed costs, such as setting-up and

maintenance costs that providers need to bear during

the whole lifecycle. Ilan (2011) presents a cost

comparison between virtual managed nodes and local

managed servers and storage, but neglects important

cost components like licenses, training, licensing and

maintenance. Finally, Walterbusch et al. (2013)

presents a comprehensive TCO model for the three

main cloud service models (i.e. IaaS, PaaS and SaaS),

and map into their model different cost components

Making the Cloud Work for Software Producers: Linking Architecture, Operating Cost and Revenue

365

across four phases of cloud computing, i.e., initiation,

evaluation, transition, operation. Costs related to

system failure and backsourcing or discarding are

listed but not included in the model since they are, by

their nature, contingent to situation contexts and

therefore difficult to translate in a mathematical

formula.

Despite the large number of studies on software

architecture-related factors for consideration in

migration, and, likewise, the large number of studies

related to TCO for cloud computing, there is a lack of

papers seeking to estimate the TCO for cloud

migration in conjunction with architecture concerns.

The extant literature is typically focused on ex-post

calculation of costs and profits independently from

the wider situational context, and typically considers

only cloud operational cost. For example,

Andrikopoulos et al. (2013) proposes a decision

support system which includes a cost calculator based

on per-use cost components only. Jinesh (2010)

presents a TCO estimation of migrating to Amazon

Web Services (AWS) that includes per-use charges

only. Similarly, Anwar et al. (2015) examine cost-

aware cloud metering for scalable services.

2.2 Two Migration Business Cases

Cloud computing adoption can dramatically change a

company business model and internal organization,

and requires investing a significant amount of

resources in the migration process. In such a context,

an ex-ante evaluation of costs and potential benefits

that such an investment may generate is crucial for

effective decision-making. In this paper, we consider

two discernible migration business types:

The migration of existing legacy customers

with perpetual licenses;

New customers with no existing economic

relationship with the SP.

In the first case, there is a significant post-migration

discontinuity in the vendor-customer relationship and

the nature of the billing. From the customer

perspective, the business case can be made by

comparing the as-is and the to-be solution, however

this is anything but a trivial process (ISACA, 2012).

There may be time, effort and additional hidden costs

related to the migration that need to be included in the

ex-ante evaluation and recovered by both SPs and

their customers (ISACA, 2012). In the second case,

customers can make their choice on the basis of the

perceived value of the service per se. In both cases a

key consideration for SPs is the amount of cost they

can sustain to generate a positive margin on their sale

over a defined time period.

TCO is used to estimate the cost of cloud investments

from the initial sourcing through to the end of the

cloud usage, whether that is the backsourcing of

information, or the client switching to other services

or providers. While the measured nature of the cloud

allows for a detailed ex-post cost analysis, ex-ante

cost estimation can be complicated due to the

uncertainty associated with multi-tenancy and

resource pooling. Similarly, while there are clear cost

savings in cloud computing there are also intangible

cost components which are more difficult to estimate

(ISACA, 2012).

By its very nature, cloud computing enables

enterprise customer scale up and down on-demand

without the ties associated with a substantial upfront

investment. Thus, forecasting the customer lifetime

(and associated value) for a cloud customer can be

difficult. Suddenly, they can leave or radically modify

their usage, since switching costs in the cloud are

significantly lower than on-premise. Notwithstanding

this, enterprise customers and SPs require a practical

approach to measuring cloud TCO.

3 INTEGRATED MIGRATION

FRAMEWORK AND PROCESS

Typically, a cloud migration is organized around an

architectural transformation of the legacy system,

independent of cost and pricing considerations. We

propose an integrated process for migration planning:

Analyze and model: use a set of migration

patterns to determine structural cloud

architecture aspects;

Right-scaling: conduct a feasibility study to

validate quality requirements such as

scalability;

Right-pricing: determine pricing for the

software service based on analysis of direct

operational costs driven by predicted usage and

experimental consumption figures generated

from the feasibility study.

While a comprehensive discussion of cloud migration

patterns, processes and issues are presented in

Jamshidi et al. (2014) and Taibi et al. (2017), right-

scaling and pricing need further discussion.

3.1 Problem 1: Right-Scaling of SaaS

Software

SPs seeking to migrate to the cloud need to find the

right architectural configuration to meet the necessary

service level agreement (SLA) obligations at the

CLOSER 2018 - 8th International Conference on Cloud Computing and Services Science

366

minimum cost. Therefore, a key question for a

decision maker is: how many components can I host

on a fixed cloud compute resource with a pre-defined

latency performance target for a forecasted number of

users of a particular application with a forecasted mix

of application operation usage?

Changes in usage require changes in the number

and/or configuration of cloud resources used, which

may result in additional costs. Estimation of the

expected usage level or patterns is needed to predict

when scaling, and related additional costs, may occur.

Furthermore, storage and networking charges are akin

to commodities that can be consumed on a per-unit of

usage basis. The compute costs are more difficult to

predict since they are determined by the users’ use of

the application. In this paper, we consider a virtual

SLA-backed service that is not entirely fixed in terms

of computational and storage resources allocated.

Finally, the actual capacity of the offered cloud

service may fluctuate over time affecting potential

economies of scale and application performance.

Only the cloud service provider, and not the SP, can

monitor the underlying service availability thus, the

first problem is right-scaling i.e., to size a predicted

workload to a machine (configuration) profile. This

requires usage prediction to configure IaaS or PaaS

through an experimental pre-migration feasibility

study, and represents the basis for an accurate

estimation of operational costs. For SPs, right-scaling

reduces overprovisioning and therefore usage cost of

their cloud infrastructure.

3.2 Problem 2: Right-Pricing of

SaaS-delivered Products

Monetization refers to how organizations capture

value i.e. when, what and how value is converted into

money (Baden-Fuller and Haefliger 2013). Despite

the fact that how SPs price and monetize their cloud

offering is beyond the scope of the TCO framework

adopted in this paper, it is important to understand as

the TCO represents a critical component of SPs’

pricing decision. A monetization framework for SPs

usually comprise three models, namely:

Architecture model: the source and target

architecture need to be considered together

with planned changes in functional or non-

functional properties;

Cost model: the expected direct operational

costs need to be estimated including basic

infrastructure and platform costs, additional

features for external access and networking,

internal quality management, and development

and testing costs, and mapped into the TCO

estimation;

Revenue model: expected revenues based on a

selected pay-per-use or subscription model.

From an SP perspective, the relationship between

cloud cost and price (P) can represented as follows:

=×

1+

(1)

Where μ represents the percentage of profit the

producer aims to obtain. Understanding how SaaS

usage translates in to IaaS costs is of primary

importance for SPs since the SaaS income should

cover the corresponding infrastructure costs. The

interplay between these three models ultimately

determines the attractiveness of the cloud offering of

an SP in the marketplace.

Relevant questions are: (a) which factors are static

and might be considered as a baseline for the cost

calculation? (b) What are the additional costs for

scaling up beyond the baseline? And (c) what is the

best combination of cost and revenue model that

maximize profit in the short- and long-term?

3.3 Total Cost of Ownership and Cost

Factors

TCO in a strict sense, is the sum of the initial

investment required to purchase an asset (CapEx)

plus the operating costs that the cloud generates

(OpEx). When choosing among alternatives, SPs

should look at both components of TCO to evaluate

the investment properly. Migration costs tend to be

omitted in cloud TCO estimations even though they

can be substantial and change the overall return on

investment. TCO calculation can be formalized as

follows:

= +

(2)

In the context of our study, OpEx includes fixed

(e.g. location and size) and variable (i.e., usage) IaaS

Cost components while CapEx includes migration

and implementation costs (e.g. development and

testing, project management etc.). Walterbusch et al.

(2013) provide a comprehensive list of cost

components that may be considered for estimating

TCO of SP cloud migration.

In order to estimate the cost associated with the

expected SaaS usage, we consider costs at the SP

level. In terms of IaaS operational costs for an SP we

focus on compute, storage and network resources

since they usually represent the most significant cost

components. IaaS costs can be categorized as (i) fixed

(size, availability, location, and other supplemental

and/or premium services), or (ii) variable (i.e., usage

of all respective IaaS resources). Like other fixed cost

factors, reconfiguration is possible, but not

considered in this paper. Availability is considered as

a contractually guaranteed property and it is assumed

to be fixed.

Making the Cloud Work for Software Producers: Linking Architecture, Operating Cost and Revenue

367

4 IaaS COST CALCULATION

PROCESS

The nature of the cloud makes it difficult to determine

the input variables of the TCO model, but, we will

see, architecture quality concerns such as

performance and availability can drive this process.

Cloud architecture qualities, and corresponding costs,

can be influenced by compute, storage and network

resources. Figure 1 summarizes the cost estimation

process that we will now apply.

Figure 1: Costing SaaS Usage - Estimation Process.

4.1 Cost Estimation Process

In a cloud migration scenario, an SP needs to migrate

the system architecture of the product and change the

corresponding cost and revenue models at the same

time. As highlighted before, the new models heavily

depend on expected or predicted usage, both of which

are difficult to estimate. In fact, any estimation of

SaaS usage volumes will determine IaaS usage

requirements but customers’ usage can be subject to

temporary peaks that might generate spikes in costs

due to ineffective IaaS usage.

Estimation complexity varies between the two

business cases identified earlier, i.e., migrated or

cloud-native application. Usage patterns of the

existing customer base can be determined with

reasonably high accuracy, as opposed to an expansion

into a new a customer base with unknown behavior.

process for costing a SaaS service from an SP

perspective. The initial two phases are about usage

estimation at both the SaaS and IaaS level. SaaS

usage can be mapped onto IaaS by experimental

means using feasibility studies or other mechanisms.

A third phase is concerned with IaaS cost estimation,

which is driven by the usage estimation and SLA

obligations. IaaS configuration heuristics can be used

to identify the most efficient infrastructure

configuration. The fourth and final phase is related to

pricing the SaaS service based on the outcome of the

previous stages.

4.2 Architecture Selection and

Cost/Revenue Prediction

From an SP perspective, the selection criteria of a

cloud provider include fees and billing model. Many

IaaS providers offer monthly basic subscription fees

with additional fees for premium services such as

scalability, access (e.g., IP endpoint, network

bandwidth) or monitoring and advanced self-

management. An SP requires a clear comparison of

costs and revenues resulting from the cloud adoption.

This has to be an “apples to apples” comparison

(ISACA, 2012). Even though we primarily discuss

IaaS, similar assumptions can be made for PaaS

services. PaaS-level costs need to address both

development and deployment and need to be aligned

with SaaS-level income.

4.3 Heuristics – Resource Cost

Modeling and Right-Scaling

In order to make this more practically relevant, we

can look at the different resource types and compare

them in terms of utilization and cost fluctuations in

common deployments (and resulting impact on cost

estimation).

Cost modeling for compute versus storage services

are fundamentally different. Storage is more

predictable and current cloud service pricing models

support a commodity-style costing. Compute cost is

more complicated to predict and contributes

disproportionately to the achievement of economies

of scale. SPs need to make configuration assumptions

which may or may not prove to be accurate. Scenario

analysis may help to achieve better estimation.

For illustration purposes, a simple initial

configuration of IaaS resources could be based on 80

percent reserved and 20 percent on-demand instances.

This combines reliable core provisioning without

overprovisioning for extra demand (in which case on-

demand instances are acquired). The benefits of this

strategy are:

60-80 percent utilization of used instances is

achievable if the reserved instances deal with

peak demand;

Up to 50 percent cost reduction compared to

on-demand instances only.

Another factor impacting resource requirement is the

nature of the architecture. Stateless, loosely-coupled

architectures help accommodate extra demand and

enable scalability by just using additional resources

on-demand without much start-up costs (transfer of

state to other resources).

4.4 An Exemplar Pricing Model

In order to understand pricing models of IaaS and

PaaS providers, we report exemplar categories and

common pricing models (Table 1). This is largely

Estimate

SaaS Usage

Estimate

I/PaaS Usage

Cost I/PaaS

Usage

Cost SaaS

Usage

CLOSER 2018 - 8th International Conference on Cloud Computing and Services Science

368

built on Azure pricing information, but is typical of

other providers.

Relevant pricing models focus primarily on storage in

GB and transactions (read/write). A proper estimation

of IaaS costs associated with a SaaS application

provisioning is needed in order to (i) select the

technically best option, and (ii) estimate the costs for

hosting the SaaS application, for example, in a PaaS

cloud. Quality concerns other than the expected

workload (e.g. availability expectations, failover

strategy etc.) have to be considered in the process as

well. Effectively, the estimation process needs to

include the number of storage units and total size as

an input, and the costs, estimated over a defined

period, with predicted growth, and for different

replication options as an output.

Table 1: Storage Cost Component.

Component Description

Region Slightly different rates might apply per

region (relevant if data location

regulations apply).

Replication It is a mechanism to deal with down-

time and increase reliability. Sample

configurations:

Local Redundant – a number of copies

of data, all in the same data-center and

region of the storage account, across

different fault or upgrade domains.

Zone Redundant – a number of copies

of data, all in different data-centers,

which has slightly less throughput than

Local redundancy.

Geo Redundant – a number of copies of

data, all in different data-centers, with a

back-up, separate multiple saves in a

specific secondary region to allow to

recover from Region failure.

Read-Only Geo Redundant – the same

as geo redundancy with read access to

secondary data.

All replication operations are done

asynchronously.

Size It depends on actual amount of Gbytes

stored.

Transactions Number of Read/Write Blob

Operations.

Data Transfer It is measured. Sample costing:

Data Ingress Network Data Transfer is

free.

Data Egress Network Data Transfer is

free if in the same region.

Data Egress Data Transfer between

regions or out of a region is charged.

A further complication is that pricing models between

platform providers are difficult to compare due to

different definitions of price components.

Consequently, a formal and clear estimation

framework for an economic evaluation of different

solutions to deliver a SaaS service is needed.

5 CLOUD-NATIVE PaaS

ARCHITECTURE MAPPING

In the previous section, we discussed the

implementation of a SaaS product on an IaaS set of

services. Now we consider the adoption of PaaS to

provision a SaaS product. We assume here a

migration to a PaaS architecture to be cloud-native in

style, i.e., platform services, such as databases, are

provided as packaged services in a microservice style.

The migration to PaaS is more demanding

particularly where many native PaaS services are

used. Notwithstanding this, the cost estimation may

be easier. This will also further clarify the impact of

cloud software architecture on costs and revenues.

5.1 PaaS Migration

From an SP perspective, a PaaS solution has two main

benefits: (i) development costs can be mapped and

associated with the migration, and (ii) more accurate

estimation of deployment costs.

An important consideration for SPs is whether to fully

adopt the cloud as both a delivery and a development

platform. While moving software development to a

PaaS cloud allows software producers to further

reduce upfront capital expenditure, it may limit

technical options in the future. Another important

consideration is whether to have a staged migration.

Through basic virtualization, a simple VM-based

IaaS solution might emerge. The ultimate objective

would be to move from VMs to so-called cloud-

native applications at the platform level that utilize

fully cloud-based services for development and

deployment. Consequently, this provides a more

metered and granular cost model.

5.2 Staged Migration Towards

Cloud-Native

For illustration purposes, we assume that the SP

wishes to migrate a traditional stacked application

with application, middleware, DBMS and disk

storage support that runs in an on-premise setting, to

Making the Cloud Work for Software Producers: Linking Architecture, Operating Cost and Revenue

369

the cloud. A stepwise migration from on-premise via

IaaS into a PaaS cloud can happen as follows:

Phase 1 – IaaS Compute Architecture: The

application can be packaged into VMs. License

fees for components of the application are

incurred as usual. The business problem is

scaling out; adding more VMs means adding

more license fees for every replicated

component. From a technical point of view,

multiple copies of data storage that are not in

sync might cause integrity problems.

Phase 2 – DaaS Storage: Refactor and extract

storage i.e. use a virtual data-as-a-service

(DaaS) solution for storage needs. This

alleviates the technical integrity problem cited

above.

Phase 3 – PaaS Cloud Data Storage: Package

the whole DBMS into single virtual machine.

This alleviates the business license fee problem

for the DBMS and simplifies data management,

but other license fees may still occur.

Phase 4 – Full Application Migration: Migrate

to a PaaS service. Apart from solving technical

problems, this significantly mitigates the

licensing fees issue.

This process results in a so-called cloud-native

application, which is scalable/elastic, clusterable,

multi-tenancy, pay-per-use, and self-service.

6 ILLUSTRATION AND

VALIDATION – CASE STUDY

We now illustrate the estimation process presented in

Section V using a case study. The estimation process

was applied to an SP migrating a legacy client-server

on-premise single-tenant enterprise application to the

cloud by re-designing, re-engineering and recoding

the system as a cloud application. The SP is a small-

medium enterprise which provides a document

management application. Its application has over

1,000 existing client installs and in this case study, we

present the TCO estimation of migrating 240 of these

to the new cloud platform over a 3-year period. The

main business requirements for the SP to adopt the

cloud were (i) to pursue flexibility across different

devices and situational contexts, and (ii) to increase

the customer base through new market entries. The

solution requires meeting high-volume data storage

and processing needs.

6.1 Application Overview

The application is a Document Management System

(DMS), which enables a user to scan paper documents

from enterprise-grade scanners and save them on a

cloud store as electronic images. Documents are

classified under custom types, such as invoice or

delivery docket, and specific metadata templates are

used to store searchable tagged data against the

documents for future retrieval and reporting. The

application has been designed and coded specifically

to run as a cloud application on the Microsoft Azure

public cloud platform.

6.2 TCO Calculation

The TCO is made up of the implementation costs of

the new cloud application and the cloud charges

incurred in running the new system on Microsoft

Azure.

Estimated implementation costs (CapEx) were

classified into seven implementation phases:

Business Analysis, Cloud Architecture Design, Data

Design, Security Framework Design, Development

and Test, Performance and Costs Analysis. It should

be noted that the calculations do not include the

operational costs of migrating the customers to the

new cloud web application.

The application is a multi-process system since it

comprises a web server compute resource and a

separate image processing compute resource.

However, the functional dependency between these

do not need to be considered in the TCO analysis

since the image processing worker VM acts

completely asynchronously to the web server role

web requests which continue regardless of the state of

the image processor. Therefore, we have calculated

the multi-tenant VM requirements based on a simple

linear multiplication of the CPU load per tenant.

IaaS usage charges (OpEx) are estimated considering

the two most relevant cost components:

A cloud data store – made up of a NoSQL Table

structure (using the Azure Table service) and

an object store (using the Azure Blob Storage

service). Table and blob storage are platform

services that allow a more fine-grained costing.

As such, these need to be considered on an

individual service base.

A cloud compute architecture – made up of a

separate compute resource for the web server

of the web application (Web Role Virtual

Machine), and a separate compute component

for carrying out the image processing

functions, such as barcode reading (Worker

Role Virtual Machine).

Our calculation is based on the Azure services pricing

reported in Tables 2, 3, and 4. In order to forecast the

CLOSER 2018 - 8th International Conference on Cloud Computing and Services Science

370

usage of cloud storage resources, we used actual

historical data over an eleven-month period from an

existing average-sized tenant with a typical

application usage pattern. To estimate the computing

resources required, we monitored the usage and

performance statistics during a snapshot of the

operational use of the application by the same typical

user. Tables 5, 6, and 7 summarize the usage profile

adopted in the calculation.

Table 2: Blob Storage Prices.

Service Redundancy Cool Tier

General

Purpose

Price per

GB/Month

space

Local € 0.013 € 0.020

Geo € 0.025 € 0.041

Price per

10,000

transactions

Local € 0.084 € 0.003

Geo € 0.169 € 0.003

Price per

GB data

access

write

Local € 0.002 -

Geo € 0.004 -

Table 3: Table Storage Prices.

Price per

Entity/GB/Month

Local Redundant € 0.059

Geo Redundant € 0.085

Price per 10,000

transactions (PUT)

Local Redundant € 0.003

Geo Redundant € 0.003

Table 4: Compute Prices.

VM

Type

No. of

CPU

Cores

Annual

cost

Azure

VM (€)

VM

Type

No. of

CPU

Cores

Annual

cost Azure

VM (€)

a1 1 602.4 d4 8 8,937.00

a2 2 1,204.68 d1 v2 1 1,114.32

a3 4 2,409.36 d2 v2 2 2,236.20

a4 8 4,818.60 d3 v2 4 4,464.72

d1 1 1,114.32 d4 v2 8 8,937.00

d2 2 2,236.20 d5 v2 16 17,873.88

d3 4 4,464.72

Table 5: Usage Profile of a Typical Tenant.

Total Number of Scanned Documents per

annum

145,853

Average Document Table Entities per Month 14,675

Peak Entities per Day 3,551

Peak Entities per Hour 1,137

Average Table Entity Size in Bytes 2,160

Average Scanned Image File Size in KB 666

Average Template File Size in Bytes 2,200

Table 6: Forecasted Input Parameters.

Per Tenant End of Year

1 2 3

No. of documents 176,105 352,210 528,314

Document table size

(GB)

0.380 0.761 1.141

No. of image blobs 176,105 352,210 528,314

Image blobs size (GB) 117 235 352

Document Template

File Blobs

2 3 6

Total Template blob

storage (bytes)

4,400 8,800 13,200

Table 7: Summary Parameter Values.

Web Role Peak CPU Load 67.1%

Web Role Average CPU Load 31.5%

Worker Role Peak CPU Load 24.3%

Worker Role Average CPU Load 10.4%

6.3 Experimentation – Usage and Cost

Table 8 summarizes the estimated implementation

and migration costs for the SP (€168,647). The most

significant cost component, which represents 47.83%

of the overall migration costs, is by far consultancy

costs for design and development, followed by

security design (16.15%). Such a significant amount

of upfront migration costs further highlights the need

to include such costs into TCO estimation to inform

both adoption and pricing decisions.

Table 8: Migration and Implementation Costs.

Implementation Phase Cost (€)

Implementation Consultancy Costs –

Business Analysis (Contract hours)

16,078

Implementation Consultancy Costs –

Security Design (Contract hours)

27,237

Implementation Consultancy Costs –

Design and Development (Contract hours)

80,662

Project Management and Implementation

Design (Staff Salaries)

16,265

Development and Testing (Staff Salaries) 17,465

Non-Staff or Non-Contractor Costs

(Cloud Testbed subscription, test

equipment, travel)

10,940

Total 168,647

Tables 9, 10, and 11 summarize IaaS usage costs

estimated as a linear combination of usage parameters

and price of each service.

Making the Cloud Work for Software Producers: Linking Architecture, Operating Cost and Revenue

371

Table 9: Blob Storage Costs.

Costs per

tenant

Space Cost (€)

Transactions Cost

(€)

Redundancy Local Geo Local Geo

End year 1 8.87 17.80 1.48 2.97

End year 2 26.60 53.41 1.48 2.97

End year 3 44.33 89.02 1.48 2.97

Data Access

Write Cost (€)

Total Cost (€)

Redundancy Local Geo Local Geo

End year 1 1.48 2.96 11.83 23.73

End year 2 4.43 8.87 32.52 65.25

End year 3 7.39 14.78 53.21 106.77

Note: Blob storage costs for template files were ignored due to their

negligible amount.

Table 10: Table Storage Costs.

Costs

per

tenant

Space Cost

(€)

Transaction

s Cost (€)

Total Cost

(€)

Redund. LR GR LR GR LR GR

End

year 1

0.13 0.19 0.05 0.05 0.19 0.25

End

year 2

0.40 0.58 0.05 0.05 0.46 0.63

End

year 3

0.67 0.97 0.05 0.05 0.73 1.02

Note: LR (Local Redundant); GR (Geo Redundant); Redund.(Redundancy)

Table 11: Compute Costs.

End

year

Clients

migrated

Number

of VMs

(WeR)

Number

of VMs

(WoR)

Storage

Costs

(LR) (€)

1 80 5 2 946

2 80 14 5 3,548

3 80 24 8 7,805

Storage

Costs

(GR) (€)

Compute

Costs

(WS) (€)

Comput

e Costs

(IP) (€)

1 80 1,898 11,181 4,473

2 80 7,118 31,307 11,181

3 80 15,660 53,669 17,890

Note: WeR (Web Role); WoR (Worker Role); LR (Local Redundant); GR

(Geo Redundant); WS (Web Server VMs);IP (Image Processing VMs).

The use case we present in this paper involves a

significant image-processing component resulting in

high upload- and download- volumes and the in-cloud

processing of images. The most critical challenge at

the architectural level was to select the optimal

Virtual Machine type from the available types on the

Azure platform; we carried out a benchmark study of

the performance of the different “flavors” of the role

VMs, when running the data layer functions of the

new application. The costs presented in Tables 9, 10,

and 11 are based on the D2-v2 VM type which

represented the best trade-off between TCO and SLA

requirements on the basis of the average tenant usage.

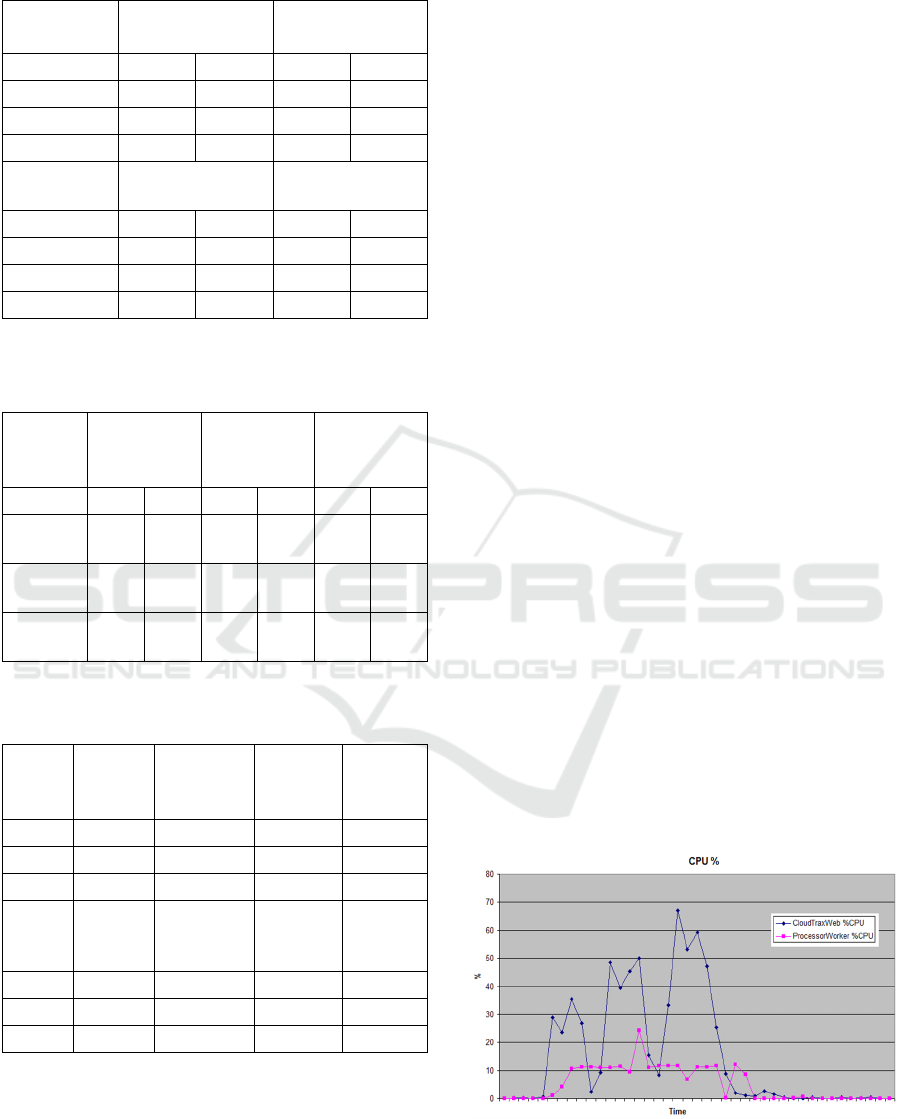

Among different TCO components, compute is by far

the most significant (€129,701), and also the most

fluctuating resource (see Figure 2). As such, its

efficient and effective usage should be the main

concern of the SP. Storage, as predicted, is relatively

stable and predictable with essentially fixed costs (see

Figure 3), and accounts for a very tiny portion of the

TCO (€293.31 – 0.001%).

The heavy image processing, results in higher-than-

normal network bandwidth and storage requirements.

As a consequence, the observations should also hold

for applications with less data volume and would thus

cover the majority of typical transactional business

applications.

Note that these pragmatic/empirical observations

stem from experiments in a live feasibility study, and

have been implemented on the basis of the following

assumptions:

The existing deployment does not include any

data caching which would obviously reduce the

CPU overhead and data storage access costs.

No optimization of the queries to the table

service to optimize CPU load over the TCO

estimation period.

No performance tuning on the application

and/or on the platform during the TCO

estimation period.

There is no smoothing effect of multiple

tenants sharing the same application compute

resources.

Figure 2: Compute Usage Over a Twenty-Minute

Monitoring Period.

CLOSER 2018 - 8th International Conference on Cloud Computing and Services Science

372

Figure 3: Storage Usage Over a Twenty-Minute Monitoring

Period.

7 CONCLUSIONS AND FUTURE

DEVELOPMENTS

Research has covered costing and migration

separately. Our literature review did not identify a

detailed framework that integrated both costing and

software architecture within a cloud migration

scenario. An investigation linking architectural

decisions and the impact on costing in cloud

migration is therefore important and this paper makes

an initial contribution in this context (Li et al., 2011).

We have identified the major components and

integrated them into an integrated framework to

estimate the cost of hosting a SaaS application on an

IaaS or PaaS platform, and to use this as the basis of

a SaaS licensing model. As a generic, formalized

model cannot exist due to the differences in factors

and account types between the IaaS/PaaS providers,

our aim was to identify the factors influencing this

calculation and to illustrate this through a real case

study.

No single formula, which allows right-scaling and

right-pricing to be easily determined, was identified

in our literature review. In this paper, we propose:

An approach for cost estimations in cloud

migration.

Heuristics for providing better estimation

accuracy.

An experimental determination of usage and

cost patterns for reliable cost.

We have focused on a business-to-business SP thus

our conclusion is not directly generalizable to

business-to-consumer SPs and consumer buyers.

Similarly, we have focused on migration and

operational costs as the primary cost unit and fees

paid as the main components of the cost of ownership.

Cloud adoption, like all IT investments, results in

direct tangible costs such as cloud resources but also

in intangible costs, e.g., change management, vendor

management, risk mitigation etc. (Misra and Mondal,

2011). We sought to explore and illustrate a relatively

simple but practical process for cost estimation in

cloud migration targeting small and medium

enterprises. Further studies may account for more

complex models suitable for larger and more mature

organizations. Similarly, we limited our case study to

one cloud service provider and a small number of

services. Future studies may seek to compare

functionality, quality and costs, but this stage has

been neglected in the literature (Gilia and S. Sood,

2013).

From an architecture perspective, container

technology and micro-service style architectures are

an increasing feature in the enterprise cloud and are

impacting cloud-native architectures. New

provisioning and payment models moving away from

pay-per-hour models towards payment by business

cycles are emerging in PaaS, linking the SaaS

provisioning costs for the software producer with the

platform.

Cloud service providers are also innovating in ways

that will impact how software producers

conceptualize costs and pricing. For example, AWS

Lambda is a compute service where code is uploaded

and the Lambda service executes the code using the

AWS infrastructure. The uploaded code is used to

create a so-called Lambda function. The AWS

Lambda service then handles provisioning and

managing the servers to run the code. The charging

model is innovative in that the user is charged based

on the number of requests for the software producers

functions and the time the software producer code

executes. Google has recently announced a similar

Cloud Functions model. These initiatives are too

recent to allow a deeper analysis of concerns.

However, they are worthwhile future research.

Our work shows that an integrated perspective

accommodating architecture, cost and revenue is

needed and that the traditional TCO approaches

cannot be applied without adaptation. Our paper

highlights the need for collaboration between

business, accounting and computer science

researchers in order to understand the implications for

costing, pricing and software design in the cloud

computing context. This may require not only

adaptation in common activity-based and resource-

based costing methodologies but also in software and

systems design.

ACKNOWLEDGEMENTS

The research work described in this paper was

supported by the Irish Centre for Cloud Computing

Making the Cloud Work for Software Producers: Linking Architecture, Operating Cost and Revenue

373

and Commerce, an Irish National Technology Centre

funded by Enterprise Ireland and the Irish Industrial

Development Authority.

REFERENCES

Andrikopoulos, V., Song, Z. and Leymann, F., 2013.

Supporting the migration of applications to the cloud

through a decision support system. IEEE Sixth

International Conference on Cloud Computing.

Anwar, A., Sailer, A., Kochut, A., Schulz, C.O., Segal, A.

and Butt, A.R., 2015. Cost-Aware Cloud Metering with

Scalable Service Management Infrastructure. CLOUD,

IEEE, pp. 285-292.

Armbrust, M., Fox, A., Griffith, R., Joseph, A.D., Katz, R.,

Konwinski, A., Lee, G. Patterson, D., Rabkin, A.,

Stoica, I. and Zaharia, M., 2010. A view of cloud

computing. Communications of the ACM, Vol. 53, No.

4, 2010, pp.50-58.

Baden-Fuller, C. and Haefliger, S., 2013. Business models

and techno-logical innovation. Long range planning,

Vol. 46, No. 6, 2013, pp.419-426.

Bain and Company, 2017. The Changing Faces of the

Cloud. Available from: http://www.bain.com/

publications/articles/the-changing-faces-of-the-

cloud.aspx [January 25, 2017].

Berman, S.J., Kesterson-Townes, L., Marshall, A. and

Srivathsa, R., 2012. How cloud computing enables

process and business model innovation. Strategy &

Leadership, Vol. 40, No. 4, pp.27-35.

CFO Research, 2012. The Business Value of Cloud

Computing: A Survey of Senior Finance Executives.

CFO Publishing. Available from: http://lp.google-

mkto.com/rs/google/images/CFO%2520Research-Goo

gle_research%2520report_061512.pdf [June, 2012].

DaSilva, C.M., Trkman, P., Desouza, K. and Lindic, J.,

2013. Disruptive technologies: a business model pers-

pective on cloud computing. Technology Analysis &

Strategic Management, Vol. 25, No. 10, pp. 1161-1173.

Dillon, T., Wu, C. and Chang, E., 2010. Cloud computing:

issues and challenges. IEEE international conference

on advanced information networking and applications,

pp. 27-33.

Durkee, D., 2010. Why Cloud computing Will Never Be

Free. Communications of the ACM, Vol. 53, No. 5,

2010, pp. 62-69.

Ferrante, D., 2006. Software Licensing Models: What’s Out

There?. IT Professional, Vol. 8, No. 6, pp.24-29.

Filiopoulou, E., Mitropoulo, P. and Tsadimas, A., 2015.

Integrating cost analysis in the cloud: A SoS approach.

11th International Conference on Innovations in

Information Technology (IIT).

Giardino, C., Bajwa, S.S., Wang X. and Abrahamsson, P.,

2015. Key Challenges in Early-Stage Software

Startups. XP Conference 2015.

Gilia, P. and Sood, S., 2013. Automatic Selection and

Ranking of Cloud Providers using Service Level

Agreements. International Journal of Computer

Applications, Vol. 72, No. 11, pp. 45-52.

Han, Y., 2011. Cloud computing: case studies and total

costs of ownership. Information technology and

libraries, Vol. 30, No. 4, pp. 198-206.

ISACA, 2012. Calculating Cloud ROI: From the Customer

Perspective. Available from: https://www.isaca.org/

knowledge-center/research/researchdeliverables/pages/

calculating-cloud-roi-from-the-customer-perspective.

aspx.

Jamshidi, P., Ahmad, A. and Pahl, C., 2013. Cloud

Migration Research: A Systematic Review. IEEE

Transactions on Cloud Computing, Vol. 1, No. 2, pp.

142-157.

Jamshidi, P., Pahl, C., Chinenyeze, S. and Liu, X., 2014.

Cloud Migration Patterns: A Multi-Cloud Service

Architecture Perspective. International Workshop on

Engineering Service Oriented Applications -

WESOA14.

Jinesh, V., 2010. Migrating your existing applications to the

aws cloud. A Phase-driven Approach to Cloud

Migration. Available from: http://docs.huihoo.com/

amazon/aws/whitepapers/Migrating-your-Existing-

Applications-to-the-AWS-Cloud-October-2010.pdf.

Leimbach, T., Hallinan, D., Bachlechner, D., Weber, A.,

Jaglo, M., Hennen, L., Nielsen, R.Ø., Nentwich, M.,

Strauß, S., Lynn, T. and Hunt, G., 2016. Potential and

Impacts of Cloud Computing Services and Social

Network Websites. Science and Technology Options

Assessment (STOA). Available from: http://www.

europarl.europa.eu/RegData/etudes/etudes/join/2014/5

13546/IPOL-JOIN_ET(2014)513546_EN.pdf. [15

August 2016].

Li, X., Li, Y., Liu, T. Qiu, J. and Wang, F., 2009. The

Method and Tool of Cost Analysis for Cloud

Computing. 2009 IEEE International Conference on

Cloud Computing, pp. 93-100.

Li, H., Zhong, L., Liu, J., Li, B. and Xu, K., 2011. Cost-

effective partial migration of VoD services to content

clouds. IEEE International Conference on Cloud

Computing, pp. 203-210.

Marston, S., Li, Z., Bandyopadhyay, S., Zhang, J. and

Ghalsasi, A, 1999. Cloud computing The business

perspective. Decision support systems, Vol. 51, No. 1,

pp.176-189.

Martens, B., Walterbusch, M. and Teuteberg, F., 2012.

Costing of cloud computing services: A total cost of

ownership approach. 45th Hawaii International

Conference on System Science (HICSS).

Misra, S.C. and Mondal, A., 2011. Identification of a

company’s suitability for the adoption of cloud

computing and modelling its corresponding Return on

Investment. Mathematical and Computer Modelling,

Vol. 53, No. 3, pp. 504-521.

Pahl, C. and Xiong, H., 2013. Migration to PaaS Clouds -

Migration Process and Architectural Concerns. IEEE

International Symposium on the Maintenance and

Evolution of Service-Oriented and Cloud-Based

Systems, pp. 86-91.

CLOSER 2018 - 8th International Conference on Cloud Computing and Services Science

374

Strebel, J. and Stage, A., 2010. An economic decision

model for business software application deployment on

hybrid cloud environments. Multikonferenz

Wirtschaftsinformatik, MKWI 2010.

Taibi, D., Lenarduzzi, V. and Pahl, C., 2017. Processes,

Motivations and Issues for Migrating to Microservices

Architectures: An Empirical Investigation. IEEE Cloud

2017.

Walterbusch, M., Martens, B. and Teuteberg, F., 2013.

Evaluating cloud computing services from a total cost

of ownership perspective. Management Research

Review, Vol. 36, No. 6.

Making the Cloud Work for Software Producers: Linking Architecture, Operating Cost and Revenue

375