Piecewise Chebyshev Factorization based Nearest Neighbour

Classification for Time Series

Qinglin Cai, Ling Chen and Jianling Sun

College of Computer Science and Technology, Zhejiang University, Hangzhou, China

Keywords: Time Series, Piecewise Approximation, Similarity Measure.

Abstract: In the research field of time series analysis and mining, the nearest neighbour classifier (1NN) based on

dynamic time warping distance (DTW) is well known for its high accuracy. However, the high

computational complexity of DTW can lead to the expensive time consumption of classification. An

effective solution is to compute DTW in the piecewise approximation space (PA-DTW), which transforms

the raw data into the feature space based on segmentation, and extracts the discriminatory features for

similarity measure. However, most of existing piecewise approximation methods need to fix the segment

length, and focus on the simple statistical features, which would influence the precision of PA-DTW. To

address this problem, we propose a novel piecewise factorization model for time series, which uses an

adaptive segmentation method and factorizes the subsequences with the Chebyshev polynomials. The

Chebyshev coefficients are extracted as features for PA-DTW measure (ChebyDTW), which are able to

capture the fluctuation information of time series. The comprehensive experimental results show that

ChebyDTW can support the accurate and fast 1NN classification.

1 INTRODUCTION

In the research field of time series analysis and

mining, time series classification is an important

task. A plethora of classifiers have been developed

for this task (Esling et al, 2012; Fu, 2011), e.g.,

decision tree, nearest neighbor (1NN), naive Bayes,

Bayesian network, random forest, support vector

machine, etc. However, the recent empirical

evidence (Ding et al, 2008; Hills et al, 2014; Serra et

al, 2014) strongly suggests that, with the merits of

robustness, high accuracy, and free parameter, the

simple 1NN classifier employing generic time series

similarity measure is exceptionally difficult to beat.

Besides, due to the high precision of dynamic time

warping distance (DTW), the 1NN classifier based

on DTW has been found to outperform an

exhaustive list of alternatives (Serra et al, 2014),

including the decision trees, the multi-scale

histograms, the multi-layer perception neural

networks, the order logic rules with boosting, as well

as the 1NN classifiers based on many other

similarity measures. However, the computational

complexity of DTW is quadratic to the time series

length, i.e., O(n

2

), and the 1NN classifier has to

search the entire dataset to classify an object. As a

result, the 1NN classifier based on DTW is low

efficient for the high-dimensional time series. To

address this problem, researchers have proposed to

compute DTW in the alternative piecewise

approximation space (PA-DTW) (Keogh et al, 2001;

Keogh et al, 2004; Chakrabarti et al, 2002; Gullo et

al, 2009), which transforms the raw data into the

feature space based on segmentation, and extracts

the discriminatory and low-dimensional features for

similarity measure. If the original time series with

length n is segmented into N (N << n) subsequences,

the computational complexity of PA-DTW will

reduce to O(N

2

).

Many piecewise approximation methods have

been proposed so far, e.g., piecewise aggregation

approximation (PAA) (Keogh et al, 2001), piecewise

linear approximation (PLA) (Keogh et al, 2004;

Keogh et al, 1999), adaptive piecewise constant

approximation (APCA) (Chakrabarti et al, 2002),

derivative time series segment approximation (DSA)

(Gullo et al, 2009), piecewise cloud approximation

(PWCA) (Li et al, 2011), etc. The most prominent

merit of piecewise approximation is the ability of

capturing the local characteristics of time series.

However, most of the existing piecewise

approximation methods need to fix the segment

84

Cai, Q., Chen, L. and Sun, J..

Piecewise Chebyshev Factorization based Nearest Neighbour Classification for Time Series.

In Proceedings of the 7th International Joint Conference on Knowledge Discovery, Knowledge Engineering and Knowledge Management (IC3K 2015) - Volume 1: KDIR, pages 84-91

ISBN: 978-989-758-158-8

Copyright

c

2015 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

length, which is hard to be predefined for the

different kinds of time series, and focus on the

simple statistical features, which only capture the

aggregation characteristics of time series. For

example, PAA and APCA extract the mean values,

PLA extracts the linear fitting slopes, and DSA

extracts the mean values of the derivative

subsequences. If PA-DTW is computed on these

methods, its precision would be influenced.

In this paper, we propose a novel piecewise

factorization model for time series, named piecewise

Chebyshev approximation (PCHA), where a novel

code-based segmentation method is proposed to

adaptively segment time series. Rather than focusing

on the statistical features, we factorize the

subsequences with Chebyshev polynomials, and

employ the Chebyshev coefficients as features to

approximate the raw data. Besides, the PA-DTW

based on PCHA (ChebyDTW) is proposed for the

1NN classification. Since the Chebyshev

polynomials with different degrees represent the

fluctuation components of time series, the local

fluctuation information can be captured from time

series for the ChebyDTW measure. The

comprehensive experimental results show that

ChebyDTW can support the accurate and fast 1NN

classification.

2 RELATED WORK

2.1 Data Representation

In many application fields, the high dimensionality

of time series has limited the performance of a

myriad of algorithms. With this problem, a great

number of data approximation methods have been

proposed to reduce the dimensionality of time series

(Esling et al, 2012; Fu, 2011). In these methods, the

piecewise approximation methods are prevalent for

their simplicity and effectiveness. The first attempt

is the PAA representation (Keogh et al, 2001),

which segments time series into the equal-length

subsequences, and extracts the mean values of the

subsequences as features to approximate the raw

data. However, the extracted single sort of features

only indicates the height of the subsequences, which

may cause the local information loss. Consecutively,

an adaptive version of PAA, named piecewise

constant approximation (APCA) (Chakrabarti et al,

2002), was proposed, which can segment time series

into the subsequences with adaptive lengths and thus

can approximate time series with less error. As well,

a multi-resolution version of PAA, named MPAA

(Lin et al, 2005), was proposed, which can

iteratively segment time series into 2

i

subsequences.

However, both of the variations inherit the poor

expressivity of PAA. Another pioneer piecewise

representation is the PLA (Keogh et al, 2004; Keogh

et al, 1999), which extracts the linear fitting slopes

of the subsequences as features to approximate the

raw data. However, the fitting slopes only reflect the

movement trends of the subsequences. For the time

series fluctuating sharply with high frequency, the

effect of PLA on dimension reduction is not

prominent. In addition, two novel piecewise

approximation methods were proposed recently. One

is the DSA representation (Gullo et al, 2009), which

takes the mean values of the derivative subsequences

of time series as features. However, it is sensitive to

the small fluctuation caused by the noise. The other

is the PWCA representation (Li et al, 2011), which

employs the cloud models to fit the data distribution

of the subsequences. However, the extracted features

only reflect the data distribution characteristics and

cannot capture the fluctuation information of time

series.

2.2 Similarity Measure

DTW (Esling et al, 2012; Fu, 2011; Serra et al,

2014) is one of the most prevalent similarity

measures for time series, which is computed by

realigning the indices of time series. It is robust to

the time warping and phase-shift, and has high

measure precision. However, it is computed by the

dynamic programming algorithm, and thus has the

expensive O(n

2

) computational complexity, which

largely limits its application to the high dimensional

time series (Rakthanmanon et al, 2012). To

overcome this shortcoming, the PA-DTW measures

were proposed. The PAA representation based

PDTW (Keogh et al, 2000) and the PLA

representation based SDTW (Keogh et al, 1999) are

the early pioneers, and the DSA representation based

DSADTW (Gullo et al, 2009) is the state-of-the-art

method. Rather than in the raw data space, they

compute DTW in the PAA, PLA, and DSA spaces

respectively. Since the segment numbers are much

less than the original time series length, the PA-

DTW methods can greatly decrease the

computational complexity of the original DTW.

Nonetheless, the precision of PA-DTWs greatly

depends on the used piecewise approximation

methods, where both the segmentation method and

the extracted features are crucial factors. As a result,

with the weakness of the existing piecewise

approximation methods, the PA-DTWs cannot

Piecewise Chebyshev Factorization based Nearest Neighbour Classification for Time Series

85

achieve the high precision. In our proposed

ChebyDTW, a novel adaptive segmentation method

and the Chebyshev factorization are used, which

overcomes the drawback of the fixed segmentation,

and can capture the fluctuation information of time

series for similarity measure.

3 PIECEWISE FACTORIZATION

Without loss of generality, we first give the relevant

definitions as follows.

Definition 1. (Time Series): The sample

sequence of a variable X over n contiguous time

moments is called time series, denoted as T = {t

1

, t

2

,

…, t

i

, …, t

n

}, where t

i

∈

R denotes the sample value

of X on the i-th moment, and n is the length of T.

Definition 2. (Subsequence): Given a time series

T = {t

1

, t

2

, …, t

i

, …, t

n

}, the subset S of T that

consists of the continuous samples {t

i+1

, t

i+2

, …, t

i+l

},

where 0 ≤ i ≤ n-l and 0 ≤ l ≤ n, is called the

subsequence of T.

Definition 3. (Piecewise Approximation

Representation): Given a time series T = {t

1

, t

2

, …,

t

i

, …, t

n

}, which is segmented into the subsequence

set S = {S

1

, S

2

, …, S

j

, …, S

N

}, if ∃ f: S

j

→ V

j

= [v

1

, ...,

v

m

]

∈

R

m

, then the set V = {V

1

, V

2

, …, V

j

, …, V

N

} is

called the piecewise approximation of T.

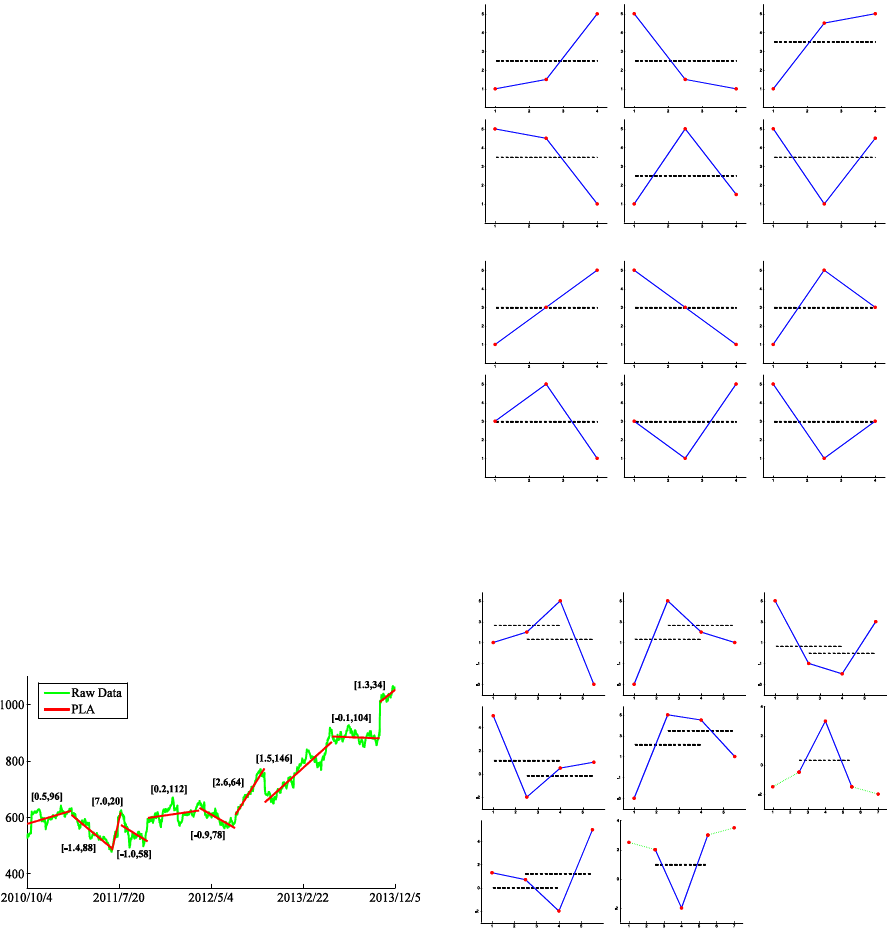

Figure 1 shows the example of PLA

representation (in red), for the stock price time series

(in green) of Google Inc. (symbol: GOOG) from The

NASDAQ Stock Market, which consists of the close

prices at 800 consecutive trading days

(2010/10/4~2013/12/5). As shown, PLA takes the

linear fitting slopes and the spans of the

subsequences as features to approximate the raw

data, e.g., [0.5, 96] for the first subsequence.

Figure 1: The PLA representation for the stock price time

series.

3.1 Adaptive Segmentation

Inspired by the Marr's theory of vision (Ullman et al,

1982), we regard the turning points, where the trend

of time series changes, as a good choice to segment

time series. However, the practical time series is

mixed with a mass of noise, which results in many

trivial turning points with small fluctuation. This

problem can be simply solved by the efficient

moving average (MA) smoothing method (Gao et al,

2010).

(a)

(b)

Figure 2: Three adjacent samples with the cell codes of (a)

basic relationships, and (b) specific relationships.

Figure 3: The minimum turning patterns composed with

two cell codes.

In order to recognize the significant turning

points, we first exhaustively enumerate the location

001-110 011-100

100-001

100-011

011-110

110-001

0

0

μ

0

0

0

1

1

011

110

1

0

010

1

0

0

1

100

1

001

001

0

110

0

1

1

0

0

1

010

0

1

1

0

1

010

0

μ

1

0

1 1

101

1

0

101

1

0

1

101

101

010

KDIR 2015 - 7th International Conference on Knowledge Discovery and Information Retrieval

86

relationships of three adjacent samples t

1

-t

3

with

their mean μ in time series, as shown in Figure 2. Six

basic cell codes can be defined as Figure 2(a), which

is composed by the binary codes δ

1

-δ

3

of t

1

-t

3

, and

denoted as Φ(t

1

, t

2

, t

3

) = (δ

1

δ

2

δ

3

)

b

. Six special

relationships that one of t

1

-t

3

equals to μ are encoded

as Figure 2(b).

Based on the cell codes, all the minimum turning

patterns (composed with two cell codes) at the

turning points can be enumerated as Figure 3. Note

that, the basic cell codes 010 and 101 per se are the

turning patterns. Then, we employ a sliding window

with length 3 to scan the time series, and encode the

samples within each window by Figure 2. In this

process, all the significant turning points can be

found by matching Figure 3, with which time series

can be segmented into the subsequences with the

adaptive lengths.

However, the above segmentation is not perfect.

Although the trivial turning points can be removed

with the MA, the "singular" turning patterns may

exist, i.e., the turning patterns appearing very close.

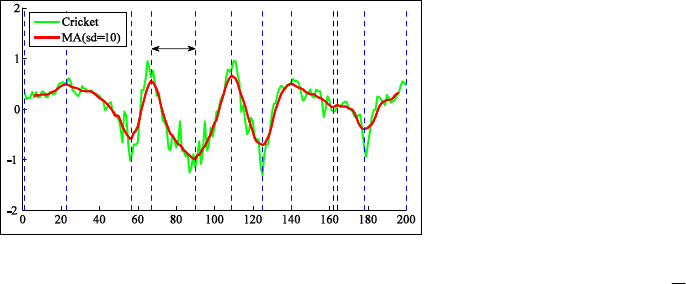

As shown in Figure 4, a Cricket time series from the

UCR time series archive (Keogh et al, 2011) is

segmented by the turning patterns (dash line), where

the raw data is first smoothed with the smooth

degree 10 (sd = 10).

Figure 4: Segmentation for the Cricket time series.

Obviously, the dash lines can significantly

segment the time series, but the two black dash lines

are so close that the segment between them can be

ignored. In view of this, we introduce the segment

threshold ρ that stipulates the minimum segment

length. This parameter can be set as the ratio to the

time series length. Since the time series from a

specific filed exhibit the same fluctuation

characteristics, ρ is data-adaptive and can be learned

from the labeled dataset. Nevertheless, the

segmentation is still primarily established on the

recognition of turning patterns, which determines the

segment number or lengths adaptively, and is

essentially different from the principles of the

existing segmentation methods.

3.2 Chebyshev Factorization

At the beginning, it is necessary to z-normalize the

obtained subsequences as a pre-processing step.

Rather than focusing on the statistical features,

PCHA will factorize each subsequence with the first

kind of Chebyshev polynomials, and take the

Chebyshev coefficients as features. Since the

Chebyshev polynomials with different degrees

represent the fluctuation components, the local

fluctuation information of time series can be

captured in PCHA.

The first kind of Chebyshev polynomials are

derived from the trigonometric identity T

n

(cos(θ)) =

cos(nθ), which can be rewritten as a polynomial of

variable t with degree n, as Formula (1).

−≤−−

≥

−∈

=

−

−

−

1 )),(coshcosh()1(

1 )),(coshcosh(

]1 ,1[ )),(coscos(

)(

1

1

1

ttn

ttn

ttn

tT

n

n

(1)

For the sake of consistent approximation, we

only employ the first sub-expression to factorize the

subsequences, which is defined over the interval [-1,

1]. With the Chebyshev polynomials, a function F(t)

can be factorized as Formula (2).

=

≅

n

i

ii

tTctF

0

)()(

(2)

The approximation is exact if F(t) is a

polynomial with the degree of less than or equal to

n. The coefficients c

i

can be calculated from the

Gauss-Chebyshev Formula (3), where k is 1 for c

0

and 2 for the other c

i

, and t

j

is one of the n roots of

T

n

(t), which can be get from the formula t

j

= cos[(j-

0.5)π/n].

=

=

n

j

jiji

tTtF

n

k

c

1

)()(

(3)

However, the employed Chebyshev polynomials

are defined over the interval [-1, 1]. If the

subsequences are factorized with this "interval

function", they must be scaled into the time interval

[-1, 1]. Besides, the Chebyshev polynomials are

defined everywhere in the interval, but time series is

a discrete function, whose values are defined only at

the sample moments. To compute the Chebyshev

coefficients, we would process each subsequence

with the method proposed in (Cai et al, 2004), which

can extend time series into an interval function.

Given a scaled subsequence S = {(v

1

, t

1

), ..., (v

m

, t

m

)},

ρ

Piecewise Chebyshev Factorization based Nearest Neighbour Classification for Time Series

87

where -1 ≤ t

1

< ... < t

m

≤ 1, we first divide the

interval [-1, 1] into m disjoint subintervals as follows:

=

+

−≤≤

+

=

+

−

=

−

+−

mi

tt

mi

tttt

i

tt

I

mm

iiii

i

],1,

2

[

12),

2

,

2

,

[

1),

2

,1[

1

11

21

Then, the original subsequence can be extended

into a step function as Formula (4), where each

subinterval [t

i

, t

i+1

] is divided by the mid-point

(t

i

+t

i+1

)/2. The first half takes the value v

i

, and the

second half takes v

i+1

.

miItvtF

ii

≤≤∈= 1 , ,)(

(4)

After the above processing, the Chebyshev

coefficients c

i

can be computed. For the sake of

dimension reduction, we only take the first several

coefficients to approximate the raw data, which can

reflect the principal fluctuation components of time

series.

In the entire procedure, the time series needs to

be scanned only once for the adaptive segmentation

and factorization. Thus, the computational

complexity of piecewise factorization is O(kn),

where k is the extracted Chebyshev coefficient

number and much less than the time series length n.

4 SIMILARITY MEASURE

DTW is one of the most prevalent similarity

measures for time series (Serra et al, 2014), which

can find the optimal alignment between time series

by the dynamic programming algorithm. Given a

sample space F, time series T = {t

1

, t

2

, …, t

i

, …, t

m

}

and Q = {q

1

, q

2

, …, q

j

, …, q

n

}, t

i

, q

j

∈ F, a local

distance measure d: (x, y) →

R

+

should be first set in

DTW for measuring two samples. Then, a distance

matrix

C ∈ R

m×n

is computed, where each cell

records the distance between each pair of samples

from T and Q respectively, i.e.,

C(i, j) = d(t

i

, q

j

).

There is an optimal warping path in

C, which has the

minimal sum of the cells.

Definition 4. (Warping Path): Given the distance

matrix

C ∈ R

m×n

, if the sequence p = {c

1

, ..., c

l

, ...,

c

L

}, where c

l

= (a

l

, b

l

)

∈

[1 : n] × [1 : m] for l

∈

[1 :

L], satisfies the conditions that:

i) c

1

= (1, 1) and c

L

= (m, n);

ii) c

l+1

− c

l

∈

{(1, 0), (0, 1), (1, 1)} for l

∈

[1 :

L−1];

iii) a

1

≤ a

2

≤ ... ≤ a

L

and b

1

≤ b

2

≤ ... ≤ b

L

;

Then, p is called warping path. The sum of cells

in p is defined as Formula (5).

)()()(

21 Lp

cccΦ CCC +++=

(5)

Definition 5. (Dynamic Time Warping Distance):

Given the distance matrix

C ∈ R

m×n

over time series

T and Q, and its warping path set

P = {p

1

, …, p

i

, …,

p

x

}, i, x ∈ R

+

, the minimal sum of the cells in the

warping paths Φ

min

= {Φ

ξ

|Φ

ξ

≤ Φ

λ

, ξ, λ ∈ P} is

defined as the DTW distance between T and Q.

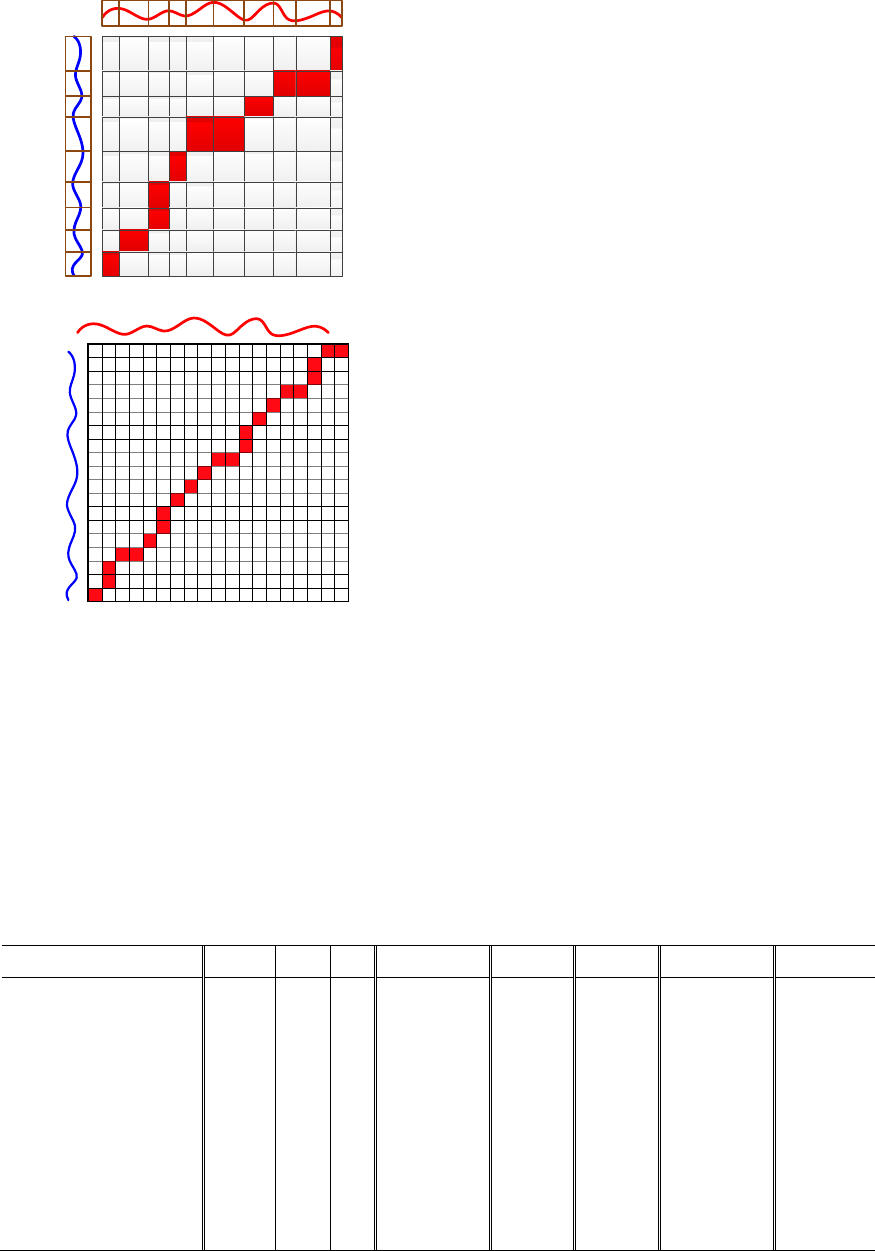

Based on PCHA, we propose a novel PA-DTW

measure, named ChebyDTW. The algorithm of

ChebyDTW contains two layers: subsequence

matching and dynamic programming computation.

Figure 5(a) shows the dynamic programming table

with the optimal-aligned path (red shadow) of

ChebyDTW, against that of the original DTW in

Figure 5(b). In Figure 5(a), each cell of the table

records the subsequence matching result over the

Chebyshev coefficients. By the intuitive comparison,

ChebyDTW would have much lower computational

complexity than the original DTW.

With high computational efficiency, the squared

Euclidean distance is a proper measure for the

subsequence matching. Given d Chebyshev

coefficients are employed in PCHA, for

subsequences S

1

and S

2

, respectively approximated

as

C = [c

1

, ..., c

d

] and Ĉ =[ĉ

1

, ..., ĉ

d

], the squared

Euclidean distance between them can be computed

as Formula (6).

=

−=

d

i

ii

ccD

1

2

)

ˆ

()

ˆ

,( CC

(6)

Over the subsequence matching, the dynamic

programming computation performs. Given that

time series T with length m is segmented into M

subsequences, and time series Q with length n is

segmented into N subsequences, ChebyDTW can be

computed as Formula (7). C

T

and C

Q

are the PCHA

representations of T and Q respectively; C

1

T

and C

1

Q

are the first coefficient vectors of C

T

and C

Q

respectively; rest(C

T

) means the rest coefficient

vectors of C

T

except for C

1

T

; the same meaning is

taken for rest(C

Q

).

+

==∞

==

=

otherwise

restrestChebyDTW

restChebyDTW

restChebyDTW

CCD

nm

nm

Q

T

ChebyDT

W

QT

QT

QT

QT

,

)](),([

)],(,[

],),([

min),(

0or 0 if ,

0 if ,0

),(

11

CC

CC

CC

(7)

KDIR 2015 - 7th International Conference on Knowledge Discovery and Information Retrieval

88

(a)

(b)

Figure 5: (a) The dynamic programming table with the

optimal-aligned path (red shadow) of ChebyDTW, (b)

against that of the original DTW.

5 EXPERIMENTS

We evaluate the 1NN classifier based on

ChebyDTW from the aspects of accuracy and

efficiency respectively. 12 real-world datasets

provided by the UCR time series archive (Keogh et

al, 2011) are employed, as shown in Table 1, which

come from various application domains and are

characterized by different series profiles and

dimensionality. All datasets have been z-normalized

and partitioned into training and testing sets by the

provider. Besides, we take the 1NN classifiers

respectively based on four prevalent PA-DTWs as

baselines, i.e., PDTW, SDTW, APCADTW, and

DSADTW. All parameters in the measures are

learned on the training datasets by the DIRECT

global optimization algorithm (Björkman et al,

1999), which is used to seek for the global minimum

of multivariate function within a constraint domain.

The experiment environment is Intel(R) Core(TM)

i5-2400 CPU @ 3.10GHz; 8G Memory; Windows 7

64-bit OS; MATLAB 8.0_R2012b.

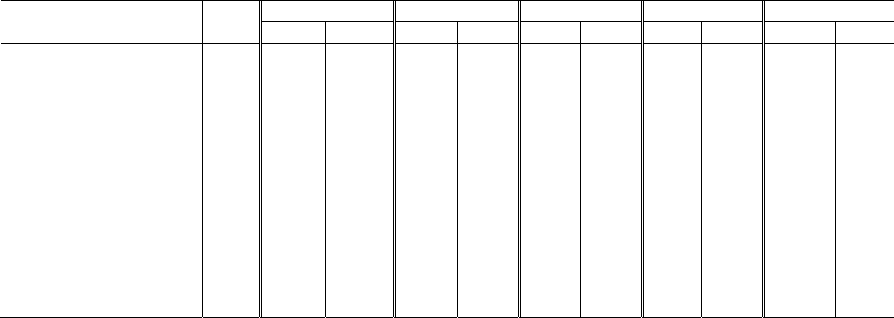

5.1 Accuracy

Table 1 shows the 1NN classification accuracy (acc.)

based on the above PA-DTWs. The best result on

each dataset is highlighted in bold. The learned

parameters are also presented, which could make

each classifier achieve the highest accuracy on each

training dataset, including the segment threshold (ρ),

the smooth degree (sd), and the extracted Chebyshev

coefficient number (θ). For the sake of

dimensionality reduction, we learn the parameter θ

in the range of [1, 10] for ChebyDTW.

It is clear that, the 1NN classifier based on

ChebyDTW wins all datasets and has the highest

accuracy. Its superiority mainly derives from the

distinctive features extracted in ChebyDTW, which

can capture the fluctuation information for similarity

measure. Whereas the statistical features extracted in

the baselines only focus on the aggregation

characteristics of time series, which would result in

much fluctuation information loss.

Table 1: 1NN classification accuracy results based on five PA-DTWs.

Dataset

ρ sd θ

ChebyDTW PDTW SDTW APCADTW DSADTW

Adiac 0.21 22 9

0.72

0.61 0.34 0.28 0.38

Beef 0.18 17 5

0.57

0.50 0.57 0.57 0.47

CBF 0.98 8 10

0.98 0.98

0.95 0.91 0.50

ChlorineConcentration 0.73 25 8

0.65

0.60 0.55 0.56 0.62

CinC_ECG_torso 0.29 4 9

0.81

0.65 0.63 0.61 0.63

Coffee 0.51 14 9

0.89

0.79 0.75 0.82 0.61

ECG200 0.80 7 9

0.89

0.80 0.83 0.77 0.81

ECGFiveDays 0.73 17 9

0.91

0.79 0.68 0.68 0.57

FaceAll 0.51 29 10

0.73

0.63 0.50 0.63 0.71

FacesUCR 0.51 4 6

0.80

0.60 0.57 0.72 0.70

ItalyPowerDemand 0.51 7 5

0.94

0.93 0.80 0.90 0.87

SonyAIBORobotSurface 0.95 25 6

0.80

0.76 0.73 0.76 0.70

Piecewise Chebyshev Factorization based Nearest Neighbour Classification for Time Series

89

Table 2: The DCR results of five PA-DTWs.

Dataset

n

ChebyDTW PDTW SDTW APCADTW DSADTW

w DCR w DCR w DCR w DCR w DCR

Adiac 176 3.99

44.13

36 4.89 13 13.54 43 4.10 70.00 2.51

Beef 470 5.18

90.68

61 7.70 10 47.00 61 7.70 192.32 2.44

CBF 128 1.00

128.0

30 4.27 27 4.74 15 8.53 46.19 2.77

ChlorineConcentration 166 2.00

83.00

36 4.61 29 5.72 34 4.88 64.77 2.56

CinC_ECG_torso 1639 4.00

409.9

103 15.91 94 17.44 84 19.51 655.49 2.50

Coffee 286 2.00

143.0

60 4.77 33 8.67 40 7.15 117.34 2.44

ECG200 96 1.93

49.74

14 6.86 19 5.05 23 4.17 35.84 2.68

ECGFiveDays 136 1.61

84.43

9 15.11 9 15.11 5 27.20 48.24 2.82

FaceAll 131 2.00

65.50

32 4.09 32 4.09 32 4.09 53.96 2.43

FacesUCR 131 2.00

65.50

24 5.46 32 4.09 31 4.23 54.43 2.41

ItalyPowerDemand 24 1.98

12.13

5 4.80 6 4.00 6 4.00 10.61 2.26

SonyAIBORobotSurface 70 1.00

70.00

13 5.38 9 7.78 8 8.75 27.41 2.55

5.2 Efficiency

Since the efficiency of 1NN classifier is determined

by the used similarity measure, we perform the

efficiency evaluation by comparing the

computational efficiency of ChebyDTW against the

baseline PA-DTWs. The speedup of computational

complexity gained by PA-DTW over the original

DTW is O(n

2

/w

2

), where n is the time series length,

and w is the segment number. It is positively

correlated with the data compression rate (DCR =

n/w) of piecewise approximation over the raw data.

In Table 2, we present the DCRs of five PA-DTWs

on all datasets, as well as n and w. Since

ChebyDTW and DSADTW both employ the

adaptive segmentation method, the average segment

numbers on each dataset are computed for them.

As shown by the results, the DCRs of

ChebyDTW are not only much larger than the

baselines on all datasets, but also robust to the time

series length. Thus, it has the highest computational

efficiency among the five PA-DTWs. The efficiency

superiority of ChebyDTW mainly derives from the

precise approximation of PCHA over the raw data,

and the data-adaptive segmentation method, which

can segment time series into the less number of

subsequences with the adaptive lengths.

6 CONCLUSIONS

We proposed a novel piecewise factorization model

for time series, i.e., PCHA, where a novel adaptive

segmentation method was proposed, and the

subsequences were factorized with the Chebyshev

polynomials. We employed the Chebyshev

coefficients as features for PA-DTW measure, and

thus proposed the ChebyDTW for 1NN

classification. The comprehensive experimental

results show that ChebyDTW can support the

accurate and fast 1NN classification.

ACKNOWLEDGEMENTS

This work was funded by the Ministry of Industry

and Information Technology of China (No.

2010ZX01042-002-003-001), China Knowledge

Centre for Engineering Sciences and Technology

(No. CKCEST-2014-1-5), and National Natural

Science Foundation of China (No. 61332017).

REFERENCES

Esling P., Agon C., 2012. Time-series data mining. ACM

Computer Survey, 45(1).

Fu T., 2011. A review on time series data mining.

Engineering Applacations of Artificial Intelligence,

24(1): 164-181.

Ding H., Trajcevski G., Scheuermann P., Wang X., Keogh

E., 2008. Querying and mining of time series data:

experimental comparison of representations and

distance measures. In Proceedings of the VLDB

Endowment, New Zealand, pp. 1542-1552.

Hills J., Lines J., Baranauskas E., Mapp J., Bagnall A.,

2014. Classification of time series by shapelet

transformation. Data Mining and Knowledge

Discovery, 28(4): 851-881.

Serra J., Arcos J L., 2014. An empirical evaluation of

similarity measures for time series classification.

Knowledge-Based System, 67: 305-314.

Keogh E., Chakrabarti K., Pazzani M., Mehrotra S., 2001.

Dimensionality reduction for fast similarity search in

large time series databases. Knowledge Information

System, 3(3): 263-286.

KDIR 2015 - 7th International Conference on Knowledge Discovery and Information Retrieval

90

Keogh E., Chu S., Hart D., Pazzani M., 2004. Segmenting

time series: A survey and novel approach. Data

Mining in Time Series Databases. London: World

Scientific.

Chakrabarti K., Keogh E., Mehrotra S., Pazzani M., 2002.

Locally adaptive dimensionality reduction for

indexing large time series databases. ACM

Transactions on Database System, 27(2): 188-228.

Gullo F., Ponti G., Tagarelli A., Greco S., 2009. A time

series representation model for accurate and fast

similarity detection. Pattern Recognition, 42(11):

2998-3014.

Li H., Guo C., 2011. Piecewise cloud approximation for

time series mining. Knowledge-Based System, 24(4):

492-500.

Ullman S., Poggio T., 1982. Vision: A computational

investagation into the human representation and

processing of visual information, MIT Press.

Gao J., Sultan H., Hu J., Tung W., 2010. Denoising

nonlinear time series by adaptive filtering and wavelet

shrinkage: a comparison. IEEE Signal Processing

Letters, 17(3): 237-240.

Keogh E., Zhu Q., Hu B., Hao. Y., Xi X., Wei L.,

Ratanamahatana C. A., 2011. UCR time series

classification/clustering homepage:

www.cs.ucr.edu/~eamonn/time_series_data/.

Cai Y., Ng R., 2004. Indexing spatio-temporal trajectories

with Chebyshev polynomials. In Proceedings of the

2004 ACM SIGMOD international conference on

Management of data, France, pp. 599-610.

Björkman M., Holmström K., 1999. Global optimization

using the DIRECT algorithm in matlab. Advanced

Model. Optimization, 1(2): 17-37.

Keogh E., Pazzani M. J., 1999. Relevance feedback

retrieval of time series data. In Proceedings of the

22nd annual international ACM SIGIR conference on

Research and development in information retrieval,

USA, pp. 183-190.

Lin J., Vlachos M., Keogh E., 2005. A MPAA-based

iterative clustering algorithm augmented by nearest

neighbors search for time-series data streams.

Advances in Knowledge Discovery and Data Mining.

Springer Berlin Heidelberg.

Rakthanmanon T., Campana B., Mueen A., 2012.

Searching and mining trillions of time series

subsequences under dynamic time warping. In

Proceedings of the 18th ACM SIGKDD International

Conference on Knowledge Discovery and Data

Mining, China, pp. 262-270.

Keogh E. J., Pazzani M. J., 2000. Scaling up dynamic time

warping for data mining applications. In Proceedings

of the 6th ACM SIGKDD International Conference on

Knowledge Discovery and Data Mining, USA, pp.

285-289.

Keogh E. J., Pazzani M. J., 1999. Scaling up dynamic time

warping to massive datasets. Principles of Data

Mining and Knowledge Discovery. Springer Berlin

Heidelberg.

Piecewise Chebyshev Factorization based Nearest Neighbour Classification for Time Series

91