The Influence of Financing Against Profitability at Bank Syariah in

Indonesia in General 2010-2016

Yola Yunisa Pratami, Kusnendi Kusnendi and Heraeni Heraeni

Economics and Islamic Finance Department, Universitas Pendidikan Indonesia, Jl. Dr. Setiabudhi, Bandung, Indonesia

risa.sari.pertiwi@student.upi.edu

Keyword: trade financing, profit-loss sharing financing, lease financing, profitability (ROA).

Abstract: The aim of this study is to test empirically about effects of trade financing, profit-loss sharing financing, and

lease financing to profitability rate. The objects that used in this study is seven Islamic Commercial Banks

which giving the three types of financing in 2010-2016 period. This research uses quantitative approach by

using panel data. The data analysis technique in this study uses panel data regression with common effect

model. The results of study show that trade financing and lease financing have positive effect on

profitability. Therefore, profit-loss sharing financing has negative effect on profitability. The result of

simultaneous regression show that three types of financing have effect on profitability.

1 INTRODUCTION

Market share and increasing Islamic banking assets

have not showed a better performance than

conventional banking, particularly the level of

profitability as measured by ROA. The Financial

Services Authority data (2017) pointed out that ROA

on public Bank Syariah (BUS) is much lower than

with a conventional public Bank (BUK). In

December 2016 level ROA on the BUS of 0.63

percent while ROA on the THUMP of 2.23 percent.

Low levels of ROA on the BUS means that

managerial BUS performance and less efficient asset

utilization (Marbelanty and Adityawarman, 2015).

Islamic banks serve as the intermediary

institutions that connect between the parties that

have excess funds and those who require funding

through financing activities. Financing is a product

of channeling funds Islamic banking which became

the Foundation of the survival efforts of Islamic

banking and can support the growth of Islamic

banking market share nationwide.

Based on Sharia Banking Statistics data

published by the financial services authority (2017),

financing is channeling funds between the highest

types of channeling funds to each other. On average

the share of remittances in the form of financing

during the year 2014 to 2016 is over one hundred

per cent of the total funds disbursed, the rest is

channeled through placement in Bank Indonesia,

placement in other banks, investment securities, and

inclusion.

Islamic banking is generally provides funding in

three contract, such contract and selling (murabaha,

greetings, and istishna), sharing (mudharabah and

musyarakah) and rent (ijarah). Among the three

types of financing, financing and selling is a product

of the most sought after by most customer financing,

especially the use of contract murabahah.

Based on statistical data of Sharia Banking the

financial services authority (2017), through the year

2016 total funds from these three types of financing

are disbursed is Rp. 173,599 billion. Financing and

selling got 63 percent of the total parts financing

channelled BUS, followed by the financing for the

results amounted to 36 percent of the total financing,

and amounted to one percent of the total financing is

a financing lease.

The reason the large number of product use and

selling financing is marked up and sure enough

transactions and ease compared to the profit and loss

sharing, so that the bank is able to obtain

comparable to banking conventional interest-based

(Rahman and Rochmanika, 2012). In addition, the

financing for the results is financing the second

transmitted after financing and selling. The cause is

the financing for the results have the biggest risk

levels whereas financing in the form for these results

is the main operational principles of Islamic banking

and impacting directly to economic growth (Hadi,

2011).

782

Pratami, Y., Kusnendi, K. and Heraeni, H.

The Influence of Financing Against Profitability at Bank Syariah in Indonesia in General 2010-2016.

In Proceedings of the 1st International Conference on Islamic Economics, Business, and Philanthropy (ICIEBP 2017) - Transforming Islamic Economy and Societies, pages 782-786

ISBN: 978-989-758-315-5

Copyright © 2018 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

According to Muhammad (2002) is a non-profit

or profit in Islamic banking can be obtained from the

margin of the selling price of the financing of the

sale, the share of business results of the financing for

the results, the results of the ijarah contract rent, as

well as fee and the administrative fee upon services

others. This is supported by the research of Izhar and

Asutay (2007) which revealed that the portion of the

income of the bank from channeling financing

generally positive effect against the probitabilitas

Islamic banks.

2 METHODOLOGY

Approach this research using a quantitative approach

(Tanjung and Dewi, 2013). Based on the methods

used in this research is quantitative research of

causality (Muhammad, 2008). Based on the goal of

this research including research into verifikatif

(Arikunto, 2006). The object in this study is the

amount of funds channelled financing of financing

and selling, for results, and rent, as well as the

profitability measured by ROA. This research will

be conducted on annual financial reports published

by the seven companies public Bank Syariah (BUS)

in Indonesia. Research related to financing and

selling was done by Abusharbeh (2014) in his

journal holds that the relationship of distribution

financing and selling a positive effect towards

profitability

Data analysis techniques used in this research is

the analysis of the influence of the test through the

panel data regression testing (regression pooling).

According to Rosadi (2012) data panel is "Data that

presents a number of variables over some categories

and collected in a specific time period for the

observed". In panel data regression analysis there are

three approaches to parameter estimation techniques

of regression model data between other panels

common effect, fixed effects, and random effect.

3 RESULTS

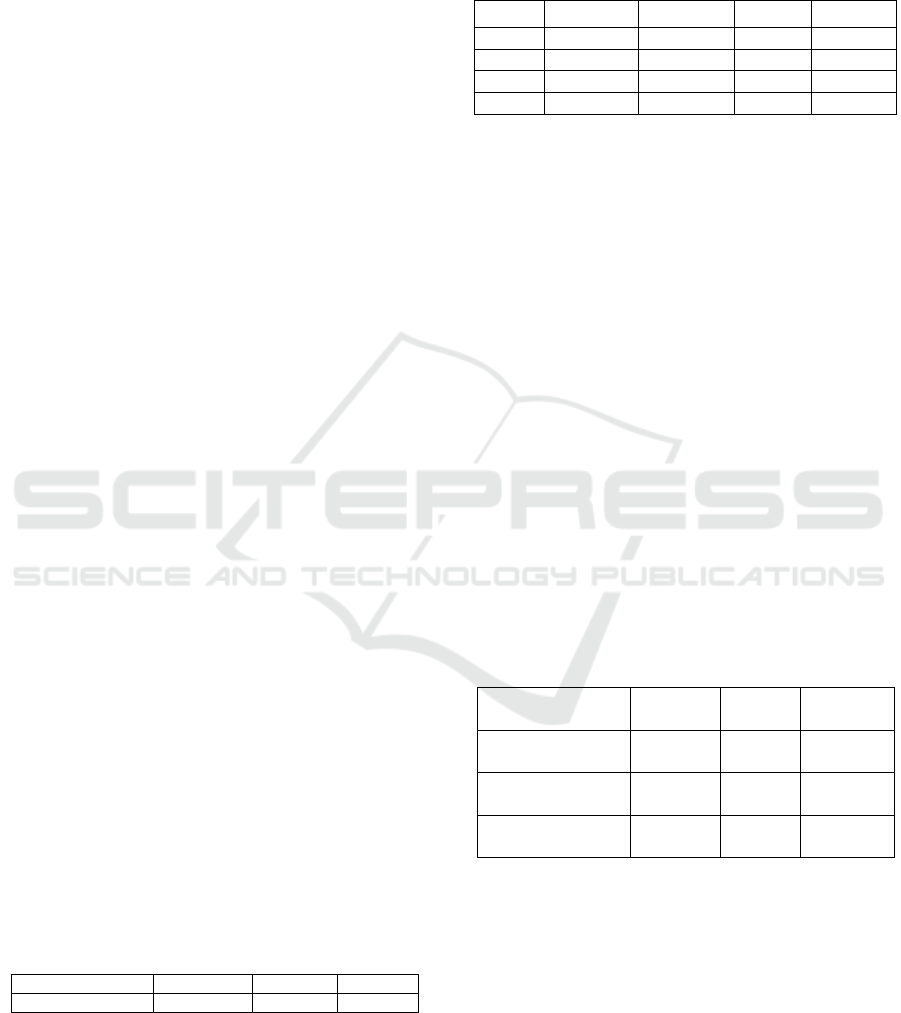

Table 1: The Result of Test Chow.

Effects Test Statistic d.f. Prob.

Cross-section F 0.944164 (6,39) 0.4750

Source: Research Result (2017).

Based on table 1, the test results with the Test

value indicated that Chow Prob Cross-section F of

0.4750 or more than 0.05. Thus, this research can

perform regression analysis by using the common

model of the effect and the Test Hausman is not

necessary

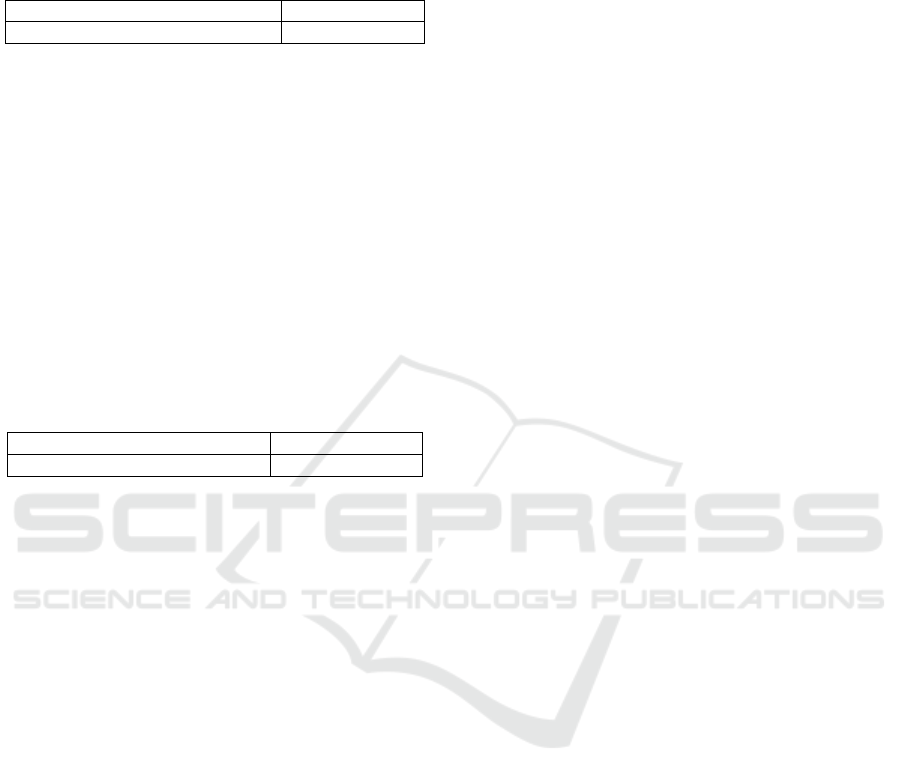

Table 2: Panel Data Regression Results.

Variable Coefficient Std. Error t-Statistic Prob.

C -1.017704 0.900791 -1.129788 0.2646

X1 0.317748 0.105130 3.022443 0.0041

X2 -0.327017 0.104125 -3.140625 0.0030

X3 0.146372 0.049888 2.934007 0.0053

Source: Research Result (2017).

Based on the results of the regression test output

in table 2 regression equations were obtained with

the model of common effect, namely:

Y = -1,017704 + 0,317748X

1

– 0,327017X

2

+

0,146372X

3

Y = -1,017704, This means that if none of

these three types of financing are provided

then the level of profitability of the BUS

which was projected with the ROA will

decrease amounting to 1.017704 percent;

β

1

= 0,317748, This means that any increase in

rupiah financing and selling one provided,

level of profitability also increased by

0.317748 percent;

β

2

= -0,327017, This means that every rise of

one rupiah financing for the results provided

will lower the profitability rate of 0.327017

percent;

β

3

= 0,146372, This means that every rise of

one lease financing given the rupiah will raise

the level of profitability of 0.146372 percent.

Table 3: The t-test Result.

Variable Value t Table t

Prob. T

Value

Financing

Selling (X1)

3,022443 1,67943 0,0041

Financing for

Result (X2)

-3,14062 1,67943 0,0030

Financing Lease

(X3)

2,934007 1,67943 0,0053

Source: Research Result (2017).

Based on table 3, the value t calculate on the

third independent variable is greater than the value

of t and t probability values tabulated in the third

independent variable is below the value significance

of 0.05. So the third type of influential and

significant funding towards profitability. Variable

selling and financing financing lease has influence

with the direction of the relationship is positive

while the financing for the results variable has

The Influence of Financing Against Profitability at Bank Syariah in Indonesia in General 2010-2016

783

influence with the direction of the relationship is

negative.

Table 4: The F-Test Result.

F-statistic 7.576816

Prob(F-statistic) 0.000332

Source: Research Result (2017).

In table 4, the value of F tables obtained from the

values of the numerator and denominator df df. With

the provisions of the value k = 4 and the value of df

is the denominator (N2) is 45 where N2 = n – k = 49

– 4 = 45 and the value of df is the numerator (N1)

was where N1 = k-1 = 4-1 = 3. The value F table

with 0.05 significance is 2.81. Based on the results

of a regression test in table 5 were obtained F value

count of 7.576816. Thus the value of F F table value

> count and value probability 0.05 significance level

< F. This test result is obtained that third F

independent variable affect the dependent variables

simultaneously (profitability).

Table 5: The R

2

Result.

R-s

q

uare

d

0.335602

Ad

j

usted R-s

q

uare

d

0.291308

Source: Research Result (2017).

Based on the regression results shown in Table 5

retrieved value R2 of 0.335602 and the adjusted R2

value (Adjusted R-squared) of 0.291308. This means

that 33.5602 percent of profitability can be

explained by a third independent variable (financing

and selling, financing for results, and lease

financing). As for the 66.4398 percent of affected by

other factors that are not included in the regression

model.

Results of testing the hypothesis concerning the

influence of financing and selling against the

profitability of selling financing showed that

positive effect significantly to profitability. It means

an increase in funds for financing of the sale

provided a BUS every year potentially will increase

the profitability of the BUS as measured by ROA.

Thus the hypothesis which States that the existence

of a positive influence between financing and selling

with acceptable profitability.

Otoritas Jasa Keuangan (2017) in Shariah Banking

Statistics 2016 States that selling financing provided

by BUS is the largest financing portion in between

other types of financing, that amounted to 63 percent

of the total financing. According to Karim (2011),

when compared with Akkadian istishna customer

greeting, and prefer to apply for financing from the

side of murabaha financing object acceptance,

especially for financing consumer clients.

Selling financing in accordance with the theory

of Exchange or natural certainty contracts (NCC)

where the financing deals and selling give certainty

of payment, both in terms of quantities or time, so

that the flow of funds for sure or already agreed at

the beginning of the object of exchange of contracts

and also certainly in quantity, quality, time, and

price (Rivai and Veithzal, 2008). Flow of funds

financing repayment the definite buy sell and fit the

target can support towards income generation BUS

itself so that it can increase the ROA.

The research is in line with research Haq (2015)

and Abusharbeh (2014) stating that the financing

and selling a significant and positive effect toward

profitability. Similarly, research conducted with

Rahman and Rochmanika (2012) that the financing

of the sale of influential positive towards

profitability. Selling financing potential greater than

other financing was able to give positive influence

against ROA because the level marked up from

selling financing can provide the greatest revenue

for Islamic banks.

Results of testing the hypothesis concerning the

influence of finance for results against profitability

indicates that financing for the negative effect the

results significantly to profitability. This research

was originally alleged that financing for the results

have a positive affect toward profitability, but after

doing a panel data regression test research

hypotheses stated that financing for the results of a

positive effect against the profitability of denied.

The results of this study indicate that if financing for

results increases then it will lower the profitability

on the BUS.

According to Karim (2011), financing for results

is a form of investment contracts that are included in

the theory of mixture or natural uncertainty contracts

(NUC). In the NUC parties Transact mutually

mixing assets into one, and then run the risk of being

together for profit. This investment contracts do not

provide certainty of income (return), both in terms of

quantities or time. Income and the timing of cash

flows obtained depends on the performance of the

sector riilnya.

The level of profits that accrue to the bank

always did not remain high due to the low profits

from financing for results obtained depends on the

success of bank business borrowers. Part of the

profits be shared revenue is directly proportional to

the customer. That means if the rate of profit a great

effort both parties got a big part anyway and if the

level of small business advantage then gained the

advantage small part anyway. The repayment of any

loan principal in accordance with the customer's

ICIEBP 2017 - 1st International Conference on Islamic Economics, Business and Philanthropy

784

business cash flow. Division of business results have

difficulties to apply because the calculation of the

profit sharing is complicated and would have to

follow what's happening in actual business. In

addition the cost of funds obtained on the basis of

the system for results not known clearly and

definitely (Veithzal and Rivai, 2008).

Karim (2011) suggested that in the event of

losses in finance for the results the bank took losses

of profits in advance because the advantage is patron

capital, whereas if the losses exceed the amount of

the advantage then the bank can pick it up from the

principal capital.

Research conducted by Riyadi and Yulianto

(2014) also revealed that the financing for the results

negative effect against the profitability of foreign

exchange on the BUS. This is so because of the high

risk of moral hazard posed by customer financing.

Results of testing the hypothesis concerning the

influence of lease financing toward profitability

indicates that the positive effect of lease financing

significantly to profitability. It means an increase in

funds for financing of the sale provided a BUS every

year potentially will increase the profitability of the

BUS as measured by ROA. Thus the hypothesis

which States that the existence of a positive

influence between financing and selling with

acceptable profitability.

Finance leases are included in the category of

natural certainty contracts (NCC) or Exchange

theory. Technically, any lease financing have in

common with the financing. The difference is in

financing the transaction object is used. On the

financing lease financing is object services then the

bank can also serve clients who only need the

services, i.e. the benefit upon the object of financing

given Sharia bank (Karim, 2011).

Object of financing lease transferable ownership

at the end of the rental period or known as ijarah

muntahiya bi tamlik (IMBT). According to Antonio

(2001), Islamic banking more use IMBT in

financing the lease because of a simple bookkeeping

and maintenance of asset financing that is not too

complicated. To get the maximum income is usually

the bank selling the object of financing to customers

after the ending of contract rent compared to grant

the lease assets. In addition to obtaining rental

income, the bank also gets revenue from the margin

of the selling price of the asset sale transaction

financing leases. Therefore technical contract IMBT

do not differ greatly with technical selling financing,

particularly Akkadian murabaha.

The results of this research are consistent with

research conducted by Ogilo (2016) and Pratama et

al. (2017), Both these studies reveal that financing

leases given a positive effect against Islamic bank

profitability. The potential rental income obtained by

the bank especially in the revenue generated from

the Akkadian IMBT contribute to increased

profitability of Islamic banks.

But there are also studies that show different

results as research done Haq (2015); Haron and Wan

(2004) that the financing for the influential results

negatively to profitability. So did research with

Haron and Wan (2004) that the financing and selling

does not have significant influence towards Islamic

banking profitability.

The results of testing hypotheses about the

influence of these three types of financing against

profitability indicates that financing has an impact

on the profitability of the BUS. It means financing

provided to contribute to the improvement of

profitability on a BUS in Indonesia.

Rivai and Veithzal (2008) and Muhammad

(2005) suggests that profitability (profitability) is

one of the objectives of the financing reached

syariah bank acquires the maximum profit. This goal

is achieved by increasing the ability of the BUS

companies in the management of the Fund's

financing. The profit margin earned from selling

price, the portion for the results, and the rental fee is

the dominant source of income so that they can have

an effect on the development of profitability on a

BUS.

The results of this research are consistent with

research conducted by Izhar and Asutay (2007) that

the revenue obtained from the Islamic bank

financing channelling effect on profitability as

measured by ROA. So did research with Ogilo

(2016) who suggested that the financing of

mudharabah musyarakah, financing, financing of

murabaha, ijarah financing and simultaneous effect

on profitability.

4 CONCLUSIONS

There is a trend of increased financing and selling

will result in increased levels of profitability so that

financing and selling a positive effect towards

profitability. Selling financing gives the certainty of

payment, both in terms of quantities or time, as well

as the use of sales margin was able to contribute to

the improvement of the profitability of the BUS.

There is a trend of increased financing for results

will result in a decrease in the level of profitability

so that financing for the influential results negatively

The Influence of Financing Against Profitability at Bank Syariah in Indonesia in General 2010-2016

785

to profitability. Financing system for results that are

still fairly complicated and risky hasn't been able to

contribute to the improvement of the profitability of

the BUS.

There is a tendency of an increase in lease

financing will result in increased levels of

profitability so that the positive effect of lease

financing toward profitability. The BUS can increase

profitability through financing lease contract IMBT

with techniques, mainly by selling assets leases to

customers.

There is a tendency that the financing of the sale,

the financing for the results, and lease financing can

support the development of profitability so that these

three types of financing on the BUS simultaneously

has an impact on profitability.

REFERENCES

Abusharbeh, M. T., 2014. Credit Risks and Profitability of

Islamic Banks: Evidence from Indonesia. World

Review of Business Research. 4(3), 136-147.

Antonio, M. S., 2001. Bank Syariah: Dari Teori ke

Praktik, Gema Insani. Jakarta.

Arikunto, S., 2006. Prosedur Penelitian: Suatu

Pendekatan Praktik, Rineka Cipta. Jakarta.

Hadi, A. C., 2011. Problematika Pembiayaan Mudharabah.

Al-Iqtishad. 3(2), 193-208.

Haron, S., Wan, A. W. N., 2004. Profitability

Determinants of Islamic Banks: A Cointegration

Approach. Islamic Banking Conference. (hal. 1-18).

Beirut: Union Arab Bank.

Haq, N. A., 2015. Pengaruh Pembiayaan dan Efisiensi

terhadap Profitabilitas Bank Umum Syariah. Perbanas

Review. 1(1), 107-124.

Izhar, H., Asutay, M., 2007. Estimating the Profitability of

Islamic Banking: Evidence from Bank Muamalat

Indonesia. Review of Islamic Economics. 11(2), 17-29.

Karim, A., 2011. Bank Islam: Analisis Fiqh dan

Keuangan, Rajawali Pers. Jakarta.

Marbelanty, F., Adityawarman, 2015. Analisis

Perbandingan Kinerja Keuangan Antara Perbankan

Konvensional dengan Perbankan Syariah di Indonesia.

Diponegoro Journal of Accounting. 4(4), 1-10.

Muhammad, 2002. Manajemen Bank Syariah, UPP AMP

YKPN. Yogyakarta.

Muhammad, 2005. Manajemen Pembiayaan Bank

Syariah, UPP AMP YKPN. Yogyakarta.

Muhammad, 2008. Metodologi Penelitian Ekonomi Islam:

Pendekatan Kuantitatif, Rajagrafindo Persada. Jakarta.

Ogilo, F., 2016. Effects of Financial Instruments on

Performance of Islamic Banks in Kenya. The

International Journal of Bussiness and Management.

4(8), 40-45.

Otoritas Jasa Keuangan, 2017. Statistik Perbankan

Indonesia Desember 2016, Otoritas Jasa Keuangan.

Jakarta.

Pratama, D. N., Martika, L. D., Rahmawati, T., 2017.

Pengaruh Pembiayaan Mudharabah, Pembiayaan

Musyarakah dan Sewa Ijarah terhadap Profitabilitas.

Jurnal Riset Keuangan dan Akuntansi. 3(1), 53-68.

Rahman, A. F., Rochmanika, R., 2012. Pengaruh

Pembiayaan Jual Beli, Pembiayaan Bagi Hasil, dan

Rasio Non Performing Financing terhadap

Profitabilitas Bank Umum Syariah di Indonesia.

Jurnal Iqtishoduna. 8(1), 1-16.

Rivai, V., Veithzal, A. P., 2008. Islamic Financial

Management, Rajagrafiindo Persada. Jakarta.

Riyadi, S., Yulianto, A., 2014. Pengaruh Pembiayaan Bagi

Hasil, Pembiayaan Jual Beli, Financing To Deposit

Ratio (FDR) dan Non Performing Financing (NPF)

terhadap Profitabilitas Bank Umum Syariah di

Indonesia. Accounting Analysis Journal. 3(4), 466-

474.

Rosadi, D., 2012. Ekonometrika and Analisis Runtun

Waktu Terapan, Penerbit Andi. Yogyakarta.

Tanjung, H., Dewi, A., 2013. Metodologi Penelitian

Ekonomi Islam, Gramata Publisihing. Jakarta.

ICIEBP 2017 - 1st International Conference on Islamic Economics, Business and Philanthropy

786