Love of Money and Auditor Ethical Assessment

Fraud Perception Analysis

Evita Puspitasari and Mustika Riskafuri

Universitas Padjadjaran

evita.puspitasari@unpad.ac.id, evitapuspitagumilar@gmail.com

Keywords: Gender, Total Income, Ethical Perception, Love of Money.

Abstract: The aim of this study is to investigate the relation between the auditor ethical perception and the love of

money that can drive the fraud, along with the age, gender, and income as other factors. The research

method of this study is Path Analysis with decomposition model. The result found that there was a

correlation for gender and love of money. Male tended to have the higher-level love of money. The result

implied that male tended to put money as an important thing. We assumed this happened since in eastern

culture it was the male that had responsibility in fulfilling the needs of his family. Further, this study proved

that the respondent income did not affect the love of money. The finding indicated that the amount of salary

respondents had did not correlate to the level of the love of money. The wealth of people was more

determined by his/her mindset, not by the income they got. In this study, we also found that gender and

income did not influence the auditor ethical perception about fraud. Both male and female auditor had

indifferent fraud ethical perception; and income of the respondents did not affect the fraud ethical

perception of auditor. Finally, this study found that the respondents’ level of love of money did not correlate

with the fraud ethical perception of auditor.

1 INTRODUCTION

Recently, the accountant profession is facing many

issues which are related to fraud. Enron (2001),

WorldCom (2002) Tyco (2002) are accounting

scandals happened. The Sarbanes-Oxley (SOX) Act,

held by U.S. Congress in July 2002, is a crucial step

that will lead to the rules and code of ethic

improvement. But fraud actions still happened.

American Insurance Group (2005), PT Kereta Api

Indonesia (2006), Tesco (2014) and Toshiba (2015)

scandals are the example of the most current issue.

Therefore, it cannot be denied that the reliability of

accountant profession has been declined.

Ethical perception of accountant has become one

of most interesting research materials in order to

examine what factors that will reduce fraud. This

research is conducted to examine the ethical

perception of accounting students in Indonesia.

Individual behavior is derived from external and

internal factors. External factors are factors which

come from outside of the individual (cultures,

economic and social factors) and internal factors

come from the individual itself (knowledge,

perception, etc.)

Perception is the way someone look at something

and believe that it is the right things to do. Based on

expectancy theory, perception can be the basis of

someone’s motivation to perform some actions.

Money is believed to become an important

motivator. In the business, managers frequently use

money to control and motivate employees

(Milkovich and Newman, 2002). McClelland said,

money is an important aspect of everyday life.

Although the money is used universally, the

meaning and importance of money is not universally

accepted (Tang, 1992).

Love of money can be explained literally as the

individual perception about money; how they

respect money. Based on Tang and Chiu (2003) and

Elias and Magdy (2010), love of money has direct

impact related to personal unethical behavior.

Money ethics scale (MES) developed by Tang

(1992) to measure the individual’s love of money.

This research is closely related with Elias and

Magdy (2010) study, where the results found that the

love of money is significantly related to perceptions

of cheating. Money worshippers view cheating

actions as more ethical followed by money‐admirers

and money‐repellents who view such actions as

Puspitasari, E. and Riskafuri, M.

Love of Money and Auditor Ethical Assessment - Fraud Perception Analysis.

In Proceedings of the 1st International Conference on Islamic Economics, Business, and Philanthropy (ICIEBP 2017) - Transforming Islamic Economy and Societies, pages 331-334

ISBN: 978-989-758-315-5

Copyright © 2018 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

331

more unethical. The purpose of this study is to

investigate the relation between the auditor ethical

perception and the love of money that can drive the

fraud, along with the age, gender, and income as

other factors.

2 METHODS

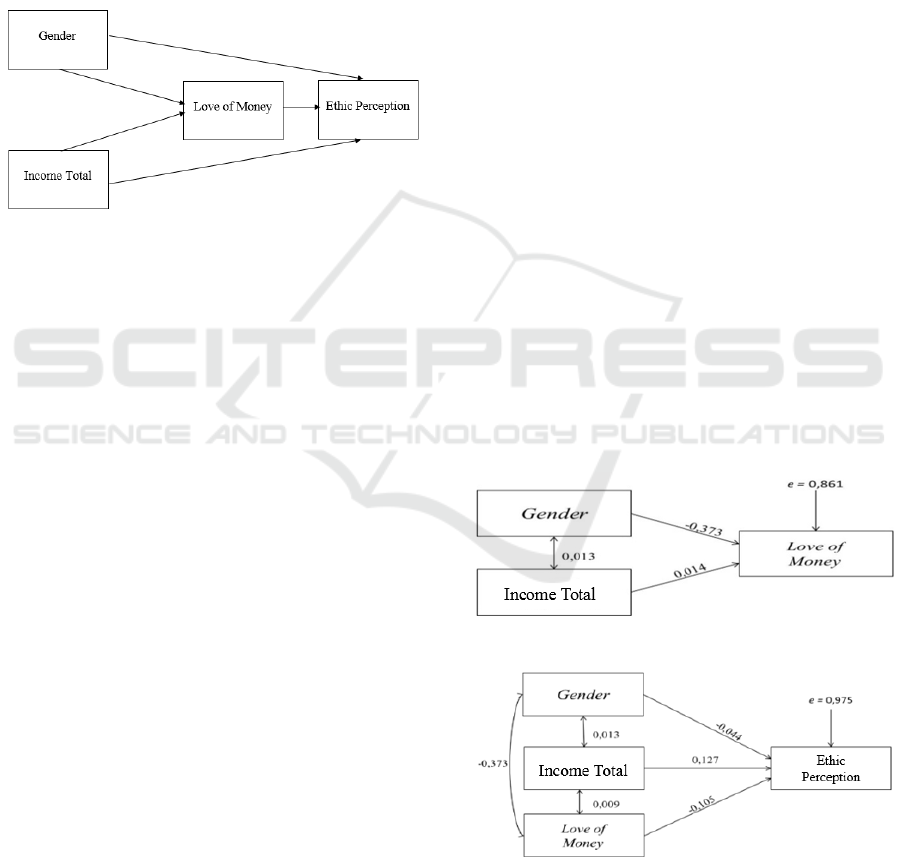

2.1 Research Model

Figure 1: Path analysis model.

2.2 Analysis of Variables

2.2.1 Ethical Perception

The endogenous variable in this study is ethical

perception of accounting students. The ethical

perception in this study is determined from

individual's view to accounting fraud that is occurred

(Elias and Magdy, 2010). In order to measure ethical

perception, this study uses the scenarios applied by

Elias and Magdy (2010), consist of four scenarios of

fraudulent act.

Scenario 1 deals with early recognition of

revenues (an example of earnings

management).

Scenario 2 deals with classifying long-term

marketable securities as current, to improve the

current ratio.

Scenario 3 deals with including some of the

consigned inventory as assets.

Scenario 4 deals with not reporting contingent

liabilities (a violation of the conservatism

principle).

2.2.2 Gender

There is no specific measurement to measure the

gender factor. In this study, gender will be

determined as dummy variables to separate male and

female; male is 0 and female is 1.

2.2.3 Love of Money

Love of money measures the value of individual’s

desire to money, although not for their mutual needs

(Tang et al., 2004). In this research, love of money

will be measured by using Money Ethics Scale

(MES) which is developed by Tang (1992). MES is

regarded as the best developed survey to measure

individual's attitude towards money; contains 30

items of question which resulted in 6 indicators

(good, evil, achievement, respect, budget, and

freedom) with regard to the love of money.

2.2.4 Population and Samples

Population in this research is the employees of

Internal Government Auditor (BPKP/Badan

Pengawasan Keuangan dan Pembangunan Negara).

Among 1.127 employees, we use 100 staffs as our

respondent randomly.

3 RESULTS AND DISCUSSION

3.1 Hypotheses Testing – Path Analysis

After the normality test is done and the data have

normal distribution, our next step is to determine the

path coefficient and the path diagram of each

construct or sub-structure. For this step, I use SPSS

20.0 to measure the path coefficient and LISREL to

create the path diagram.

Figure 2: Sub structure 1.

Figure 3: Sub structure 2.

ICIEBP 2017 - 1st International Conference on Islamic Economics, Business and Philanthropy

332

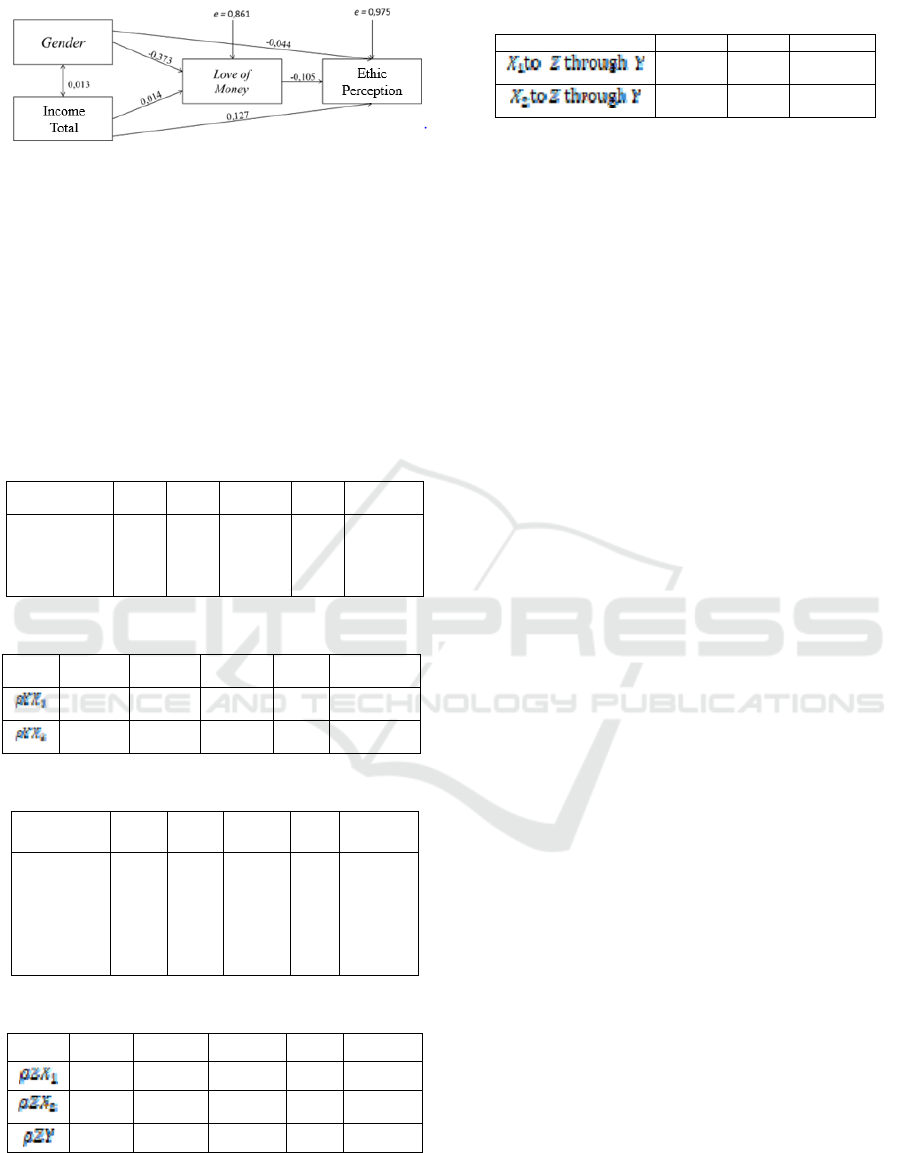

Figure 4: Path model.

3.2 Testing Hypothesis

For testing the hypothesis, we can use F-test for

simultaneous test and two-sided t-test for partial test;

the result will be compared with the value of F-table

and t-table for α = 10% to find out any exogenous

variables that affect the endogenous variable (love of

money). However, we can also use look at sig. value

in ANOVA table and coefficient table from SPSS

output.

Table 1: Simultaneous hypothesis testing – model I.

Hypothesis F-

stat

F-table

Decision Sig. Conclusion

Gender and

Income

simultaneously

influence love

of mone

y

7,856 3,090

H

0

rejected

0,001 Sig

Table 2: Partial hypothesis testing – model I.

Path

Coeff

t-stat t-table Decision Sig. Conclusion

-3,963 ± 1,985 H

0

re

j

ecte

d

0,000 Significant

0,148 1,661 H

0

accepte

d

0,883 Not

Si

g

nificant

Table 3: Simultaneous hypothesis testing – model II.

Hypothesis F-stat F-

table

Dec Sig. Conclusion

Gender and

Income and

love of money

on

simultaneously

influence

Ethical

Perception

0,828 2,699

H

0

accepted

0,482 Not Sig

Table 4: Partial hypothesis testing – model I.

Path

Coeff

t-stat t-table Decision Sig. Conclusion

-0,406 ± 1,985

H

0

accepted

0,685 Not

Significant

1,257 -1,661 H

0

accepted 0,212 Not

Significant

-0,968 -1,661 H

0

accepted 0,335 Not

Significant

Table 5: Hypothesis testing – influence through mediation.

H

yp

othesis t-stat t-table Decision

0,2187 ±

1,985

H

0

acce

p

te

d

-0,588 -1,661 H

0

acce

p

te

d

3.3 Gender to Love of Money

From this study, the path coefficient confirms that

male respondents have higher love of money than

female respondents. This result is in accordance with

the psychological studies of Furnham (1984). There

are differences between males and females

according to their perception towards money. The

different perception comes from the culture, where

males are the one who is responsible to earn money

for the family and females are the one who manages

the money. The role differences develop different

perspective towards money. Females tend to be

more traditionalist, retentive, and precautions toward

money than males. Meanwhile, the males are

presumed must earn more money for them and for

their family, then increase the males’ love of money.

This result is consistent with Ratna and Birton, and

Tang (Elias and Magdy, 2010).

3.4 Income to Love of Money

According to our investigation, we find that the

income influences the love of money positively yet

insignificantly. This finding does not support the

proposed hypothesis, that the income influences the

love of money positively and significantly. This

result is in accordance with the study of Tang et al.

(2005). We assume this result shows that learning

process of person in appreciating the money, from

the childhood to the maturity (Tang et.al, 2005).

When time passes by, even the person with the

lower income will be grateful at the certain time.

Further, we believe that this finding caused by the

remuneration system in the BPKP. The employees

get fixed income and also variable income when

they are doing additional assignment. Therefore, the

money is not a problem for them.

3.5 Gender to Ethical Perception

This research finds that both male and female have

the same level of ethical perception. It means, the

proposed hypothesis is rejected. This finding is in

line with the study of Smith and Oakley (1997). We

believe that the prove we find show that both male

and female have earned value education, therefore

Love of Money and Auditor Ethical Assessment - Fraud Perception Analysis

333

they give good response when they are faced with

the fraud ethical question.

3.6 Income to Ethical Perception

We find that the income gives positive influence

towards ethical perception, yet insignificantly. This

result rejects the proposed hypothesis. We presume

this evidence is caused because the remuneration

system for the respondent. As auditors, beside get

the fixed income, they also get variable income for

additional assignments they have. Therefore, the

financial needs of them have been already fulfilled

and the income does not influence the ethical

perception.

3.7 Love of Money to Ethical

Perception

We find that the level of money negatively

influences the ethical perception insignificantly. It

means the higher people’s level of love of money, it

does not make that they will behave unethically.

This finding is not in line with other study. Tang and

Chiu (2003) explain that love of money was strongly

related to the concept of “greed”. They also found

the direct path between the love of money and

unethical behavior among employees in Hong Kong.

Tang and Liu (2012) also found that it is not the

income (money), but the motive (love of money)

which cause people to behave unethically. Love of

money may cause the dissatisfaction with income

which leads to unethical behavior of employees; the

more people love money the higher probability of

people will be dissatisfied with their income. The

higher level of love of money tend to make people to

behave more unethically. However, we find

dissimilar result.

We consider this proof indicates that the auditors

in BPKP have a good professional commitment.

Elias (2006) shows when a person has high

professional commitment, it will increase their

ethical perception. This finding is supported by the

fact that the BPKP keep renewing the integrity

agreement with the auditors and other employees.

This contract works as a guarantee that all of the

employees will work with high professional

commitment in accordance to the work ethical

standard.

4 CONCLUSIONS

From this study, gender and love of money that

affect the ethical perception. In term of ethical

perception, both female and male auditor tend to

have same ethical level Considering the fact that this

is a very new topic and the research is still rare,

hence future research is indispensable. The

variables, methods, or population of the study can be

expanded. Also, the population can be taken from

practical and other professional accountants (such as

public accountants, governmental accountants in

BPK, etc.).

REFERENCES

Elias, R. Z., 2006. The impact of Professional

Commitment and Anticipatory Socialization on

Accounting Students’ Ethical Orientation, Journal of

Business Ethics.

Elias, R. Z., Magdy F., 2010. The relationship between

accounting students' love of money and Reviews their

ethical perception, Managerial Auditing Journal,

Emerald Group Publishing, 25 (3), 269-281.

Furnham, A., 1984. Many sides of the coin: the

psychology of money usage. Personality and

Individual Differences, 5(5), 501–509.

Milkovich, G., Newman, N., 2002. Compensation, Mc

Graw-Hill Irwin. America, 7th edition.

Smith, P. L., Oakley, E. F., 1997, Gender-Related

Differences in Ethical and Social Values of Business

Students: Implications for Maanagement, Journal of

Business Ethics 16(1), 37–45.

Tang, T. L. P., 1992. The Meaning of Money Revisited,

Journal of Organizational Behavior, Vol. 13, pp. 197-

202.

Tang, T. L. P., Chiu, R. K., 2003. Income, money ethic,

pay satisfaction, commitment, and unethical behavior:

Is the love of money the root of evil for Hong Kong

employees? Journal of Business Ethics, 46 (1), 13-30.

Tang, T. L. P., Luna-Arocas, R., Sutarso, T., Tang, D. S.

H., 2004. Does the love of money moderate and

mediate the income-pay satisfaction relationship?

Journal of Managerial Psychology, 2, 111–135.

Tang, T. L. P., Luna-Arocas, R., Sutarso, T., 2005. From

income to pay satisfaction: The love of money and pay

equity comparison as mediators and culture (the US

and Spain) and gender as moderators. Management

Research: The Journal of the Iberoamerican Academy

of Management, 3(1), 7–26.

Tang, T. L. P., Liu, H., 2012. Love of money and

unethical behavior intention: does an Authentic

Supervisor’s Personal Integrity and Character

(ASPIRE) make a difference? Journal Business Ethics,

107, 295–312.

ICIEBP 2017 - 1st International Conference on Islamic Economics, Business and Philanthropy

334