Measuring the Efficient of Islamic Rural Bank in Java Island Based

on Stochastic Frontier Analysis (SFA) Method

Nisful Laila and Fitri Syarahfina Putri

Faculty of Economic and Business, Airlangga University, Surabaya, Indonesia

nisful.laila@feb.unair.ac.id, fsyarahfina@gmail.com

Keyword: Cost Efficiency, Profit Efficiency, Islamic Rural Bank, Stochastic Frontier Analysis.

Abstract: The aim of this research is to measure the efficiency of Islamic rural bank in Java from 2011- 2015. The

method applied is Stochastic Frontier Analysis (SFA) to know the level of cost efficiency and alternative

profit efficiency of Islamic rural bank. The are 12 Islamic rural banks as sample, with 7 variables: total cost,

total profit, cost of labor, cost of fund, cost of capital, total financing, and total of productive assets. The

result shows efficiency of Islamic rural bank indicated that there is no Islamic rural bank with perfect value

(value of efficiency =1) in cost efficiency and alternative profit efficiency. The average of cost efficiency

for 5 years is 0.9449, the highest 0.9705 is by the Amanah Ummah Islamic rural bank. And the lowest value

0.8918 is by Situbondo Islamic Rural Bank. The average of profit efficiency is 0.7536, with the highest

value 0.8775 is by the Islamic rural Bank Sukowati Sragen and the lowest is 0.5413 is owned by the Bina

Amanah Satria Islamic rural bank.

1 INTRODUCTION

Islamic Economics is becoming part of the whole

the objective of BPRS is to serve people who are

unable to access modern banking services. The more

demand of commercial banks to small and rural

towns. So the BPRS competition with commercial

banks will increase. The role of BPRS is important

for the development of real sector business units in

various regions and the function of BPRS as one of

the financial intermediation institutions. BPRS must

be well maintained so as not to lose competition

with commercial banks, especially in the

microfinance segment.

There are several reasons why researchers use

BPRS in Java as a research object. Firstly, in Sharia

Financial Development Report 2015 regionally,

sharia banking is still concentrated in 4 provinces in

Java: Special Capital District of Jakarta, West Java,

East Java and Central Java both from fund raising

and financing distribution. The contribution of the 4

provinces reached 75.94% for fund raising and

71.82% for financing distribution. Secondly,

according to the Head of BPS, Java is still the center

of national economic growth. Compared to other

regions, Java contributes 58.29 percent of the

national gross domestic product (GDP), the high role

of Java to the national economic growth sustained

by three regions. Provinces of Special Capital

District of Jakarta, East Java, and West Java account

for the largest share of GDP. Therefore, BPRS is

considered as one of the right financial institutions

to facilitate it. Based on the background and reasons

written by the researcher, the selection of the

background will answer whether the BPRS in Java

has operated efficiently. There are two approach in

measuring economics performance, namely financial

performance and efficiency performance, as stated

by Abidin (2007). The measurement method to

evaluate financial performance is using Capital (C),

Asset Quality (A), Management (M), Earning (E),

Liability (L) and Sensistivity Market to Risk (S) or

as known as CAMELS method (Erol et al., 2014).

On the other hand efficiency performance is very

important to measure monetary policy including tool

to increase the real sector of economy. The

efficiency in banking industry are measured by

applying some financial ratios such as return on

equity (ROE), return on asset, asset turn over and

return on permanent capital. But if efficiency

measurement are derived from accounting ratios, the

source of inefficiency is difficult to find out

(Sutawijaya and Lestari, 2009). To measure how

much cost-efficiency and profit efficiency BPRS in

Java, the method used by researchers is Stochastic

Frontier Analysis (SFA) which is based on the

702

Laila, N. and Putri, F.

Measuring the Efficient of Islamic Rural Bank in Java Island Based on Stochastic Frontier Analysis (SFA) Method.

In Proceedings of the 1st International Conference on Islamic Economics, Business, and Philanthropy (ICIEBP 2017) - Transforming Islamic Economy and Societies, pages 702-706

ISBN: 978-989-758-315-5

Copyright © 2018 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

consideration that these methods are still rarely used

in the efficiency research of Sharia Society

Financing Bank.

The formulation of the problem in this research

is how is the level of cost efficiency and profit

efficiency in BPRS in Java in 2011-2015 by using

SFA method and what input and output components

affecting cost efficiency and profit efficiency of

BPRS.

The purpose of this research is to figure out,

measure and analyze cost efficiency and profit

efficiency of BPRS in Java and to know what input

and output component affecting efficiency cost and

efficiency of profit at BPRS.

2 LITERATUR REVIEW

2.1 Efficiency Concept in Islamic

Perspective

Efficiency is defined as the ratio between output and

input, or the amount generated from one input that is

used (Iswardono, 2000). This efficiency concept is

very important in Islamic bank as it also comply

with Islamic principle in fulfilling maqashid Syariah

or the goal of Islamic law. (Kamaruddin, 2008).

Efficiency according to Hansen and Marynne (2003)

can be achieved in three ways: (1) with smaller

inputs producing the same output, (2) with the same

input producing larger outputs, or (3) The smaller

ones produce larger outputs.

2.2 Stochastic Frontier Approach

(SFA)

Measuring the efficiency value of financial

institutions will use a frontier in the SFA approach.

The explanation of this frontier can be in the form of

cost function, profit or production relation of a

number of input, output and environmental factors

and take into account the existence of random error.

A bank is said to be inefficient if the cost of a bank

is higher than the cost of the frontier bank operating

at its best performance level (best practice). Aigner

et al. (1977) suggested the stochastic frontier

function which is an extension of the deterministic

original model to measure unexpected effects

(stochastic frontier) within the production limits.

Coelli and Rao (2003), stated several reason why

applying SFA is suggested: (i) involved disturbance

term, mismeasurement and exogent shock that out of

control, (ii) environtal variabels are easily to be

applied (iii) able to conduct hiphotesis test using

statistic tools, (iv) easier to identify “outliers”, (v)

cost frontier and distance function can be used to

measure business efficiency with many output.

2.3 The Comparison of SFA and Other

Efficiency Approach

The efficiency measurement method can be

classified into two, they are parametric and non-

parametric approach. The parametric approach is a

statistical approach that takes into consideration the

type of distribution or distribution of data by

viewing the data whether it spreads normally or not.

Generally if the data is not normally spreads, the

data must be done by non-parametric statistics

method, or conducted a transformation in advance so

that the data follow the normal distribution.

Efficiency with non parametric approach can apply

data envelopment analysis (DEA) method and

disposal hull (FDH) that has general assumtion

where random error did not exist (Berger and

Humphrey, 1997). SFA is one of the parametric

methods that can be used.

2.4 Specification of Input and Output

To measure the efficiency with the SFA approach, it

can be done through an output-oriented approach for

technical efficiency measurement, and an input-

oriented approach for cost efficiency measurement.

To measure efficiency with SFA, can be used

output-oriented approach to measure technical

efficiency, and input-oriented approach to measure

cost efficiency. Technical efficiency measure based

on production frontier, while cost efficiency

measured based on cost frontier (Khumbakar and

Lovell, 2000). To determine input-output process in

banking industry is important since there are no

devine concencuss to identify the input and output

variabel to measure bank efficiency. Berger and

Mester (1997) stated that identification input and

output relation in financial activities of the financial

institution can be done by several approach namely:

1)asset approach, 2) Production approach, and 3)

intermediation approach. In this research is the price

of labor (personal expense/ total asset), the price of

funds (share of profit/ total third party funds, and

capital price (administration and general costs and

other costs/ fixed assets). While the output in this

research is total financing and other earning assets.

The total financing consists of Debts (Murabahah,

Salam, Istishna, Ijarah and Multijasa), and Shared

Measuring the Efficient of Islamic Rural Bank in Java Island Based on Stochastic Frontier Analysis (SFA) Method

703

Financing (Musyarakah and Mudharabah). The

other earning assets consist of Bank Indonesia

Wadiah Certificates, Placements with Other Banks,

and Owned Securities.

3 METHODOLOGY

Finally, complete content and organizational editing

before formatting. Please take note of the following

items when proofreading spelling and grammar:

3.1 Research Approach

This approach uses quantitative approach, this

efficiency calculation method requires estimation of

cost function and profit function econometrically,

then residual value from estimation of cost function

and profit function is used to calculate efficiency

value by using method of Stochastic Frontier

Analysis (SFA). Variable in this research are: Total

Cost, Total Profit, Price of Labor, Fund Price,

Capital Price, Total Financing, Other Earning Assets

according to Srairi (2009). In this research, the used

data is secondary data. The used data is in the form

of quarterly financial statements that have been

published from the official website of Bank

Indonesia that is www.bi.go.id, the website of the

Financial Services Authority is www.ojk.go.id. The

data processing is done by using Eviews 6 software.

3.2 Population and Sample

In this research, the used sampling collection is

purposive sampling. Population in this research is

BPRS in Java registered in Bank Indonesia in the

period of 2011-2015. The used sample is collected

based on the provisions that have been determined

by the researcher. Below is the list of the qualified

BPRS:

4 RESULTS AND DISCUSSIONS

4.1 Description of Research Results

The calculation of profit efficiency and cost

efficiency of sharia financing bank of Java use

intermediation approach. The objects in this research

were 12 BPRS of Java registered in the Financial

Services Authority within the 2011-2015 timeframe,

so that the descriptive statistics BPRS of the sample

are presented in table 1 below:

Table 1: Descriptive Statistic of Cost Function and BPRS

Profit Variables.

Variabel

Mean

Std. Dev

Maximum

Minimum

TC

8815363.967

11189951.66

60307133

229389

Π

980319495.8

1204383528

5756385000

11824000

Y1

0.033335478

0.020769327

0.10699502

0.005428859

Y2

0.067233579

0.058839467

0.602588765

0.00836036

Y3

0.672810944

0.462732018

2.397661013

0.047829489

P1

84943033.05

97013178.35

412456182

4700186.00

P2

13891464692

16276018738

1.03297

498455000

4.2 Cost Efficiency Level of Stochastic

Frontier Approach (SFA) Method

Table 2: Formation Result in Translog Cost Function.

Variabel

Coefficient

Std. Error

t-Statistic

Prob./Sig

C

6.210932

0.440270

14.10710

0.0000

Y1?

0.599935

0.025649

23.39040

0.0000

Y2?

0.290242

0.019371

14.98322

0.0000

Y3?

0.078727

0.021147

3.722942

0.0002

P1?

0.821483

0.021885

37.53694

0.0000

P2?

0.197383

0.014748

13.38355

0.0000

The constant of TC is 6.210932. This means that

if the input and output variables are considered

constant. For input and output variables in the cost

function are as follows:

4.2.1 Price of Labor

Based on the table above, it is known that input of

price of labor shows positive value of regression

coefficient 0,599935 shows that if exponent of price

of labor have increase equal to unit, hence total cost

will increase by 0,59935.

4.2.2 Fund Price

Shows positive value of regression coefficient

0,290242 it means that if the exponent of fund price

have increase equal to unit, hence total fund will

increase by 0,290242.

4.2.3 Capital Price

The last input in the form of capital price also shows

the positive value of regression coefficient

0.672810944 indicate that if exponent of capital

price have increase equal to unit, hence total cost

will have increase by 0,672810944.

4.2.4 Total Financing

Based on the table 2, it is known that the total

financing variable has a regression coefficient of

0.821483 indicating that if total exponent of total

ICIEBP 2017 - 1st International Conference on Islamic Economics, Business and Philanthropy

704

financing have increase equal to unit, hence total

cost will increase by 0.821483.

4.2.5 Other Earning Assets

Another earning asset value is a positive regression

coefficient of 0.197383 indicating that if the

exponents of other earning assets have increase

equal to unit, hence total cost will increase by 0.197.

4.2.6 Analysis of Stochastic Frontier

Analysis

The model of analysis used in this research is panel

data model, it is intended to consider the observation

period of a bank and will result in the value of

efficiency level both Cost Efficiency and Alternative

Profit Efficiency based on the research in the period

for 5 years. The panel data model used to estimate

the efficiency function uses the fixed effect model.

The following is cost efficiency results with SFA

method on 12 BPRS:

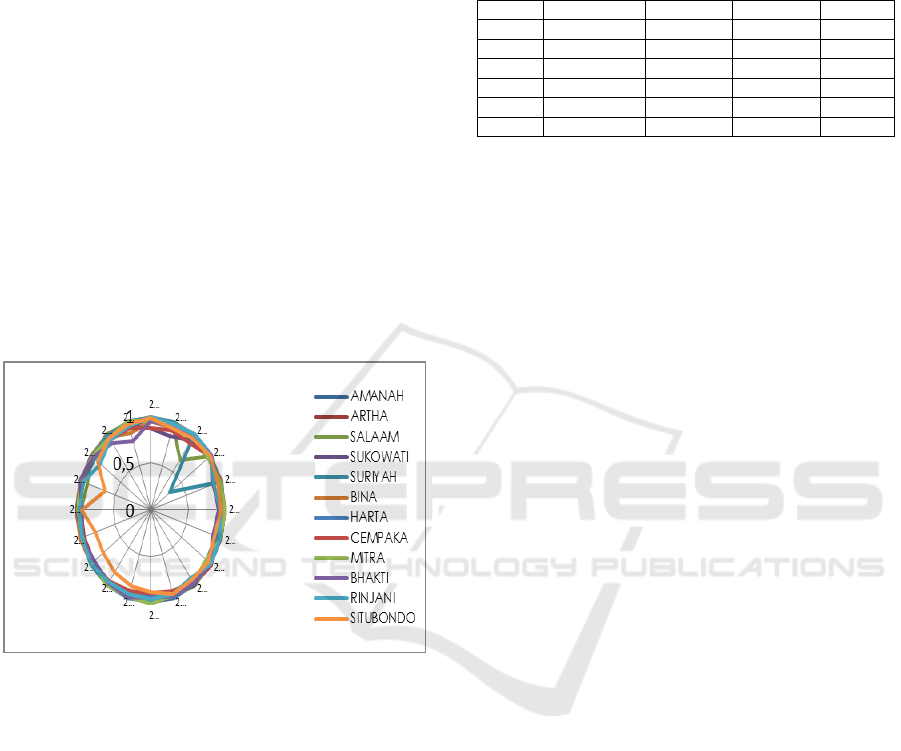

Figure 1: Cost Efficiency on 12 BPRS.

The figure 1 shows BPRS Suriyah is the most

inefficient bank in cost, although the value of its

Cost Efficiency tends to be stable it can be seen

from the movement of BPRS Suriyah chart above.

BPRS Sukowati Sragen is one of the banks that has

a positive Cost Efficiency trend, which initially has a

Cost Efficiency of 0.8665 in the first quarter of

2011, in the fourth quarter of 2015 to 0.9573.

Overall almost all BPRS have a positive trend that

has an increase in the value of Cost Efficiency.

Unlike the BPRS Suriyah although it experienced a

decline in the value of efficiency, BPRS Suriyah

actually increased in the fourth quarter of 2015 with

a score of 0.9891 or greater than the value in the first

quarter of 2011 which amounted to 0.9790.

4.3 Profit Alternative Efficiency Level

of Stochastic Frontier Approach

(SFA) Method

Table 3: Results Formation in Translog Functions profit .

Variable

Coefficient

Std. Error

t-Statistic

Prob.

C

6.988475

1.696603

4.119098

0.0001

Y1?

-0.317617

0.098839

-3.213478

0.0015

Y2?

0.200792

0.074648

2.689853

0.0077

Y3?

0.180391

0.081489

2.213679

0.0279

P1?

0.753170

0.084334

8.930832

0.0000

P2?

0.036729

0.056833

0.646257

0.5188

In the regression equation above, the TP constant

is 6.988475. This means that if the input and output

variables are considered constant. In the frontier

function as described in the table 3, the estimation

results for the input and output variables in the profit

function are as follows:

4.3.1 Price of Labor

Based on the above table on labor price input has a

regression coefficient of -0.317617 and shows a

negative value, this means that if the price of labor

exponents increased by units, then the total profit

will decrease by 0.317617.

4.3.2 The Price of Funds

The price of funds shows a positive value, and has a

regression coefficient of 0.200792 indicates that if

the exponent price of funds increased by units, then

the total profit will increase by 0.200792.

4.3.3 Capital Price

The last input in the form of capital price shows a

positive value, regression coefficient of 0.180391

indicates that if exponent price of capital increased

by unit, then the total cost will increase by 0.180391.

4.3.4 Total Financing

The total financing variable has a regression

coefficient of 0.753170, indicating that if total

exponent of financing has increased unit, then total

profit will increase by 0.180391.

4.3.5 Other Earning Assets

Another earning asset value is positive, has a

regression coefficient of 0.036729 indicates that if

the exponent of other productive assets increased by

Measuring the Efficient of Islamic Rural Bank in Java Island Based on Stochastic Frontier Analysis (SFA) Method

705

unit, then the total profit will increase by 0.036729.

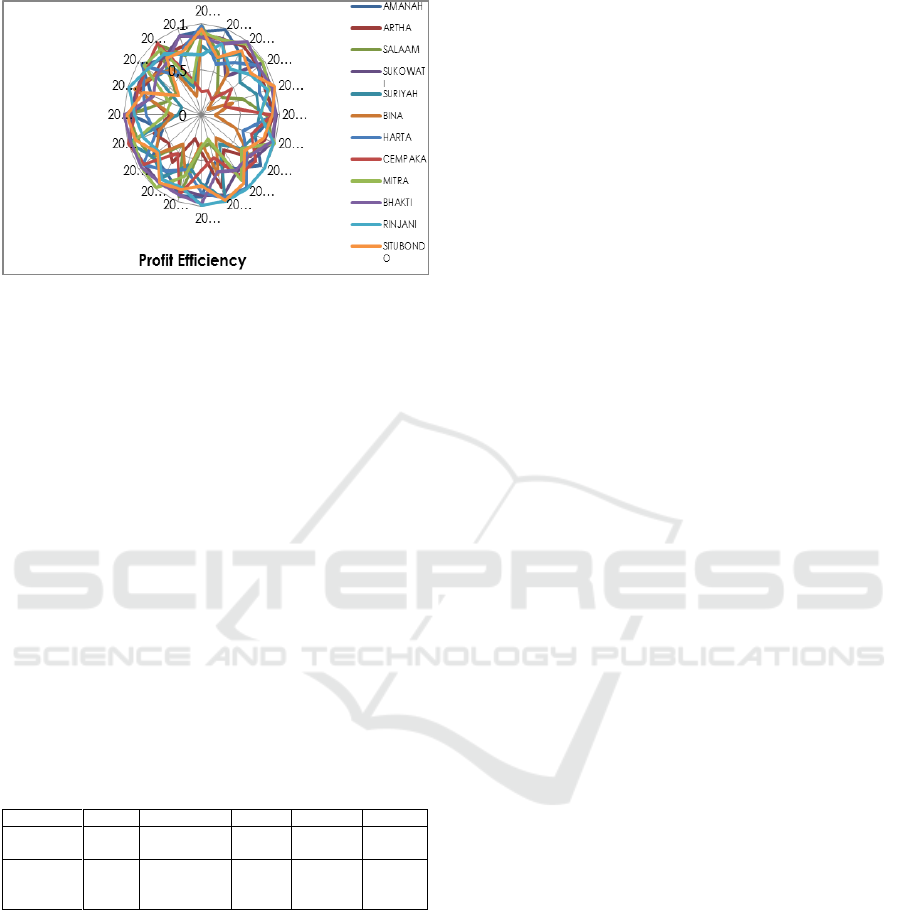

Profit Efficiency can see in figure 2

Figure 2: Profit Efficiency.

5 CONCLUSIONS

It can be concluded that the average cost efficiency

of BPRS in Java in the period of 2011-2015 is equal

to 0.9449 or 94.49% and experiencing cost

inefficiency as 5.51%. BPRS Situbondo is the most

inefficient bank in cost that is with average cost

efficiency score of 0,8918 or 89.18% and

experienced cost inefficiency of 10.82%. While

BPRS Amanah Ummah became the most efficient

bank during the research period, which is getting the

average cost efficiency score of 0.9705 or 97.05%

and cost inefficiency of 2.95%. The efficiency cost

in BPRS in Java has a downward or fluctuate trend

value. Summary of estimation results of cost and

profit efficiency can see in table 4.

Table 4: Summary of Estimation Results of Cost and

Profit Efficiency.

Average

Best

Value

Worst

Value

Cost

efficiency

0.9449

BPRS Amanah

Ummah

0.9705

BPRS

Situbondo

0.8918

Alternative

profit

efficiency

0.7536

BPRS Sukowati

Sragen

0.8775

BPRS Bina

Amanah

Satria

0.5413

The average of profit efficiency score of BPRS

in Java during the research period in 2011-2015 is

0.7536 or 75.36%. BPRS Sukowati Sragen become

the most efficient bank in generating profit that is

with profit efficiency score equal to 0.8775 or

87.75%, after that followed in second and third

position by BPRS Bhakti Sumekar, BPRS Bumi

Rinjani Kepanjen, that is with efficiency score equal

to 0.8686 or 86.86 %, and 0.8449 or 84.49%. BPRS

Bina Amanah satria became the most inefficient

bank in generating profit, that is with a score of

0.5413 or 54.13% .. The profit efficiency of BPRS in

Java has a downward trend. Based on the research

period of 2011-2015, the average value of profit

efficiency tends to decrease and the peak occurs in

2011 first quarter with an average efficiency score of

0.8225 or 82.25%. During the research period the

average profit efficiency has decreased by 0.6460 or

64.60%. The regression result shows that the Total

Financing variable has the largest regression

coefficient value and has significant effect on the

translog cost function and the translog profit

function. This indicates that the amount of financing

distributed by the BPRS in the research sample.

REFERENCES

Abidin, Z., 2007. Analisis Eksistensial, PT. Raja Grafindo

Persada. Jakarta.

Aigner, D., Lovell, C. A. K., Schmidt, P., 1997.

Formulation and Estimattion of Stochastic Frontier

Production Function Models. Journal of

Econometrics. 6, 21-37

Berger, A. N., Mester, L. J., 1997. Inside The Black Box;

What Explains Differences In The Efficiencies of

Financial Institutions?. Journal of Banking &

Finance. 21, 895-947.

Coelli, T. J., Rao, D. S. P., 2003. Total Factor Productivity

Growth in Agriculture: A Mainquist Index Analysis

of 93 Countries, 1980-2000. CEPA Working Papers,

2/2003 School of Economics University of

Queensland. St. Lucia, Qld. Australia, 1-31.

Erol, C., 2014. Performance comparison of Islamic

(participation) banks and commercial banks in

Turkish banking sector. EuroMed Journal of

Business. Vol. 9: 114 – 128.

Hansen, D. R., Marynne, M. M., 2003. Management

Accounting, Thomson South Western. United Stated

of America,

6th

edition.

Iswardono, 2000. Uang dan Bank, BPPE. Yogyakarta,

5th

edition.

Kamaruddin, B. S., 2008. Assesing Production

Efficiency of Islamic Banks and Conventional Bank

Islamic Windows in Malaysia. International Journal

of Business and Management Science. Vol 1(1),

pp.33

Srairi, S. A., 2009. Cost and Profit Efficiency of

Conventional and Islamic Banking in GCC

Countries.

Sutawijaya, A., Lestari, E. P., 2009. Efisiensi Teknik

Perbankan Indonesia Pasca Krisis Ekonomi; Sebuah

Studi Empiris Penerapan Model DEA. Jurnal

EKonomi Pembangunan. Volume 10 (1).

ICIEBP 2017 - 1st International Conference on Islamic Economics, Business and Philanthropy

706