The Changing Nature of Campus Health Insurance: Testing

Portability Issues of National Health Insurance

Nuzulul Kusuma Putri and Ernawaty Ernawaty

Faculty of Public Health Universitas Airlangga, Mulyorejo, Surabaya, Indonesia

nuzululkusuma@fkm.unair.ac.id

Keywords: Migrant students, Campus, Health insurance, National health insurance.

Abstract: Before National Health Insurance was implemented, the majority of leading universities in Indonesia

already covered their students with a health insurance scheme. They managed their own campus health

insurance independently. Both National Health Insurance in 2014 and single tuition policy in 2015 brought

huge change to campus health insurance. This study aims to analyse students' needs in health insurance after

implementation of these policies. This is an exploratory study with cross-sectional design. The sample was

taken by voluntary sample through online questionnaire. There were 83 students across different academic

degree participated in this study. Most of the students (65.1%) came from various districts outside the

campus district and chose to reside in boarder houses around the campus. There were only 52.9% of the

students already listed as National Health Insurance participants. Out-of-pocket risk belongs to 35.5%

students who were not covered by health insurance at all. Almost all of the students who already

participated in National Health Insurance (93.3%) were registered in the primary healthcare in their

hometown. The students are already paying for single tuition which does not accommodate health

insurance. A real changing need of migrant students for health insurance coverage exists in the National

Health Insurance era.

1 INTRODUCTION

Universal Health Coverage swept many countries

in the last decade, including Indonesia. Even though

Indonesia is the biggest archipelago country with a

widely dispersed territory, National Health

Insurance is chosen as the health insurance

mechanism rather than region-based insurance. This

decision has consequences in the portability

challenges of the preferred health insurance scheme.

Previous region-based health insurance mechanisms

already implemented by local government should be

merged into a national scheme. It should enable not

only raising the pooling level in local government,

but also maintaining the cross-regional participation

transfer (Pan et al., 2016).

Previously, the majority of universities in

Indonesia had institutionally managed health

services for their students before the enactment of

the National Health Insurance. The provision of this

health service is funded through a student health

insurance scheme that is managed independently by

the university and which is limited only for students

in the university. Student health insurance is

regulated through the policy of each rector.

Generally, this fund pooling is collected through a

semi-annual contribution in addition to the tuition

fee. These funds are managed to finance the health

of students during their education. However, in

accordance with the mandate of the Ministry of

Education, universities are not permitted to collect

additional fees outside the national rate. However,

the calculation of this national rate does not

accommodate student healthcare insurance. The

National Health Insurance that was launched one

year previously also makes this situation more

complicated. The availability of parental health

insurance can have significant effects on the

probability that a young individual enrols as a full-

time student in university (Jung et al., 2013).

Unfortunately, there is no individual student

membership in National Health Insurance. To be

able to be covered by National Health Insurance,

students should be registered with all of their family

members.

The huge variations of health insurance

mechanisms bring many obstacles to the citizens

who wish to temporarily move to another region for

some years. In Indonesia, young adults from rural

regions who have just graduated from senior high

14

Putri, N. and Ernawaty, .

The Changing Nature of Campus Health Insurance: Testing Portability Issues of National Health Insurance.

In Proceedings of the 4th Annual Meeting of the Indonesian Health Economics Association (INAHEA 2017), pages 14-19

ISBN: 978-989-758-335-3

Copyright © 2018 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

school compete to be able to enrol in the best

universities, which are mostly located in urban

regions. According to Callahan (2007), young adults

are twice as likely to be uninsured as children or

older adults. This specific group is a form of a

mobile population with a disproportionate number of

unemployed or irregularly employed members who

must weigh the financial and time costs of their

study and living costs.

Moreover, Pan et al. (2016) explained that a

migrant population which is already covered by

health insurance is commonly restricted from

claiming benefits in the destination region. On the

other hand, these migrants consistently underuse

services in both their communities of origin and

their destination cities. The probability for students

to voluntary register into health insurance is also

possibly small. Undergraduate students appear to

have formed perceptions on health insurance which

is similar to adult including their family (Price PhD,

MPH et al. 2010). The unclear identity of

civilization is worsen their willingness to participate

in a national health insurance program. Study by

Ybarra et al. (2017) addressed a gap in the literature

on access and use of health insurance and routine

medical and dental care among children by including

the legal statuses of both parents and children, there

are limitations.

Based on those background, this study examines

how the portability issue of National Health

Insurance in Indonesia has impacted the students’

need of health insurance after implementation of the

policies.

2 METHOD

This is an exploratory study analysing the

implications of National Health Insurance policies

affecting a university providing a healthcare service

for its students during college. The data were

collected by cross-sectional survey in the second

year of implementation of National Health

Insurance. The sample was taken by voluntary

sample through online questionnaire. The

questionnaires were broadcast to various student

groups on the official social media of the university.

At the end of a week of data collection period, there

were 83 students across different academic degrees

and universities who participated in this study.

The survey captures the student characteristics

related to National Health Insurance membership

requirement and student utilisation of healthcare

service during college. The need of college students

for health insurance after implementation of

National Health Insurance was analysed by

comparing the gap between both sections.

3 RESULT & DISCUSSION

The majority of respondents (65.1%) are migrant

students whose home is not in the same city as the

campus location. Most of the students choose to live

near the campus by moving to the city in which

campus is located. Many of the students who

participated in this study are of undergraduate level.

This means that most of the students are of young

adult age. This age group is dominantly dependent

on their parents for all their living costs. Based on

the membership conditions in the National Health

Insurance policy, this age group is still able to be

covered by parental health insurance by showing

that they are still not financially independent. The

possibility of parental health insurance is high due to

fact that more than half of the parent population are

wage earners. The National Health Insurance policy

officially regulates that the wage earners must be

registered by their employers in National Health

Insurance. The majority of migrant students

(52.9%), who are basically at some distance from

their parents’ authorisation during college, are

already protected through the National Health

Insurance mechanism. Unfortunately, the rest of the

migrant students are barely covered by any health

insurance during college. Moreover, there are still

30.1% of students who are not covered by health

insurance at all.

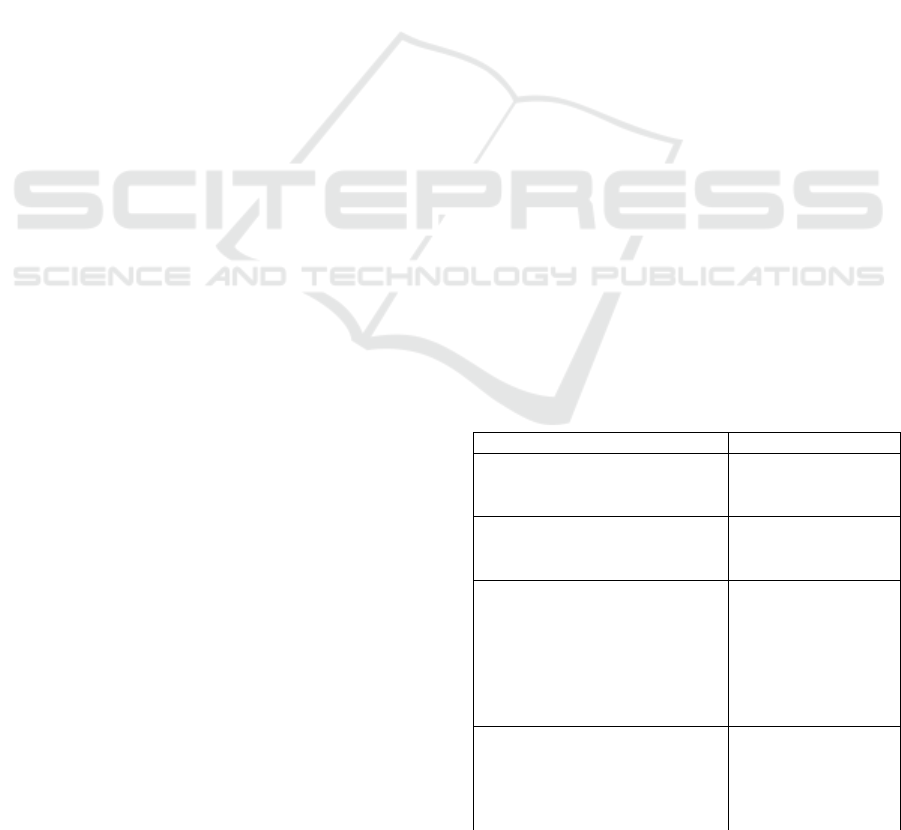

Table 1: Student characteristics

n

%

Student origin

Not migrant student

29

34.9

Migrant student

54

65.1

Home base while study

Move to campus location

73

88.0

Stay in hometown

10

12.0

Education level

Diploma

1

1.2

Undergraduate student

(extension)

11

13.3

Undergraduate student

(regular)

57

68.7

Post Graduate

14

16.9

Parents’ job

Civil servants

25

30.1

Unemployment

20

24.1

Informal workers

15

18.1

Private company employee

14

16.9

The Changing Nature of Campus Health Insurance: Testing Portability Issues of National Health Insurance

15

n

%

Pensioner

9

10.8

Health Insurance

National Health Insurance

44

53.0

Commercial Health

Insurance

10

12.0

Both

4

4.8

None

25

30.1

Those characteristics impact the health insurance

utilisation. Migrant students who are not covered by

health insurance should be able to set aside their

living cost for healthcare purposes when sick. In this

case, a university health insurance scheme is very

much needed to ensure accessible healthcare service

during college. In 2019, when the National Health

Insurance is targeted to reach universal health

coverage, the university health insurance scheme

should be considered as another option to crawling

the niche market of students that are left behind by

the implementation of National Health Insurance.

A second alignment that should also be

considered is the existence of students who are

already registered as National Health Insurance

participants, but still choose primary healthcare in

their hometown. Based on the National Health

Insurance regulations, participants should choose

one primary healthcare to be the patient’s first

contact in using the healthcare facilities. By

choosing the primary healthcare facility, participants

can only be treated by that chosen primary

healthcare. Participants are not be allowed to access

other primary healthcare, except for the emergency

room. The portability issue has become the main

problem in this case.

3.1 The Chosen Primary Healthcare: A

Matter of Portability Issues

In the term of National Health Insurance

implementation, participants cannot directly utilise

the referral hospital without appropriate medical

indications. There is a strict referral mechanism

which has been created to ensure that there will be

no unnecessary treatment which potentially

disembogues high treatment cost.

National Health Insurance participants should

choose only one primary healthcare facility. This

primary healthcare facility is responsible for treating

the registered participants. This will be paid for by a

capitation mechanism based on the number of

National Health Insurance participants registered in

the primary healthcare facility. Participants do not

need to pay anything to the primary healthcare

facility when accessing the services. Vice versa, the

primary healthcare facility is prohibited to take a fee

for its service to the participants. Unfortunately,

participants cannot access the other primary

healthcare facilities freely. If participants want to

access a different one, they must change their

primary healthcare facility. Table 2 shows that most

of the students who already registered as National

Health Insurance participants are varied according to

the primary healthcare facility type chosen.

Table 2 The chosen primary healthcare facility by students

n

%

Location

Hometown

40

90.9

City of present campus

4

9.1

Type

General practitioner

13

29.5

24-hour clinic

4

9.1

Company-affiliated clinic

2

4.5

Public health centre

25

56.8

Most of the primary healthcare facilities chosen

by students are located in the student’s hometown.

Even though these students realise the long period of

study in college, they have decided to not change

their primary healthcare facility to a primary

healthcare facility located near their present college.

This means that this group of students will be face

difficulties when assessing a primary healthcare

facility using the National Health Insurance.

Students either need to return to their hometown to

access primary healthcare without charge or pay to

get treatment in their current city.

What if there is an emergency situation? National

Health Insurance accommodates emergency

situations, but with specific medical indications for

each disease or accident. Students with National

Health Insurance can use emergency treatment only

in the emergency room of a hospital without

consideration of where their primary healthcare

facility is situated. Even though students can access

it without any fee, incidence of emergency situations

is commonly rare. Most of the illnesses among

students are not considered as emergency cases. As

such, primary healthcare still becomes the first need

of students.

In spite of decentralization which promises to

bring health equity among citizens, the implications

of decentralised governance of health systems on

health- related equity are varied and depend on pre-

existing socio-economic and organisational context

(Costa-Font & Moscone 2008). It also argued that

decentralization results in ambiguous consequences

on efficiency; equity consequences are controversial

and address the relevance of redistribution

INAHEA 2017 - 4th Annual Meeting of the Indonesian Health Economics Association

16

mechanisms (Alves et al. 2013). Whereas

decentralization is pointed to responsible financing

the mobile citizens across the district area.

3.2 Students’ Need of Healthcare during

College

Normally, undergraduate students spend 3-4

years of their life struggling to graduate from

college. During this period, there are many

possibilities of students getting sick or having

accidents. Table 3 shows how students deal with

these conditions during college.

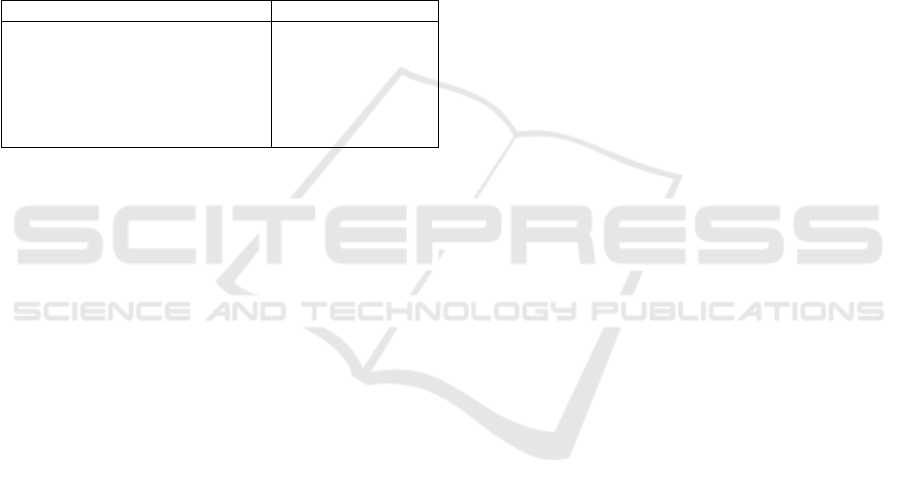

Table 3: Health-seeking behaviour of students during

college

Health-seeking behaviour

n

%

Self-treatment

24

28.9

Utilise private healthcare (OOP)

18

21.7

Utilise health facility with

commercial insurance

2

2.4

Utilise campus clinic

32

38.6

Return to hometown

7

8.4

Most of the students choose to utilise the

healthcare facility that is provided by their

university. This shows that the most accessible

healthcare treatment for students during college is

the campus clinic. Students also tend to cure their

sickness by self-treatment. Self-treatment is

commonly found in Indonesia due to the ease of

obtaining over-the-counter (OTC) medicine. As

educated people, students are confident in guessing

what their illness is and what kind of medicine they

should buy.

Surprisingly, none of students who participated

in this study utilised a healthcare facility using the

National Health Insurance scheme in the college

location. Students who were registered as National

Health Insurance participants chose to return to their

hometown to get treatment. This indicates that

portability issues still exist in the implementation of

National Health Insurance among migrant members.

Private health providers, including private healthcare

facilities and commercial health insurance providers,

could take advantage through this situation. There

are 21.7% of students who prefer to utilise the

private healthcare facility. Most of the students spent

Rp150,000 ($11) each time in utilising this private

healthcare. They pay this through an out-of-pocket

(OOP) mechanism.

Experience of how China finances its health

insurance system shows that the behaviour

management and purchasing mechanisms of

National Health Insurance perform poorly (Liu et al.,

2014). National Health Insurance participation has a

weak negative or even no significant association

with the OOP of hospitalised patients. National

Health Insurance seems to fail to reduce people’s

OOP. This also happens in our study. The trend of

students using OOP is high even though National

Health Insurance is already implemented.

There are emerging healthcare needs of migrant

students considering the location of the primary

healthcare facility they choose. The majority of

migrant students (93.3%) registered as National

Health Insurance participants still belong to the

primary healthcare facility in their hometown.

Vietnam’s experience clearly suggests that health

insurance strongly increases the access and reduces

the financial burden in healthcare utilisation

(Sepehri et al., 2009). In the case of migrant students

in Indonesia, rural-to-urban migrants should be

given increased portability. Pan et al. (2016) suggest

that the government should think about raising the

level of pooling or develop specific policies on

cross-regional transfer of entitlements. Our findings

show that National Health Insurance simply cannot

promote the students’ ability to access healthcare in

the campus location if the portability issue still

exists.

3.3 Inefficiency of Healthcare Service among

Students

This study provides evidence that portability is

something that should be rethought in providing

insurance for college students. Different from other

levels of education, students in college are

commonly separated from their parents during study.

They must take care of their health by themselves.

Rising et al. (2007) explained that even though

health insurance facilitates access to care, enrolment

alone is not enough to ensure the receipt of

preventive health care. Study by Jung et al. (2013)

revealed that the availability of parental health

insurance can have significant effects on the

probability that a young individual enrols as a full-

time student. College enrolment policy is the first

screening effort to capture the ability of each student

in protecting their life during college. A study about

the health need of college students also shows that

they learn to manage their own health, gain their

health knowledge and begin to start health habits

during study period (Nguyen et al. 2016). These

findings imply that campus student health centres

should be better evaluate and facilitate health

education.

The Changing Nature of Campus Health Insurance: Testing Portability Issues of National Health Insurance

17

Before National Health Insurance

implementation, the college enrolment system in

Indonesia never prescribed that such students should

be covered by health insurance. By 2019, Indonesia

is targeted to achieve Universal Health Coverage.

Considering this roadmap, since 2017, the National

Health Insurance provider has cooperated with

universities to ensure that all new students are

already registered. Unfortunately, a university

cannot push their students to change their primary

healthcare facility to the campus clinic. This

potentially causes inefficiency in campus clinic

management. Universities should finance their

clinics in providing healthcare service for students.

On the other hand, students still have to pay the

National Health Insurance dues.

Moreover, most students in university in

Indonesia are regular undergraduate students who

have used the single tuition system for college

payment. In the single tuition system, the university

only permitted to collect funds from students once in

one education year. The amount of this fund is

determined by the Ministry of High Education. A

university should be able to manage this fund for all

education processes. Unfortunately, in the single

tuition fee policy, the amount of funds for students’

healthcare during college is unclear. University

clinics have difficulty in managing the health portion

that is embedded in the single tuition fee. The

benefit package received by students at the

university clinic is highly dependent on the

university’s ability in financing the campus clinic.

4 CONCLUSION

Indonesia faces big challenges regarding its

portability issues. The wide area of Indonesia brings

consequences in the application of National Health

Insurance across different primary healthcare

facilities across the country. Migrant college

students are one of the vulnerable groups of

population that have high risk in this case. The

portability issue regarding health insurance for

college students not only disadvantage them, but

also induces inefficiency in the campus clinic

management. The campus enrolment system should

be designed to accommodate this portability issue in

order to guarantee that all students will be able to

access a qualified healthcare service during study.

ACKNOWLEDGEMENTS

We would like to send our appreciation to the

management of Airlangga University Healthcare

Centre (AHCC) for intensive discussion about

campus clinic management in the National Health

Insurance scheme.

REFERENCES

Alves, J., Peralta, S. & Perelman, J., 2013. Efficiency and

equity consequences of decentralization in health: An

economic perspective. Revista Portuguesa de Saude

Publica, 31(1), pp.74–83. Available at:

http://dx.doi.org/10.1016/j.rpsp.2013.01.002.

Callahan, S.T., 2007. Bridging the gaps in health

insurance coverage for young adults. The Journal of

adolescent health : official publication of the Society

for Adolescent Medicine, 41(4), pp.321–2. Available

at: http://www.ncbi.nlm.nih.gov/pubmed/17875456.

Costa-Font, J. & Moscone, F., 2008. The impact of

decentralization and inter-territorial interactions on

Spanish health expenditure. Empirical Economics,

34(1), pp.167–184.

Jung, J., Hall, D.M.H. & Rhoads, T., 2013. Does the

availability of parental health insurance affect the

college enrollment decision of young Americans?

Economics of Education Review, 32(1), pp.49–65.

Available at:

http://dx.doi.org/10.1016/j.econedurev.2012.09.010.

Liu, K., Wu, Q. & Liu, J., 2014. Examining the

association between social health insurance

participation and patients’ out-of-pocket payments in

China: The role of institutional arrangement. Social

Science and Medicine, 113(2014), pp.95–103.

Available at:

http://dx.doi.org/10.1016/j.socscimed.2014.05.011.

Nguyen, J. et al., 2016. Use and interest in complementary

and alternative medicine among college students

seeking healthcare at a university campus student

health center. Complementary Therapies in Clinical

Practice, 24(2016), pp.103–108. Available at:

http://dx.doi.org/10.1016/j.ctcp.2016.06.001.

Pan, X.-F., Xu, J. & Meng, Q., 2016. Integrating social

health insurance systems in China. The Lancet,

387(10025), pp.1274–1275. Available at:

http://www.thelancet.com/article/S0140673616300216

/fulltext.

Price PhD, MPH, J.H. et al., 2010. College Students’

Perceptions and Experiences With Health Insurance.

Journal of the National Medical Association, 102(12),

pp.1222–1230. Available at:

http://proxygw.wrlc.org/login?url=http://search.proque

st.com/docview/822764203?accountid=11243%5Cnhtt

p://findit.library.gwu.edu/go?ctx_ver=Z39.88-

2004&ctx_enc=info:ofi/enc:UTF-

8&rfr_id=info:sid/ProQ:sciencejournals&rft_val_fmt=

INAHEA 2017 - 4th Annual Meeting of the Indonesian Health Economics Association

18

info:ofi/fmt:kev:mtx:journal.

Rising, J.P. et al., 2007. Healthy Young Adults:

Description and Use of an Innovative Health Insurance

Program. Journal of Adolescent Health, 41(4),

pp.350–356.

Sepehri, A., Sarma, S. & Serieux, J., 2009. Who is giving

up the free lunch? The insured patients’ decision to

access health insurance benefits and its determinants:

Evidence from a low-income country. Health Policy,

92(2–3), pp.250–258.

Ybarra, M., Ha, Y. & Chang, J., 2017. Health insurance

coverage and routine health care use among children

by family immigration status. Children and Youth

Services Review, 79(2016), pp.97–106. Available at:

http://dx.doi.org/10.1016/j.childyouth.2017.05.027.

The Changing Nature of Campus Health Insurance: Testing Portability Issues of National Health Insurance

19