Analysis on Dynamic Relationship between Equity Financing and

Agricultural Integration

Based on VAR Model and Impulse Response

Kun Song, Xiaoqian Liu

School of Economics, Sichuan Agricultural University, Chengdu 611130, China

Keywords: Agricultural Integration; Equity Financing; Vector Auto-Regression Model; Impulse Response.

Abstract: Equity financing of agricultural firm is one of financing methods encouraged by the government. Research

on the relationships is the key problem of how equity financing supports agricultural integration. Based on

VAR model, cointegration analysis and Granger causality test is done to study the equilibrium relationship

and the dynamic impact is analyzed by using impulse response. Results show that size and efficiency of

equity financing have a positive relationship with agricultural integration. But size is more useful than

efficiency, and structure of equity financing and agricultural integration move in the opposite direction.

Thus, only equity financing with large size, efficiency, reasonable structure and right investment will

actually have an active impact on agricultural integration. Meanwhile, the development of agricultural

integration has not played a leading role on equity financing, and they have been in a low collaborative

degree.

1 INTRODUCTION

As agricultural integration is the "short slab" of

China's socialist modernization,Chinese government

attaches great importance to the structural

contradiction. From 2014 to 2016, "agricultural

modernization" has been written in the title of No.1

Central Document for consecutive three years.

Reform and Innovation are required by accelerating

the agricultural modernization, one of the key is to

develop the agricultural integration, which is the

developing direction of modern agriculture. But

reform needs capital support greatly. At present, the

fund investment of agriculture integration in China

can

’

t meet the demand of the development of the

agricultural integration: (Cuifang Wu, 2009) roughly

estimates that rural capital supply and demand gap

in 2012 is 18.8489 trillion Yuan, not to mention the

lack and serious insufficient of services in securities,

insurance and trust organizations; (Peng Jia, etc,

2011) etc find even areas where the development of

agricultural integration are better, financing

difficulty is still prominent; (Cheng Zhao and

Zhihong Huang, 2011) point out that the financial

repression exists in the process of agricultural

integration in our country, so (Zheng Hong, 2011)

puts forward obtaining financial support by the rural

financial innovation, has become an important

support for the development of agricultural

integration.

Thus, research on the correlation is the key

problem of how equity financing supports

agricultural integration. The following three

problems must be answered: Firstly, what is the

actual impact about the expanse of the absolute scale

of equity financing to the promotion of agricultural

integration? Secondly, the absolute scale of

agricultural integration or efficiency, which is more

important? Thirdly, the increase of the proportion of

equity financing to bank credit whether can play a

positive role in promoting the agriculture integration?

Currently no scholars study the above problems.

2 VARIBLE AND DATA SOURCES

2.1 The development of agricultural

integration

Use AL to indicate agricultural integration. To

quantitatively depict the development of agricultural

integration per year in our country, using Weng

Yao

’

s discriminant analysis method as reference,

construct discriminant index system: per capita GDP

277

Liu X. and Song K.

Analysis on Dynamic Relationship between Equity Financing and Agricultural Integration - Based on VAR Model and Impulse Response.

DOI: 10.5220/0006449002770282

In ISME 2016 - Information Science and Management Engineering IV (ISME 2016), pages 277-282

ISBN: 978-989-758-208-0

Copyright

c

2016 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

277

(X

1

), GDP proportion in the first industry (X

2

), the

second industry labor proportion (X

3

), per capita

grain output (X

4

) and the Engel’s coefficient (X

5

),

and get the started stage of agricultural integration

(F

1

), growth stage(F

2

) and mature stage’s (F

3

)

discriminant value. These data are from "China

Agricultural Yearbook", "China Rural Statistical

Yearbook", "China Statistical Yearbook" and

"China

’

s State Administration of Foreign Exchange".

2.2 Setting the equity financing

variables

To reveal the relationship between the equity

financing development and agricultural integration,

this paper builds three sets of indicators to

comprehensively measure the development of equity

financing: equity financing scale index (SIZE=raised

total funds by agricultural firm through issuing

stocks within the territory/nominal agricultural

GDP), equity financing efficiency index

(EFF=raised total funds by agricultural firm through

issuing stocks within the territory /rural fixed asset

investment) , equity structure index (STR= raised

total funds by agricultural firm through issuing

stocks within the territory /agricultural loans).

2.3 The data source

(1) Agriculture GDP. Select the first industry as

nominal agriculture GDP, data from "China

Statistical Yearbook". (2) Agricultural loans. Data is

from "Almanac of China's Finance and Banking",

"China Compendium of Statistics" and "China's

Rural Financial Report". (3) Rural fixed asset

investment. The data is from "Rural China

Statistical Yearbook". (4) This paper chooses the

ecological-economic enterprises and agricultural

product processing industry. Raising funds by

issuing stocks in the main board, the small and

medium-sized board, the "New Three Board", as

well as in the national regional equity trading center

is equal to that by agricultural firm. In 1992, the

earliest agricultural firm went public in Shanghai

and Shenzhen stock exchange, so this paper sample

time spans from 1992 to 2015, 24 years in total. This

part of the data is from Wind information.

3 EMPIRICAL ANALYSES

3.1 Measurement of agricultural

integration level

According to the set variables and collected data,

from 1992 to 2015, the paper calculates the

discriminant value of agricultural integration in the

start, grow and mature stage and the level of

agricultural integration (as shown in table 1).

Table 1:1992-2015 year value of Agricultural integration.

year AL year AL

1992 0.9803 2004 0.9207

1993 0.9840 2005 0.9173

1994 0.9810 2006 0.9162

1995 0.9800 2007 0.9252

1996 0.9840 2008 0.9372

1997 0.9914 2009 0.9423

1998 0.9988 2010 0.9510

1999 0.9216 2011 0.9638

2000 0.9197 2012 0.9703

2001 0.9191 2013 0.9799

2002 0.9187 2014 0.9879

2003 0.9164 2015 0.9927

3.2 Equilibrium relationship of Equity

financing and agricultural

integration

3.2.1 The stationary test of variables

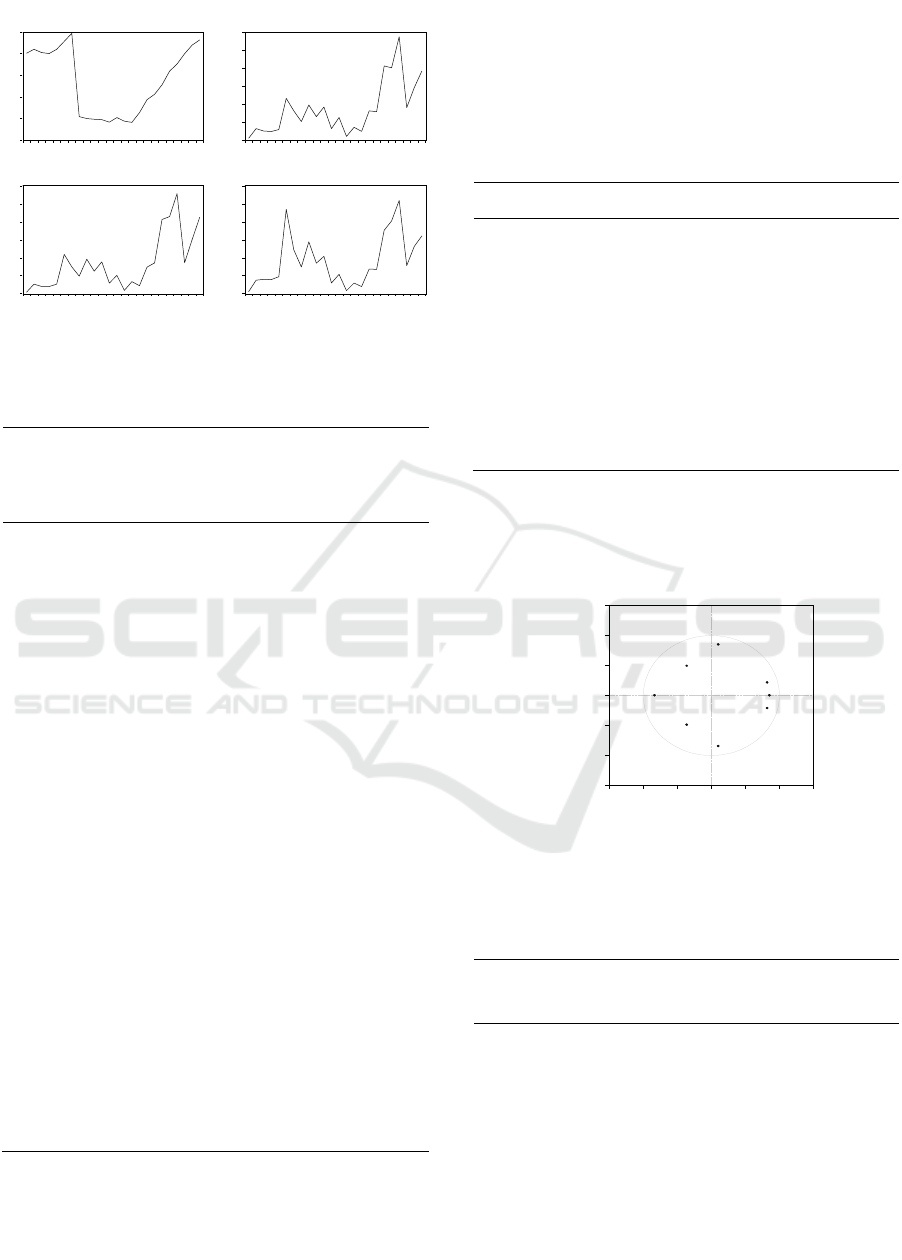

Figure 1 shows that ADF unit root test should

contain intercept and trend items. Table 2 shows the

original sequences of the variables are unstable; the

first order difference sequences are stable under 1%

significance level.

ISME 2016 - Information Science and Management Engineering IV

278

ISME 2016 - International Conference on Information System and Management Engineering

278

0.90

0.92

0.94

0.96

0.98

1.00

92 94 96 98 00 02 04 06 08 10 12 14

A

L

.000

.005

.010

.015

.020

.025

.030

92 94 96 98 00 02 04 06 08 10 12 14

EFF

.000

.001

.002

.003

.004

.005

.006

92 94 96 98 00 02 04 06 08 10 12 14

SIZE

.000

.002

.004

.006

.008

.010

.012

92 94 96 98 00 02 04 06 08 10 12 14

STR

Fig1: The tendency of the variables.

Table 2: ADF results of Variable.

variab

le

Inspecti

on type

(c t p)

AD

F

1%

critical

value

5%

critical

value

10%

critical

value

result

AL

(c t 0)

-0.9

1

-4.41 -3.62 -3.24

nonstat

ionary

*

SIZE

(c t 0)

-2.8

5

-4.41 -3.62 -3.24

nonstat

ionary

*

EFF

(c t 0)

-3.1

3

-4.41 -3.62 -3.24

nonstat

ionary

*

STR

(c t 0)

-3.0

4

-4.41 -3.62 -3.24

nonstat

ionary

*

D(AL)

(c t 5)

-6.8

5

-4.61 -3.71 -3.29

station

ary***

D(SIZ

E)

(c t 0)

-6.2

4

-4.44 -3.63 -3.25

station

ary***

D(EF

F)

(c t 0)

-7.0

4

-4.44 -3.63 -3.25

station

ary***

D(ST

R)

(c t 0)

-6.3

4

-4.44 -3.63 -3.25

station

ary***

3.2.2 The optimum lag of VAR model

Table 3 shows that except the Log L, the rest clearly

show that the optimum lag is 2 period, so VAR(2)

model is established in this paper.

Table 3: Judgment of VAR lag phase.

Log L LR FPE AIC SC HQ

0

388.84

26

NA 1.42e-21 -36.65 -36.45 -36.60

1

424.49

57

54.32 2.27e-22 -38.52 -37.52 -38.30

2

464.24

26

45.425

*

2.89e-23

*

-40.78* -38.99*

-40.39

*

3

478.70

61

11.019 6.08e-23 -40.63 -38.05 -40.07

3.2.3 The stationary test of VAR model

Figure 2 indicates that the VAR model satisfy the

stability condition.

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

-1.5 -1.0 -0.5 0.0 0.5 1.0 1.5

In

v

e

r

se Roots of AR Cha

r

acte

r

istic Pol

y

nomial

Fig 2: Test figure of AR root of VAR (2).

3.2.4 The Cointegration Test

Table 4: Johansen’s co-integration test of VAR(2).

hypothetical

data

characteristi

cs value

Trac

e test

5%critical

value

probability

(**)

none 0.72 57.71 47.85 0.00

at most one 0.56 30.83 29.79 0.03

at most two 0.45 13.36 15.49 0.10

at most three 0.02 0.561 3.841 0.45

Analysis on Dynamic Relationship between Equity Financing and Agricultural Integration - Based on VAR Model and

Impulse Response

279

Analysis on Dynamic Relationship between Equity Financing and Agricultural Integration - Based on VAR Model and Impulse Response

279

Statistics in table 4 illustrates there is long-term

equilibrium relationships between the EFF, STR,

SIZE and AL.

)67.11()93.70()62.342(

52.013.33133.1616

μ

+

−−= STREFFSIZE

A

L

(1)

The analysis of formula (1) is as follows: (1)

Equity financing scale (SIZE) expending has played

a positive role in promoting agricultural integration.

(2)Improvement of the equity financing efficiency

(EFF) also has played a positive role in promoting

the development of agriculture integration. But

coefficient shows that the positive promoting effect

of the efficiency is weaker than the scale, which is

due to relatively limited attractive of the agricultural

investment environment, At present, agricultural

firm is in small scale(Cuifang Wu, 2009), and the

endogenous financing is extremely limited(

Peng Jia,

etc, 2011

), which lead to general low efficiency of

equity financing. (3) The structure of equity

financing and agricultural integration moves in the

opposite direction, indicating that the more

proportion in credit funds equity financing takes, the

worse the ascension of agriculture integration is.

3.2.5 Causality test

Table 5 shows that the probability values of statistics

AL to SIZE, EFF and STR are 0.0435, 0.0536,

0.0000, illustrating SIZE, EFF and STR variable are

the causes of Granger of AL, three variables need to

be included in the corresponding equation of AL

endogenous variable. From joint survey analysis of

AL to SIZE, EFF and STR, probability value of

statistics are 0.0000, showing that lags of SIZE, EFF

and STR to AL are significant. In addition, SIZE,

EFF and STR to AL individual factors are not

significant, namely, SIZE, EFF and STR to AL are

not significant: that is to say, the Granger cause of

SIZE, EFF, and STR is not AL, and state that the

development of agriculture integration does no good

to equity financing.

Table 5:Grangertest of VAR(2).

explained variable: AL

explanatory

variable

Chi-sq df P value

SIZE 6.2694 2 0.0435

EFF 5.7437 2 0.0536

STR 65.7177 2 0.0000

total 81.4202 6 0.0000

explained variable: SIZE

explanatory

variable

Chi-sq df P value

AL 1.4185 2 0.4920

EFF 26.528 2 0.0000

STR 1.5211 2 0.4674

total 33.329 6 0.0000

explained variable: EFF

explanatory

variable

Chi-sq df P value

AL 1.3162 2 0.5178

SIZE 30.710 2 0.0000

STR 0.7756 2 0.6785

total 38.064 6 0.0000

explained variable: STR

explanatory

variable

Chi-sq df P value

AL 3.0809 2 0.2143

SIZE 11.948 2 0.0025

EFF 11.804 2 0.0027

total 17.225 6 0.0085

3.3 Dynamic effect analysis based

impulse response function

3.3.1 Response of multi-factor to the

development of agricultural

integration

Figure 3(1) shows the following three aspects: (1)

Disturbed by SIZE standard deviation, the initial

response of AL is zero, in the second period, there is

a slightly negative response, and then quickly into

third period, reach a maximum 0.009. Namely, the

equity financing scale changes in the third period

has the strongest impaction on the agriculture

integration. Although over time the impact gradually

weakened, but the trend reached the maximum value

0.009, which illustrates that the increasing scale of

equity financing can bring a positive influence to the

agriculture integration. (2)Response of AL to one

S.D. EFF innovation presents zero in the first period,

in the second period,it begins to decline to a

negative response, until the third period. Then it

reaches the minimum negative response value. Soon,

ISME 2016 - Information Science and Management Engineering IV

280

ISME 2016 - International Conference on Information System and Management Engineering

280

in the seventh period it begins to appear positive

response and fiercely rise, until 12th period. This

suggests that the promotion of the efficiency of

equity financing brings negative impact on

agriculture integration, but it is relatively short, in

the long run. Probably it takes times to translate

equity financing funds into agricultural fixed assets

(eg, agricultural infrastructure construction). After

the completion of the investment, it will continue to

accelerate the process of agriculture integration

naturally. (3)Response of AL to STR in the initial

period is still zero, in the second period turns to a

positive response, then in the third period rapidly

dropped to zero, and kept negative response all the

time. This shows that equity financing structure

changes can bring positive influence to the

agriculture integration in the short time, but be

negative in the long run. This negative impact is

undoubtedly caused by changing investment of

agricultural funds.

3.3.2 Response of development of

agricultural integration to the

multi-factor

Figure 3(2), (3) and (4) show that response of SIZE,

EFF and STR to S.D.AL innovation are very similar.

At first, there is biggest positive response. Then the

response continues to decline, and be positive or

negative continuously. But the trend is positive, and

tends to zero at the 21st period. The above reality

illustrates that agriculture integration may produce

positive influence on rural equity financing scale,

efficiency and structure, but the effect is weak and it

is difficult to distinguish, which is caused by small

shares of agricultural firms in the capital market.

-.016

-.012

-.008

-.004

.000

.004

.008

.012

2 4 6 8 10 12 14 16 18 20 22 24

AL EFF SIZE STR

Response of AL to Cholesky

One S.D. Innovations

-.004

-.002

.000

.002

.004

.006

2 4 6 8 10 12 14 16 18 20 22 24

AL EFF SIZE STR

Respons e of EFF to Cholesky

One S.D. Innovations

-

.0008

-

.0004

.0000

.0004

.0008

.0012

2 4 6 8 10 12 14 16 18 20 22 24

AL EFF SIZE STR

Response of SIZE to Cholesky

One S.D. Innovations

-.002

-.001

.000

.001

.002

2 4 6 8 10 12 14 16 18 20 22 24

AL EFF SIZE STR

Response of STR to Cholesky

One S.D. Innovations

(1)

Fig3: Response to Generalized One S.D.

Innovations

±

2 S.E.

4 CONCLUSIONS AND

RECOMMENDATION

4.1 Main conclusions

4.1.1 Long-term equilibrium relationship

Equity financing in China and agriculture integration

have a long-term equilibrium relationship, scale and

efficiency of equity financing have a positive impact

on agriculture integration. But expanding the scale

of equity financing should be a dominant factor, and

the efficiency has a limited role in promoting the

agriculture integration. So vigorously developing

equity financing can contribute to the promotion of

agriculture integration, which is based on two

conditions: firstly, increase the financing scale of

agricultural firms; secondly, restrict agricultural

firms changing direction of investment. Otherwise,

the equity financing will not conducive to the

development of agriculture integration.

4.1.2 Short term equilibrium relationship

Only equity financing with large size, efficiency,

reasonable structure and right investment will

actually have an active impact on agricultural

integration. However, Agriculture integration is not

the Granger reason of all variables, which is related

to that equity financing takes too small shares in

overall financing in our country, so they have been

in a low collaborative degree.

4.1.3 Dynamic Relationship

Equity financing efficiency will begin to have a

negative impact on agriculture integration, but it

begins and always keeps a positive response in the

seventh period, and this is related to the cycle of

fixed assets projects of agriculture integration,

presenting positive for a long time. As long term

equity financing structure impacted, it restrains the

development of the agriculture integration, still

related to the listed firms changing funds investing

direction. Only equity financing with large size,

efficiency, reasonable structure and right investment

will actually have an active impact on agricultural

integration, but these influences show certain

hysteresis. After agriculture integration hit, the

impact on other variables is not sure. The reason is

that shares of agricultural firms in the capital market

are too small.

Analysis on Dynamic Relationship between Equity Financing and Agricultural Integration - Based on VAR Model and

Impulse Response

281

Analysis on Dynamic Relationship between Equity Financing and Agricultural Integration - Based on VAR Model and Impulse Response

281

4.2 Policy recommendations

4.2.1 About enlarging the scale of equity

Speed up the listing process is a necessary method.

The recognized standard of the government to

leading enterprises of national agriculture integration

is very strict, and it needs to reach both standard of

business scale and indicators so that the company

can have the qualification. For this kind of

enterprises, as long as the relevant indicators meet

the requirements of the listed company, regulators

should ease stock reform time.

4.2.2 About changes investment of raised

funds

Apart from strengthening the regulation of securities

regulators, the government should play the

government's coordination services, and give

industry guidance to the listed agricultural firms on

how to raise and use funds. In addition, government

should optimize rural agricultural

industry

environment and soft financing environment, such as

invest to rural public infrastructure, and innovate the

operation mechanism of government, in order to

attract more capital investment.

REFERENCES:

Cuifang Wu., 2009. Study on the Outflow of Rural Capital

in China, China Social Sciences Publishing House.

Beijing, 1

st

edition.

Cheng Zhao, Zhihong Huang., 2014. Study of Financial

Repression and Counter Measures of Development of

Agricultural Industrialization Based on the Analysis of

Operating Risk of Corporation Perspective. HUNAN

SOCIAL SCIENCES.

Chibo Chen, Peng Jia, Panfeng Zhang., 2011. Research on

the Relationship between Agricultural

Industrialization and Financial Supply in Rural

Areas

:

Taking Henan Province as Example.

JOURNAL OF NORTHEAST NORMAL

UNIVERSITY(Philosophy and Social Sciences) .

Zheng Hong., 2011. Is the Reform of New Rural Financial

Institutions Feasible? Analysis from the Perspective of

Monitoring Efficiency. ECONOMIC RESEARCH

JOURNAL.

ISME 2016 - Information Science and Management Engineering IV

282

ISME 2016 - International Conference on Information System and Management Engineering

282