Data Mining Tool for Decision Support in Stock Market

Sung-Dong Kim

Dept. of Computer Engineering, Hansung University, 389 Samseon-dong, Seongbuk-gu, Seoul, Republic of Korea

Keywords: Data Mining, Decision Support System, Stock Price Prediction, Neural Networks, Decision Trees.

Abstract: Stock investors want to make continuous profits in stock market. They have to choose profitable stocks and

to follow the appropriate trading policy to achieve their goal. It is difficult for individual investors to

determine what to buy and when to buy and sell. This paper proposes a data mining tool for stock investors’

decision support by recommending profitable stocks and proposing the trading policy. The proposed tool

provides three functions: stock data management, stock price prediction model generation by applying the

machine learning algorithms and the investment simulation for seeking the profitable trading policy. Users

can generate and test the stock price prediction model by selecting their own technical indicators, simulate

the trading and select the best trading policy through the evaluation of the trading results.

1 INTRODUCTION

Stock investors have a common goal of continuously

making high profits. There are many stocks in the

market and lots of information is flowing. In this

situation, investors seek the profitable stocks by

referring to the analysis results of such information.

Because they usually determine subjectively, it is

difficult for them to make profits. TradeStation is the

software which performs the technical analysis

(www.tradestation.com). The system is used in

many securities companies and includes the trading

(buying/selling) functions. This system is expensive

for individual users and the usage is difficult for

them.

This paper proposes the data mining tool for the

individual short-term investors’ decision support.

They select the stocks through analysing the

technical indicators by viewing the candle charts.

Though the prices of the selected stocks may

increase, they must determine the selling prices and

the selling time in order to achieve their goal. That is,

the investors must determine the buying stocks, the

buying price, the selling price and the selling time.

Data mining techniques are adaptible for

recommending profitable stocks from the large stock

data (Kannan, Sekar, Sathik and Arumugam, 2010).

The proposed data mining tool provides the

following functions. First, the stock data is managed

to calculate various technical indicators. Second, it

provides the technical indicator selection function by

which the users can select their own technical

indicators in building the stock price prediction

models. Third, machine learning techniques, artifical

neural networks and decision trees widely used in

financial prediction problems (Tsai and Wang, 2009),

can be applied to generate stock price prediction

models. Data generation for the machine learning is

also possible. Fourth, the investment simulation

function validates the generated stock price

prediction model and induces the profitable trading

policy. With the help of the proposed tool, users can

build the prediction model which proposes the

profitable stocks. Also, they can trade based on the

trading policy which guides the buying price, the

selling price and the holding period.

This paper is orgarnized as follows. Section 2

explains the structure and the function of the

proposed data mining tool. In section 3, we describe

the process of the stock price prediction model

generation and the investment simulation. Also, the

results of the model generation and the simulation

are presented. Section 4 concludes the paper with

further works.

2 STRUCTURE AND FUNCTIONS

OF THE DATA MINING TOOL

The proposed data mining tool supports the

individual investors’ decision making by

recommending profitable stocks and helping

473

Kim S..

Data Mining Tool for Decision Support in Stock Market.

DOI: 10.5220/0004240804730477

In Proceedings of the 5th International Conference on Agents and Artificial Intelligence (ICAART-2013), pages 473-477

ISBN: 978-989-8565-39-6

Copyright

c

2013 SCITEPRESS (Science and Technology Publications, Lda.)

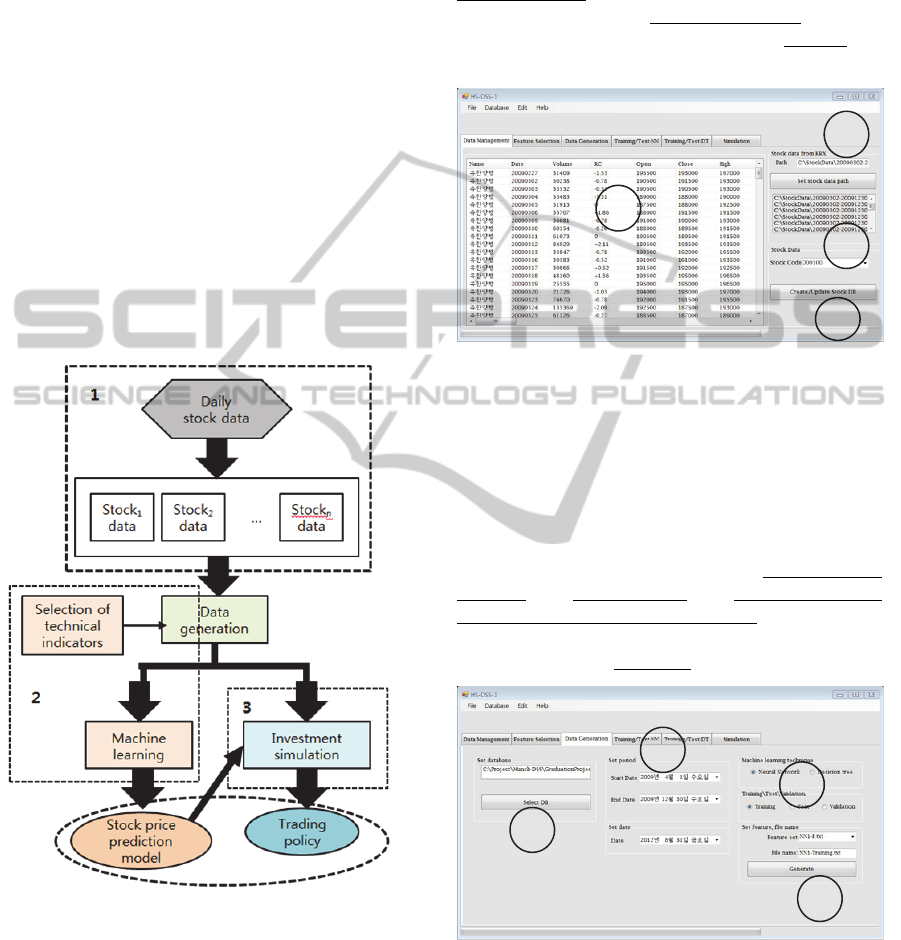

establish their own trading policy. Figure 1 shows

the logical structure of the proposed data mining tool

which consists of three modules. First is the stock

data management module (“1” in figure 1). This

module takes daily stock data from stock market and

generates data for each stock. The generated data

includes the technical indicators of each stock. The

stock database consists of such stock data. Second

module is for the stock price prediction model

generation (“2” in figure 1). In order to generate the

prediction model, users select the technical

indicators which, they think, may affect the future

price of the stocks. This module provides the

selection facility. Machine learning techniques can

be easily applied to generate the prediction model.

The investment simulation module (“3” in figure 1)

tries to back-test and presents the investment results

for various trading policies. The users analyse the

results and select one of the trading policies

satisfying their criteria.

Figure 1: The logical structure of the data mining tool.

2.1 Stock Data Management

2.1.1 Stock Database

In order to predict the future price of each stock, we

must manage the stock data individually. Korea

Exchange (KRX) provides the daily stock data

which contains data for all stocks in Korea stock

market. The data mining tool takes the daily stock

data, calculates technical indicators for each stock

and stores them in the file for each stock. Figure 2

shows the stock data management screen. After (1)

setting the path as the folder name which includes

daily stock data and (2) clicking the button, the stock

database is generated. Users can (3) confirm the

correct data generation.

Figure 2: Stock data management screen.

2.1.2 Stock Database Interface

In order to generate the stock price prediction model

by applying machine learning techniques, the

training/validation/test data is required. For an

investment simulation, test data is also required.

Figure 3 shows the stock database interface for

easily generating such data. After (1) selecting stock

database, (2) setting period, (3) selecting machine

learning algorithm and the usage of the to-be

generated data and setting the selected features, the

required data is (4) generated.

Figure 3: Stock database interface screen.

2.2 Stock Price Prediction Model

Generation

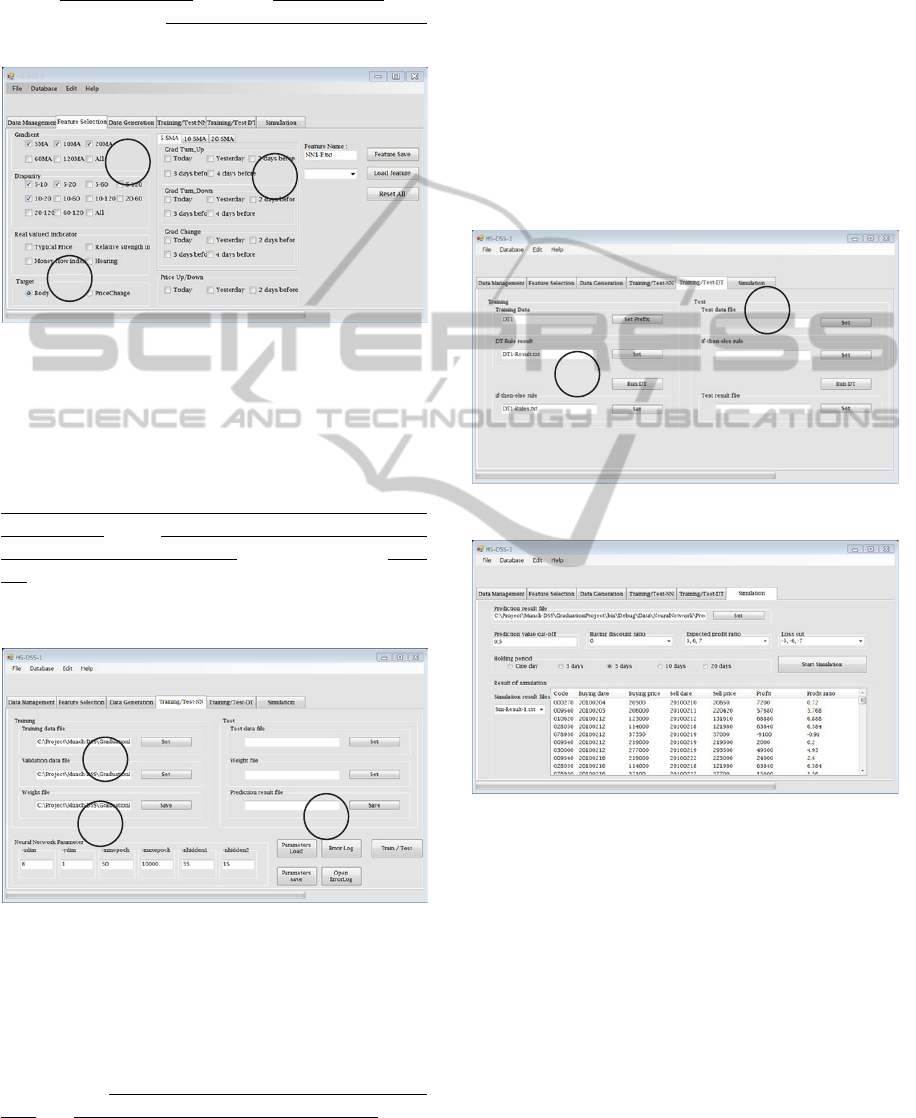

2.2.1 Selection of Technical Indicators

In building the models, the users must select

1

2

3

3

1

2

3

4

ICAART2013-InternationalConferenceonAgentsandArtificialIntelligence

474

technical indicators as the features. Figure 4 shows

the screen for the technical indicator selection. The

currently available technical indicators are classified

as (1) real-valued type and (2) binary-valued one.

We consider the (3) body size and the rate of change

as the target of the machine learning.

Figure 4: Screen for technical indicators selection.

2.2.2 Applying Machine Learning

Techniques

The result of the neural networks learning is the

weights of the neural networks. Using the tool, (1)

users can specify the training, validation, test and

weight files. (2) The parameters of the neural

network can be pre-set or set by users. The (3) error

log during the training can be shown to identify the

number of training epochs for the minimum error.

Figure 5 is the screen for the neural network learning.

Figure 5: Screen for neural networks training/test.

Decision tree algorithm is appropriate for binary-

valued input. The tool provides the application of the

C4.5 algorithm (Quinlan, 1993). Figure 6 is the

screen for decision tree learning. The decision tree

learning outputs if-then-else rules. The screen

provides (1) the selection facility for the necessary

files. (2) The users can test the generated rules.

2.3 Investment Simulation

In order to make profit, the investors have to follow

the appropriate trading policy. That is, they must

determine the buying/selling price and the holding

period. We define the trading policy which consists

of 4 elements: buying discount rate (BDR), expected

profit ratio (EPR), loss cut ratio (LCR), and holding

period (HP). Users can verify various trading

policies with changing four elements of the policy.

The user compares the results and selects the best

trading. Figure 7 shows the screen for the investment

simulation.

Figure 6: Screen for decision trees training/test.

Figure 7: Investment simulation screen.

3 EXPERIMENT

We describe the process of the stock price prediction

model generation and the investment simulation. We

collect stock data from 2008/1/2 to 2010/3/17. We

construct stock database consisting of 68 stocks in

KOSPI (Korea Composite Stock Price Index) on the

screen in figure 2. For the prediction model

generation, we select the technical indicators on the

screen in figure 4. Then, we generate the

training/validation/test data files on the screen in

figure 3. We run the neural network algorithm on the

1

2

3

1

2

3

1

2

DataMiningToolforDecisionSupportinStockMarket

475

screen in figure 5. As shown in figure 5, we use two-

layer networks with 35 and 15 nodes respectively.

And the network has 6 inputs and 1 output. Through

the multiple trials of training and test, we select one

of the models with the minimum error rate. We

perform the investment simulation with the selected

prediction model on the screen in figure 7.

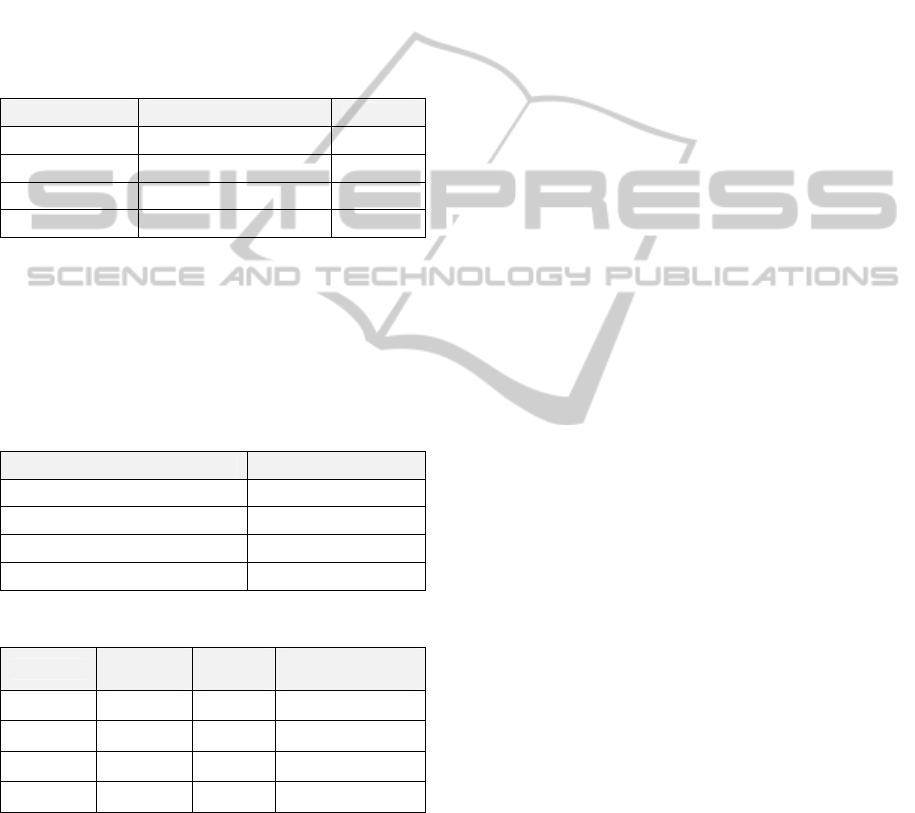

We generate the data as shown in table 1. The

price prediction model calculates the prediction

values for the stocks in the simulation data which are

the criteria for decision making of buying stocks.

Table 1: Data for model generation and investment

simulation.

Period # of data

Training data 2009.4.1 ~ 2009.12.30 24,548

Validation data 2008.4.1 ~ 2008.5.30 5,440

Test data 2008.6.2 ~ 2008.8.29 5,235

Simulation data 2010.2.1 ~ 2010.3.16 2,312

We perform the simulation with changing the

elements of the trading policy. Table 2 shows the

values of the elements of the trading policy used in

the simulation. We have 108 results from the

simulation and some of them are presented in table 4.

Table 2: The values of the trading policy elements for

simulation.

Elements Values

Holding period (days), H 1, 3, 5

Buying discount rate (%), B 0

Expected profit ratio (%), E 2, 3, 4, 5, 6, 7

Loss cut ratio (%), L -2, -3, -4, -5, -6, -7

Table 3: Some results of the investment simulation.

H, B, E, L

# of

profits

# of

loss

Total profit

(Won)

1, 0, 2, -2 94 66 485,080

3, 0, 2, -2 116 50 1,158,701

3, 0, 5, -5 122 40 2,257,588

5, 0, 5, -5 142 22 3,765,845

We use 0.5 as the cut-off value of the prediction

value. We have 169 transactions (one transaction

includes both buying and selling) and assume that

one million won is used to buy each recommended

stock. During the simulation period (2010/2/1 ~

2010~3/16), KOSPI rises about 2.6% from 1606.44

to 1648.01. The first line in table 4 means the

followings: the holding period is one day, the BDR,

EPR, LCR are 0%, 2%, -2% respectively. Among

169 transactions we make profits 94 times and have

loss 66 times. We got profits as 485,080 Korean

Won. Table 3 shows that the results can be

considerably different according to the different

trading policies. As a result, we can say that the user

select the trading policy outperforming the average

market profits through the investment simulation.

4 CONCLUSIONS

In this paper, we propose the data mining tool which

provides the three functions: stock data management,

the stock price prediction model generation using

machine learning techniques and the investment

simulation. The prediction model recommends the

stocks to buy and the investment simulation suggests

the trading policy. Thus, the proposed tool can

support the short-term investors’ decision-making.

Users have only to get daily stock data from

KRX and update the existing stock database. Once

the prediction model is built and the proper trading

policy is established, users can perform the objective

decision-making based on the data rather than the

emotional judgements. Users have only to get the

recommended stocks through the application of the

today’s data to the prediction model under the

established trading policy.

Other machine learning techniques, such as the

support vector machines (SVM) and the genetic

algorithms, have studied for the stock price

prediction. We will expand the data mining tool for

including such techniques. More technical indicators

are required for more sophisticated prediction

models. We will consider the asset allocation

problem in the investment simulation, which will

present more definite results and be more helpful.

ACKNOWLEDGEMENTS

This research was financially supported by Hansung

University.

REFERENCES

C. F. Tsai and S. P. Wang. 2009. Stock Price Forecasting

by Hybrid Machine Learning Techniques. Proceedings

of the International MultiConference of Engineers and

Computer Scientists. Vol. 1. 755-760.

J. R. Quinlan. 1993. C4.5: Programs for Machine Learning,

Morgan Kaufmann Publishers.

ICAART2013-InternationalConferenceonAgentsandArtificialIntelligence

476

K. S. Kannan, P. S. Sekar, M. M. Sathik, and P.

Arumugam. 2010. Financial Stock Market Forecast

using Data Mining Techniques. Proceedings of the

International MultiConference of Engineers and

Computer Scientists.

DataMiningToolforDecisionSupportinStockMarket

477