Risk Mitigation of Cattle Livestock in Indonesia:

Problematic in Insurance Scheme

Ari Prasetyo

12

, Dian Purnama Anugerah

3

, Ria Setyawati

3

1

Economic and Business Faculty of Universitas Airlangga, Indonesia

2

Vocational Faculty of Universitas Airlangga, Indonesia

3

Law Faculty of Universitas Airlangga, Indonesia

Keywords: cattle, insurance, indonesia, risk, mitigation.

Abstract: The number of local cattle in Indonesia is not sufficient for national needs. As a result, the price of beef in the

market is increasing from year to year. The problem of import quota of beef is actually can be overcome if

Indonesia is able to realize food self-sufficiency in the livestock sector. Ministry of Agriculture issued a policy

emphasized on increasing the amount of credit disbursement for farmers and ranchers. In addition to lending,

the Government of Indonesia launched insurance products based on Crop Insurance and Livestock Insurance.

In this paper constrained by two issues, the first is whether the regulation on the risks borne by Cattle

Livestock Insurance has provided protection for cattle ranchers in Indonesia. The second problem is how the

Cattle Livestock Insurance Model Regulation based on the principle of benefit to achieve self-sufficiency in

food. Appropriate arrangements related to livestock insurance should focus on protecting farmers from losses

due to crop failure, and food sufficiency for the Indonesian community. Legal uncertainty related to the

acquisition of losses from farmers who have followed the livestock insurance program will actually bring

harm to farmers and for the entire people of Indonesia.

1 INTRODUCTION

Beef consumption in Indonesia is still relatively low

compares to the neighboring countries such as

Singapore and Malaysia. According to the 2015 data,

the average need of beef is 2.2 kilograms per capita

per year (Dyah, 2015). That number is still

categorized as low considering the 255 million

population of Indonesia. Even though beef

consumption is low, but the needs are still high.

According to the 2015 data, the need for beef is

653,000 tons or equivalent with 3,657,000 cattle.

Meanwhile, the local cattlemen can only produce

406,000 tons of beef or equivalent to 1,318,000 cattle

(Dyah, 2015). Therefore, there is still 1.5 million of

cattle deficiency per year. As the result, the price of

beef is rising from year to year.

To anticipate the deficiency of beef stock and to

repress its price in market, the government imported

beef from various countries such as America,

Australia, India, and others. The government’s

decision to import cattle gave the excess to the

establishment of cattle import quota. Importers then

compete to seize the biggest quota with using illegal

actions. In 2011, the issue of cattle import rose to the

surface again. That cattle import scandal has dragged

some party officials, representative members, and

cattle importers (Tempo.co, 2013). The import quota

became an issue again when the Justice of

Constitutional Court, Patrialis Akbar, was presumed

to be bribed regarding the case verdict number

129/PUU-XIII/2015 on the judicial review of Law

No. 41 year 2014 about Animal Husbandry and

Health (Pratiwi, 2017).

The problem of import quota actually can be

resolve only if Indonesia is self-sufficient in livestock

sector especially regarding the cattle. Low

technological capability in the field of cattle is the

problem faced by Indonesian cattlemen. Therefore,

the productivity of cattle cannot be maximized. Due

to the low technological capability, cattle breeding

management cannot produce qualified cattle for

proper cutting. Other than that, diseases that attack

cattle cause a big loss for the cattlemen and the

venture capital becomes the problem to be able to rise

again (Sitanggang, 2015).

The Ministry of Agriculture through Directorate

General of Animal Husbandry and Health tried to

Prasetyo, A., Anugerah, D. and Setyawati, R.

Risk Mitigation of Cattle Livestock in Indonesia: Problematic in Insurance Scheme.

DOI: 10.5220/0010052203850390

In Proceedings of the International Law Conference (iN-LAC 2018) - Law, Technology and the Imperative of Change in the 21st Century, pages 385-390

ISBN: 978-989-758-482-4

Copyright

c

2020 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

385

increase the productivity by making cooperation with

Financial Service Authority (OJK). This cooperation

developed Program AKSI Pangan which in one of its

policies emphasized on increasing the amount of

credit for farmers and breeders also to launch the

insurance based on Crop Insurance and Livestock

Insurance known as Asuransi Usaha Tanam Padi

(AUTP) and Asuransi Usaha Ternak Sapi (AUTS)

(Sidik, 2017). These programs were launched in 2016

and still become the priority in 2017.

Asuransi Usaha Ternak Sapi or Cattle Business

Insurance (hereinafter AUTS) is accordance with the

mandate of Law No. 19 Year 2013 about Protection

and Empowerment of Farmers. This law, then, was

followed up by Regulation of Minister of Agriculture

No. 40/Permentan/SR.230/7/2015 about Farming

Insurance Facility. Initially, there was insurance

corporate consortium that offered the insurance to

Indonesian cattlemen. However, since 2017, there is

only P.T. Asuransi Jasindo which still offers the

insurance. This is because according to Article 28 of

Law No. 19 Year 2013, the state government and

regional government based on its authority assign the

state-owned company or regional-owned company in

the field of insurance to conduct agricultural

insurance (Hana, 2016).

According to the background above, the

formulation of issues to be studied are: First, has the

regulation about risks covered by Cattle Business

Insurance (AUTS) already give protection to the

Indonesian cattlemen? Second, regulation model

about Cattle Business Insurance (AUTS) which based

on the principle of benefits to achieve food self-

sufficiency.

This research is normative (doctrinal) legal

research. It means that the research relating to library-

based academic activities. This study focuses its

analysis on primary and secondary legal materials

that can be accessed.

The approach to the problem used in this study is

the statute approach and the conceptual approach.

The statute approach was chosen because this study

will examine various laws and regulations relating to

the problems formulated in this study. The conceptual

approach will be used in this study intended to gain

an understanding of the concepts, notions, doctrines,

legal principles and views of scholars regarding

Livestock Insurance.

2 THE RISK OF CATTLEMEN IN

INDONESIA

There were 16,599,247 cattle in Indonesia in 2017.

This number increased by 529,150 cattle from the

previous year. In East Java itself, the population of

cattle from 2017 reached 4.511.613 cattle by

producing 96.917 tons of beef production. From these

data, the government has a technical plan or

foreseeable data of the increasing number of cattle for

2018 until 2020. The Animal Husbandry Department

Office of East Java Province itself has a technical plan

for the number of beef cattle for 2018 amounting to

4,657,564, then 2019 as many as 4,808,236, up to

2020 it is expected that cattle can reach 4,963,783. It

is also expected to increase beef production to lead to

food self-sufficiency with production of 104,369 tons

in 2020 (Badan Pusat Statistik, 2017).

However, there are some problems in order to

improve the quality and quantity of cattle. In addition

to productivity issues, in practice, the business of beef

cattle is faced with various perils and risks. There are

several conditions faced by the people's beef

business, namely 1) price, 2) disease, 3) feeding, 4)

marketing, 5) theft, and 6) relationship with traders,

with different main risks depending on the central

region production. The death of cattle can be caused

by several things such as death due to illness, death

from childbirth, and death due to natural disasters.

Some of the largest cattle deaths are caused by the

Jembrana virus. Referring to the data from the

Department of Animal Husbandry and Food Security

of the Province of South Sumatra, the number of Bali

cattle that died due to Jembrana virus infection during

2017 was 200 cattle (Inge, 2018). In addition,

residents of Muaro Jambi regency were stunned by

the death of more than 500 cattle due to the same virus

(Santoso, 2018). From the data compiled by the East

Java Provincial Livestock Service, in 2015 to 2017

there were several cases of diseases that infected

cattle. Among them are three cases of anthrax and 43

cases of brucellosis in East Java. Moreover, the

Septicaemia Epizo Otica disease or snoring cow

disease (Bere, 2017) is also a factor of death in cattle.

The cause of the death of another cattle is death due

to childbirth. Due to the inadequate care and fatigue

of delivery, as many as 35 Brahman cross cattle in

North Penajam Paser District, East Kalimantan, died

during childbirth (Kokino, 2016). Natural disasters

such as floods and volcanic eruptions also become

one of the perils supporting the death of cattle.

Ministry of Agriculture (Kementan) stated that the

total cattle that died from the eruption of Mount

Merapi has been identified to reach 1962 cattle

iN-LAC 2018 - International Law Conference 2018

386

(Sudarsono, 2010). In addition, cattle that are kept

shepherd have a high likelihood of contracting

parasitic diseases. The main disadvantages due to

parasitic diseases are emaciation, late growth,

decreased resistance to other diseases and metabolic

disorders (Sudardjat, 2017).

Another peril is a cattle theft. The cattlemen

associated in Cattle Association of Suka Tani in

North Sangatta, East Kutai district complained that

they often lose their pregnant cattle (Hazliansyah,

2012). Meanwhile, in Putat Village, Cirebon District,

approximately eight cattle were stolen from its

cowshed. Not only that, the death of cattle during the

transfer of distribution also be a peril of its own. By

mid-2015, approximately 12,000 cattle died when

shipped over the sea. The cattle distributed from East

Nusa Tenggara were dying because the temperature

of the cargo ship is too hot. The peril happened in

shipping caused a lot of risk to be borne

(Iskandarsjah, 2015).

2.1 Indonesia Regulation on Cattle

Insurance

The basic matters regarding livestock and health are

regulated in Law No. 67 Year 1967 concerning Basic

Provisions on Animal Husbandry and Animal Health.

In essence, this Law regulates in several chapters

namely General Provisions, Animal Husbandry,

Animal Health, as well as the provisions of sanctions

and transitions. The next regulation is Law No. 18

Year 2009 and its amendment of Law No. 41 Year

2014 on Animal Husbandry and Animal Health.

While the regulations referring to the protection of

breeders are regulated in Law no. 19 Year 2013 on

the Protection and Empowerment of Farmers.

Furthermore, as mandated by the law, there is

Government Regulation No. 6 Year 2013 on

Empowerment of Livestock Breeders.

In accordance with Article 1 number 1 of Law No.

6 Year 2013, Farmers Empowerment is all efforts

made by the Government, provincial government,

district / city government, and stakeholders in the

field of Animal Husbandry and Animal Health to

enhance the independence, facilitate and improve

business, and improve the competitiveness and

welfare of livestock breeders. Therefore, the

government made efforts in the form of cattle

business insurance to increase productivity and

reduce risk by doing mitigation. AUTS is then

regulated in detail on the Decree of the Minister of

Agriculture No. 56 / Kpts / SR.230 / B / 06/2016

regarding the Guidance of Insurance Premium for

Cattle Livestock Business Insurance. The Decree of

the Minister of Agriculture regulates the basic rules

and regulations in carrying out the AUTS.

2.2 Cattle Lifestock Business Insurance

According to the Cattle Business Insurance Premium

Assistance Guidelines, AUTS is an agreement

between an insurance company as an insurer and a

farmer as an insured where by accepting insurance

premiums, the insurance company will compensate

farmers because cattle die due to illness, accidents

and breeding, and / or loss under the terms and

conditions of the Insurance Policy. Criteria that must

be met by farmers to insure their cattle are cattlemen

who conduct business of cattle nurseries and / or

breeding or small-scale cattle breeders in accordance

with the provisions of the legislation. The cattle that

can be insured are female cattle in healthy condition,

at least 1 (one) year old and still productive. In

addition, cattle must also have identity markings such

as microchips or ear-tags.

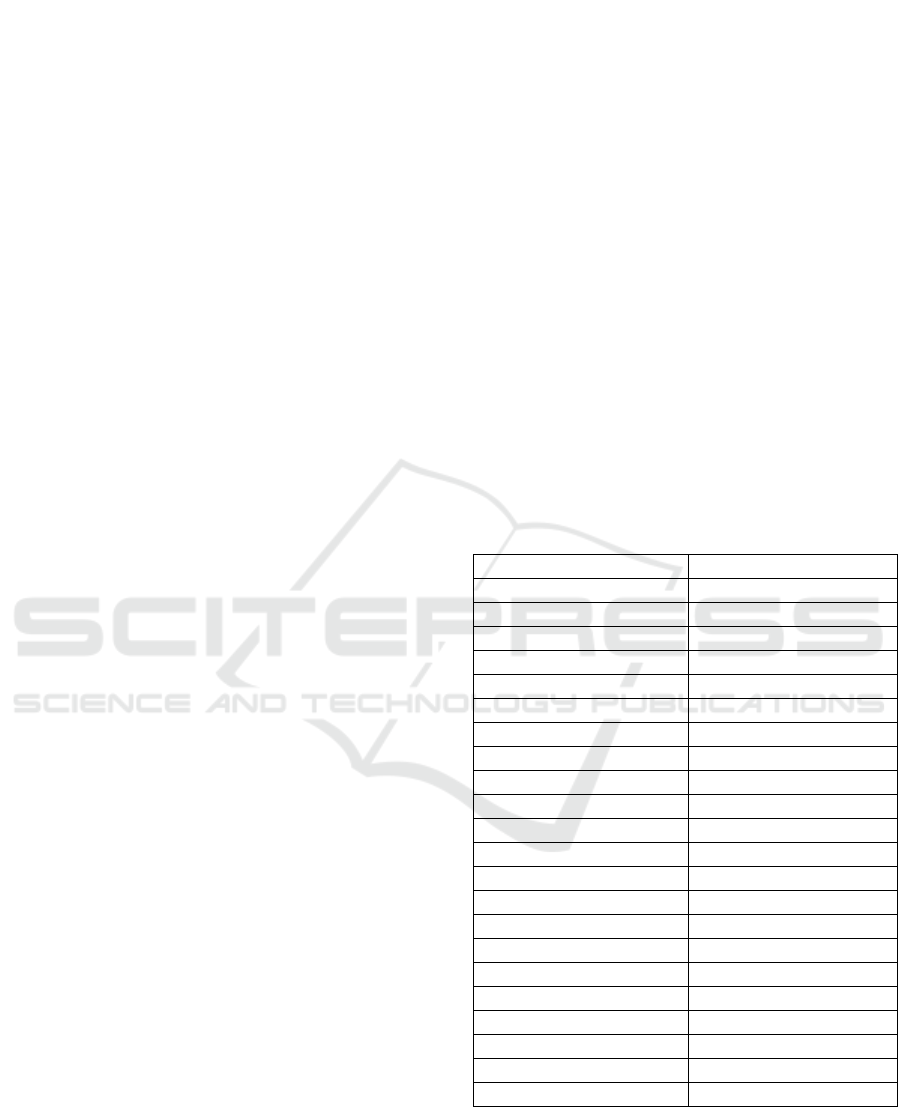

Until 2018, in East Java alone has been recorded

as many as 6.678 participants of Cattle Livestock

Business Insurance with the following details:

City Number of Cattle

Jombang 295

Probolinggo 164

Ngawi 349

Tulungagung 417

Lumajang 362

Lamongan 508

Kediri 122

Mojokerto 254

Pamekasan 60

Bondowoso 13

Nganjuk 174

Malang 1.205

Probolinggo 874

Ponorogo 254

Pacitan 322

Pasuruan 320

Bojonegoro 69

Madiun 165

Sidoarjo 132

Blitar 133

Magetan 235

Batu 251

Source:East Java Animal Husbandry Department

Risks covered in the AUTS include cattle deaths

due to illness, accident, and childbirth. The risk of

cattle lost due to theft is also the scope of perils

guaranteed by the AUTS. The coverage price for each

Risk Mitigation of Cattle Livestock in Indonesia: Problematic in Insurance Scheme

387

cattle is up to 10,000,000 (ten million) rupiah. As for

the amount of premiums that must be paid by farmers,

is 20 percent from 2 percent of the price of cattle

coverage, which is 40,000 rupiah per cattle per year.

The coverage price of cattle is the nominal price of

cattle acquisition without the addition of other costs

agreed upon by the Insured and the Insurer. The total

sum insured is the sum of the price of the entire cattle.

The sum Insured is the basis for calculating the

premium, and is the maximum amount of

compensation. However, as for the term of coverage

is 1 (one) year started since the payment of insurance

premiums.

The AUTS implementation mechanism involves

several agencies. In general, the implementation

mechanism begins with the socialization of the

Department of Animal Husbandry of the Regency /

City so that it can invite the breeders / breeder groups

to register themselves. Subsequently, the District /

Municipal Animal Husbandry Office conducted data

collection and inventory of Participant Candidate

Location Candidate (CPCL) to the Provincial Animal

Husbandry Department and provided the participant's

temporary data to the insurance company to verify the

feasibility. Cattle breeders who have been declared

eligible to become AUTS insured can pay the

premiums to the insurance company and then the

company will issue the insurance policy certificate.

Proof of payment and insurance policy certificate are

then also reported to the District Animal Husbandry

Department by the insurance company so the

Provincial Animal Husbandry Department can issue

a definitive list of participants. The list of Definitive

Participants is recapitulated by the Directorate

General of Animal Husbandry and Animal Health and

declared as AUTS List of Participants by the

Directorate General of Infrastructure and Livestock

Facilities of the Ministry of Animal Husbandry. With

this, the Directorate General of Infrastructure and

Livestock Facilities of the Ministry of Animal

Husbandry can pay the subsidized insurance premium

of 80 percent of the insurance coverage of 2 percent

of the insurance company.

Moreover, to file a claim, the insured breeder must

have paid the premium according to the provisions,

the potential death of the insured cattle, and the death

of the cattle and/or loss within the coverage period. If

there is a potential claim, the insured may be able to

immediately notify the claimant to immediately be

examined and take mitigation measures such as

ordering to cut cattle or sell them immediately. The

results of the acquisition / rescue will be calculated as

a deduction from the number of claims that will be

obtained by the insured. If the cattle are lost due to

theft, then the replacement of the claim will be

reduced by its own risk to a maximum of 30 percent

of the insurance price. In the case of payment of

claims that have been approved and verified, the

implementing insurance company must pay claims up

to 14 working days from the date of claim approval.

AUTS implementation is not without risk. The

risk that may occur is not achieving the realization

target of distribution of premium assistance because

lack of understanding of farmers and objections to

paying the premium that has been determined.

Another risk that may be faced is less precise target

of subsidized insurance premium. Therefore, in order

to prevent the occurrence of these things, the

preparation of detailed guidelines is needed. In

addition, socialization and assistance are also needed

by the cattle breeders as AUTS targets.

2.2.1 The Idea for Regulatory Model for

Livestock Business Insurance

The implementation of AUTS in Indonesia is

conducted by PT Asuransi Jasa Indonesia (PT

Asuransi Jasindo). In accordance with the guidelines

previously discussed, PT Asuransi Jasindo acts as the

underwriter of the insured which is the cattlemen who

enroll and pay the premium. The risks covered by PT

Asuransi Jasindo in its AUTS products are only for

cattle deaths due to illness, accident, and childbirth

and cattle losses due to theft. The coverage of the

above risks is quite narrow compared to some

countries that offer similar insurance to

farmers/cattlemen.

In terms of the amount of coverage provided by

AUTS, the sum insured of 10 million is sufficient for

one cattle with a premium cost of 40,000 per year.

Prices of cattle on the market are varied depending on

the type, age, and weight of the cattle. With the sum

insured, cattlemen/breeder can get a calf depending

on the types. For limousine-type calf sold at a price

range of 8 million to 12 million for male calf and 3

million for female calf. While for PO calf that are

most commonly found, are sold at prices ranging

from 7 million to 11 million rupiah for males and 3

million for female calf. As for Brahman cross cattle,

the calf is sold at a price range of 6 million to 9

million rupiah. For the price of semi-adult cattle

closest to the coverage given is a Brahman cross type

cattle that is sold at a price of 14 million rupiah

(Agrobisnisinfo.com, 2018).

We compare cattle insurance in several countries

such as United States, India and New Zealand

regarding the coverage of protection against perils.

These three countries were chosen because they were

iN-LAC 2018 - International Law Conference 2018

388

the largest meat exporters to the Indonesian market.

According to Badan Pusat Statistik (BPS), in 2017,

the values of imported beef from India reaches 45

thousand tons with a value of US $ 166 million. The

third largest was The United States with 14.4

thousand tons worth US $ 55.98 million. Meanwhile

New Zealand was ranked fourth with the total 13.6

thousands ton. (BPS, 2018)

In New Zealand, one of the insurance companies

providing livestock insurance is FMG Advice and

Insurance. The scope of risks borne by the company

is wide and detailed. For the protection of livestock in

open air, the risk of death is borne by several causes

of death, such as death from fire, electric shock,

lightning, sudden, external, and visible impact of

violence, stress, explosion, shortness of breath due to

smoke of fire, lightning, or explosions, hail,

earthquakes, floods, objects falling from aircraft. As

for the cattle that are indoors, the scope of the risk

includes sudden death or theft. In addition, FMG

Advice and Insurance also provides protection when

livestock dies while transported and accidents occur.

The death of cattle due to poisoning can also be

covered by the insurance offered by FMG. The

insurance company also offers the disposal of dead

animal carcasses either because of illness or because

of other reasons. Preventive measures such as

servicing by a veterinarian to prevent cattle death also

become the scope of the offered insurance facility. All

risks will be borne according to market price up to the

amount stated on the farmer's livestock certificate.

Similar to New Zealand, Trusted Choice

insurance company in America also provide livestock

insurance with a wide range of risk scopes. According

to the company, the coverage of livestock insurance

risks is divided into comprehensive coverage and

limited coverage. Comprehensive coverage is a wide

range including accidents, illnesses, and theft. While

limited coverage is a scope that specifically mentions

the cause of the risk to livestock including accidents

due to drowning, being shot, loading and unloading,

falling objects, fires, smoke, electric shock, and

explosions; flood, lightning, wind, and hail; natural

disasters such as earthquakes, volcanoes, and

sinkholes; theft and vandalism; damage to water and

heating systems; animal attacks; as well as collisions

or other causes of death while transporting the cattle.

Meanwhile, in India, HDFC ERGO with its Cattle

Insurance Policy product offers to bear the risk of

livestock death covering the insured cattle within the

geographic area specified in the policy, in case of life

loss due to accident, illness, or surgery. The policy

also covers livestock deaths that are insurance issues

that occur outside of the geographical area during

droughts, epidemics and other natural disasters.

From the example of livestock insurance

companies from several countries above, there are

some differences in the coverage of risks that can be

borne by the insurance company. Insurance

companies in New Zealand and the United States,

according to the example above, provide a wide range

of risks for the insured when the livestock is dying or

other things that jeopardize the cattlemen. On the

other hand, AUTS in Indonesia provided by PT

Asuransi Jasindo only provides protection on the

limited perils. PT Asuransi Jasindo only bears the risk

of cattle death due to certain causes of accidents,

illness and childbirth. Cattle lost due to theft will also

be borne by PT Asuransi Jasindo with its own risk

reduction.

Risk coverage is considered not enough

considering the location of the majority of cattlemen

in Indonesia with geographical conditions that allow

natural disasters such as volcanoes erupt or

landslides. Therefore, in order to meet the needs and

attract more cattlemen, the coverage of risk protected

by the company can be expanded by adding some

events that pose a risk of loss to cattlemen such as

erupting volcanoes or landslides. Not only that, the

security of the distribution of cattle between islands

must also be protected by providing a range of risks

for cattle deaths due to peril of transfer or distribution.

3 CONCLUSIONS

Regulations regarding the risks in Cattle Livestock

Insurance have not provided sufficient protection for

cattle farmers in Indonesia. Decree of the Minister of

Agriculture of the Republic of Indonesia No. 56 /

Kpts / SR.230 / B / 06/2016 is made to provide basic

settings and formats for running AUTS. The risks in

AUTS include deaths due to illness, accidents, and

childbirth. Therefore, in order to prevent the

occurrence of these matters, the preparation of

detailed guidelines is needed. In addition,

socialization and assistance are also needed by

farmers as the target of AUTS.

The risk coverage is considered in adequate given

the location of the majority of cattle farmers in

Indonesia with geographical conditions that allow

natural disasters such as erupting mountains or

landslides. Therefore, in order to meet the needs and

capture more cattle breeders in the regions, the risk

coverage protected by AUTS can be expanded by

adding a number of events that pose a risk of loss to

cattle farmers. Not only that, the safety of inter-island

Risk Mitigation of Cattle Livestock in Indonesia: Problematic in Insurance Scheme

389

distribution of cattle must also be protected by

providing coverage of the risk of death due to

displacement or distribution.

REFERENCES

Tempo.co, 2013. [Online] Available at:

https://nasional.tempo.co/read/458101/suap-daging-

pks-begini-awal-mulanya [Accessed 29 June 2018].

Pratiwi, P. S., 2017. [Online] Available at:

https://www.cnnindonesia.com/nasional/20170206124

716-12-191557/dalami-kasus-patrialis-kpk-periksa-

pemohon-uji-materi? [Accessed 21 June 2018].

Sitanggang, N., 2015. [Online] Available at:

http://agribisnis.co.id/atasi-kendala-ternak-sapi-untuk-

hasil-memuaskan/ [Accessed 26 June 2018].

Sidik, F., 2017. [Online] Available at:

http://finansial.bisnis.com/read/20170324/215/640046/

ojk-dorong-penyaluran-kredit-asuransi-pertanian-

peternakan [Accessed 24 July 2018].

Hana, O. D., 2016. [Online] Available at:

http://finansial.bisnis.com/read/20160406/215/535045/

asuransi-ternak-sapi-tahun-ini-tanpa-konsorsium

[Accessed 24 July 2018].

Badan Pusat Statistik, 2017. Populasi Sapi Potong menurut

Provinsi, 2009-2017. [Online] Available at:

https://www.bps.go.id/linkTableDinamis/view/id/1016

[Accessed 7 August 2018].

Sudardjat, S., 2017. Epidemiology of Animal Diseases Vol.

1, Jakarta: Directorate of Animal Health Development.

Iskandarsjah, E., 2015. [Online] Available at:

https://www.republika.co.id/berita/ekonomi/makro/17/

08/02/dpd-ri/berita-dpd/15/06/24/nqg3w6-dpd-20-

persen-sapi-dari-dan-%20ntt-die-when-delivery

[Accessed 8 August 2018].

Agrobisnisinfo.com, 2018. [Online] Available at:

http://www.agrobisnisinfo.com/2018/01/harga-sapi-

2018-semua-jenis-limousin.html [Accessed 7 August

2018].

Inge, N., 2018. [Online] Available at: www.liputan6.com:

https://www.liputan6.com/regional/read/3297390/17-

tahun-berlalu-virus-jembrana-kembali-jangkiti-sapi-di-

sumsel

Santoso, B., 2018. [Online] Available at:

www.liputan6.com:

https://www.liputan6.com/regional/read/3230496/pulu

han-sapi-di-cianjur-mati-mendadak-terserang-virus-

apa

Bere, S. M., 2017. [Online] Available at:

https://regional.kompas.com/read/2017/01/30/1236207

1/puluhan.sapi.mati.mendadak.diduga.terjangkit.penya

kit.se

Kokino, I., 2016. [Online] Available at:

http://www.kalamanthana.com:

http://www.kalamanthana.com/2016/07/09/5-persen-

sapi-brahman-cross-penajam-mati-saat-melahirkan-

ada-apa/

Sudarsono, 2010. [Online] Available at:

https://news.okezone.com/read/2010/11/15/340/39361

7/hampir-2000-sapi-mati-akibat-letusan-merapi

Hazliansyah, 2012. [Online] Available at:

https://www.republika.co.id/berita/nasional/umum/12/

05/02/m3dmnm-peternak-sangata-mengeluh-sering-

kehilangan-sapi

Dyah, 2015. [Online] Available at:

https://www.antaranews.com/berita/527724/konsumsi-

daging-sapi-orang-indonesia-masih-rendah

[Accessed 20 June 2018].

BPS, 2018. [Online] Available at:

https://databoks.katadata.co.id/datapublish/2018/03/22

/separuh-impor-daging-indonesia-dari-australia

iN-LAC 2018 - International Law Conference 2018

390