The Challenges on Beneficial Ownership Disclosure in Indonesia:

A Study of the Enactment of Presidential Regulation No. 13 of 2018

on the Application of Know-Your-Beneficial-Ownership Principles by

Corporations for the Prevention and Eradication of Money

Laundering and Terrorism Financing

Masitoh Indriani and Dian Purnama Anugerah

Faculty of Law Universitas Airlangga, Indonesia

Keywords: Beneficial Ownership, Disclosure, Transparency.

Abstract: The Indonesia Government passed Presidential Regulation No. 13 of 2018 on the Application of Know-Your-

Beneficial Ownership (BO) Principle by Corporations for the Prevention and Eradication of Money

Laundering and Terrorism Financing. Under this regulation, each corporation must determine the BO

information of its business entity in order to create transparency as the obligation for Indonesia as a state

member of the Financial Action Task Force (FATF) in implementing global standards for anti-money

laundering and combating the terrorism financing. The information to be collected and disclosed includes the

BO’s full name, identity number or driver license or passport number, date of birth, nationality, address or

domicile and taxation identity number. These set of information considered as personal data that protected by

laws. While the registration and submission of those information filed by the company’s shareholders or its

executive boards, a public notary or an authorized agency, it still remains vague since the issue on its system

readiness and also lack of coordination with some government agencies. As a result, there might be delay or

rejection on the new company establishment when there is suspected, withheld or concealed on BO data. This

paper aims to discuss the implementation of Presidential Regulation No.13 of 2018 specifically on the

incorporation of BO registering and submitting process, secondly, whether the BO disclosing process might

face issues on transparency specifically in the access of BO information, the issue on database and the right

to privacy.

1 INTRODUCTION

Beneficial Ownership (hereinafter BO) concept has

been known since 1977 when the Organization for

Economic Co-operation and Development (OECD)

first introduced the OECD Model Tax Convention.

Although OECD put the BO, but the debate over the

scope and interpretation of BO remains a discussion

for decades.

Based on recent development in 2016, OECD has

set definition as follow : a beneficial owner is the

natural person who is ultimately entitled to the

benefits accruing from the beneficial ownership of the

securities, and/or has power to exercise controlling

influence over the voting rights attached to the shares

(even if the legal title is held by another person)

(OECD, 2016). Although in general BO is related to

the natural person, but BO can also be a legal person

as long as the ultimate owner is a state or state owned

enterprise. Compared to other Asian countries,

Indonesia is lagging behind in regulatory framework

regarding BO. In a country like. Hong Kong, China,

Malaysia, Thailand and Singapore, the regulatory

framework has regulated BO both de facto and de

jure. De Jure means that regulations specify clearly

about who qualifies as BO, usually measured by the

percentage of share ownership. Meanwhile de facto

related to a situation or condition that stipulated in

regulation where a person can be qualified as BO.

In Indonesia, the concept of BO initiated as

subject of discussion after the media preach about

leaked Panama Papers in which a list of 2.619

Indonesian’s ranges from tycoons to public officials

and Attorney General Fugitive (Firmansyah, 2016).

The Government of Indonesia then made a policy on

Tax Amnesty initiated by Sri Mulyani, Minister of

Indriani, M. and Anugerah, D.

The Challenges on Beneficial Ownership Disclosure in Indonesia: A Study of the Enactment of Presidential Regulation No. 13 of 2018 on the Application of Know-Your-Beneficial-Ownership

Principles by Corporations for the Prevention and Eradication of Money Laundering and Terrorism Financing.

DOI: 10.5220/0010053004110416

In Proceedings of the International Law Conference (iN-LAC 2018) - Law, Technology and the Imperative of Change in the 21st Century, pages 411-416

ISBN: 978-989-758-482-4

Copyright

c

2020 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

411

Finance of Indonesia. Although this policy was

success to collect tax revenues from private property

disclosure, the repatriation of the program was far

from the target. In the end of tax amnesty program,

only 147 trillion rupiah is collected from 1.000 trillion

rupiah targeted by the Ministry of Finance (Maulia &

Suzuki, 2017). This is showing that many wealthy

individuals are placing their assets abroad by

disguising the identity of the asset owners through the

shell company. The obvious consideration is to avoid

taxes by utilizing regulations in tax haven country.

Therefore, on March 5, 2018, President Joko

Widodo responded by enacting Presidential

Regulation No. 13 of 2018 concerning the

Implementation of Principles of Recognizing the

Beneficial Ownership of Corporations for the

Prevention and Eradication of Money Laundering and

Terrorism Financing (hereinafter BO Regulation).

This regulation is government’s response in urgency

of protection for the company and its shareholders,

legal certainty to assess criminal liability and to

recover assets (Alecci, 2018). Although at this

moment still in the level of Presidential Regulation

but this is a fairly reactive step by the government.

According to Indonesia legal system, Presidential

Regulation is an instrument that is not strong as the

Act. One of the disadvantages is regarding

enforceability since the Presidential Regulation does

not have sanctions as a force of coercion. Moreover,

there is still a need to harmonize with other

regulation, considering that for the implementation of

database BO coordination is required with the cross-

sectoral authority. By using statute and conceptual

approach, this paper will address two main issues,

first the implementation of BO Regulation

specifically in the incorporation of BO registering and

submitting process; secondly, the challenges on BO

disclosing process.

2 DISCUSSION

2.1 The Urgency of BO Disclosure

After revealing Indonesian company listed on

panama papers, Indonesian authority begun to

response the need of BO Regulation. Before BO

regulation enacted, judicial authority has introduced

new opinion regarding BO that go beyond the

“Piercing the Corporate Veil” doctrine. This could be

found on recent judgments in the Sitorus Case and

Rifuel Ltd. Case (Videotron Case).

In 2017, Indonesia Supreme Court ruling on

Labora Sitorus Case (Case No. 1081/K/Pid.Sus/2014)

made a turning point for a new development of BO.

Sitorus was an active police officer who controls the

company in illegal logging and fuel smuggling

activities. Rotua Ltd. was established in October 2010

as a company engaged in wood working and

furniture. As an active police officer, he is forbidden

by the law to run a company. Sitorus appointed the

nominee director and his wife as a non-executive

director (commissioner). The company begun to

operate under his command until finally the business

activities are uncovered by the authorities. The

Financial Transaction Report and Analysis Center

(PPATK) detected transactions more than 1.5 trillion

rupiahs (approximately US$ 146 Million) in his

account (Somba & Dharma, 2013) .The money came

from the transactions of two companies and several

business entities controlled by Sitorus. From the

PPATK report it was found that the money was came

from buying and selling illegal timber and fuel

smuggling. Shortly afterwards, the police responded

by investigating the “fat” account of Sitorus. No

evidence found that Sitorus is the shareholder,

director nor employee of the company.

The case was brought to District Court of Papua

by prosecutor on 2015. The court gave two years in

prison sentence and 50 million rupiah fine. The

prosecutor was dissatisfied with that verdict and

lodging an appeal to High Court. The High Court’s

upheld District Court verdict and gave 8 years prison

sentence, but the money laundering crime cannot be

proven. However, Artidjo Alkostar, the head judge of

Supreme Court panel has different opinion. The court

ruled that even Sitorus is not formally a shareholder

or director of the company, but he has a power to

appoint the director. The court also sought that

Sitorus in fact has power and authority that is very

significant and very decisive in decision making and

company policy. Thus, the Supreme Court aggravates

the sentence into 15 years in prison because the

money laundering was clearly proven.

In other case, Supreme Court also overturns the

district court decision regarding the responsibility of

nominee director. The Case No 980K/Pid.Sus/2015

was about Hendra Saputra who is the director of Imaji

Media ltd., a company that won a tender of videotron

in Ministry of Cooperatives. Hendra was an office

boy in Rifuel ltd., one of the companies also owned

by Riefan Avrian. It was later revealed that Riefan is

the son of the Minister of Cooperation and Small

Medium Enterprises, Syarief Hasan. Riefan was

using the name of Hendra to be used as a nominee

director in Imaji Media ltd. In 2012, Imaji Media Ltd.

and Rifuel Ltd. are participated in tender of videotron

in Ministry of Cooperatives. Rifuel ltd. did not win

iN-LAC 2018 - International Law Conference 2018

412

the tender; however, Imaji Media ltd. won the tender.

Although Reifan name cannot be found in the

company as a shareholder nor director but in fact he

runs the company in that project. The videotron

project finished but the specifications are not agreed

as in tender document. Under the audit from The

Audit Board of Republic of Indonesia (Badan

Pemeriksa Keuangan/BPK) in 2013, BPK has found

difference in payments of almost 5 billion rupiahs in

total. Supreme Court ruling that act committed by

Hendra as a director are not based on the wishes of

the defendant (mens rea), but merely used by Riefan

who is his employer at Rifuel ltd. The court finally

releases the defendant from all lawsuit and ordered

defendant to be released from detention.

2.2 BO Criteria in Indonesia

Under BO Regulation, the definition of BO can be

categorised based on the owners’ ability to exercise

right or power to control corporation such as the right

to appoint or dismiss a board of directors, board of

commissioners, management, or supervisor of the

corporation. Further, an individual who has the ability

to control the corporation is entitled to and/or receives

the benefits of the corporation, whether directly or

indirectly. Thirdly, an individual who is the true

owner of the fund or shares of the corporation and/or

fulfils the criteria referred to BO Regulation.

The ambit of BO Regulation is not only for

company but also other business entities including

those which not considered as a legal person. Below

is the matrix of the BO criteria according to the BO

Regulation:

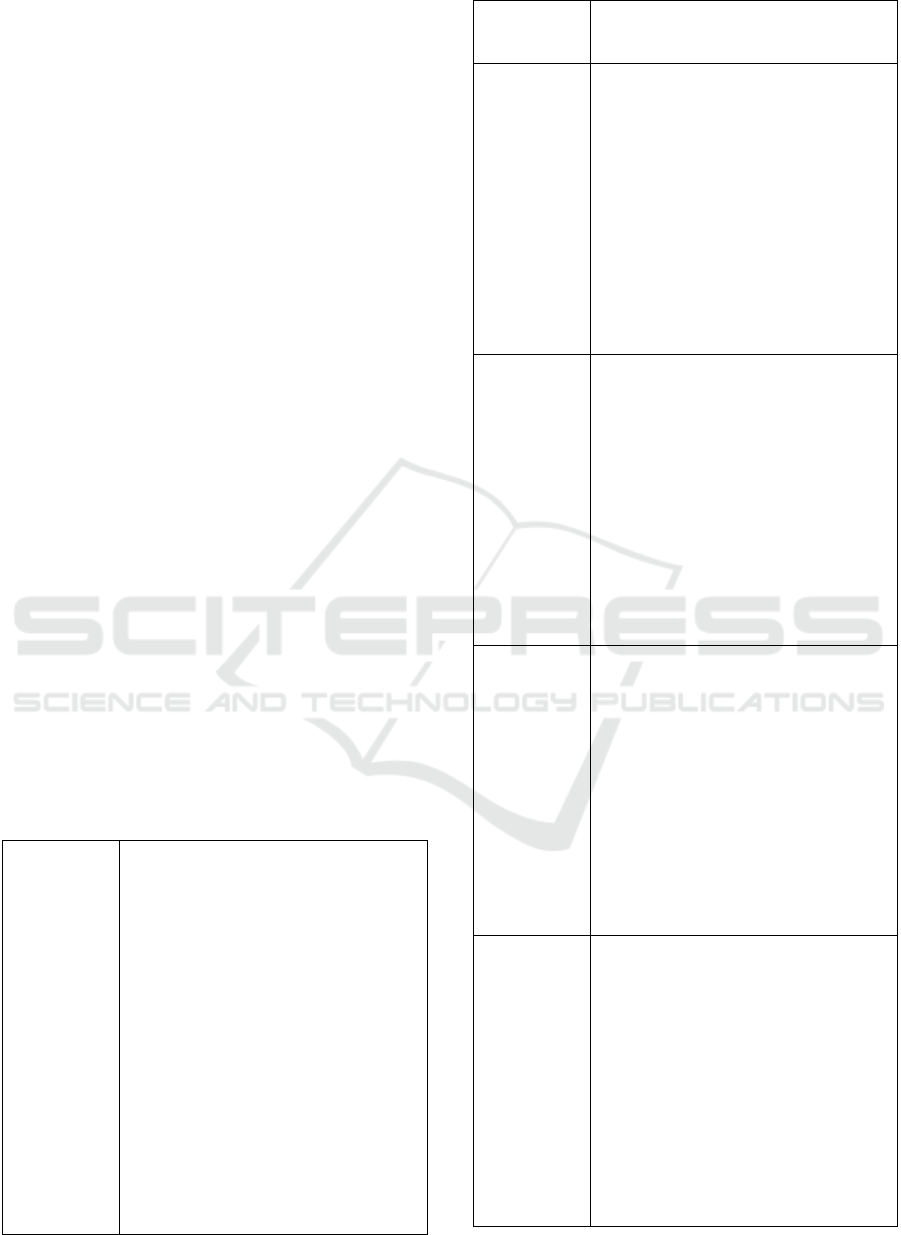

Table 1: BO Criteria according to BO Regulation

Limited

Liability

Company

(LLC)

a. holds shares of more than 25% to a

limited liability company as stated in

the articles of association;

b. has a voting rights of more than 25%

to a limited liability company as

stated in the articles of association;

c. receive a profit or profit of more than

25% of the profit or profit earned by

a limited liability company per year;

d. has the authority to appoint,

supersede, or dismiss members of the

board of directors and members of the

board of commissioners;

e. has the authority or power to

influence or control a limited liability

company without having to obtain

authorization from any party;

f. receive benefits from a limited

liability company; and/or

g. the true owner of the fund for the

ownership of shares of limited

liability company.

Foundation a. has a separated asset of more than

25% on the foundation as stated in the

articles of association;

b. has the authority to appoint or dismiss

the supervisor, board, and supervisor

of the foundation;

c. have the authority or power to

influence or control the foundation

without having to obtain

authorization from any party;

d. receive benefits from the foundation;

and/or

e. the true owner of funds of other assets

or inclusion in the foundation.

Cooperatives a. receives dividends more than 25% of

the profits or profits derived by the

cooperative per year;

b. have direct or indirect authority, may

appoint or dismiss the cooperative's

management and supervisor;

c. has the authority or power to

influence or control the cooperative

without having to obtain

authorization from any party;

d. receive benefits from cooperatives;

and/or

e. the true owner of the capital over

cooperative capital.

Limited

Partnership

a. has capital and/or goods deposited

more than 25% as stated in the deed

of the establishment;

b. receive a profit of more than 25% of

the partnership profits;

c. have the authority or power to

influence or control the partnership

without having to obtain

authorization from any party;

d. receive benefits from a partnership;

and or

e. the true owner of funds on capital

and/or the value of goods deposited in

a partnership.

Partnership a. has deposited paid up capital of more

than 25% as stated in the engagement

agreement of the lyrical partnership;

b. receive a profit or profit of more than

25% of the profits derived by the

firm's annually;

c. has the authority or power to

influence or control the firm's

fellowship without having to obtain

authorization from any party;

d. receive benefits from the partnership;

and/or

e. the true owner of the capital and/or

assets paid up as partnership capital.

The Challenges on Beneficial Ownership Disclosure in Indonesia: A Study of the Enactment of Presidential Regulation No. 13 of 2018 on

the Application of Know-Your-Beneficial-Ownership Principles by Corporations for the Prevention and Eradication of Money Laundering

and Terrorism Financing

413

BO disclosure mechanism is carried out by self-

reporting method. Every corporation must identify

BO based on criteria in the BO Regulation (see table

1). Pursuant to article 12 BO Regulation, there are

three categories, namely: a. BO has been identified;

b. BO has not been identified; or c. BO has not been

verified. After being identified, the corporation must

make a document that determines who becomes the

BO of the corporation. This information is submitted

to Company Registry Authority (hereinafter SABH -

Sistem Administrasi Badan Hukum).

Article 18 par. 3 BO Regulation stipulated that the

information may submit by: a. the founder or manager

of corporation; b. Public Notary; or c. other party

authorized by the founder or manager of corporation.

However, in order to fill the information on SABH,

not every person has access authorization. Only

registered Notary can submit the BO information

through SABH channel. The information in SABH

can be accessed by public using website

www.ahu.go.id. Each company profile can be

downloaded including BO data.

2.3 The Challenge of Transparency on

BO Disclosure

Transparency is the main element for the investors to

ensure that they put their money in the right place.

Thus the transparency is also important to contribute

economy for the country. Therefore, discover the

person who gets the beneficial of the corporations

ultimately will make the country as a perfect place for

the investor to do business. Furthermore, it also will

help the government to prevent and stop the misuse

of companies and give sanction to who responsible

doing the illegal activities (Kingdom, 2014).

However, there are other concerns on the

transparency issue for disclosing such as access to BO

information and database and the privacy issue. These

three issues will be explained further below.

2.3.1 Access to Data/Information

In many countries, information on the BO (in addition

to the legal owner) of a corporate vehicle is not

available as it is not collected and sufficiently verified

at the time the corporate vehicle is created, nor at any

stage throughout its existence (FATF, 2014).

Furthermore, a study found that issue for

transparency BO depends on the integrating all data

related to BO (Nuruliza, 2016). Those data are

financial transaction, banking, taxes, legal data

corporate ownership and even further population and

civil registration. These data are contributed for

policymaking to overlook of state revenue (Rini,

2016).

Before BO Regulation was enacted, the access to

BO data can be reached through Kustodian Sentral

Efek Indonesia/Indonesian Central Securities (KSEI).

The disclosure procedure is based on annual report of

companies listed on the stock exchange (BAPEPAM,

2012). This annual report is available on the

Indonesia Stock Exchange website. However, the

information on the website was remaining

insufficient since it did not provide information in

English. As a result, the intended information to

provide access to the stakeholders, investors, issuers

and other public companies could not efficient and

adequate (Nuruliza, 2016).

As BO Regulation enacted in 2018, there is an

obligation for the corporation to provide information

of their BO. Corporations are required to appoint a

person-in-charge who will responsible for the

implementation of identification and verification over

BO. Identification is undertaken through the

collection of personal information of BO, while

verification is undertaken to assess the conformity

between the BO information and other supporting

documents (Lie, et al., 2018).

Regarding to the access of BO information, it

should be observed further since the provided annual

report of the corporations will be just formality for the

corporations to comply with, or whether it will

provide the Authorized Agency with the power and

the legal grounds to require corporations to structure

or re-structure their investment or shareholding

composition in the manner acceptable to the

Authorized Agency (Lie, et al., 2018).

2.3.2 BO Database

Based on the FATF study, the lack of accurate

information on BO was utilized by the perpetrators to

conduct criminal acts (Keuangan, 2018). By enacting

BO Regulation, the Indonesian Government took

precautionary measure and prevention to tackle such

criminal acts. While based on study of Transparency

International (TI) on Corruption Perceptions Index

2017, there are more than two-thirds countries scored

below 50 (International, 2017). The number indicates

that there is no progress in many countries in ending

corruption. Fraud, corruption, organised crime and

tax evasion are enabled by anonymous shell

companies, thus the access to data or database on who

owns what, the harder it will be for corrupt

individuals to hide (Ownership, 2019).

A centralized database is believed to help

preventing such crimes. By implementing an

iN-LAC 2018 - International Law Conference 2018

414

adequate set of data protection law, the database

system might limit business activities (Cosgrove,

2018). The standardization and centralized collection

and maintenance of BO record or data would allow

data controllers to disclose certain data to help

authorities in investigation. This legitimate action

surely would increase the transparency in revealing

BO. Thus, it is needed that the integration among BO

data related.

In a fact, there are certain technical and

bureaucracy matters in incorporating such related

data. In Indonesia, different information is hold by

different authorities/ministries. For example, banking

account is hold by bank, legality of company is hold

by Ministry of Law and Human Rights, taxpayer

identification numbers is hold by Ministry of Finance,

while civil registration number is hold by Ministry of

Internal Affairs. It is very easy to individual or group

of individual possess certain licenses in certain sector.

Since there is no integrated data system yet, the result

will appear as struggle to expose the truth owner for

responsible in certain sector.

Certainly, creating transparency in BO disclosure

will need collaboration from such government

authorities in term of seeking single database.

Furthermore, the need of single identification number

should be prioritised.

2.3.3 The Privacy Issue

Privacy has first been defined as a legal concept as the

right to be let alone (Warren & Brandeis, 1890). The

long debate on privacy has brought more

interpretation as the right to choose seclusion from

the attention of the other (Solove, 2008). In the

context of BO disclosure, the information contains in

BO is personal data (Informatics, 2016). In this case,

the process of disclosing will be clearly removing the

nature of the BO itself. The benefit of anonymity and

privacy might not be enjoyed for the owner.

However the privacy issue in BO’s disclosure is

still debatable. Hence, BO Regulation should be

considered as a foundational element that can

strengthen the community’s efforts to address

corruption, fraud, organised crime and tax evasion

(Pradhan, 2018).

In the Indonesia context, the right to privacy is

guaranteed by the Constitution. Therefore, the

disclosing process should be construed to guarantee

the reputation of the owner. Indeed, there is should be

‘balancing principle’ since the right to privacy might

be limited in order to respect others right (Taufik,

2011).

In line with that, in disclosing such BO

information, the authorities must follow the

disclosing principles to ensure that the right to

privacy would not be infringed as stated on Article 2

Data Protection Regulation.

3 CONCLUSION

As the Labora Sitorus case and Panama Paper scandal

has illustrated, the cases were increasingly attractive

to reveal BO in Indonesia. Although the Government

of Indonesia has enacted BO Regulation, there are

concerns on the BO disclosure process. The

corporations oblige to provide a person-in-charge

who will be responsible for implementing the

principles on BO disclosure namely identification and

verification over personal information of BO. The

problem is arising when comes to the implementation

of BO Regulation. The challenge lies in corporate

compliance in disclosing BO. Another challenge are

the access to the BO information that remains limited,

the absence of BO database since there is no single

identification number which cause bureaucracy

problem among responsible authorities and the last is

the issue on privacy over disclosing personal data.

Responding to the concerns above, the

transparency issue in revealing BO would be the main

key to the authorities by ensuring the data protection

principles while corporations must comply with all

existing regulations.

REFERENCES

Alecci, S., 2018. After Panama Papers: Indonesia Urges

Beneficial Owners To Come Out Of Hiding. [Online]

Available At:

Https://Www.Icij.Org/Blog/2018/03/Panama-Papers-

Indonesia-Urges-Beneficial-Owners-Come-Hiding/

BAPEPAM, 2012. Peraturan Badan Pengawas Pasar

Modal dan Lembaga Keuangan (BAPEPAM) Kep-

431/BL/2012. s.l.:s.n.

Cosgrove, T., 2018. Dun & Bradstreet. [Online]

Available at:

https://www.dnb.com/perspectives/corporate-

compliance/fincen-national-database-bill-

proposed.html

[Accessed 15 January 2019].

FATF, 2014. FATF Guidance: Transparency and

Beneficial Ownership. s.l.:The Financial Action Task

Force.

Firmansyah, F., 2016. 803 Indonesians Named in Panama

Papers. [Online]

Available at:

The Challenges on Beneficial Ownership Disclosure in Indonesia: A Study of the Enactment of Presidential Regulation No. 13 of 2018 on

the Application of Know-Your-Beneficial-Ownership Principles by Corporations for the Prevention and Eradication of Money Laundering

and Terrorism Financing

415

https://en.tempo.co/read/news/2016/04/06/055760378/

803-Indonesians-Named-in-Panama-Papers

Informatics, M. o. C. a., 2016. Regulation of Ministry of

Communication and Informatics No. 20 of 2016

concerning Personal Data Protection in the Electronic

System. s.l.:s.n.

International, T., 2017. Corruption Perceptions Index 2017,

s.l.: Transparency International.

Keuangan, P. P. d. T., 2018. Perpres Beneficial Owner

(BO), Upaya Cegah Korporasi Digunakan Oleh Pelaku

Tindak Pidana.

s.l.:http://www.ppatk.go.id/siaran_pers/read/775/perpr

es-beneficial-owner-bo-upaya-cegah-korporasi-

digunakan-oleh-pelaku-tindak-pidana-.html.

Kingdom, D. f. B. I. a. S. t. U., 2014. Understanding the

New Requirements, Recording Control on the PSC

Register and Protecting People, s.l.: Department for

Business Innovation and Skills the United Kingdom,

The Register of People with Significant COntrol (PSC)

Register.

Lie, V. A., Ariananto, A. & Lestari, R. I., 2018.

www.makarim.com. [Online]

Available at:

http://www.makarim.com/uploads/839021_Advisory

%20-%20Indonesia%20Introduces%20Know-Your-

Beneficial%20Owner%20Principle%20for%20Corpor

ations%20(20%20March%202018).pdf

[Accessed 21 January 2019].

Maulia, E. & Suzuki, W., 2017. Indonesia’s Tax Amnesty

Fails To Bring Money Home. [Online]

Available at:

https://asia.nikkei.com/Economy/Indonesia-s-tax-

amnesty-fails-to-bring-money-home

Nuruliza, A. T., 2016. Disclosure of Ultimate Beneficial

Ownership in Indonesia. s.l.:Tilburg University.

OECD, 2016. Disclosure of Beneficial Ownership and

Control in Listed Companies in Asia 2016, Bangkok:

OECD.

Ownership, O., 2019. https://openownership.org/. [Online]

Available at: https://openownership.org/

[Accessed 15 January 2019].

Pradhan, S., 2018. Open Government Partnership. [Online]

Available at:

https://www.opengovpartnership.org/stories/can-

beneficial-ownership-transparency-really-be-

compatible-data-protection)

Rini, R. A. W. S., 2016. Beneficial Ownership

Transparency, State Revenue and EITI, s.l.: PWYP

Indonesia; Natural Resource Governance Institute.

Solove, D. J., 2008. Understanding Privacy. Cambridge,

Massachusetts: Harvard University Press.

Somba, Y. P. & Dharma, N., 2013. Papua police hand over

Labora Sitorus' dossier to prosecutors. [Online]

Available at:

https://www.thejakartapost.com/news/2013/07/26/pap

ua-police-hand-over-labora-sitorus-dossier-

prosecutors.html

Taufik, G. A., 2011. Identifying the Traces of Particularity

in Indonesia Freedom of Expression. Bangkok, s.n.

Warren, S. & Brandeis, L., 1890. The Right to Privacy.

Harvard Law Review.

iN-LAC 2018 - International Law Conference 2018

416