Knowledge-based Design Cost Estimation Through Extending

Industry Foundation Classes

Shen Xu

1

, Kecheng Liu

2

and Weizi Li

1

1

Business Informatics, Systems & Accounting, Henley Business School, University of Reading,

Whiteknights Campus, Reading, U.K.

2

School of Information Management and Engineering, Shanghai University of Finance and Economics, Shanghai, China

Keywords: Design Cost Estimation, Knowledge Representation, Information System Development, Industry

Foundation Classes.

Abstract: In order to overcome divergence of estimation with the same data, the proposed costing process adopts an

integrated design of information system to design the process knowledge and costing system together. By

employing and extending a widely used international standard, industry foundation classes, the system can

provide an integrated process which can harvest information and knowledge of current quantity surveying

practice of costing method and data. Knowledge of quantification is encoded from literatures, motivation

case and standards. It can reduce the time consumption of current manual practice. The further development

will represent the pricing process in a different type of knowledge representation. The hybrid types of

knowledge representation can produce a reliable estimation for construction project. In a practical term, the

knowledge management of quantity surveying can improve the system of construction estimation. The

theoretical significance of this study lies in the fact that its content and conclusion make it possible to

develop an automatic estimation system based on hybrid knowledge representation approach.

1 INTRODUCTION

Researchers and professionals have continued to

address the importance of cost estimation to

construction industry. Accurate cost estimation is a

core foundation to construction project

successfulness. Moreover the most widely used

design costing model is quantity-based cost

estimation model (Akintoye and Fitzgerald, 2000).

The quantity-based relationships between product

and cost information are helpful in assisting quantity

surveyors with the creation of estimates.

Quantity surveying is a knowledge-based,

dynamic and collaborative process and evolves with

variance and up-to-date evidence. With the

development of information technology, many

activities of quantity surveying such as cost

itemization, quantification, and pricing are being

supported by computer aided design system,

quantity taking off system, and spread sheet which

have already being integrated into core business of

quantity surveying company. If the knowledge

accumulated in these systems can be shared,

communicated and integrated together during the

execution of cost estimation, the costing practice can

be well monitored.

However, the quantity surveying knowledge has

not been integrated into the process of cost

estimation; the knowledge in the current system has

not been represented neither. Even though there are

various applications to support quantity surveying

practice, for example CostX, and Nomitech (Exactal,

2013; Nomitech, 2013). They can only support

certain part of cost estimation instead of the whole

process. Consequently in order to keep the accuracy

of cost estimation, many of these efforts require

substantial manual input including remodelling the

product model into process model which is time

consuming, error prone and tedious task, and the

user acceptance of such application is low (Forgues

and Iordanova, 2012; Tanyer and Aouad, 2005).

Recently with the emergence of industry foundation

classes (IFC) in architectural, engineering, and

construction (AEC) industries opportunities exist for

improving costing processes. However, both of our

case study and one quantitative study of BIM’s

impact on detailed cost estimation reveals that the

impact on costing practice of IFC is still remaining

161

Xu S., Liu K. and Li W..

Knowledge-based Design Cost Estimation Through Extending Industry Foundation Classes.

DOI: 10.5220/0004866401610168

In Proceedings of the 16th International Conference on Enterprise Information Systems (ICEIS-2014), pages 161-168

ISBN: 978-989-758-028-4

Copyright

c

2014 SCITEPRESS (Science and Technology Publications, Lda.)

on the junior level of quantity surveyor which his

major task is calculating product based quantities of

a construction project (Shen and Issa, 2010; Xu and

Tang, 2011).

In order to meet this challenge this paper

proposes a knowledge extension on IFC. We attempt

to extend IFC with the built-in knowledge by

analysing sources of quantity surveying knowledge

for where we consider (1) construction classification

system (2) standard documents (3) published

literatures (4) tacit knowledge of domain experts (5)

cost data in current database application. It is

expected to make use of quantity surveying

knowledge to support and optimize costing process

by delivering accurate quantity and reliable price of

cost items. Firstly, we examine current detailed cost

estimation process and specify the knowledge spaces

along the process. After that we elaborate the

knowledge within the IFC environment to provide

the capability for decision support to costing

process. It provides the foundation of the

development of detailed cost estimation system. By

combining the built-in intelligence of IFC with

above mentioned research efforts we can further

improve the automation of cost estimation. Finally

we illustrate the application of knowledge-based IFC

to derive cost estimation on a construction product

as a motivation case.

2 PROCESS OF CONSTRUCTION

COST ESTIMATION

The detailed cost estimation models the distributions

of each cost element in a building via bill of

quantities. In order to demonstrate the process of

cost estimation at LOD 300, direct observation has

been conducted. Study shows that in a detailed

construction cost estimation process, cost

itemization is the first step of cost estimation. It is

the process of decomposing and re-categorizing

building components based on cost break-down

structure and standard method of measurement

(Dell’Isola, 2003; Hietanen, 2000; Royal Institution

of Chartered Surveyors, 2011). Measurement

standards have been published to help quantity

surveyor to decomposing building components,

however an empirical study indicates that quantity

surveyor will select the most possible working

method based on their experience (Tan and

Makwasha, 2010).

The most common complaint from professional

quantity survey or about quantity surveying in

Table 1: The difficulties of applying resource based

costing model.

Problems Difficulties

Inadequate

Interoperability

Lack of understanding of

construction process (Bowen

and Edwards, 1985; Skitmore

and Patchell, 1990);

No available data (Ashworth,

2004; Fortune and Lees, 1996);

Traditional fragmentation of

the design and construction

functions (Love et al., 1998).

Unregulated

Assumptions

Additional assumptions

(Skitmore and Marston, 1999);

Lack of understanding of

resource based cost model

(Fortune and Lees, 1996);

Different data requirements

(Kim et al., 2004).

Others

Time constraints (Akintoye and

Fitzgerald, 2000).

costing practice was that they are so busy dealing

with assumptions that has no time to monitor their

process. In order to reveal assumptions made in the

detailed cost estimation from professional quantity

surveyor, we further investigated the documents

provided by professional quantity surveyor.

Focusing on LOD 300 phase, by given specific

assembles, cost estimation is predicting the

construction works at LOD 400 phase and LOD 500

(Xu and Tang, 2011). As a result there are large

numbers of assumptions that need to be made during

this stage and it is time consuming and error prone

process, refer to table 1 the difficulties of doing cost

estimation.

In our study, we divide the transcript process into

three steps, which are cost itemization,

quantification and pricing. These three steps should

be discussed separately because of the different type

of knowledge. Institutions like Royal Institution of

Chartered Surveyors and American Institute of

Architects defines how quantity surveyor should

estimate the quantities of buildings (Royal

Institution of Chartered Surveyors, 2011).

In order to fully understand the quantity

surveying practice in detailed cost estimation based

on existing system, an analysis of cost items is

required. In the case study there are 108 cost items

for each building, and the whole project have 14

buildings. We listed three common cost items to

demonstrate the classifiers we have acquired, see

table 2. For example MU10 standard brick is product,

masonry with M10 cement mortar is working

method.

Therefore, there are four classifiers need to be

ICEIS2014-16thInternationalConferenceonEnterpriseInformationSystems

162

Table 2: Examples of cost items in case study.

N

U

M

Se

cti

on

Cost items Classifiers

1

Masonry

External Wall, MU10

standard brick,

masonry with M10

cement mortar

[Building

component]+[Const

ruction Product]

+[Working method]

240mm thickness,

below elevation ±1.1

[Product’s property:

thickness],

[Applied Location]

2

Finishes

‘911’ Waterproof

non-tar polyurethane

coating

[Construction

Product]

1.2mm thickness,

applied at bathroom

floor

[Product’s property:

thickness],

[Applied Location]

3

Finishes

1:3 cement mortar,

trowel compaction

[Construction

Product] +[Working

method]

20mm thickness,

applied at floor

[Product’s property:

thickness],

[Applied Location]

identified, i.e. building component, construction

product, product property, and location. In practise,

cost estimator have two options that could complete

the working method attach to construction product.

Firstly cost estimator would like to form up certain

working method based on their experience, design

specification and discussion with design team.

Secondly cost estimator would refer to cost data

base to check available of existing working methods

and select the most possible one based on their

experience. Commercially available of cost database

facilitate the second approach of forming up cost

items, e.g. R.S. Means, and Building Cost

Information Service (BCIS).

3 KNOWLEDGE IN DESIGN

COSTING

The process-related knowledge which means the

type of knowledge is used by quantity surveyors

when an estimation process is being executed

(Seethamraju and Marjanovic, 2009). Furthermore

we classified knowledge into two further subtypes:

concepts and rules that support process-related

activities efficiently through the creation of cost

estimation. The concepts describe all the building

components and concepts related to construction

cost estimation in order to form the basis of cost

estimation, there are more than 6000 concepts (El-

Diraby et al., 2005). Therefore we are not including

all the concepts but mainly provide the categories

along the costing process, please see table 3.

The rules further specified the details of the

activities such as when and how certain calculation

must be executed.

After cost itemization, we have differentiated

construction product with cost item, for each cost

item, standard method of measurement specified the

corresponding rules respectively, including the unit

and the deduction rules. Table 4 shows the rules in

the standards in order to get the actual quantity of a

construction product. Particularly the knowledge of

quantity calculation designs a control structure that

triggers the calculation operation when the

conditions become true.

Table 3: Description of Concept-based Knowledge.

Targeted

Process

Concepts

Category

Description

The whole

construction

process

Building

components

classification

system

The classification system involves all construction concepts, including

different application domains. For example OmniClasses, MasterFormat, and

ISO 14177.

Cost

Itemization

Working

breakdown

structure

This document provides the template of breaking down a construction project

in a hierarchy structure and is well documented by professional intuitions,

e.g. RICS, AACE. It has three typical structures depend on the division of

component and has 61 sections. For example New Rules of Measurements

(Royal Institution of Chartered Surveyors, 2011).

Quantification Construction

products

relationships

Construction products are derived from building components, thus their

quantities are related but may not same. For example IFC modelled wall and

it’s related finishes (buildingSMART International Limited, 2013)

Pricing Cost item

database

The database records common construction product and its labour cost and

material cost. The data descript productivity and labour sources. A typical

commercialized database is being developed by R.S. Mean Company.

Knowledge-basedDesignCostEstimationThroughExtendingIndustryFoundationClasses

163

Table 4: Description of Rule-based Knowledge.

Targeted

Process

Category of

rules

Description

Quantification Deduction

rules

Depicting different situation that applying different deduction rules. For

example Damp-proof courses less than 300mm wide should be measured

in length, and Damp-proof courses more than 300mm wide should be

measured in square meter etc. In production rules, it can be translated as if

the damp-proof is wider that 300mm, then measure it in square meter.

Regarding pricing stage, practitioners support

subjective probability distributions, firstly due to the

fact that in the construction industry relevant data

seem to be lacking or is not organized in a way that

allows it to be used for analysis. Secondly, as

Flanagan & Norman (1983) highlighted, cost

management in construction seems to be based on

feel and experience therefore modelling should

incorporate some form of expert judgement.

Expert judgement has to be exercised on the

relevance of the inputs or data to be used for

estimation of project costs. It seems though that in

practise there is no consensus on the degree to which

subjective is applied as some practitioners also

decide on the correlation between cost items or

elements based on personal experience and

judgement rather than historical data.

4 KNOWLEDGE-BASED

EXTENSION TO IFC

Industry Foundation Class (IFC), was developed by

buildingSMART and is a common data ‘schema’

intended for holding interdisciplinary information

for building lifecycle in a building information

model, and exchanging it among software

applications used in AEC (BuildingSMART UK,

2010). A schema, often called ‘Product (Data)

Model’, is captured in IFC specification, and

composed of (1) entities, (2) attributes, and (3)

relationships between entities. Schema defines the

way by which the population of these entities and

relationships needs to be represented.

The ultimate goal is to determine the cost of

construction project from design results by using

IFC. As a first step, a formal description of the IFC

data model and related building information data

models (such as material databases) such that they

can be used by a formal rule language need to be

established (Staub et al., 2003). This kind of

knowledge representation can be derived from

quantity surveyor’s rationale and the same research

efforts are leading by (Staub and Nepal, 2007). Thus

based on this ontology language and decomposing

mechanism a further development can be carried out

(Xu et al., 2013).

We employ hybrid knowledge management

techniques, which are solver and rule (Holsapple and

Whinston, 1996). In our study the solver is an

executable algorithm that can solve one particular

class of problem and rule is the underpinning

reasoning knowledge. Particularly in this paper we

are focusing on rules.

The process of IFC based cost estimation

presents an automatic decomposing building element

into construction products, semi-automatic

classifying construction products into cost items,

automatically taking off quantities for cost items,

and pricing each cost items (Xu et al., 2013). The

extension to IFC is the rule-based knowledge, and

attempts to integrate the knowledge into IFC in

order to automate the described cost estimation

process.

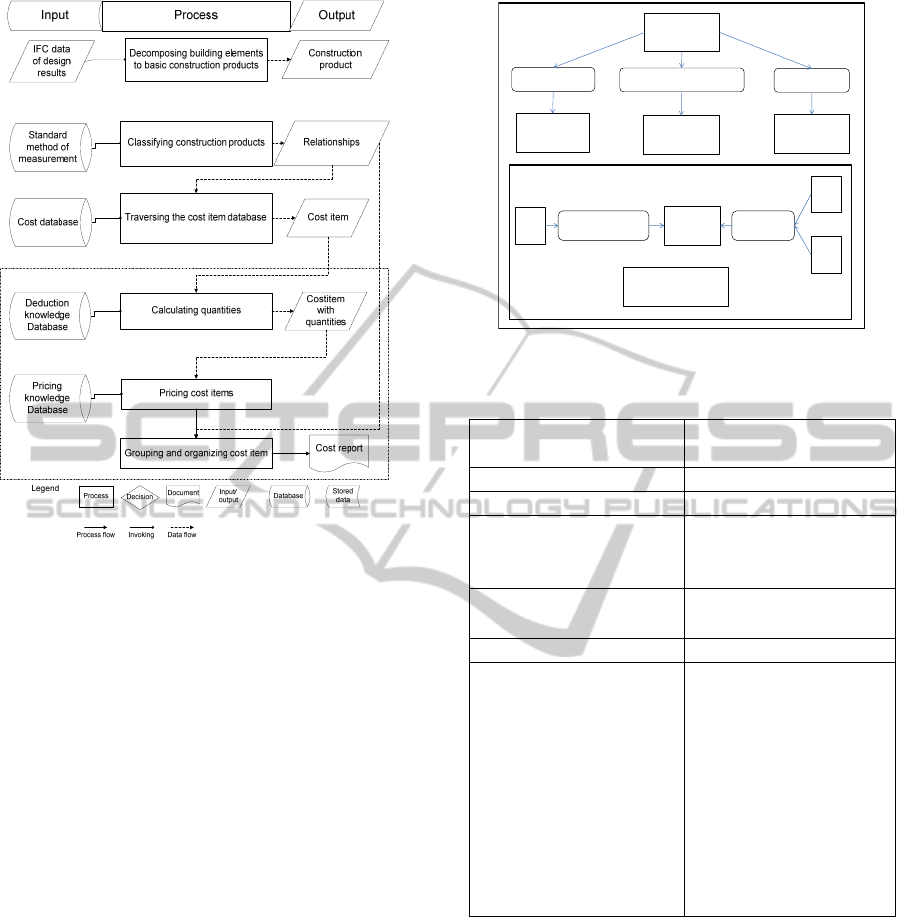

In order to illustrate our knowledge extension to

IFC, it is essential for us to present the process of

cost estimation process in IFC, see figure 1. It is not

the main focus of this paper, but briefly the

application harvests information from BIM objects

in various manners – either enhancing object

definitions within the model, using a classification

system to link objects to more detailed information

stored externally from the BIM application in a

database. The design of this particular costing

application split the databases into design results

database (specified in IFC), cost value database

(realized in R.S. Means cost information company),

and cost knowledge database (proposed cost

knowledge base) rather than traditional cost database

that records company’s core competence in the form

of cost items’ value and leave the cost knowledge to

individual quantity surveyors. On the other hand,

IFC data modelling is based on EXPRESS data

modelling language is that combines ideas from the

entity-attribute-relationship family of modelling

languages with object modelling ideas of the late

1980s. Wermelinger and Bejan (1993) describe a

mapping of EXPRESS into conceptual graphs (CGs).

Thus our first step is translating the domain rules

ICEIS2014-16thInternationalConferenceonEnterpriseInformationSystems

164

Figure 1: Cost estimation process in IFC.

into CGs which can be evaluated by domain experts.

This kind of rule can be expressed by

corresponding entities in IFC. Building Element is

expressed by IfcBuildingElement and with subtype

of IfcWall, IfcColumn, IfcSlab etc; HasCovering

relationship is defined by

IfcRelCoversBldgElements; Finishes is defined by

IfcCovering; ElementQuantity is expressed by

IfcElementQuantity; HasVoids is expressed by

IfcOpeningElement and subtype of IfcWindow and

IfcDoor; HasVoids area is expressed by

IfcElementQuantity assigned to IfcOpeningElement;

Subtraction calculation is expressed by

IfcFeatureElementSubtraction.

RICS defines that no deduction is made for voids

not exceeding 1.00m2; Boundary work to voids is

only measured where the void exceeds 1.00m2, and

is measured by length (Royal Institution of

Chartered Surveyors, 2011, p. 152). The translation

of the domain rule is straightforward after identified

static knowledge of construction. Take a piece of

‘knowledge’ as follows:

QS measures the quantities of finishes in area

and created boundary works.

The IFC model defines a flexible and powerful

mechanism that allows extensions to the model

through the use of the IfcPropertySet entity. An IFC

property set could be used to define a set of

Figure 2: A Conceptual Graph of Quantity surveying rule.

Table 5: A decent representation.

measuring(e) e is a measuring

‘event’

agent(e, QS) QS was the measurer

unit(e, area) measured unit was area

∃b,

buildingelementb ∧

finishes(f, b)

Building element b has

finishes f

∃f, finishes(f) ∧

object(e, f)

A covering f is the

object of measuring

voids(e, w) measured voids was w

∀e,f,w,area

measuring(e)∧ unit(e,

area) ∧object(e, f) ∧

voids(e, w>1) →

quantity(e, b-w) ∧

creates(boundaryworks)

If a building element x

has covering a, has

an element quantity

of area b, has a void

area larger than 1m

2

,

then the actual

quantity of covering

a is the subtraction

of b and w and

create new cost item

boundary work

properties (IfcProperty entities or other nested

IfcPropertySet entities), and can be linked to any

number of IFC objects using the

IfcRelAssignsProperties entity. Using this approach,

we could, for example, define a property set that

describes the specifications of a building element

and link this set to the IfcProduct entity that

represents a specific building element using an

IfcRelAssignsProperties entity (Halfawy and Froese,

2002).

Thus we can apply deduction rules using similar

approach. A new IfcEstimationDef entity could be

created as a container for object-related rules

and procedures, both of which are supported by

BuildingEle

ment:*x

Finishes:*a

Area:*b

Area:

*w>1m2

If:

Then:

HasCovering

ElementQuantity

HasVoids

?a ActualQuantity Quantity SubQuant

?b

?w

Create Boundary

Works

Knowledge-basedDesignCostEstimationThroughExtendingIndustryFoundationClasses

165

Table 6: Components of Rule-based Knowledge.

Design model and

corresponding construction

products

Situation Corresponding

deduction rule

Quantity takeoff result

Ceramic wall

tile,

33cm*33cm*

0.8cm

3.5m*5m wall area is covered by tile;

The tile size is 0.33m*0.33m (Tile is

traded by piece and need to be cut in

order to cover the boundary of the

applied locations)

The wall area is 17.5 m

2

and with

opening voids of 1.3*2.4=3.21 m

2

Wall area –

Opening area

Plus, create new

cost item: Boundary

work of window

edge

Net girth of window

A= 17.5-3.21=14.29m

2

B=(1.3+2.4)*2=7.4m

the EXPRESS language. The linkage between

IfcEstimationDef entity and any number of IFC

entity can be realized by using the defined

relationship entity called IfcRelAssignsEstimation.

Unstructured knowledge, in the form of documents,

can be defined using properties in a property set

linked to the object.

In a typical IfcEstimationDef entity, rules may

refer to the attributes of same object or other object.

To execute these rules, IFC application would need

to implement or to interface with a rule-based engine,

and the engine should be examined in a further

research. Also, the procedures are defined by their

interface and could be implemented using standard

component interfaces. Objects would need to access

these components to execute these procedures. For

example, an “CalculateBoundaryWorksQuantity”

procedure may be implemented in a standard

interface, to compute and create the boundary works.

Other procedures could be implemented to check

some object values or to retrieve some data (e.g.

form an online product repository).

5 APPLICATION OF

KNOWLEDGE-BASED IFC

We are using life example to demonstrate the

process of cost estimation. We take a building

element ‘wall’ as an example. The products and its

relationship with building element are created in IFC

after this step. The relationship would be stored for

further use and construction products need to be

carried to next process. Furthermore, Ma et al. (2013)

indicate that fully automatic of decomposing process

can be accomplished in IFC.

The information available in this case indicates

the wall area has finishes of tile, which has property

of 33cm*33cm*0.8cm, using adhesive set; the wall’s

area is 17.5m

2

, has opening window of 1.3m*2.4m

The actual quantity of finishes: tile should be

14.9 m

2

with 7.4 m boundary work. Refer to table 6

Components of Rule-based Knowledge. Based on

the knowledge we specified in previous section, we

can identify that there are two cost items. They are

the tiles and boundary works, which the quantities

are showing in the table.

There is, however as discussed previous, a

danger of applying published data or software

database pricing without first adjusting for the

particular aspects of the project currently under

consideration. In construction every project is

unique, with a distinct set of local factors (such as

size of project, desirability, level of competition,

flexibility of specifications, work site conditions,

hour restrictions etc.) that come into play in current

project. Previously, when an estimating system is

used that is attached to a price database, the

professional estimator would still have reviewed

each line of the item price to determine if it is

applicable to the project being estimated, as pricing

and estimation is captured within one entity.

In order to demonstrate the process of selection

of working methods and pricing process, the cost

database has been examined as well as the price

analysis process. There are approximately 1000

items in each cost breakdown sections, we only

illustrate the finishes and tile section and focusing

on the flooring tile. We execute 54 cost items in

ceramic tile in R.S. Means construction cost

database. And manually decomposing the cost items

based on our classification conditions and has been

reorganized respectively, e.g. product types, product

property, applied area, geometric shape, and

working methods. Based on the example we

provided, cost item: Ceramic flooring tile,

33cm*33cm*0.8cm, applied in external wall, thus

we can list three possible cost item records which

represents three different working methods.

The daily output or productivity recorded in

commercial database is based on several factors: R.S.

Means’ engineer's experience, trade labour

productivity publications, contractors’ input, and in

ICEIS2014-16thInternationalConferenceonEnterpriseInformationSystems

166

Table 7: Reorganized Cost Database.

some cases actual time and motion study observation.

Labour hours calculated by dividing the crew labour

hours worked in a day by the daily output. Note:

Multiply labour hours by 60 to convert to hours and

minutes. Crews have already been determined for

each cost item, detailed crews information can refer

to R.S. Means cost database reference: Crew

standard Union

Based on traversing the cost database, we

acquired three possible working methods in adhesive

set, due to no further information revealed;

professional quantity surveyor will assume the

uniform distribution of such method. Thus it is

common that professional will take the average of

possible methods that can represent the most

possible unit price and productivity. Thus this

process will be the further investigation in our

research.

6 DISCUSSION AND FUTURE

WORKS

Ma et al., (2013) demonstrate the costing process for

building structure in IFC, based on their

decomposing process that we can further extend IFC

into finishes of building by incorporating surveying

knowledge and pricing knowledge. Meanwhile there

is little research on quantity surveying knowledge

(Senaratne and Sabesan, 2010). Hence without

incorporate the knowledge into the process it is

difficult for applications to deliver a completed

costing report. Thus this gap highlights the

contribution of our research.

In practical term, knowledge management of

quantity surveying can improve the system of

construction estimation. The theoretical significance

of this study lies in the fact that its content and

conclusion make it possible to develop an automatic

estimation system. Furthermore the combination of

knowledge representation and automatic system

development can establish a sustainable

development loop of construction cost estimation

digitalization.

This paper provides the initial result from the

motivation case of a knowledge based approach and

more evidences are required to further evaluate this

work, for instance a real case study with empirical

results and prototype of the system. Meanwhile, the

reasoning process, inference engine and system

architecture will be further investigated in order to

reveal the pricing stage of quantity surveying.

Furthermore certain conclusion can be made is

that a hybrid knowledge representation of quantity

surveying is essential to develop an estimation

system. As delivering a reliable estimation of

construction project, two steps are essential.

Quantification step is incorporated with rule-based

knowledge representation. And pricing step is

incorporated with other knowledge representation

type. Thus a hybrid knowledge representation can

enable the development of an automatic estimation

system via quantity surveying approach in future.

REFERENCES

Akintoye, A., Fitzgerald, E., 2000. A survey of current

cost estimating practices in the UK. Constr. Manag.

Econ. 18, 161–172.

Ashworth, A., 2004. Cost studies of buildings.

Construction

product

Applie d

area

Product

prope rty

Crew

Daily

Output

Labour

Hours

Unit Mate rial Labour Total

Ceramic tile

External

Wall

33cm x

33cm

tiles

adhesive

set

using

0.8cm

high

piece

D7 8.93 1.8 m2 $45.45 $64.8 $110.25

Ceramic tile

External

Wall

33cm x

33cm

tiles

adhesive

set

D7 13.94 1.17 m2 $42.58 $42.12 $84.7

Ceramic tile

External

Wall

33cm x

33cm

tiles

adhesive

set

with

140.25c

m x

140.25c

m tile

wainscot

D7 5.7 2.81 m2 $77.78 $101.16 $178.94

Working method

Knowledge-basedDesignCostEstimationThroughExtendingIndustryFoundationClasses

167

Bowen, P.A., Edwards, 1985. Cost modelling and price

forecasting: practice and theory in perspective. Constr.

Manag. Econ. 3, 199–215.

buildingSMART International Limited, 2013. IFC

Standard (WWW Document). URL about:blank

(accessed 3.31.13).

BuildingSMART UK, 2010. Investing in BIM competence

BuildingSMART: a guide to collaborative working for

project owners and building professionals, Endeavour.

UK.

Dell’Isola, M. D., 2003. Detailed Cost Estimating. Excerpt

from Archit. Handb. Prof. Pract. 1–13.

El-Diraby, T., Lima, C., Feis, B., 2005. Domain taxonomy

for construction concepts: toward a formal ontology

for construction knowledge. J. Comput. Civ. … 394–

406.

Exactal, 2013. CostX® | Exactal CostX : Construction

Estimating Software | On-screen Takeoff Software

(WWW Document). URL http://www.exactal.co.uk/

products/costX (accessed 11.4.13).

Flanagan, R., Norman, G., 1983. The accuracy and

monitoring of quantity surveyors’ price forecasting for

building work. Constr. Manag. Econ. 1, 157–180.

Forgues, D., Iordanova, I., 2012. Rethinking the Cost

Estimating Process through 5D BIM: A Case Study. …

Res. Congr. 2012 … 778–786.

Fortune, C., Lees, M., 1996. The relative performance of

new and traditional cost models in strategic advice for

clients. RICS Res. Pap. Ser. 2.

Halfawy, M., Froese, T., 2002. Modeling and

implementation of smart AEC objects: an IFC

perspective. In: CIB W78 2002 Conference, Aarhus,

Denmark. pp. 12–14.

Hietanen, J., 2000. Quantity Takeoff using IFC R2 . 0.

Holsapple, C., Whinston, A., 1996. Decision Support

Systems: A Knowledge-Based Approach. Course

Technologies, Cambridge, MA.

Kim, G.-H., An, S.-H., Kang, K.-I., 2004. Comparison of

construction cost estimating models based on

regression analysis, neural networks, and case-based

reasoning. Build. Environ. 39, 1235–1242.

Love, P.E.D., Gunasekaran, A., Li, H., 1998. Concurrent

engineering: a strategy for procuring construction

projects. Int. J. Proj. Manag. 16, 375–383.

Ma, Z., Wei, Z., Zhang, X., 2013. Semi-automatic and

specification-compliant cost estimation for tendering

of building projects based on IFC data of design model.

Autom. Constr. 30, 126–135.

Nomitech, 2013. Nomitech Construction Oil & Gas BIM

Cost Estimating Software, Estimating Services | Home

(WWW Document). URL http://www.nomitech.eu/

cms/en/c/index.html (accessed 11.4.13).

Royal Institution of Chartered Surveyors, 2011. RICS New

Rules of M EASUREMENT Bill of Quantities for

Works Procurement.

Seethamraju, R., Marjanovic, O., 2009. Role of process

knowledge in business process improvement

methodology: a case study. Bus. Process Manag. J. 15,

920–936.

Senaratne, S., Sabesan, S., 2010. Managing knowledge as

quantity surveyors: An exploratory case study in Sri

Lanka. Built-Environment Sri Lanka 8, 41–47.

Shen, Z., Issa, R., 2010. Quantitative evaluation of the

BIM-assisted construction detailed cost estimates. Pap.

Constr. Manag.

Skitmore, M., Marston, V.K., 1999. Cost Modelling.

E&FN Spon., London.

Skitmore, M., Patchell, B., 1990. Developments in

contract price forecasting and bidding techniques.

Quant. Surv. Tech. New … 75–120.

Staub, F.S., Fischer, M., Kunz, J., Ishii, K., Paulson, B.,

2003. A feature ontology to support construction cost

estimating. Artif. Intell. Eng. Des. Anal. Manuf. 17,

133–154.

Staub, F. S., Nepal, M. P., 2007. Reasoning about

component similarity in building product models from

the construction perspective. Autom. Constr. 17, 11–

21.

Tan, F., Makwasha, T., 2010. “ Best practice ” cost

estimation in land transport infrastructure projects 1–

15.

Tanyer, A. M., Aouad, G., 2005. Moving beyond the

fourth dimension with an IFC-based single project

database. Autom. Constr. 14, 15–32.

Wermelinger, M., Bejan, A., 1993. Conceptual Structures

for Modeling in CIM.

Xu, S., Liu, K., Tang, L. C. M., 2013. Cost Estimation in

Building Information Model. In: International

Conference on Construction and Real Estate

Management (ICCREM 2013).

Xu, S., Tang, L.C.M., 2011. BIM Environment : Quantity

Surveyor ’ s Information Lifecycle. In: The Innovation

and the Built Environment Academy.

ICEIS2014-16thInternationalConferenceonEnterpriseInformationSystems

168