Implementation of Work Ethic of Appraiser through KEPI in Effort

to Build Capability and Performance of Appraiser in Medan

Elisabet Siahaan

1

, Khaira Amalia Fachrudin

1

and Beby Kendida Hasibuan

2

1

Magister Management Property and Valuation, Postgraduate Program, Universitas Sumatera Utara, Medan, Indonesia

2

Faculty of Economics and Business, Universitas Sumatera Utara, Medan, Indonesia

Keywords: Appraisers, Work Ethic, Capabilities, Performance

Abstract: Indonesian Appraisers Code of Ethics (KEPI) has been updated and socialized to all appraisers in Indonesia.

KEPI contains guidelines for behaving ethically in performing duties as a professional and responsible

appraiser. A good performance of appraiser is necessary in encouraging the implementation of business in

industry 4.0 so much effort is needed in improving the performance of the appraiser in general. This study

included 110 certified appraisers from the Indonesian Society of Appraisers (MAPPI). The research model

was evaluated using descriptive statistics and path analysis. The results of this study showed that the work

ethic summarized in KEPI has a positive and significant role in generating the capability of the appraiser as

well as encouraging the performance in Medan. This research suggested to the appraisers that during carrying

out the appraisal process, they are guided by KEPI in order to resulting in a higher quality performance

appraisal.

1 INTRODUCTION

1.1 Research Background

The development of the 4th generation industrial

revolution (Industry 4.0) increasingly demands

organizations to operate effectively and efficiently.

High performance is always required to produce

competitive advantages and benefits the users of the

organization. Achievement of performance is directly

related to the achievement of organizational goals.

Vosloban (2012) states that continuously achieving

the highest levels of performance for the organization

becomes a major challenge in the ever-evolving

business environment as well as higher market

standards.

In industry 4.0, the company is not only required

to be able to produce goods or services that can meet

the needs of the market, but also workforce with high

performance by applying the use of technology and

communication optimally. Competitive advantages

for the company will be higher along with the

increase in employee performance realization

compared with company expectations on the

employee. Gruman and Saks (2011) states that

performance management is a very important aspect

in achieving company efficiency. Now, effort to

improve employee performance become one part of

the main objectives of the company in an effort to

improve the competitiveness of the company (Rusu,

et al., 2016). The Company seeks to create individual

performance improvements in an effort to drive the

company's performance in general (Hartog et al.,

2004).

Previous research has confirmed that

organizational performance is related to the behavior

of individuals within the organization (Boxall and

Macky, 2007; Yasir et al., 2013). Nevertheless, the

focus on individual behavior of human resources in

the organization has not been described specifically

(Purcell et al., 2009). One thing that is capable of

forming individual behavior in the organization is

professional ethics. Professional ethics are the set of

rules perceived as the right thing to apply in work and

it shapes the values and behavior of individuals in

work (Omisore, 2015). In the revolution of industry

4.0, professional ethics will assist in establishing a

firm organizational framework that unifies behavior

and shapes the expected performance outcomes.

This research raises the issue of work ethic or

professional ethics in the appraisal environment in

Medan. Appraisers are professions that play an

important role in supporting the implementation of

industry 4.0. Evaluation of business feasibility,

property values, and business development prospects

1392

Siahaan, E., Fachrudin, K. and Hasibuan, B.

Implementation of Work Ethic of Appraiser through KEPI in Effort to Build Capability and Performance of Appraiser in Medan.

DOI: 10.5220/0010076513921398

In Proceedings of the International Conference of Science, Technology, Engineering, Environmental and Ramification Researches (ICOSTEERR 2018) - Research in Industry 4.0, pages

1392-1398

ISBN: 978-989-758-449-7

Copyright

c

2020 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

are issues that require a competent appraiser. The

results of the work of a good appraisal agency will

greatly assist the smooth operation of various sectors

in the 4.0 industry. Nizam et al. (2016) reflects the

work ethic as a standard to declare an acceptable or

unacceptable in the execution of work. This will

encourage the standardization of behavior expected

for an appraiser to achieve better performance.

This study focuses on discussing two things; that

are:

1. The role of ethics to build capability and

performance of appraisers in Medan;

2. Measuring mapping of application of

appraiser professional ethics summarized in

KEPI that has been implemented by

appraisers in Medan

1.2 The Importance of Performance

Appraisal in Industry 4.0

Appraiser is one of the professions that provides sub-

sector services and plays an important role in

determining the economic value of the actual wealth

and the potential of wealth owned (Prima, 2007).

Appraisal concept that has been widely known by the

public, especially in Medan related to the profession

of the appraiser, that is the person who plays a role in

measuring the worthy value of an object. The concept

of apraisal is still widely growing in Indonesian

society. Public Appraisal Services (KJPP) is an

external body that is independent in providing an

appraisal of a property or assets of a client using its

services. The Appraisal Institute (2011) states that

estimating values is a complex process involving

various appraisal standards. Siahaan et al. (2018)

identifies that the value of the property is influenced

by economic factors and location.

The presence of appraiser in the nation's

economic development is very helpful in estimating

the value and feasibility of business, especially in the

face of industry 4.0. In a financial institution,

valuation activities can assist in accurately assessing

the object of collateral goods, valuation of assets for

debt guarantee, for the purpose of buying and selling,

collateral, insurance interests, evaluation of

compensation, financial statements and so forth. Due

to the many objectives of the appraisal in life, the

appraiser plays an important role in Indonesia's

development in the future (Resmi, 2003). The scope

of appraisers in Indonesia includes government

agencies, appraisal services associations, and

appraiser companies in the form of Limited Liability

Company. A government agency conducting a state

asset valuation activity is the Directorate of State

Assets Appraisal within the Directorate General of

State Assets Management.

The scope of the appraiser and the role of the

appraiser in various economic sectors are very high.

The research proposed in this proposal relates to how

efforts are made to improve individual performance

from an appraiser with an effort to improve individual

capability in performing appraisal tasks based on

Indonesian Valuation Standards (SPI) through the

implementation of KEPI.

2 LITERATURE REVIEW

2.1 Performance of Appraiser

Armstrong (2006) states that good performance is not

only seen from the good final results but also from the

work process by seeing how people achieve it.

Colquitt et al. (2009) states that performance is the

contribution of employees to the organization.

Measuring employee performance according to

Dharma (2013) means considering the quality and

quantity aspects of work.

2.2 Capabilities

Robbins and Judge (2013) define capability as the

capacity of individuals to perform various tasks in a

job. Everyone has strengths and weaknesses in the

ability that make them relatively superior or inferior

to other individuals in performing certain tasks or

activities. Management must know how people differ

in capabilities and use knowledge to increase the

likelihood that a worker will do a good job. Amir

(2011) explains that the capability is the ability to

exploit both the resources possessed within himself

and within the organization, as well as the potential

of self to perform certain activities or a series of

activities.

Krietner and Kinicki (2005) identifies that a

person's capabilities play a major role in driving

performance. Krietner and Kinicki also shares that in

essence capability is divided into two categories,

namely, physical capability and cognitive capablity.

Respatiningsih and Sudirjo (2015) show that one's

capabilities play a dominant role in encouraging

individual performance along with commitment,

motivation, and job satisfaction.

Self-capability is one of assets that professionals

must have in completing their work . The appraiser in

practice requires two forms of such capability. Jobs

will be more likely to be solved with physical health

support, especially when it comes to assessing the

field. Nonetheless the aspect of cognitive capabilities

also plays an important role, particularly in

understanding the Indonesian Appraisers Code of

Ethics (KEPI) and Indonesian Valuation Standards

Implementation of Work Ethic of Appraiser through KEPI in Effort to Build Capability and Performance of Appraiser in Medan

1393

(SPI). Therefore, this study focuses the self-capability

on cognition and attitude, i.e., understanding of KEPI,

such as mastering the nature of appraisers and general

principles in the appraisal; Mastering Market Value

as a Basis of Appraisal; Value Control Other than

Market Value; acting in accordance with applicable

rules, as well as objectives.

2.3 Professional Ethics of Appraiser

The professional ethics of the appraiser are regulated

in the form of the Indonesian Appraisers Code of

Ethics (KEPI). The code is set by law and promoted

by the Directorate of Appraisal, Ministry of Finance

of Republic of Indonesia (2016) as well as

associations of MAPPI in the books of KEPI and SPI

Edition VI 2015. KEPI is structured as a fundamental

foundation in the implementation of SPI so that the

results of the work meet the main requirements of

Honest, Competent, and Professional. KEPI is

basically mandatory and binding on all appraisers in

Indonesia and also sets the appraisers to have ethics

and competence in performing their duties. There are

five basic components of KEPI that must be applied

by appraisers in Indonesia.

2.3.1 Integrity

Requiring the Appraiser to be honest and credible in

all professional and business relationships. Should

not carry out an appraisal containing false or

misleading statements or information or omitting or

obscuring important information that must be

included due to negligence or ambiguity that can be

misleading. If he is aware of any incorrect

information, he must immediately take action related

to the information. Not allowed to participate or take

role in an appraisal service which is not justified.

Compulsory to act according to law and in

accordance with applicable laws and regulations. It is

not permissible to deliberately misinterpret a

professional qualification that he does not have.

2.3.2 Objectivity

Requiring the Appraiser to work professionally,

impartially, has no interest or is influenced by others.

In the event of a threat to objectivity which is

unavoidable, professional Appraisers shall refuse the

assignment. In reappraisal of the same asset, a review

of another Appraiser must be reviewed or periodically

replacing the Appraiser for the assignment. The

Appraiser shall not act for two or more parties to the

same assignment and purpose, except with the written

consent of the parties concerned. Must not accept an

assignment which appraisal report includes

predetermined opinions and conclusions. The

remuneration shall not be subject to the outcome of

any pre-determined judgment. It is not permissible to

provide conclusions that are not supported by

sufficient and prejudicial reasons, or reporting

conclusions that reflect an opinion that such

presumptions may affect value. In the case of a

Review of the appraisal report of other appraisers, he

must be impartial and consider his reasons for

agreeing or disagreeing with the report's conclusions.

It is not permissible to base his work on information

provided by the assignor only without proper

clarification or confirmation.

2.3.3 Competence

Appraisers are required to maintain professional

knowledge and skills at the required level.

Professional competence is divided into the

achievement and maintenance of professional

competence. Maintenance of professional

competence requires awareness and technical

understanding, professional development and

sustainable business. Perseverance includes the

responsibility to act in accordance with the scope of

the assignment, be careful, thorough and timely.

Appraisers ensure that their work is under the

authority of the Appraiser in a professional capacity

with proper training and supervision. If the Appraiser

does not have the necessary professional knowledge

and experience, the Appraiser must reject the duty.

2.3.4 Confidentiality

Disclosure outside the company or use of confidential

information obtained from the appraisal services

without the assignor's approval is prohibited.

Appraiser must maintain confidentiality, including in

the social environment. The Appraiser shall maintain

the confidentiality of the information disclosed by the

Assignor. Appraiser must maintain the confidentiality

of information within the company or work team. The

Appraiser must ensure that the staff helps to maintain

confidentiality. It takes to adhere to the principle of

continuing confidentiality even after the expiration of

the employment relationship with the client.

2.3.5 Professionalism Behavior

Appraiser must act carefully in providing services and

ensure that the services provided are in conformity

with legal, technical and professional standards

applicable to the subject of appraisal, appraisal

objectives or both. Professional behavior involves

accepting responsibility for acting in the public

interest not only of the Assignor's interests.

Appraisers must be honest and correct and do not

create excessive promotions for the services they

ICOSTEERR 2018 - International Conference of Science, Technology, Engineering, Environmental and Ramification Researches

1394

offer and are prohibited from making incorrect

references. Professional behavior includes

responsible and polite actions in all respects with the

assignor and the public in general and responds

promptly and effectively to all reasonable instructions

or complaints. Appraiser should avoid actions that

may discredit the profession.

3 RESEARCH METHOD

3.1 Research Time

The study was conducted in the area of Medan

appraisers in March to June 2018.

3.2 Participant

The study involved 110 appraisers in Medan who

were registered as members of the Indonesian Society

of Appraisers (MAPPI) and had worked as appraisers

for at least one year with a minimum membership of

P (Participant) at the MAPPI association . Research

carried out by visiting the office of MAPPI in North

Sumatra and Public Appraiser Services (KJPP) in

Medan.

3.3 Data Collection Procedures

The data were collected by using research

questionnaires compiled based on literature study

related to research variables. The research

questionnaire had passed the stage of validity and

reliability of the questionnaire before it was given to

the research sample . Researchers visited the offices

of MAPPI in Medan as a reference database of the

study sample, selected the sample, then visited KJPP

in Medan to spread out the questionnaire and collect

research data. The grace period for returning the

questionnaire was a week for further resampling by

the researcher on the research sample in his working

environment.

3.4 Validity and Reliability of

Questionnaire

Validity and reliability of the questionnaire were

conducted on 30 appraisers in Medan outside of the

study sample. Those who had followed the study as a

sample in the validity and reliability test were no

longer selected as samples in the study.

Table 1. Cronbach's Alpha Research Questionnaire

Variables Number of

Statements

Cronbach's

Alpha

Conclusion

Professional

Ethics

15 0.878 Reliable

Capability

of Appraise

r

10 0.891 Reliable

Performance

of Appraise

r

10 0.914 Reliable

The questionnaire validity test was done by

using Pearson's correlation from each item statement

to the total of each variable. The critical point (r-

table) used for 30 samples was 0.361. All of the

proposed statements met the criteria of the validity of

the research questionnaire. Table 1 encapsulates the

reliability test of the questionnaire by using the

consistency of Cronbach's alpha. Each variable had

been consistently measured by the proposed

statement with an alpha value > 0.7. Therefore all the

questions posed on the validity and reliability test

were valid and reliable.

3.5 Data Processing and Analysis

Method

Data were analyzed using path analysis method that

estimated the role of the application of the Indonesian

appraiser professional ethics in shaping the

capabilities of appraiser and producing the expected

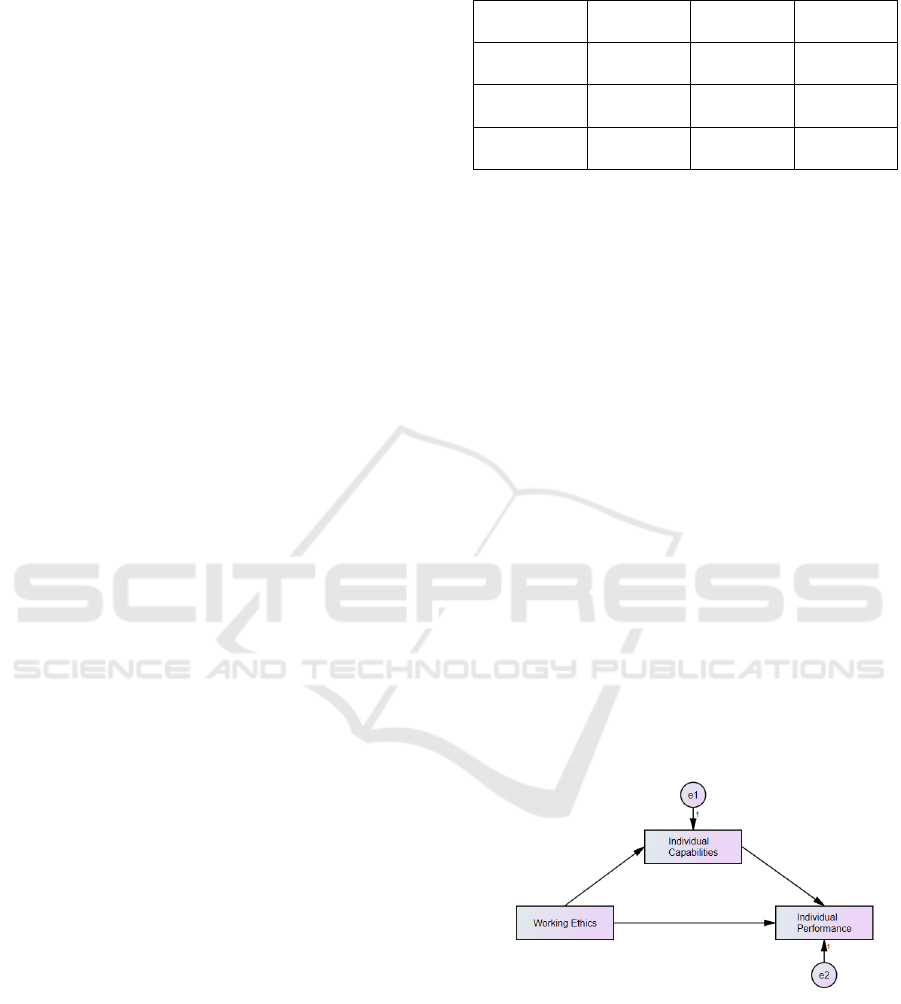

performance of the appraiser. The path model used in

the study refers to Figure 1. Hypothesis testing was

performed using 5% significance level. The analysis

was performed using direct, indirect, and total effects

in the estimates.

Figure 1. Research Model

Implementation of Work Ethic of Appraiser through KEPI in Effort to Build Capability and Performance of Appraiser in Medan

1395

4 FINDINGS

4.1 The Current Practice of Work

Ethic

Descriptive statistical analysis was used to evaluate

the current situation of the professional ethics

variable. Each aspect (dimensions) are measured

using three indicators with five scales, so the

minimum value is always worth 3 and the maximum

is 15. The current state of the professional ethical

practice in the Medan appraiser is summarized in

Table 2.

Table 2. Descriptive Statistics of Appraiser Professional

Ethics in Medan

Aspec

t

N

Min Max Mean

Inte

g

rit

y

110 3 15 13.63

Ob

j

ectivit

y

110 3 15 13.27

Competenc

y

110 3 15 11.99

Confidentialit

y

110 3 15 12.42

Professionalism 110 3 15 13.22

Table 2 indicates that in general all aspects of

professional ethics had been applied well by

appraisers in Medan, especially in integrity aspect,

then the principles of objectivity and professionalism

were always upheld. An average score above 12.00

indicated an excellent ethical achievement. The

smallest aspect that was reflected by the respondent's

answer was the problem of competency control in

working as an appraiser.

4.2 Path Analysis

This study uses path analysis to evaluate the role of

the code of ethics of appraisal in an effort to improve

the ability of the appraiser and the performance of the

appraiser. Path analysis in this research is assisted by

using AMOS analysis tool.

Figure 2. AMOS Path Analysis

Table 3. Path Estimate Analysis

Indepen

dent

Depende

nt

Mediating

Role

Path Analysis

Dire

c

t

Indir

ec

t

Total

Effect

Work

Ethic

--

>

Capabili

t

y

a

0.41

1*

- 0.411

Work

Ethic

--

>

Perform

ance

b

Capabilit

y

0.44

1*

0.15

5*

0.596

Capabi

lity

--

>

Perform

ance

0.23

3*

- 0.233

* Significant at 5%;

a

Adjusted R-squared = 0.169;

b

Adjusted R-squared = 0.436

The model in the research was able to predict each

of 16.9% and 43.6% variance on dependent variables,

capability and individual performance from appraiser

in Medan. This indicated that the research model was

good enough in predicting the performance of

appraisers based on professional ethics and capability

of appraiser with predictive numbers up to 43.6%

performance. Professional ethics were only able to

explain 16.9% ability of appraiser in Medan.

Work ethic significantly affected the capability

and performance of appraisers in Medan. If the

appraiser applied the work ethic in the appraisal

process, the capabilities and performance of the

appraiser would increase. The performance of the

appraiser was influenced by ethics and capabilities

together. Work ethic was more instrumental in

influencing the performance of Indonesian

appraisers. Indirectly, ethics will form capabilities

which encourage the creation of individual

performance.

5 DISCUSSION

Work ethic had positive and significant influence to

individual capability of appraiser in Medan. This

indicated that the stronger the work ethic was applied

by the appraiser, the higher the level of individual

capability that reflected the ability to complete the

appraisal report properly and appropriately because

the work behavior was in accordance with the

appraiser professional ethics which were the guide in

acting and behaving. The willingness of the appraiser

in applying the basic principles of ethics that includes

integrity, objectivity, competence , maintaining

confidentiality, and professional behavior in working

will result in responsible work behaviors, more skilful

in the appraisal, more detail in understanding the

technics of completing the work based on the basic

ethical principles of appraisal. Okpara and Wynn

(2008) affirms how the code of ethics in the company

will shape the behavior that the company expects in

each employee. Omisore (2015) also states that a set

of rules or ethics in running the work will be a

ICOSTEERR 2018 - International Conference of Science, Technology, Engineering, Environmental and Ramification Researches

1396

guideline for workers in acting about what is right and

what needs to be avoided in doing the work. As a

result, work ethic will shape the behavior. The

problem is how individuals are willing to implement

the work ethic in accordance with the applicable

rules. The results of this study confirm that if an

appraiser is willing to apply work ethic in completing

the appraisal task, then the self-capability of the

appraiser will increase. The results of this study are

supported by Arend (2013) which states that the

ability to implement the code of ethics in completing

the work will affect the ability to finish the work.

Work ethic has a positive and significant

influence on the performance of appraisers, either

directly or indirectly through the formation of the

capability of the appraiser. Sharma et al. (2009)

shows how the influence of work ethic in the

company to encourage performance in general.

Ethical behavior of the company will encourage

image formation, reduce hazard and improve

efficiency so that company performance can increase.

In line with this, the implementation of work ethic in

an individual environment will help the achievement

of individual performance. Professional ethics are

essentially structured to aid the smooth running of

one's work. Thus, the implementation of professional

ethics will assist in encouraging the performance by

ensuring the work is complete both in quality and

quantity. In addition, professional ethics will produce

capability that encourages higher performance

achievement.

Self-capability has a positive and significant

effect on the performance of appraisers. Tan et al.

(2007) provides the role of operating business

capability in producing the company's performance.

Capability reflects the ability to perform tasks as they

should. In this study, capability is reflected by the

application of the Indonesian Valuation Standards in

the form of work behavior. As this capability

improves, appraisers will progressively work as

required that will lead to higher performance

achievements.

In general, the work ethic represented in KEPI has

been well implemented by appraisers in Medan. In

line with these conditions, appraisers in Medan

already have behaviors that are in line with the

Indonesian Valuation Standards (SPI) and produce

good performance. So far, there are very few

problems that have been caused by mistakes in

Indonesia. This condition encourages the results of

research where the application of work ethic will

encourage the capability and performance of

appraisers in Medan. Nevertheless, the application of

work ethic can still be improved, especially through

improving self-competence in the work ethic referred

to by KEPI.

6 CONCLUSION

In general all aspects of professional ethics had

been applied well by appraisers in Medan, especially

in integrity aspect, the principles of objectivity and

professionalism were always upheld. Behaviors of

appraisers which implement code of ethics during the

appraisal process are significantly able to improve

self-capability and performance of the appraiser.

Implementing the code of ethics during the appraisal

process will result in qualified performance and

personally accountable to the appraiser, assignor,

fellow appraisers, Public Appraiser Services (KJPP),

and the public. Indonesian Appraisers Code of Ethics

(KEPI) is structured according to the rules necessary

to control the behavior of the appraiser in order to act

ethically, effectively and efficiently. In the end, an

objective and appropriate appraisal report will be

resulted.

ACKNOWLEDGMENTS

The authors gratefully acknowledge that the present

research is supported Universitas Sumatera Utara.

The support is under the research grant Basic

Research of TALENTA 2018. The research were

funded by Non-PNBP.

REFERENCES

Amir, M.T. (2011). Manajemen Strategi. Jakarta: PT Raja

Grafindo Persada

Appraisal Institute. (2008). Appraisal of Real Estate.

Chicago: Illinois

Arend, J.R. (2013). Ethics-focused dynamic capabilities: a

small business perspective. Small Business Economics,

41(1), pp 1-24

Armstrong, M. (2006). Performance Management: Key

Strategies and Practical Guidelines. London: Kogan

Page Limited, 3

rd

edition

Boxall, P., and Macky, K. (2007). High-performance work

systems and organization. Journal of Human Resource

Management, 14(2), pp 15-35

Colquitt, J., Le-Pine, J., and Wesson, M. (2009)

Organizational Behavior: Improving Performance and

Commitment in the Workplace. New York: McGraw-

Hill

Dharma, S. (2013). Manajemen Kinerja. Yogyakarta:

Pustaka Pelajar

Gruman, J.A., and Saks, A.M. (2011). Performance

management and employee engagement. Human

Resource Management Review, 21, pp 123-136

Hartog, D.N., Boselie, P., and Paauew., J. (2004)

Performance management: a model and research

Implementation of Work Ethic of Appraiser through KEPI in Effort to Build Capability and Performance of Appraiser in Medan

1397

agenda. Applied Psychology: An International Review,

53(4), pp 556-569

Kreitner, R., and Kinicki, A. (2005) Orgaizational

Behavior. Jakarta: Salemba Empat, Translated to

Bahasa

Ministry of Finance. (2016). Kode Etik Penilai Indonesia

dan Standar Penilaian Indonesia (KEPI dan SPI).

Jakarta: Kementerian Keuangan Republik Indonesia

Nizam, S., Ruzainy, M.N., Sarah, S., and Syafina, S. (2016)

The relationship between work ethics and job

performance. The European Proceedings of Social and

Behavioural Sciences, pp 465-471

Okpara, J.O., and Wynn, P. (2008). The impact of ethical

climate on job satisfaction and commitment in Nigeria:

implications for management development. Journal of

Management Development, 27(9), pp 935–950

Omisore, B.O. (2015). Work ethics, values, attitudes and

performance in the Nigerian public service: issues,

challenges and the way forward. Journal of Public

Administration and Governance, 5(1), pp 157-172

Prima, A. (2007). Penilaian Properti Berbasis Nilai Pasar

berdasarkan Standar Penilai Indonesia pada

Perusahaan Appraisal

Purcell, J., Kinnie, N., Swart, J., Rayton, B., Hutchinson, S.

(2009). People Management and Performance.

London: Routledge

Resmi, S.S. (2003). Urgensi Penilaian Properti dalam

Tatanan Ekonomi Masyarakat Usahawan

Respatiningsih, I., and Sudirjo, F. (2015). Pengaruh

komitmen organisasi kapabilitas dan kepuasan kerja

terhadap kinerja pegawai. Serat Acitya [Online], 4(3)

Robbins, S.P., and Judge, T.A. (2013). Organizational

Behaviour. United States of America: Prentice Hall,

15

th

Edition, E-book Edition

Rusu, G., Avasilcai, S., and Hutu, C. (2016). Organizational

Context Factors influencing employee performace

appraisal:a research framework. Presented in 13th

International Symposium in Management/Elsevier,

Procedia - Social and Behavioral Sciences 221, pp 57-

65

Sharma, D., Borna, S., and Stearns, J.M. (2009). An

investigation of the effects of corporate ethical values

on employee commitment and performance: examining

the moderating role of perceived fairness. Journal of

Business Ethics, 89(2), pp 251–260

Siahaan, E., Fachrudin, K.A., and Sibarani, M.L.L. (2018).

Evaluation of location aspect in buyer's decision to

purchase elite residence in Medan Advances in

Economics Business and Management Research, 46, pp

623-629

Tan, K.C., Kannan, V.R., and Narasimhan, R. (2007). The

impact of operations capability on firm performance.

International Journal of Production Research, 45(21),

pp 5135-5156

Vosloban, R.I. (2012). The influence of the employee's

performance on the company's growth - a managerial

perspective Procedia Economics and Finance, 3, pp

660-666

Yasir, M., Imran, R., and Irshad, M.K. (2013) Mediating

role of organizational climate in the relationship

between transformational leadership, its facets and

organizational performance Actual Problems of

Economics/Aktual’ni Problemi Ekonomìki, 145(7).

ICOSTEERR 2018 - International Conference of Science, Technology, Engineering, Environmental and Ramification Researches

1398