Performance Indicators and their Relationship with Organizational

Strategy

A Study in Brazilian Companies

Rosimeire Pimentel Gonzaga

1

, Antonio Thadeu Mattos da Luz

2

, Flávia de Araújo e Silva

3

and Marcos Paulo Valadares de Oliveira

4

1

Departamento de Ciências Contábies da Universidade Federal de Minas Gerais (UFMG), Belo Horizonte, MG, Brazil

2

Fundação Instituto Capixaba de Pesquisa em Contabilidade, Economia e Finanças – (FUCAPE), Vitória, ES, Brazil

3

Universidade Federal de Minas Gerais (UFMG), Belo Horizonte, MG, Brazil

4

Departamento de Administração, Universidade Federal do Espírito Santo, Campus Goiabeiras, Vitória, ES, Brazil

Keywords: Institutional Mission, Performance Indicators, Objectives, Goals, Organizational Strategies, Business

Process Management.

Abstract: The institutional mission declared by an organization can be taken as baseline for management as well as a

mechanism for communicating its objectives and organizational strategies. In a complementary fashion,

performance indicators support the evaluation of the processes aimed to execute companies specific

strategies. Thus, the present study sought, through an empirical quantitative approach, test the hypothesis of

the performance indicators used by a company is associated with the content of the mission it declares. A

sample of 85 Brazilian companies listed in BM&FBovespa’s IbrX Index was used. Data has been extracted

from the mandatory reference reports issued annually by companies and from its institutional sites. For

examination of the data, the technique of content analysis was used in order to identify the characteristics

present in the missions reported by the companies studied. Further, the logistic regression was used to test

the association between the variables studied. In the context analyzed, no evidence of association between

the characteristics of the missions reported by the companies and the performance indicators used by them

was observed in the results. The results found contradict, in part, the logic and theory of organizations

management control, especially regarding the congruence amongst the objectives that must be pursued,

including the alignment of what an organization declared as being relevant in its mission with the indicators

it uses to evaluate its performance. Finally, Business Process Management (BPM) is discussed as a

fundamental support for the definition of performance indicators in order to guarantee the alignment to the

organization’s strategic objectives.

1 INTRODUCTION

A common goal, integrating all involved parties, is a

fundamental attribute of a system. From that

perspective, a company's mission can be seen as an

effort to formalize one or more goals that will drive

the organization towards the achievement of

established strategies. A company’s mission

apparently is of significant importance in the

organizational context, and should be able to guide

the definition of strategies and goals to be pursued,

reflecting the management’s philosophy (Rafaeli et

al., 2007).

Performance indicators are pointed out in the

literature as tools used by organizations to achieve

their goals and implement their strategy, in addition

to their mission statement (Anthony and

Govindarajan, 2008).

The unceasing pursue of their strategic objectives

led companies to pay more attention to the

improvement of their business processes. Key

business processes should be frequently monitored

and, if necessary, remodeled (Jeston and Nelis,

2008). Business Process Management, a concept

defined by the Object Management Group as a set of

techniques for continuous and iterative improvement

of an organization’s business processes, has come

into widespread use (OMG, 2010). The use of

process management can help organizations define

performance indicators more finely tuned to their

559

Pimentel Gonzaga R., Mattos da Luz A., de Araújo e Silva F. and Valadares de Oliveira M. (2013).

Performance Indicators and their Relationship with Organizational Strategy - A Study in Brazilian Companies .

In Proceedings of the International Conference on Knowledge Discovery and Information Retrieval and the International Conference on Knowledge

Management and Information Sharing, pages 559-566

DOI: 10.5220/0004655305590566

Copyright

c

SCITEPRESS

strategy, providing an accurate measurement of what

is sought after as a company’s mission.

Given that the stated mission and performance

evaluation indicators used by organizations have

complementary purposes, this paper aims to

determine whether there is an association between

the institutional mission declared by the companies

sampled for the study and their performance

indicators. The question that arises from the above

is: is there an association between the stated mission

of the company and its performance indicators?

We thus seek, in the present paper, to empirically

test the following hypothesis:

H

0

: the performance indicators used by a

company is associated with the content of the

mission it declares.

Given the multidimensional aspect,

contemporarily bestowed upon organizational

performance and hence its evaluation, the present

study contributes to research on management control

by exploring whether the sampled organizations

have become alert to a fundamental requirement in

the management control process: the essential need

for goals, in order to develop any kind of control

(Otley and Berry, 1980).

It is important that performance indicators are

periodically reviewed and adapted to a company’s

systems and actual needs. Thus, after the analysis on

the association between indicators and institutional

mission, we examine how Business Process

Management (BPM) can help define performance

indicators that are directly linked to the

organization’s strategic objectives.

This paper is comprised of five sections, the first

being this introduction. Section 2 presents the

theoretical framework of the study and a literature

review on institutional mission, performance

indicators and business process management.

Section 3 presents the methodological procedures

used in the research. Section 4 presents and

discusses the main results. Finally, in section 5 are

exposed final remarks and suggestions for future

research.

2 THEORETICAL FRAMEWORK

2.1 Institutional Mission

The management of organizations is driven by their

main objective, which is in turn intimately

connected with the organization’s established

mission. Business strategies are related to the

interaction between the company and the elements

comprising their internal and external environments,

and mutate given the need to adapt the dynamics of

their activities and skills (Machado, 2005); (Porter,

2002); (Sette, 1998). The institutional mission can

be defined as a company’s central goal, the reason

behind its existence, used as guidance to goals and

strategies that express its work philosophy (Rafaeli

et al., 2007). Ackoff (1986) argues, accordingly, that

missions reported by companies must contain

measurable objectives that can differentiate a

company from others toiling in the market, inform

about its aspirations and inspire those directly or

indirectly involved with it.

To David and David (2003), nine characteristics

can be considered as key elements, and should be

pondered upon, during the establishment of missions

by companies. Some of them are: identification of

target customers; identification of the core business;

geographic specification of the market; commitment

to survival, growth and profitability; Importance of

employees; Identification of the company’s desired

public image, etc. Mullane (2002) stated that

mission or any other declarations are irrelevant if

used solely as billboards to be displayed in a

company’s. Thus, a company's mission can be used

to disclose its objectives and strategies, allowing,

through the commitment of all actors involved, that

specific goals are achieved and the desired

organizational performance is reached (Rafaeli et al.,

2007). In recent times, the mission statement has

been widely used by companies as a support to

management issues (Analoui and Karami, 2002),

thus suggesting that an association exists between

the presence of features related to an organization’s

stated mission and the performance indicators it

uses.

2.2 Performance Indicators

For Rafaeli and Müller (2007), from the moment in

which the goals and mission of a company are set

and strategies are being implemented, it is necessary

to check whether the company is following the

planned path towards mission accomplishment,

therefore requiring that a system capable of

performing such control is functioning. Performance

evaluation systems complementarily assist in

strategy implementation, also enabling the

monitoring of results (Anthony and Govindarajan,

2008).

Performance indicators seek to reflect the

philosophy and culture of organizations, while

evaluating the achievement of established strategies.

Performance indicators, to be effective, should

KDIR2013-InternationalConferenceonKnowledgeDiscoveryandInformationRetrieval

560

reflect the variations in competitiveness (Tatikonda

and Tatikonda, 1998). In this context, performance

indicators are defined from established strategies

and exert the function of performance evaluation.

Their main objective is offering subsidies to make

managers decisions converge with established goals

and strategies (Aguiar et al., 2012).

An extensive set of performance indicators may

turn out to be necessary in developing the process of

performance evaluation. The nature of such

indicators can be financial and non-financial,

strategic and operational, accounting and non-

accounting, among others (Frezatti et al., 2009);

(Kaplan and Norton, 2000).

According to Fitzgerald (2007), performance

indicators, as part of the performance appraisal

system, start from an organization’s goals and

strategies and comprise several other elements, such

as: aspects of performance that should be monitored,

considering financial and non-financial dimensions;

aspects related to goals to be achieved, considering

characteristics like degree of difficulty and

participation of everyone involved.

Globerson (1985) analyzed the relationship

between strategies and performance indicators,

emphasizing that the latter should be inferred from

the strategies and objectives of companies, and

should also possess the ability to provide feedback,

be objectively, concisely and clearly defined, and

provide clear and specific goals as well.

2.3 Business Process Management

Business Process Management (BPM) is a

methodology designed for managing an

organization’s key business processes,

contemplating the modeling of processes in order to

make them more efficient (Santos et al., 2012). The

purpose of using BPM is to obtain improvements in

corporate performance (Harmon, 2005). BPM has

come into widespread use lately, proving to be much

more than a technological tool (Jeston and Nelis,

2008).

In the present research, process is defined as a set

of activities or behaviors performed by individuals

or by machinery with the intention of achieving a

particular goal. The core activities of the BPM cycle

contemplate continuous process improvement

through planning, analysis, design, modeling,

implementation, monitoring and control (ABPMP,

2009).

The modeling of business processes also allows

for: a) commonality of understanding on how work

should be done, enabling integration, analysis and

improvements in information flow; b) explicit

knowledge of processes, thereby preserving an

organization’s know-how; c) analysis of the

organization and performance indicators, and d)

simulations to support an organization’s decision

making and management (Vernadat, 1996).

A number of critical factors merit consideration

in implementing business processes management.

The handling of proposed changes, where possible

resistance should be properly addressed, is one of

them (Jeston and Nelis, 2008). Strategic alignment,

measurement and monitoring of the remodeled

process and process automation can also be cited,

among others (SANTOS et al., 2012). BPM can also

be used to alter performance indicators in view of

the need to redefine the indicators for each process

(Sipioni, 2009). A major difficulty involved in the

strategic management process is the choice of

indicators that best reflect organizational

performance.

BPM enables an organization to change

processes by altering only graphical models,

providing greater flexibility when compared to

conventional information systems (Sipioni, 2009).

3 METHODOLOGY

In this section we describe the methodological

procedures employed in this research. This is an

empirical study, with a quantitative approach for

treatment and analysis of collected data.

With regard to the universe studied, we sought to

investigate whether there is association between the

mission and performance indicators of 85 Brazilian

companies traded and listed, in August 2011, on the

São Paulo Stock Exchange, Commodities and

Futures Exchange (BM&FBovespa). These

companies are present in the makeup of the IbrX

index, which measures the return on a theoretical

100 stocks portfolio selected among the most

actively traded stocks, based on the number of trades

and financial value (BM&FBOVESPA, 2011). The

companies that make up the IbrX index annually

publish, in compliance with requirements of the

BM&FBovespa, a report called Reference Report, or

Referral Form, containing information ranging from

financial issues to human resources and control.

To carry out this research, part of the data

(performance indicators) was extracted from the

reference report issued annually by the companies,

as required by BM&FBovespa, and another part

(institutional mission) was collected from the

websites of the sampled companies.

PerformanceIndicatorsandtheirRelationshipwithOrganizationalStrategy-AStudyinBrazilianCompanies

561

The investigation followed an empirical-

quantitative approach, where we sought to determine

the association between variables. Thus, in this

particular case, the independent variables were the

performance indicators used by companies and

obtained from their reference reports. The stated

mission of the company was the addressed

dependent variable, and was extracted from the

websites of companies. In order to test the possible

association, missions collected in the websites were

categorized according to the characteristics present

in their statement.

For the outlining of features present in the stated

mission declared by Brazilian companies listed in

IBrX, content analysis technique was used (Bardin,

1977). Initially, based on the literature review, some

categories were pre-defined as guidance for the

content analysis. Thus, oriented by the work of

David and David (2003), and following also the

Rafaeli, Campagnolo and Müller (2007) reasoning,

we performed a content analysis of the missions

collected from the websites of the companies

studied, focusing in the categories set forth in Figure

1:

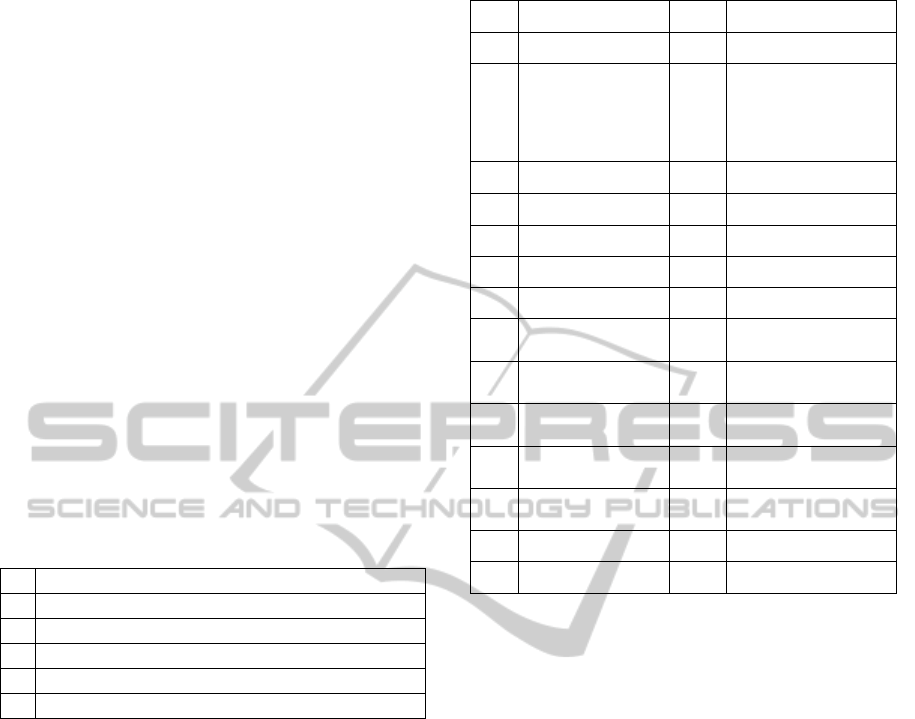

M1 Identification of target customers

M2 Identification of the core business

M3 Geographic specification of the market

M4 Commitment to survival, growth and profitability

M5 Importance of employees

M6 Identification of the company’s desired public image

Source: Adapted from David and David (2003) and Rafaeli et al.

(2007).

Figure 1: Pre-defined categories for content analysis.

We considered as a company’s declared mission

statement the one published in its official website.

At first, companies that published the mission in

their respective institutional websites were sorted

from those that did not. Subsequently, we analyzed

the content of the declared missions, determining

which of the pre-defined categories features

highlighted by David and David (2003) and Rafaeli,

Campagnolo and Müller (2007) were present in

them. In a second stage, data was collected

regarding performance indicators used by

companies, as disclosed in item three of their

respective public reference report. As shown in

Figure 2, we found evidences pointing to the use of

30 different indicators by companies in the sample.

I01 Net Equity I16 EBITDA

I02 Total Assets I17 Service Indicators

I03

Net Income /

Financial

Intermediation

Income / Gains with

Insurance Premiums

I18 Adjusted Net Income

I04 Net Income I19 Accounts Receivable

I05 Book Value I20 Number of Branches

I06 Gross Earnings I21 Basel Index

I07 Number of Shares I22 Market Indicators

I08 Net Earnings I23 Adjusted Net Earnings

I09

Book Value per

thousand shares

I24 Inventories

I10

Number of Paid-in

Shares

I25 Number of Employees

I11

Net Earnings per

thousand shares

I26 Domestic Suppliers

I12

Net Earnings per

Share

I27 Foreign Suppliers

I13

Net Earnings per

common share

I28

Investment Funds under

management

I14 Current Assets I29 Loans (short term)

I15 Current Liabilities I30 Loans (long term)

Figure 2: Indicators used by companies.

To verify the association between the mentioned

variables, we used the statistical technique of

logistic regression, according to the following

model:

MISSION

n

= β

0

+ β

01

.INDICATOR

01

+...+

β

k

.INDICATOR

k

+ ε

(1)

Where:

MISSION

n

- Features of missions reported by the

companies, ranging from feature 1 to feature 6, as

previously described, ascribed a value of 1 for

companies presenting that particular feature in their

missions and a value of 0 for those not presenting;

INDICATORS

k

- Performance indicators used by the

sampled companies, ranging from Indicator01 to

Indicator30, as described in Figure 2, ascribed a

value of 1 when a particular performance indicator is

used by the company and a value of 0 when not

used.

Given the findings reported in the reviewed

literature on the studied subject, it is expected to find

associations between the variables, thus presenting

evidences that companies use certain performance

indicators to assess the achievement of their mission,

i.e., the achievement of established objectives and

KDIR2013-InternationalConferenceonKnowledgeDiscoveryandInformationRetrieval

562

organizational strategies. After analysis of the results

found, as a way to contribute to the management of

corporate indicators, a suggestion will be offered for

the application of the performance indicators

revision/definition process.

4 DISCUSSION OF RESULTS

4.1 Association between the Stated

Mission and their Respective

Performance Evaluation Indicators

In this section we present the analysis and discussion

of the results of the present research, which was

developed with the purpose of ascertaining whether

there is an association between the institutional

mission declared by the Brazilian companies listed

in BM&FBovespa’s IbrX index and their

performance indicators.

The descriptive statistics of the sample data is

presented based on the count of companies where

certain mission characteristics or particular

performance indicator were present or not.

Initially, descriptive statistics for the analyzed

sample, regarding the dependent variables, are

shown in Table 1:

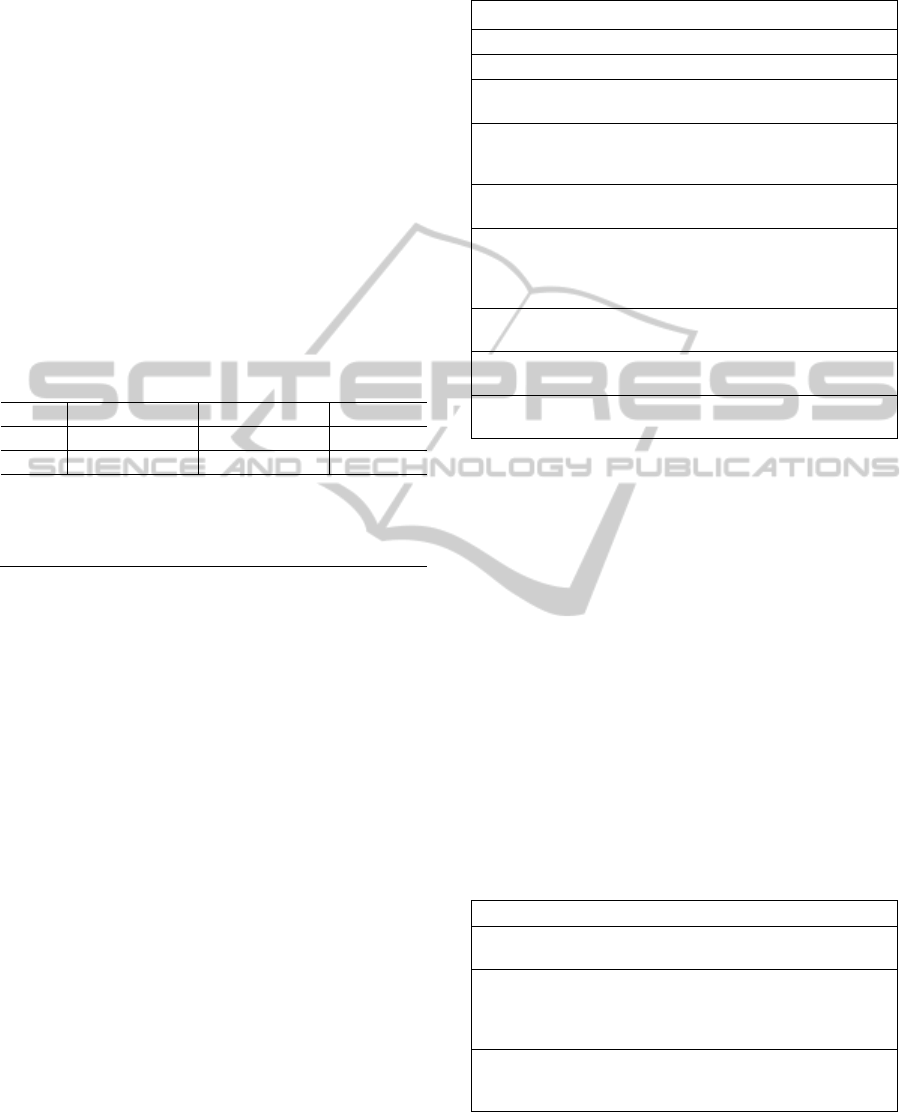

Table 1: Descriptive statistics: dependent variables.

Variable

Present Not Present Total

Count % Count % Count %

M1 09 11 76 89 85 100

M2 51 60 34 40 85 100

M3 14 16 71 84 85 100

M4 30 35 55 65 85 100

M5 11 13 74 87 85 100

M6 36 42 49 58 85 100

As characteristics of the mission, variables M2

(identification of the core business), M4

(commitment to survival, growth and profitability)

and M6 (Identification of the company’s desired

public image) stand out as the most frequent mission

features, all being present in more than 30% of the

missions stated by companies in the sample, as

shown in Table 1. Characteristics represented by

variables M1 (identification of target customers),

M3 (geographic specification of the market) and M5

(importance of employees) are less frequent, being

all present in less than 20% of the sampled missions.

Regarding the performance indicators used by

companies, I01 (Equity), I02 (Total Assets), I05

(Book Value), I06 (Gross Earnings), I07 (Number of

Shares) and I08 (Net Earnings) stand out as the most

frequent, all of these indicators being used by more

than 80% of the sampled companies.

When logistic regressions were run for each

mission characteristic, most models turned out as

non-convergent, making standard errors impossible

to calculate, and with most of the independent

variables discarded due to collinearity.

Thus, nothing can be said about the associations

between the mission characteristics and performance

indicators used by the sampled companies.

However, for mission characteristics M4, M5 and

M6 and performance indicators I03 and I04, the

results showed some variability, as presented in the

descriptive statistics above, allowing evaluation of

models involving such variables.

Results for the logistic regression using the

model depicted in equation 1 and the characteristic

M4 (commitment to survival, growth and

profitability) as dependent variable, are shown in

Table 3:

Table 3: Logistic regression statistics: Equation 1.

M4 = β

0

+ β

3

I03 + β

4

I04 + ε

M4 Odds Ratio Z-Statistic P-value

I03 0.000005 -0.47 0.638

I04 0.555555 -0.41 0.683

Number of obs = 85

LR chi2 = 0.23

Prob > chi2 = 0.8909

PseudoR2 = 0.0021

No evidences can be found of association

between mission features identified as commitment

to survival, growth and profitability and the

performance indicators Net Income / Financial

Intermediation Income / Gains with Insurance

Premiums or Net Income, as well as there is no

evidence that they do not occur randomly (Prob >

chi2 = 0.8909). Table 4 presents the results using

characteristic M5 (importance of employees) as

dependent variable:

Table 4: Logistic regression statistics: Equation 1.

M5 = β

0

+ β

3

I03 + β

4

I04 + ε

M5 Odds Ratio Z-Statistic P-value

I03 0.0384615 -1.87 0.062*

I04 0.1914894 -1.13 0.258*

Number of obs = 85

LR chi2 = 4.79

Prob > chi2 = 0.0910*

PseudoR2 = 0.0732

Where *, **, ***: statistically significant at 10%, 5% and 1% levels

respectively.

PerformanceIndicatorsandtheirRelationshipwithOrganizationalStrategy-AStudyinBrazilianCompanies

563

The results show that there is evidence of

association between the dependent variable and

indicator I03 (Net Income / Financial Intermediation

Income / Gains with Insurance Premiums) and that it

does not occur at random, though the association is

weak (Prob > chi2 = 0.0910). Interpreting the results

in light of the odds ratios, one can observe that the

chance of finding a company that uses indicator I03

and declares the importance of employees as

characteristic of its mission, is about 0.03 times

higher than that for companies where both are not

present, but the evidence is still weak to allow any

conclusion.

Results using the characteristic M6

(identification of the company’s desired public

image) as dependent variable, are shown in Table 5:

Table 5: Logistic regression statistics: Equation 1.

M6 = β

0

+ β

3

I03 + β

4

I04 + ε

M6 Odds Ratio Z-Statistic P-value

I03 0.000008 -0.15 0.879

I04 0.696969 -0.25 0.802

Number of obs = 85

LR chi2 = 0.13

Prob > chi2 = 0.9355

PseudoR2 = 0.0012

Again, there is no observable evidence as to the

existence of association between the dependent

variable M6 (identification of the company’s desired

public image) and independent variables I03 and

I04. It is therefore impossible to establish an

association between the facts that companies

evidencing through its missions to be concerned

with identifying their desired public image use the

indicators Net Income / Financial Intermediation

Income / Gains with Insurance Premiums or Net

Income.

4.2 Revision of Performance Indicators

through BPM

Given the results in Section 4.1, it is apparently

necessary to review performance indicators currently

used by companies in order to align them with the

organizational mission.To this end, we suggest using

the model of performance indicators revision

process, developed by Sipioni (2009), which is

supported by Business Process Modeling Notation

(BPMN). It is a process founded on the BSC system

principles, capable of sustaining all the

organization's strategy. The model was developed

with the BSC vision and BPM’s methodology and

integration. The model’s step by step flow is shown

in Figure 3 (Sipioni, 2009):

Step/ Description

Step 1 - Entry: corporate strategic objectives;

Step 2 - Deployment of strategic objectives to the business unit;

Step 3 - Unfolding of strategic objectives for each macro-

process of the organization;

Step 4 - Verification: the unfolding of the strategic objectives

for each macro-process is consistent with the strategic

objectives of the business unit?

Step 5 - Unfolding of the strategic objectives of each macro-

process for each sub-process;

Step 6 - Review of performance indicators: evaluation of

strategic objectives for the sub-process, which develops new

indicators in accordance with the strategic objectives of the

macro-process;

Step 7 - Comparison of the developed indicators with the

existing performance indicators for each sub-process;

Step 8 - Check: the new performance indicators are in line with

the strategic objectives?

Step 9 - Output: new performance indicators defined in

accordance with the corporate strategy.

Source: adapted from Sipioni (2009).

Figure 3: Convergence of BSC and BPM systematics.

According to Sipioni (2009) the third stage in the

process is one of the most important, the critical

point of this phase being the verification of whether

managers actually understood the strategic

objectives of the business unit and whether those in

charge of each sub-process can turn these objectives

into indicators that do meet the needs of the business

unit. Macro-processes managers often design

indicators to meet their own goals and not those of

the business unit. Once the new indicators are

defined, Sipioni (2009) also proposes a process for

monitoring indicators, in order to ensure that all

indicators still in the process of definition, at all

stages, are in line with the organization’s strategic

objectives. This process consists of three steps, as

outlined in Figure 4:

Step/ Description

Step 1 - Monthly monitoring of each business unit

achievements;

Step 2 - Monitoring of strategic objectives for each macro-

process of the organization, with monthly meetings held to

evaluate the results and request enhancements or modifications

to the indicator;

Step 3 - Monitoring of strategic objectives for each sub-process,

with monthly meetings held to review results and request

improvements or modification of the indicator.

Source: adapted from Sipioni (2009).

Figure 4: Monitoring process of performance indicators.

Sipioni (2009) points out that the proposed

KDIR2013-InternationalConferenceonKnowledgeDiscoveryandInformationRetrieval

564

process for revision of indicators is relatively simple

and can be performed by any area of an

organization. It is an easily operationalized process,

as already tested by the author during a case study

conducted in a Brazilian manufacturing firm.

5 CONCLUSIONS

This study aimed to check whether there is an

association between missions reported by

companies, and the indicators that such companies

use to assess their performance.

The results, after applying logistic regressions to

treat the data obtained, indicate that there is no

association between the characteristics of missions

declared by the sampled companies and the

performance indicators they use, considering those

evidenced in their reference reports. These results

suggest that firms in the sample appear not to use the

indicators stated in their reference reports as

instruments to measure the achievement of certain

goals or declared strategies. Thus, some implications

can derive from the evidences found. Companies

missions designed solely for purposes of public

disclosure may turn out as not convergent with the

indicators used to guide the achievement of desired

goals, rebutting the idea that the establishment of

missions can bring about real benefits for

organizations (Piercy and Morgan, 1994).

After analyzing the results, the use of a model

proposed by Sipioni (2009) was suggested. The

model advocates a process designed to review

performance indicators, integrating the BSC and

BPM methodologies. According to the author, the

two methods complement one another: BSC directed

to the development of strategic management and

BPM to model processes.

Even though the results in the present study

contradict the logic underlying the management

control of organizations, particularly in respect to

the congruence of objectives that should be pursued,

including ties between what an organization declares

as relevant in its mission and indicators it uses to

evaluate performance, it should be noted that this

study has some limitations that cannot be neglected,

which suggests that its results cannot be generalized.

As a first point, in methodologies involving content

analysis results could be biased by the analyst’s

assessment. Secondly, companies may use other

specific performance indicators for internal

purposes, which are not disclosed publicly,

preventing access to all performance indicators used

by companies. Moreover, results may have been

influenced by sample size and low variability,

precluding extrapolation.

It is suggested that future studies consider the

possible use of other performance indicators, in

addition to those disclosed by mandatory reports.

We also suggest the expansion of pre-defined

categories for content analysis of companies’ stated

missions, as well as the expansion of the sample.

It is also suggested that the business process

model, presented here as tool to be used in the

definition of performance indicators, can be applied

in various organizations in order to assess its real

contribution to the alignment of indicators with the

strategic objectives defined by an organization.

REFERENCES

ABPMP. BPM CBOK - Guide to the business process

management common body of knowledge. Versão 2.

2009.

Ackoff, R. L. Management in small doses. Nova Iorque:

John Wiley & Sons, 1986.

Aguiar, Andson Braga de; Teixeira, Aridelmo J. C.;

Nossa, Valcemiro; Gonzaga, Rosimeire Pimentel.

Associação entre sistemas de incentivos gerenciais e

práticas de contabilidade gerencial. Revista de

Administração de Empresas – RAE. São Paulo. v. 52,

n. 1, jan./fev. 2012.

Analoui, F.; Karami, A. CEO’s and development of the

meaningful mission statement. Corporate

Governance. Bradford, v. 2, n. 3, p. 13-20, 2002.

Anthony, Robert N.; Govindarajan, Vijay. Sistemas de

controle gerencial. 12.ed. São Paulo: McGraw-Hill,

2008.

Bardin, Laurence. Análise de Conteúdo. Lisboa: Edições

70, 1977.

Bolsa De Valores, Mercadorias E Futuros De São Paulo.

Disponível em http://www.bmfbovespa.com.br/home.

aspx?idioma=pt-br. Acess in 5th November 2011.

David, Forest R.; David, Fred R. It’s time to redraft your

mission statement. The Journal of Business Strategy.

Boston, v. 24, n. 1, p. 11-4, jan.-feb, 2003.

Fitzgerald, L. Performance measurement. In: HOPPER,

Trevor et al. Issues in Management Accounting. 3 ed.

Pearson Education Ltd., 2007. pp. 223-241.

Frezatti, F.; Rocha, Welington; Nascimento, A. R.;

Junqueira, E. R. . Controle Gerencial: uma abordagem

da contabilidade gerencial no contexto econômico,

comportamental e sociológico. 1. ed. São Paulo:

Editora Atlas, 2009.

Globerson, S. Issues in developing a performance criteria

system for an organisation. International Journal of

Production Research. Loughborough, v. 23, n. 4, p.

639-646, 1985.

Harmon, P. Service orientated architectures and BPM.

Business Process Trends, 22 Feb. 2005.

Hirota, Shinichi; Kubo, Katsuyuki; Miyajima, Hideaki;

PerformanceIndicatorsandtheirRelationshipwithOrganizationalStrategy-AStudyinBrazilianCompanies

565

Hong, Paul; Park, Young Won. Corporate mission,

corporate policies and business outcomes: evidence

from Japan. Management Decision. v. 48, n. 7, p.

1134-1153, 2010.

Kaplan, R. S., Norton, D. P. Organização orientada para a

estratégia: como as empresas que adotam o Balanced

Scorecard prosperam no novo ambiente de negócios.

Rio de Janeiro. Elsevier: 2000.

Jeston, J.; Nelis, J. Business process management,

practical guidelines to successful implementations. 2.

ed. Oxford: Elsevier, 2008.

Machado, Rosa Tereza Moreira. Estratégia e

competitividade em organizações agroindustriais.

Lavras: UFLA/FAEPE, 2005.

Matejka, K., Kurke, L. B., Gregory, B. Mission

Impossible? Designing a great mission statement to

ignite your plans. Management Decision. Londres, v.

31, n. 4, p. 34-7, 1993.

Mullane, John V. The mission statement is a strategic tool:

when used properly. Management Decision. Londres,

v. 40, n. 5-6, p. 448-55, 2002.

Müller, Cláudio José. Modelo de gestão integrando

planejamento estratégico, sistemas de avaliação de

desempenho e gerenciamento de processos (MEIO –

Modelo de Estratégia, Indicadores e Operações).

2003. 292f.. Tese (Doutorado em Engenharia) –

Escola de Engenharia, Universidade Federal do Rio

Grande do Sul, Porto Alegre, 2003.

OMG. Business process management with OMG

specifications. Object Management Group. Disponivel

em: http://www.bpm-consortium.org/literature.htm.

Acesso em: 05 Junho 2010.

Otley, David T. Did Kaplan and Johnson get it right?

Accounting, Auditing & Accountability Journal. v. 21,

n. 2, p. 229-239. 2008.

Otley, David T.; Berry, A. J. Control, Organisation and

accounting. Accounting, Organizations and Society. v.

5, n. 2, p. 231-244, 1980.

Piercy, J.; Morgan, N. Mission analysis: an operational

approach. Journal of General Management. Henleyon-

Thames, v. 19, n. 3, p. 01-19, 1994.

Porter, M. E. A nova estratégia. In: JÚLIO, C. A.; SALIBI

NETO, J. (Orgs.). Estratégia e Planejamento. São

Paulo: Publifolha, 2002.

Rafaeli, Leonardo; Campagnolo, Rodrigo Rech; Müller,

Cláudio José. Missão declarada e missão desdobrada:

uma abordagem para o planejamento estratégico. In:

Simpósio de Engenharia de Produção, 14., 2007, São

Paulo. Anais ... Bauru, 2007.

Rafaeli, Leonardo; Müller, Cláudio José. Estruturação de

um índice consolidado de desempenho utilizando o

AHP. Gest. Prod., São Carlos, v. 14, n. 2, p. 363-377,

mai-ago. 2007.

Santos, H. M.; Santana, A. F.; Alves, C. F. Análise dos

fatores críticos de sucesso da gestão de processos de

negócios em organizações públicas. Revista Eletrônica

de Sistemas de Informação, v. 11, n. 1, jan.-jun., 2012

Sette, R. S. Estratégia empresarial. Lavras:

UFLA/FAEPE, 1998.

Sipioni, Fabio. Modelo para revisão de Indicadores de

Desempenho aplicado a Processos de Manufatura

utilizando a Integração do Balanced Scorecard e

Business Process Management. Dissertação (Mestrado

em Engenharia de Produção e Sistemas) – Pontifícia

Universidade Católica do Paraná, Curitiba, 2009.

Tatikonda, L. V. & Tatikonda, R. J. (1998) - We need

dynamic performance measures. Journal of

Management Accounting, Pittsburgh, Vol. 80, n.3,

p.49-51.

Zairi, Mohamed; Letza, Steve. Corporate Reporting.

Management Decision. v. 32, n. 2, p. 30-40, 1994.

KDIR2013-InternationalConferenceonKnowledgeDiscoveryandInformationRetrieval

566